Sample Category Title

EUR/GBP: EU Industrial Production

The EUR/GBP exchange rate decreased on the report showing stronger-than-expected growth in the EU industrial production. The Euro lost against the British Pound 11 base points, but then jumped to be seen trading above the 0.9000 mark. After the ECB President Mario Draghi delivered his speech, the pair fell and continued consolidation nearing the 0.8920 level.

The Eurostat reported that the growth of industrial production in the Euro area expanded to the nine-month high over the course of August, revealing a 1.4% climb versus 0.5% expected. The improvement in the EU industrial output pointed to the sector's strong growth in the Q3, which is likely to support healthy economic recovery.

EUR/USD: US Producer Prices Index

The Euro fell slightly against its American counterpart, reflecting an anticipated increase in the US producer prices. The EUR/USD exchange rate edged 10 base points lower to the 1.1844 mark to continue temporary depreciation, though the pair passed across the 1.1850 area again on Friday morning.

The Labour Department revealed that the US Producer Price Index climbed 0.4% in September. Data suggested the growth fuelled by higher gasoline prices, as they marked the strongest rise in two years due to production disruptions in Texas oil refineries caused by Hurricane Harvey. Moreover, the gain is set to bolster the Fed's case for the next rate hike this year despite sluggish inflation readings.

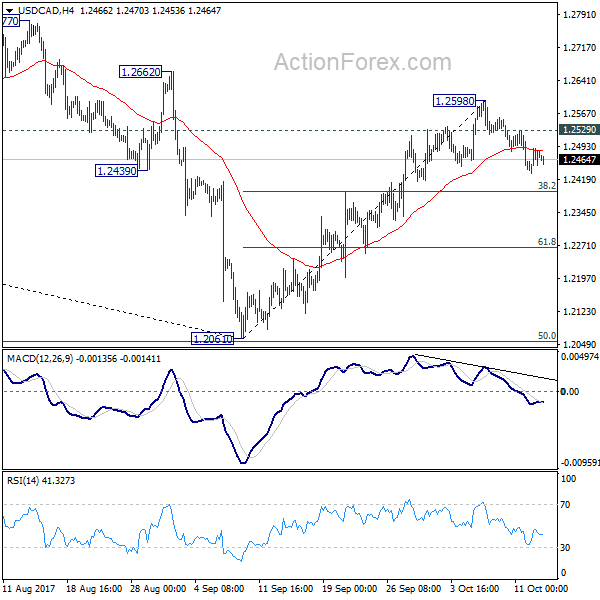

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2440; (P) 1.2465; (R1) 1.2498; More....

At this point, pull back from 1.2598 short term top is expected to extend lower to 38.2% retracement of 1.2061 to 1.2598 at 1.2393, or even further to 61.8% retracement at 1.2266. But we'll look for bottoming sign below 1.2266. On the upside, break of 1.2529 minor resistance will resume the rise from 1.2061 for 1.2777 resistance.

