Sample Category Title

Summary 12/11 – 12/15

Monday, Dec 11, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Dec 12, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Dec 13, 2017

[php_everywhere] [/php_everywhere]

Thursday, Dec 14, 2017

[php_everywhere] [/php_everywhere]

Friday, Dec 15, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Solid Job Gains in November, But Wages Disappoint

U.S. Review

Solid Job Gains in November, But Wages Disappoint

- Hiring was solid in November with employers adding 228,000 new jobs. The unemployment rate held steady at 4.1 percent, while wage growth rose less than expected.

- The ISM non-manufacturing index fell 2.7 points in November, but remained firmly in expansion territory at 57.4.

- Despite total factory orders slipping 0.1 percent in October, core capital goods orders signaled equipment spending is likely to remain strong in Q4.

- The trade balance widened by $3.8 billion in October and points toward trade being a drag on GDP growth in Q4.

Solid Job Gains in November, But Wages Disappoint

Employers added 228,000 new jobs in November, which was better than expected. The print is particularly encouraging given that the distortions related to the storms this hurricane season have largely dissipated. Gains were widespread across major industries, with only information and federal government employment seeing declines.

Unemployment held steady at 4.1 percent last month but is down from 4.6 percent a year ago. The labor force participation rate was also unchanged at 62.7 percent, which we view positively in light of the aging of the population weighing on overall participation.

Wage growth remained muted in November. Average hourly earnings rose 0.2 percent, which was short of expectations and followed downward revisions to September and October. The year-over-year rate rose to 2.5 percent, but has weakened since late last year. One offset to the tepid wage growth this month, however, was that workers were offered more hours at work. The average length of the workweek edged up to 34.5 hours, which, along with the net jobs added, suggest income derived from the labor market has strengthened at a 4.7 percent annualized rate the past three months.

Activity Expanding Across Industries

Like the employment report, the November ISM nonmanufacturing index pointed to broad growth across industries. The index slipped 2.7 points, but remained squarely in expansion territory at 57.4. Of 18 industries, only one reported contracting over the month (agriculture & forestry). Most sub-indexes, including new orders, employment, and backlogs, pulled back in November, but remained at levels consistent with a decent pace of growth.

The ISM manufacturing index was released last Friday and showed that factory activity has also remained strong in recent months. This week we got additional insight on the manufacturing sector in the factory orders report. The total value of orders edged down 0.1 percent in October, but this this came on the heels of a solid (and upwardly revised) 1.7 percent gain in September. The negative print for October stemmed largely from a drop in aircraft orders. Nondefense capital goods orders, excluding aircraft—a bellwether of private equipment spending— edged up and have risen at an impressive 16.4 percent three month average-annualized pace. The nondurables segment has also improved in recent months, with shipments rising 0.7 percent in October.

Trade Winds Shifting

A narrowing in the trade deficit has been additive to GDP in recent quarters, but that support looks to be coming to an end. In October, the trade balanced widened by $3.8 billion. Exports stalled over the month, while imports rose 1.6 percent. The trade data are still being affected from the hurricanes this season, so revisions could be larger than usual. That said, we expect that the trade balance will continue to widen on trend in the year ahead as steady domestic demand leads import growth to outpace exports.

U.S. Outlook

CPI • Wednesday

October's Consumer Price Index (CPI) grew a slower 0.1 percent over the month, pulling the year-over-year rate back to 2.0 percent behind a hurricane-driven pullback in energy prices. However, core inflation, which excludes food and energy, rose to 1.8 percent over the year, and over the past three months has grown at an annualized 2.4 percent rate. Core services was the primary culprit behind inflation weakness earlier in the year, but bounced back in October by 0.3 percent on broad-based gains. On the goods side, used car prices were up a strong 0.7 percent, while medical goods and tobacco products also showed strength.

Our outlook has been that inflation weakness has been caused by unique, transitory factors that have understated the "true" CPI. Many categories that had held back inflation have gained some momentum, which is supportive of a December rate hike and continued, tightening, in our view.

Previous: 0.1% Wells Fargo: 0.4% Consensus: 0.4% (Month-over-Month)

Retail Sales • Thursday

Retail sales rose 0.2 percent in October, down from an upwardly revised September print of 1.9 percent but besting expectations of a flat month. September's gain was the highest monthly increase since March 2010 thanks to surges in fuel prices, building supplies and auto sales. Hurricane factors caused the boosts in these categories. Furniture stores likely also received storm boosts, up 0.7 on the month and up 4.4 percent over the year, as replacement purchases are made. Retail sales are now up a solid 4.6 percent over the year as the holiday season approaches.

In all, retail sales showed broad-based strength in October, consistent with continued consumer spending growth. Control group sales, stripping out the volatile food, auto and home improvement categories, increased stronger than the headline in the month, an encouraging sign for retailers and fourth quarter GDP.

Previous: 0.2% Wells Fargo: 0.2% Consensus: 0.3% (Month-over-Month)

Industrial Production • Friday

Industrial production (IP) increased by 0.9 percent in October, boosted by a 1.3 percent gain in manufacturing output, equaling the largest monthly increase since 2010. While a strong reading, the surge is exaggerated by factories coming back online after being knocked out of production from hurricanes. Specifically, chemicals, petroleum & coal and motor vehicle & parts output each saw significant increases. Although exaggerated, the general trend in IP is one of positive growth. Over the year, IP and manufacturing are up 2.9 and 2.7 percent, respectively. The ISM manufacturing index remains near cycle highs, business equipment investment looks to be encouraging and nearly three times as many manufacturing jobs have been added year to date compared to this time last year.

Global economic growth has helped drive up IP this year, and combined with the weaker dollar, we see steady growth in IP and manufacturing on the horizon.

Previous: 0.9% Wells Fargo: 0.2% Consensus: 0.3% (Month-over-Month)

Global Review

Economic Expansions in Europe Remain Intact

- Data released this week showed that the drivers of real GDP growth in the Eurozone in Q3 were broad based, which enhances the self-sustaining nature of the expansion. Despite some recent weakness in German industrial production, the expansion in the Eurozone appears to have remained intact in the fourth quarter.

