Sample Category Title

Orders For US-Produced Durable Goods Grow Less Than Expected

'Business investment appears to have some better momentum early in 2017 and, while growth is far from hot, we appear to be transitioning away from the declines that plagued much of 2016.' - Robert Kavcic, BMO Capital Markets

Orders for US-manufactured goods rose less than experts estimated in March, official figures revealed on Thursday. The US Department of Commerce reported that orders for durable goods in March soared only 0.7%, following the previous month's increase of 1.8%. Excluding transportation items, orders for core durable goods plunged 0.2%, while analysts anticipated 0.4% growth. This negative figure represented the first decline since June 2016. The main cause of March's drop was associated with weaker demand for automobiles, fabricated metal products and machinery. Namely, the number of orders for motor vehicles tumbled 0.8%, the slowest rate of growth in the last 25 months. At the same time, orders for fabricated metal products slipped 0.8%, whereas machinery orders fell 0.2%. In contrast, bookings in the civil aircraft sector jumped 7%. Furthermore, the number of orders for defence equipment advanced 12%. According to analysts, the slowdown at the end of the Q1 was mainly driven by the strong US Dollar, struggles in the energy sector and the weather-related factors. Nevertheless, they believe that businesses are going to increase their capital expenditures in the near future amid the US President Donald Trump's announced tax reform.

Daily Technical Analysis: Multiple Trend And Reversal Patterns Visible In Forex Market

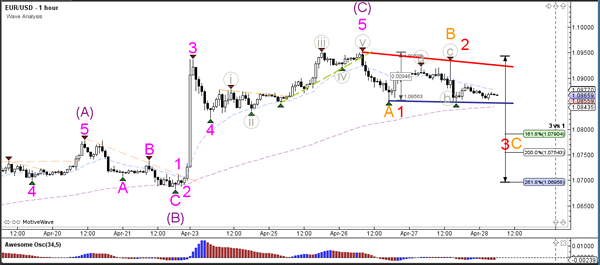

Currency pair EUR/USD

The EUR/could be building a head and shoulders reversal chart pattern (purple boxes), which would be confirmed once price breaks below the support trend line (blue). A bullish break above resistance (red) would invalidate the pattern and could indicate a potential uptrend continuation towards the 78.6% Fibonacci level of wave 2 (green).

The EUR/USD has not managed to break the top as expected yesterday. This could be explained by a potential 123 (red) or ABC (orange) correction. A break below support (blue) could start the bearish continuation towards the Fibonacci targets.

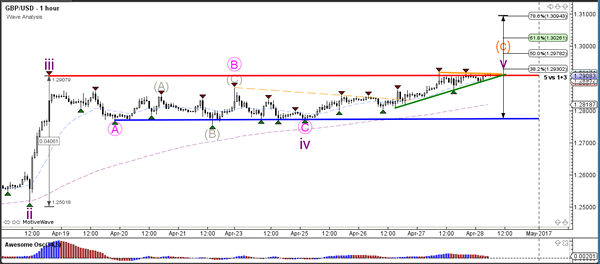

Currency pair GBP/USD

The GBP/USD is challenging the resistance level (red) of the sideways zone (red/blue). A bullish break could see price challenge the round level of 1.30.

The GBP/USD is forming an ascending wedge chart pattern which is indicated by support (green) and resistance (red/orange). A break above the resistance could see price move up towards the Fibonacci targets of wave 5 (purple).

Currency pair USD/JPY

The USD/JPY seems to have completed a wave 3 (brown) and is now be building a potential wave 4 (brown) retracement if price stops at one of the shallow Fibonacci levels (23.6-50%).

The USD/JPY is building a contracting triangle (red/green) chart pattern. A break below the support trend line (green) could see a larger retracement unfold towards the Fib levels of wave 4 (brown).

Market Update – European Session: Euro Zone CPI Higher Than Expected As Core Inflation Breaks Out Of Recent 1-Year...

