Sample Category Title

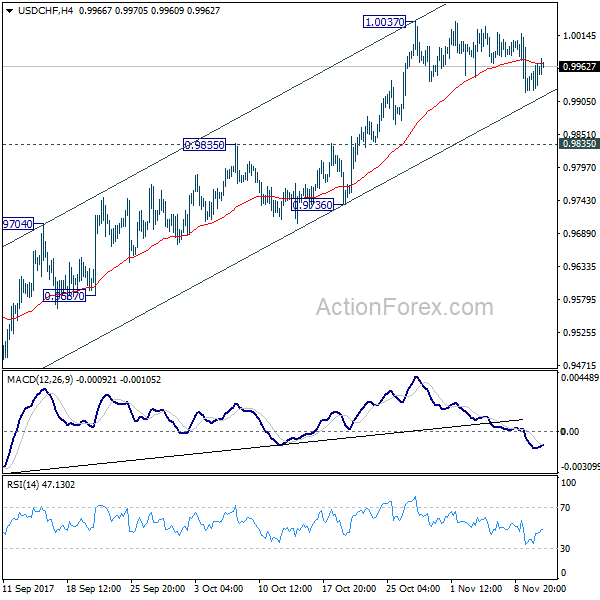

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9929; (P) 0.9949; (R1) 0.9974; More....

Intraday bias in USD/CHF remains neutral as consolidation from 1.0037 is still in progress. We'd continue to expect downside to be contained above 0.9835 resistance turned support and bring rally resumption. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.14% against the JPY and closed at 113.60 per ounce on Friday.

In the Asian session, at GMT0400, the pair is trading at 113.68, with the USD trading 0.07% higher against the JPY from Friday’s close.

The pair is expected to find support at 113.36, and a fall through could take it to the next support level of 113.05. The pair is expected to find its first resistance at 113.85, and a rise through could take it to the next resistance level of 114.03.

Going forward, a speech by the Bank of Japan (BoJ) Governor, Haruhiko Kuroda, scheduled overnight, will be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

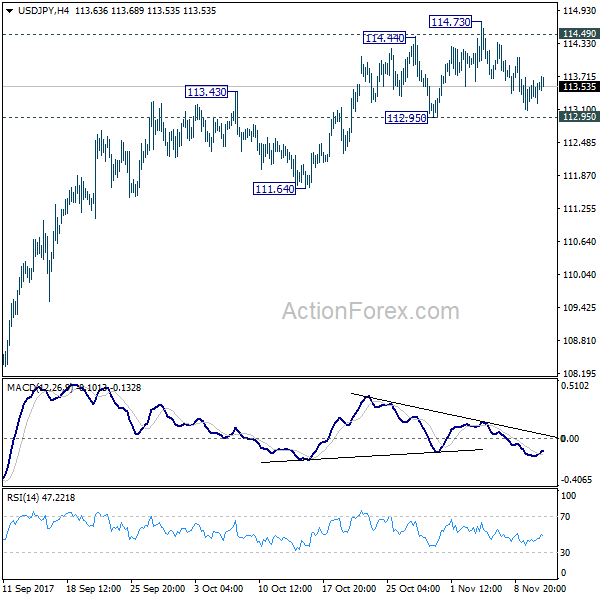

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.28; (P) 113.45; (R1) 113.69; More...

Intraday bias in USD/JPY remains neutral for the moment. As long as 112.95 support holds, near term outlook remains bullish and further rise is expected. On the upside, sustained break of 114.49 key resistance will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

Swiss Franc Extends Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.16% against the CHF and closed at 0.9957 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9965, with the USD trading 0.08% higher against the CHF from Friday’s close.

The pair is expected to find support at 0.9935, and a fall through could take it to the next support level of 0.9905. The pair is expected to find its first resistance at 0.9986, and a rise through could take it to the next resistance level of 1.0007.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Loonie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD slightly declined against the CAD and closed at 1.2677 on Friday.

