Sample Category Title

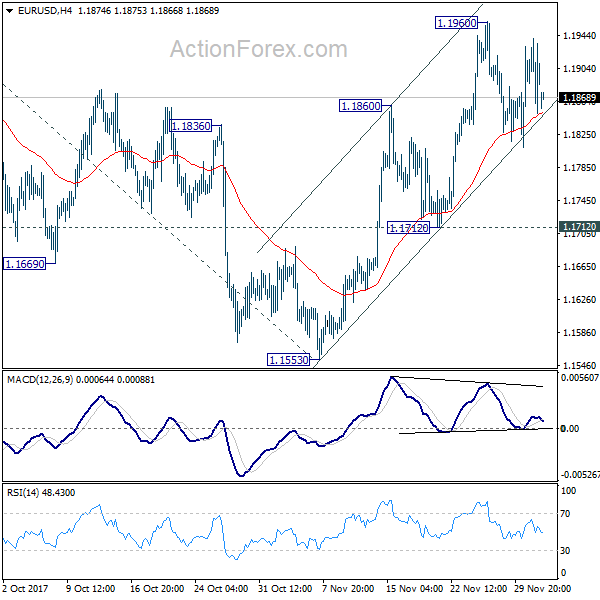

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1851; (P) 1.1896 (R1) 1.1941; More....

Intraday bias in EUR/USD remains neutral for consolidation below 1.1960. With 1.1712 support intact, rise from 1.1553 is expected to resume later. Break of 1.1960 will turn bias to the upside for retesting 1.2091 high first. Break there will resume medium term up trend from 1.0339 and target 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494, which is close to 1.2516 long term fibonacci level. We'd expect strong resistance from there to bring reversal. On the downside, break of 1.1712 will indicate completion of the rise from 1.1553 and turn near term outlook bearish.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

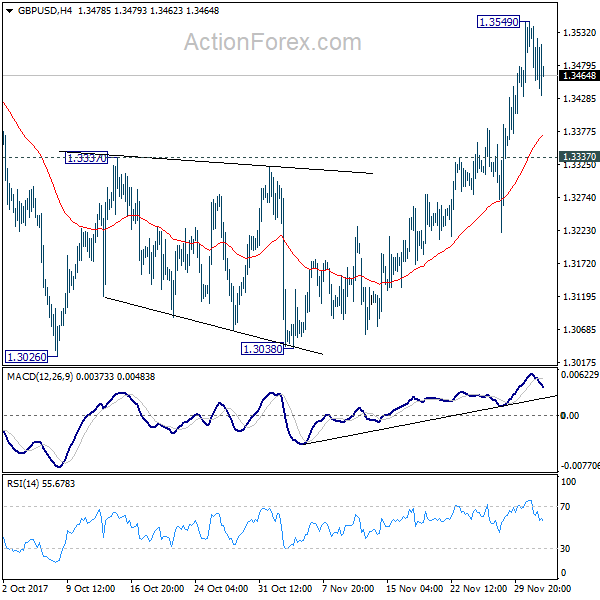

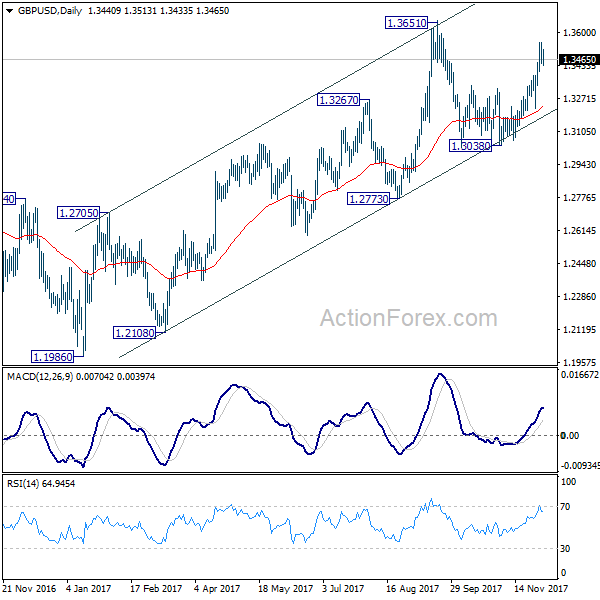

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3423; (P) 1.3486; (R1) 1.3529; More....

