Sample Category Title

US Retail Sales Rise 0.5% in April, Reinforcing Resilient Demand

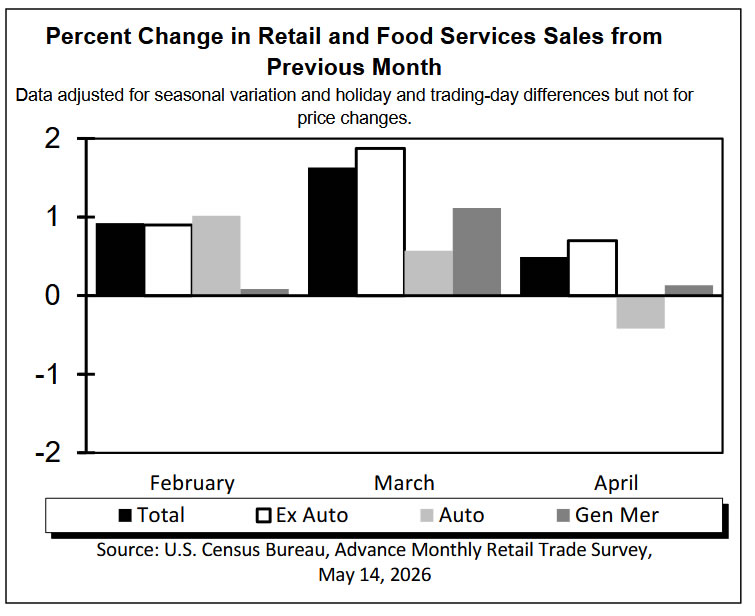

US retail sales rose 0.5% mom in April, matching market expectations and reinforcing the view that consumer demand remains resilient despite rising inflation pressures and elevated interest rates. Core readings were slightly firmer, with retail sales excluding autos rising 0.7% mom, above expectations of 0.6% mom, suggesting underlying household spending momentum remains relatively healthy.

The broader breakdown of the report also pointed to stable domestic demand conditions. Retail sales excluding gasoline increased 0.3% mom. The closely watched control group excluding both autos and gasoline rose 0.5% mom. The data suggests consumers continue spending even as higher energy prices linked to the Middle East conflict begin filtering through the broader economy.

On a longer-term basis, total retail sales for the February through April period were up 4.4% compared with the same period a year earlier.

| Indicator | Latest | Expectation |

|---|---|---|

| Headline Retail Sales (MoM) | 0.5% | 0.5% |

| Retail Sales ex-Autos (MoM) | 0.7% | 0.6% |

| Retail Sales ex-Gasoline (MoM) | 0.3% | |

| Retail Sales ex-Autos & Gasoline (MoM) | 0.5% | |

| Feb-Apr Total Sales (YoY) | 4.4% |

US initial jobless claims rise to 211k vs exp 205k

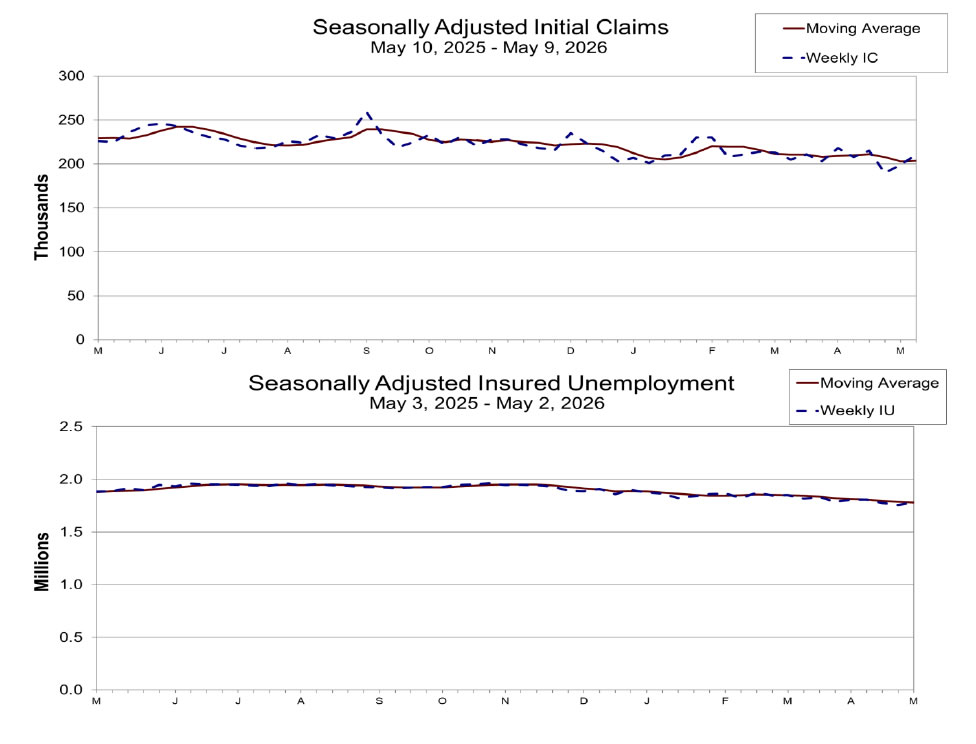

US initial jobless claims rose 12k to 211k in the week ending May 9, coming in slightly above expectations of 205k and signaling some modest cooling in labor market conditions. The four-week moving average of initial claims, which helps smooth weekly volatility, also edged higher by 750 to 203.75k.

Continuing claims increased by 24k to 1.782m in the week ending May 2, suggesting unemployed workers are taking slightly longer to find new jobs. Still, the broader trend remains relatively stable, with the four-week moving average of continuing claims dipping slightly to 1.781m.

| Indicator | Previous | Latest | Expectation |

|---|---|---|---|

| Initial Jobless Claims | 199k | 211k | 205k |

| Initial Claims 4-Week Average | 203k | 203.75k | |

| Continuing Claims | 1.758m | 1.782m | |

| Continuing Claims 4-Week Average | 1.788m | 1.781m |

The ECB and BoE Unlikely to Rush With Rate Hikes

- The futures market is mistaken in expecting 2–3 ECB rate hikes in 2026.

- Accelerating US inflation will prompt the Fed to adopt a more hawkish stance.

