Sample Category Title

Technical Outlook: USDJPY – Extension Above Weekly Cloud, Eyes Immediate Target At 112.18, Fed Is In Focus For More...

Strong bullish signals are generating on Monday's fresh acceleration above weekly cloud top (above which the pair closed last week) and probe above next pivots at 111.80/87 (weekly Tenkan-sen/daily 55SMA). Broader dollar bulls received boost on lift above weekly cloud and may accelerate through next key barrier at 112.18 (31 Mar high) for further retracement of larger 115.49/108.11 descend. Repeated close above weekly cloud will be seen as confirmation of bullish continuation, however, focus is on the tone of Fed's meeting that ends on Wednesday that is expected to give fresh direction signals for the greenback.

Res: 112.18, 112.67, 113.00, 113.36

Sup: 111.36, 111.19, 110.85, 110.44

EURUSD Intraday View

European markets are closed today in in observance of Labor Day so we can expect limited price action and no real breakouts or trend changes yet. That said, EURUSD can see another test of 1.0950 high if we consider that drop was made in three waves at the end of last week. But we still think that upside is going to be limited, so reversal may follow sometime this week.

EURUSD, 1H

Equities Higher, USD Mixed Following Averted Shutdown Of US Congress

Global equities rose with U.S. futures, fixed income retreated and JPY weakened as a tentative deal by the U.S. Congress to avert a government shutdown overshadowed weaker economic data from China and the U.S. over the past few days. Per Republican and democratic aides, the U.S. House and Senate negotiators reached a tentative bipartisan agreement Sunday night on a $1.1 trillion bill to keep the government open through the end of September. The news triggered a swing in markets after equities and currencies' traders had been loath to take additional risk ahead of a busy week for macro-economic events and data.

Japanese equities advanced to their highest level since March after their best week of the year. With Japan225 holding firm above 19300. JPY weakened for the fifth day out of six, comfortably holding above 111.50. Gold has retreated to 1260 following the retracement of US treasuries.

Oil is holding at its lowest level in a month trading just above 49.00 with high inventories dragging on markets that have been grappling with a global supply glut for the last few years. Iran's oil minister said on Saturday that “OPEC and non-OPEC countries had given positive signals for an extension of output cuts, which Tehran would also back”. The Organization of the Petroleum Exporting Countries (OPEC)meets this month to discuss oil supply policy.

Trading volumes are lower than average due to the Labor Day/May Day holiday in Asia and Europe. Later this week Japan will be closed for a three-day holiday.

Traders will be watching comments from a policy meeting of the Federal Open Market Committee this week with the monthly U.S. employment report on Friday being a major focus. We will also see corporate earnings from global heavyweights. The second round of the French presidential election takes place May 7, candidate Marine Le Pen said Monday she would begin negotiations on a euro exit immediately if elected. Traders are also weighing the possibility of escalating tension between the U.S. and North Korea.

Technical Outlook: GBPUSD Eases From Fresh Multi-Month High, Stronger Corrections Signals Expected Below 1.2876/59

Cable eased to 1.2900 zone in early Monday, after peaking at 1.2963 on Friday (the highest since 30 Sep 2016) but holds strong bullish stance that resulted in the third straight bullish week and made the strongest monthly gains after Brexit vote. Comments released on Sunday showed the first stronger verbal clash between EU officials and British PM, signaling tough divorce negotiations. Sterling is maintaining strong bullish sentiment, accompanied with firmly bullish technicals, eyeing psychological 1.3000 barrier after former peak at 1.2904 was taken out. However, further corrective easing could be sparked by overbought daily RSI/slow stochastic. Below 1.2900 handle, hourly cloud (spanned between 1.2894 and 1.2876) marks next good support, underpinned by daily Tenkan-sen in steep ascend (currently at 1.2859). Break here would signal stronger correction towards 1.2834 (Fibo 61.8% of 1.2755/1.2963 upleg) and round-figure 1.2800 support. Key supports lay at 1.2700/55 (low of recent consolidation), loss of which would generate stronger bearish signal.

