Sample Category Title

GBPUSD Pushed Towards 1.3100

Sterling continues to move higher during the European trading session, as the U.S dollar index comes under selling pressure, ahead of the European Central Bank's policy decision in Frankfurt, later today.

Currently, price-action is testing resistance towards the current the 1.3100 region, which the pair now trading above the 1.3082 level, which represents the former monthly pivot point for the GBPUSD pair.

This afternoons price moves in the GBPUSD pair, may be strongly correlated to the direction the EURUSD pair takes, during and after ECB President Mario Draghi's press conference.

Key technical resistance above the 1.3100 level is located at 1.3125,1.3190 and 1.3220.

To the downside, intraday GBPUSD support is found at 1.3045, 1.3019, and the daily pivot point, at 1.2998. Below the 1.2998 level, the 50-day moving average becomes key support, at 1.2984.

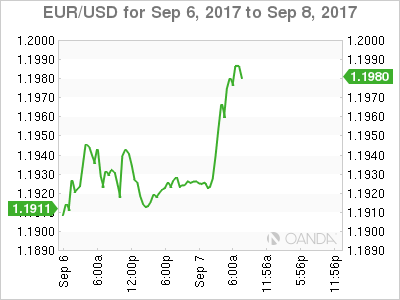

EURUSD Tests 1.20 ahead of ECB Meeting

The EURUSD continues to advance higher during the European trading session, with the pair falling just short of 1.2000, hitting 1.1995, ahead of today's European Central Bank interest rate decision and press conference.

Euro buyers look ready to continue the strong uptrend seen over the summer months, with technical traders ready to test towards the historical 1.2139 Fibonacci resistance level.

The EURUSD remains strongly bullish against the U.S dollar on all-time frames, although fundamental developments from today's ECB press conference will dictate the pairs intraday directional bias.

Key technical resistance is located at 1.2030, the yearly price high at 1.2070, and the 1.2100 level. Above the 1.2100 level, traders should look to strong weekly resistance from 1.2139, 1.2160 and the December 2014 price high, at 1.2220.

To the downside, look for key intraday support at 1.1945, 1.1918 and 1.1884.

Below 1.1884, look for strong EURUSD weekly support at the 1.1744 and 1.1664 levels.

Markets Seek Clarity From Draghi

Thursday September 7: Five things the markets are talking about

The best-laid plans sometimes fail to materialize. For instance, if the ECB had been hoping to exit QE undercover of the Fed's observance to a predictable path of 'normalisation' has very much been complicated by stubbornly low U.S inflation and U.S political uncertainty.

The EUR has appreciated close to +14% since the start of this year outright, causing a few sleepless nights at the ECB because it has been pushing inflation lower, the opposite to what the Euro policy makers require.

What to expect from the ECB?

Consensus expect the ECB to delay announcing plans to reduce monetary stimulus or QE until October, following the 'single' unit's recent rise above the psychological €1.20 handle – the banks pain threshold level. The ECB will have to revise inflation projections down, blaming the strong EUR, and to acknowledge further downside risks – which should cap the EUR for the short-term.

Note: Saying nothing would constitute an invitation to drive the EUR higher, which no doubt is not in the interest of the ECB.

The 'smart' money will be 'short' EUR's or small core 'long' the single unit heading into this morning's ECB press conference (08:30 am EDT) in particular, with many expecting Draghi to address the pace of EUR appreciation.

The markets objective will be to buy dips, which should be short lived as any decline will be used to position for a further move up in EUR/USD on a 6-12 month horizon (€1.25-27).

Elsewhere, the U.S dollar continues to struggle against its G-10 peers as tensions over North Korea outweigh positive sentiment arising from yesterday's extension of the U.S debt limit. The market is also keeping an eye on Hurricane Ira (and crude prices), which is currently barrelling towards Florida.

1. Stocks get the green light

In Japan, the Nikkei share average rallied overnight, pulling away from its four-month intraday low after news of an agreement to raise the U.S debt limit yesterday helped restore investors' risk appetites. The Nikkei ended +0.2% higher, while the broader Topix rallied +0.4%.

Down-under, Australia's S&P/ASX 200 Index was little changed after Aussie retail sales data struggled last month (+0.0% vs. +0.2%e). In South Korea, the Kospi rallied +1.1%.

