Sample Category Title

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

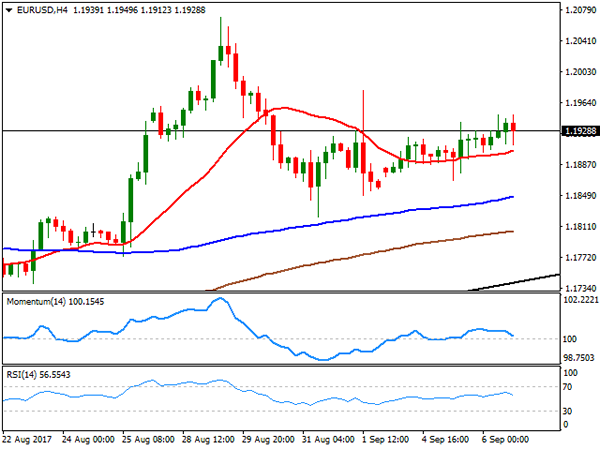

EURUSD

The EURUSD had another indecisive movement yesterday. The bias remains neutral in nearest term. Immediate resistance is seen around 1.1950. A clear break above that area could trigger further bullish pressure testing 1.2000 psychological /key level which need to be clearly broken to the upside to end the current bearish correction phase targeting 1.2175 area. Immediate support is seen around 1.1900. A clear break below that area could trigger further bearish pressure testing 1.1823 key support. Overall I remain bullish and any downside pullback should be seen as a good opportunity to buy.

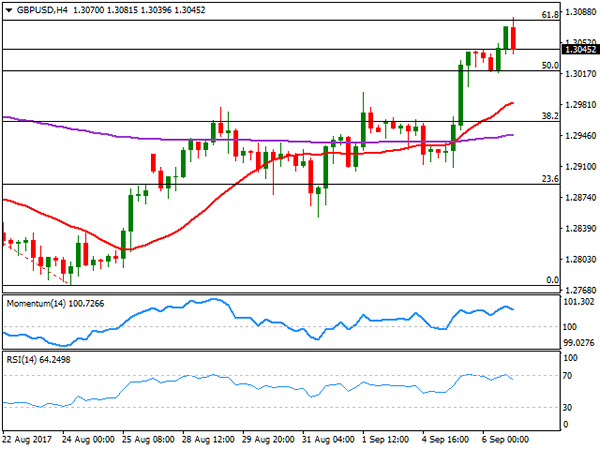

GBPUSD

The GBPUSD attempted to push higher yesterday topped at 1.3082 but closed lower at 1.3041, formed a bearish pin bar as you can see on my daily chart below, suggests a potential bearish view. The bias is bearish in nearest term testing 1.2980 support area. Immediate resistance is seen around 1.3082. A clear break above that area would nullify the bearish pin bar scenario targeting 1.3125/60 region as nearest bullish target. Overall I remain neutral.

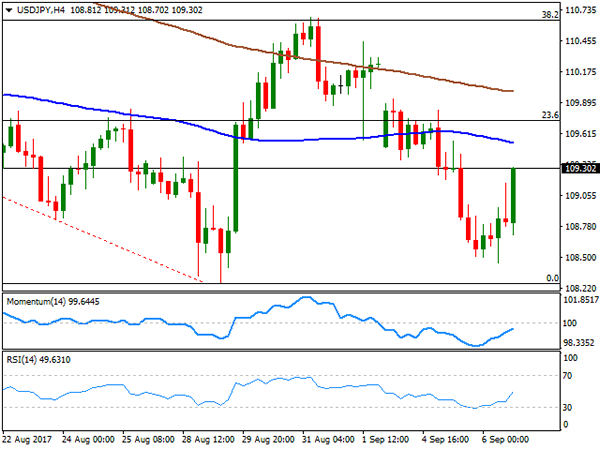

USDJPY

The USDJPY attempted to push lower yesterday slipped below 108.70 key support but again, unable to make a clear break below that key level and closed higher at 109.17. The bias is neutral in nearest term. Key support remains at 108.70, which is a good place to buy with a tight stop loss. Immediate resistance is seen around 109.40. A clear break above that area could trigger further bullish pressure testing 110.00 region but key resistance is seen at 111.00 which is a good place to sell. On the downside, a clear break and consistent movement below 108.70 would expose 108.00 – 107.50 as nearest bearish target. Overall I remain neutral.

USDCHF

The USDCHF was indecisive yesterday. The bias is neutral in nearest term. Immediate support is seen around 0.9525. A clear break and daily close below that area could trigger further bearish pressure testing 0.9450 key support which remains a good place to buy with a tight stop loss. Immediate resistance is seen around 0.9615 followed by 0.9650 but key resistance remains at 0.9765 – 0.9807 region which remains a good place to sell with a tight stop loss. Overall I remain neutral.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EUR/USD pair posted another modest advance this Wednesday, ending the day not far below a weekly high of 1.1949 achieved in the US afternoon. The greenback remained under pressure during the first half of the day amid persistent risk aversion, extending its losses during the American afternoon on poor US macroeconomic figures. Germany released its July factory orders, unexpectedly down by 0.7% in the month, but with little effect over the common currency. As for the US, trade balance figures showed that the deficit shrank to 43.7B beating expectations of -44.6B, but the final services PMI for August were below expected, with the Markit index at 56.0, and the official ISM one down to 55.3 from market's forecast of 55.8.