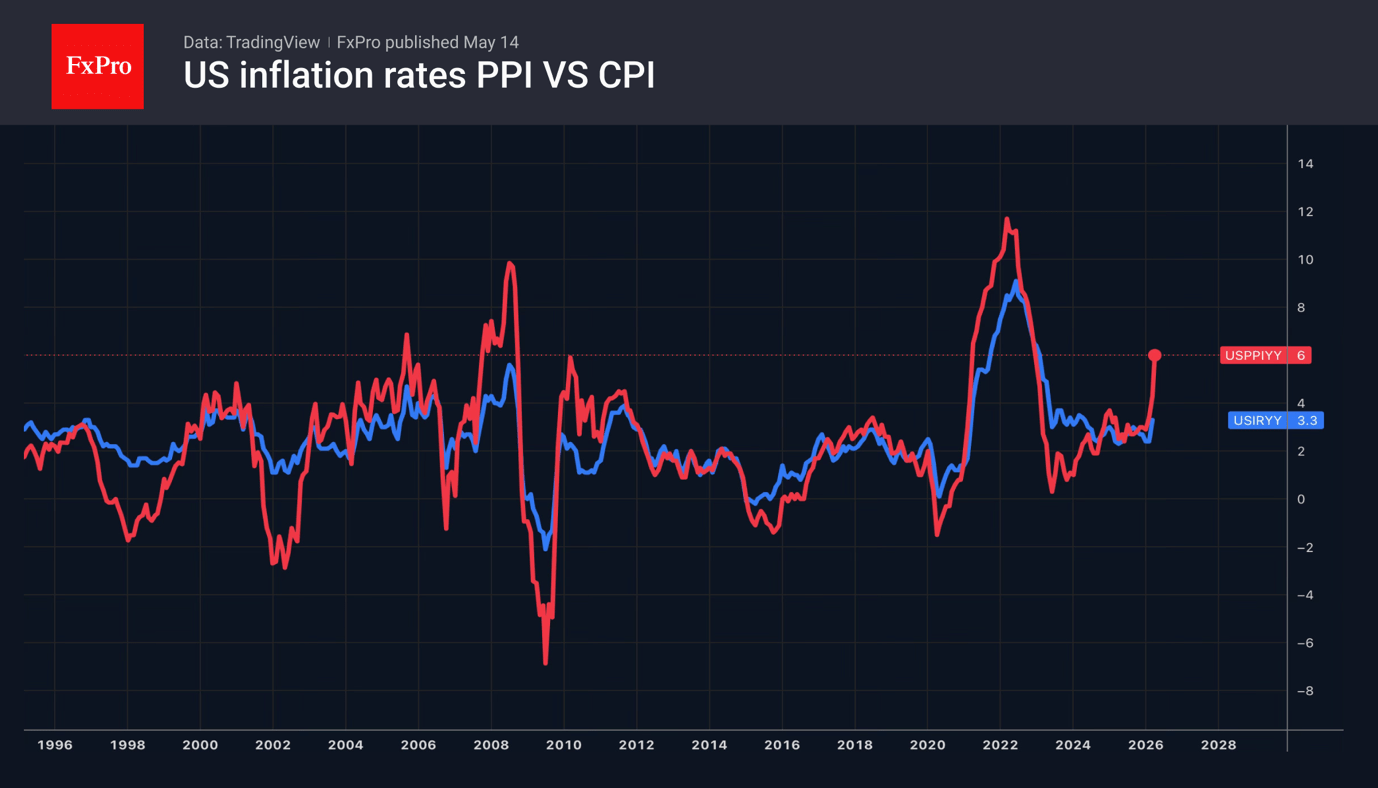

The US dollar took two steps forward and one back following another batch of hawkish macroeconomic data and new record highs for US indices. NVIDIA’s market capitalisation rising to $5.5 trillion triggered an S&P 500 rally, boosted global risk appetite and reduced demand for the greenback as a safe-haven asset. Bears on EURUSD were unable to fully capitalise on the sharpest PPI acceleration since 2022, up to 6% in April.

The Fed prefers to gauge inflation using the Personal Consumption Expenditures (PCE) index. Based on CPI and PPI data, core PCE could accelerate to 3.3% in April. Coupled with the stabilisation of the labour market, this gives CME derivatives a probability of over 30% of a rate hike in 2026, rising to 50% by March 2027.

Meanwhile, the ECB has signalled that it may not share the view of Bloomberg experts and the futures market that there will be 2–3 rate hikes of 0.25 percentage points this year. Executive Board member Olli Rehn stated that the eurozone is on the brink of a stagflationary shock, whilst Chief Economist Philip Lane believes that a contraction in domestic demand will make it difficult to adjust monetary policy.