Intraday bias is GBP/USD remains neutral for consolidation below 1.3549 temporary top. Downside of retreat should be contained by 1.3337 resistance turned support to bring another rise. Above 1.3549 will target 1.3651 and above. However, decisive break of 1.3337 will argue that rise from 1.3038 has completed and turn bias back to the downside for this support.

In the bigger picture, while the medium term rebound from 1.1946 low is strong, it's still limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

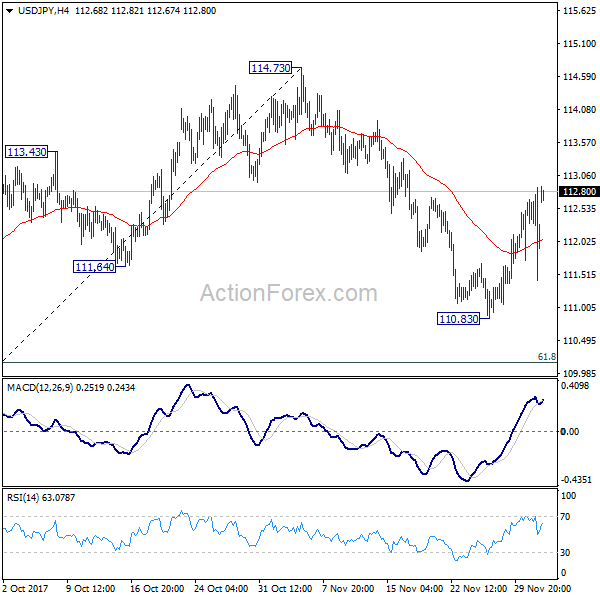

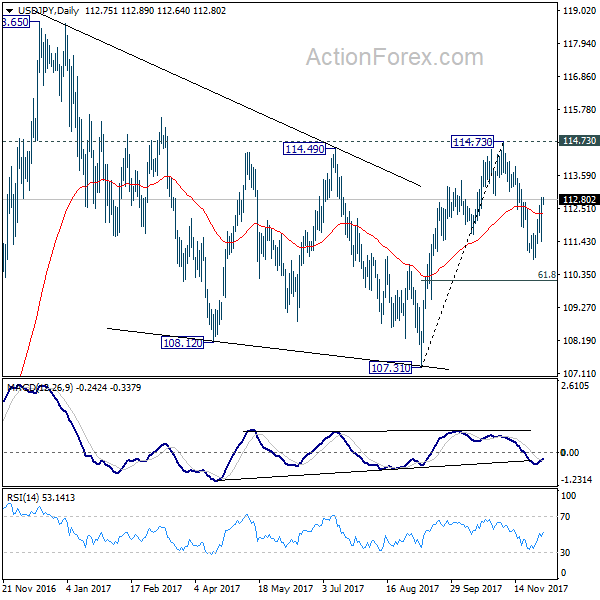

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.40; (P) 112.14; (R1) 112.89; More...

Breach of 112.8y suggests that USD/JPY's rebound from 110.83 is resuming. More importantly, pull back from 114.73 is likely completed. Intraday bias is back on the upside for retesting 114.73 key resistance. Decisive break there will extend the rally from 107.31 to retest 118.65 high. In case of another fall, we'll look for bottoming again below 61.8% retracement of 107.31 to 114.73 at 110.14.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

