Sample Category Title

USD/JPY Weekly Outlook

USD/JPY rebounded strongly last week and breached 111.58 support turned resistance. The development argues that corrective fall from 118.65 could be completed with three waves down to 108.12. But, we'd prefer to see sustained trading above 111.58 to confirm it. This will be the focus this week.

Initial bias in USD/JPY is neutral this week first. As long as 109.58 minor support intact, further rise is still expected. Sustained trading above 111.58 support turned resistance will indicate that fall from 118.65 is merely a corrective move and has completed. Outlook will then be turned bullish for 115.49 resistance and above. However, break of 109.58 will argue that fall from 118.65 is still in progress and will turn bias to the downside for 108.12 and below.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

In the long term picture, the rise from 75.56 long term bottom to 125.85 medium term top is viewed as an impulsive move. Price actions from 125.85 are seen as a corrective move which could still extend. But, up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

GBP/USD Weekly Outlook

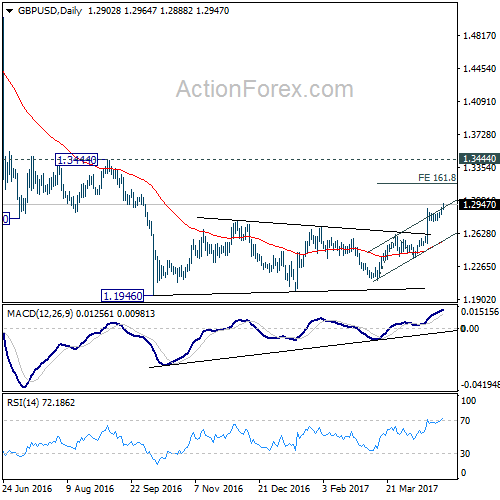

GBP/USD's rally continued last week and outlook is unchanged. Rise from 1.2108 is still in progress and further rally would be seen to 1.3184 projection level. But price actions from 1.1946 are viewed as a corrective pattern. Hence we'd start to look for reversal signal above 1.3184.

Initial bias in GBP/USD remains on the upside this week. Current rise should target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

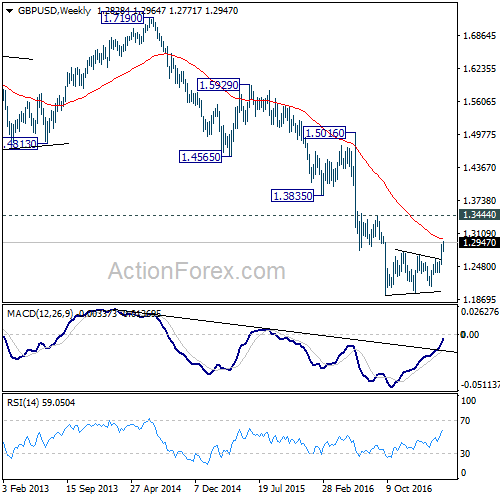

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

In the longer term picture, no change in the view that down trend from 2.1161 is still in progress. Current momentum suggests that the down trend will go deeper than originally expected to 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532.

USD/CHF Weekly Outlook

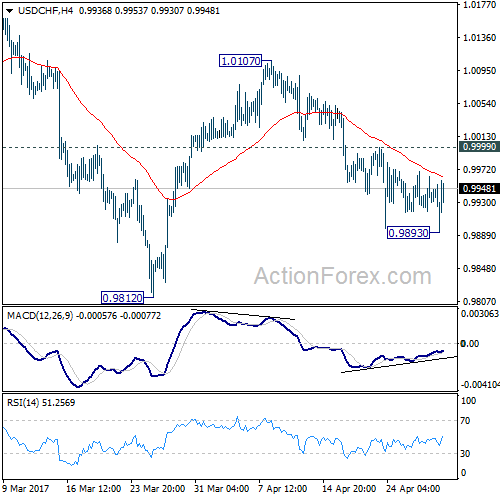

USD/CHF dipped to 0.9893 last week but downside momentum was very unconvincing. At this point, we're slightly favoring the case that 1.0342 is still in progress for another low below 0.9812. But even in that case, such decline is seen as a correction and thus, break of 0.9812 should be brief.

