Sample Category Title

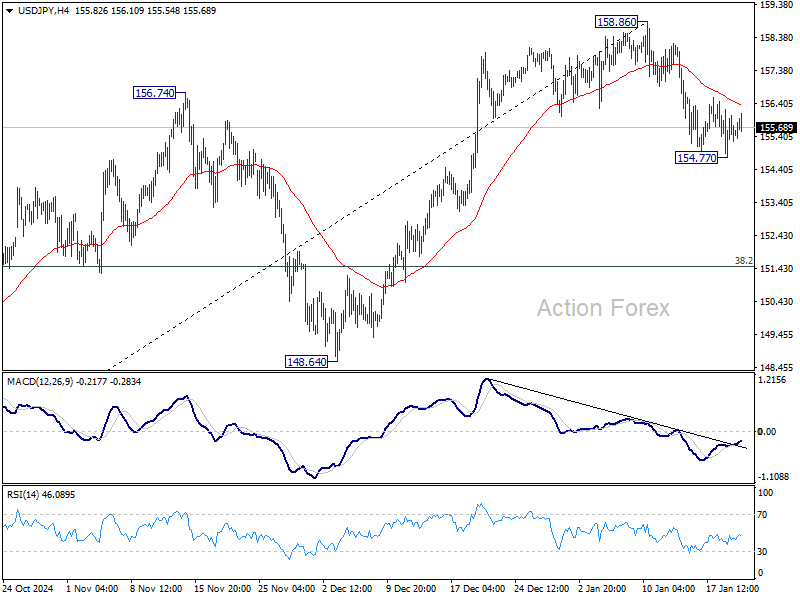

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.78; (P) 155.51; (R1) 156.24; More...

Intraday bias in USD/JPY is turned neutral on loss of momentum, as seen in 4H MACD. But risk will stay on the downside as long as 158.86 short term top holds. Sustained trading below 55 D EMA (now at 154.64) will extend the fall from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