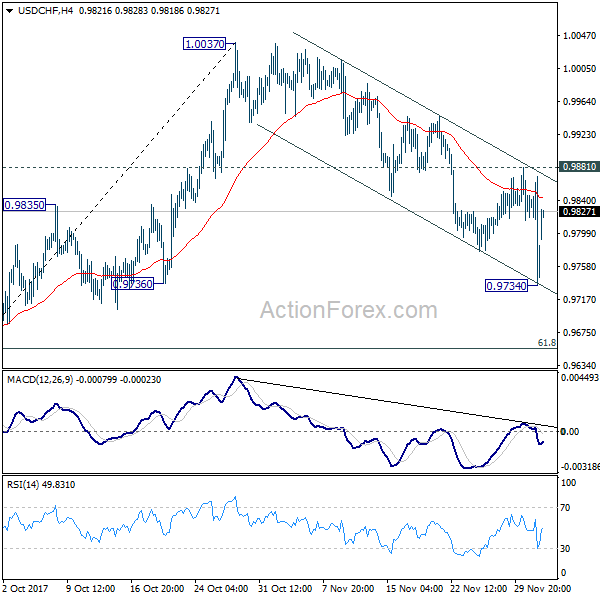

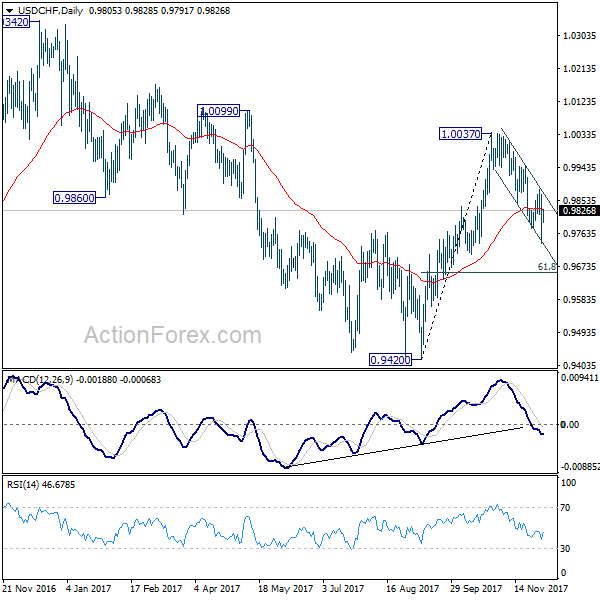

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9701; (P) 0.9786; (R1) 0.9836; More....

USD/CHF rebounds strongly today and intraday bias is turned neutral first. With 0.9881 minor resistance intact, deeper fall cannot be ruled out. Break of 0.9734 will target 61.8% retracement of 0.9420 to 1.0037 at 0.9656. Nonetheless, as choppy fall from 1.0037 is seen as a correction, we'll look for bottoming again below 0.9656 and above 0.9420. On the upside, break of 0.9881 resistance will now indicate completion of the decline. And intraday bias will be turned back to the upside for 1.0037.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Dollar Higher on Senate Tax Bill Passage, Cautious ahead of Busy Week

Dollar opens the week generally higher as boosted by news that Senate has finally passed their tax bill. But strength is relatively limited firstly on concern that Russian probe is getting closer to President Donald Trump. Secondly, there are talks that the final version of the tax bill would just give very little lift to the economy. Sterling is also cautious bullish on optimism over Brexit negotiation. Swiss Franc and Japanese Yen are trading as the weakest one today. Looking ahead, the week is jam-packed with RBA and BoC meeting, plus many heavy weight economic data including non-farm payrolls.

Final tax bill could only give 0.3% boost in 2018 growth

The US Senate finally passed their version of tax bill on Saturday after marathon debates and votes on amendments. Now Republicans will take the legislative process to the next stage and work on reconciliation of the bills of the House and the Senate. Goldman Sachs economists believe that the final structure of the reconciled bill will "reflect more of the Senate bill than the House bill". That would include having corporate tax cut to 20% effective in 2019, instead of 2018. Also, while the cut from 35% to 20% looks huge, they pointed out that considering the whole package of the tax reform, corporate tax rate will come down effective by "only a couple of percentage points". And, Gold Sachs forecast US growth to be boosted by a mere 0.3% for 2018 and 2019.

UK PM May to meet EC Juncker

UK Prime Minister Theresa May is going to have a lunch meeting with European Commission President Jean-Claude Juncker today. Juncker has set today as the deadline for May to revise her offer on Brexit. But UK government played down today's significance and pointed to the EU summit on December 14/15 as the crucial one. In a statement, UK said that "with plenty of discussions still to go, Monday will be an important staging post on the road to the crucial December council."

For now, there seems to be agreements, in principles, on two of the three key issues already. It's believed that May is going to offer between GBP 40b and GBP 50b for settling the divorce. And it's reported that Irish officials and EU are optimistic on solving the problem of Irish border. But there are reports that EU MEPS are unhappy as the rights of EU citizens in UK post Brexit are being forgotten. The sticky point here is that EU is urged to insist that EU citizens rights in UK are being protected by the European Court of Justice. But this is firmly ruled out by May and UK politicians.