Focus now shifted to the upcoming ECB monetary policy decision, and how Draghi will balance a cautious stance on QE with the optimistic economic outlook. A leaked draft of the ECB's statement made the rounds in the US afternoon, suggesting the ECB will cut its 2018/19 inflation forecast, anticipating also that they will plan the discussion over QE but won't reach any decision until the next meeting, by the end of October. Seems unlikely Draghi would say anything negative enough to put the common currency under pressure, despite nothing would make him more happy than a weaker EUR.

The technical picture is short-term neutral for the EUR/USD pair, confined to a tight range above a still directionless 20 SMA in the 4 hours chart, but also well above the larger ones. Technical indicators in the mentioned chart have turned marginally lower above their mid-lines, lacking enough strength to indicate the upcoming direction. The pair has relevant intraday lows in the 1.1860 region, the immediate support, followed by last week's low of 1.1822. Below this last the risk will turn towards the downside, but there's still a long way ahead before calling it bearish. Steady gains beyond 1.2000 after the ECB's dust settles, will open doors for gains beyond the yearly high set late August at 1.2070.

Support levels: 1.1900 1.1860 1.1820

Resistance levels: 1.1960 1.2000 1.2035

USD/JPY

The USD/JPY pair fell to a fresh weekly low of 108.45 late Asia, changing course abruptly in the US afternoon to settle above 109.30, on the back of news indicating that the US Congress agreed on a Harvey aid package, and extending the debt ceiling to avoid defaulting. The news brought relief to the poor greenback, hit by different fronts these last few days, although across the FX board, the yen seems to be the most sensitive to the headline. Japan will release its coincident and leading indexes during the upcoming session, although market will likely remain cautious ahead of the ECB announcement later on the day. Technically, the recovery remains corrective, as despite the almost 100 pips' advance, the pair remains below its moving averages in the 4 hours chart, also below the 23.6% retracement of the July/August decline, this last around 109.75. Technical indicators in the mentioned chart have bounced sharply from oversold readings, but remain within negative territory, overall indicating that the upward potential is limited at least as long as the price remains below the mentioned Fibonacci resistance.

Support levels: 108.60 108.10 107.70

Resistance levels: 109.00 109.35 109.80

GBP/USD

The GBP/USD pair kept advancing this Wednesday, with no negative UK headlines to alter its latest advance. The pair rallied up to 1.3081, its highest in over a month, before retreating from the 61.8% retracement of its August monthly decline, holding, however, on to gains at the end of the day. Dollar's broad weakness was the sole responsible of Pound's gains, as there were no macroeconomic releases coming from the UK, whilst the c calendar will remain scarce this Thursday. On Friday, however trade balance and industrial production figures for July will take center stage. Brexit negotiations remain in a limbo as the clock keeps ticking towards the 2-year term. For now, seems not a big issue for the Pound, but sooner rather than later will take its toll. In the meantime, the pair retains its positive tone in the short term, as in the 4 hours chart, it holds well above a now bullish 20 SMA, which advance well beyond the 200 EMA, this last around 1.2945. In the same chart, technical indicators are modestly retreating from overbought levels, but still well above their mid-lines. Nevertheless, the pair would need to surpass the mentioned Fibonacci resistance to be able to extend its gains, with scope then to test 1.3140 region.

Support levels: 1.3020 1.2985 1.2950

Resistance levels: 1.3080 1.3110 1.3140

GOLD

Gold trimmed all of its Tuesday's gains, plummeting in the US afternoon as the greenback surged against safe-haven assets, on news announcing US President Trump agreed to a request from Democrats to raise the debt ceiling and extend government funding through Dec. 15, alongside with approving an aid package for the victims of Hurricane Harvey. The commodity fell to a daily low of $1,331.62 a troy ounce, and stands right above this last ahead of Wall Street's close, pointing to its lowest settlement for the week. From a technical point of view, the commodity is poised to correct further lower, as in the daily chart, technical indicators are finally retreating substantially from overbought readings, although the price remains far above bullish moving averages, these lasts indicating that the bullish case is not over yet. Shorter term, and according to the 4 hours chart, the risk has also turned towards the downside, as the price is breaking below its 20 SMA, the Momentum is entering negative territory with a strong downward slope, whilst the RSI also heads, south, but currently at 53. The weekly low was set at 1,326.40, while Friday's close comes at 1,324.21, making of the region around 1,325.00 a strong support level, and a line in the sand ahead of a steeper declines for this Thursday.

Support levels: 1,331.60 1,325.00 1,318.40

Resistance levels: 1,338.50 1,344.30 1,352.55

WTI CRUDE OIL

Crude prices keep advancing this Wednesday, with the US benchmark settling at $49.10 a barrel, its highest settlement in nearly a month. The commodity maintains the positive tone amid renewed demand for crude after the Hurricane Harvey passed through Texas, and ore refineries are resuming activity. A new Hurricane in the area, Irma, also helped lifting prices, on fears it will hurt US oil production. News that Russia and Saudi Arabia may extend the output cut, added to the bullish case. The daily chart shows that the price moved one step further towards the 200 DMA, but closed right below it, whilst technical indicators have extended beyond their mid-lines, maintaining their strong upward momentum ahead of the API release. In the 4 hours chart, the price is far above its 100 and 200 SMAs, while technical indicators consolidate within overbought readings, far anyway from suggesting upward exhaustion. The 50.00 level is a tough bone to break, yet if WTI manages to break above it, 52.00 becomes a more than likely bullish target.