In the Asian session, at GMT0400, the pair is trading at 1.2688, with the USD trading 0.09% higher against the CAD from Friday’s close.

The pair is expected to find support at 1.2670, and a fall through could take it to the next support level of 1.2653. The pair is expected to find its first resistance at 1.2701, and a rise through could take it to the next resistance level of 1.2715.

With no macroeconomic releases in Switzerland today, market participants would focus on global macroeconomic factors for further direction.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Market Update – Asian Session: TPP Moves Ahead Without US As Trump Wraps Up Visit To Asia

Asia Summary

Following the declines seen in US equity markets on Friday's session, Asian bourses have opened mixed.

In South Korea, cosmetics companies (including Amorepacific, LG Household and Cosmax) have traded higher, as companies release their sales figures from China's ‘Singles Day.' Alibaba reported that its gross merchandise value related to the annual shopping festival rose by 39% y/y to $25.3B. Japan's Fast Retailing has declined by more than 1.5%.

Steelmakers in Japan are also trading lower, with shares of Nippon Steel down by over 2%. In Australia, the ASX 200 Resources Index has risen by over 0.5%, after declining by 1.6% on Friday's session. At the same time, the Hang Seng Materials index has declined by more than 0.7%. Shares of Aluminum Corp of China have declined by more than 1.4%, while Rusal has moved lower by over 1% following the release of its earnings report .

Property developer, Country Garden, has gained over 7% in Hong Kong, as the company is due to be added to the Hang Seng index. Sunny Optical Technology, which is also due to be added to the index, has traded higher by more than 4%. Meanwhile, shares of Cathay Pacific and Kunlun Energy are trading lower by over 1% and 2.5% respectively, as both firms are due to be removed from the Hang Sang index.

At the same time, the Hang Seng Information Technology index has rallied by more than 1%. Shares of PC gaming firm Razer have moved higher by over 40% in their trading debut. Japanese online gaming firm Nexon has gained over 7%, following the release of its earnings report and guidance.

Amid today's decline being seen in Japanese equity markets, the Topix Securities broker index has lost over 1%. Mega banks are also trading slightly lower, ahead of Mizuho Financial's earnings release, which is expected later today. The Hang Seng Financials index has risen by more than 0.5%, amid the gains being seen in China's bond yields.

China's 10-year bond yield has risen to highs not seen since 2014. While today's session, has been fairly light in terms of macro-economic data, various data points are due to be released by China's on Tuesday's session including, October Retail Sales, Industrial Production at Fixed Assets Investment.

In the currency markets, the US dollar is trading generally firmer. Data releases for the US include, Oct CPI and Retail Sales, which are both expected on Wednesday

GBP/USD has declined by over 0.5%. Forty UK MPs are said to have agreed to sign a letter of no confidence in PM May, according to a UK press report. Forty eight signatures are required to force a leader ship vote. The most recent report on PM May, followed prior reports that there were over two dozen parliament members that were said to be prepared to call for her to resign.

In Australia, the Q3 wage price index is due to be released on Wednesday, while the Oct Employment Change is expected to be released on Thursday.

In Japan, preliminary Q3 GDP data is due to be released on Wed.

Japanese companies expected to report earnings today include Aeon Financial Service, Aozora Bank, Ebara Corp, Funai Electric, Fukuoka Financial, Fukushima Industries, Hamamatsu Photonics KK, Hirata, Hokuetsu Paper, Hokuhoku Financial, J Trust, Kenedix, Kinetsu Corp, Juroku Bank, Konoike Transport, Mizuho Financial, Noritz Corp, Rakuten, Sawai Pharmaceuticals, Senshu Ikeda Holdings, Sumitomo Bakelite, T&D Holdings, THK, TPR, Taikisha, Takasago Thermal Eng, Temp Holdings, Toridoll Company and Towa Pharmaceuticals.