Res: 1.2943, 1.2963, 1.3000, 1.3055

Sup: 1.2900, 1.2876, 1.2859, 1.2821

Technical Outlook: EURUSD Is Looking For Firmer Signals From Fed, NFP This Week For Eventual Break Out Of One-Week...

The Euro remains within the previous week's range, underpinned by 200SMA but repeated upside rejections at 1.0950, keep the larger rally from 1.0568(10 Apr trough) limited for now. Firm bullish setup of daily MA's that formed multiple bull-crosses and strong momentum studies are supportive but reversal of slow stochastic from overbought territory offsets bullish signals for now. Friday's daily candle with long upper shadow weighs on the near-term structure, however, the price is expected to remain directionless while range boundaries (200SMA at 1.0833 and multiple upside rejection at 1.0950) are intact. From the fundamental side, optimism for Macron's victory on the final round of French election and positive recent EU data are supporting the Euro which is eyeing this week's FOMC policy meeting for further signals. Although, Fed is unlikely to change interest rates at this meeting, markets are focusing on the comments after meeting. More hawkish tone would be a good signal for the action in June's meeting that would boost the dollar and send the Euro into deeper correction. On the other side, dovish tone from Fed, accompanied with rising evidence of dysfunctional US Congress, would have a negative impact on the greenback and eventually send the single currency above 1.0950 barrier towards next target at 1.1000. Markets are also focusing on US Nonfarm Payrolls due on Friday, for more clues. Forecast for April is 185K after surprise drop to 98K in March.

Res: 1.0900, 1.0950, 1.1000, 1.1033

Sup: 1.0850, 1.0833, 1.0804, 1.0776

Market Update – Asian Session: China Official PMIs Slow To 6-Month Lows

Asia Mid-Session Market Update: China official PMIs slow to 6-month lows; Risk trade recovers on reports of US govt funding agreement

Friday US Session Highlights

(US) Q1 ADVANCE GDP ANNUALIZED Q/Q: 0.7% V 1.0%E; PERSONAL CONSUMPTION: 0.3% V 0.9%E

(US) Q1 EMPLOYMENT COST INDEX (ECI): 0.8% V 0.6%E

(US) APR CHICAGO PURCHASING MANAGER: 58.3 V 56.2E; new orders and employment show significant m/m growth

(US) APR FINAL MICHIGAN CONFIDENCE: 97.0 V 98.0E

Politics

(US) Congress negotiators from both parties said to have reached a tentative deal on $1.1T omnibus spending bill to fund the govt through Sept 30th - financial press

(FR) French presidential candidate Le Pen indicating she would not rush to leave the euro if elected - press

(US) Pres Trump signs Congressional stopgap funding to keep the govt open until May 5th

Weekend US/EU Corporate Headlines

COH: Coach said to be interested in a possible offer for Jimmy Choo after failed takeover of Burberry - UK press

TRCO: Fox and Blackstone said to be in talks to acquire Tribune Media - financial press

Key economic data:

(CN) CHINA APR MANUFACTURING PMI (GOVT OFFICIAL): 51.2 (6-MONTH LOW) V 51.6E; NON-MANUFACTURING PMI: 54.0 (6-MONTH LOW) V 55.1 PRIOR

(JP) JAPAN APR FINAL PMI MANUFACTURING: 52.7 V 52.8 PRELIM (confirms 8th straight month of expansion)

(AU) AUSTRALIA APR MELBOURNE INSTITUTE INFLATION M/M: 0.5% (3-month high) V 0.1% PRIOR; Y/Y: 2.6% (highest since July 2014) V 2.2% PRIOR

(AU) AUSTRALIA APR AIG MANUFACTURING INDEX: 59.2 V 57.5 PRIOR; 7TH MONTH OF EXPANSION

(AU) AUSTRALIA APR CORELOGIC RPDATA HOUSE PRICES M/M: 0.1% V 1.4% (slowest gain in 16-months)