Notes/Observations

Japan barrage of economic releases pointed towards economic growth but with soft inflation

UK GDP YoY registered a slight miss but bounces off 4-year lows

Euro Zone inflation higher than expected; Core inflation breaks out of recent 1-year range; Headline CPI back at ECB target

Focus turns to US Q1 Advance GDP reading

Overnight:

Asia:

Japan Mar Jobless Rate 2.8% v 2.9%e (matches lowest rate since Jun 1994); Job to applicant: 1.45 v 1.43e (highest since November 1990)

Japan Mar National CPI falls to a 5-month low (Y/Y: 0.2% v 0.3%e); CPI Ex Food, Energy (core-core) registers its first decline since July 2013 (Y/Y: -0.1% v 0.0%e)

Japan Mar Overall Household Spending misses (Y/Y: -1.3% v -0.5%e)

Japan Mar Preliminary Industrial Production MoM reading registers its biggest decline since June of 2016 (MoM: -2.1% v -0.8%e

Europe:

UK Apr GFK Consumer Confidence hits a 4-month los (-7 v -7e) - UK drawing up post-Brexit laws that will allow it to continue imposing sanctions on foreign countries

EU leaders said to be preparing to recognize the "potential for a united Ireland" within the EU. Northern Ireland would seamlessly re-join bloc after Brexit in event of a vote for Irish reunification

Americas:

House Republican leaders said to have delayed a vote on Obamacare replacement bill until next week at earliest due to lack of support. At least 15 House Republicans remain solidly opposed to a revised leadership plan with another 20 leaning towards ‘no' or are still undecided

President Trump: North Korea is my biggest worry; Would love to resolve situation diplomatically, but its "very difficult". There is a chance that we could end up having a major, major conflict with North Korea. Absolutely

Economic Data

(FR) France Q1 Advance GDP Q/Q: 0.3% v 0.4%e; Y/Y: 0.8% v 0.9%e

(DE) Germany Mar Retail Sales M/M: 0.1% v 0.0%e; Y/Y: 2.3% v 2.2%e

(DE) Germany Mar Import Price Index M/M: -0.5% v -0.1%e; Y/Y: 6.1% v 6.5%e

(UK) Apr Nationwide House Prices M/M: -0.4% v +0.1%e; Y/Y: 2.6% v 3.3%e

(FR) France Apr Preliminary CPI M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e

(FR) France Apr Preliminary CPI EU Harmonized M/M: 0.1% v 0.1%e ; Y/Y: 1.2% v 1.4%e

(FR) France Mar Consumer Spending M/M: -0.4% v +0.5%e; Y/Y: -1.0% v +0.9%e

(ES) Spain Q1 Preliminary GDP Q/Q: 0.8% v 0.7%e; Y/Y: 3.0% v 2.9%e

(CH) Swiss Apr KOF Leading Indicator: 106.0 v 107.5e

(AT) Austria Q1 Preliminary GDP Q/Q: 0.5% v 0.6% prior; Y/Y: 2.0% v 1.7% prior

(TR) Turkey Mar Trade Balance: -$4.5B v -$4.5Be

(HU) Hungary Mar Unemployment Rate: 4.5% v 4.5%e

(EU) Euro Zone Mar M3 Money Supply Y/Y: 5.3% v 4.7%e

(NO) Norway Apr Unemployment Rate: 2.8% v 2.8%e

(UK) Q1 Advance GDP Q/Q: 0.3% v 0.4%e; Y/Y: 2.1% v 2.2%e

(UK) Mar BBA Loans for House Purchase: 41.1K v 42.0Ke

(EU) Euro Zone Apr Advance CPI Estimate Y/Y: 1.9% v 1.8%e; CPI Core Y/Y: 1.2% v 1.0%e

(IT) Italy Apr Preliminary CPI (including Tobacco) M/M: 0.3% v 0.2%e; Y/Y: 1.8% v 1.6%e

