Sample Category Title

Swiss Franc Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.17% against the CHF and closed at 0.9928 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9920, with the USD trading 0.08% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9898, and a fall through could take it to the next support level of 0.9876. The pair is expected to find its first resistance at 0.9960, and a rise through could take it to the next resistance level of 1.0000.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada Housing Starts Unexpectedly Surged In November

For the 24 hours to 23:00 GMT, the USD rose 0.09% against the CAD and closed at 1.2865 on Friday.

Macroeconomic data revealed that Canada’s seasonally adjusted housing starts unexpectedly advanced to a level of 252.2K in November, compared to a revised reading of 222.7K in the prior month and defying market anticipations for a fall to a level of 213.0K.

In the Asian session, at GMT0400, the pair is trading at 1.2846, with the USD trading 0.15% lower against the CAD from Friday’s close.

The pair is expected to find support at 1.2808, and a fall through could take it to the next support level of 1.277. The pair is expected to find its first resistance at 1.2882, and a rise through could take it to the next resistance level of 1.2918.

With no macroeconomic releases in Canada today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

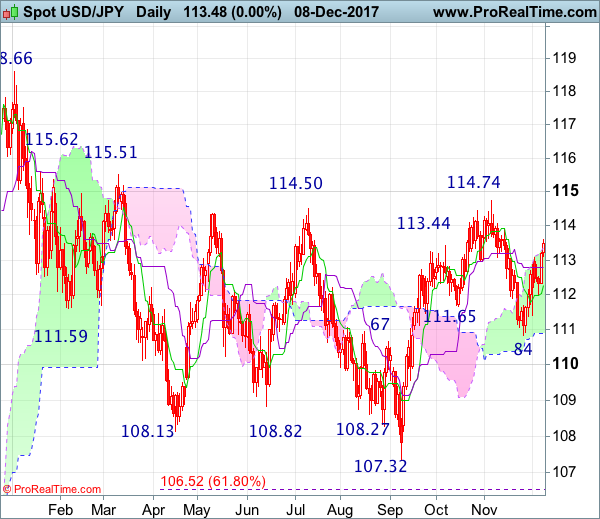

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Dark cloud cover

• Time of formation: 10 Jul 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Evening doji

• Time of formation: 7 Aug 2017

• Trend bias: Down

USD/JPY – 112.87

Although the greenback retreated initially last week, renewed buying interest did emerge at 111.99 (we recommended to buy at 112.10 and a long position was entered) and dollar has rallied from there since, adding credence to our bullish view that low has been formed at 110.84 last month and upside bias remains for this move to extend further gain to 113.91 resistance, however, a daily close above this level is needed to retain bullishness and confirm the fall from 114.74 has ended, bring further gain to 114.40-50 first.

On the downside, whilst pullback to 113.00-10 cannot be ruled out, reckon the Kijun-Sen (now at 112.79) would limit downside and bring another rise later. A daily close below the Tenkan-Sen (now at 112.53) would defer and risk another test of said support at 111.99, having said that, only a break below this level would abort and signal top is formed instead, bring further fall towards support at 111.41. Only a drop below this support would shift risk to downside and signal the rebound from 110.84 low has ended, bring retest of this level. In the unlikely event that dollar drops below 110.84, this would signal the fall from 114.74 top has resumed forweakness to 110.00, then 109.50-60 but price should stay above 109.00-10.

Recommendation : Hold long entered at 112.10 for 114.10 with stop below 112.50

On the weekly chart, the greenback found renewed buying interest at 111.99 last week and has risen again, adding credence to our view that the pullback from 114.74 has ended, then further gain to 113.90-95 would be seen, break there would being a retest of said resistance. Once this resistance is penetrated, this would signal the rise from 107.32 low has resumed for headway to 115.51-62 resistance area, break there would add credence to our view that early erratic decline from 118.66 has ended at 107.32, then upmove to 116.50-60 and possibly 117.00-10 would follow.

On the downside, expect pullback to be limited to 113.00-10 and bring another rebound later to aforesaid upside targets. Below 112.50 would risk test of said support at 111.99 but only break there would abort and suggest top is formed instead, bring test of 111.41 support, break there would suggest the rebound from 110.84 has ended instead, bring retest of this level, break there would extend the fall from 114.74 to 110.00-10, then 109.50-60 but reckon downside would be limited to 109.00 and 108.10-15 should hold from here.

