Sample Category Title

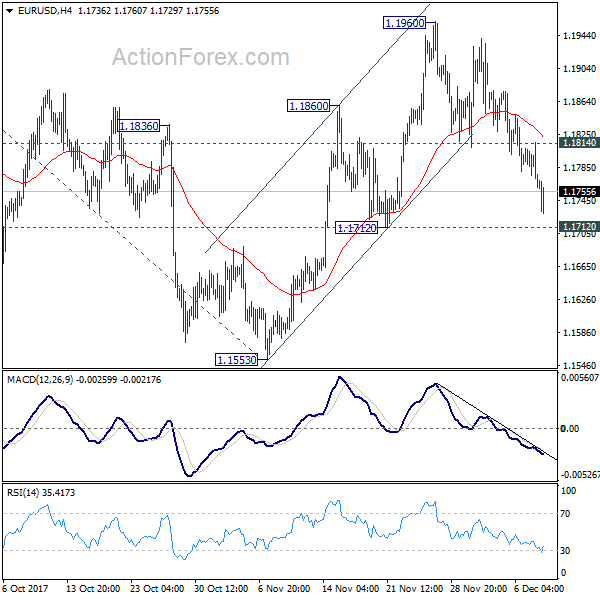

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1757; (P) 1.1786 (R1) 1.1800; More....

EUR/USD drops to as low as 1.1729 so far today and focus in now on 1.1712 near term support. Decisive break there will indicate that rebound from 1.1553 has completed at 1.1960. In that case, deeper fall would be seen to retest 1.1553 low. Meanwhile, with 1.1712 support intact, break of 1.1814 will retain near term bullishness. And in that case, intraday bias will be turned back to the upside for 1.1960. Break will target 1.2091 high.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Dollar Pares Gain as Wage Growth Missed, Sterling Weakens as Brexit Breakthrough Becomes Fact

Initial reactions show markets are not too happy with US non-farm payroll report. While headline job growth beat expectation, it was partly offset by downward revision in prior month's figure. More importantly, wage growth came in weaker than expected. It's seen as a crucial factor for inflationary pressure, or the lack thereof. While the greenback retreats mildly as knee jerk reaction, there is no sign of a reversal. Instead, the greenback stays very strong against Euro and Swiss Franc. 1.1712 in EUR/USD is now at risk and break will probably trigger broad based acceleration in Dollar. Meanwhile, Sterling reversed earlier gains as Brexit negotiation breakthrough finally becomes a fact today.

Non-farm payroll report showed 228k growth in jobs in November, above expectation of 200k. Prior month's figure was revised down to 244k, from 261k. Unemployment rate was unchanged at 4.1% as expected. However, average hourly earnings rose 0.2% mom only, below expectation of 0.3% mom.

Also release in US session, Canada housing starts rose to 252.2k in November. Capacity utilization rate was unchanged at 85% in Q3.

Brexit: Sufficient progress finally made to move on to trade talks

Brexit negotiations between UK and EU have finally made the break through o move on to trade agreements. European Commission President Jean-Claude Juncker declared after meeting UK Prime Minister Theresa May that "sufficient progress has now been made on the three terms of the divorce." May said that "getting to this point required give and take on both sides." A joint report was published detailing the agreements. In short:

- Divorce bill: UK agreed to contribute to EU budget up the end of 2020 "as if it had remained in the union". And UK will be liable for its commitments and liabilities up to December 3, 2020. No hard figure was given but according to the framework, the net payment should be around GBP 40b.

- EU citizen rights in UK: EU citizens in UK will continue to have the rights to live, work and study after Brexit. UK court will enforce the rights in concession to EU. And, the European Court of Justice will continue to have a role in overseeing the rights for eight years. On the other hand, guarantees will also apply to UK citizens living in EU.

- Irish border: The report noted that "in the absence of agreed solutions, as set out in the previous paragraph, the United Kingdom will ensure that no new regulatory barriers develop between Northern Ireland and the rest of the United Kingdom, unless, consistent with the 1998 Agreement, the Northern Ireland Executive and Assembly agree that distinct arrangements are appropriate for Northern Ireland." But both EU and UK will "establish mechanisms to ensure the implementation and oversight of any specific arrangement to safeguard the integrity of the EU Internal Market and the Customs Union."