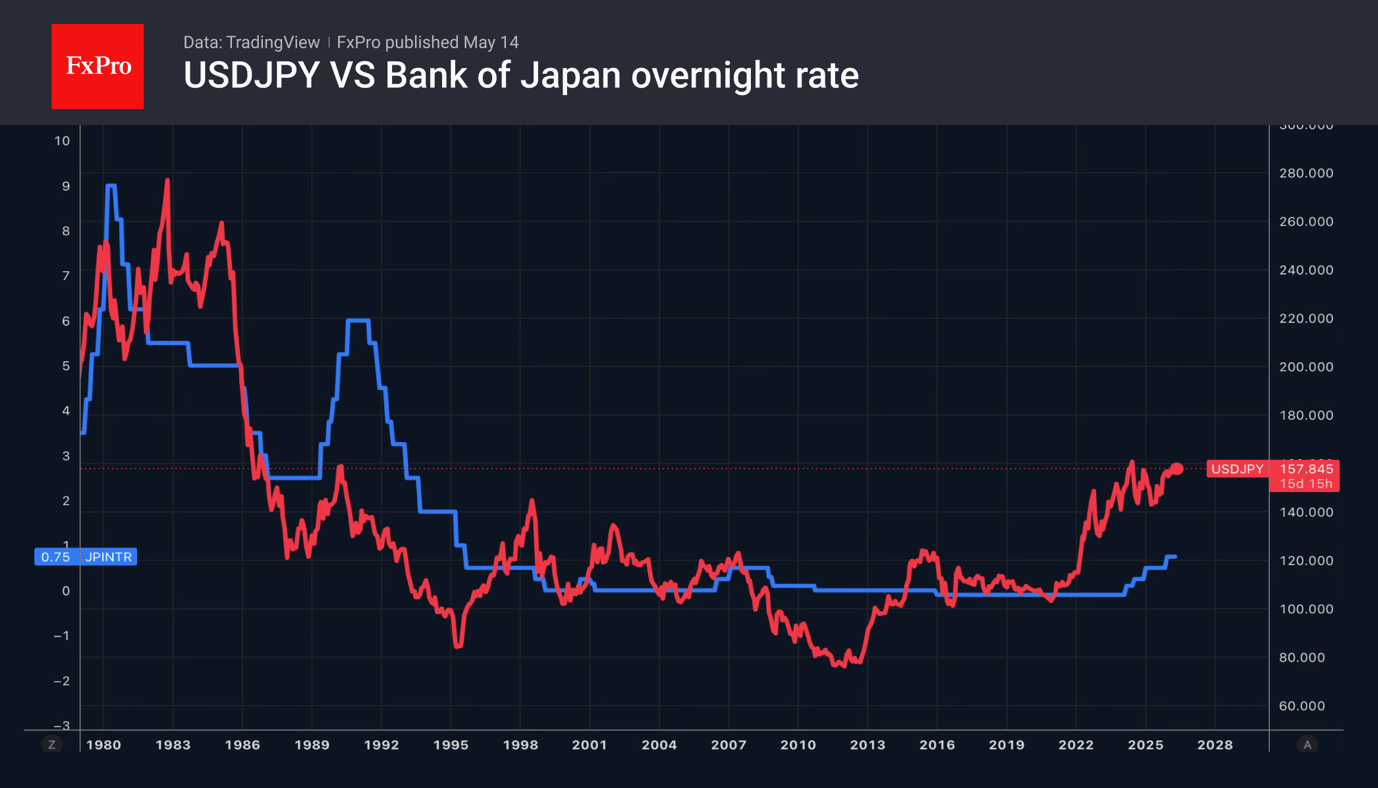

The yen found its footing after three days of selling following an OECD statement that the Bank of Japan would raise its overnight rate to 2% by the end of 2027. It must continue its cycle of monetary tightening to prevent the economy from overheating.

From the perspective of the bond yield spread, USDJPY looks overbought. This allows the government to argue that the pair has become detached from economic fundamentals. However, speculators are betting on high oil prices, carry trades and strong demand for the US dollar as a safe-haven asset.

The pound continued to fall amid comments from central bank officials. Sarah Breeden believes that the Bank of England cannot wait forever, but that monetary policy tightening is not required in either June or July. Previously, traders were buying GBPUSD on expectations of three rate hikes in 2026 but rising political risks and the BoE’s dovish rhetoric are forcing them to offload sterling.