Support levels: 48.20 47.70 47.15

Resistance levels: 49.40 49.90 50.40

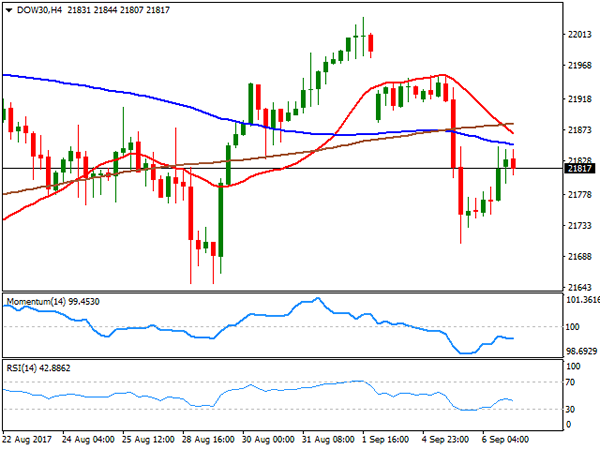

DJIA

Wall Street closed with gains, with the DJIA adding 54 points, to 21,807.64, and the Nasdaq Composite up 0.28%, to 6,393.31. The S&P added 7 points and settled at 2,465.54. Backing the rally were higher energy prices, as oil began recovering post-Harvey, while US lawmakers reached a deal to extend the debt ceiling until December. Home Depot was the best performer within the Dow, up 2.37%, followed by Chevron that gained 2.15%. Exxon was also within the top 10 winning list, after gaining 2.07%. United Technologies, on the other hand, was the worst performer, losing 1.42%. The index trimmed part of its Tuesday's losses, but further gains are still at doubt, as in the daily chart, the intraday advance stalled around the 20 SMA, while technical indicators have turned modestly higher, but are currently within neutral territory. In the shorter term an according to the 4 hours chart, the index remains below all of its moving averages, with the 20 SMA maintains a sharp downward slope, whilst technical indicators have corrected oversold conditions, but are currently resuming their declines within negative territory, limiting chances of further gains as long as the index remains below 21,845, the daily high.

Support levels: 21,795 21,758 21,721

Resistance levels: 21,845 21,891 21,932

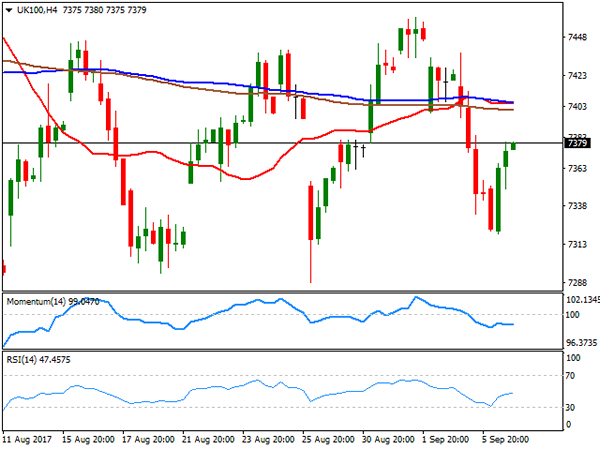

FTSE100

The FTSE 100 remained under pressure this Wednesday down 18 points, to close at 7,354.13, as despite market mood improved modestly, the Footsie was weighed by a strong Pound. Despite most members closed higher, the benchmark was dragged lower by Barratt Developments, which shed 4.57%, as despite posting a record annual profit, it offered a forecast of only "modest growth" in the next financial year. Micro Focus International added 6.16% leading advancers, and followed by Next that gained 2.51%. The index has partially recovered previous losses, but is still looking bearish according to the daily chart, as it held below a bearish 20 DMA which extends its decline below the 100 DMA, while technical indicators remain within bearish territory, although with limited directional strength. Shorter term and according to the 4 hours chart, the risk is also towards the downside as the index keeps developing below all of its moving averages, anyway converging directionless in the 7,400 region, whilst technical indicators seem to be resuming their declines within bearish territory.

Support levels: 7,333 7,288 7,241

Resistance levels: 7,400 7,444 7482

DAX

European equities closed marginally higher, led by the German DAX, as the automotive sector was lifted by rating upgrades. The benchmark added 90 points, to end at 12,214.54, with Daimler being the best performer, up by 4.34%, followed by Volkswagen which added 2.98% after Goldman Sachs upgraded the first from neutral to buy. Deutsche Bank added 2.13% after its CEO said that the ECB should begin tapering, in spite of a strong EUR. Only E.ON closed in the red, down 0.56%. The index gained upward potential according to the daily chart, surpassing sharply its 20 DMA, and with technical indicators maintaining strong upward slopes within positive territory. In the 4 hours chart, the index settled a few points above its 200 SMA for the first time in almost two months, and far above the shorter ones, whilst technical indicators have lost part of their upward strength, but remain within positive territory. ECB's announcement this Thursday will be the main market motor for the index.