- Growth in the British economy appears to have remained positive in the fourth quarter as well. However, as long as Brexit uncertainties linger, the outlook for the U.K. economy will remain clouded.

Economic Expansions in Europe Remain Intact

Data released this week confirmed that real GDP in the Eurozone rose 0.6 percent (2.4 percent at an annualized rate) on a sequential basis in Q3 (see graph on front page). The preliminary estimate of Q3 GDP growth was released a few weeks ago, but the data that were released this week provided a breakdown of the GDP data into its underlying demand-side components. Importantly, all the major components posted positive growth rates in Q3. Specifically, real consumer spending grew at an annualized rate of 1.3 percent, fixed investment spending rose 4.3 percent, real government consumption expenditures edged up 1.0 percent, and real exports climbed 4.7 percent. The broadbased nature of the spending increases enhances the selfsustaining nature of the economic expansion in the euro area.

That said, the fourth quarter appears to have gotten off to a slow start. Industrial production (IP) in Germany plunged 1.4 percent on a monthly basis in October, which follows the 0.9 percent drop registered during the previous month. If German IP remains unchanged in November and December, then it will decline 1.2 percent (not annualized) in Q4 relative to Q3. Is the expansion in the Eurozone running out of steam?

In our view, it would be premature to panic about the economic outlook in the overall euro area. For starters, IP in France jumped 1.9 percent in October, which follows the 0.8 percent gain registered during the previous month. Moreover, German factory orders, which are highly correlated with German IP, rose 1.2 percent in September and another 0.5 percent in October. On a year-over-year basis, growth in German factory orders remains resilient (top graph). In other words, the pipeline in Germany remains full despite some temporary weakness in production recently. German IP should rebound in coming months.

Across the English Channel, IP in the United Kingdom was flat in October on a sequential basis although the year-over-year growth rate remained solid (middle graph). However, the construction sector remained weak with output in that sector down 1.7 percent in October relative to the previous month. On a year-ago basis, construction output was down 0.2 percent in October.

If the purchasing managers' indices are any indication, then the U.K. economy has continued to expand in the fourth quarter, albeit at a modest pace. As shown in the bottom graph, the manufacturing PMI rose to a four-year high in November. However, the comparable index for the service sector, which accounts for the vast majority of value added in the British economy, fell back during the month although it remained above the demarcation line separating expansion from contraction.

As discussed on page 5, the Bank of England (BoE) holds a policy meeting next week, and it is virtually assured that it will keep policy unchanged. Although the UK and the EU this week appear to have agreed to the terms of their divorce, there is much uncertainty still surrounding the Brexit process. As long as that uncertainly lingers, the outlook for the U.K. economy will remain clouded and the BoE will remain cautious.

Global Outlook

China Industrial Production • Wednesday

The week sees two important releases, one that looks at the production side in China: the industrial production index while the second, the retail sales index, look at what is happening to domestic consumption in the country. Both releases are for the month of November. The Chinese industrial production index has been relatively stable on a year-over-year basis as well as on a year-todate basis. However, markets are expecting a slight slowdown from the average over the past three months, consistent with what we have seen from analysts with regards to economic growth in the second-largest economy of the world.

Meanwhile, the retail sales index has shown some weakening lately while consensus is expecting some slight rebound. If that is not the case and we see some more weakness in this index, it will be the first time since February 2004 that growth in this index has dropped below 10 percent on a year-earlier basis.

Previous: 6.2% Consensus: 6.2% (Year-over-Year)

Eurozone Manufacturing PMI • Thursday

On Thursday, markets will have a chance to look at an advance reading of how the Eurozone manufacturing sector ended the year with the release of the preliminary December manufacturing PMI. We will also get the release of Germany's preliminary manufacturing PMI. Both manufacturing PMIs surprised the markets in November by hitting high levels for the series, at 60.1 for the Eurozone and at 62.5 for Germany, so an improvement from such strong performances is probably not expected (see the Global Review section for more insights on this topic). However, if these preliminary readings for the Eurozone are able to beat the November numbers, then this will be a good signal for the continuity of growth in the Eurozone as well as in the global economy in general.

Meanwhile, on Tuesday markets will also get the ZEW expectations index for both the Eurozone as well as for Germany.

Previous: 60.1 Consensus: 59.7

Bank of England Interest Rate • Thursday

On Thursday, markets are expecting the Bank of England to stay put in terms of monetary policy by not changing the policy rate, which today stands at 0.50 percent. The decision will end a week full of data releases for the United Kingdom, with consumer price inflation scheduled to be released on Tuesday. Several employment measures are going to be released on Wednesday, including the claimant count rate and the jobless claims change for November along with the ILO unemployment rate and several data points on average and weekly earnings for October.

Also on Thursday, we will also get the release of retail sales for the month of November, a series that has been weakening considerably lately and that could point to further weakness in consumer demand in the United Kingdom.

Previous: 0.50% Wells Fargo: 0.50% Consensus: 0.50%

Point of View

Interest Rate Watch

Turning a Blind Corner

Economic fundamentals and policy intentions are turning a corner as we turn to a new year. Our view is that the economic fundamentals signal a pick up in the pace of inflation, as measured by the PCE deflator, while monetary policy intentions are for further fed funds rate increases in 2018. The upward turn in both series alters the pattern of flat and low for the past three years. We are turning the blind corner in the fundamentals.

Inflation Upswing

With the PCE deflator at 1.4 percent on average over the past three years, which is significantly below the FOMC's benchmark 2.0 percent target, our expectations are for a rise in the PCE deflator to 2.0 percent in 2018. In contrast, the median inflation expectations from the University of Michigan survey (top graph) has drifted lower since 2014 and settled in around 2.5 percent for next year. An upward turn in the measured pace of the deflator would support the case for further FOMC rate increases.

Smaller Margin for Error

One concern we have expressed in recent months has been the narrowing of the margin between the Fed funds rate and the PCE measure of inflation (middle graph). Looking into 2018, the implied future of the FOMC's intended funds rate path would produce a positive real funds rate that we have not seen for the past two years. How would this positive real rate impact credit demand and supply, would be an interesting question given our lack of experience in recent years, and the recent extent of market financing.

A Turn in NFC Interest Expense?