Initial bias in USD/CHF remains neutral this week for consolidations above 0.0.9893 temporary low. Deeper fall is expected as long as 0.9999 minor resistance holds. Break below 0.9893 will target 0.9812 and possibly below. Nonetheless, whole decline from 1.0342 is seen as a correction. Hence, we'll look for bottoming signal below 0.9812. Meanwhile, on the upside, above 0.9999 minor resistance argues that fall from 1.0107 is finished, with bullish convergence condition in 4 hour MACD. In that case, intraday bias will be flipped back to the upside for 1.0107 resistance first.

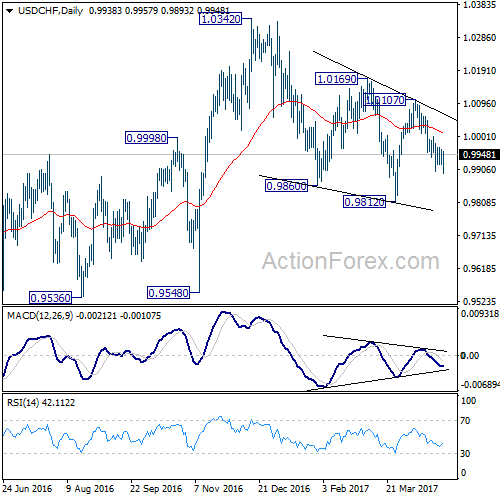

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

The long term outlook in USD/CHF stays a bit mixed for the moment. But in case of another medium term fall, we'd expect strong support from 0.9443/9548 support zone. Meanwhile, firm break of 1.0342 will target 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

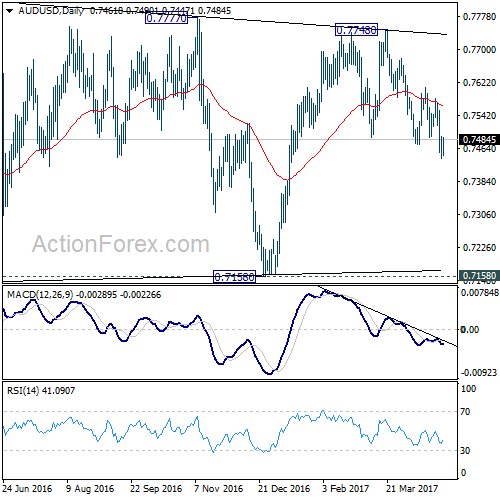

AUD/USD Weekly Outlook

AUD/USD weakened last week and took out 0.7472 support. The development revived that case that rise from 0.71580 has completed at 0.7748. Therefore, deeper fall is now expected back to 0.7144/7158 support zone.

Initial bias in AUD/USD is neutral this week for consolidation above 0.7439 temporary low. But outlook will remain bearish as long as 0.7609 resistance holds. Below 0.7439 will target 0.7144/7158 support zone. At this point, there is no clear sign of larger down trend resumption yet. Hence we'll be cautious on strong support from0.7144/58 to contain downside and bring rebound. On the upside, break of 0.7609 will argue that the fall from 0.7748 has completed. In such case, bias will be turned back to the upside for 0.7748 resistance.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8144) and above.

In the longer term picture, while the down trend from 1.1079 might extend lower, we're not anticipating a break of 0.6008 (2008 low) yet. We'll look for bottoming above there to reverse the medium term trend.