(KR) SOUTH KOREA APR TRADE BALANCE: $13.3B V $8.6BE

Asia Session Notable Observations, Speakers and Press

Asian trading is light to start the week despite the release of key data out of China, with most markets closed for May 1st Labor Day. April's official manufacturing and non-manufacturing PMIs both hit 6-month low on lower prices and lower demand - new export orders and employment components slumped to a 3-month low, while Input Prices are at a 10-month low. Risk-on flows were initially depressed with firmer JPY and lower US futures at the open before a mid-day reversal on reports that Congressional negotiators from both parties said to have reached a tentative deal on $1.1T omnibus spending bill to fund the govt through Sept 30th. The deal does not include funding for the border wall and was cheered by Senate Minority leader Schumer as a "good agreement".

In other key datapoints, Japan Apr Manufacturing PMI was confirmed at an 8-month high, as Markit economist noted growth is supported by strengthening overall demand across the South East Asia region with exports as a key driver of growth. Australia MI inflation also trended hotter, reaching July-2014 highs, while Aussie manufacturing expanded for 8th straight month.

Geopolitical tensions around the Korean peninsula remained an issue following a missile test late on Friday. Even though the projectile had reportedly failed, landing within North Korean territory, US CIA director Pompeo was said to be meeting with South Korea's national security officials about the buildup of nuclear capability of the North. Also out over the weekend, US National Security Advisor McMaster assured South Korea that US is paying for THAAD despite Pres Trump claiming Seoul should pay a $1B for deployment.

Japan

(JP) According to Kyodo poll 49% favor changing Article 9 of Japan constitution (outlaws war as a means to settle international disputes involving the state) v 47% opposed

Australia/New Zealand

(AU) Australia Treasurer Morrison did not commit for ruling Coalition to return govt to surplus by 2021; Looking to lower living costs in upcoming May 9th budget - press

(NZ) RBNZ seeks views on capital adequacy framework for banks

(NZ) New Zealand Treasury: Inflation to hold near 2% over 2017 in absence of any additional shocks - press

Korea

(KR) CIA director Pompeo said to have met South Korea National Security officials in Seoul - Korean press

(KR) South Korea Fin Min Yoo: Already working with US on reducing trade surplus - press

(KR) US National Security Advisor McMaster said to have spoken with South Korea chief Kim Kwan-jin; Assured him that US will pay for THAAD system deployment - press

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.4%, Hang Seng closed, Shanghai closed, ASX200 +0.3%, Kospi closed

Equity Futures: S&P500 flat; Nasdaq +0.1%, Dax closed, FTSE100 closed

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0890-1.0910; JPY 111.20-111.75; AUD 0.7465-0.7490; NZD 0.6850-0.6880; GBP 1.2900-1.2940

June Gold -0.3% at 1,264/oz; June Crude Oil -0.2% at $49.24brl; July Copper -0.4% at $2.60/lb

(AU) Australia MoF sells A$300M 2.75% 2035 bonds, avg yield 3.1375%, bid-to-cover 3.59x

Asia equities / Notables / movers

Australia

RCG Corp (RCG) -21.7%; Cuts FY17 Underlying EBITDA guidance to A$74-80M (prior A$85-88M)