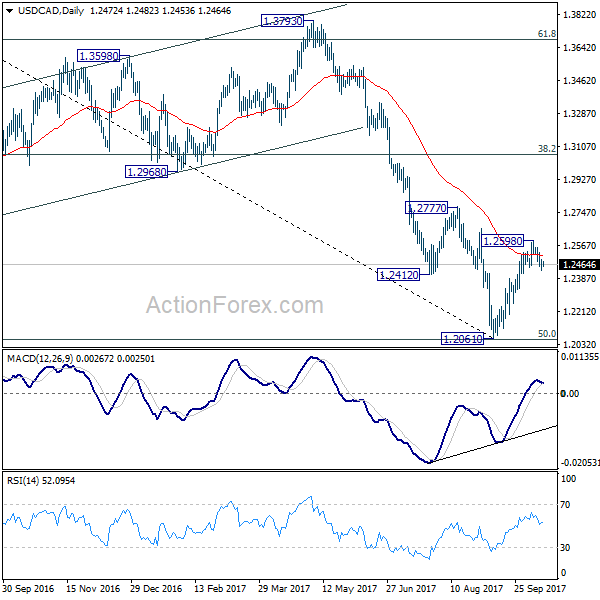

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

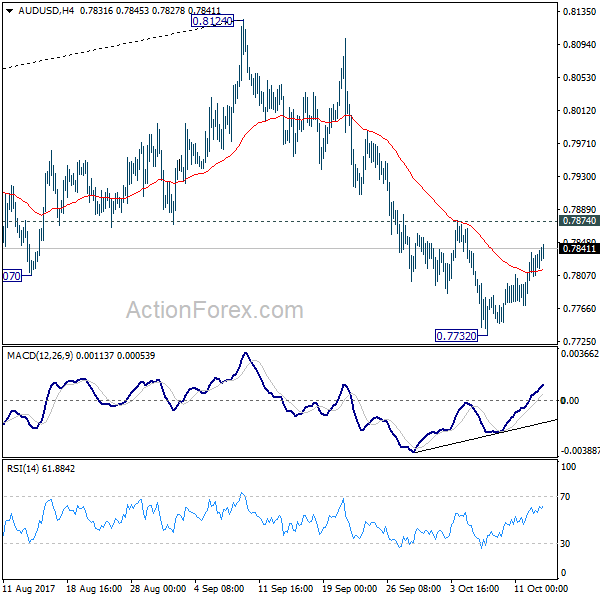

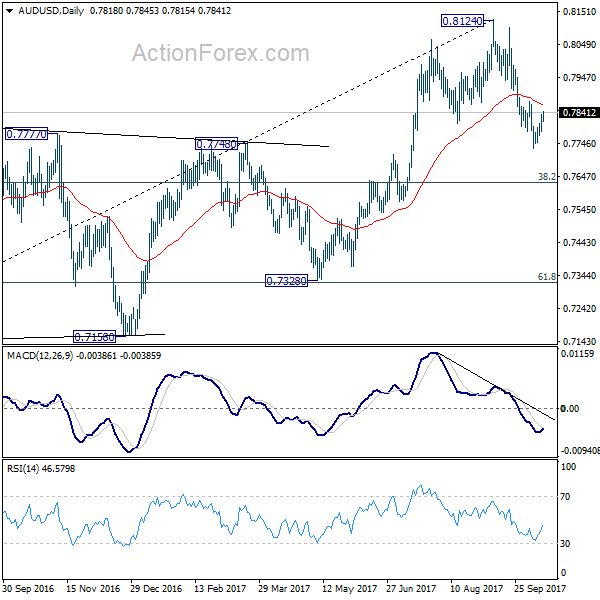

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7792; (P) 0.7813; (R1) 0.7843; More...

Intraday bias in AUD/USD remains neutral for consolidation above 0.7732 temporary low. Another fall is expected as long as 0.7874 resistance holds. As noted before, rise from 0.7382 is possibly completed at 0.8124 already. Below 0.7732 will target medium term fibonacci level at 0.7628 first. Decisive break there will target 0.7328 key cluster support. On the upside, break of 0.7874 will argue that the decline is completed and turn bias back to the upside.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will firm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