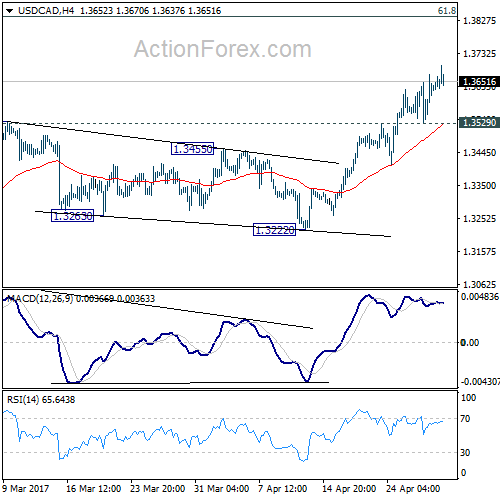

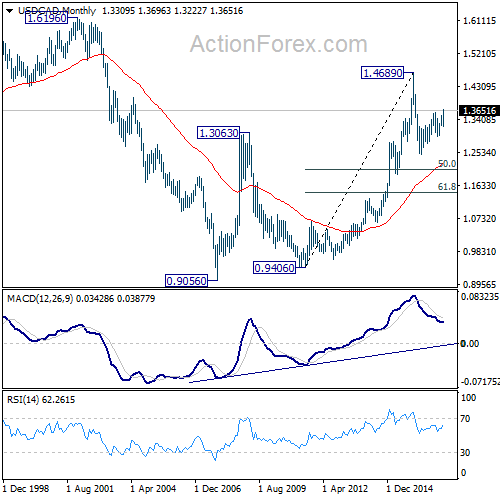

USD/CAD Weekly Outlook

USD/CAD rose strongly to as high as 1.3693 last week. The break of 1.3598 resistance confirms resumption of medium term rise from 1.2460. Further rally would now be seen to next medium term fibonacci level at 1.3838 ahead.

Initial bias in USD/CAD remains on the upside this week. Current rise from 1.3222 should now target 1.3838 fibonacci level. Rise from 1.2460 is having a corrective structure. Hence, we'd look for topping signal above 1.3898. On the downside, below 1.3529 minor support will turn bias neutral and bring consolidation. But for now, outlook will remain bullish as long as 1.3222 support holds.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.3222 support will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

In the longer term picture, rise from 0.9056 (2007 low) is viewed as a long term up trend. It's taking a breath after hitting 1.4689. But such rise expected to resume later to test 1.6196 down the road.

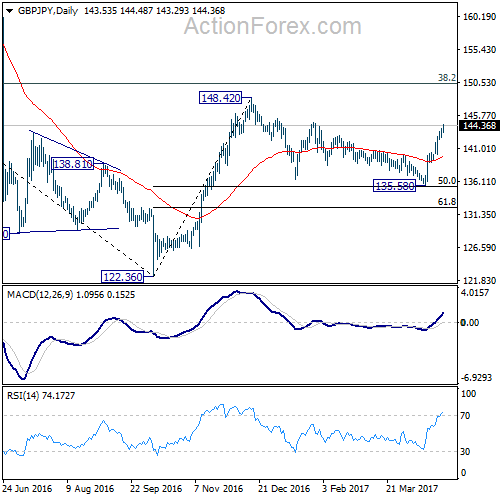

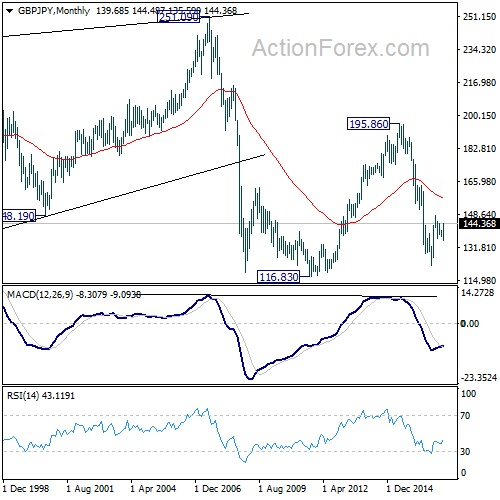

GBP/JPY Weekly Outlook

GBP/JPY rose sharply to as high as 144.48 last week. The development should have confirmed our view that consolidation pattern from 148.42 has completed at 135.58, ahead of 135.39 medium term fibonacci level. Further rise should be seen through 148.42 ahead.