In recent years, the pace of corporate bond issuance has been very strong. As illustrated in the bottom graph, net interest expense as a percent of operating surplus has been very low compared to the past but the series is rising just modestly over the past two years. With the rise in interest rates projected by the FOMC we should see a sharper upward turn in these interest rate expenses and perhaps a stretch for credit quality.

Credit Market Insights

How Will Consumers Pay for Their Holiday Purchases?

Over the 2017 holiday season, consumers are planning to spend $967.13 on average, according to the National Retail Federation. This year, more of these transactions are likely to be made using debit and credit cards, which has implications for credit card balances and how much consumers spend.

Cash remains a dominant payment method. In 2016, 31 percent of U.S. transactions were conducted in cash, compared to 27 percent using debit cards and 18 percent using credit cards, according to the Diary of Consumer Payment Choice. However, cash made up only 8 percent of the value of transactions, since it is typically used for small sums (average of $22, versus $57 for credit cards).

While cash is not close to its deathbed, cash use is declining as a share of transactions. As recently as 2012, cash made up 40 percent of transactions, but is now being replaced by credit, debit and electronic bill pay. One factor behind this trend is the rise of e-commerce, since cash transactions almost always occur in person. In the third quarter, retail e-commerce sales reached $115.3 billion, up 15.5 percent on the year. A continued shift to online shopping may therefore contribute to increased demand for credit cards and, potentially, rising credit utilization.

Higher credit and debit card use may also boost spending. Customers can be willing to pay up to twice as much when using credit cards rather than cash, because of higher liquidity but also because "plastic" divorces the joy of shopping from the pain of paying.

Topic of the Week

Don't Count Out Millennial Homeownership

Millennials came of age during one of the most tumultuous economic periods in generations. A poor labor market and a vastly different housing landscape following the financial crisis has sparked many to wonder whether Millennials' relationship with housing would ever resemble that of the generations that came before.

In 2016, the share of 25-34 olds living with their parents rose to a record high 15.0 percent. The increase over the past decade marked an acceleration from a longer-term trend of fewer young adults living independently (top graph). Economic factors and shifting preferences are to blame. In addition to starting their career in what was until rather recently a sluggish job market, a hallmark of the Millennial generation has been hefty student debt loads. Housing costs that have outpaced wage growth during this expansion have made also it more difficult for Millennials to afford to live on their own.

Changing family forms are partly responsible for "failure to launch" as well. Over the last half-century, the age of first marriage increased by more than six years. As fewer young adults live with spouses/partners, staying with relatives or roommates offers an alternative means to reduce living costs by sharing expenses.

There are some recent signs of improvement, however, in Millennials moving out and becoming homeowners. In 2017, the share of young adults aged 25-34 living with parents declined for the first time since 2011. Ownership among households under age 35 has risen 1.5 percentage points since the cycle low set in mid-2016, which is more than any other age group (bottom graph).

While the timeline may be pushed back, the vast majority of Millennials still report a desire to buy a home one day. As Millennials age into higher-paid, more secure jobs and settle down with partners, they are gaining the financial resources to support independent households more easily. We believe that is too early to write them off as a generation of renters. See our recent report "Are Millennials Moving Out and Settling Down?" for more detail.

The Weekly Bottom Line: The Fed Can’t Ignore A 3-Handle On Unemployment

U.S. Highlights

- The Federal Reserve meets next week and is near-universally expected to raise interest rates by 25 basis points, bringing the target for the fed funds to a range of 1.25% to 1.5%.

- The U.S. labor market continues to make progress with 228k jobs added in November. Given the current rate of job creation, it is only a matter of months before the unemployment rate pushes below 4%.

- The American economy is likely to continue its winning streak. Even without tax cuts, 2018 is likely to see growth around 2.5%. With increasing prospects for fiscal stimulus to push growth even higher, the Federal Reserve will continue to remove monetary accommodation.

Canadian Highlights

- October trade data showed real exports increasing and imports dropping, setting up for net trade to make a sizeable positive contribution to economic growth in the fourth quarter.

- Housing starts surged in November, but building permits suggest that some cool-off in building activity is likely going forward. November data from local real estate boards was a mixed bag with strength in Toronto but some moderation in Vancouver.

- The Bank of Canada stood pat on rates but was surprisingly dovish in the accompanying statement, causing the Canadian dollar to sell off and throwing some cold water on near-term rate hikes.

U.S. - The Fed Can't Ignore A 3-Handle On Unemployment

As the Federal Reserve meets next week to decide interest rate policy for the final time in 2017 it is faced with ebullient financial markets and an economy that is operating increasingly close to full capacity. With November's gain of 228k jobs, the streak of positive job creation entered its 86th month. The unemployment rate in November held steady at 4.1% (a seventeen year low), but with job growth trending above 200k, it is only a matter of months before it pushes to lows not seen since the 1960s.

Monetary policy is set with an eye to the future. As a thought experiment, assume that the rate of job creation continues at around its current pace of 200k a month. Given demographics, this is more than double the pace needed to keep up with labor market growth. Should this continue over the next year it will push the unemployment rate to just 3.4% - the lowest rate on record (data goes back to 1947).

While there are some doubts about the strength of the relationship between unemployment and inflation, an unemployment rate that begins with a three handle is certain to raise eyebrows. The unemployment rate is already below the FOMC's assumed neutral level of 4.6%, and other broader measures of labor market slack, such as long-term unemployed and the U-6 measure of labor underutilization, continue to trend lower.

The hope is that employer demand for labor will draw discouraged workers back into the labor force, but the pool of such potential workers is dwindling. Relative to the population, the share of people outside of the workforce (not actively searching for a job), who want a job now is at the same rate it was prior to the recession (Chart 1). The employment to population ratio of core working-aged women (between 25 to 54) has already regained its pre-recession peak (Chart 2). The ratio is still lower for men, but it has been steadily declining for no less than seventy years. Subtracting the long-run trend, the ratio does not appear all that abnormal.

Even without tax cuts, the U.S. economy appears likely to continue its winning streak. Growth in the fourth quarter is tracking close to 3%. With supportive financial conditions, economic growth in the range of 2-2.5% appears likely over the next year. Into this environment, Congress looks increasingly likely to pass a tax cut that will raise the deficit and add as much as $1 trillion to the national debt over the next decade.

