Sample Category Title

Fed’s Waller backs further rate cuts, flags tariffs as potential inflation risk

Fed Governor Christopher Waller reaffirmed his support for continued rate cuts in 2025, while emphasizing that the pace will hinge on inflation progress and labor market stability.

In a speech today today, Waller noted that the median expectation from the latest Summary of Economic Projections suggests two 25-basis-point cuts this year, but highlighted the "range of views is quite large" within the FOMC, from no cuts to as many as five. But his "bottom-line message" is that "more cuts will be appropriate".

Waller described the US economy as being on “solid footing,” with a labor market near the maximum-employment objective. "I have seen nothing in the data or forecasts" that suggests the labor market will dramatically weaken over coming months," he added.

The governor pointed to steady progress on inflation but acknowledged upside risks, including geopolitical conflicts and new tariff proposals. “Tariff proposals raise the possibility that a new source of upward pressure on inflation could emerge,” he said. However, he downplayed the likelihood of tariffs significantly altering monetary policy, assuming their effects on prices are neither substantial nor persistent.

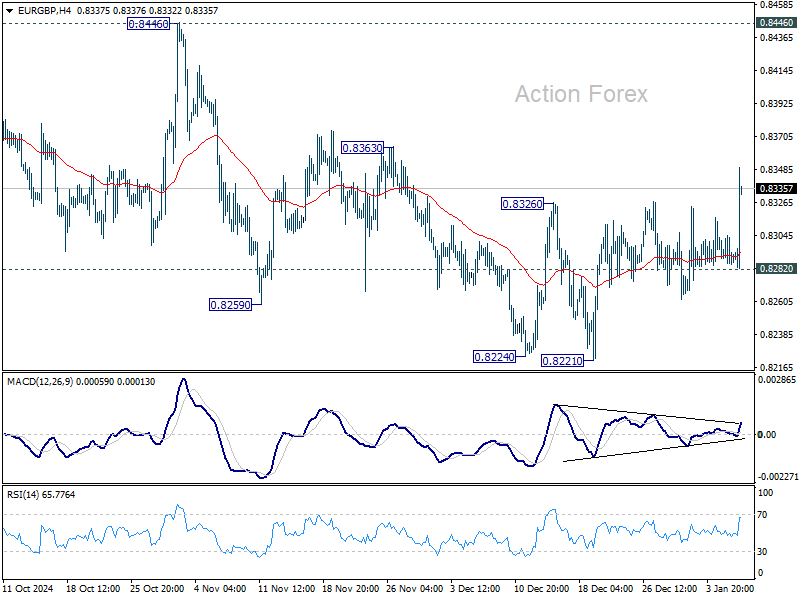

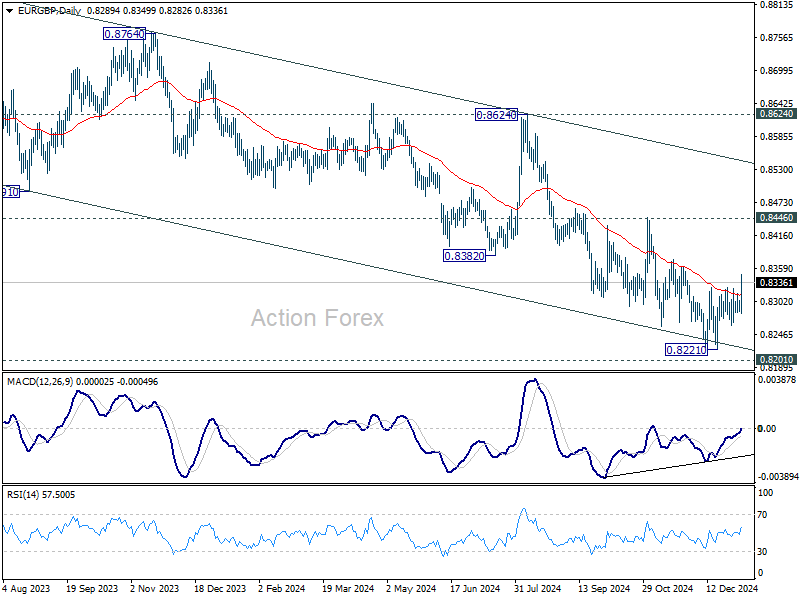

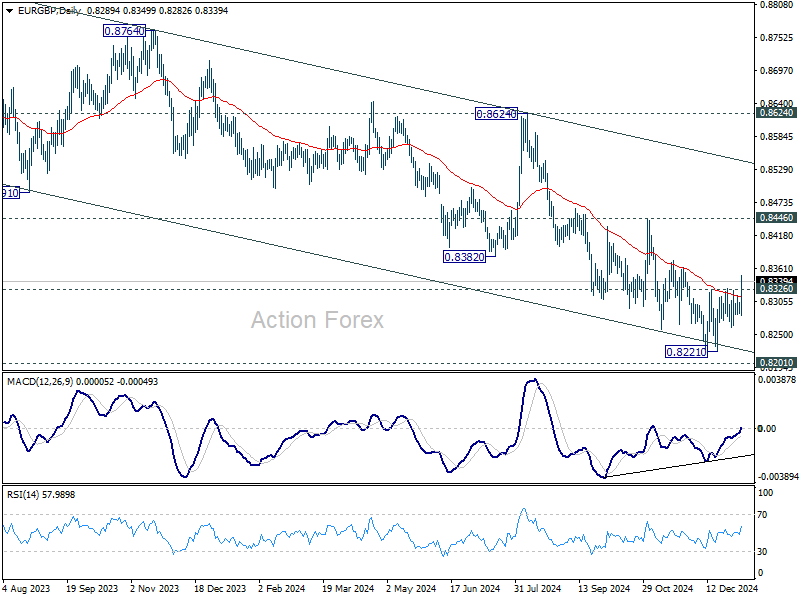

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8280; (P) 0.8293; (R1) 0.8300; More...

EUR/GBP's break of 0.8326 resistance confirms short term bottoming at 0.8221, just ahead of 0.8201 key support. Intraday bias is back on the upside for 0.8446 key resistance. Strong resistance might be seen there to limit upside, at least on first attempt. But for now, further rally will remain in favor as long as 0.8282 support holds, in case of retreat.

In the bigger picture, focus remains on whether 0.8201 key support (2022 low) is strong enough to complete the whole down trend from 0.9267 (2022 high). In any case, medium term outlook will be neutral at best until decisive break of 0.8624 key resistance. Risk will stay on the downside even in case of strong rebound.

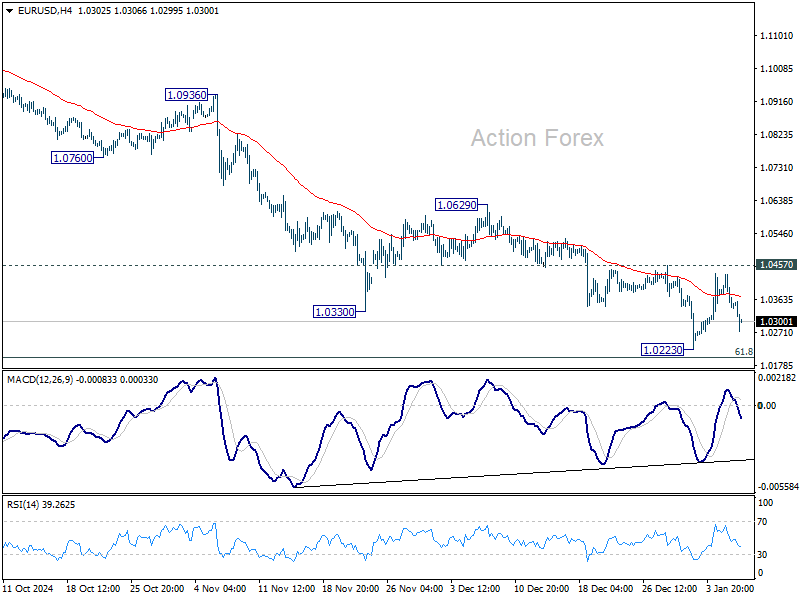

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0309; (P) 1.0371; (R1) 1.0403; More...