Initial bias in GBP/JPY remains on the upside this week. Break of 144.77 resistance will likely resume the whole rebound from 122.36 through 148.42 resistance. On the downside, break of 143.13 minor support will turn bias neutral and bring consolidation before staging another rally.

In the bigger picture, based on current momentum, rise from 122.36 bottom should be developing into a medium term move. Break of 38.2% retracement of 195.86 to 122.36 at 150.42 should pave the way to 61.8% retracement at 167.78. This will now be the favored case as long as 135.58 support holds.

In the longer term picture, based on the impulsive structure of the decline from 195.86 to 122.36, such fall should be completed yet. But we will now pay close attention to the structure of the rise from 122.36 to determine whether it's a corrective move, or an impulsive move. That would decide whether a break of 116.83 low would be seen.

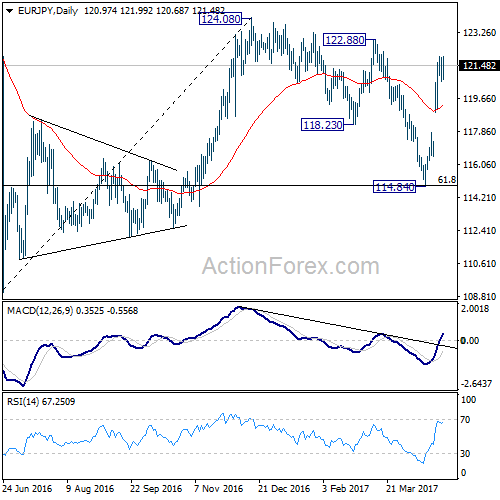

EUR/JPY Weekly Outlook

EUR/JPY jumped to as high as 121.99 last week. The development indicates completion of correction from 124.08, with three waves down to 114.84. And, whole medium term rebound from 109.20 is resuming. We'd expect further rally in near term, through 124.08 to 126.09 key resistance next.

Upside momentum in EUR/JPY is a bit unconvincing as seen in 4 hour MACD. Further rise is expected this week as long as 118.91 support holds. Above 121.99 will target 122.88 resistance. Decisive break there should send EUR/JPY through 124.08 to 126.09 key resistance next. However, break of 118.91 will turn focus back to 114.84 instead.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

In the long term picture, medium term decline from 149.76 is seen as part of a long term sideway pattern from 88.96. We're not seeing any sign of an established long term trend yet. Hence, we'll be cautious on strong support at 94.11 in case of another fall. Also, there could be strong resistance at 149.76 in case of a medium term rise.

EUR/AUD Weekly Outlook

EUR/AUD soared to as high as 1.4334 last week but lost momentum ahead 1.4721 key resistance. Overall, we're holding on to the view of trend reversal after defending 1.3671 key support. As long as 1.3443 support holds, we'd expect another rise to break through 1.4721 to confirm our bullish view.

Initial bias in EUR/AUD is neutral this week first. Some consolidation could be seen but retreat should be contained by 1.4334 resistance turned support and bring another rally. Above 1.4649 will target 1.4721 key resistance. Decisive break of 1.4721 will confirm our bullish view. However, break of 1.4334 will suggest rejection from 1.4721 and turn bias back to the downside for 1.3980 support instead.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after defending 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

In the longer term picture, the rise from 1.1602 long term bottom isn't over yet. We'll keep monitoring the development but there is prospect of extending the rise to 61.8% retracement of 2.1127 to 1.1602 at 1.7488 and above. However, sustained trading below 1.3671 should confirm trend reversal and target 1.1602 long term bottom again.