EUR/USD Decline Is Trend Change Or Correction?

Key Highlights

- The Euro made a short-term top near 1.1960 and started a downside move versus the US Dollar.

- EURUSD broke a key bullish trend line at 1.1840 on the 4-hours chart, but does that mean a change in trend?

- Chinese Consumer Price Index in Nov 2017 increased by 1.7% compared with the +1.8% forecast.

- Chinese Producer Price Index in Nov 2017 jumped by 5.8%, less than the +5.9% forecast.

EURUSD Technical Analysis

During late November 2017, the Euro failed to move above 1.1950-1.2000 against the US Dollar. The EUR/USD declined since then and broke key supports such as 1.1900 and 1.1840.

However, does the recent downside break can be seen as a trend change in EUR/USD? Well, the current price action seems corrective from the 1.1960 swing high. The pair has breached the 38.2% Fib retracement level of the last major upside wave from the 1.1554 low to 1.1961 high.

The pair also settled below 1.1800 and the 100 simple moving average (red, 4-hour). Having said that, there is a major support on the downside at 1.1720-1.1740. The stated region is also around the 61.8% Fib retracement level of the last major upside wave from the 1.1554 low to 1.1961 high.

The 1.1700 support is a pivot level and a break below it won’t be easy. Therefore, as long as the pair is above the 1.1700 support, the current downside can be considered as a correction.

Should there be a close below the 1.1700 handle, the pair might decline further and will most likely establish a medium term downtrend.

On the upside, the broken support at 1.1840 and the 100 simple moving average (red, 4-hour) are resistance zones. Once the pair break these resistances, it could resume its uptrend and move past 1.1900.

Chinese CPI

The start to this week was not very positive since China’s CPI in November posted a rise of 1.7% (YoY), which was less than the forecast of +1.8% and even less than the last +1.9%.

In terms of the monthly change, the CPI remained flat at 0%. Looking at the Producer Price Index in Nov 2017, there was an increase of 5.8%, which was less than the +5.9% forecast.

Today, the economic calendar is light, which means the market moves might be limited and will most likely depend on the current sentiment. Last week’s positive US NFP release (228K versus 200K forecast) accelerated USD/JPY’s rise towards 114.00. Therefore, there can be more upsides in the US Dollar in the short term.

Market Morning Briefing: Dollar-Yen Is Currently Testing Resistance

STOCKS

Dow (24329.16, +0.49%) has room on the upside towards 24600-24800 levels. Near to medium term support is visible at 24000 which is likely to hold in the coming sessions.

Dax (13153.70, +0.83%) attempted to break on the upside after some sideways consolidation in the 13200-12900 region. While the index remains above 13000-13100, there could be some scope of testing higher levels near 13400. Else a fall back to levels near 12900 could be possible.

Nikkei (22821.20, +0.04%) has again attempted to test 23000-23200 resistance zone from where a fall back to 22800-22600 is likely this week.

Shanghai (3303.98, +0.43%) seems to have bounced from support near 3260 on the daily candles and while the support holds, a rise towards 3320-3340 again is possible in the coming sessions.

Nifty (10265.65, +0.97%) and Sensex (33250.30, +0.91%) had bounced back last week from support levels as expected. Nifty could see some pause in the 10300-10350 region while Sensex may test interim resistance near 33300. If a pause is not seen just now, Sensex could be headed towards 33500 or higher. Nifty will have to break important resistance at 10350 to turn bullish for the longer term.

COMMODITIES

Gold (1248.60) continues to move down. But note our earlier mentioned support near 1240 has not breached yet and while that holds, some chances of a bounce back from here is likely. Else 1200 could be the next target on the downside. Watch Dollar Index (93.82) which has important resistance near 94. If that holds and produces a sharp rejection, Gold may bounce back from 1240 and not move to further downside in the near term.

Brent (63.10) has resistance at 64, just above current levels and while that holds, a temporary short term fall towards 62-61 levels is possible in the near term.

WTI (57.08) could trade within 56-59 region in the coming sessions while the upward channel on the 3-day candle holds well. Break above crucial resistance at 59 is required to turn bullish for the longer term but that may take at least a couple of more attempts to break above 59.

Copper (2.9775) has been trading along the support near 2.95 for the last 3-4 sessions. While support near 2.95 holds, there could be scope of rising towards 3.00-3.05 in the near term. Near term looks bullish.