Any boost to growth from the proposed tax reform plan is likely to show up in higher wages and inflation, which may have to be offset by additional interest rate hikes. Our model simulations based on a Taylor Rule monetary policy reaction function suggest that for every 0.25 percentage points added to economic growth above its trend rate, the Fed should raise rates by an additional 25 basis points. While there is considerable uncertainty around the timing of tax cuts, investors should not discount the likelihood that what Congress giveth the Federal Reserve may taketh away.

Canada - BoC Stands Pat on Rates, But Statement Dovish

After last week's bevy of data, and a blowout jobs report, this week was a little bit calmer. However, there were still a few key economic data releases on trade and housing to keep investors occupied, with a fireworks-inspiring starts report this morning. Still, the highlight of the week was arguably the Bank of Canada's interest rate decision which, despite the consensus decision, left many scratching their heads and the loonie reeling.

Earlier in the week, the merchandise trade report indicated that Canada's trade deficit narrowed to $1.5 billion in October, marking its lowest level since May (Chart 1). The narrowing was related to both a rise in exports (+2.7%) as well as a sizable drop in imports (-1.6%). In volume terms, exports also increased while imports declined. The bounce back in exports was welcomed, particularly in light of the extremely weak Q3 performance. Overall, the improvement in the trade balance sets up for net exports to make a positive contribution to growth in the fourth quarter.

Canada's housing market was also thrust into the spotlight this week, thanks to a trio of releases. October's permitting data showed residential construction intentions slowing (Chart 2), continuing a recent trend and pointing to some moderation in activity. However, that moderation is not yet upon us, with housing starts data for November indicating that builders broke ground on a whopping 252k homes (in annualized terms) (Chart 2). The increase was led by the multifamily segment, with Toronto starts surging 28k to 45k while Vancouver's pulled back 3k to 32k. The same pattern showed up in housing resales data for Toronto and Vancouver from their respective real estate boards, with the sales increase in Toronto providing further evidence that the market is shrugging off the recent policy-induced turbulence.

Arguably, the biggest event on the economic calendar in Canada this week was the Bank of Canada's decision on interest rates. The Bank held rates steady, as largely expected, though the sharply dovish slant in the accompanying statement was a bit of a head-scratcher. The reference to "labour market slack" was particularly surprising after Friday's LFS report which showed that the unemployment rate dropped to the lowest level in nearly ten years in November. The cautious tone, which threw cold water on near-term hikes, led the Canadian dollar to sell off by nearly 1% in the wake of the Bank's communication.

The Bank gave a nod to improving data, given its upbeat assessment of the economy and indicated that higher rates would likely be required over time. At the same time, the Governing Council chose to be extremely patient, noting that they will be "cautious" and "guided by incoming data" before any rate hike occurs. Given that the economy is effectively becoming one of excess demand and growth expected to exceed the BoC's projection in the fourth quarter of this year, we believe the case for higher rates remains intact. And while a January hike is not without merit, the recent dovish tilt by the Bank of Canada suggests that the next hike may not come until later in the quarter and maybe as late as spring time.

U.S.: Upcoming Key Economic Releases

U.S. Consumer Price Index - November

Release Date: December 13, 2017

Previous Result: 0.1% m/m

TD Forecast: 0.4% m/m

Consensus: 0.4% m/m

We expect headline CPI inflation to firm to 2.3% y/y in November, with prices up 0.4% m/m. Energy prices should be a net positive, helped by higher gasoline prices, while continued subdued gains in food prices cannot be excluded. Base effects for the latter, however, still point to a y/ y acceleration. Excluding food and energy, we expect core CPI to print a 0.2% m/m increase. A key driver is core goods prices, which in the prior month posted its first m/m increase since January. We believe another m/m gain is possible on the back of firming import prices, keeping the core inflation rate stable at 1.8% y/y.

U.S. Retail Sales - November

Release Date: December 14, 2017

Previous Result: 0.2%, ex-auto 0.1%

TD Forecast: 0.2%, ex-auto 0.6%

Consensus: 0.3%, ex-auto 0.7%

We expect retail sales to rise 0.2% in November, consistent with Q4 real consumer spending at a pace slightly above 2%. Motor vehicle sales are likely to be a drag, in line with the continued moderation in light weight auto and truck sales after Hurricane Harvey boosted sales substantially in September. Offsetting increases should be found in gasoline station receipts, on higher gasoline prices, along with a modest rise in the control group (excluding auto, gasoline station, food services and building material sales). We are cautious to take any signal from holiday shopping reports, which were upbeat for online sales and relatively bearish for in-store sales. If anything, risks skew to the downside based on the strength in the prior two months, and we look for a 0.2% increase in this category. Our forecasts would still leave Q4 real consumer spending tracking above 2%.

Canada: Upcoming Key Economic Releases

Canadian Manufacturing Sales - October

Release Date: December 15, 2017

Previous Result: 0.6% m/m

TD Forecast: 1.0% m/m

Consensus: N/A

We expect Canadian manufacturers to head into Q4 on a decent note. Headline manufacturing sales should rise 1.0% m/m, reflecting a sharp increase in factory prices whereas volumes should underperform. Labour disruptions will continue to weigh on motor vehicle production and a correction of the outsized gains in other transportations categories (i.e., aerospace, railroad, and "other") will provide a headwind. Petroleum shipments should rise on foreign demand while a pickup in refining activity will support shipments of chemicals used in the process. Overall, manufacturing should make a positive, albeit muted, contribution to October GDP, though we expect a strong print in November on a rebound in motor vehicle output.

Dollar Higher Ahead of Fed December Rate Hike

Central bank decisions to dominate busy week

The US dollar appreciated during the week as the tax reform inched closer to reality. Fundamental data in the US was positive for the currency but hourly wages again disappointed by coming below expectations. Given the importance of inflation indicators inside the Fed stagnant wages could make it hard on the US central bank to keep raising rates in 2018.