Released from UK, industrial production rose 0.0% mom, 3.6% yoy in October. Manufacturing production rose 0.1% mom, 3.9% yoy. Construction output dropped -1.7% mom. Visible trade deficit narrowed to GBP -10.8b in October. NIESR GDP estimate rose 0.5% in November. From Eurozone, German trade surplus narrowed to EUR 19.9b in October.

Japan GDP grew 0.6% qoq in Q3, doubled initial estimate

Japan GDP growth was finalized at 0.6% qoq in Q3, double the pace of initial estimate of 0.3% qoq. Annualized rate was 2.5%. GDP deflator was finalized at 0.1% yoy, unchanged. The data showed that Abenomics and BoJ's easing have definite boosted growth, but is so far having little impact on lifting inflation. Also from Japan current account surplus widened to JPY 2.44T in October. Labor cash earnings rose 0.6% yoy, below expectation of 0.8% yoy.

China trade surplus widened to USD 40.2b in November, up from USD 38.2b and above expectation of USD 34.9b.Exports rose 12.3% yoy while imports also surged 18% yoy. In Yuan, trade surplus widened to CNY 264b, up fro CNY 254b and beat expectation of CNY 238b. Also from Asia Pacific, Australia home loans dropped -0.6% mom in October. New Zealand manufacturing activity rose 0.5% in Q3.

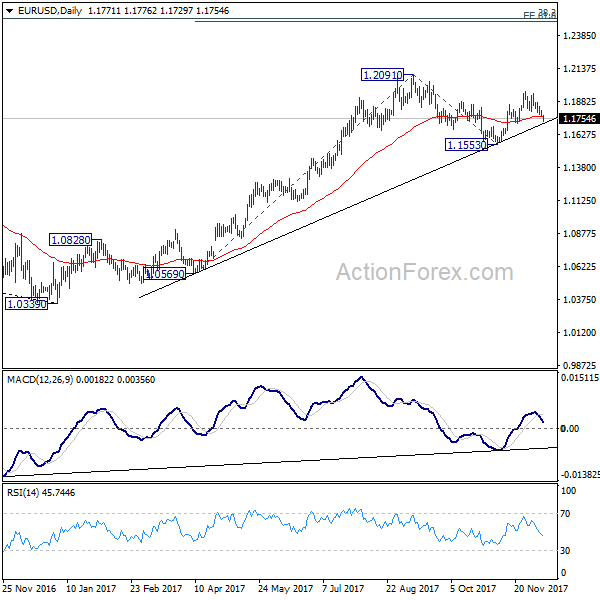

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1757; (P) 1.1786 (R1) 1.1800; More....

EUR/USD drops to as low as 1.1729 so far today and focus in now on 1.1712 near term support. Decisive break there will indicate that rebound from 1.1553 has completed at 1.1960. In that case, deeper fall would be seen to retest 1.1553 low. Meanwhile, with 1.1712 support intact, break of 1.1814 will retain near term bullishness. And in that case, intraday bias will be turned back to the upside for 1.1960. Break will target 1.2091 high.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity Q3 | 0.50% | 3.90% | 3.40% | |

| 23:50 | JPY | Current Account (JPY) Oct | 2.44T | 1.93T | 1.84T | |

| 23:50 | JPY | GDP Q/Q Q3 F | 0.60% | 0.40% | 0.30% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | 0.10% | 0.10% | 0.10% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y Oct | 0.60% | 0.80% | 0.90% | |