FOREX

Dollar-Index (93.858) looks like it could test resistance around 94.00 on 3 day & daily line charts in the next couple of sessions, as we have been expecting since last week, or else, it could see a corrective dip from current levels itself. In case it goes past 94, it could tend towards 94.4-94.5 on the daily candles.

Euro (1.1777) reached a low of 1.173 on Friday, thereby testing support on the 3 day candles (earlier mentioned as 1.175-1.176). It is currently trading at higher levels (around 1.177), which might indicate towards a possible bounce taking place. However, further bearishness would take it lower to test support near 1.17 on the daily candles.

Dollar-Yen (113.54) is currently testing resistance, as earlier mentioned, at 113.5-113.6 on the daily line chart and could now either see a dip or a further rise towards resistance at 114 on the 3 day and weekly charts. This could correspond to Dollar Index moving towards 94.5 and Euro moving towards 1.17.

Pound (1.3399), contrary to our expectations, has again made a move back towards support at 1.335 instead of going up towards resistance near 1.355 on the daily candles. In case this support breaks, we could see pound move further down towards new support at 1.32-1.322 on the daily candles.

Dollar Rupee (64.45) dipped after reaching 64.58 on Friday and could now be expected to test 64.30/40 in the next couple of sessions.

INTEREST RATES

The US yields are all trading higher. The 5Yr (2.15%), the 10YR (2.38%) and the 30Yr (2.77%) are higher by 1bps. The 10Yr may face some rejection near 2.40% in the next few sessions while the 5YR is likely to trade sideways and the 30YR may take a pause near 2.80%.

The Japan-US 10Y (2.33%) has been trading in a narrow region along the resistance on the short term charts. Looking at the medium term charts, there could be some room on the upside in the longer run.

The German-US 10YR (-2.07%) may test -2.10% and then see a short bounce from there in the near term.

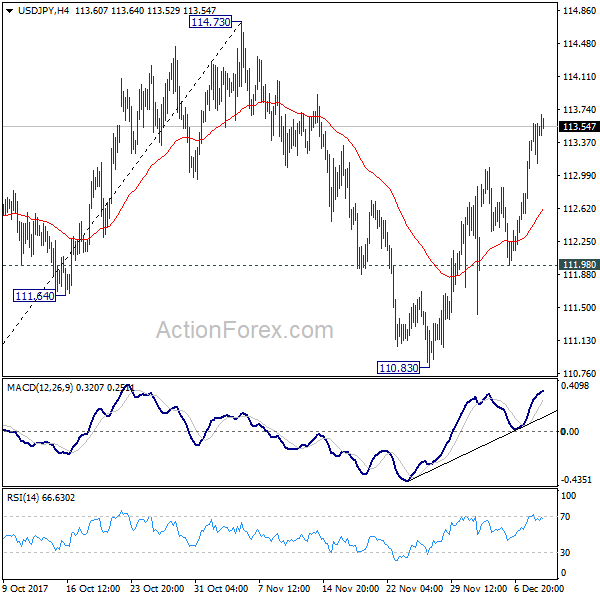

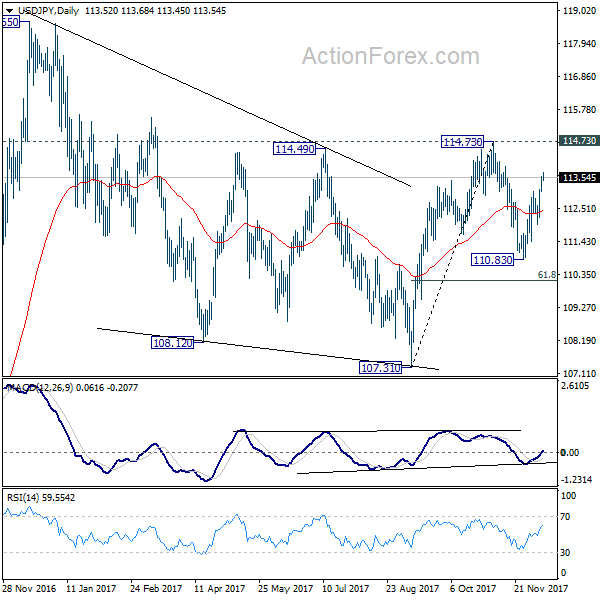

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.16; (P) 113.37; (R1) 113.67; More...