Support levels: 12,241 12,207 12,166

Resistance levels: 12,301 12,342 12,383

Market Update – European Session: Focus On ECB And Timing Of Potential Taper

Notes/Observations

Sweden’s Riksbank sticking to its established policy script; keeps both policy and rate path unchanged

ECB expected to keep policy steady; focus on whether ECB provides guidelines on QE taper

China Aug FX Reserves registers its 7th straight month of increase to $3.0915T

Overnight

Asia:

UN Draft resolution has US seeking to freeze the assets of Kim Jong-Un and ban North Korean guest workers. Also continues to seek an oil embargo on North Korea, though Russia has indicated it opposes this move

White House: Trump, China’s Xi condemned N Korea’s latest provocative, destabilizing action. Both leaders committed to achieving denuclearization of Korean peninsula

Europe:

ECB still not likely to reach decision on QE before the Oct 26th MPC meeting. ECB technical committee said to still be reviewing informal policy proposals for the General Council on various scenarios for size/duration of asset purchase for QE program in 2018

PM's Office said to be asking leaders of largest UK companies to sign letter of support for May's Brexit strategy, but many CEOs are refusing

EU to call on UK to find solutions that avoid the creation of hard border with Ireland and guarantee peace on the island

Catalonia Parliament sets binding referendum on independence from Spain for Oct 1

Americas:

President Trump and Congressional leaders have agreed to pass Harvey aid along with a short term debt limit and govt funding bill (would fund the govt and extend the debt limit through Dec 15th). Both sides want to avoid a default in December

President Trump: military action is not the first choice for dealing with North Korea. Would have to see what happens with N Korea. Had very strong, very frank conversation with China President Xi

Fed Beige Book noted that economic activity expanded at modest pace across all districts. Majority of districts saw limited wage pressures and modest to moderate wage growth.

Energy:

Weekly API Oil Inventories: Crude: +2.8M v -5.8M prior

Economic data

(NL) Netherlands Aug CPI M/M: 9=0.2 v 0.7% prior; Y/Y: 1.4% v 1.3% prior

(NL) Netherlands Aug CPI EU Harmonized M/M: 0.2% v 0.8% prior; Y/Y: 1.5% v 1.5% prior

(JP) Japan July Preliminary Leading Index: 105.0 v 105.1e; Coincident Index: 115.6 v 115.8e

(DE) Germany July Industrial Production M/M: 0.0% v 0.5%e; Y/Y: 4.0% v 4.6%e

(NO) Norway July Credit Indicator Growth Y/Y: 5.7% v 5.9%e

(NO) Norway July Industrial Production M/M: 0.7% v 0.3% prior; Y/Y: 0.5% v 5.4% prior

(NO) Norway July Manufacturing Production M/M: 1.9% v 0.8%e; Y/Y: 1.4% v 1.1% prior

(FR) France July Trade Balance: -€6.0B v -€4.9B prior

(MY) Malaysia Central Bank (BNM) left its Overnight Policy Rate unchanged at 3.00% (as expected)

(CH) Swiss Aug Foreign Currency Reserves (CHF): 716.7B v 714.9B prior

(UK) Aug Halifax House Prices M/M: 1.1% v 0.2%e; 3M/Y: 2.6% v 2.1%e

(SE) Sweden Central Bank (Riksbank) left its Repo Rate unchanged at -0.50% (as expected); maintained its Repo Rate path

(CN) China Aug Foreign Reserves: $3.0915T v $3.095Te (7th straight month of increase)

(EU) Euro Zone Q2 Final GDP Q/Q: 0.6% v 0.6%e ; Y/Y: 2.3% v 2.2%e

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €4.57B vs. €3.5-4.5B indicated range in 2022, 2027 and 2033 Bonds

Sold €1.78B in 0.4% Apr 2022 SPGB; Avg yield: 0.213% v 0.233% prior; Bid-to-cover: 1.88x v 1.60x prior

Sold €1.31B in 1.45% Oct 2027 SPGB; Avg yield: 1.54% v 1.649% prior; Bid-to-cover: 1.97x v 1.23x prior

Sold €1.48B in 2.35% July 2033 SPGB; Avg Yield: 2.17% v 2.29% prior; Bid-to-cover: 1.78x v 1.37x prior

(ES) Spain Debt Agency (Tesoro) sold €700M vs. €250-750M in 0.65% Nov I/L 2027 bonds; Real Yield: 0.371%; Bid-to-cover: 1.94x

(FR) France Debt Agency (AFT) sold total €8.999B vs. €8.0-9.0B indicated range in 2027, 2036, 2041 and 2060 Oats

Sold €5.214B in 1.00% May 2027 Oat; Avg Yield: 0.67% v 0.75% prior; Bid-to-cover: 1.99x v 2.15x prior

Sold €1.575B in 1.25% May 2036 Oat; Avg Yield 1.38% v 1.49% prior; Bid-to-cover: 1.76x v 2.23x prior