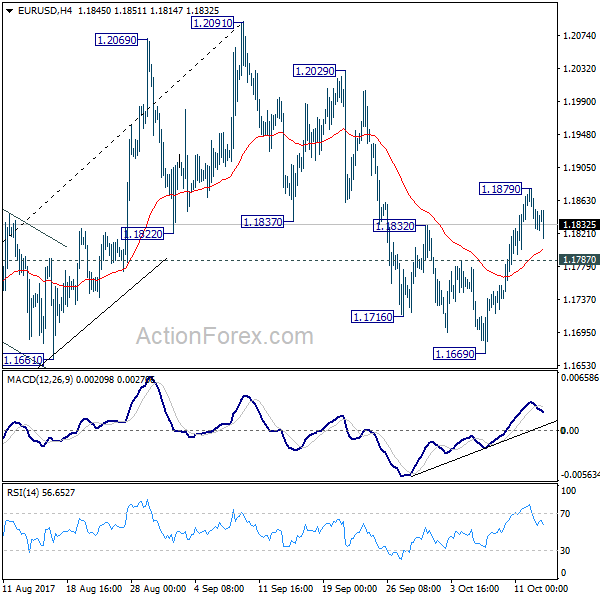

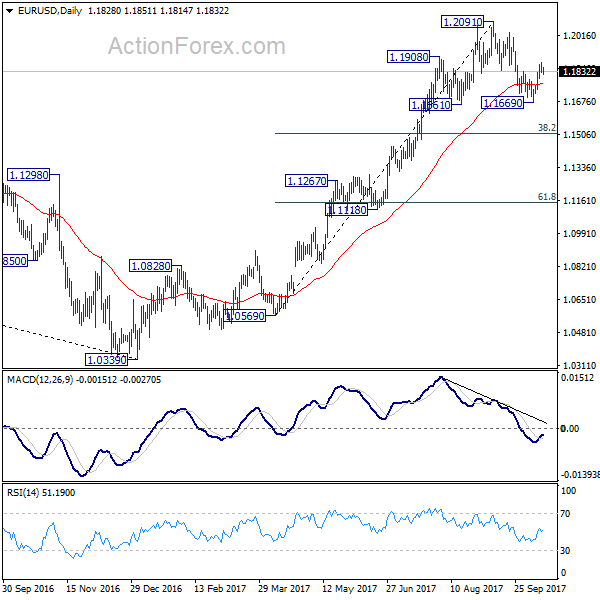

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1811; (P) 1.1845 (R1) 1.1864; More...

A temporary top is in place at 1.1879 in EUR/USD and intraday bias is turned neutral first. Another rally is mildly in favor as long as 1.1787 minor support holds. As noted before, pull back from 1.2091 should have completed at 1.1669, ahead of 1.1661 support. Above 1.1879 will target a test on 1.2091 high. Nonetheless, break of 1.1787 will likely extend the corrective fall from 1.2091 through 1.1669 instead.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

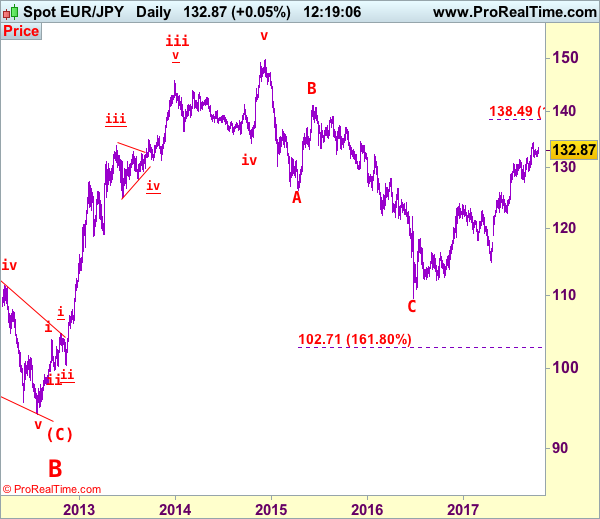

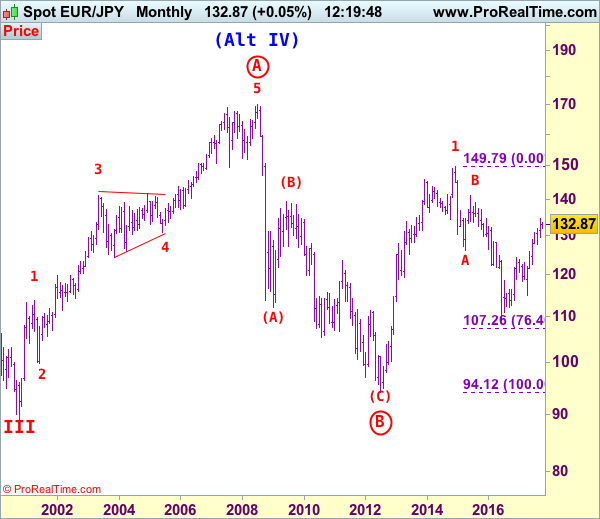

EUR/JPY Elliott Wave Analysis

EUR/JPY - 132.75

The single currency rebounded after holding above indicated support at 131.75, however, euro met resistance at 133.50 and has retreated again, suggesting further sideways consolidation would take place, however, as long as said support at 131.75 holds, bullishness remains for another rebound to 133.50, then towards 134.00 but break of recent high of 134.41 is needed to confirm upmove has resumed and extend further gain to 135.00 but loss of upward momentum should prevent sharp move beyond 136.00-10 and reckon 136.95-00 would hold, price should falter well below 138.45-50 (1.618 times extension of 109.49-124.10 measuring from 114.85).