Three Signs of a Bearish Crypto Market

Market Overview

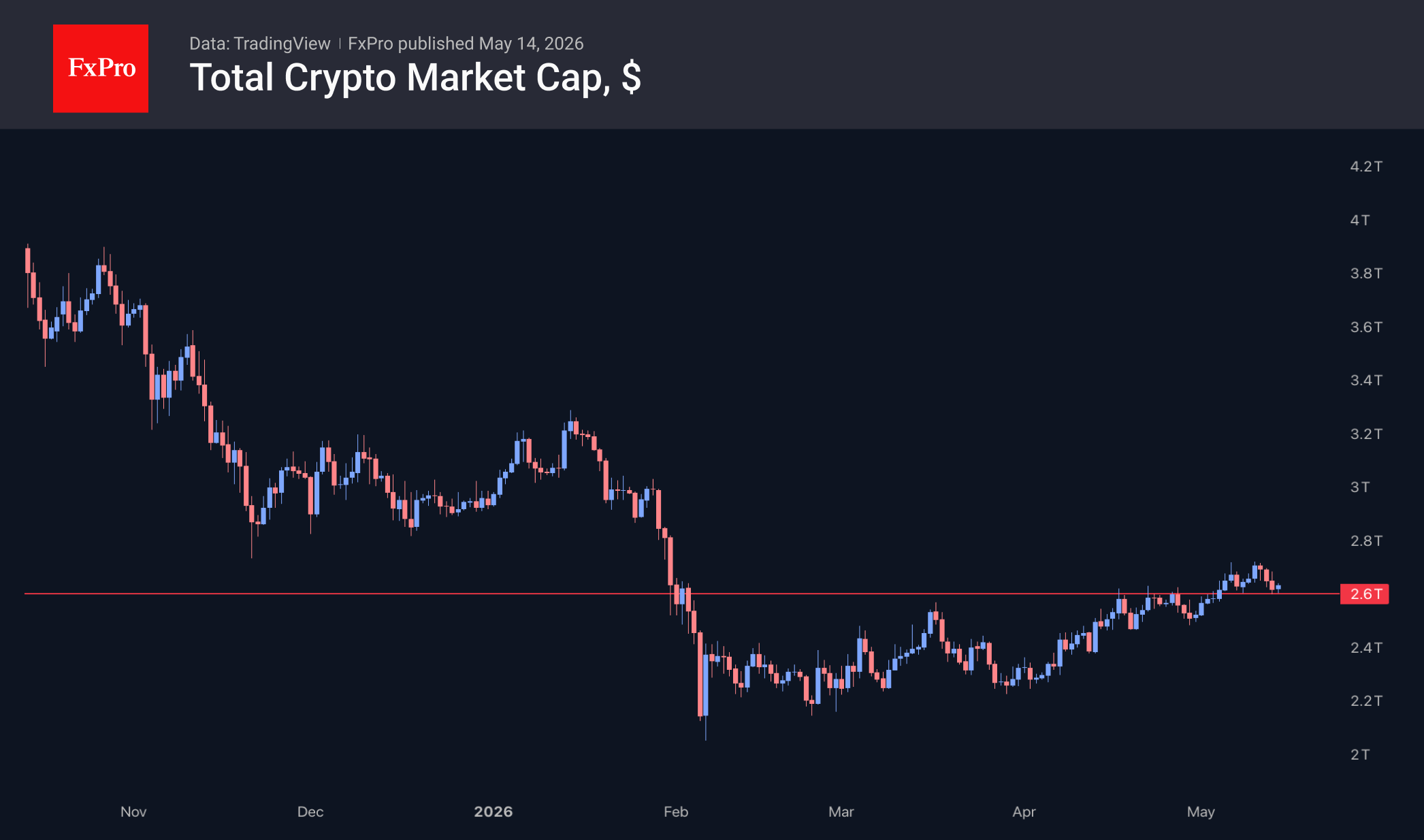

The crypto market has been retreating towards the lower end of the range seen over the last couple of weeks, near $2.61T, but at the time of writing has pared its losses to around 1% over the past 24 hours, trading at $2.66T. Once again, the cryptocurrency market is underperforming the stock market, which buyers have pushed to new highs. A key reason for buyers’ caution is the anticipation of the vote on the CLARITY Act. The best performers over the last day have been Dogecoin (+2.4%), Immutable (+2%) and Tron (+0.3%). The biggest declines among the most popular coins were seen in Theta (-8.3%), Internet Computer (-7.8%) and Toncoin (-6.9%).

The sentiment index has fallen for the second day in a row, dropping to 34 from 49. Alongside lagging equities, weak sentiment, and the inability to move into ‘greed’ territory, this is further evidence that cryptocurrencies are not ready to enter a long-term bull market.

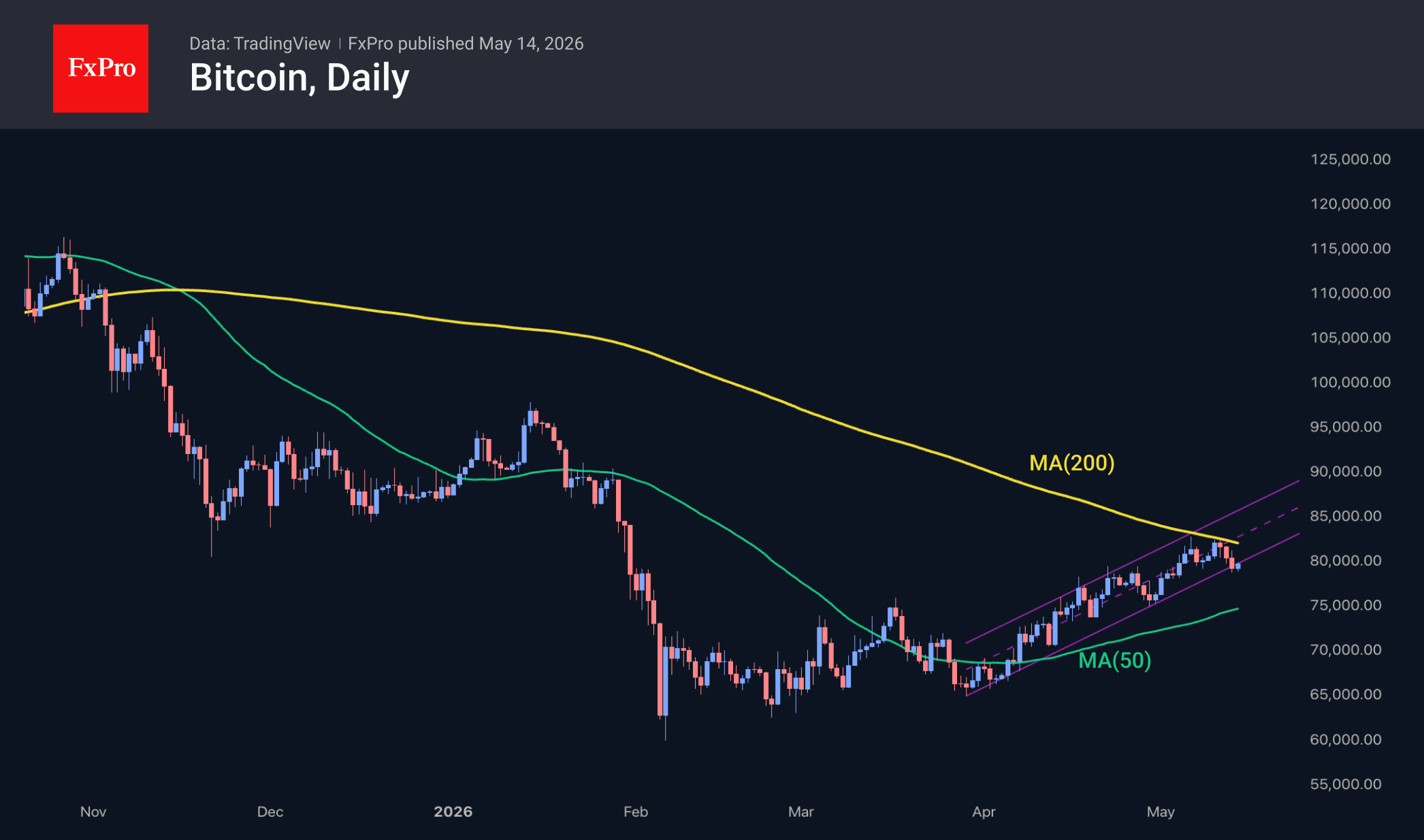

Bitcoin fell below $79K at the low point of a 6-hour sell-off on Wednesday evening. A significant catalyst for the sell-off was data showing an acceleration in producer price inflation, prompting a reassessment of the Fed’s plans for the key interest rate. However, right at the start of the new day, buyers are once again in the driving seat, pushing the price of the leading cryptocurrency towards $80K. The stock market quickly digested the negative inflation news, which also bolstered the confidence of cryptocurrency buyers. The declining 200-day MA remains an important line of resistance, serving as a stark reminder of the market’s bearish phase.

News Background

Higher inflation figures have reduced risk in Bitcoin derivatives. Open interest on major crypto exchanges has fallen by nearly $1.25 billion, CryptoQuant notes. Rising inflation is undermining the narrative of a more accommodative monetary policy.

Financial giant Charles Schwab has launched direct trading in Bitcoin and Ethereum, opening access to an initial group of retail clients. Previously, the company offered only indirect investments via ETFs and derivatives.

21Shares has launched the first spot ETF based on Hyperliquid. The fund provides access to the Hyperliquid token without requiring the purchase of the asset, and it includes staking rewards. The Hyperliquid ETF raised $1.2 million on its first day of trading.