EUR/USD is staying above 1.0223 support despite today's deep decline. Intraday bias remains neutral for the moment. Outlook also stays bearish with 1.0457 resistance intact. Firm break of 1.0223 will resume the fall from 1.1213. However, sustained break of 1.0457 will confirm short term bottoming, and turn bias to the upside for 55 D EMA (now at 1.0551).

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

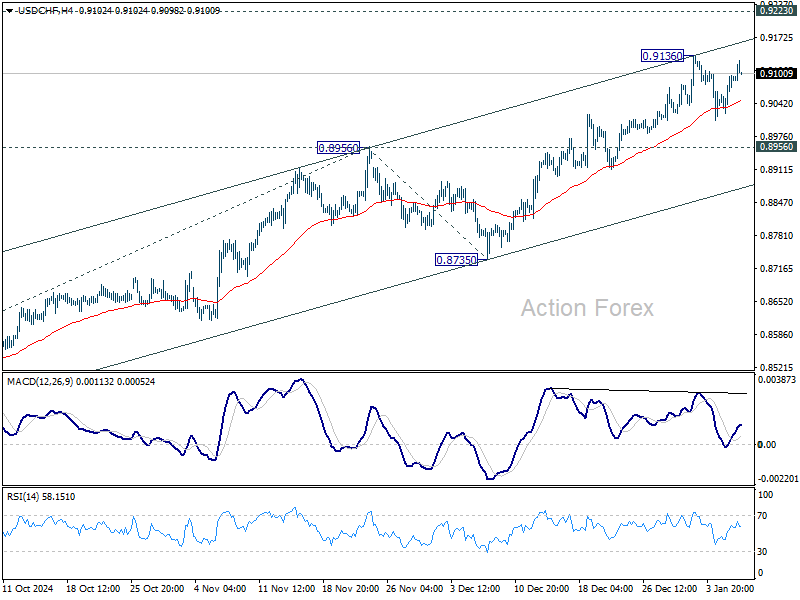

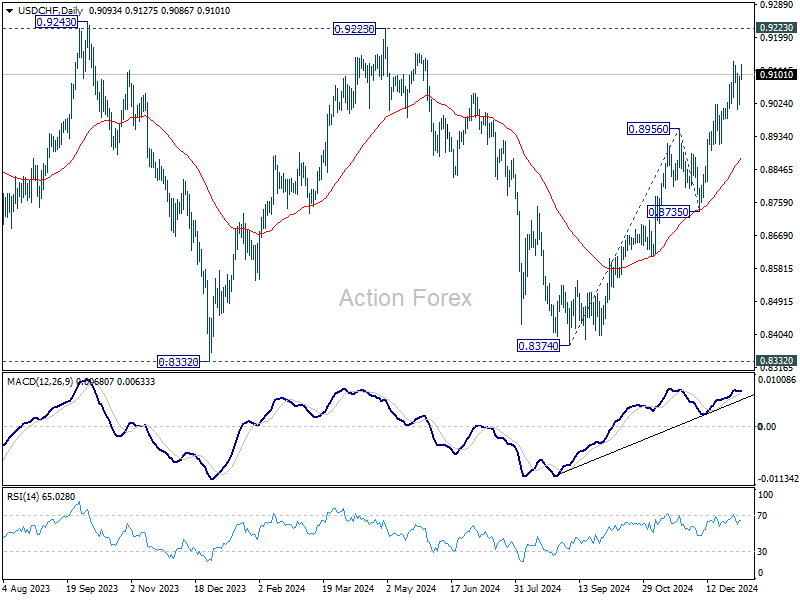

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9047; (P) 0.9073; (R1) 0.9122; More…

Range trading continues in USD/CHF and intraday bias remains neutral. More consolidations could be seen below 0.9136 resistance. But further rally is expected as long as 0.8956 resistance turned support holds. Above 0.9136 will resume the rally from 0.8374 to 0.9223 key resistance next. However, firm break of 0.8956 will turn bias back to the downside for 55 D EMA (now at 0.8879).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