(IT) Italy Apr Preliminary CPI EU Harmonzied M/M: 0.8% v 0.5%e; Y/Y: 2.0% v 1.6%e

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2022, 2026, 2034 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 flat at 3,562, FTSE -0.2% at 7,222, DAX flat at 12,445, CAC-40 +0.1% at 5,275, IBEX-35 +0.1% at 10,696, FTSE MIB +0.2% at 20,647, SMI -0.1% at 8,836, S&P 500 Futures flat]

Market Focal Points/Key Themes: European equity indices have been trading generally lower in the morning session but currently mixed as market participants digest comments by ECB's Draghi that there isn't enough evidence to change the inflation outlook; banking stocks mixed in the Eurostoxx with shares of Nokia leading the gains in the index in continuation from yesterday's rally after releasing its Q1 results; shares of Barclays trading notably lower in the FTSE 100 after releasing Q1 results; commodity and mining stocks providing some support in the index as copper prices trade higher intraday; Asian markets generally ending lower but mixed overnight.

A plethora of upcoming scheduled US earnings (pre-market) include Aaron's Adient, AGCO, Autoliv, Apollo Global Management, AVX, Barnes Group, Franklin Resources, Colgate-Palmolive, Cabot Oil & Gas, Calpine, Chevron, General Motors, Group 1 Automotive, Goodyear Tire & Rubber, Hill-Rom, Host Hotels & Resorts, IDEXX Labs, KBR, LifePoint Health, LyondellBassell, Moog, Materion, Public Service Enterprise, Portland General Electric, Phillips 66, Royal Caribbean Cruises, Roper Technologies, SAIA, Spirit Airlines, Synchrony Financial, Thomson Reuters, VF Vorp, Ventas, Exxon Mobil, and Olympic Steel.

Equities (as of 09:50 GMT)

Consumer Discretionary: [Continental CON.DE +1.0% (prelim Q1 results)]

Energy: [Fuchs Petrolub FPE.DE -1.9% (Q1 results), Norsk Hydro NHY.NO -6.8% (Q1 results)]

Financials: [Barclays BARC.UK -4.2% (Q1 results), Bankia BKIA.ES -1.1% (Q1 results), CaixaBank CABK.ES +1.6% (Q1 results), Danske Bank DANSKE.DK +0.9% (Q1 results), DNB NOR ASA DNB.NO +0.6% (Q1 results), Royal Bank of Scotland RBS.UK +2.0% (Q1 results), UBS UBSN.CH +3.3% (Q1 results)]

Healthcare: [Sanofi-Aventis SAN.FR +1.7% (Q1 results)]

Industrials: [Electrolux ELUXB.SE +3.6% (Q1 results), Linde LIN.DE -1.6% (Q1 results), MTU Aero MTX.DE +2.6% (Q1 results), Zodiac Aerospace ZC.FR +3.7% (H1 results)]

Technology: [Gemalto GTO.FR -11.6% (Q1 sales), Rexel RXL.FR -3.6% (Q1 results)]

Speakers

SNB's Jordan reiterated view that loose monetary policy was appropriate given the low inflation and that SNB could again cut rates and step up intervention if needed

Turkey Central Bank (CBRT) Quarterly Inflation Report reiterated to keep monetary policy tight until inflation outlook improved and could do extra tightening if necessary. Inflation was expected to fall in coming months. Gradual recovery trend observed in Turkey. TRY currency (Lira) volatility has decreased

China Academy of Social Sciences (CASS): China 2017 GDP growth expected at 6.6%; trade surplus at $303B

South Korea Foreign Ministry: No request from US on THAAD payment; No changes in its operational cost issue

China Foreign Ministry: Will not comment on what China will do if North Korea carried out another nuclear test

Russia Oil Min Novak: Have reached the planned pledged under OPEC cooperation agreement of reducing production by 300K bpd

Currencies

End-of-month and upcoming May-Day holiday kept FX flows at a minimum but the USD was a touch softer as the NY morning approached

EUR/USD was slightly higher but holding below the 1.09 level for the bulk of the morning but the pair surged higher after Apr Core CPI finally broke out of its year-long trading range of 0.7-0.8% to surge to 1.2%

GBP/USD was near 7-month highs ahead of the UK Q1 Advance GDP data but was little changed after the data came in slightly below expectations.