The economic calendar is packed on the week of December 11 to 15. Inflation data in the US will be published by the Bureau of Labor Statistics on Wednesday, December 13 at 8:30 am. Core CPI is expected to gain 0.2 percent but prices taking into consideration food and energy are forecasted to increase by 0.4 percent.

The U.S. Federal Reserve will release its quarterly economic projections and Federal Open Market Committee (FOMC) statement on Wednesday, December 13 at 2:00 pm EST. The highly anticipated December meeting of the Fed is expected to bring a 25 basis points rate hike. The market has already priced in that move as it was heavily telegraphed by policy makers. Economists are forecasting 3 rate hikes in 2018 and the dot-plots could align with those estimates. Fed Chair Janet Yellen will make her final appliance as Chair when she hosts the FOMC press conference at 2:30 pm EST.

The Bank of England (BoE) will release its monetary policy summary on Thursday, December 14 at 7:00 am EST. There is no change expected to the UK benchmark rate which stands at 0.50 percent. The European Central Bank (ECB) will follow close by with their release of their rate statement at 7:45 am EST. ECB President Mario Draghi will host a press conference at 8:30 am EST. The ECB is not expected to change its QE program or interest rates at this time, but the market will be on the lookout for its 2020 growth and inflation forecasts.

The EUR/USD lost 1.12 percent in the last five days. The single currency is trading at 1.1762 depreciating against a rising USD. The dollar has gained on the back of tax reform optimism. The lack of pro-growth policies this year saw the dollar freefall as the promised tax reform and infrastructure spending have not materialized. The two bills passed by Senate and Congress could make tax reform a reality and have given the greenback a shot in the arm. Politics remain a big driver of the market. This week President Trump signed a short term funding bill pushing back the larger debt ceiling debate to December 22.

Central banks will be front and center in the coming days, with the U.S. Federal Reserve and the European Central Bank (ECB) a day apart. The anticipated December rate hike in the US will widen the gap between benchmark rates as the Mario Draghi is not expected to tighten monetary policy yet, despite strong economic data out of Europe.

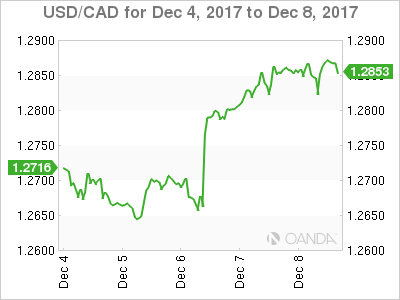

The USD/CAD gained 1.45 percent during the week. The currency pair is trading at 1.2868 after the Bank of Canada (BoC) kept rates unchanged at 1.00 percent and softer oil prices. The central bank did mention a strong job growth and rising inflation signalling that the next move could be a rate hike, but the timing of the monetary policy decision is up in the air. The fate of the NAFTA negotiations is still uncertain and with such a large portion fo the economy tied to the outcome it would be premature for the BoC to speculate on something so outside its control, but very much a factor on its mandate.

The USD kept getting support from tax cut optimism and a strong jobs report ahead of the Federal Open Market Committee (FOMC) on December 13. The BoC is on wait-and-see mode as there are a lot of unknowns that could have a significant impact on the Canadian economy. The market is not pricing in a rise in interest rates until the second quarter. The Fed by comparison is expected to hike 3 times in 2018, with the first lift coming in March as Jerome Powell begins to make his mark on the central bank.

The Canadian economic calendar will be thin as the year winds to an end. Housing data on new dwelling prices will be release on Thursday, December 14 at 8:30 am EST. BOC Governor Stephen Poloz will give a talk titled: "Three Things Keeping Me Awake at Night" in Toronto at 12:25 pm EST.

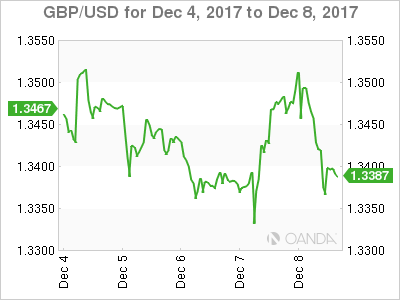

The GBP/USD lost 0.57 percent in the last five days. The currency pair is trading at 1.3395 after Brexit negotiations were unlocked with an agreement on the Irish border. The optimism was short lived as the pound is once again on the back foot given the uncertainty of trade negotiations. The divorce between the UK and the EU is seen as amicable, but real talks could be delayed as the EU is asking for a vision of the future of UK conservatives given the fracture within the party. The EU is hoping to get a less contradictory stand from Britain regarding leaving the Union.

The EU's chief negotiator has been clear that despite the UK concessions the divorce is for real and a trade agreement will be based more on the one currently in place with Canada, that the one enjoyed by the UK but invalid after two years when Brexit becomes final.

The Bank of England (BoE) has shifted monetary policy to deal with the side effects of the Brexit referendum and political instability. High inflation has forced the central bank to hike interest rates, but as more details emerge on Brexit a rate cut is not out of the question. Inflation data will be released on Tuesday, December 12 at 4:30 am EST. The forecast calls for a flat reading at 3.00 percent inflation. Surveys on inflation continue to point to higher prices and a faster pace of UK interest rate rises. BoE Governor Mark Carney has said that gradual increases were likely in the next couple of years.

Market events to watch this week:

Tuesday, December 12

- 4:30 am GBP CPI y/y

- 8:30 am USD PPI m/m

Wednesday, December 13

- 4:30 am GBP Average Earnings Index 3m/y

- 8:30 am USD CPI m/m

- 8:30 am USD Core CPI m/m

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Economic Projections

- 2:00 pm USD FOMC Statement

- 2:00 pm USD Federal Funds Rate

- 2:30 pm USD FOMC Press Conference

- 7:30 pm AUD Employment Change

- 7:30 pm AUD Unemployment Rate

- 9:00 pm CNY Industrial Production y/y

Thursday, December 14

- 3:30 am CHF Libor Rate

- 3:30 am CHF SNB Monetary Policy Assessment

- 4:00 am CHF SNB Press Conference

- 4:30 am GBP Retail Sales m/m

- 7:00 am GBP MPC Official Bank Rate Votes

- 7:00 am GBP Monetary Policy Summary

- 7:00 am GBP Official Bank Rate

- 7:45 am EUR Minimum Bid Rate

- 8:30 am EUR ECB Press Conference

- 8:30 am USD Core Retail Sales m/m

- 8:30 am USD Retail Sales m/m

- 8:30 am USD Unemployment Claims

*All times EDT

Fed to Raise Rates in Busy Week for Central Banks; EU Summit Decides on Brexit

Numerous central banks are scheduled to meet to set monetary policy next week. This includes the Federal Reserve, probably the world's most closely watched central bank. It is also the one expected to make a move in the direction of policy normalization. Beyond this, major economies will see the release of important data, the UK being one of them with releases on inflation, wage growth and retail sales being eagerly awaited. In politics, the US tax story and the EU's official decision on whether Brexit talks can move to the next stage are expected to gather most attention.