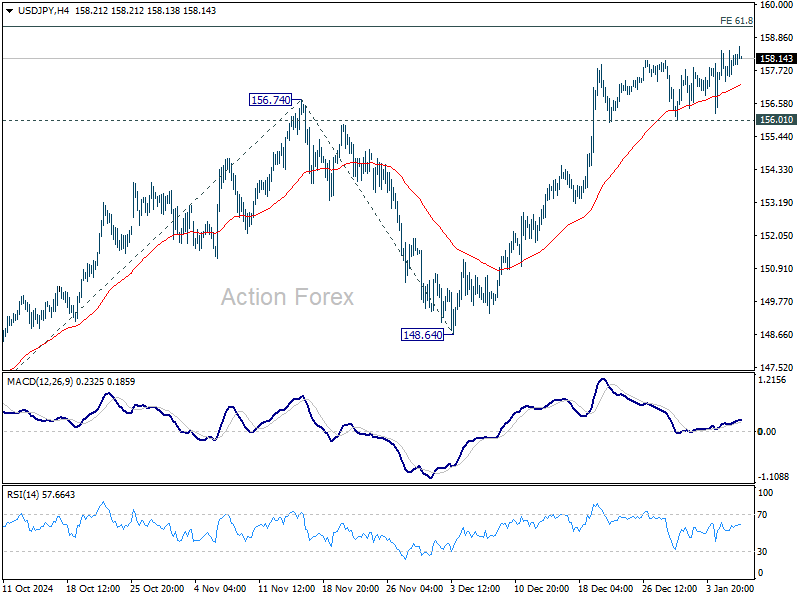

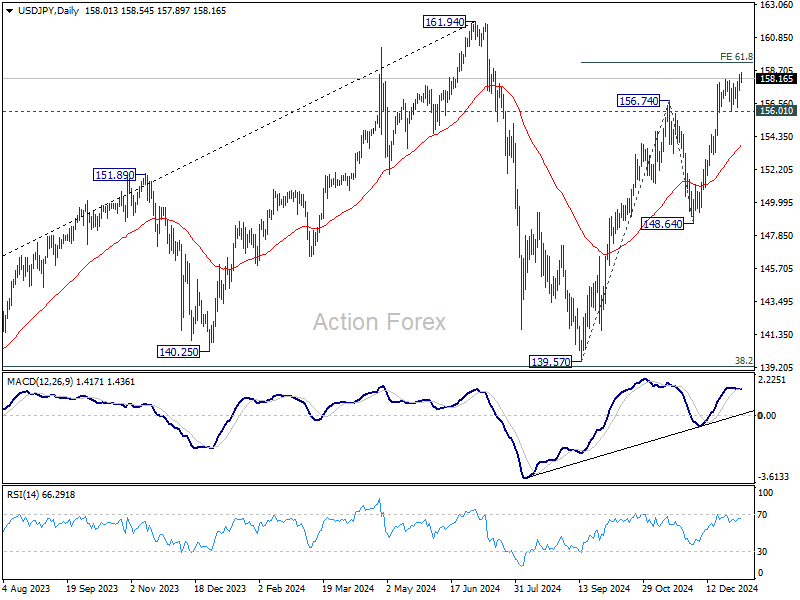

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.49; (P) 157.96; (R1) 158.54; More...

Intraday bias in USD/JPY stays mildly on the upside for the moment. Rise from 139.57 is still in progress for 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will e target 161.94 high. However, break of 156.01 support will indicate short term topping, likely with bearish divergence condition. Intraday bias will then be back on the downside for 55 D EMA (now at 153.82) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