| 00:30 | AUD | Home Loans M/M Oct | -0.60% | -2.00% | -2.30% | -2.50% |

| 03:13 | CNY | Trade Balance (CNY) Nov | 264B | 238B | 254B | |

| 03:36 | CNY | Trade Balance (USD) Nov | 40.2B | 34.9B | 38.2B | |

| 07:00 | EUR | German Trade Balance (EUR) Oct | 19.9B | 22.3B | 21.8B | 21.9B |

| 09:30 | GBP | Industrial Production M/M Oct | 0.00% | 0.00% | 0.70% | |

| 09:30 | GBP | Industrial Production Y/Y Oct | 3.60% | 3.50% | 2.50% | |

| 09:30 | GBP | Manufacturing Production M/M Oct | 0.10% | 0.00% | 0.70% | |

| 09:30 | GBP | Manufacturing Production Y/Y Oct | 3.90% | 3.80% | 2.70% | |

| 09:30 | GBP | Construction Output M/M Oct | -1.70% | 0.10% | -1.60% | |

| 09:30 | GBP | Visible Trade Balance (GBP) Oct | -10.8B | -11.5B | -11.3B | |

| 12:06 | GBP | NIESR GDP Estimate Nov | 0.50% | 0.40% | 0.50% | |

| 13:15 | CAD | Housing Starts Nov | 252.2K | 221K | 223K | 222.7K |

| 13:30 | CAD | Capacity Utilization Rate Q3 | 85.00% | 85.20% | 85.00% | |

| 13:30 | USD | Change in Non-farm Payrolls Nov | 228K | 200K | 261K | 244K |

| 13:30 | USD | Unemployment Rate Nov | 4.10% | 4.10% | 4.10% | |

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.20% | 0.30% | 0.00% | |

| 15:00 | USD | U. of Mich. Sentiment (Dec P) | 99 | 98.5 |

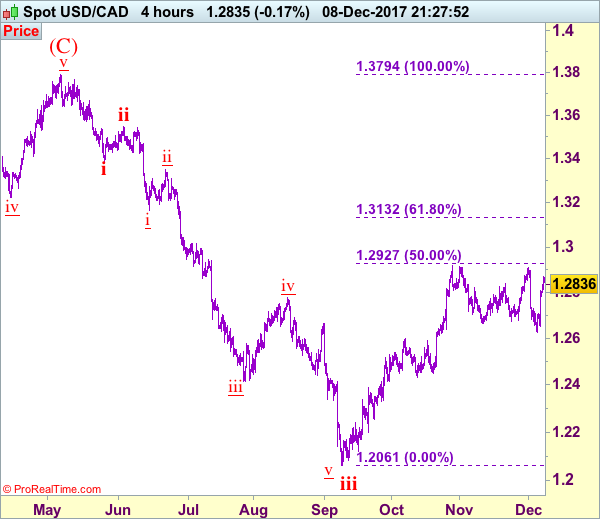

Trade Idea: USD/CAD – Stand aside

USD/CAD - 1.2833

Trend: Near term up

Original strategy :

Sold at 1.2800, stopped at 1.2860

Position: - Short at 1.2800

Target: -

Stop: - 1.2860

New strategy :

Stand aside

Position: -

Target: -

Stop:-

The greenback found decent demand at 1.2623 and staged a much stronger-than-expected rebound, dampening our bearishness and suggesting low has been formed there at 1.2623, hence upside risk remains for gain to 1.2875-80 but break of resistance at 1.2917 is needed to confirm upmove has resumed for headway to 1.2975-80 (61.8% Fibonacci retracement of 1.3547-1.2061), then towards psychological resistance at 1.3000.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 1.2760-65 would prolong choppy trading and bring weakness to 1.2700-05, however, downside should be limited to 1.2650-55 and price should stay above said support at 1.2623, bring another rebound later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Dollar Strengthens ahead of NFP Report; Stocks Up

Here are the latest developments in global markets:

FOREX: The dollar gained further momentum, crawling towards a fresh three-week high of 113.58 (+0.36%) versus the yen during early European trading hours as investors remained confident after a potential government shutdown in the US was averted on Thursday. The dollar index broke above the 94 key level (+0.25%). The pound stalled around 1.3463 (-0.19%) after reaching a four-day high of 1.3512 against the greenback, while it consolidated near six-month highs versus the euro (+0.10%). Although the EU announced that "sufficient progress" has been made on Brexit talks, the President of the European Council, Donald Tusk, signaled that building future relations would be even harder. Euro/dollar weakened to 1.1735 (-0.30%).

STOCKS: European stocks continued to rally on Friday following their Asian counterparts with bank stocks leading the indices as the Basel Committee on Banking Supervision set new rules to measure asset risks which could reduce capital requirements. The pan-European STOXX 600 was 0.86% up at 1100GMT, the German DAX 30 surged by 1.37% and the Spanish IBEX 35 climbed by 0.92%. The British FTSE 100 moved up by 0.26% as Brexit fears eased – yesterday's rise in sterling acted as a drag on the exporter-heavy benchmark.