USD/JPY edges higher to 113.68 so far and intraday bias remains on the upside. Current rise from 110.83 would extend to 114.73 key near term resistance. Decisive break there will resume whole rise form 107.31. More importantly, that will confirm completion of medium term correction from 118.65 at 107.31. In that case, retest of 118.65 should be seen next. However, break of 111.98 support will extend the correction from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

Markets Opened Quietly, Preparing for Busy Week with Fed, SNB, ECB, BoE

The forex markets opened the week relatively quietly. Yen is the notably weaker one, extending last week's selloff. Sterling is trading mildly firmer but there is no clear strength. Similarly, Euro also recovers mildly too but it's kept below 1.1814 resistance against dollar so far, maintains an undertone. The calendar is relatively light today and trading could remain subdued. But activity will quickly increase as a busy week starts "informally" on Tuesday. Fed, ECB, BoE and SNB will meet and there are heavy data including US and UK CPI to be featured.

Bitcoin futures trading starts in CBOE

Bitcoin futures trading started with (Chicago Board Options Exchange) CBOE futures Exchange together at the start of this week's global trading hours. CBOE said in a tweet that while operations are generally normal, heavy traffic caused the system to perform "performing slower than usual and may at times be temporarily unavailable." But that was mainly due to interests from the world, rather than actual trading. The futures are based on auction price of bitcoin in USD on the Gemini Exchange.

UK BCC warned of Brexit uncertainty despite last week's deal

UK British Chambers of Commerce warned that despite last week's progress on Brexit negotiation, the vast uncertainties would still undermine investments, until the picture is cleared. BCC director general said that "despite last week's deal, Brexit uncertainty still lingers over business communities, and is undermining many firms' investment decisions and confidence." Also, "despite pockets of resilience and success, and strong results for some UK firms, the bigger picture is one of slow economic growth amid uncertain trading conditions." The lobby group forecasts BoE to keep interest rates on hold until end of 2019. And it downgraded 2018 growth projection from 1.2% to 1.1%.

Japan business conditions improved

In Japan, the Ministry of Finance's business survey index (BSI) showed generally improved business conditions. For large corporations, with capital of JPY 1b or above), all industry business conditions improved to 6.2, up from 5.1. Large manufacturing conditions rose to 9.7, up from 9.4. Large non-manufacturing business conditions rose to 4.5, up from 2.9.

China CPI slowed, ease pressure for tightening

In China, CPI slowed to 1.7% yoy in November, down from 1.9% yoy and missed expectation of 1.8% yoy. PPI also dropped to 5.8% yoy, down from 6.9% yoy and met expectations. Slowing inflation is seen as welcomed by both the authority and the markets. The data suggests that China is in no rush to raise interest rate or tighten up monetary policies.

Looking ahead - Fed, ECB, BoE, SNB to meet

It's an extremely busy week with four central banks featured. SNB, ECB and BoE are all expected to keep policies unchanged. And, we're not expecting any surprise from them. Fed is widely expected to raise interest rate for the third time this year. Federal funds rate would be hiked by 25bps to 1.25-1.50%. The voting, inflation forecast and policymakers' own dot plot forecast will be key for assessing whether Fed would hike three more times next year.

In addition to that, UK CPI and US CPI will catch most attentions. Other important data include German ZEW, Eurozone PMIs, US retail sales, Japan Tankan survey and Australia employment

Here are some highlights for the week ahead:

- Tuesday: Australia house price index, NAB business confidence; Japan tertiary industry index, PPI; UK CPI, PPI; German ZEW; US PPI

- Wednesday: German CPI final; UK employment; US CPI, FOMC rate decision

- Thursday: Australia employment; China industrial production, fixed asset investment, retail sales; UK RICS house price balance; Swiss PPI, SNB rate decision; Eurozone PMIs, ECB rate decision; UK retail sales, BoE rate decisions; Canada new housing price index; US retail sales, jobless claims, import prices, PMIs

- Friday: New Zealand manufacturing index; Japan tankan survey; Eurozone trade balance; Canada manufacturing sales; US Empire State manufacturing, industrial production

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.16; (P) 113.37; (R1) 113.67; More...