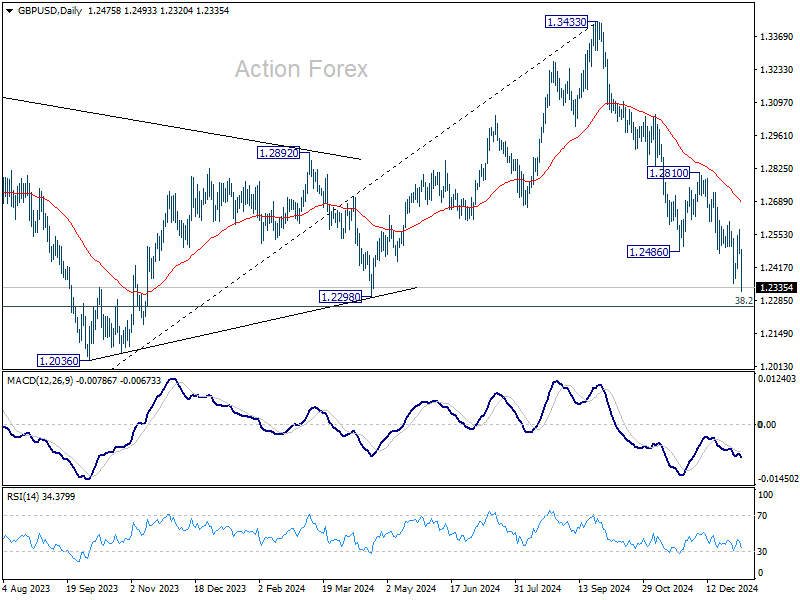

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2445; (P) 1.2510; (R1) 1.2544; More...

GBP/USD's fall from 1.3433 resumed by breaking through 1.2352 today and intraday bias is back on the downside. Deeper decline would be seen to 1.2256/98 cluster support zone. Strong support could be seen there to bring sustainable rebound. But break of 1.2575 resistance is needed to signal short term bottoming. Otherwise, risk will stay on the downside. Decisive break of 1.2256/98 will carry larger bearish implications.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

Dollar Soars and Yields Spike Fuels on Talk of Trump’s Emergency Tariffs

Volatility soared across markets today as reports of emergency trade measures by President-elect Donald Trump overshadowed the day’s economic data. According to CNN, which cited four unnamed sources, Trump is weighing the option of declaring a national economic emergency to justify widespread tariffs on all trade partners, including allies and adversaries.

The plan would rely on the International Economic Emergency Powers Act, a law granting broad authority for a president to manage imports during national emergencies. Trump previously leveraged IEEPA in 2019, when he threatened escalating tariffs on Mexican imports if Mexico failed to curb migrant flows into the United States.

While no final decision on the new measures has been reached, the speculation alone fueled strong rally in Dollar, propelling it to the top spot among major currencies and pushing the 10-year Treasury yield above 4.7%.

Among the majors, Canadian Dollar and Yen followed Dollar’s lead, while Sterling, Kiwi, and Aussie struggled at the bottom of the performance table. Euro and Swiss Franc traded in middle.

Technically, EUR/GBP's strong break of 0.8326 resistance today confirms that a short term bottom was at least formed at 0.8221. Considering bullish convergence condition in D MACD, and the notable support from 0.8201 key level, current rebound should likely sustain to 0.8446 resistance, even though it's still early to declare medium term bullish reversal.

US initial jobless claims fall to 201k vs exp 218k

US initial jobless claims fell -10k to 201k in the week ending January 4, below expectation of 218k. That's also the slowest number since February 2024. Four-week moving average of initial claims fell -10k to 223k.

Continuing claims rose 33k to 1867k in the week ending December 28. Four-week moving average of continuing claims fell -3k to 1866k.

US ADP employment rises 122k, growth slows in Dec

US ADP private employment data revealed a slowdown in job creation for December, with 122k jobs added, missing market expectations of 143k, and prior month's 146k.

Breaking down the numbers, goods-producing sectors added 10k jobs, while service-providing industries contributed 112k. Among these, healthcare emerged as a standout performer, leading job creation across sectors in the latter half of 2024.

By establishment size, large companies drove the gains with 97k new hires, while medium-sized businesses added 9k, and small firms contributed a modest 5k.

Wage growth continued to decelerate, with year-over-year pay increases for job-stayers at 4.6%, the slowest since July 2021. Job-changers saw slightly better gains at 7.1%, though this marked a decline from November.

Commenting on the results, Nela Richardson, Chief Economist at ADP, noted, “The labor market downshifted to a more modest pace of growth in the final month of 2024, with a slowdown in both hiring and pay gains.”

Eurozone PPI rises 1.6% mom, energy prices drive monthly gains

Eurozone producer prices rebounded more than expected in November, with PPI rising 1.6% mom, surpassing market forecasts of 1.5% mom. On an annual basis, PPI improved to -1.2% yoy from -3.3% in October, slightly better than the anticipated -1.3% yoy. The data highlights the ongoing influence of energy price volatility on the region's industrial sector.