COMMODITIES: Oil prices moved up after data showed on Friday that Chinese crude imports stood at record highs in November, raising prospects for improving demand. WTI crude rose by 1.25% to $57.40 per barrel and Brent increased by 1.17% to $62.93. Gold remained flat at $1,246 per ounce.

Day ahead: Nonfarm payrolls in focus but wage growth takes the stage

Next on Friday, US Nonfarm payrolls will be closely watched, with analysts predicting 200,000 new entrants joining the labour force in November compared to the 261,000 seen in October. The report is due at 1330GMT and will also include readings on the unemployment rate and average hourly earnings which would be in focus as Fed policymakers look for clues to justifying further policy normalization moving ahead. Particularly, the Fed thinks that a tighter labour market reflected by the unemployment rate which currently stands at the lowest level since 2000 will lead to higher wage growth and therefore lift inflation to the Fed's target of 2.0%. Forecasts are for the jobless rate to remain flat at 4.1% in November and for average hourly earnings to rise by 0.3% after remaining unchanged in the previous month.

In other data releases, the Canada Mortgage and Housing Corporation will deliver figures on housing starts for the month of November at 1315GMT. The number of new constructions is anticipated to slow down by 1,800 to 221,000.

Traders will also be eager to hear any updates on Brexit developments after the EU and the UK managed to unlock negotiations on early Friday by reaching a preliminary agreement on three key divorce issues involving the Irish border, the rights of EU citizens and the UK's financial obligations to the block. However, the agreed outline must be formally approved by the EU leaders at next week's summit starting on December 14 for talks to move officially to transitional period and future trade relations.

Attention Shifts to US Jobs After Brexit Deal

- Jobs Data Unlikely to Impact December Rate Hike;

- Sterling Slides After Brexit Phase One Agreement;

- Bitcoin Slides on Profit Taking Ahead of CBOE Futures Launch.

Jobs Data Unlikely to Impact December Rate Hike

It's been a lively start to trading on Friday and with the US jobs report still to come, it should be a very interesting end to the week.

The jobs report is widely regarded as the most important economic report each month but with tax reform and Brexit stealing the spotlight, not to mention Bitcoin, it's been a little overshadowed so far this week. There's perhaps also been a little less hype about it this month because a rate hike next week is already baked in and today's numbers are unlikely to change anything on that front.

When it comes to next year, the Federal Reserve is currently anticipating another three rate hikes but with there still being so many unknowns – tax reform, open Fed positions etc – that could easily change. While the unemployment and NFP numbers tend to write the headlines, wage growth is arguably the most important piece of data we'll get from the report. This has been lacking from the economic recovery in the US, despite unemployment falling to 4.1% and the absence of it has cast strong doubt over whether inflation will in fact move back towards its 2% target.

Sterling Slides After Brexit Phase One Agreement

After months of tough negotiations, the UK and EU this morning agreed to move on to phase two of Brexit talks which involves discussing trade and the transition period, pending approval from the European Council. Jean-Claude Juncker this morning confirmed that the European Commission will recommend to the EC that talks move on having come to an agreement on the financial settlement, citizens right and the Irish border, the last of which proved the most difficult to agree on despite months of back and forth over money.

Despite an agreement being reached, the response to it was negative in the pound which came off its highs and remains lower on the day against the dollar. I think we've seen a classic case of the rumour being bought and the fact sold, with sterling having rallied early last week in anticipation of a deal being close then again on Thursday. We could see more upside in the pound in the coming months but as it was before, the road ahead is bumpy and that will be reflected in the currency markets. The pound will remain vulnerable to any suggestion that a deal may not be reached in time, as observed this morning when it tumbled in response to the suggestion by an EU official that a trade deal by March 2019 is unrealistic.

Bitcoin Slides on Profit Taking Ahead of CBOE Futures Launch

After two days in which we've seen a mammoth 42% gain in Bitcoin, depending on the exchange, the cryptocurrency is trading around 10% lower this morning having recovered slightly from a near 20% drop earlier in the day. This is just another reminder of how volatile the cryptocurrency space is and while the ride higher can be exciting, it's not a one way street and the price can plunge just as rapidly.