In Hong Kong, stocks reversed earlier gains to end lower overnight, pressured by losses in the mainland share market. The Hang Seng index fell -0.3%, while the China Enterprises Index lost -0.2%.

In China, equities fell, as profit taking in resource shares following their recent rally and weakness in the banking sector offset strong gains in real estate companies. The blue-chip CSI300 index fell -0.5%, while the Shanghai Composite Index lost -0.6%.

In Europe, regional bourses trade mixed with outperformance in the DAX, whilst weakness is observed on the FTSE 100 and the Swiss SMI. Markets are trading in a holding pattern ahead of this morning's ECB rate decision and press conference.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx600 flat at 373.8, FTSE flat at 7357, DAX +0.6% at 12283, CAC-40 +0.3% at 5115, IBEX-35 +0.1% at 10140, FTSE MIB -0.4% at 21739, SMI -0.2% at 8839, S&P 500 Futures -0.2%

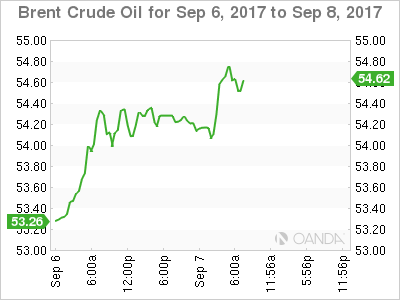

2. Oil dips on fears 'Irma' could hit crude shipments, gold steady

Oil prices have dipped a tad overnight over fears that Hurricane Irma could interrupt crude shipments in and out of the U.S, and as Libyan output begins to recover from disruptions.

Note: However, prices are receiving some support from rising demand in the U.S, where Gulf Coast refineries are restarting in the wake of Hurricane Harvey.

Brent crude futures have dipped -21c, or -0.4% to +$53.99 a barrel, while U.S West Texas Intermediate (WTI) crude futures are down -18c, or -0.4% at +$48.98 a barrel.

Also putting pressure on crude prices is oil output at Libya's Sharara field, the country's largest, resumed yesterday, which had been shut down for more than two-weeks.

Investors will take direction from todays EIA inventory report (11:00 am EDT).

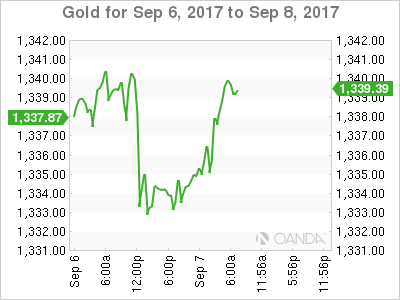

Expectations that the Fed will raise rates gradually have been a boon for gold. Ongoing rising tensions between the U.S and North Korea have also boosted demand for the 'yellow' metal, contributing to a +15% gain this year.

Overnight, gold prices held steady, supported by a weaker dollar, as markets await the outcome of today's ECB policy meet – spot gold is unchanged at +$1,333.90 per ounce, after easing -0.3% in yesterday's session.

3. Unexpectedly 'hawkish' Draghi could trigger Bund sell-off

With the ECB expected to do whatever it takes to keep short end rates anchored has fixed income dealers believing that the eurozone bond yield cure will steepen even further. Current Eonia forwards imply no rate rises by the ECB until spring 2019.

Therefore, any 'hawkish' talk should push longer yields higher. If Draghi sounds more hawkish than expected, this would trigger a sell-off in German bunds, with 10-year yields rising back to the +0.40-0.45% area. 10-year Bund yields currently trade at +0.36%.

Elsewhere, U.S 10-year Treasuries declined -1 bps to +2.09%, while U.K Gilt yields back up +2 bps to +1.026%.

In Sweden, the Riksbank is sticking to its established policy script – this morning policy makers kept both policy and rate path unchanged. The statement reiterated that first rate hike will not be seen until mid-2018, but was prepared for more easing if necessary. Governor Ingves noted that the “domestic economy was developing better than expected, but its too early to make policy less expansionary.” The SEK ($7.9688) currency has strengthened faster than its July forecast.