A data barrage of Japanese data failed to move the JPY currency much. USD/JPY was steady at 111.30 area in the session.

Fixed Income

Bund futures trade at 161.42 down down 59 ticks retracing from highs seen yesterday following the ECB rate decision and stronger then expected inflation data out of Europe which has put further pressure on futures. A continued move lower targets 161.07 then 160.65 low. Resistance moves to yesterday high of 162.15 with eventual target of 162.52 gap fill.

Gilt futures trade at 128.12 down 34 ticks, despite slightly weaker Q1 GDP data. Continuation to the downward trend eyes 127.94 followed by 127.74. Resistance stands at 128.58 then 128.81 followed by 129.14. Short Sterling futures trade flat to down 1bp with Jun17Jun18 steepening to 13.0bp.

Friday's liquidity report showed Thursday's excess liquidity fell to €1.587T a fall of €21B from €1.608T prior. Use of the marginal lending facility fell to €259M from €313M prior.

Corporate issuance saw activity pick up with $12.4B coming to market via 7 issuers, with American Express 3 part $4B offering, PepsiCo $3B 5 part offering and Dupont $2B offering accounting for the bulk of the issuance. This put issuance for the week at $24.5B. With no deals expected today, Issuance for the month of April stands just above $80B. For the week ending April 26th Lipper US fund flows reported IG funds net inflows $4.70B bringing YTD inflows to $48.04B, High yield funds reported inflows of $290.7M bringing YTD outflows to $3.98B.

Looking Ahead

05:30 (SL) Sri Lanka Apr CPI Y/Y: No est v 7.3% prior

06:00 (PT) Portugal Mar Retail Sales M/M: No est v 3.1% prior; Y/Y: No est v 1.9% prior

06:00 (PT) Portugal Mar Industrial Production M/M: No est v -0.7% prior; Y/Y: No est v 2.1% prior

06:00 (IT) Italy Mar PPI M/M: No est v 0.3% prior; Y/Y: No est v 3.7% prior

06:00 (IE) Ireland Mar Retail sales Volume M/M: No est v -0.5% prior; Y/Y: No est v 1.1% prior

06:00 (UK) DMO to sell combined £2.0B in 1-month, 3-month and 6-month bills (£0.5B, £0.5B and £1.0B respectively)

06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to cut 7-day Auction Rate by 25bps to 9.50%

06:45 (US) Daily Libor Fixing - 07:30 (IN) India Weekly Forex Reserves

08:00 (ZA) South Africa Mar Trade Balance (ZAR): 6.2Be v 5.2B prior

08:00 (ZA) South Africa Mar Budget Balance (ZAR): No est v 13.8B prior

08:00 (PL) Poland Apr Preliminary CPI M/M: +0.3%e v -0.1% prior; Y/Y: 2.0%e v 2.0% prior

08:00 (BR) Brazil Mar National Unemployment Rate: 13.7%e v 13.2% prior

08:00 (CL) Chile Mar Total Copper Production: No est v 377.0K prior

08:00 (CL) Chile Mar Unemployment Rate: 6.6%e v 6.4% prior

08:00 (CL) Chile Mar Manufacturing Production Y/Y: -1.5%e v -1.0% prior, Industrial Production Y/Y: -6.3%e v -7.6% prior

08:00 (ES) Spain Debt Agency (Tesoro) announces specific bonds to be issued in next week auction

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Q1 Advance GDP Annualized Q/Q: 1.0%e v 2.1% prior; Personal Consumption: 0.9%e v 3.5% prior