USD/JPY edges higher to 113.68 so far and intraday bias remains on the upside. Current rise from 110.83 would extend to 114.73 key near term resistance. Decisive break there will resume whole rise form 107.31. More importantly, that will confirm completion of medium term correction from 118.65 at 107.31. In that case, retest of 118.65 should be seen next. However, break of 111.98 support will extend the correction from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large All Industry Q/Q Q4 | 6.2 | 5.8 | 5.1 | |

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q4 | 9.7 | 10 | 9.4 | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Nov | 4.00% | 4.10% | 4.10% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | 49.80% |

Central Banks Competing For Stage Time With The Crypto Craze

Central Banks competing for stage time with the Crypto Craze

A quorum Central bank policy decision will take place this week; only the Fed is expected to change its policy. None the less policy guidance from the FED, ECB and BOE will be monitored and will play a significant factor on year-end positioning. We’re off to an inconspicuous start this morning but I’m confident things will pick up quickly given several evolving narratives.

Non-Farm Payroll

Traders initially took hawkish inference of Friday’s employment headline but markets where tempered again by the soft AHE print. While the wage data did little to forward the view for an early Fed hike in 2018, the unexpected bounce in inflation forecasts after the University of Michigan ( UofM)Sentiment’s 1year inflation expectation gauge jumped from 0.3% to 2.8% supported the dollar into the NY close.

While we could see a more poignant shift to the four rate hike camp for 2018, the actual raw inflation data indicates slow forming wage growth suggesting little haste to price in more than three hikes next year at this point.

G-10 FX

The Japanese Yen

The Trump trade is back on the radar with US infrastructure spending on the table and could underpin USDJPY sentiment.The market was reluctant to chase the USD aggressively higher on that basis alone initially, but fiscal spend could play out as a significant dollar driver in 2018

Friday’s US economic data was a tower of strength for the greenback suggesting the best trend trades heading for year-end are stocks, rates and USDJPY higher.

USDJPY may be under-owned after Novembers tendency to print lower highs, and more depressed lows kept a lot of USD bulls at bay, suggesting the pair could be in catch up mode heading into year-end.

The Euro

If there was s currency weighted down by year-end positioning, it has to be the Euro. Last week’s European November PMI came in at their highest level since 2011 yet failed to inspire as short EURGBP trades remain the flavour de jour with the positive shift on Brixit. Enigmatic or not duly appreciated, EURUSD dealers may be underpricing a more hawkish outcome from this weeks ECB which could provide a significant push higher for the Euro.

The Australian Dollar

The Aussie continues to limp along following last week’s weak GDP data and weaker than expected trade data due to the sharp decline in Iron ore prices. There are far too many domestic economic disappointments for traders to overlook and with the Australian employment data looming large, the Aussie is prone to a one-two knock out punch from the cocktail of more hawkish fed forward guidance and weaker employment data this week. While the RBA will put up little fuss, anyone still holding out for a year-end Aussie dollar recovery would have a painful week if this toxic cocktail did unfold.

Asia FX

Chinese Yuan

The Yuan remains handcuffed by domestic economic uncertainty but as we enter the year-end stretch run a resurgent USD is likely to present some headwinds to the RMB complex as well.

On the data front, China PPI cooled, and CPI remained low key. The producer price index rose 5.8 percent in November from a year earlier, matching the projection in a Bloomberg survey and slowing from 6.9 percent in October while the consumer price index climbed 1.7 percent, the National Bureau of Statistics said on Saturday, less than the median forecast of 1.8 percent. The moderate inflation eases pressure on the Pboc to hike rates which is a positive as mainland markets remain a bit wobbly as market regulators look for a delicate balance between financial reform and market stability.

Food prices were the most significant drag on the consumer side while at the factory gate, lower commodity prices were the primary cause of the drop.

Singapore Dollar

Asian currencies have done well this year, and the SGD is no exception. But like its regional peers, a stronger USD and a faster pace of US interest rate normalisation will be the most significant negative driver to local sentiment.

However, with the positive global growth narrative and to this point, a rather benign Fed, the SGD could be well be positioned to appreciate further in 2018.

But with China’s policy prerogatives shifting from expansionary to controlling risk, there remain substantial downside risks to China’s growth even as its deleveraging efforts are expected to moderate. Lower production in China could present some gusty headwinds to the stronger SGD narrative in 2018.

In the meantime, local traders will focus on this week’s US Rate decision but more so to the forwarding guidance as a more hawkish leaning Federal; Reserve Board into 2018 would weigh negatively on SGD sentiment heading into years end.