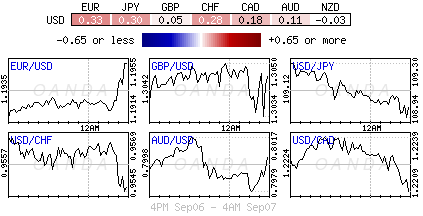

4. Dollar under pressure vs. G10

The EUR/USD (€1.1980) is trading at session highs ahead of the ECB rate decision. The ECB is expected to keep policy steady with particular focus on whether euro policy makers would provide any guidelines on its looming QE taper. No final decision on the next steps is expected until next month's meeting.

Overall, the FX market is relatively quiet, but the USD remains on soft footing vs. its G10 counterparts. USD/JPY (¥108.88) is a tad lower as the Korea peninsula concerns remain on the front burner with another N. Korean missile launch possible ahead of Sept. 9.

GBP (£1.3071) has rallied to a four-week high ahead of the U.S open. Down-under overnight, the AUD (A$0.8015) briefly held some strength for most of the session before falling back after a tepid Aussie retail sales report last month.

5. Eurozone economy stronger than estimated

Data this morning showed that the eurozone economy grew more quickly over the 12 months through June than previously estimated. Eurostat left its estimate of quarter-to-quarter growth for the three months to June unchanged at +0.6%. But, raised its estimate of growth in Q3, 2016 to +0.5% from +0.4%.

As a result, it now estimates that the economy was +2.3% larger in the three months to June than it was in the same period last year – the fastest rate of growth recorded in six-years.

Note: The Eurozone has outpaced the U.S in Q1 and accelerated further in the three months to June.

But data released by the European Union's statistics agency showed the pickup began earlier than previously thought. it raised its estimate of growth in the third quarter of last year to 0.5% from 0.4%.

Note: The ECB is expected to raise their growth forecasts for this year and next later this morning.

Bank Of Canada Rate Hike, FOMC And Debt Limit Extension Rock The Markets

U.S. Lawmakers Agree On Debt Limit Extension. The dollar recovered from its recent dive on an extension of the debt limit deadline to December 15 to make way for Harvey disaster bill and resignation of FOMC member Fischer due to personal reasons.

The Loonie Stands Tall After Rallying On BOC Hike And Upbeat Canadian Data. The Bank of Canada decided to hike interest rates by 0.25% instead of staying put for the second time this year. That gave the Canadian a strong boost across the board, on top of the pickup in crude oil prices in anticipation of better than expected EIA inventory data. Upcoming Canadian jobs release could garner a lot of market attention as this could make or break future hike speculations.

Euro Awaits ECB’s Policy Decision Due Later On Thursday. The euro held firm on Thursday ahead of a European Central Bank policy meeting. The euro edged up 0.1 percent to $1.1928 , although it was still trading below last week’s high of $1.2070, its highest level since January 2015.

Watch Out Today For:

09:00 am GMT: EUR Gross Domestic Product

11:45 am GMT: EUR ECB Interest Rate Decision

12:30 pm GMT: EUR ECB Monetary Policy Statement And Press Conference

USDSEK Downside Momentum Eases But Bias Still Bearish

USDSEK has been range-bound over the past week as the pair pauses after two months of heavy losses. Upside momentum has been gaining ground during the past week according to the stochastics, with the %K and %D lines trending up to rise above 50. However, the RSI is indicating only an easing of the bearish bias as it remains below the 50-neutral level and its flat direction suggests the consolidation will continue in the near-term.

Should the upside momentum gain further traction, immediate resistance should come at the top of the current range at 8.0200. Further up, the area around 8.12 could act as another hurdle as this has been a heavily congested region in the past. Above this area, the 50-day moving average (MA) comes into focus (currently at 8.17), followed by the previous resistance level of 8.225. A break above the 50-day MA would shift the bias to positive.

To the downside, the bottom of the range at 7.9065 is the nearest support. A break of this level would take the pair towards the May 2016 low of 7.8913. Further declines below this trough would deepen the bearish bias not only in the short term but also in the medium term, and open the way towards the 7.50 level.