I think what we may be seeing here is some profit taking ahead of the CBOE Bitcoin futures launch on Sunday, which some have suggested may open the door to short speculators who believe the price has risen far too quickly. It will certainly be interesting to see how the market responds to the launch of the contract, especially ahead of the CME launch on 18th December. The initial bounce after this morning's sell-off suggests there's still appetite for buying dips but that may not last if we don't see the kind of rebound witnessed previously. Saying that, the way Bitcoin is trading at the minute, I don't think anyone would be surprised to see it end the day in the green.

USDJPY Strongly Bullish Above 113.10 Level

The U.S dollar has moved to a 4-week trading high against the Japanese yen, hitting 113.60, as traders pile into greenbacks. Buying in the USDJPY pair accelerated, after price-action broke above the 113.10 level, signaling a clear upside technical breakout. Going forward, the next technical hurdle ahead for the pair is the 114 handle, where supply and demand will be strongly tested. Headed into the U.S session, traders now await the Non-farm payrolls jobs report, where the U.S unemployment rate, wage growth, and headline jobs figure will be under scrutiny.

Should price action trade above the 113.60 level, further upside towards the 114 level appears likely, extended resistance is found at the 114.40 level.

If the USDJPY pair moves back below the 113.10 technical level, sellers may test toward the 112.70 and 112.40 support levels.

EURUSD Further Breaish Below 1.1750 Level

The slide lower in the euro currency has spilled over into the European trading session, with the EURUSD hitting a new monthly price-low, at 1.1732. The U.S dollar index has moved above the key 94 mark, with the greenback gaining strongly against a basket of top-tier currencies. The single currency has also been hit hard by cross-pair outflows, with EURGBP pair moving lower towards the 0.8700 level, as the British pound strengthens. Traders now await the U.S Non-farm payrolls jobs report, with the U.S unemployment rate expected in at 4.1 percent and headline jobs figure at 200,000.

The EURUSD pair is strongly bearish while trading below the 1.1750 level, further downside towards the 1.1713 and 1.1665 levels seems possible on a positive jobs number.

Should EURUSD price-action move above the 1.1750 level, buyers may look to target towards the 1.1780 and 1.1815 resistance levels.

DAX Soars to 4-Week High on Brexit Progress

The DAX index has posted sharp gains in the Friday session, and is poised to record a third straight winning week. Currently, the DAX is at 13,201.00, up 1.26% on the day and at its highest level since November 9. Financial stocks have surged, as Commerzbank and Deutsche Bank have climbed 2.87% and 3.07%, respectively.

In economic news, Germany's trade surplus fell to EUR 19.9 billion, missing the estimate of EUR 22.0 billion. This marked a 3-month low. In the US, the focus is on employment numbers, led by Nonfarm payrolls. The indicator is expected to come in at 198 thousand, compared to the previous reading of 261 thousand.

Are the Brexit talks, which have been mired in the mud for months, on track at long last? Apparently yes, after EU Commissioner Jean-Claude Juncker announced on Friday that sufficient progress had been made on non-trade issues. If the EU accepts this recommendation, the sides will then move to trade talks. What has held up the talks until now? The two non-trade sticking points have been the status of the Irish border and the role of the European Court of Justice after Brexit. Ireland wants some arrangement whereby EU regulations also apply to Northern Ireland, but the small DUP party, which is keeping the May government afloat, is against any steps which could be seen as separating Northern Ireland from the UK mainland. A solution that will satisfy the UK, the EU and the DUP over the Irish border has still not been reached. Another thorny issue is whether the European Court of Justice will apply to European citizens in the UK after Brexit. While the EU is in favor of the court having authority over these citizens, many British lawmakers feel that such a move would undermines British sovereignty. After months of difficult talks, moving on to trade issues would be a major breakthrough, especially for embattled Prime Minister May, who has been heavily criticized for her handling of the Brexit negotiations.