The Solana blockchain update, known as Alpenglow, which will increase transaction efficiency 100-fold, is one step closer to deployment on the mainnet. The upgrade has entered the public testing phase and could be ready for launch on the mainnet as early as the third or fourth quarter of this year.

GBP/AUD Sinks to 1½-Year Lows as Aussie Risk Rally Meets UK Political Paralysis

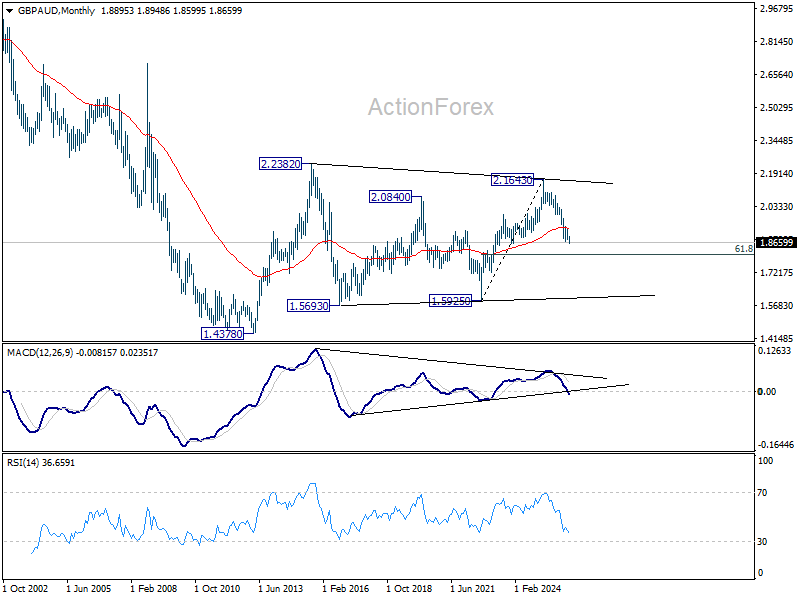

GBP/AUD extended its medium-term downtrend this week, briefly breaking below the 1.86 handle and falling to its lowest level since late 2023 as markets increasingly favored the Australian Dollar’s strong growth and yield profile over Sterling’s mounting political and policy uncertainty.

On the Australian side, the story remains overwhelmingly supportive.

The Australian Dollar continues benefiting from one of the strongest macro combinations in global currency markets right now: resilient global risk appetite, elevated yield expectations, and continued AI-driven equity optimism. Global stock markets have remained remarkably strong this week, with NASDAQ, Nikkei, and KOSPI all extending toward fresh highs as investors continue pouring into technology and semiconductor-linked assets. As one of the world’s highest-beta major currencies, AUD tends to outperform strongly during periods of broad “risk-on” sentiment.

Yield expectations are providing additional support. Even after three rate hikes already this year, markets are aligning with the RBA’s own projections that the cash rate could climb toward 4.70% by year-end as policymakers continue confronting sticky inflation pressures tied partly to higher energy costs. That hawkish outlook continues widening the policy contrast against other major central banks where uncertainty and caution are becoming more dominant.

Sterling, by contrast, is increasingly trading under a cloud of uncertainty.

Sterling, meanwhile, is weighed down by a growing “uncertainty discount.” Although recent UK economic data has shown some resilience — including stronger-than-expected GDP growth — investors remain increasingly uneasy about both the political outlook and the Bank of England’s policy direction. The BoE’s April decision to hold rates at 3.75% with a heavily split 8–1 vote reinforced the perception that policymakers are trapped between persistent inflation risks and concern about damaging a fragile recovery.

Politics has become the larger problem. Following Labour’s disastrous May 7 local election results, where the party reportedly lost more than 1,300 council seats and control of 35 councils, pressure on Prime Minister Keir Starmer has intensified sharply. Reports of possible leadership challenges later this year have added a growing political risk premium into Sterling pricing as investors worry Britain may face prolonged policy instability just as markets are already becoming more sensitive to fiscal credibility and gilt market volatility.

Technically, the break below 1.8690 confirms resumption of the medium term downtrend from 2.1643 (2025 high). Further decline is now expected toward 61.8% projection of 2.0286 to 1.8690 from 1.9399 at 1.8411. Near-term outlook will remain bearish while 1.8954 resistance holds, in case of recovery.

In the long term picture, the break of 55 W EMA (now at 1.9298) suggests that fall from 2.1643 (2025 high) is reversing whole rise from 1.5925 (2022 low). This decline is also viewed as another falling leg inside the sideway pattern from 2.2382 (2015 high). Sustained break of 61.8% retracement of 1.5925 to 2.1643 at 1.8109 will pave the way towards 1.5925.

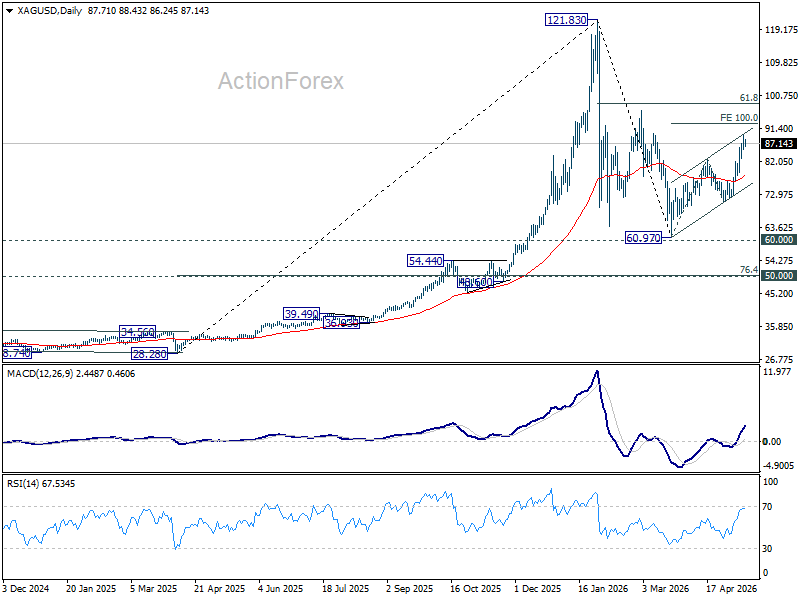

Silver’s Momentum Stalls Below $90, but Bigger Breakout Risks Are Building

Silver briefly pushed above the $89 level this week before losing some momentum ahead of $90 psychologically mark. Yet this pause appears more like consolidation than exhaustion. And, the most important signal in Silver right now is the fact that the rally continueed despite hotter US inflation data and rising expectations for tighter Federal Reserve policy.