Breaking down the monthly changes, Eurozone's energy prices surged by 5.4% mom, providing the largest contribution to the overall increase. Intermediate goods saw a modest decline of -0.1% mom, while prices for capital goods and non-durable consumer goods remained stable. Durable consumer goods recorded a slight decline of -0.2% mom.

At the EU level, industrial producer prices climbed by 1.7% mom but fell -1.1% yoy. Among member states, Bulgaria (+4.9%), Ireland (+4.5%), and Sweden (+4.2%) posted the highest monthly gains in producer prices, reflecting the energy-driven rise. Conversely, Estonia, Cyprus (-1.4% each), Slovakia (-0.5%), and Luxembourg (-0.4%) saw the sharpest declines, highlighting regional disparities.

Australian monthly CPI rises to 2.3%, but easing core pressures offer RBA relief

Australia's monthly CPI rose from 2.1% yoy to 2.3% yoy in November, slightly above market expectations of 2.2%. Inflation excluding volatile items and holiday travel jumped from 2.4% yoy to 2.8% yoy. However, trimmed mean CPI, a measure closely watched by RBA, declined from 3.5% to 3.2%, signaling some relief in underlying inflationary pressures.

The rise in CPI was influenced by the reduced impact of government electricity rebates compared to previous months. According to Michelle Marquardt, head of prices statistics at ABS, Electricity prices were -21.5% lower in November, compared to a -35.6% annual fall in October." Excluding government rebates, electricity prices would have declined by only -1.7% over the same period.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2445; (P) 1.2510; (R1) 1.2544; More...

GBP/USD's fall from 1.3433 resumed by breaking through 1.2352 today and intraday bias is back on the downside. Deeper decline would be seen to 1.2256/98 cluster support zone. Strong support could be seen there to bring sustainable rebound. But break of 1.2575 resistance is needed to signal short term bottoming. Otherwise, risk will stay on the downside. Decisive break of 1.2256/98 will carry larger bearish implications.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

US initial jobless claims fall to 201k vs exp 218k

US initial jobless claims fell -10k to 201k in the week ending January 4, below expectation of 218k. That's also the slowest number since February 2024. Four-week moving average of initial claims fell -10k to 223k.

Continuing claims rose 33k to 1867k in the week ending December 28. Four-week moving average of continuing claims fell -3k to 1866k.

US ADP employment rises 122k, growth slows in Dec

US ADP private employment data revealed a slowdown in job creation for December, with 122k jobs added, missing market expectations of 143k, and prior month's 146k.

Breaking down the numbers, goods-producing sectors added 10k jobs, while service-providing industries contributed 112k. Among these, healthcare emerged as a standout performer, leading job creation across sectors in the latter half of 2024.

By establishment size, large companies drove the gains with 97k new hires, while medium-sized businesses added 9k, and small firms contributed a modest 5k.

Wage growth continued to decelerate, with year-over-year pay increases for job-stayers at 4.6%, the slowest since July 2021. Job-changers saw slightly better gains at 7.1%, though this marked a decline from November.

Commenting on the results, Nela Richardson, Chief Economist at ADP, noted, “The labor market downshifted to a more modest pace of growth in the final month of 2024, with a slowdown in both hiring and pay gains.”