Looking ahead - RBA, BoC and NFP

RBA rate decision and Australian data will be closely watched. The central bank is widely expected to keep its cash rate unchanged at record low of 1.50% on Tuesday. Considering weak wage growth and lack of inflationary pressure, there is little push for a hike at the moment. On the other hand, there were even talks that RBA is in "cut" territory due to sluggish house price growth. According to CoreLogic data back in November, annual price growth mere stood at 5.2%, half of the peak of 10.4% back in May 2017. More importantly, the six month price growth stood at 0.7%. And in the past 30 years, 7 out of 9 times RBA cut interest rates as 6-month house price growth weakened to zero or turned negative. But of course, considering RBA's high alertness on household debts, the central bank is also nowhere near a cut. Also to be released include retail sales, GDP and trade balance.

BoC rate decision is another key focus of the week. Despite last week's stellar employment data, there is little chance for the central bank hike interest rate this time. Nonetheless, the strong job data would eased the worries that the two hikes this year were too aggressive. Going forward, giving the unknown outcome of NAFTA renegotiation, the central could likely hold their hands for a while. Governor Stephen Poloz would also want to see how the domestic economy absorbs the prior hikes. If the incoming data continue to show strength, BoC could act again in April or afterwards.

There are also other heavy weight data to be featured this week, including ISM services and non-farm payroll. These data shouldn't derail Fed's December hike and would instead affect the chance of the projected three hikes next year. UK will also release PMIs as productions.

Here are some highlights of the week ahead:

- Monday: Japan consumer confidence; Eurozone Sentix investor confidence; UK construction PMI; US factory orders

- Tuesday: UK BRC retail sales; RBA rate decision, Australia retail sales, current account; Eurozone services PMI final, retail sales, GDP revision; UK services PMI; Canada trade balance; US trade balance, ISM services

- Wednesday: Australia GDP; Germany factory orders; Swiss CPI; US ADP employment, non-farm productivity; BoC rate decision, Canada labor productivity

- Thursday: Australia trade balance; Japan leading indicators; Swiss unemployment rate, foreign currency reserves; German industrial production; Canada building permits, Ivey PMI; US jobless claims

- Friday: Australia home loans; China trade balance; Germany trade balance; UK productions, trade balance; Canada housing starts; US non-farm payroll, U of Michigan sentiment

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9701; (P) 0.9786; (R1) 0.9836; More....

USD/CHF rebounds strongly today and intraday bias is turned neutral first. With 0.9881 minor resistance intact, deeper fall cannot be ruled out. Break of 0.9734 will target 61.8% retracement of 0.9420 to 1.0037 at 0.9656. Nonetheless, as choppy fall from 1.0037 is seen as a correction, we'll look for bottoming again below 0.9656 and above 0.9420. On the upside, break of 0.9881 resistance will now indicate completion of the decline. And intraday bias will be turned back to the upside for 1.0037.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Nov | 13.20% | 13.20% | 14.50% | |

| 0:00 | AUD | TD Securities Inflation M/M Nov | 0.20% | 0.30% | ||

| 5:00 | JPY | Consumer Confidence Index Nov | 44.9 | 44.5 | ||

| 9:30 | GBP | Construction PMI Nov | 51 | 50.8 | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Dec | 32.7 | 34 | ||

| 10:00 | EUR | Eurozone PPI M/M Oct | 0.30% | 0.60% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Oct | 2.60% | 2.90% | ||

| 15:00 | USD | Factory Orders Oct | -0.40% | 1.40% |

Market Morning Briefing: Pound Had Breached Resistance Near 1.35

STOCKS

Dow (24231.59, -0.17%) is testing immediate channel resistance on the daily candles and could trade in the 23800-24400 region for a couple of sessions before rising towards 24600-24800 by the end of the month. With 3-weeks to go for the year to end we may not expect a rise above 25000 this month.

Dax (12861.49, -1.25%) came down sharply contrary to our expectation that the index would rise towards 13200 and may not break below 12900 just now. The weekly closing at levels below 12900 is important and could take the index towards 12800-12600 in the next few sessions if the downside momentum remains strong just now. Near term looks bearish.

Nikkei (22778.69, -0.18%) tried to test 23000 last week but could not move up above that. A corrective dip towards 22500 or lower is likely to be seen in the coming sessions on a break below 22666.

Shanghai (3308.65, -0.27%) is trapped in the 3350-3300 region and unless a sharp bounce back from current levels is seen towards 3350 and higher, the index could be vulnerable to a fall towards 3275 in the near term.