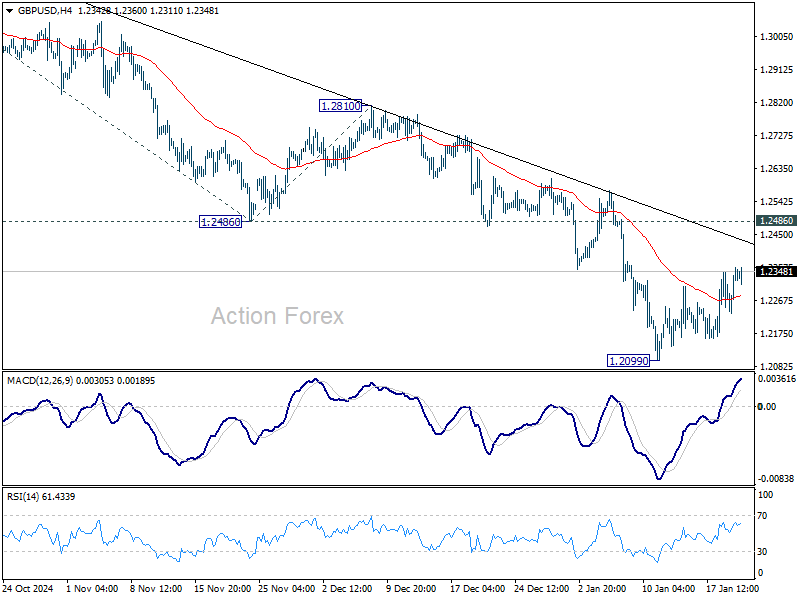

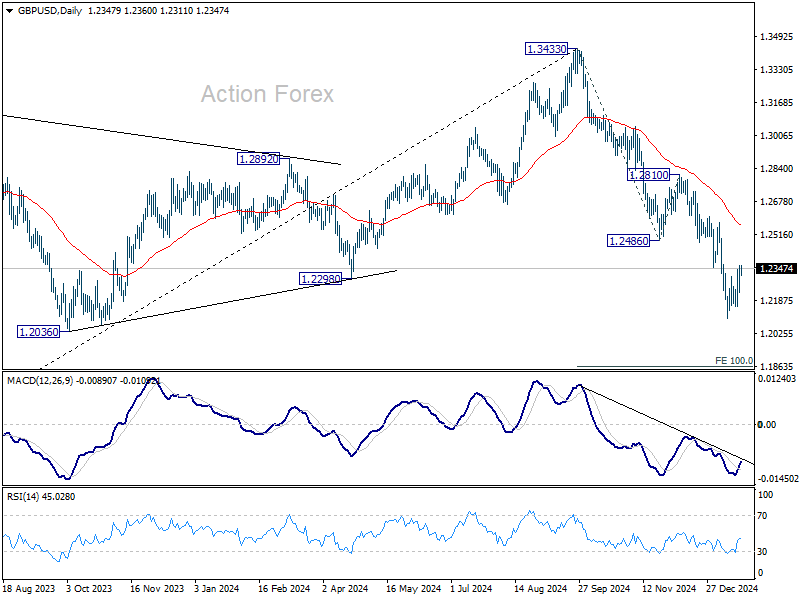

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2267; (P) 1.2313; (R1) 1.2398; More...

GBP/USD is staying in consolations above 1.2099 and intraday bias stays neutral. Further decline is expected with 1.2486 support turned resistance intact. On the downside, break of 1.2099 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

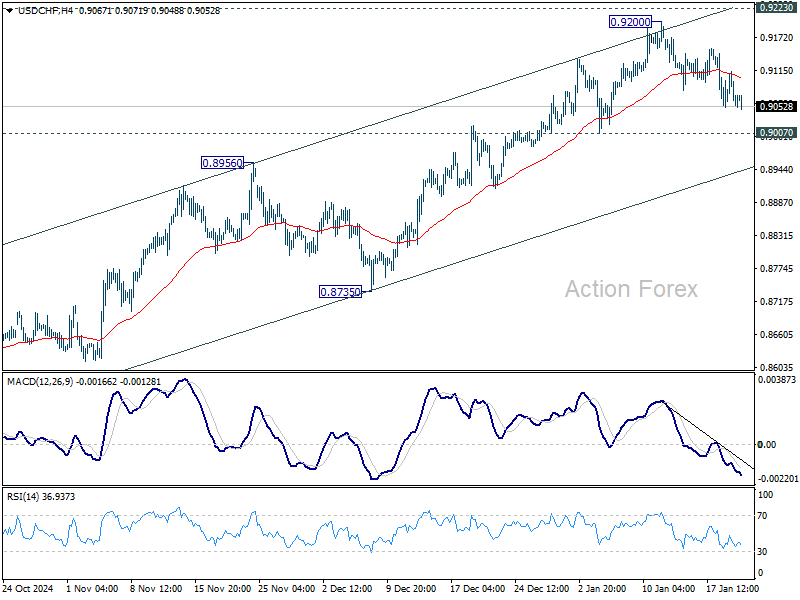

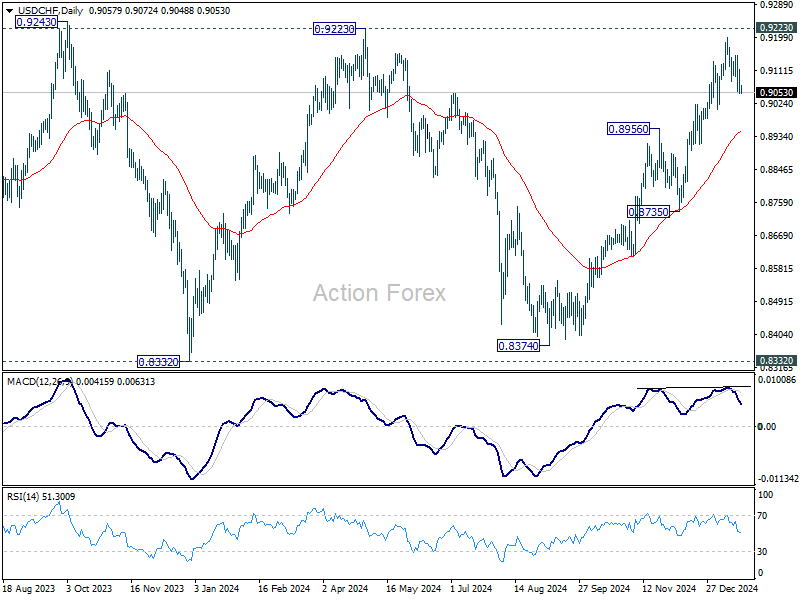

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9032; (P) 0.9077; (R1) 0.9102; More…

Intraday bias in USD/CHF remains neutral and outlook is unchanged. Intraday bias stays neutral for consolidations below 0.9200. Further rally is expected with 0.9007 support intact. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 0.8950).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4236; (P) 1.4377; (R1) 1.4464; More...