The daily chart is labeled as attached, early selloff from 169.97 (July 2008) to 112.08 is wave (A) of B instead of end of entire wave B and then the rebound from there to 139.26 is wave (B), hence, wave (C) has possibly ended at 94.12 with a diagonal triangle as labeled in the daily chart, hence upside bias is seen for further gain. Recent rally above indicated retracement level at 116.69 (50% Fibonacci retracement of the intermediate fall from 139.26-94.12) adds credence to this view and signal major reversal has commenced but first leg of this wave C has possibly ended at 149.79, hence wave 2 has commenced with wave A ended at 126.09, followed by wave B at 141.06, wave C commenced and could have ended at 109.49, indicated upside targets at 126.00 and 130.00 had been met and further gain to 135.00 would follow.

On the downside, whilst initial pullback to 132.20-25 cannot be ruled out, still reckon said support at 131.75 would hold and bring another rebound. Only a break below this level would signal a temporary top is formed, bring retracement of recent rise to 131.00 and possibly test of support at 130.62 but downside should be limited to 130.00 and strong support at 129.37 should remain intact, bring another upmove later.

Recommendation: Hold long entered at 132.70 for 135.00 with stop below 131.70.

To re-cap the corrective upmove from the record low of 88.93 (18 Oct 2000), the wave A from there is subdivided as: 1:88.93-113.72, 2:99.88 (1 Jun 2001), 3:140.91 (30 May 2003), 4:124.17 (10 Nov 2003) and 5 ended at record high of 169.97 (21 Jul 2008). The brief but sharp selloff to 112.08 is viewed as a-b-c x a-b-c wave (A) of B. The subsequent rebound to 139.26 is (B) of B and (C) of (B) has possibly ended at 94.12 and in any case price should stay well above previous chart support at 88.93, bring rally in larger degree wave C towards 150.00.

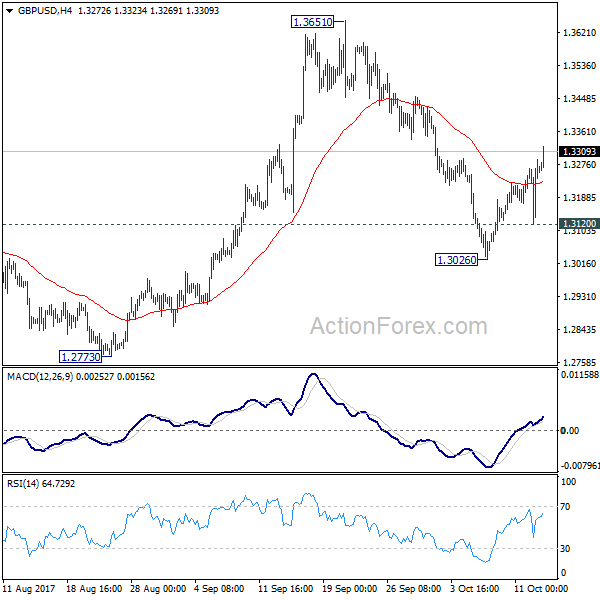

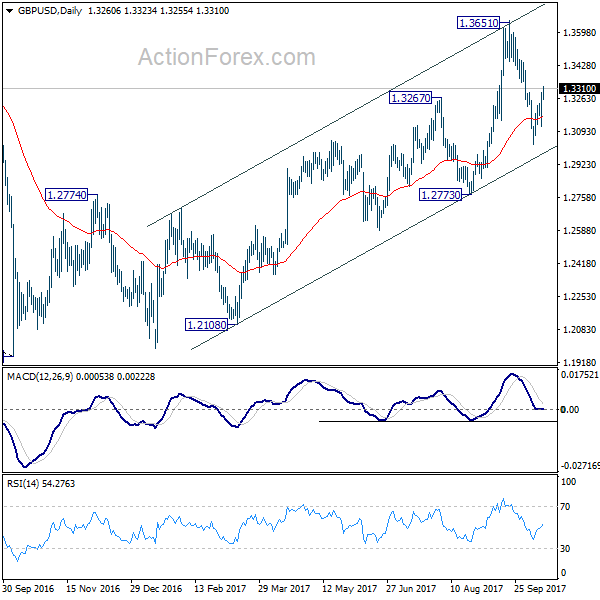

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3160; (P) 1.3225; (R1) 1.3329; More....