Euro Gaining Ground Ahead Of ECB Announcement

EUR/USD has posted slight gains in the Thursday session. Currently, the pair is trading at 1.1960, up 0.31% on the day. On the release front, German Industrial Production came in at a flat 0.0%, shy of the estimate of 0.5%. Later in the day, the ECB releases its monthly statement, followed by a press conference with ECB President Mario Draghi. In the US, the key event is Unemployment Claims, which is expected to jump to 245 thousand.

The euro continues to trade at high levels, and is within striking distance of the symbolic 1.20 level. The euro has risen 13% against the dollar in 2017, and the trend could continue if the ECB decides to withdraw or taper its current quantitative easing (QE) program, in which the ECB makes monthly asset purchases of EUR 60 billion/month. The QE scheme is scheduled to terminate in December, and the ECB is yet to determine what happens next. Policymakers must weigh competing interests – Germany would like nothing more than the ECB to simply exit the program, which was brought in as an emergency measure to begin with. However, other eurozone members, which are not enjoying German-style growth, favor a gradual tapering of the program, perhaps lowering monthly asset purchases from EUR 60 billion to EUR 45 billion. Analysts are not expecting any announcements regarding QE at the Thursday meeting, although Mario Draghi has surprised the markets in his press conferences more than once. The exchange rate has also become a factor, as a stronger euro is equivalent to a raise in interest rates and has resulted in monetary tightening even without the ECB taking any action. In determining what course of action to take, ECB policymakers must wrestle with a dilemma which the Federal Reserve and other central banks are also struggling with – is tighter monetary policy warranted when the economy has improved, but inflation is mired at low levels? The markets will be dissecting the rate statement and Draghi's follow-up comments, and any hints about a change in policy could trigger significant movement from the euro.

It's been a disappointing week for German industrial numbers. Factory Orders declined 0.7%, well off the forecast of a 0.2% gain. This marked a 3-month low. On Thursday, German Industrial Production followed suit, as the reading of 0.0% missed the estimate of 0.5%. The unexpectedly weak readings come as a surprise, as the German economy has looked strong in 2017, and has been an important factor in the improvement in the eurozone economy. Global demand, which had been very strong in the first half of 2017, is showing signs of softening, and this could have a negative impact on the manufacturing sectors in Germany and throughout the eurozone. Germany releases Trade Balance on Friday, with the markets braced for a drop in the surplus for July.

Technical Outlook: GBPUSD Extends Advance, Strong Bullish Signal On Probe Above Daily Cloud

Fresh bullish acceleration in European session broke above key barriers provided by daily cloud top and Fibo 61.8% of 1.3268/1.2773 descend, generating strong bullish signal.

Bulls are pressuring round-figure barrier at 1.3100 and may extend to 1.3151 (Fibo 76.4%), with close above 1.3080 required to confirm.

Hourly 10/20SMA/Tenkan-sen/Kijun-sen bull-crosses at 1.3050 underpin the action and offer solid supports.

Res: 1.3100, 1.3151, 1.3164, 1.3200

Sup: 1.3080, 1.3050, 1.3020, 1.3000

Technical Outlook: SPOT GOLD – Consolidation To Precede Fresh Upside, Targets At $1347/52 Eyed

Spot Gold is trading in extended consolidation under fresh high at $1344, posted on Tuesday, as broader bulls are taking a breather before resuming higher.

The yellow metal is riding at the third wave of five-wave cycle from $1204, which eyes its next target at $1347 (FE 138.2%), but bulls may be delayed by negative signals from overbought daily studies.

Extended dips should be contained by rising 10SMA (currently at $1320) before bulls resume.

Conversely, early downside rejection would prompt fresh bullish acceleration towards initial target at $1347, possibly to $1352 (04 Sep 2016 peak) in extension.

Gold remains well supported as deterioration of geopolitical situation over North Korea’s nuclear probes maintains strong demand for safe-haven assets.

Res: 1344, 1347, 1352, 1358

Sup: 1331, 1326, 1321, 1318

US: Debt Limit Fight Postponed Amid Increased Fed Uncertainty

- Yesterday was a very eventful day, as Donald Trump struck a deal with the Democrats on Harvey aid, government funding until December and a suspension of the debt limit until mid-December.

- In our view, this is just kicking the can down the road, as we now risk a government shutdown in December and/or a government default at some pint early next year.