Saracen Mineral (SAR) +2.9%; Canaccord Genuity Raised SAR.AU to Buy from Hold

Japan

Sojitz (2768) +3.2%; FY16/17 results

Sharp (6753) +2.7%; FY16/17 results

Ricoh (7752) -7.3%; FY16/17 results

Fujitsu (6702) +9.0; FY16/17 results

ANA (9202) -2.8%; FY16/17 results

JAL (9201) -7.3%; FY16/17 results

Honda (7267) +0.3%; FY16/17 results

Tokyo Electron) +13.3%; FY16/17 results

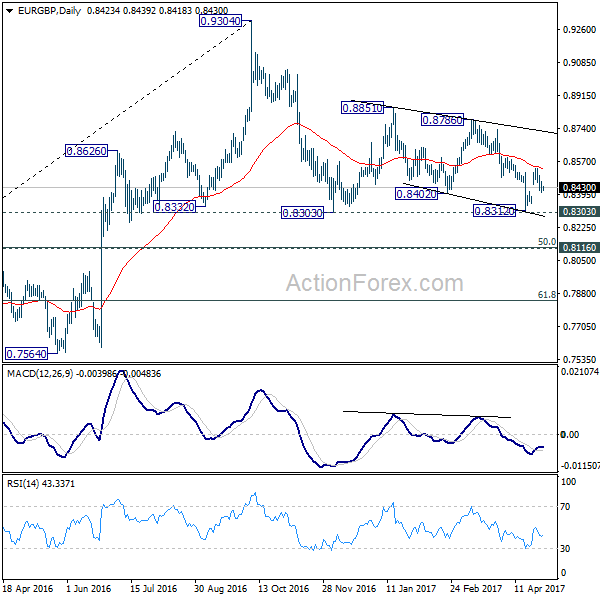

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8390; (P) 0.8426; (R1) 0.8447; More...

Intraday bias in EUR/GBP is mildly on the downside for 0.8303/12 support zone. Break there will extend the corrective fall from 0.9304 to to 0.8116/20 cluster support. We'd expect strong support from there to bring rebound. On the upside, above 0.8461 minor resistance will turn bias to the upside for 0.8529. Break will resume the rebound from 0.8312 and target 0.8786 resistance.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

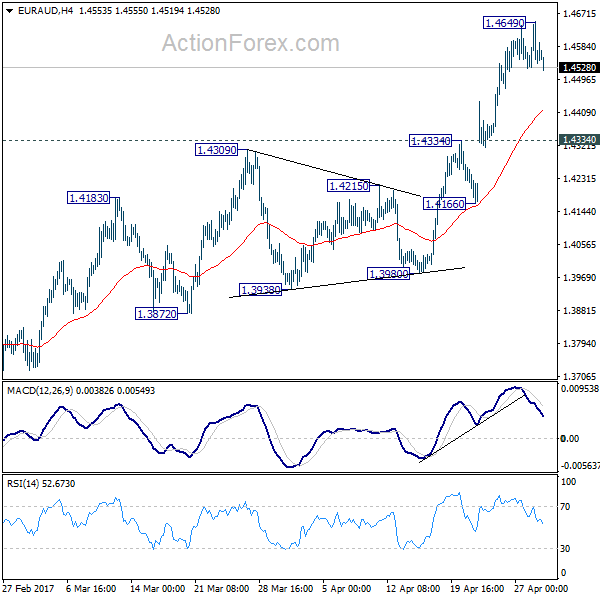

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4496; (P) 1.4573; (R1) 1.4619; More...

Intraday bias in EUR/AUD remains neutral for consolidation below 1.4649 temporary top. We're holding on to the view of trend reversal after defending 1.3671 key support. Hence, downside of retreat should be contained by 1.4334 resistance turned support and bring another rally. Above 1.4649 will target 1.4721 key resistance. Decisive break of 1.4721 will confirm our bullish view. However, break of 1.4334 will suggest rejection from 1.4721 and turn bias back to the downside for 1.3980 support instead.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after defending 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

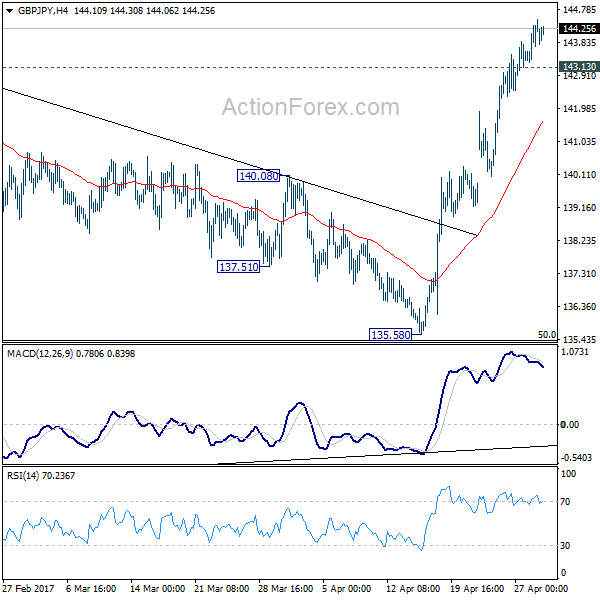

GBP/JPY Daily Outlook

Daily Pivots: (S1) 143.53; (P) 144.01; (R1) 144.74; More....