Sold €1.28B in 4.50% Apr 2041 Oat; Avg yield 1.49% v 1.50% prior; Bid-to-cover: 1.95x v 2.25x prior

Sold €930M in Apr 4% 2060 Oat; Avg yield: 1.84% v 2.17% prior; Bid-to-cover: 2.13x v 1.53x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 373.8, FTSE flat at 7357, DAX +0.6% at 12283, CAC-40 +0.3% at 5115, IBEX-35 +0.1% at 10140, FTSE MIB -0.4% at 21739, SMI -0.2% at 8839, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes:

European Indices trade mixed with outperfomance in the German Dax, whilst weakness is observed on the FTSE MIB and the Swiss SMI. Markets are trading in a holding pattern ahead of the ECB rate decision later today. In the UK Microfocus continues its momentum higher following on from results from HPE, trading a further 4% higher. Bovis Homes outperforms after results, on the downside Go Ahead Group lags after disappointing results. Elsewhere Altran outperforms following earnings whilst Wendel trades sharply lower.

Looking ahead to the US morning, notable earners include Dell Tech, Conn and Barnes and Noble.

Equities

Consumer discretionary [Havelock [HVE.UK] -50% (Profit warning, Go Ahead Grp [GOG.UK] -8.7% (Earnings)]

Financials: [Ashmore [ASHM.UK] -6% (Earnings), ZPG [ZPG.UK] +4.9% (Acquistion), Direct Line [DLG.UK] +3.6% (No reason seen), Wendel [MF.FR] -7% (Earnings)]

Technology: [ Altran [ALT.UK] +4% (Earnings)]

Healthcare: [Circassia [CIR.UK] +15% (Phase III AMPLIFY trial demonstrated a statistically- significant improvement in lung function in patients with COPD)]

Real Estate: [Bovis Home [BVS.UK] +9% (Earnings)]

Speakers

SwedenCentral Bank (Riksbank) policy statement reiterated that 1st rate hike not seen until mid-2018 but was prepared for more easing if necessary. To change inflation gauge to CPIF and introduce variation band around target; 2% target still applied

Sweden Central Bank (Riksbank) Gov Ingves post rate decision press conference noted that the domestic economy was developing better than expected but too early to make policy less expansionary. SEK currency has strengthened faster than its July forecast

France Constitutional Council said to have approved labor reform process

Norway Stats Agency (SSB) Quarterly forecasts raised 2017 Mainland GDP from 1.9% to 2.0% but cut 2018 Mainland GDP from 2.2% to 2.1%. It also cut 2017 Underlying CPI from 1.7% to 1.6%

Germany Chemical Industry Group (VCI) maintained its 2017 Sales growth at 5.0% and Production growth at 1.5%

Hungary Central bank's Virag: CPI seen returning to around 2% by end-2017

Ukraine President Poroshenko: 2017 GDP growth seen at 1.8%

Turkey Presidential advisor Ertem: Economy can grow over 5% without creating inflation

Malaysia Central Bank policy statement reiterated that its monetary policy stance remained accommodative and expected headline inflation expected to moderat. MYR currency (Ringgit) had appreciated to better reflect fundamentals. Domestic Demand to remain key driver of growth

China FX Regulator SAFE reiterated to keep forex reserves at reasonable, appropriate level

South Korea Foreign Ministry spokesman: Sanctions on North Korea should inflict pain this time and such practical measures were needed

South Korea President Moon: Warned of another North Korea missile launch possibly as early as this Saturday (national founding day)

North Korea: Will take powerful counter-measures in response to US pressure

Currencies

EUR/USD was slightly higher ahead of the ECB rate decision. ECB expected to keep policy steady with particular focus on whether the central bank would provide any guidelines on its looming QE taper. No final decision on the next steps is expected until at least the October meeting, suggesting there are many variations of the wind-down being discussed. The pair has been holding above the 1.1820 level keeping the current uptrend intact

Overall FX markets relatively quiet but the USD remained on soft-footing. USD/JPY slightly lower just below the 109 level as Korea remains on the front burner with another NK missile launch possible around the weekend.

Fixed Income

Bund futures trades at 162.28 down 28 ticks, ahead of the ECB rate meeting. Trading has been range bound with immediate support at 162.93, with support lying just below 162.00.

Gilt futures trades at 127.37 down 22 ticks trading towards the session low, with continued downside targeting 126.88, followed by 126.49. A reversal targets 127.83 initially.

Thursday’s liquidity report showed Wednesday’s excess liquidity fell to €1.773T from €1.780T prior. Use of the marginal lending facility rose sharply to €1.04B from €248M.

Corporate issuance continued to see strong flows with $13.3B coming to market via 11 issuers following on from $22B seen yesterday. Notable issuers included Visa $2.5B 3 part offering, Sinopec $3.25B 4 part offering and Bank of Montreal $2.5B 2 part offering.