Intraday bias in USD/CAD remains neutral as range trading continues. Further rise is expected as long as 1.4260 support holds. Break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.4203) and below.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

Kiwi Eases as NZ CPI Backs RBNZ 50bps Cut, Dollar Unmoved by Trump’s Continuous Tariff Talks

New Zealand Dollar softened mildly today as Q4 inflation data reinforced the case for continued monetary easing by RBNZ. The central bank has ample room to swiftly bring interest rate from the current 4.25% to neutral, with inflation staying at around mid-point of 1-3% target range for the second straight quarter.

Another 50bps rate cut on February 19 should be solidified. However, beyond this, the scale further rate reductions by RBNZ will depend heavily on domestic disinflationary progress, especially in non-tradeable prices, as the effects of falling tradeable prices fade.

Elsewhere, Dollar's pull back this week have slowed, but it has yet to stage a convincing recovery. President Donald Trump’s ongoing rhetoric on tariffs continued to draw attention but had little immediate impact on markets. Trump reiterated yesterday his intention to impose a 10% tariff on China, accusing it of enabling fentanyl shipments through Canada and Mexico to the US. He also repeated his threat to target EU with tariffs, calling it the “only way” to achieve trade "fairness". Markets, however, appeared unfazed, awaiting concrete actions to back Trump’s statements.

Key dates for tariff announcements include February 1, when decisions on 25% tariffs for Canada and Mexico and 10% tariffs on China are expected. For other countries, tariff measures may be delayed until federal trade reviews conclude on April 1. With no immediate actions, Trump’s remarks seem more rhetorical than actionable.

In terms of weekly performance so far, Dollar remains the weakest major currency, followed by Yen and Swiss Franc, reflecting a risk-on sentiment across US and European markets. Kiwi continues to lead gains despite today’s pullback, with Euro and Sterling following suit. Aussie and Loonie are mixed in middle positions.

Technically, a short term bottom is formed at 0.5540 in NZD/USD, just ahead of 0.5511 (2022 low). More consolidations would be seen with risk of stronger recovery. But as long as 55 D EMA (now at 0.5751) holds, larger down trend is expected to resume through 0.5511/40 sooner rather than later. Nevertheless, strong break of 55 D EMA will bring further rebound to 38.2% retracement of 0.6378 to 0.5540 at 0.5860, as the corrective pattern lengthens.

ECB’s Knot supports near-term rate cuts, not convinced of of stimulus mode

Dutch ECB Governing Council member Klaas Knot expressed agreement with market expectations for rate cuts at the January and March meetings, saying he is “pretty comfortable” with them. However, he added it is "too early to comment" on further cuts beyond March.

“As long as the incoming data is in line with our projected return of inflation to target later this year then I think there is little obstacle to making another rate cut," Knot said. "To change my mind for next week, it’s rather unlikely.”

Knot reiterated ECB’s trajectory toward a neutral policy stance. But he emphasized, “I’m not convinced yet that we need to go into stimulative mode as well.”

He expressed optimism that recent inflation data is "encouraging". “It confirms the broad picture that we will return to target in the remainder of the year, and hopefully the economy will also finally recover a bit," he added.

However, Knot flagged risks posed by US trade policies, describing punitive tariffs as a “clear downside risk on the horizon.”

New Zealand CPI unchanged at 2.2% yoy, non-tradeable pressures persist

New Zealand’s CPI rose 0.5% qoq in Q4 2024, in line with expectations, as tradeable inflation increased 0.3% qoq and non-tradeable inflation rose 0.7% qoq. Annually, CPI was unchanged at 2.2% yoy, slightly exceeding the anticipated 2.1% yoy. This marks the second consecutive quarter that inflation has stayed within RBNZ's target range of 1% to 3%.

The data highlights diverging trends within inflation components. Non-tradeable inflation, which reflects domestic demand and supply conditions and excludes foreign competition, stood at 4.5% yoy, highlighting persistent internal price pressures. Tradeable inflation, influenced by global factors, recorded a -1.1% yoy decline.

Rent prices were the largest contributor to the annual CPI increase, rising 4.2% and accounting for nearly 20% of the overall 2.2% gain. Lower petrol prices, down -9.2% yoy, offset some of the upward momentum, with CPI excluding petrol increasing 2.7% yoy.

Australia's Westpac Leading Index falls to 0.25%, signals gradual growth pickup

Westpac Leading Index for Australia dipped slightly in December, moving from 0.33% to 0.25%. Westpac noted that while the growth signal remains modest, it reflects a marked improvement from the consistently negative and below-trend readings observed over the past two years. This uptick hints at a gradual lift in economic momentum through the first half of 2025.