Australian labor market data due

In terms of potential market movers for the antipodean currencies: Sunday's (Monday for Asian traders) November electronic card retail sales out of New Zealand would be of interest. Australia will see the release of November employment (and unemployment) data on Thursday. There is much talk of elevated house prices in Australia and thus the third quarter's home price index due earlier in the week (Tuesday) will be attracting attention as well. National Australia Bank's surveys on November business conditions & confidence will also be released on the same day as house price data.

Chinese urban investment, industrial output and retail sales; slew of data out of Japan

Thursday's figures on urban investment, industrial output and retail sales - all for November - are expected to attract most attention out of China. The annual pace of growth for the former two readings is expected to slightly ease, though still reflect relatively robust expansion. Retail sales are expected to expand by 10.2% on an annual basis. This compares to a 10.0% y/y growth in October. The Chinese government seems to increasingly worry about rising debt levels as of late and loan data out of the world's second largest economy next week will also be eyed (these data though lack a specific release date).

In Japan, figures on November corporate goods prices are due on Monday (Greenwich Mean Time). October's machinery orders will follow on Tuesday and December's Nikkei flash manufacturing PMI will be released on Thursday. Later on Thursday, the world's third largest economy will see the release of the Bank of Japan's fourth quarter Tankan surveys on, among others, big and small manufacturers and their respective capital expenditures. Big manufacturers' confidence in business conditions in Japan stood at a decade high in the third quarter. It would be interesting to see if momentum is maintained in the final quarter of the year.

ECB meeting and eurozone PMIs likely market movers; EU decides on Brexit; Bank of England meets in overall data-busy week for the UK

On Tuesday, Germany will see the release of the ZEW institute's December surveys assessing economic sentiment as well as current economic conditions in the country. The following day, final November inflation figures for eurozone's (and Europe's) largest economy are due.

Out of the eurozone, October industrial production figures will be released on Tuesday. The greatest volatility in euro pairs though is likely to come from Thursday's release of December flash PMI estimates for the manufacturing and services sectors as well as the composite measure that blends the two sectors. Expectations are for the readings to ease a bit from November's releases, though still remain robust and well above the 50-mark that separates sectoral growth from contraction (the respective individual country readings for Germany and others will be released earlier on the same day).

The European Central Bank's decision on interest rates due on Thursday is another event having the capacity to generate movements in the euro. ECB chief Mario Draghi will be holding a press conference shortly after the policy announcement. Rates are expected to remain on hold but it would be interesting to see whether Draghi signals hawkish voices within the ECB are getting strengthened. Minutes from the bank's latest meeting showed diverging views among policymakers on whether the asset purchase program that will be in effect starting next year should have been open-ended or not. According to the minutes, some policymakers demanded a clear end date.

In the UK, prior to the Bank of England meeting on Thursday - the central bank is widely expected to keep rates on hold - Tuesday's inflation figures for the month of November will be closely watched. The inflation rate is expected to remain at the more than 5-year high of 3.0% on an annual basis. This compares to the BoE's inflation target of 2.0%. Data on November producer prices will be made public at the same time as inflation numbers. Wednesday will see the release of November's claimant count pertaining to unemployed individuals, as well as October's unemployment rate and average earnings. The unemployment rate is expected to remain steady at the 42-year low of 4.3% for the fourth consecutive month, while it would be interesting to see to what extent the divergence between inflation and wage growth, which eats into households' purchasing power, continues. The final important release before the BoE meeting will be Thursday's retail sales for November.

On the political front, the EU heads of state summit is set to take place on December 14-15. Upon completion of the summit, the 27 remaining - following Britain's departure - EU member states will be making a formal decision on whether Brexit negotiations are allowed to enter the second stage, that of determining the future relationship between the two parties. Sterling, which has proved highly sensitive to Brexit developments, will be in focus.

Fed to hike rates; inflation, retail sales and industrial production also eyed in US

The Federal Reserve's December 12-13 meeting is widely expected to result in a quarter percentage point increase in the Fed Funds rate. The press conference that will follow upon the completion of the two-day meeting will be Janet Yellen's last as Fed chair before she is succeeded by Jerome Powell in February. Thus, one might think that markets won't be paying as much attention to her comments. Given that Powell was dubbed by many as "Mr. Continuity" though, such a perspective would most likely be unwise. The FOMC's dot plot that encapsulates policymakers' expectations for rates further ahead is also spurring the interest of forex market participants. One should not forget though the upcoming changes on the Fed Board, with several members soon departing; the new composition would have the capacity to reshape Fed hike expectations depending on where the new members would stand on the dovish to hawkish spectrum. So far markets have priced in close to two rate hikes for 2018 (the second one is more than fifty percent priced in).

Of most interest in terms of US data are likely to be Wednesday's inflation figures, Thursday's retail sales and Friday's release on industrial production, all for the month of November. On a monthly basis, inflation is expected to grow by 0.4%; October's reading was at 0.1%. Month-on-month, retail sales are projected to have grown by 0.3%, above October's 0.2%. November's industrial production is forecast to have expanded by 0.4%, at a slower pace relative to October's 0.9%. Beyond these, another key release out of the world's largest economy will be October JOLTS job openings (Monday).

On the US political front, lawmakers' efforts on tax reform will be at the center of attention. Senate Republicans agreed this week to engage in discussions with the House of Representatives in an attempt to reconcile the two versions of the tax bill they voted in favor of, with a December 22 self-imposed deadline being in place.