08:30 (US) Q1 Advance GDP Price Index: 2.0%e v2.1% prior; Core PCE Q/Q: 2.0%e v 1.3% prior

08:30 (US) Q1 Employment Cost Index (ECI): 0.6%e v 0.5% prior

08:30 (CA) Canada Feb GDP M/M: 0.1%e v 0.6% prior; Y/Y: 2.6%e v 2.3% prior

08:30 (CA) Canada Mar Industrial Product Price M/M: 0.3%e v 0.1% prior; Raw Materials Price Index M/M: -0.5%e v +1.2% prior

09:00 (BE) Belgium Q1 Preliminary GDP Q/Q: No est v 0.5% prior; Y/Y: No est v 1.2% prior

09:00 (MX) Mexico Q1 Preliminary GDP Q/Q: 0.5%e v 0.7% prior; Y/Y: 2.5%e v 2.4% prior

09:30 (BR) Brazil Mar Nominal Budget Balance (BRL): -34.6Be v -54.2 prior; Primary Budget Balance: -11.3Be v -23.5B prior

09:45 (US) Apr Chicago Purchasing Manager: 56.4e v 57.7 prior

10:00 (MX) Mexico Mar Net Outstanding Loans (MXN): No est v 3.63T prior

10:00 (US) Apr Final Michigan Confidence: 98.0e v 98.0 prelim

11:00 (CO) Colombia Mar Urban Unemployment Rate: 10.6%e v 11.0% prior; National Unemployment Rate: No est v 10.5% prior

11:00 (EU) Potential sovereign ratings:

(DE) Germany Sovereign Debt to be rated by S&P

(UK) United Kingdom Sovereign Debt to be rated by S&P

(NL) Netherlands Sovereign Debt to be rated by Fitch

(UR) Ukraine Sovereign Debt to be rated by Fitch

13:00 (US) Weekly Baker Hughes Rig Count data

14:30 (US) Fed's Harker speaks in Washington

15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to cut Overnight Lending Rate by 25bps to 6.75%

(CO) Colombia Mar Industrial Confidence: No est v -0.1 prior; Retail Confidence: No est v 23.2 prior

(MX) Mexico Mar YTD Budget Balance (MXN): No est v -31.5B prior Weekend

(DE) FDP Holds 2-day Election-Year Party Convention in Berlin

Britannia Rules The Nay’s

The end of the month is turning into a tough one for GBP naysayers as cable sales higher. Meanwhile, Draghi drags Euro lower, and Trump threatens to terminate, again.

Month end flows should always be taken with a grain of salt, as institutions rebalance international portfolios or do last minute hedging etc. These execute at best once a month flows may or may not fit in with the general theme of the week or month, especially ahead of an almost global long weekend.We can also expect to see a lot of large options expiries and that dirtiest of words, 'fixings', throughout the London and New York sessions.

Month end noise aside and somewhat belying the timid ranges we have seen in the G-10 universe over the last 12 hours quite a lot is actually going on. Setting the scene nicely for a rather more frisky FX market next week with the FOMC and Non-Farms on Friday.

GBP continued to rule the waves, moving higher against the USD and the EUR. We will look at this in a bit more detail later but needless to say, it still feels as if some structural shorts are yet to be unwound.

President Trump set a few cats among the pigeons this morning by threatening to either renegotiate or terminate South Korea's trade deal with the U.S. and in a Mexico moment, handing the South Korean armed forces a $1 billion bill for the installation of their THAAD system around Seoul.

The two interesting things that came out of this were that a. Neither the Kospi nor the Korean Won reacted at all to the statement, suggesting that the President's modus operandi with regards to negotiations is starting to fall on deaf ears globally. The carrot and the stick approach is refreshing, it is just not very subtle.

Secondly, in an equally Mexican response, the South Korean Defence Ministry said they had absolutely no intention of paying for it and the greenback started weakening.