While GBP/JPY is losing upside momentum, there is no sign of topping yet. Intraday bias remains on the upside for 144.77 resistance. As noted before, consolidation pattern from 148.42 has completed at 135.58, ahead of 135.39 medium term fibonacci level. Break of 144.77 will resume the whole rebound from 122.36 through 148.42 resistance. On the downside, break of 143.13 minor support will turn bias neutral and bring consolidation before staging another rally.

In the bigger picture, based on current momentum, rise from 122.36 bottom should be developing into a medium term move. Break of 38.2% retracement of 195.86 to 122.36 at 150.42 should pave the way to 61.8% retracement at 167.78. This will now be the favored case as long as 135.58 support holds.

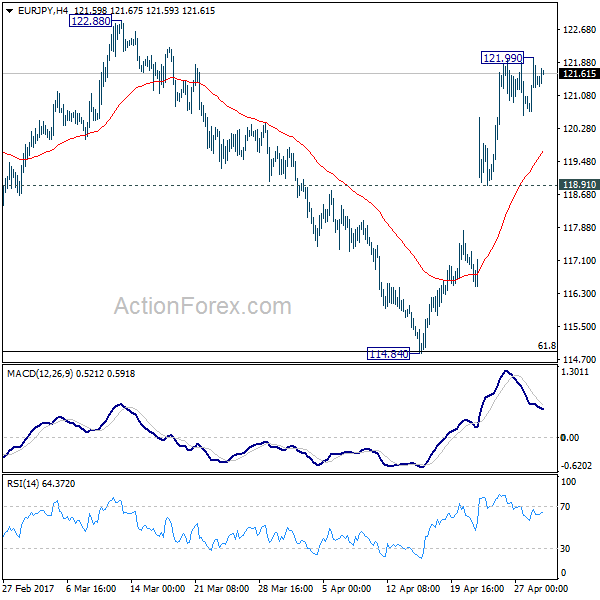

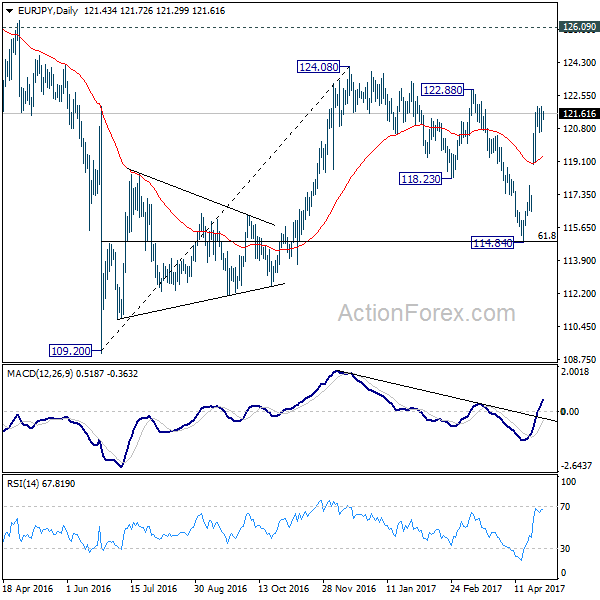

EUR/JPY Daily Outlook

Daily Pivots: (S1) 120.79; (P) 121.39; (R1) 122.09; More...

No change in EUR/JPY's outlook as further rise is expected as long as 118.91 support holds. As noted before, correction from 124.08 should have completed with three waves down to 114.84. Break of 122.88 resistance will extend larger rise from 109.20 through 124.08 high. On the downside, however, break of 118.91 will turn focus back to 114.84 instead.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.