Remaining within North America, it will be a quiet week for Canada, with Friday's manufacturing sales potentially causing some volatility in dollar/loonie as well as in other loonie pairs.

Finally, it should also be mentioned that the Swiss National Bank and Norges Bank will also be completing their meetings on monetary policy next week (December 14).

November Jobs Solid, Good Sign for Incomes and Growth

November jobs were up 228,000 and up 170,000 on average over the last three months. Gains were broad based in service, manufacturing and construction sectors while wage growth remained modest.

November Jobs at 228,000: Solid Sign for Income and Growth

Nonfarm payrolls rose 228,000 in November, with the three-month average at 170,000 jobs. Job gains are consistent with 2.5-3.0 percent economic growth in the first half of 2018, with steady consumer spending, better business investment and a likely FOMC December rate hike with another one in Q1-2018. The diffusion index indicates that 63 percent of industries added jobs in November compared to 52 percent a year ago.

Jobs gains appeared in many sectors including business services, trade & transport as well as education & health (top graph). Federal and state & local government jobs have declined over the past three months.

Over the past three months, aggregate hours worked are up 1.6 percent, consistent with continued growth in personal income, personal consumption and overall GDP growth.

Wage Growth: Real Wage Gains Over the Past Two Years?

Nominal average hourly earnings rose 0.2 percent in November, which was short of expectations. However, the average length of the workweek edged up to 34.5 hours. Along with the net jobs added, this suggests income derived from the labor market has strengthened at a 4.7 percent annualized rate the past three months (middle graph).

The gradual rise in earnings over the past three months (2.5 percent year over year) signals higher incomes but also pressure on profits for firms that have modest top-line pricing power (especially in the goods sector). We expect wage growth to pick up a bit faster next year given unemployment headed towards sub-four percent.

Longer term, the modest inflation readings and weak productivity numbers have limited the gains in nominal wage growth. Lackluster productivity growth in the current cycle has weighed on wage growth and will likely continue to hamper wage appreciation, even with low unemployment.

Structural Problems Persist: Drag on Growth

For any given unemployment rate (labor supply), the vacancy rate (job openings) remains wider than in the previous expansion (bottom graph), however the slack is gradually tightening. This Beveridge Curve signals a structural weakness in the labor market which is confirmed by several labor market survey indicators. Compared to a year ago, the unemployment rate for those without a high school education and with a high school diploma remains higher than the unemployment rate for those with some college.

The mean duration of unemployment came in at 25.4 weeks in November, close to the average over the past year, while the labor force participation rate has remained nearly unchanged compared to a year ago.

Solid US Job Growth Confirms Fed Should Raise Rates Next Week

Highlights:

- Payroll employment rose 228k in November, one of the strongest gains this year. Impressive job growth over the last two months partly reflects continued recovery from the hurricane-related slowing in September.

- The unemployment rate held steady at a cycle low of 4.1%.

- A broader measure of unemployment that includes marginally attached workers and those employed part time for economic reasons edged up to 8.0% but is still down more than a percentage point from a year ago.

- Wage growth ticked up to 2.5% in November from a two-year low of 2.3% in October.

Our Take:

Not that they really needed it, but today's payroll report gives the Fed a green light to raise rates next Wednesday. With hurricane-related volatility largely behind us, economic conditions are clearly strong enough for businesses to continue hiring at an impressive pace for this point in the cycle. Unemployment was steady in November, but if job growth continues at the 170k rate seen over the last three months, the jobless rate should drift even further below what the Fed sees as sustainable in the longer run.

With a move at December's meeting widely expected, attention will be focused on how the central bank sees monetary policy evolving in 2018. Key to that debate will be wage and inflation dynamics. The Fed can only raise rates so much in anticipation of increasing price pressures—we'll need to see wage growth and inflation actually picking up for the committee to hike more than once or twice next year. In that respect, today's report wasn't exactly stellar. Wage growth ticked higher but remained at the lower end of the range seen over the last two years. An upward trend will need to continue for policymakers to become confident that rising labour costs are putting a floor under inflation. For our part, we expect a 4% unemployment rate, combined with what is clearly strong hiring demand, will boost wage growth next year, helping inflation return to 2% on a sustained basis. If upcoming payroll and inflation reports provide evidence of that dynamic, we think the Fed will raise rates once a quarter in 2018.

Canadian Housing Starts Unexpectedly Jumped in November

Highlights:

- Housing starts jumped to 252k annualized units in November from 223k in October. November's reading matches the strongest monthly pace in five years.

- Even looking through monthly volatility, the six month trend in housing starts hit a cycle high of 226k.

- The increase in November reflected a jump in multi-unit construction to a record high. Single unit starts also increased but only partially retraced last month's decline.

- A sharp increase in multi-unit construction in Ontario accounted for much of November's gain. The increase was broadly-based across the province, not just in Toronto.

Our Take:

Housing starts were well ahead of expectations in November, rising above the 250k mark for just the third time this cycle. That pace won't be sustained - with permits running at 222k over the last six months, starts should come back down to earth in the months ahead. But clearly the trend is quite strong. Homes are being built at the fastest pace in a decade despite resales cooling off at the national level following a brisk first quarter. There is some evidence of that slowdown influencing homebuilding activity - single unit starts in Ontario, where the dip in resales has been most significant, have trended lower in recent months. But builders continue to respond to demand for multi-unit housing in the province, a fact that was clearly evident in today's report. Elsewhere in the country, starts are picking up alongside resales in Quebec and BC, also largely in the multi-unit segment. And new construction in the Prairies continues to increase, albeit from a low base, as Alberta and Saskatchewan's economies recover. With these dynamics swamping a modest slowdown in Ontario's single unit segment, starts will likely continue to run above their longer-run demographic trend. We still think moderation in home sales next year, amid tightening mortgage regulations and rising interest rates, will translate into slower homebuilding activity. But given resilience in the sector this year, we have revised up our 2018 starts forecast to 195k from 185k previously.

Poor Wage Growth Caps Further USD Gains

- European equity markets gain between 0.5% and 1%. Gains mainly occurred in the European opening, welcoming political decisions in the US and the EU/UK. US stock markets opened open with gains of about 0.3/0.4% (Dow & S&P). The Nasdaq again outperforms (+0.75 %).