Westpac forecasts GDP growth to improve steadily over the course of 2025, projecting a year-end expansion of 2.2%—a notable recovery from the weak 0.8% growth recorded in the year to September 2024. However, the bank noted that while this represents progress, it remains below the economy’s long-term potential.

Westpac highlighted that recent improvements in the Leading Index coincide with mixed signals on broader economy. A key concern for RBA is the labor market, where the "rebalancing" stalled in H2 2024.

"A further slowdown in underlying measures of inflation could still see the Bank ease in February or April but we suspect the RBA will need to be more comfortable about some of these risks before it is prepared to begin easing," Westpac noted.

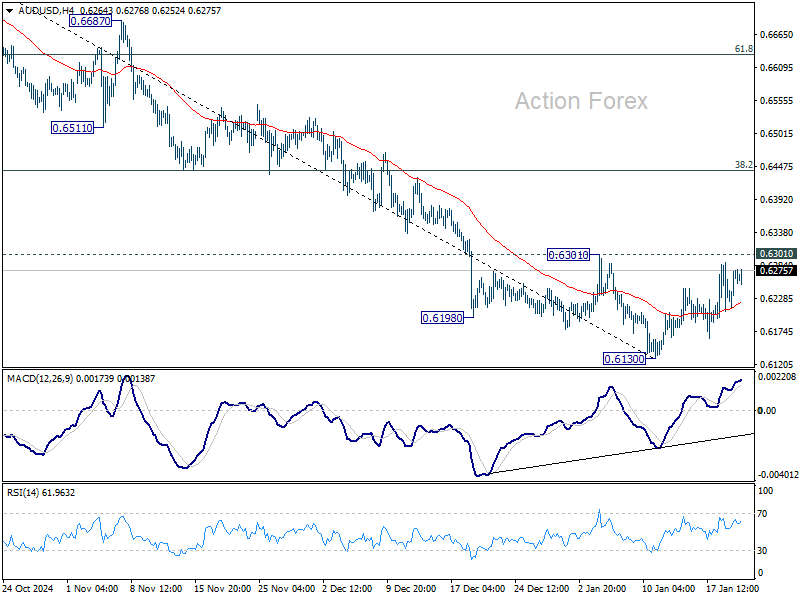

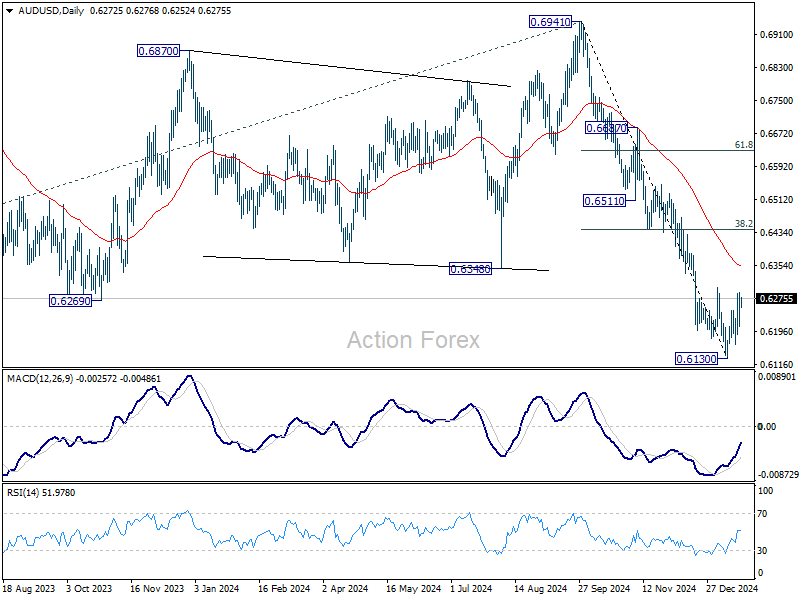

AUD/USD Daily Report

Daily Pivots: (S1) 0.6224; (P) 0.6257; (R1) 0.6305; More...

Intraday bias in AUD/USD stays neutral for the moment. With 0.6301 resistance intact, consolidations from 0.6130 should be relatively brief, and further decline is expected. Break of 0.6130 will resume the fall from 0.6941. However, firm break of 0.6310 will turn bias back to the upside for stronger rebound to 55 D EMA (now at 0.6352), and possibly above.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6224; (P) 0.6257; (R1) 0.6305; More...