EUR/USD

Starting with the ECB overnight, Mr Draghi has most certainly caused a drag on Euro with some decidedly dovish comments overnight.

'We have not yet seen sufficient evidence to materially alter our assessment of the inflation outlook - which remains conditional on a very substantial degree of monetary accommodation.'

'Interest rates will 'remain at present or lower levels for an extended period of time, and well past the horizon' of asset purchases.'

source: Bloomberg

This saw EUR/USD drift lower by over nearly a 100 points in yesterday's session although Mr Trumps terminating comments have seen the single currency make some ground back. The Euro is delicately poised on the charts as we head into the long weekend, sitting midrange at 1.0895.

As highlighted by the yellow circle, the EUR has formed a double top at 1.0950 and has made a series of lower highs since the start of the week. This becomes the closest major resistance.

Support is denoted by a clear double bottom at 1.0850 with the 200-day moving average (DMA) just below there at 1.0841. A close below here could set the EUR up for a correction to fill its Monday gap to 1.0730 early next week. Longer term trendline support and the 100-DMA lie below in the 1.0640/50 area.

GBP/USD

Her Majesty's British Pound has enjoyed an excellent week. Consolidating its gains post the snap election announcement and on the charts looking like it may be getting ready to move higher. U.K GDP has just come out.

16:30 *(UK) Q1 ADVANCE GDP Q/Q: 0.3% V 0.4%E; Y/Y: 2.1% V 2.2%E – Source TradeTheNews.com

Interestingly the slight miss has had a zero effect on the GBP, in contrast to the effects a miss on any data from the U.K. would have had a few weeks ago. Polls are showing the Tories will win over 50% of the vote if the election were to happen today must be having some effect. However, I suspect this has more to do with the amount of structural longer term shorts that are out there in GBP generally and I suspect the break though 1.2800 made some palms sweaty. A break of 1.3000 could see an all out anxiety attack amongst GBP bears.

The chart below shows the GBP bullish consolidation in stark detail. Looking at the technicals, GBP has broken through resistance at 1.2917 with the next resistance at 1.30000 more psychological than scientific. A daily close above this level could imply a larger move to the 1.3400 area.

Support is initially at 1.2917 followed by 1.2750 and the 1.2600 area. A series of previous daily highs and the 200-DMA.

EUR/GBP

In the big picture, EUR/GBP is still in its broad post-Brexit consolidation range of 8300/8850. More importantly, the GBP rally has seen the Monday morning election gap filled on the charts. However, it is important to note the gap has been filled by the GBP rallying, not the EUR dropping. With this gap out of the way, we can ponder the EUR/GBP chart from a more unbiased perspective.

We are trading nearer to the lower end of the longer term range, but it is not yet clear that we will move through the bottom. A break in GBP/USD above 1.3000 and a drop in EUR/USD to 1.0730 could change that dynamic.

In the meantime, EUR/GBP has resistance at 8530 followed by the 100 and 200 DMA's at 8550 and 8595. Support is nearer, at 8410 with the key level of 8300 behind that.

Summary

We appear to be at some interesting inflexion points with EUR and GBP as the month draws to an end. From a macro perspective, it appears that Sterling's Brexit day of reckoning will not be coming as soon as many longer term structural bears would want. From a technical perspective, GBP is looking constructive against both the USD and EUR. The Euro itself meanwhile, is looking decidedly less so against the greenback, with the charts implying the single currency may not mind the gap, it may fill the gap.

DAX Yawns As Eurozone CPI Beats Estimate, US GDP Next

After starting the week with strong gains, the DAX has shown little movement. The index is trading at 12,446.25 in the Friday session. In the eurozone, German Retail Sales dropped to 0.1%, matching the estimate. There was positive news on the inflation front, as CPI Flash Estimate improved to 1.9%, above the estimate of 1.8%. The US will release Advance GDP, with a forecast of 1.3%.