Key economic data

(KR) SOUTH KOREA OCT EXPORT PRICE INDEX M/M: 0.5% V 1.1% PRIOR; Y/Y: 8.0% V 11.2% PRIOR; Import Price Index M/M: 0.6% v 1.8% prior; Y/Y: 6.8% v 10.8% prior

(JP) JAPAN OCT PPI (CGPI) M/M: 0.3% V 0.1%E; Y/Y: 3.4% V 3.1%E

Speakers and Press

Japan

(JP) Follow Up: TPP members made significant progress toward reaching a major trade pact (without the US) but disagreements from Canada prevented a final deal – press

(JP) Ministerial meeting of Regional Comprehensive Economic Partnership (RCEP) member states concluded that negotiations will continue into 2018 rather than reaching an agreement this year - Nikkei

Korea

(KR) South Korea Foreign Min Kang: North Korea needs to show signs of change before any talks

Philippines

(PH) Philippines Central Bank (BSP) Gov Espenilla: Policy makers are considering slowly cutting banks' reserve requirements

China/Hong Kong

(CN) President Trump: Expressed strong desire to conduct trade on a fair basis; will make bilateral trade deals with any APEC nation (Friday)

Australia/New Zealand

(AU) RBA Assist Gov Debelle: now appears that there has been a solid upward trajectory in non-mining business investment over the past couple of years

Outside Asia

(UK) 40 MPs have agreed to sign a letter of no confidence in PM May, short of number required to force leadership vote (48 required) - UK press

(US) Fed's Harker (voter, hawk): Lightly penciled in Dec rate hike; Inflation weakness has been puzzling

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.5%, Hang Seng +0.3%; Shanghai Composite +0.3%; ASX200 -0.3%, Kospi -0.5%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.2%, Dax +0.1%; FTSE100 +0.3%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1668-1.1645; JPY 113.71-113.47; AUD 0.7664-0.7642;NZD 0.6936-0.6916

Dec Gold +0.1% at $1,275/oz; Nov Crude Oil +0.1% at $56.77/brl; Dec Copper +0.4% at $3.09/lb

USD/CNY (CN) PBOC sets yuan reference rate at 6.6347 v 6.6282 prior

(CN) PBoC OMO: CNY180B v CNY80B injected in 7, 14 and 63-day reverse repos prior; Net injection CNY150B v CNY50B prior

(KR) South Korea sells 10-yr pre-issuance Govt bonds at 2.61%

(KR) Bank of Korea (BOK) sells KRW400B in 1-yr monetary stabilization bonds at 1.87%

Equities notable movers

Australia/New Zealand

BLY.AU Reports Q3 (A$) Adj Net loss 3.0M v loss 23M y/y Rev 199M v 175M y/y; +18%

MLD.AU Trading update: revenue in line with expectations, earnings adversely affected by under-performing contracts; -21%

Japan

UBER.IPO Confirms investment by consortium led by Softbank

5706.JP Reports Q2 Net profit ¥5.82B v ¥5.90Be, Op profit ¥12.1B v ¥11.4Be; +14%

China/Hong Kong

2007.HK Country Garden added to Hang Seng Index; +7.5%

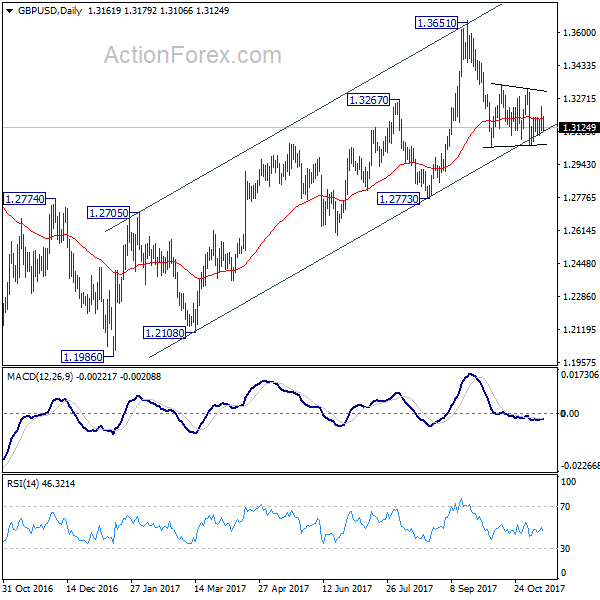

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3124; (P) 1.3177; (R1) 1.3241; More....