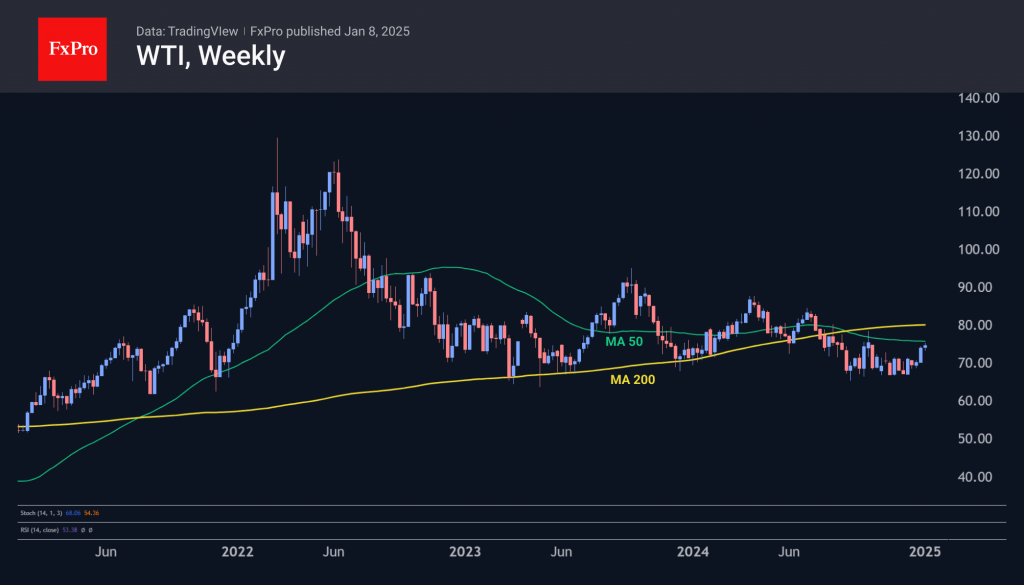

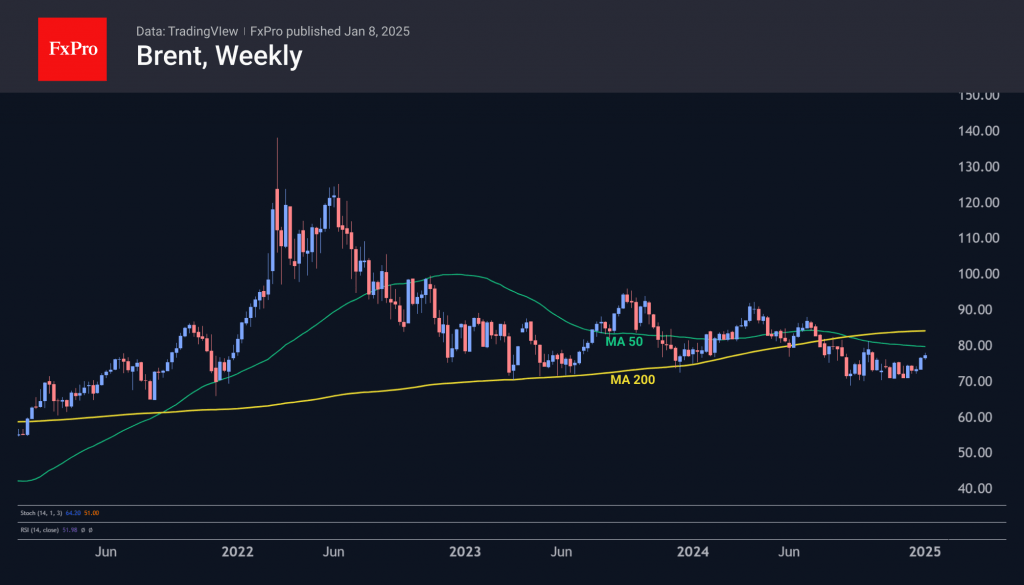

Oil Rises on Balance Shift

Crude oil continues to rise for a third week. On Wednesday, the price of a barrel of Brent crude rose above $77.50, its highest level in almost three months.

Better-than-expected economic data from the US in recent days has fuelled expectations of stronger demand.

At the same time, oil is being helped by the outgoing Biden team’s recent ban on offshore oil drilling.

Another factor on the bulls’ side is the decline in commercial inventories. Last week’s data showed the sixth consecutive week of declines. Although the year-on-year decline is a modest 3.6%, it is hovering near the lower end of the range over the past decade.

The government is reducing the weekly pace of purchases into the oil reserve to 260k barrels from over 1.1m a month earlier, but this is still not enough to tip the balance to the positive side.

Important 200-day moving averages are near $75/bbl for WTI and $78.8/bbl for Brent, separating the downtrend from the uptrend. The North Sea variety still has room to rise by around 2%, while its US counterpart is already testing this line.

According to our observations, the clearer signals for oil come in a weekly timeframe. At the beginning of October, the 50-week level was a resistance that halted the rise. If oil breaks above $75 for WTI and $80 for Brent in the coming week, it could be an important signal for a reversal in growth that could last for months or quarters.