Under normal macro conditions, a stronger Dollar and increasing expectations for an eventual Fed “insurance” rate hike would typically weigh heavily on precious metals. Instead, Silver has continued printing higher highs and higher lows while Gold remains comparatively sluggish near support around $4,700.

The divergence inside the precious metals complex suggests that Silver is trading on its industrial scarcity story. The steady compression in the Gold-Silver Ratio suggests investors are favoring Silver’s structural demand profile. Markets are focused on persistent physical deficits in Silver supply, with 2026 projected to mark another year where global demand exceeds production. At the same time, demand tied to AI infrastructure, semiconductors, and high-efficiency solar panels continues providing a powerful underlying tailwind.

More importantly, any meaningful progress toward reopening the Strait of Hormuz could trigger a broader return of global risk appetite, lower oil prices, and a softer Dollar — a combination that would significantly strengthen the industrial demand outlook for Silver while easing macro headwinds from rising Fed expectations. In that case, Silver would likely have the powerful momentum to push through $90, and probably $100 too.

Technically, further rise is expected in Silver as long as 83.01 minor support holds. Next target is 100% projection of 60.97 to 83.04 from 70.83 at 92.90. That level could become a critical test for determining whether the rally from 60.97 is evolving into a larger impulsive breakout rather than merely a corrective rebound.

However, a break below 83.01 would argue that the current rally phase has temporarily run its course and that Silver may need a longer consolidation period above 70.83 before building a stronger base for the next advance.

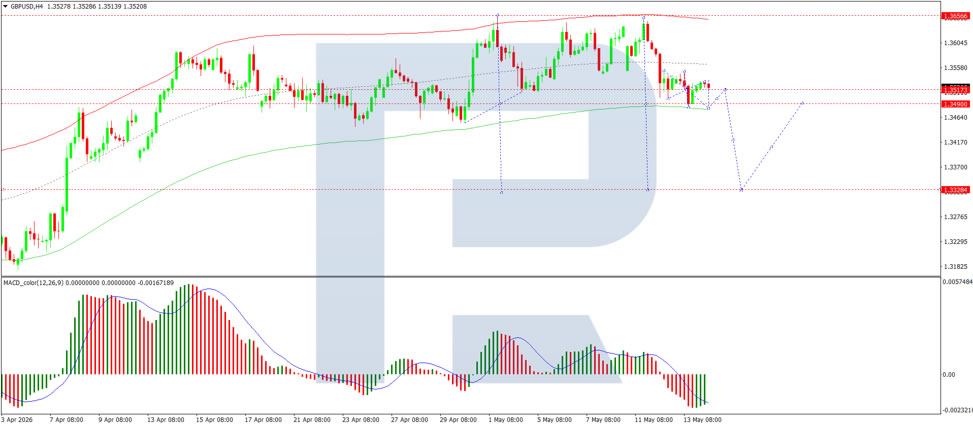

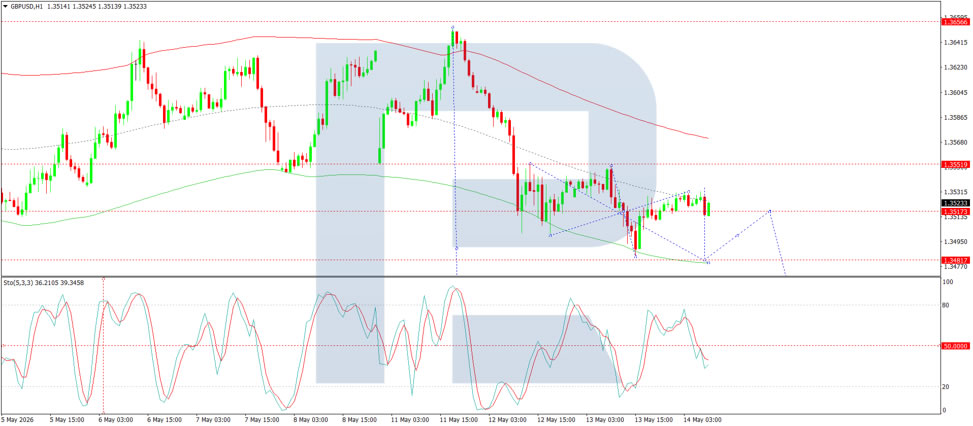

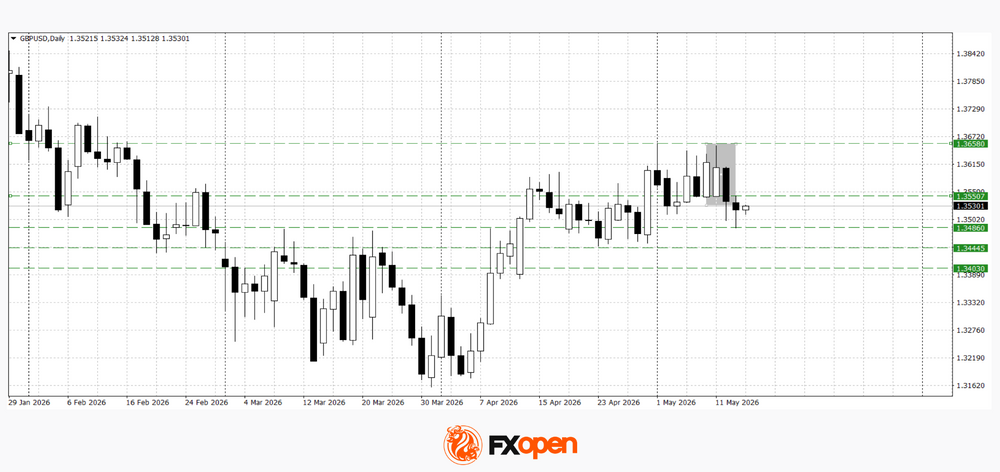

GBP/USD Under Policy Pressure: What Lies Ahead for the Prime Minister?