Bitcoin Bonanza

We are fast approaching the make-or-break moment for Bitcoin. Prices gyrated wildly Thursday with some exchanges nearing $20,000 but systems clearly came under a strain. In FX, sterling gathers upward momentum on news that DUP intends to strike a deal with PM May and on firm services PMI and the Australian dollar quietly fell to a six-month low. The US jobs report is up next. 2 new trade actions in the Premium Insights were issued on EURUSD.

It's impossible to avoid talking about Bitcoin at the moment, which is now surely the defining mania of our era. What's not clear is how and when it will end but aside from the violent price swings, the warnings signs are mounting. The first is the increasingly slow and expensive transaction costs. It's clear that Bitcoin will never replace fiat currency – long one of the tenants of the bull theory. It currently costs $13 to do any transaction and takes upwards of 7 hours to verify a transaction at that price.

One thing everyone will be hearing more about in the days ahead are the mempool. This is the backlog of transactions and it's growing at a fast rate. If there is ever a stampede to the exits, this problem will be a devastating bottleneck. At the same time, the exchanges are under increasing strain. Outages hit the main trading hubs again on Thursday. That's a major red flag.

Bitcoin has proven significant resilience to bad news. The dip after hitting $10,000 was bought and reports of hacks, theft and fraud are brushed aside. That's a sign of a roaring market.

The catalyst that everyone is watching is the introduction of futures trading this week at CBOE and next week at the CME. Both are cash-settled contracts so they shouldn't affect the underlying market, especially since short-term arbitrage is nearly impossible because of the transaction times.We will be watching closely.

Elsewhere, the US dollar founds its legs on Thursday as USD/JPY rose to a three-week high and AUD/USD fell to a six-month low. Non-farm payrolls is due on Friday and indications from the ADP report was another strong jobs print but the focus will remain on wages. If they tick up, then the dollar could start to recover much of the July/Aug declines.

Euro Falls To 2-Week Low, US Nonfarm Payrolls Ahead

The euro continues to lose ground this week. In the Friday session, EUR/USD is trading at 1.1735, down 0.32% on the day. In economic news, Germany's trade surplus fell to EUR 19.9 billion, missing the estimate of EUR 22.0 billion. This marked a 3-month low. There was better news out of France, as Industrial Production surged 1.9%, crushing the estimate of -0.1%. This marked the strongest manufacturing output reading since May. In the US, the focus is on employment numbers. Nonfarm payrolls is expected to soften to 198 thousand, while wage growth is forecast to rebound with a gain of 0.3%. The unemployment rate, which stands at a sizzling 4.1%, is expected to remain unchanged.

November's ADP nonfarm payrolls managed to beat expectations earlier this week, but the reading was sharply lower than the October release. Will the official nonfarm payrolls follow suit? The markets are bracing for a soft NFP, with a forecast of 200 thousand, down from 261 thousand in the previous release. Wage growth has been stubbornly low, despite a strong labor market and assurances from Fed policymakers that inflation and wages will move upwards. The markets are expecting some good news on Friday, with Average Hourly Earnings expected to gain 0.3%. The October reading of 0.0% was a disappointment, missing the forecast of 0.2%. Traders should be prepared for some movement from EUR/USD during the North American session.

Ireland is in the spotlight on both sides of the Channel, as the UK and European Union scramble to find a solution to the vexing question of the status of the Irish border after Brexit. An embattled Prime Minister May is desperate to move on to trade talks with the EU, but the Europeans want to wrap up the non-trade issues first. There had been hopes of a major announcement following a meeting between Prime Minister May and European Commission President Jean-Claude Juckner. However, these expectations were left on hold, as it became apparent that wide gaps remain on two key issues – Northern Ireland and the European Court of Justice. The European Union is willing to let EU rules apply to Northern Ireland, but the small DUP party, which is keeping the May government afloat, is against any steps which could be seen as separating the UK mainland from Northern Ireland. A solution that will satisfy the UK, the EU and the DUP over the Irish border remains elusive. Another thorny issue is whether the European Court of Justice will apply to European citizens in the UK after Brexit. While the EU is in favor of the court having authority over these citizens, many British lawmakers feel that such a move would undermines British sovereignty. The EU holds a key summit on December 12, and all sides are hoping to wrap up the non-trade sticking points before the meeting.