Inflation in the eurozone remains at strong levels, and is forecast to rise to 1.9% in April, up from 1.5% in March. Although inflation levels have moved higher, Mario Draghi stated on Thursday that the ECB was not changing its inflation forecast or making any changes to its asset-purchase program. The ECB held rates at a flat 0.00%, and the rate statement and comments from Mario Draghi were more dovish than the markets would have liked. The current ultra-loose policy, which includes a quantitative easing program of EUR 60 billion/mth, has been in place since 2008. Draghi acknowledged more favorable economic conditions, noting the eurozone economy had improved and downside risks had decreased. There had been speculation that the ECB might taper or bring forward its asset-purchase program, which runs until December. The ECB holds its next meeting in June, and the markets will again be looking for some tightening from the ECB.

The French presidential election may be in the daily headlines, but European stock markets haven’t shown much response this week. Voters will be back at the ballot boxes next Sunday, and the markets have priced in a victory by Emmanuel Macron over Marie Le Pen. A major reason for the market’s calmness is that opinion polls before the first round were fairly accurate, and correctly forecast that Macron would win 24% of the vote and Le Pen 22%, with both advancing to the May 7 runoff. The markets are thus relying on the polls for the second round, which show Macron with a comfortable lead of 60-40. Le Pen is a heavy underdog, compounded by the fact that some candidates from the first round, as well as former President Francois Hollande, have publicly called for voters to support Macron. Still, a strong showing by Le Pen next Sunday would show that her strident anti-EU stance has wide popularity, and this could sour investor sentiment and send the euro downwards.

President Trump announced his long-awaited tax plan on Wednesday. The proposal calls for sharp reductions for both individuals and corporations. The plans calls three tax brackets for individuals – 10%, 25% and 35%. The corporate sector would also see significant tax relief, with the corporate tax rate dropping from 35% to 15%, and the tax on multinationals’ overseas profits lowered from 35% to 10%. However, any tax reform proposals from the White House will require a stamp of approval from Congress, so Trump’s proposal should be viewed as a blueprint that is a long way off from becoming law. Trump’s proposal was short on details, although government officials are praising it as one of the largest tax cuts and broadest overhauls of the tax system in history.

US Data And Earnings In Focus As Euro Rises On Inflation Spike

- Euro tests highs as inflation accelerates in April;

- Sterling higher as consumer feels inflation pinch;

- Weak US Q1 GDP number expected for fourth year.

US futures are pointing to a slightly higher open on Friday as we await economic data and earnings for the first quarter. It's already been a lively start to trading in Europe where we got some surprising numbers from the UK and the euro area.

The euro has made some strong gains this morning, a day after having fallen back below 1.09 against the dollar as ECB President Mario Draghi warned that the path back to the central banks inflation target will be gradual. He did, however, warn that we should see a pick-up in inflation this month and that it would remain around this level until the end of the year, and this morning's flash CPI data has confirmed the first part of his forecast.

Prices rose more than expected in April, with the CPI measure rising to 1.9% year on year – in line with the ECBs target of below but close to 2% - and the core reading jumping 0.4% to 1.2%. With Draghi acknowledging this spike in yesterday's press conference, it's unlikely that it's going to change the outlook as far as the ECB is concerned but it will likely feed into the discussion come June, when many think the central bank will start planning for future tapering of its asset purchases.

The pound is also trading higher again this morning despite GDP data for the first quarter coming out weaker than expected at 0.3%. It would appear that the consumer is starting to feel the inflation bite, with the services sector growing at its slowest rate in two years, significantly below the levels achieved in the previous two quarters. Still, sterling is testing 1.2950 against the dollar and close to breaking through a key technical level that could open up a move towards 1.3450, having entered back into last year's June to September range.