- US payrolls beat forecasts in November as net job growth increased by 228k vs 195k expectations. The previous two months' numbers were upwardly revised by 3k. The US unemployment rate stabilized at 4.1%, the lowest level since 2000. Average hourly earnings (0.2% M/M and 2.5% Y/Y) increased from October, but remained below consensus.

- German exports fell unexpectedly in October (-0.4% M/M) while vibrant domestic demand pushed up imports (+1.8% M/M), narrowing the trade surplus and adding to evidence that Europe's biggest economy started the fourth quarter on a weak footing.

- UK manufacturers extended their winning streak in October as foreign demand sent car production to a record. Factory output rose 0.1% from September, marking six consecutive increases for the first time since modern records began in 1997. Overall industrial production was unchanged as warmer weather reduced demand for energy.

- Italy's anti-establishment 5-Star Movement supports the EU and wants significant law-making powers transferred from governments to the European Parliament, its leader Luigi Di Maio told Reuters. 5-Star, which leads opinion polls ahead of an election to be held by May, is trying to reassure Italy's partners and financial markets that it can be trusted in government, and distance itself from its previously eurosceptic positions.

Rates

U-turn on disappointing wage inflation

Global core bonds trading showed two faces. They traded with a downward bias going into the US payrolls report on the back of positive risk sentiment. The US government averted an imminent shutdown, but the deal only postpones the problem by two weeks (Dec 22 new deadline). US President Trumps was rumoured to be readying phase two in its fiscal stimulus plan, infrastructure spending, by January. PM May and EC Juncker sounded confident on the completion of part 1 of Brexit-talks even if the agreement lacked details. Nevertheless, political developments weighed on core bonds. Trading made a U-turn after the payrolls report. Net job creation remained strong and the unemployment rate is still at the lowest level since 2000. However, earnings disappointed. The market reaction proves sensitivity to price/inflation data. The US Note future gradually gained momentum and trades currently around the intraday highs. The scale of the move remains limited though with next week's Fed meeting looming. Investors don't want to be wrongfooted by a Fed who still intends to hike rates three times next year.

At the time of writing, the German yields curve shifts 0.6 bps to 0.9 bps higher. The German 10-yr yield remains dangerously close to the 0.3% support level. The US yield curve steepens with yield changes ranging between -1.4 bps (2-yr) and +0.7 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany are unchanged with the periphery outperforming (-3 bps to -5 bps) and a stellar performance from Greece (-33 bps). Greek bonds continue to profit from last week's debt swap.

Currencies

Poor wage growth caps further USD gains

A positive risk sentiment kept the dollar near recent highs against the euro and the yen this morning as markets counted down to the US payrolls. US job growth remained strong, but wage growth again missed expectations. With markets currently giving more weight to prices rather than activity data, the dollar even declined off the intraday peak after the payrolls. EUR/USD trades in the 1.1760 area. USD/JPY is changing hands around 113.30.

Asian equities extended yesterday's comeback overnight with Japan taking the lead. Regional data (Japan Q3 GDP and Chinese trade data) were supportive for equities and so was the prospect of a EU/UK Brexit agreement and the US Congress avoiding a government shutdown. The overall positive sentiment via higher core yields supported the dollar. USD/JPY extended gains north of 113. EUR/USD drifted to the mid 1.17 area.

There were plenty of headlines on Brexit and US politics (Agreement to extend government funding till 22 Dec; Trump proposals on infrastructure investment) this morning. The reaction of global markets was quite similar to what often happened late. European equities succeeded quite an impressive risk rebound, but with little spill-overs to other markets, including interest rate and FX markets. The dollar held near the recent highs against the yen and the euro, but the rally ran into resistance, awaiting the US payrolls.

The payrolls brought again a diffuse picture. Job growth (228k) beat consensus by a substantial margin. The jobless rate remained at the lowest level since 2000, but wage growth disappointed 0.2% M/M and 2.5% Y/Y; 0.3% M/M and 2.7% Y/Y was expected). As markets are quite sensitive to price data these days, US yields and the dollar even declined slightly. USD/JPY trades in the 113.30 area. EUR/USD rebounds to the 1.1765 area, off the intraday low around 1.1730. The dollar showed quite constructive price action this week, but this mixed payrolls report probably hampers further US gains ahead of Wednesday's Fed policy decision.

Sterling rally stalls despite first 'Brexit agreement'

Sterling rallied yesterday evening and this morning on headlines that the EU and the UK agreed to move to the second stage of the Brexit negotiations. The agreement was officially announced at a press conference with EU commission head Juncker and UK PM early this morning. Sterling touched a ST top during (cable) or soon after (GBP/EUR) the press conference. Cable filled offers in the 1.3520 area. EUR/GBP almost exactly tested the 0.8593 62% retracement support. The negotiations proceeding to a next stage for sure is good news for the UK. However, markets soon realized that the hard work still has to be done, even on the details of the separation. The sterling rally ran into resistance and the UK currency gradually returned some of the overnight gain, especially against the dollar. UK production data were as expected. The trade deficit was smaller than expected. However, the data were not the focus of markets. EUR/GBP trades currently in the 0.8750/60 area. Cable dropped to the 1.34 area, but regained a few ticks on USD softness after the payrolls (currently 1.3425).

Weekly Focus: Central Bank Meetings for Christmas

Market movers ahead

- We have a very busy central bank week ahead, with Fed, ECB, BoE and Norges Bank meetings coming up. We expect only the Fed to change its policy rate, hiking the target range to 1.25-1.50%.

- We are due to get inflation data from the US, UK, Japan, Denmark, Sweden and Norway.

- We expect EU leaders to say that the UK and EU can start discussing the future relationship at next week's EU summit.

- Focus remains on US tax reform and whether the Republicans are able to pass it already before Christmas.

Global macro and market themes

- We expect the global expansion to continue lending support to profits and risk assets.

- We do not project a bond bear market though. Rather we look for more US curve flattening.

- Credit spreads are set to narrow further on a search for yield and low default rates.

- In the FX space, we look for a weaker USD and a stronger GBP and NOK in 2018.