GBP/USD's rebound from 1.3026 extends to as high as 1.3323 so far. The break of 1.3291 resistance argues that pull back from 1.3651 is completed at 1.3026. Intraday bias is turned back to the upside for retesting 1.3651 high. Decisive break there will resume whole medium term rally from 1.1946 and target 1.3835 key resistance next. On the downside, below 1.3120 minor support will resume the fall from 1.3651 through 1.3026 instead.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll turn neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

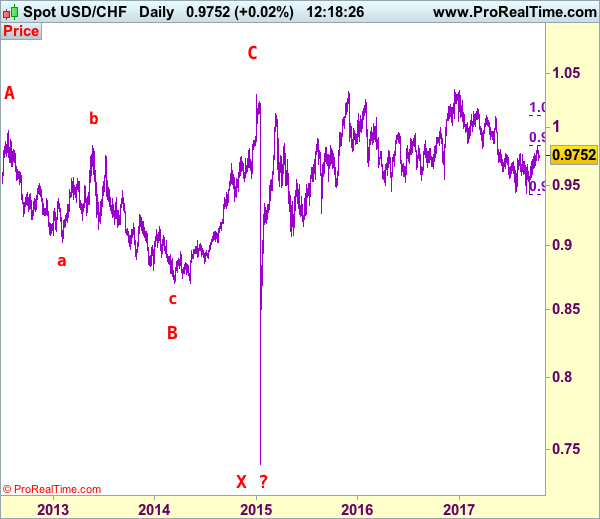

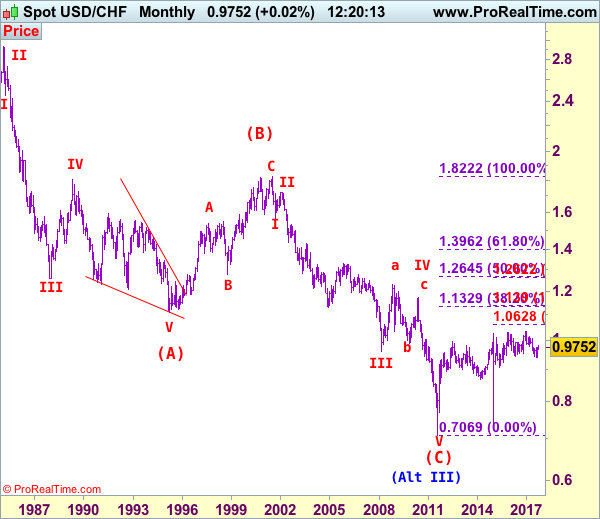

USD/CHF Elliott Wave Analysis

USD/CHF – 0.9751

As the greenback has retreated after rising to 0.9837 late last week, suggesting consolidation below this level would be seen and pullback to 0.9700, then 0.9640-45 cannot be ruled out, however, as temporary low has been formed earlier at 0.9421, reckon downside would be limited to support at 0.9565 and bring another rebound later. Above 0.9800 would signal the pullback from 0.9837 has ended, bring retest of this level, then test of previous support at 0.9859, having said that, overbought condition should limit upside to 0.9900 and price should falter well below psychological resistance at 1.0000, bring another decline later.

Our preferred count on the daily chart is that early selloff to 0.9630 is an end of the larger degree wave III and major correction is unfolding from there with a leg ended at 1.2298 (Nov 2008 with (a): 1.0625, (b):1.0011 and (c):1.2298), wave b ended at 0.9910 with (a): 1.0370, (b): 1.1967, (c): 0.9910. The rise from there to 1.1730 is the wave c which also marked the end of wave IV and wave V has possibly ended at 0.7068.