GBP/USD drops sharply as the week starts. But it's staying in range of 1.3026/3337 as consolidation continues. Intraday bias remains neutral at this point. Upside of recovery should be limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Sterling Plummets as Theresa May Steps Closer to Leadership Challenge

Sterling tumbles broadly as another week starts on political concerns. Prime Minister Theresa May's position is getting shaky as more MPs are getting impatient with her. Brexit Secretary David Davis dismissed EU's two week deadline and warned that no number nor formula would be provided on the divorce bill. On the other hand, Dollar gains broadly as riding of Friday's surge in treasury yields. For the time being, most pairs and crosses are stuck in recently established range. But with a heavy calendar ahead, and news on US tax plan, Brexit negotiation and German coalition, volatility is anticipated.

40 Conservatives MPs ready to channel PM May

It's reported that the Conservatives are getting more impatient with Prime Minister Theresa May. And, up to 40 Conservative MPs are ready to challenge May's leadership by signing a letter of no confidence. If eight more MPs are going to join, the letter would trigger a vote of no confidence, which could eventually leader to a leadership contest. Situation for May worsened sharply since the shambolic Conservative conference speech. And the list against her grew week by week after loss of Michael Fallon and Priti Patel in the cabinet.

Brexit Davis warned EU: No number or formula on divorce bill

Regarding Brexit negotiations with EU, Brexit Secretary David Davis dismissed the two-week deadline set of EU's chief negotiator Michel Barnier. Davis said that "in every negotiation each side tries to control the timetable. The real deadline on this, of course, is December. It's the December council. One of the key sticky point of the negotiation is that according to EU, "sufficient progress" is needed before moving on to the next stage in trade agreement talks. The divorce bill has to be settled before calling the progress "sufficient". But Davis said that the EU "invented this phrase" and "it's in their control what it really is". Also, he warned EU that "you won't have a number or a formula before we move on to the next stage".

German Merkel urges compromise in coalition talks

German Chancellor Angel Merkel urged party leaders to show willingness to compromise in the three-way coalition talks. The phase of exploratory talks is nearly completed and the CDU, FDP and Greens are expected to start serious negotiations. Merkel said that "from my point of view, a solution can be reached with goodwill". And, she added that "if this will be achieved, we'll not know before the end of the week, however." Merkel targets to agree with the coalition partners in principle to move on by November 16. Separately, latest survey by Emnid for Bild am Sonntag newspaper showed support for Merkel's CDU/CSU dropped to lowest level since October 2011. Only 30% of Germans would vote for CDU/CSU if there were a federal election this Sunday.

Fed Harker: "Lightly penciled in" a December rate hike

Philadelphia Fed Patrick Harker said today that he has "lightly penciled in" a December rate hike. He noted in Tokyo that "removing accommodation is the right next step". He forecast that unemployment will "drop below 4% probably late 2018 or early 2019". And that should "p[ut pressure on wages", thus, lift inflation back to target. But he emphasized the word "should" as "we've been predicting this for a while and it hasn't happened".

RBA Debelle: Solid upward trajectory in non-mining business investment

RBA Deputy Governor Guy Debelle said "there has been a solid upward trajectory in non-mining business investment over the past couple of years." Also, there is starting to be a "change in mindset from the corporate sector around the willingness to invest, around the willingness to hire." And, that "gives you some hope that eventually we might get into a world where we start to see those wage price pressures emerge." But he also reiterated the central bank's stance to stand pat until upward pressure in wages or inflation starts to emerge.