The Malaysian Ringgit

The US NFP headline was robust, but it was the U of M inflation expectation gauge the firmed the USD into weeks end and provides it with a good base entering the trading week

Its a case of a stronger USD narrative, as opposed to any tarnishing of local sentiment weighing on the Ringgit.

While Malaysia is expected to raise interest rates next year, speculation on the faster pace of interest rate normalisation and a stronger dollar may present some headwinds for the MYR near-term as the shifting USD interest rate outlook will drive investors to the US dollar.

Despite the USD dollars resurgent speculative appeal, real Malaysia domestic and external positives should outweigh risky wagers on the USD which should continue to support the Ringgit’s decisive run.

However, the market should remain reticent as we enter holiday thin liquidity conditions with the Ringgit expected to remain stable to slightly defensive as year-end USD corporate demand picks up.

Energy Markets

Oil Prices

On Friday, China’s November Crude imports surged to a staggering 9 million barrels a day, up from 7.3 million barrels a day the month prior.The eye-watering 2nd most substantial import number on record should continue to drive sentiment early in this week as buzz remains loud. Also, the weekend escalation of middle east tension should lend support to the market.

But the resurgent USD could dampen the positive sentiments after Friday bullish US economic data has dollar bulls pumped. As well US shale Drillers added two oil rigs in the week to Dec. 8, bringing the total count up to 751

As a whole, however, oil prices remain a bit of a paradox. If prices continue higher, US Shale OIl will increase production, and of course, there remains a chance that OPEC tweaks the deal to raise output at the June OPEC meeting. And on the downside, any convincing break of 50 per barrels would likely trigger verbal intervention from OPEC that would push for a production cut extension through 2018.

Monday Morning Market Musings

Crypto Craze – Bitcoin arrives in the mainstream

Bitcoin is on the verge of a watershed moment, and over the next few months, we should finally solve the vexing question if cryptos are accepted as a legitimate asset class by professional traders.The CBOE’s professionally geared seamless futures trading solution is set to kick off Bitcoin future trade today while CME Group will follow up with its Bitcoin contract, on December 18, 2017. Expected participation is purportedly not that strong out of the gate, but with year-end code freeze policies kicking in, we should see a better buy in early 2018. Hopefully, there is no rush to judgment as there remains a positive vibe on the street with most shops looking to add Bitcoin futures to there stable of assets early next year.

Regardless of what side of the debate you’re on, what’s undeniable is that the current euphoria and the extreme levels of price volatility offer the brave of heart some excellent speculative opportunities.

However and from that perspective, it’s little more than an attention-grabber to suggest future trading levels given the lack of quantified modelling. Over the years I’ve made some horrible trades using capricious and non-objective strategies, but applying guesswork to Bitcoin is little more than throwing spaghetti at the wall and fraught with peril. Bitcoin trading is a tricky proposition and risk management should be front and foremost in all strategies. After all, there’s nothing worse than chasing the markets only to find yourself the ” bag holder” at the wrong side of the range.

Self-serving Bitcoin soothsayers can influence the price but so too does headline FUD ( ‘fear, uncertainty and doubt’), naysayers. And with Bitcoin markets still evolving, no one can predict prices any more than they can accurately predict the weather.

Bitcoins are concentrated among a few players, a random move by a significant market actor could cause a paradigm shift in sentiment, but ultimately it could be ” FUD” that propels Bitcoins hurtling back to reality with the ensuing air burst leaving investor carnage in its wake.

USDCHF – Risk Remains Higher But With Warning

USDCHF - The pair may be biased to the upside but faces pullback threats. On the downside, support lies at the 0.9900 level. A turn below here will open the door for more weakness towards the 0.9850 level and then the 0.9800 level. On the upside, resistance resides at the 0.9950 level where a break will clear the way for more strength to occur towards the 1.0000 level. Further out, resistance comes in at the 1.0050 level. Above here if seen will turn attention to 1.0100. All in all, USDCHF faces further upside pressure but with caution.

EURUSD – Closes Lower On Bear Pressure But With Caution

EURUSD - The pair weakened further the past week leaving risk of more decline on the cards. Resistance comes in at 1.1850 level with a cut through here opening the door for more upside towards the 1.1900 level. Further up, resistance lies at the 1.1950 level where a break will expose the 1.2000 level. Conversely, support lies at the 1.1750 level where a violation will aim at the 1.1700 level. A break of here will aim at the 1.1650 level. Below here will open the door for more weakness towards the 1.1600. All in all, EURUSD faces further downside weakness