GBP/USD held at 1.3528 on Thursday following an overnight decline. The pound remains under pressure, close to its lowest levels since late April, amid media reports of a potential leadership contest within the ruling party. According to The Times, British Health Minister Wes Streeting is preparing to launch a campaign against Prime Minister Keir Starmer.

Despite pressure from parts of the government and more than 80 Labour Party MPs, Starmer has reiterated that he does not intend to resign following the party’s weak performance in the local elections. The cabinet composition remains largely stable, despite a few resignations from junior ministers.

External factors continue to weigh on the pound. Talks between the US and Iran remain inconclusive, while restrictions in the Strait of Hormuz keep oil prices elevated. Against this backdrop, the market continues to price in nearly three Bank of England rate hikes by the end of the year.

Investors are also awaiting the release of new UK macroeconomic data, including first-quarter GDP figures.

Technical Analysis

On the H4 chart, GBP/USD is trading within a broad consolidation range above 1.3515, currently extending up to 1.3530. A move lower towards 1.3480 is possible. After this, the pair may consolidate before attempting a move higher towards 1.3650 or a further decline towards 1.3340. The MACD indicator supports this scenario, with its signal line below zero and pointing firmly downwards.

On the H1 chart, GBP/USD is trading within a compact consolidation range around 1.3515, currently extending down to 1.3483. A rebound towards 1.3530 (testing from below) is possible, followed by a potential move lower towards 1.3480. The Stochastic oscillator confirms this scenario, with its signal line below 50 and pointing firmly downwards towards 20.

Conclusion

GBP/USD remains under dual pressure from domestic political uncertainty and global economic risks. Further weakness in the pound is possible if leadership concerns and geopolitical tensions persist, while UK GDP data may act as a short-term catalyst for volatility.

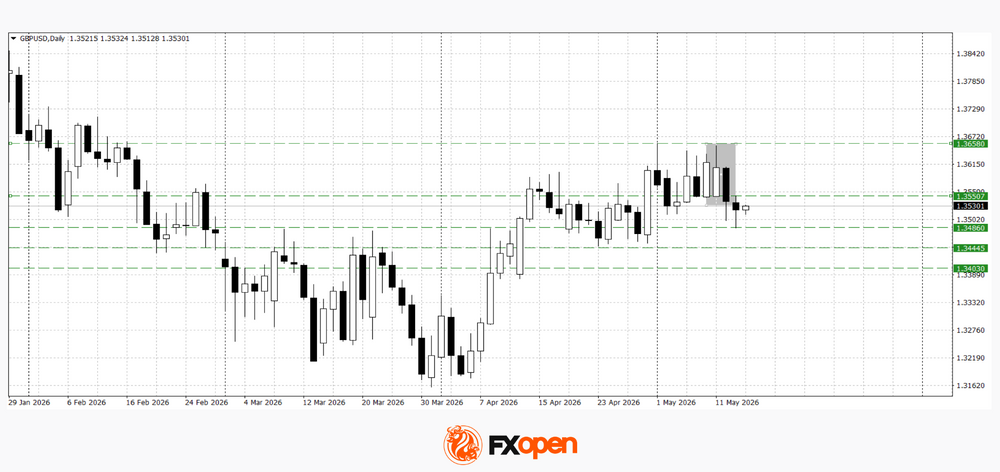

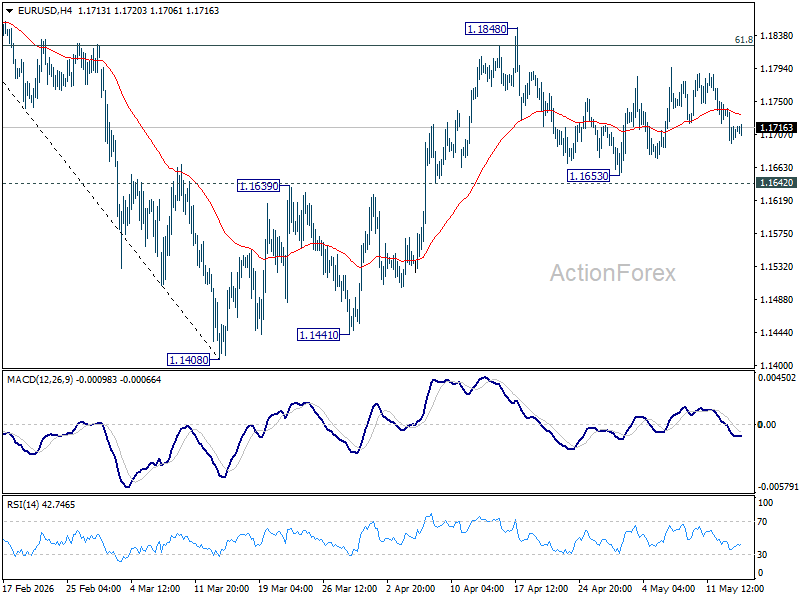

EUR/USD and GBP/USD Return to Ranges Ahead of Key Data

European currencies have moved into a corrective phase following recent gains, while market participants focus on upcoming macroeconomic data from the UK, the eurozone and the United States. After a strong upward move, both currencies returned to their previous trading ranges, signalling a shift towards consolidation ahead of important economic releases. Additional pressure on the euro and pound is coming from partial profit-taking after the earlier weakening of the US dollar.

Investors will assess data on UK GDP, industrial production and business activity across European economies. These figures may influence expectations regarding future actions by the Bank of England and the European Central Bank. At the same time, markets continue to monitor US statistics, including retail sales and jobless claims, which could affect expectations surrounding future Federal Reserve policy.

EUR/USD

EUR/USD has entered a corrective decline after recent gains and is once again trading within its previous range. Technical analysis suggests the pair may fall towards the lower boundary of the four-week range near 1.1650–1.1670, as a bearish engulfing pattern has formed on the daily timeframe. A break below these support levels could trigger a deeper downward correction. If the pair rebounds from 1.1650, a renewed test of 1.1760–1.1780 may follow.