Last week initiated a sharp correction in Nifty (10121.80, -1.02%), taking it towards 10100 from levels near 10400. Some support could come up near 10030-10000 levels from where a small bounce is possible before the index heads towards 9900 in the longer run. The Gujarat elections would be an important event to look at which could impact the Indian markets next week.

Sensex (32832.94, -0.95%) is likely to find some support near 32500 in the coming sessions. Thereafter some stability is likely to be seen above 32500.

COMMODITIES

Gold (1274.34) also came down on Friday but may not move below 1260 just now. While support at 1260 holds, we stick to our view of a bounce back towards 1300 this week.

Silver (16.37) did finally resolved on the downside last week and could find some support near 16 in the near term. has broken below immediate support and could move down to 16.75-16.60 in the near term.

Gold-Silver ratio (77.77) is rising sharply as Silver has been falling against gold. A test of 79 is possible before the ratio comes back to levels near 77.

WTI (57.99) could move up towards 60 while the immediate support near 57 holds. A break below 57, if seen could take it down to 56-55 in the medium term. Brent (63.42) on the other hand, could test support near 62 before again rising back towards 65-66. Some sideways movement is possible before a sharp upmove.

Copper (3.1095) moved back to levels above 3.05 and while that holds, we could see a bounce to levels near 3.20 or higher. A break below 3.05-3.00, if seen again could take the price back towards 2.95.

FOREX

Dollar-Index (93.109) had dropped on Friday to a low of 92.6 during intra-day trading and closed at 92.89. However, the index is again trading at levels seen prior to Friday, boosted by the late night corporate tax cut passed by the US Senate and a corresponding rise in US yields (see Interest Rates below). It would be interesting to see if this provides strength to the Dollar, in which case, the Index could test resistance levels of 93.30-93.40 on the daily charts very soon. However, a return to weakness could see the index test immediate support near 92.80 on the daily charts.

Euro (1.1871) had seen some strength on Friday with a day high of 1.1940 and a close just below 1.19 at 1.1899. However, late night news of the US tax cuts seems to have brought in bearishness and a drop to support near 1.18-1.1775 on the weekly candle charts might happen soon. There has also been a sharp decline in US-German Yield Spread which could further drive dollar strength (see Interest Rates below). However, it is yet to be seen if the impact of the tax cuts will have a lasting effect, in the absence of which, a move towards resistance near 1.19-1.195 on weekly line charts and a corresponding breach of the same can be expected.

Dollar-Yen (112.74) has been moving up for the last few days and is poised to test resistance around 113.50 on the daily line charts in this week. A move past that could imply a further test of 114 on the weekly candle chart by the end of this month.

Pound (1.3468) had breached resistance near 1.35 on Friday to reach a high of 1.355 during intraday trading but closed below 1.35 at 1.3472. It is currently trading around the same levels, thereby implying a possible hold of resistance at 1.35 for the next few sessions. A breach of the same could however push it to test resistance at 1.36 on the weekly charts.

Dollar Rupee (64.59) has opened higher compared to Thursday’s close (64.4675) and with expectations of Dollar strength resurfacing, a rise beyond 64.70 in the next couple of sessions is likely.

INTEREST RATES

US yields have risen sharply as the US moves to a better tax system. The headline cut in tax numbers have boosted the shorter term yields to move up sharply. The 10Yr (2.41%) and the 5Yr (2.16%) have risen sharply from previous levels of 2.36% and 2.0% respectively while the 30YR (2.80%) is up from 2.76%. Near term looks bullish for the yields.

The Japan-US 10YR (2.37%) is trading along the channel resistance and if doesn’t come off from here could break the resistance to move up towards 2.40% or higher in the near term, leading to arise in Nikkei and Dollar Yen which seems to be less likely for now.

The German-US 10Yr (-2.10%) has also fallen sharply and could possibly test -2.15% before moving up to higher levels in the medium term.

GOLD – Looks To Recover Higher On Bull Pressure

GOLD - The commodity looks to extend upside pressure following a price halt on Friday. On the downside, support comes in at the 1,270.00 level where a break will turn attention to the 1,260.00 level. Further down, a cut through here will open the door for a move lower towards the 1,250.00 level. Below here if seen could trigger further downside pressure towards the 1,240.00 level. Conversely, resistance resides at the 1,290.00 level where a break will aim at the 1,300.00 level. A turn above there will expose the 1,310.00 level. Further out, resistance stands at the 1,320.00 level. All in all, GOLD looks to weaken further on correction.