- Yesterday, the Fed's Vice Chair Stanley Fischer announced that he will step down on or around 13 October, leaving four empty seats in the Board of Governors.

- The Wall Street Journal reports that President Trump is unlikely to nominate Gary Cohn as the next Fed Chair. This has increased the probability of the reappointment of Janet Yellen but Trump is known for wanting his own people in key positions.

- The many empty seats mean that it is difficult to say what direction the Fed will take next year. The Republicans may use the opportunity to shift the Fed in a more hawkish and rule-based direction.

Debt limit suspended until mid-December

Despite Republican House Speaker Paul Ryan saying that the Democratic proposal to suspend the debt limit for months was ‘ridiculous and disgraceful', President Trump sided with the Democrats. This means that we now have a bipartisan deal on Harvey aid, funding for the government for three months and a suspension of the debt limit until mid-December. The deal came earlier than we had expected, as we thought (in line with Republican members of Congress) the Trump administration would be willing to fight harder for a longer lasting solution to the debt limit. Basically, the deal means the risk of a government shutdown has only been postponed from the end of this month to December. Republicans still need a budget for the fiscal year 2018 (lasting from 1 October 2017 to 30 September 2018), eventually allowing them to avoid filibusters in the Senate through budget reconciliation. However, the main problem for the Republicans remains the internal disagreement between the fiscal hawks and the more moderate Republicans. The former, unlike the latter, wants to make major cuts in fiscal spending.

While the suspension of the debt limit expires in mid-December, the stricter deadline is likely some months afterwards, as the Treasury can now ‘refill' some of the extraordinary measures it has exhausted in recent months. This means there is still a risk of a government default at some point in 2018. It is not an option only to increase the Treasury's cash buffer at the Federal Reserve, as it needs to be back at the current level when the suspension of the debt limit expires in mid-December.

The suspension of the debt limit also means that the US Treasury can increase its debt issuance again.

Vice Chair Fischer steps down, four out of seven seats are now vacant

In addition, Fed Vice Chair Stanley Fischer has written a resignation letter to President Trump due to personal circumstances. Fischer will step down on or around 13 October, leaving four vacant seats at the Fed. While this move caught everyone by surprise, most believed Trump would not reappoint Fischer anyway when his term expired in June next year, so markets barely moved on the announcement.

With four out of seven seats at the Fed Board of Governors currently vacant – and possibly soon five, as it is not our base case that Trump will reappoint Janet Yellen as Fed Chair (see more below) – Trump has the power to shape the Federal Reserve in the way he wants (although the Senate has to approve his nominations). This makes it more difficult to say what the Fed will do next year, as it is difficult to say in which direction the Fed will go. Trump has not said much about monetary policy but he has said a few mutually contradicting things: (1) he says he wants higher rates but is a ‘low interest rate guy’ and (2) he says a strong USD is a sign of strength but that a weak USD is good for US exports. In other words, it is difficult to say whether the Fed will turn more hawkish or more dovish, as Trump does not really seem interested in monetary policy, as he thinks of economic policy in terms of trade policy and tax reform/deregulation/infrastructure investments. While President Trump does not seem very interested in monetary policy and the Fed, the Republican Party certainly is, as many Republicans are dissatisfied with the Fed’s low-rate policy. Many Republicans want a more rule-based Fed, which bases its monetary policy decisions on a policy rule. Based on a simple Taylor rule, which links the Fed funds rate to inflation and unemployment, the Fed funds rate should be around 3% now. In other words, we might see a more hawkish and rule-based Fed next year but the uncertainty is high. For more, see what we wrote back in February: Research US: Trump to nominate three Fed governors – Tarullo resigns, 13 February. Overall, it seems fair to say, the Fed’s independence may come under greater pressure.

Trump has already nominated Randal K. Quarles, as former Treasury Department official, to serve as Fed Vice Chair for Supervision (see NY Times). Quarles is considered more dovish on financial regulation than Daniel Tarullo, who was previously in charge of supervision (at least in practice).

Trump’s economic adviser Gary Cohn was favourite to succeed Yellen as Fed Chair but The Wall Street Journal reports that Trump is unlikely to nominate him due to Cohn’s criticism after Charlottesville. According to PredictIt, the most likely scenario is now that Yellen will be reappointed but this is not our base case.