Intraday bias in AUD/USD stays neutral for the moment. With 0.6301 resistance intact, consolidations from 0.6130 should be relatively brief, and further decline is expected. Break of 0.6130 will resume the fall from 0.6941. However, firm break of 0.6310 will turn bias back to the upside for stronger rebound to 55 D EMA (now at 0.6352), and possibly above.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

EUR/USD Starts Increase While USD/JPY Corrects Gains

EUR/USD started a decent upward move above the 1.0350 resistance. USD/JPY is correcting gains and now consolidates below 156.00.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro found support and started a recovery wave above the 1.0360 resistance zone.

- There is a key bullish trend line forming with support near 1.0395 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY is trading in a bearish zone below the 157.00 and 156.60 levels.

- There is a connecting bearish trend line forming with resistance near 155.90 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh increase from the 1.0265 zone. The Euro climbed above the 1.0310 resistance zone against the US Dollar.

The pair even settled above the 1.0350 resistance and the 50-hour simple moving average. Finally, it tested the 1.0435 resistance. A high is formed near 1.0434 and the pair is now consolidating gains. There was a minor decline below the 23.6% Fib retracement level of the upward move from the 1.0266 swing low to the 1.0434 high.

Immediate support is near the 1.0395 level. There is also a key bullish trend line forming with support near 1.0395. The next major support is at 1.0350 and the 50% Fib retracement level of the upward move from the 1.0266 swing low to the 1.0434 high.

If there is a downside break below 1.0350, the pair could drop toward the 1.0310 support. The main support on the EUR/USD chart is near 1.0265, below which the pair could start a major decline.

On the upside, the pair is now facing resistance near 1.0435. The next major resistance is near the 1.0450 level. An upside break above 1.0450 could set the pace for another increase. In the stated case, the pair might rise toward 1.0550.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a steady decline from well above the 158.00 zone. The US Dollar gained bearish momentum below the 157.00 support against the Japanese Yen.

The pair even settled below the 156.60 level and the 50-hour simple moving average. There was a spike below 155.00 and the pair traded as low as 154.77. It is now correcting losses and trading above the 50-hour simple moving average and the 50% Fib retracement level of the recent decline from the 156.58 swing high to the 154.77 low.

Immediate resistance on the USD/JPY chart is near a connecting bearish trend line at 155.90. It is near the 61.8% Fib retracement level of the recent decline from the 156.58 swing high to the 154.77 low.

The first major resistance is near the 156.60 zone. If there is a close above the 156.60 level and the hourly RSI moves above 60, the pair could rise toward 157.00. The next major resistance is near 157.70, above which the pair could test 158.50 in the coming days.

On the downside, the first major support is near 155.35. The next major support is near the 154.80 level. If there is a close below 154.80, the pair could decline steadily. In the stated case, the pair might drop toward the 154.00 support.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Downside in Dollar Limited Short-Term

Markets

The first two days of the Trump administration as expected brought an avalanche of executive orders and new initiatives to mark a seizure wit the policy from his predecessor. However, at least from a market point of view, the start of the new Trump era didn’t bring an outright moment of disruption yet. For now, the new administration only releases it intentions on a step by step basis. This is particularly the case for way the new government will use trade tariffs as a policy instrument. For now, markets apparently feel comfortable with this approach, even as Trump keeps the pressure on his trading partners. In this respect, he yesterday suggested that 10% tariffs might be imposed on China starting as early as on February 1. This action won’t be based on issues of trade policy, but as a reprieve from the country sending drugs to the US. The debate on trade will follow later. He also warned on Europe on its structural trade surplus with the US. The step by step approach at least is no concern from (US) equity investors. US indices resumed their uptrend rising up to 1.24% (Dow). Late yesterday, a group of tech firms including Softbank, OpenAI and Oracle with the support of the new government announced the set-up of a new joined venture to fund new AI infrastructure (starting $100 bln). The announcement further supported sentiment in the US tech sector after hours. On interest rate markets, the actions of the new government also didn’t change market expectations on Fed policy in any profound way. The market still discounts between 1 and 2 additional Fed interest rate cuts by the end of this year. US yields in a first reaction yesterday morning opened lower after Monday’s holiday, but closed the session off the intraday lows (2y -0.8 bps, 30-y -5.7 bps). Change in German yields were limited (2-y -0.7 bps, 30-y -2.8 bps). The dollar is still looking for direction after an initial correction on Monday as Trump refrained from slapping tariffs in his first batch of measures. However, with this topic to continue hanging over the market for some time, the dollar is holding above first important support levels. At 108.15, DYX stays above the recent lows in the 107.6/108 area. EUR/USD has the 1.0458 ST correction top within reach, but an outright test didn’t occur yet. In case of a break, the early December top of 1.0630 is the next reference. In the current context of persistent uncertainty, at least intentionally orchestrated by the Trump administration, we expect the downside in the dollar to be limited short-term. The rebound of the USD/CNY this morning after the threat of a 10% tariff on China imports next month (USD/CNY 7.2815) serves as a case in point.