There's still plenty of data to come from the US today, including its own advanced GDP reading for the first quarter, which is expected to be 1.3% on an annualised basis. While this may seem weak and trigger concerns about stalling growth, it is worth considering that first quarter growth has been very low in each of the last three years but has recovered in the following quarters on each occasion. There's currently no reason to doubt that the same will happen again, should we see another disappointing first quarter reading. We'll also get UoM consumer sentiment, employment cost index and Chicago PMI data, and hear from Fed officials Lael Brainard and Patrick Harker. Earnings season also continues with Exxon Mobil, Chevron and General Motors among those reporting.

GOLD Consolidating, SILVER Continued Weakness, CRUDE OIL Consolidating Below 50.

GOLD Consolidating.

Gold is consolidating around 1265 after the yellow metal has faded near the hourly resistance at 1295 (18/04/2017 high). Support can be located at 1261 (intraday low). The road is wide-open for further decline.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Continued weakness.

Silver has broken strong support at 18.16 (rising trendline) indicating further downside risk. Strong support is given far away at 16.82 (15/03/2017 low). Strong resistance is given at a distance at 19.00 (09/11/2017 high). Expected to see continued bearish pressures.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Consolidating below 50.

Crude oil has declined sharply, breaking the support at 50.71, yet now has paused. Support now lies at 48.87 (25/04/2017 low). Resistance for a short-term bounce can be found at 50.71 (old support) and 53.70 (12/04/2017 high).

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/JPY Consolidating Above 120.00, EUR/GBP Selling Pressures, EUR/CHF Feeling Gravity Again!

EUR/JPY Consolidating above 120.00.

EUR/JPY's buying pressures are there. Key resistance stands at 123.31 (27/01/0217 high). Major support is given at 114.90 (18/04/2017low). Expected to see short-term consolidation before seeing another leg higher.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Selling pressures.

EUR/GBP keeps on pushing lower. The technical structure is negative as long as the resistance at 0.8596 holds. Expected to show continued weakness until resistance given at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Feeling gravity again!

EUR/CHF is back lower. Despite the sharp increase and the recent bullish breakout which is very likely psychological, we believe that the medium-term pattern suggests us to see at some point renewed bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

USD/CHF Trading Sideways, USD/CAD Strong Buying Pressures, AUD/USD Pausing.

USD/CHF Trading sideways.

USD/CHF is trading mixed. The volatility is declining. The short-term technical structure is negative as long as prices remain below the hourly resistance at 1.0171 (07/03/2017). Monitor strong support given at 0.9814 (27/03/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Strong buying pressures.

USD/CAD has broken key resistance given at 1.3599 (28/12/206 high). The pair keeps on pushing higher. Hourly support can be found at 1.3411 (24/04/2017 high) then 1.3353 (20/01/2017 high). Expected to show continued bullish pressures as long as the pair remains above 1.3411.

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Pausing.

AUD/USD is consolidating after the break of support at 0.7473 (12/04/2017 low). As long as prices remain below the resistance at 0.7608 (17/04/2017 high), the short-term technical structure is negative. Key resistance stands at 0.7681 (30/03/2017 high). Expected to show further weakness.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Bearish Consolidation, GBP/USD Pushing Higher, USD/JPY Moving Sideways.

EUR/USD Bearish consolidation.

EUR/USD is consolidating lower. Hourly support is given at 1.0852 (27/04/2017 low) then 1.0682 (21/04/2017 base). Stronger support can be found at 1.0494 (22/02/2017 low). Hourly resistance is given at 1.0951 (26/04/2017 high). Expected to show another leg higher towards 1.10.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Pushing higher.

GBP/USD keeps pushing higher. Resistance at 1.2905 (18/04/2017 low) has been broken. The pair has exited the short-term bearish momentum. Hourly support can be found at 1.2757 (21/04/2017 low). An unlikely break of this support would indicate further weakness.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Moving sideways.

USD/JPY is consolidating. Strong resistance can be found at 112.20 (31/03/2017 high). Closest support can be located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). Expected to show continued bullish pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).