The Spotlight Falls On The ECB Policy Meeting

Today, investors will be sitting on the edge of their seats in anticipation of the ECB policy gathering. Given that no change in rates is expected, market focus may be on whether the Bank will remove from its statement the easing bias that QE can be expanded both in terms of size and/or duration if needed. However, last week, reports citing sources familiar with ECB discussion, poured cold water on any removal expectations.

In our view, this suggests that in case the Bank maintains its QE easing bias, the market may react little, as it has already responded to the aforementioned reports. EUR/USD could tumble, but not much. It could test once again the key support barrier of 1.1830 (S1), or the medium-term uptrend line taken from the low of the 17th of April. The surprise would be a removal of that easing bias. This could cause EUR/USD to surge above the 1.2000 (R2) figure, and even break above 1.2100 (R3).

Another key point of interest may be any comments regarding the rapid pace of the euro's appreciation. However, even if the Bank seizes the opportunity to express some further worries about the euro's strength, we expect something like that to only trigger a correction. As long as Draghi continues to remind us that financial conditions remain accommodative, we don't expect a reversal in the common currency's uptrend. The risk to that view is any signals that financial conditions in general have started to tighten due to that.

The BoC did it again

Yesterday, the Canadian dollar skyrocketed after, in a surprise move for many market participants, the BoC decided to increase interest rates for the 2nd gathering in a row. The tone of the statement accompanying the decision remained on the hawkish side, with officials noting that recent economic data have been stronger than expected, confirming their view that growth is becoming more broadly-based and self-sustaining. On the inflation front, the Bank acknowledged that price pressures have evolved largely as expected in July, and that the latest increase is consistent with the dissipating negative impact of temporary price shocks and the absorption of economic slack.

As for future monetary policy decision, the Bank said that they will be guided by incoming economic data and financial developments as they inform the outlook for inflation. As such, investors are likely to pay extra attention to upcoming economic data in order to assess the probability for another rate hike this year. Specifically, the employment data tomorrow and the CPIs on the 22nd of September may be proven critical on that front. At the time of writing, the probability for another rate increase by year-end is around 55%. That probability could rise further if data continue to suggest that the economy continues to perform in line or better than the Bank anticipates.

USD/CAD collapsed yesterday, following BoC's unexpected decision to lift rates. The pair broke two support levels in a row, and stopped fractionally above the 1.2120 (S1) barrier, a support marked by the low of the 18th of June 2015. Then the rate rebounded and currently, it is trading slightly below the 1.2260 (R1) resistance. The BoC collapse confirmed a forthcoming lower low on both the 4-hour and daily charts and thus, we believe that the outlook remains negative. If the bears manage to take advantage of the rebound near 1.2260 (R1), we would expect them to pull the trigger for another test near the 1.2120 (S1), the break of which could open the way for the psychological zone of 1.2000 (S2).

As for the rest of today's events:

A few hours ahead of the ECB, the Riksbank will announce its own interest rate decision. The upbeat inflation data, and the stronger than expected economic growth for Q2, make us believe that the Bank could proceed with removing its interest rate bias at this policy gathering. What could make the Riksbank hesitant to remove its easing bias, is the strengthening SEK.

As for the economic data, we get Eurozone's final GDP print for Q2. Given that it is coming a couple of hours ahead of the ECB meeting, we expect it to pass unnoticed. In the US, we have initial jobless claims for the week ended on the September 1st, while in Canada, building permits for July and the Ivey PMI for August are due out.

Besides President Draghi, who will hold a press conference following the ECB decision, we have two more speakers on the agenda: Cleveland Fed President Loretta Mester and New York Fed President William Dudley. Following the latest dovish remarks from Brainard, Kashkari and Kaplan, it would be interesting to hear their view.

EUR/USD

Support: 1.1880 (S1), 1.1830 (S2), 1.1730 (S3)

Resistance: 1.1950 (R1), 1.2000 (R2), 1.2100 (R3)

USD/CAD

Support: 1.2120 (S1),1.2000 (S2), 1.1920 (S3)

Resistance: 1.2260 (R1), 1.2335 (R2), 1.2430 (R3)