On the downside, whilst initial pullback to 0.9700 and 0.9645-50 is likely, reckon downside would be limited to said support at 0.9565 and bring another rise later. Below 0.9525-30 would risk weakness to 0.9490-00 but still reckon downside would be limited to 0.9455-60 and said support at 0.9421 should remain intact, bring another rebound later. A drop below said support at 0.9421 would extend recent decline from 1.0344 top (formed back in late 2016) to 0.9350 and possibly 0.9300, however, loss of downward momentum should prevent sharp fall below 0.9250-60 and 0.9200-10 should hold.

Recommendation: Buy at 0.9575 for 0.9775 with stop below 0.9475.

Dollar's long-term downtrend started from 2.9343 (Feb 1995) and it was unfolding as a (A)-(B)-(C) with (A): 1.1100, (B): 1.8310 (26 Oct 2000), then followed by another impulsive wave (C) with wave III ended at 0.9630 (Mar 2008). Under this count, correction in wave IV has possibly ended at 1.1730 and wave V already broke below support at 0.9630 and met indicated downside target at 0.7500 and 0.7400. The reversal from 0.7068 suggests the wave V has possibly ended and the breach of resistance at 0.9595 add credence to this view and indicated upside target at 1.0000 had been met, however, the sharp retreat from 1.0296 to 0.7401 suggests choppy trading would be seen but price should stay above said record low at 0.7068.

Trade Idea: GBP/USD – Hold short entered at 1.3315

GBP/USD – 1.3313

Original strategy :

Sold at 1.3315, Target:1.3115, Stop: 1.3375

Position: - Short at 1.3315

Target: - 1.3115

Stop: - 1.3375

New strategy :

Hold short entered at 1.3315, Target:1.3115, Stop: 1.3375

Position: - Short at 1.3315

Target: - 1.3115

Stop:- 1.3375

As cable found decent demand at 1.3121 yesterday and staged a strong rebound, suggesting near term upside risk remains and marginal gain from here cannot be ruled out, however, as this move from 1.3027 low is still viewed as retracement of recent decline, reckon upside would be limited to previous support at 1.3343 and bring retreat later, below 1.3245 would bring weakness to 1.3195-00 but only break of said support at 1.3121 would signal the rebound from 1.3027 has ended, bring weakness to 1.3065-75, then retest of said support at 1.3027.

In view of this, we are holding on to our short position entered at 1.3315. Above previous support at 1.3343 would abort and signal low has been formed instead, bring at least a correction of the fall from 1.3658 top to 1.3390-00 later. Our preferred count is that (pls see the attached chart) the wave IV is unfolding as a complex double three (ABC-X-ABC) correction with 2nd wave B ended at 1.2774, hence 2nd wave C could have ended at 1.3658.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

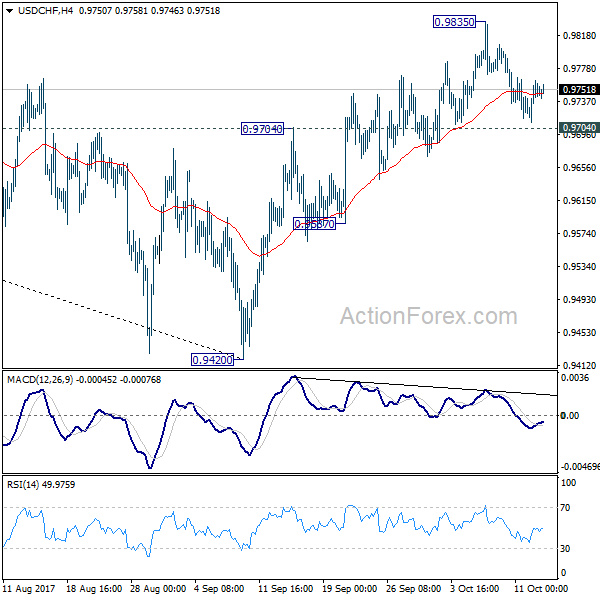

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9722; (P) 0.9742; (R1) 0.9774; More....

Intraday bias in USD/CHF remains neutral at this point. Considering bearish divergence condition in 4 hour MACD, break of 0.9704 resistance turned support will argue that rebound from 0.9420 has completed. This will also mixed up the near term outlook and turn bias back to the downside for 0.9587 support. Meanwhile, break of 0.9835 temporary top will extend the rebound to 61.8% retracement of 1.0342 to 0.9420 at 0.9990.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.