Looking Ahead

(IL) Israel Aug Foreign Currency Balance: No est v $110.1B prior

(MX) Mexico Aug Vehicle Production: No est v 286.4K prior; Vehicle Exports: No est v 243.1K prior

05:30 (ZA) South Africa July Total Mining Production M/M: +0.8%e v -2.6% prior; Y/Y: +2.0%e v -0.8% prior; Gold Production Y/Y: No est v -3.6% prior; Platinum Production Y/Y: No est v -13.7% prior

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

06:00 (IE) Ireland Aug CPI M/M: No est v 0.0% prior; Y/Y: No est v -0.2% prior

06:00 (IE) Ireland Aug CPI EU Harmonized M/M: No est v 0.1% prior; Y/Y: No est v -0.2% prior

06:00 (IE) Ireland Aug Live Registry Monthly Change: No est v -3.0K prior; Live Registry Level: No est v 256.8K prior

06:45 (US) Daily Libor Fixing

07:00 (ZA) South Africa July Manufacturing Production M/M: 0.5%e v 0.0% prior; Y/Y: -0.3%e v -2.3% prior

07:30 (CL) Chile Aug International Reserves: No est v $38.4B prior

07:30 (CL) Chile Aug Trade Balance: $0.1Be v $0.2B prior; Total Exports: $5.8Be v $5.2B prior; Total Imports: $5.6Be v $5.0B prior; Copper Exports: No est v 2.5B prior

07:45 (EU) ECB Interest Rate Decision: ECB expected to keep key rates unchanged; Leave Main Refinance Rate unchanged at 0.00%; Leave Marginal Lending rate unchanged at 0.25%; Leave Deposit Rate unchanged at -0.40%

08:00 (CL) Chile July Nominal Wage M/M: 0.5%e 0.4% prior; Y/Y: 4.4%e v 4.4% prior

08:05 (UK) Baltic Dry Bulk Index

08:00 (PL) Poland Aug Official Reserves: No est v $109.8B prior

08:20 (HU) Hungary Central Bank Gov Matolcsy speaks

08:30 (US) Initial Jobless Claims: 245Ke v 236K prior; Continuing Claims: 1.95Me v 1.942M prior

08:30 (US) Q2 Final Nonfarm Productivity: 1.1%e v 0.9% prelim; Unit Labor Costs: 0.6%e v 0.6% prelim

08:30 (CA) Canada July Building Permits M/M: -1.5%e v +2.5% prior

08:30 (EU) ECB Chief Draghi post rate decision press conference

08:30 (EU) ECB updates Staff Projections

09:00 (MX) Mexico Aug CPI M/M: 0.5%e v 0.4% prior; Y/Y: 6.7%e v 6.4% prior, CPI Core M/M: 0.3%e v 0.3% prior

09:00 (RU) Russia Gold and Forex Reserve w/e Sept 1st: No est v $420.5B prior

10:00 (CA) Canada Aug Ivey Purchasing Managers Index (Seasonally Adj): No est v 60.0 prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Weekly DOE Crude Oil Inventories

12:00 (CA) Canada to sell 3-Year Bonds

12:15 (US) Fed’s Meister on economic outlook and monetary policy

19:00 (US) Fed’s Dudley (voter) on economic outlook and monetary policy

USDJPY Showing Neutral Picture In Short And Medium Term, Risk Is To The Downside

USDJPY is showing a neutral picture in the medium term, trading within a broad range between 108.00 and 114.50 since March. The near-term bias is also neutral as the pair has been in a consolidation phase since mid-August and is pivoting around the key 110.00 level. This level is also the 50% Fibonacci retracement of the uptrend from 101.18 to 118.66 (November to December 2016 rally).

Momentum oscillators are moving sideways and highlighting the lack of direction in the market. RSI and MACD are also in bearish territory which suggest the immediate bias is tilted to the downside. The July 18 bearish crossover of the 50-day and 200-day moving averages also point to bearishness in the market.

The first support comes in the zone between 107.96 (61.8% Fibonacci) and the key 108.00 level. This is the lower end of the March-September range and a break to the downside would change the overall bias to bearish from neutral with scope to target 105.50.

USDJPY would need to clear 110.00 and break above the top of the recent range at 110.90 to weaken downside pressure. Breaking above the March-September top of the range at 114.49 could see another leg higher for a re-test of the December high at 118.66. From here, there would be increased odds for a resumption of the longer-term uptrend from November 2016.

For now, there is little momentum in the market and the neutral bias is expected to stay in place.

NZDUSD In Clear Downtrend, Ichimoku Cloud Reaffirms Bearish Picture

NZDUSD maintains a weak technical undertone and has been in a clear downtrend since retreating from the July 27 top of 0.7557. The market has been making lower highs and lower lows and is currently trading below the key 0.7200 level.

On the 4-hour chart, the immediate risk is to the downside as prices have fallen below the 20- and 50-period moving averages. The bearish view was strengthened after the crossover of the shorter-term SMA below the 50 SMA on August 23. Downside momentum is gaining traction since the RSI has broken below 50 and is entering bearish territory.

The immediate target to the downside is the August 31 low at 0.7131. From here, the focus would turn to another key area at 0.7057 which acted as support as well as resistance in the recent past (between March to June). The key psychological 0.7000 level is another support which, if broken, would target the multi-month low at 0.6817 (touched on May 11).