Key Events For EUR/USD:

- today at 10:00 (GMT+3): Spain Consumer Price Index (CPI)

- today at 13:00 (GMT+3): Thomson Reuters/Ipsos Primary Consumer Sentiment Index (PCSI) in Germany

- today at 15:30 (GMT+3): US retail sales volume

GBP/USD

GBP/USD is also correcting after its previous rally and remains within a range-bound structure. A move below yesterday’s low at 1.3490 could lead to a decline towards the 1.3400–1.3440 area. The bearish correction scenario remains valid while the pair stays below 1.3550.

Key Events For GBP/USD:

- today at 09:00 (GMT+3): UK GDP

- today at 09:00 (GMT+3): UK manufacturing production

- today at 15:30 (GMT+3): US initial jobless claims

Market attention remains focused on UK economic data, including industrial production, construction output and investment activity. At the same time, the pair will continue to be influenced by US statistics and the dollar’s reaction to macroeconomic releases. If US data confirms signs of economic slowing, the dollar may come under renewed pressure, allowing GBP/USD to resume its upward movement. However, stronger US figures could intensify the current correction and keep the pair within its established range.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

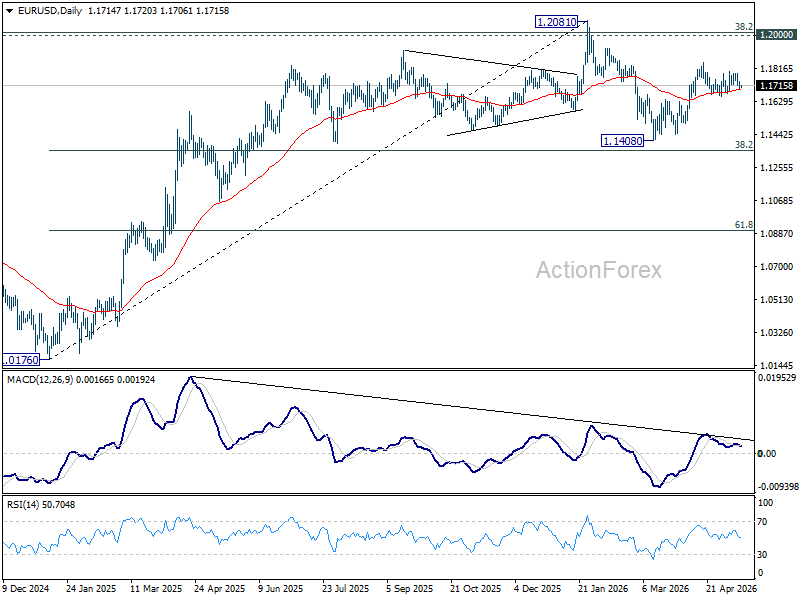

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1688; (P) 1.1714; (R1) 1.1734; More….

EUR/USD is still bounded in sideway trading and intraday bias stays neutral. Further rise is expected with 1.1642 support intact. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

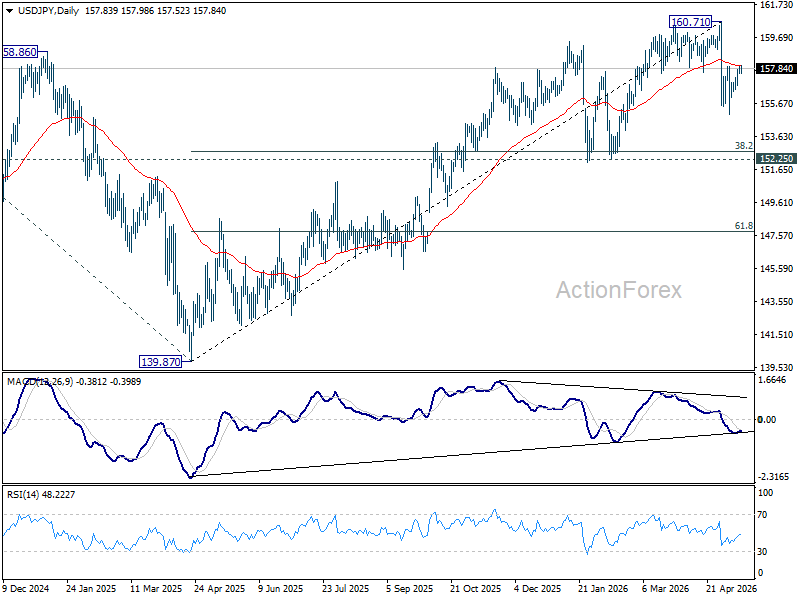

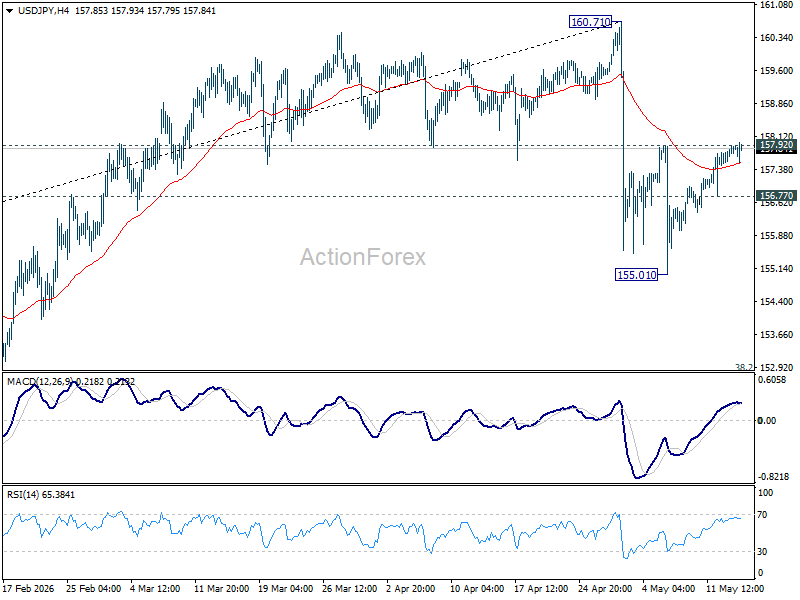

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.59; (P) 157.75; (R1) 158.00; More...

Intraday bias in USD/JPY stays neutral at this point. On the downside, below 156.77 minor support will bring retest of 155.01. Firm break there will resume the fall from 160.71 to 152.25 support next. On the upside, however, firm break of 157.92 will indicate that pullback from 160.71 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.