On the data front

Japan Domestic CGPI rose 3.4% yoy in October. UK Rightmove house price dropped -0.8% mom in November. Germany will release WPI later today. Looking ahead, the calendar is very busy this week and there are a lot of market moving indicators. Here are some highlights for the week:

- Tuesday: Australia NAB Business Confidence; China retail sales, fixed asses investment, industrial production; German GDP; Italy GDP; Eurozone GDP, industrial production. ZEW sentiment; Swiss PPI; UK CPI, PPI; US PPI

- Wednesday: Japan GDP; Australia wage price index; UK employment; Eurozone trade balance; US CPI, retail sales, Empire state manufacturing, business inventories

- Thursday: Australia employment; UK retail sales; Eurozone CPI final; Canada manufacturing sales; US jobless claims, Philly Fed survey, import price, industrial production, NAHB housing

- Friday: New Zealand PPI, business manufacturing index; Eurozone current account; Canada CPI; US housing starts

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3124; (P) 1.3177; (R1) 1.3241; More....

GBP/USD drops sharply as the week starts. But it's staying in range of 1.3026/3337 as consolidation continues. Intraday bias remains neutral at this point. Upside of recovery should be limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Oct | 3.40% | 3.10% | 3.00% | 3.10% |

| 00:01 | GBP | Rightmove House Prices M/M Nov | -0.80% | 1.10% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Oct P | 45.00% | |||

| 07:00 | EUR | German Wholesale Price Index M/M Oct | 0.60% | |||

| 19:00 | USD | Monthly Budget Statement Oct | -58.2B | 8.0B |

Market Morning Briefing: The Euro Remains Below 1.1665-1700

STOCKS

Dow (23422.21, -0.17%) is coming off from medium term resistance on the 3-day candlescoming from Feb’17 and the corrective dip is likely to last for some more time heading towards 22800 in the medium term. A break above immediate resistance could take it up towards 24000.

Dax (13127.47, -0.42%) is currently in the corrective dip phase and is likely to test decent support near 13000-12900 from where a small rise is possible before resuming the longer term fall towards levels below 12900. Immediate view remains bearish.

Nikkei (22527.21, -0.68%) made a high of 23382.14 on Wednesday last week and has been coming off thereafter. Near term top formation seems to have been completed, paving way for testing lower levels of 22250 and lower in the coming sessions.

Shanghai (3443.75, +0.32%) is firmly up unlike the other major indices. While above 3440, the index looks bullish and is likely to move up this week towards 3475 and maybe higher.

Nifty (10321.75, +0.12%) may test immediate support near 10250 which could produce a slight bounce back to 1040 or higher levels. A fall below 10250 could take it lower to test 10100.

COMMODITIES

Support near 1270-1260 region is holding well for Gold (1276.60) and while that holds, an eventual rise towards 1300 is possible in the coming sessions. Sideways trade within 1300-1260 region is possible for some sessions.

Brent (63.56) has immediate resistance near 65 which is likely to hold for some time keeping the price range-bound within 63-65 region. Thereafter upside levels of 66-67 would open up and leave a 50-50% chance of either moving up towards 66-67 or come down to test 62-61 levels.

WTI (56.80) could trade in the 56-58 region for the coming sessions. Upside chances of testing 59 looks possible. A break below 56, if seen could open up chances of a fall towards 55 in the longer run,

Copper (3.0860) is testing support just at current levels and if that holds, the price could bounce back towards 3.15-3.20 else could initiate a fall towards 3.

FOREX

Overall, the Dollar Index (94.53) has been able to maintain its strength from Friday, with all currencies trading a tad weaker against the US Dollar. Decent Support seen in the 94.35-20 region, with chances of new rise towards 95+ in the next couple of weeks.

The Euro (1.1650) remains below 1.1665-1700 as the German-US 10Yr Spread (-2.01%, see Interest Rates below) fall again. Further Resistances seen in the 1.1725-45 region.

We have to consider chances of new rise in the Dollar-Yen (113.67) given that the crucial Support at 113.00 mentioned on Friday has held well and the US yields have risen sharply. For now, look for a sideways range of 113.10-114.40 over the next few days.