Todays eco calendar is again very thin. There are no important data in the US and EMU. ECB governors today have a final opportunity to give their view on monetary policy before the black-out period in the run-up to next week’s policy meeting starts. However, a 25 bps rate cut at next week’s meeting is a done deal. The debate on the what a might be the neutral rate that the ECB has to go to later this year will continue in the run-up to the March meeting (2.25%, 2.0%?)

News & Views

New Zealand inflation rose by 0.5% Q/Q in the final quarter of last year, slightly down from the 0.6% pace in Q3 but matching expectations. Prices for international transport (+6.6% Q/Q) were the main driver with lower prices for vegetables (-11.5% Q/Q) on the other side of the balance. Details continue to show a split between tradeable CPI (+0.3% Q/Q) and more sticky, domestic, non-tradeable (services) CPI (+0.7% Q/Q). Annual inflation remained steady at 2.2%. It’s the second consecutive quarter that this metric is inside the RBNZ’s target band after three consecutive years of higher inflation (Q2 2021 – Q2 2024). The largest contributor to the annual inflation rate was rent (almost a fifth), up 4.2% Y/Y. Lower petrol prices (-9.2% Y/Y) helped offset rising prices. CPI would have stood at 2.7% Y/Y if you exclude them. Inflation numbers didn’t trigger any meaningful reaction on NZD markets. If any, they strengthened market conviction that the RBNZ will implement a third consecutive 50 bps policy rate cut at its first meeting of 2025 (Feb 19). NZD/USD (0.5650) has difficulties to really get traction above the 0.55-0.56 support area.

The head of Japan’s biggest business lobby added to BoJ rate hike calls by signaling that demand-led price growth is underway. He spoke after meeting with the leader of the nation’s biggest federation of trade unions, Rengo which is considered the official start of annual wage negotiations. Rengo’s members last year achieved average wage hikes of more than 5%, the most in over 30 years, and are looking for a repeat by March of this year. Smaller firms are even targeting 6%.

ECB’s Knot supports near-term rate cuts, not convinced of of stimulus mode

Dutch ECB Governing Council member Klaas Knot expressed agreement with market expectations for rate cuts at the January and March meetings, saying he is “pretty comfortable” with them. However, he added it is "too early to comment" on further cuts beyond March.

“As long as the incoming data is in line with our projected return of inflation to target later this year then I think there is little obstacle to making another rate cut," Knot said. "To change my mind for next week, it’s rather unlikely.”

Knot reiterated ECB’s trajectory toward a neutral policy stance. But he emphasized, “I’m not convinced yet that we need to go into stimulative mode as well.”

He expressed optimism that recent inflation data is "encouraging". “It confirms the broad picture that we will return to target in the remainder of the year, and hopefully the economy will also finally recover a bit," he added.

However, Knot flagged risks posed by US trade policies, describing punitive tariffs as a “clear downside risk on the horizon.”

Australia’s Westpac Leading Index falls to 0.25%, signals gradual growth pickup

Westpac Leading Index for Australia dipped slightly in December, moving from 0.33% to 0.25%. Westpac noted that while the growth signal remains modest, it reflects a marked improvement from the consistently negative and below-trend readings observed over the past two years. This uptick hints at a gradual lift in economic momentum through the first half of 2025.

Westpac forecasts GDP growth to improve steadily over the course of 2025, projecting a year-end expansion of 2.2%—a notable recovery from the weak 0.8% growth recorded in the year to September 2024. However, the bank noted that while this represents progress, it remains below the economy’s long-term potential.

Westpac highlighted that recent improvements in the Leading Index coincide with mixed signals on broader economy. A key concern for RBA is the labor market, where the "rebalancing" stalled in H2 2024.

"A further slowdown in underlying measures of inflation could still see the Bank ease in February or April but we suspect the RBA will need to be more comfortable about some of these risks before it is prepared to begin easing," Westpac noted.