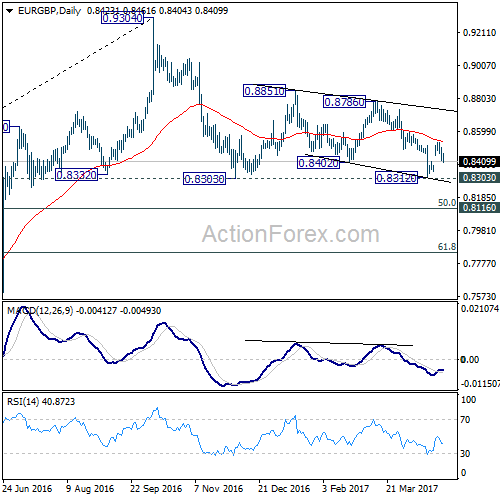

EUR/GBP Weekly Outlook

Despite rebounding to 0.8529 last week, EUR/GBP quickly lost momentum and reversed. The development now suggests that fall from 0.8786 could be resuming. And focus is back to 0.8303/12 support zone in near term. Overall, price actions form 0.9304 is seen as a corrective pattern that is extending.

Initial bias in EUR/GBP is mildly on the downside this week for 0.8303/12 support zone. Break there will extend the corrective fall from 0.9304 to to 0.8116/20 cluster support. We'd expect strong support from there to bring rebound. On the upside, above 0.8461 minor resistance will turn bias to the upside for 0.8529. Break will resume the rebound from 0.8312 and target 0.8786 resistance.

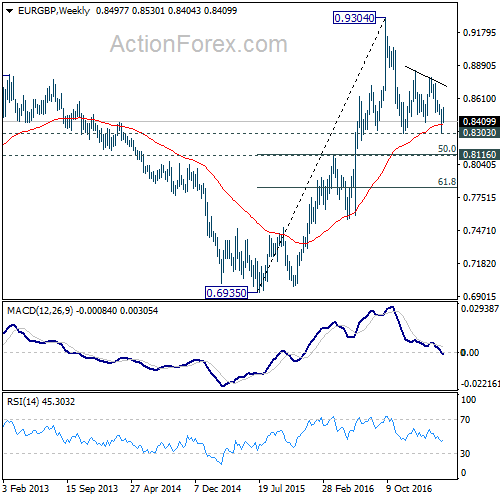

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

In the long term picture, firstly, price action from 0.9799 (2008 high) is seen as a long term corrective pattern and should have completed at 0.6935 (2015 low). Secondly, rise from 0.6935 is likely resuming up trend from 0.5680 (2000 low). Thirdly, this is supported by the impulsive structure of the rise from 0.6935 to 0.9304. Hence, after the correction from 0.9304 completes, we'd expect another medium term up trend to target 0.9799 high and above.

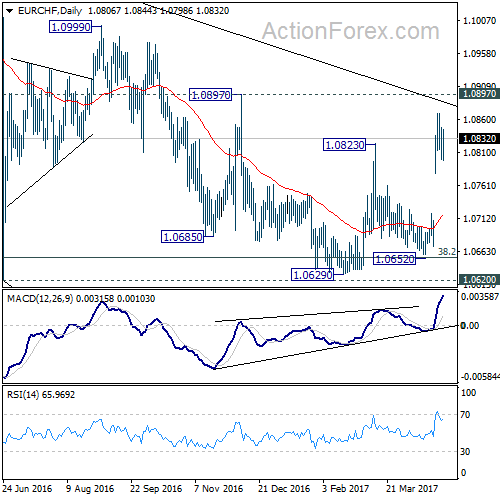

EUR/CHF Weekly Outlook

EUR/CHF surged to as high as 1.0869 last week and formed a temporary top there. It then turned into sideway consolidation. The firm break of 1.0823 is taken as a signal of larger reversal. Hence, further rally is expected in near term to 1.0897 resistance next.

Initial bias in EUR/CHF is neutral this week for consolidation first. Downside of retreat should be contained by 1.0781 minor support and bring another rise. Above 1.0869 will target 1.0897 resistance next. Decisive break there should confirm our bullish view of reversal. However, break of 1.0781 will bring deeper fall back towards 1.0652 support instead.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0652 support holds.