The bearish bias remains favorable unless there is a move above support-turned resistance at 0.7200 that would decrease downside pressure. A rise above the September 5 high of 0.7262 and cloud top would open the way to key resistances level at 0.7300 and 0.7340. A continued push higher would see a shift in the current bearish trend.

For now, there are no signals for a change in the downtrend. Ichimoku cloud chart analysis reaffirms the bearish picture as NZDUSD is below the cloud.

Dollar Fails To Rise On Higher US Debt Ceiling, Focus On ECB

After a surprise rate hike from the Bank of Canada, US Congressional leaders and the president decided unexpectedly on late Wednesday to raise the government’s debt limit. However, the dollar failed to strengthen, as geopolitical risks continued to weigh on the markets, while the Fed’s Vice Chairman surprised markets by submitting his resignation. The euro was also in focus, as investors are widely expecting the European Central Bank to kick off its policy meeting later today.

On Wednesday, the US president, Donald Trump agreed with congressional leaders to lift the maximum amount the government can borrow and extend funding until December 15. However, this was a surprise as Trump’s fellow Republicans were hoping for a longer-term debt limit extension rather than a shorter-term deal, which was mainly supported by Democrats whose proposal was finally accepted by Trump. The US Treasury Secretary, Steven Mnuchin, said to reporters after the decision that the president chose to keep the period short as he considers raising military funding this year given the heightened risks from North Korea.

In the same day, Trump said that a military response against to North Korean threats was “certainly not his first option”, while he favored stricter sanctions that will likely limit North Korea’s spending on nuclear programs. Meanwhile, in South Korea, the public protested the deployment of the country’s defense system which took place early today in order to strengthen country’s military power to refute North Korean potential attacks. This comes after the South Korean Business Daily reported that North Korea is planning to fire an intercontinental ballistic missile probably this Saturday when the regime will celebrate the founding day.

In other news out of the US, the Fed Vice Chairman, Stanley Fischer, unexpectedly submitted his resignation on Wednesday eight months before his term ends, saying that he would leave his position in mid-October.

The dollar index could not gain on the debt ceiling decision, retreating by 0.11% to 92.11 during Asian trading.

Dollar/yen declined by 0.13% to 109.09 while dollar/swissie was mainly flat around 0.9562.

Euro/dollar edged up by 0.08% to 1.1925 ahead of the ECB policy meeting later today when the markets will focus on ECB Chief Maio Draghi’s new hints on the strategy the central bank will follow to taper its asset holdings.

The loonie eased against its US counterpart but maintained most of the gains it attracted yesterday, which drove the currency to a more than two-year high after the BOC decided to hike rates to 1% on Wednesday. Dollar/loonie was slightly down by 0.01% at 1.2217.

The aussie followed a downtrend early in the session as data out of the country showed that retail sales and trade balance fell short of expectations in July. Household spending posted zero growth m/m, missing the forecast of a rise of 0.3%. The figure fell below the previous mark of 0.2% which was downwardly revised from 0.3%. Regarding the trade balance, the surplus narrowed from A$0.888bn to A$0.460bn, while analysts expected a surplus of A$0.875bn.

Following the data, the aussie retreated by 0.16% to $0.7986.

Looking at commodities, oil prices declined from yesterday’s highs as the weekly report from the American Petroleum Institute showed that oil inventories rose by 2.791mn barrels last week while expectations were for the figure to increase by 4.000mn barrels. The change in inventories was at negative 5.780mn barrels in the week ending August 31. However, experts believe that future reports will give a clearer picture on the negative impact of the disastrous tropical storm Harvey caused to the US oil industry, while the EIA statement is also expected to provide evidence on US oil inventories later today. In the meantime, energy producers are also worried about Hurricane Irma which has battered the Carribean yesterday and is currently heading towards Florida.

WTI crude dropped by 0.24% to $49.04 per barrel while Brent declined by 0.35% to $54.01.

Gold was up by 0.26% to 1337.40 an ounce as geopolitical uncertainties linger in the background.

ECB Seen Holding Off On Taper Talk

It's been a steady, albeit unremarkable, start to trading on Thursday, with risk appetite gradually improving ahead of today's ECB decision.

The euro has been well bid this morning ahead of the ECBs interest rate decision and Mario Draghi's press conference, with traders either anticipating taper talk or testing the central banks resolve as it prepares to further wind down its quantitative easing program. The current program expires at the end of the year and there is a clear desire to reduce it to zero and normalize monetary policy, but with this comes many obstacles, most notably the goal of 2% inflation.

Not only is the ECB far from achieving this target but this year's appreciation of the euro has made the job of do so all the more difficult. The euro is up more than 13% against the dollar this year and more than 7% against the pound which will continue to weigh on inflation going forward. The issue for the ECB is that by announcing a reduction in stimulus, it risks exacerbating the problem by driving the euro higher again, assuming of course that this isn't already priced in.

The ECB is clearly already uncomfortable with the gains that the currency has made – as seen by repeated mentions of it and coincidentally timed “ECB source” leaks referencing QE – to the point that it is now expected to hold off on announcing an extension to the program until later in the year. The likelihood remains that another reduction will be announced now either in October or December with the goal or ending the program at the end of next year but policy makers are clearly being very careful about how and when they announce it so as to avoid any unwanted euro appreciation.