Muted USD Reaction To Tax Reform

Muted USD reaction to Tax Reform

Its been a roller coaster of despondency given how failing the dollar continues to trade post-tax reform headlines.

The FX markets remain tacitly focused on US inflation which suggests a tax reform victory in the Senate may continue to have a muted dollar reaction as subdued inflation could ultimately weigh on US yields.

If the market continues to underprice anything around tax reform, it’s the possible repatriation flow effects.

But as it sits today, so far the Euro appears to be the more active driver in overall G-10 sentiment.

The Euro

With Traders taking cues from the EU economic data and the Euro reaffirming it’s strength on robust data flow, the Greenback may be hard pressed to make any headway against the single currency unit as Asset managers continue to flood into the Euro. Ultimately the Euro could be the USD’s biggest foil.

The Japanese Yen

The USDJPY yen should benefit from higher risk appeal and favourable US interest rate differentials. But despite what suggests a smooth path higher, trader’s are not banking on clear sailing to 114.00 especially after the USD’s spontaneous combustion on Friday’s #Russiagate headlines.

The British Pound

Brexit will be the primary focus this week which makes positioning risk a bit testy. But with negations apparently heading in the right directing its difficult not to remain constructive near-term.

FX Asia

The Malaysian Ringgit

After the recent rally, positive Ringgit momentum early in the week will be hard to come by given the emotional roller coaster G-10 traders are riding. This gnawing level of uncertainty should filter through to local EM sentiment.

Oil prices should continue to support the Ringgit as OPEC optimism should underpin prices. But the oil patch will remain susceptible to US inventory data and shale oil production

Overall, however, the market remains positive on the Ringitt on the global growth narrative providing a boon to domestic exports.

Also, the market will continue to bake in a January interest rate hike as the BNM leans hawkish. But subject to inflation and economic expansion, both of which may surpass the BNM 2018 forecasts, the market may start to price in another hike for Q 3. Mind you this will be entirely data dependent so we could see the Ringgit express more volatility around critical domestic data prints

Weekend Update

Weekend Update

Washington continues to break creative new ground when it comes to political dysfunction. However, the Tump administration took a giant step forward toward achieving the first major legislative victory of his presidency after the Senate passed its tax plan in a 51-49 vote early on Saturday morning

Stock dealers s will be monitoring the tax-sensitive, which should react positively.

In early trade, the Dollar nudged above Friday’s high water marks where tax reform momentum was building before risk aversion reared its head after ABC first reported that Flynn would testify against Trump, citing “people familiar with the matter.”

Probably not the explosive dollar bounces some were hoping for, but there remains a high level of scepticism in financial markets about the real economic benefits vs the budgetary costs within the legislation. And given all the political bluster coming out of Washington these day’s and just how reactive the USD was to risk on Friday, dealers may be reluctant to chase this much higher

Now it’s off to Republican joint Conference to arbitrate the variances between the House and Senate versions. If the legislation gets ratified quickly, there would likely be another dollar bounce, but the longer this drags out, the dollar will probably sell off as political uncertainty has been the greenback’s undoing over and over again in 2017.

Back at” Dysfunction Alley” ( 1600 PENN) While “Rexit” has apparently come and gone; the administration is yet again dealing with another looming government shut down. Dec 8 But, House GOP leaders unveiled a short-term plan over the weekend to avert a shutdown and keep the government open through Dec. 22. But dealing with Bipartisan political wrangling is a real head-scratcher at the best of times, and now that the main obstacle to tax reform has passed, currency trader may look for a rock to hide under for the rest of the year to avoid the political whipsaw.

USDCHF – Retains Downside Pressure

USDCHF - The pair backed off higher prices on Thursday leaving risk to the downside. On the downside, support lies at the 0.9800 level. A turn below here will open the door for more weakness towards the 0.9750 level and then the 0.9700 level. On the upside, resistance resides at the 0.9850 level where a break will clear the way for more strength to occur towards the 0.9900 level. Further out, resistance comes in at the 0.9950 level. Above here if seen will turn attention to 1.0000. All in all, USDCHF faces further upside pressure.