The Euro-Yen (132.47) is likely to trade sideways as well, suggesting that both the Euro and Yen are likely to rise/ fall in unison against the Dollar, suggesting again that the market is likely to see Dollar-centric trading for some days.

Dollar-Yuan (USDCNY = 6.4910%) trying to rise further. Look for strong upside if 6.65-66 is broken. Dollar-Rupee (65.1650) may test 65.20-30 in the near term and then come off a bit.

INTEREST RATES

Good rise in US yields in the run up to the US CPI data for Oct on Tuesday. The US 5Yr (2.05%), 10Yr (2.39%) and 30Yr (2.87%) have all moved up sharply. It will be interesting to see how the yields rise past their respective May '17 highs. At the short end, the US 2Yr (1.66%) continues to be on a tear, rising steadily from 1.26% on 8th September.

As expected, the German-US 10Yr (-2.01%) has come off sharply from the Resistance at -1.97% mentioned on Friday.

Sharp rise in the US-Japan 10Yr Spread (2.34%) on the back of the rise in US yields. May look for levels above 2.40%.

Did OPEC Just Admit Defeat In The Shale Oil Wars?

Key Points:

- OPEC quietly admits that its Shale Oil Strategy has failed.

- ULCC static off Oman since 2015 offloads oil.

- Imagery suggests Saudi Arabia could be fudging their inventory storage numbers

The past week has been relatively interesting on the Crude Oil news front as OPEC quietly released their 'World Oil Outlook' report. As usual, the cartel largely shrugged off the growing risk around the arrival of peak oil demand and largely painted a picture of improving price stability. However, what was particularly illuminating is the fact that the cartel drastically revised upward their assessment of U.S. shale oil production. Subsequently, the question remains if OPEC is finally ready to admit defeat in their strategy to crush shale oil producers.

Surprisingly, it was only just last year that OPEC was pushing the narrative that shale oil production would be damaged by their strategy of flooding the markets with cheap oil. In fact, the cartel was almost smug in their view that shale production would continue to fall and by 2021 represent only 4.8 mb/d.

However, clearly this hasn't happened and new technology in shale production centres has increased productivity and the marginal cost of extraction for U.S. producers. Subsequently, even OPEC has now suggested in their latest modelling that they see shale output rising to around 7.5 mb/d by 2021. This is a whopping near 50% upward revision of shale output and quietly suggests that the cartel is finally abandoning the notion that they can drive U.S. shale producers out by flooding the market with supply.

Subsequently, the likelihood of OPEC extending their production caps well into next year is relatively strong but it remains to be seen if it will actually be effective in establishing higher oil prices. In fact, some interesting tidbits of intelligence released over the past week seem to suggest that not all is well in the land of Middle Eastern oil producers.

Last week also saw the FT reporting that satellite imagery showed the offloading of one of the largest tankers in the world, a ULCC that has been stationary off Oman since 2015. The crude was apparently being stored afloat for prices to increase to an advantageous level before being sold into the market. Subsequently, this may be an interesting sign that some of the biggest players in crude markets are looking at the present market and seeing prices forming a top.

In addition, the satellite imagery also shows a major oil storage facility in Saudi Arabia may actually have greater inventory than first thought (or reported). In a case of, a picture never lies, it would seem apparent that crude stocks have actually been rising at the facility in contrast to the official reports of a fall in inventories by over 70 million barrels since 2016. Subsequently, there is plenty of scope to disbelieve the Kingdom when it comes to both their production and storage figures.

Ultimately, the current drive in prices is largely being fuelled by rising geopolitical risk within the House of Saud. Clearly, the purge that has gone on recently has seen prices spike due to many of the people that were considered as impediments to extending production caps having been removed from their respective positions. These actions have seen plenty of speculation of WTI prices trading north of the $60.00 handle. However, it may really just be a case of the ‘emperor has no clothes' as OPEC quietly admits that their strategy to crush shale oil has proved to be an unmitigated disaster. Subsequently, watch for a correction in crude prices over the next month as the market returns to the reality that is the ongoing rebalancing within crude oil markets