I therefore expect ECB President Mario Draghi to be very dovish today and possibly even leave the door ajar to no tapering to take place when the extension is announced, even if that is extremely unlikely to happen. The goal of this will be simply to take the pressure off the currency ahead of the announcement later in the year and manage its ascent. Whether traders buy it or not is another question and we're already seeing some appetite this morning to test the 1.20 level that has so far held strong.

With risk appetite gradually improving and geopolitics becoming less of a drag on markets, for now, focus is switching back to fundamentals and today's US data will give us some insight into just that. Weekly jobless claims, non-farm productivity and unit labor costs data will all be released ahead of the open on Wall Street today and we'll also get crude inventory numbers from EIA. A build of a little over 4 million barrels is expected this week with the effects of Hurricane Harvey driving much of the gains.

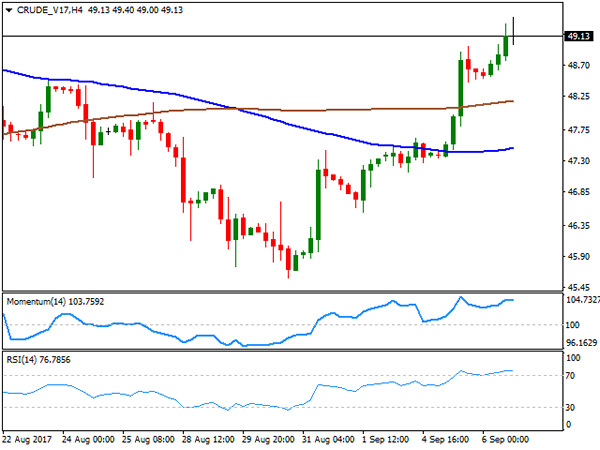

Technical Outlook: WTI Oil May Come Under Pressure On Fears Of Hurricane Irma Impact, Rising Oil Inventories

WTI oil price is consolidating in early Thursday’s trading after strong bullish acceleration in past two days peaked at $49.40.

Strong recovery rally from $45.57 low retraced 76.4% of $50.41/$45.57 pullback, as oil price received strong boost on increased demand after Texas refineries were restarted.

Technical studies on daily chart are in strong bullish setup but overbought slow stochastic suggests oil price may show hesitation ahead of key barriers at $49.65 (200SMA) and psychological $50.00 barrier.

Oil is awaiting release of EIA crude stocks data today (release was delayed for one day due to US Labor Day holiday on Monday) which may pressure the oil price as forecast for today shows a build of oil inventories by 4 million barrels after series of strong draws in previous few weeks.

On the other side, release of API crude stocks data on Tuesday showed build of 2.8 million barrels last week, compared to forecasted build of 4.0 million barrels.

Rising oil inventories signal lower price and the oil price may come under increased pressure on rising fears on impact from Hurricane Irma which is approaching the US coast and may interrupt oil shipments in and out the US.

Session low at $48.93 marks initial support followed by former highs at $48.72 and broken Fibo 61.8% barrier at $48.56.

Res: 49.40, 49.65, 50.00, 50.20

Sup: 48.93, 48.72, 48.56, 47.89

Technical Outlook: AUDUSD – Extended Hesitation At 0.8000 But Bulls Remain Intact

The Aussie dollar remains bid but show strong hesitation at 0.8000 resistance which was dented on Tue/Wed's spikes to 0.8028/20 but so far without close above. In addition, long-legged Doji that was left on Wednesday supports the notion. The pair came under pressure overnight after Australian Retail Sales miss (0.0% in July vs 0.3% forecast) but dips were limited so far at 0.7974, keeping intact rising 10SMA (currently at 0.7960) which marks initial support. Daily techs are in full bullish setup and supportive for further advance, but close above 0.8000 is required to generate bullish signal for extension towards key barrier at 0.8065 (23 July new 26-month high) and extension of broader uptrend on break. On the other side, repeated failure at 0.8000 would risk extended consolidation which needs to hold above 0.7960/50 supports (10SMA/daily Tenkan-sen) and keep immediate bulls intact. Otherwise, break lower would signal recovery stall and stronger pullback which would expose daily Kijun-sen (0.7918) and daily cloud top (0.7894)

Res: 0.8028, 0.8042, 0.8065, 0.8100

Sup: 0.7974, 0.7960, 0.7950, 0.7918

Daily Technical Analysis: USDCAD Down After An Unexpected Rate Hike

As we have seen tightening in the US by the Fed over the past year, there usually is a correlation with other Western economies following the US lead in returning Monetary Policy to historical levels. In this case, the BoC had increased their rate for the second time in recent months largely following an improvement in GDP Growth, along with price stability in their major export Oil and Gas. Needless to say, BoC is somewhat hamstrung with its ability to continue hiking due to its high household debt levels along with real estate prices in Toronto having dropped 20% since April 2017.

At this point the USD/CAD is trapped below the POC zone 1.2308-1.2336 (order block, trend line, D H3, W L3, 61.8, EMA89) and we could see another rejection if the price retraces to the zone. The MACD is way below the 0 line, while histograms are up so we might see a retracement. However 4h or strong 1h candle close below 1.2148 should target 1.2070 that is a both a weekly and daily support.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)