Sample Category Title

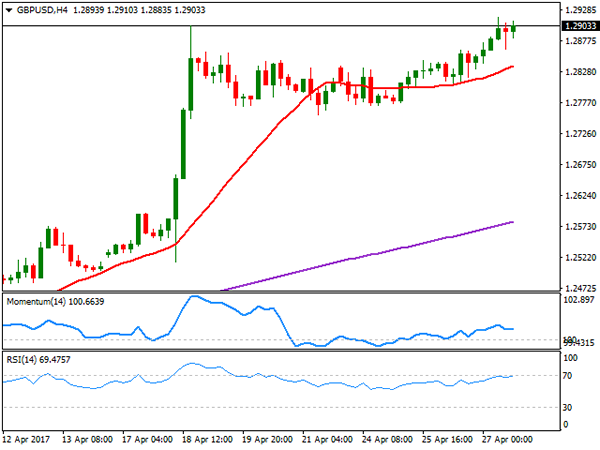

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2855; (P) 1.2885; (R1) 1.2933; More...

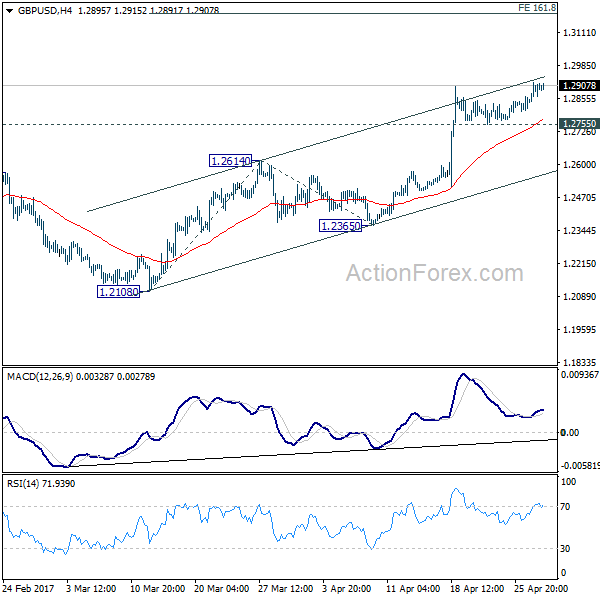

Intraday bias in GBP/USD remains on the upside. Current rise from 1.2108 should target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

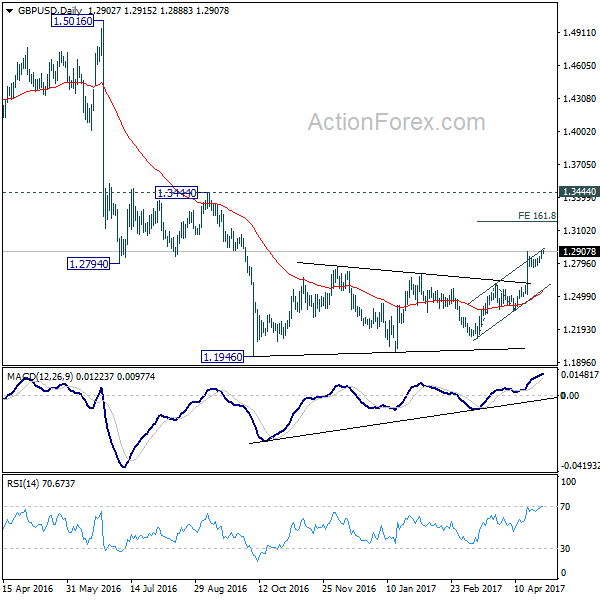

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9919; (P) 0.9941; (R1) 0.9963; More.....

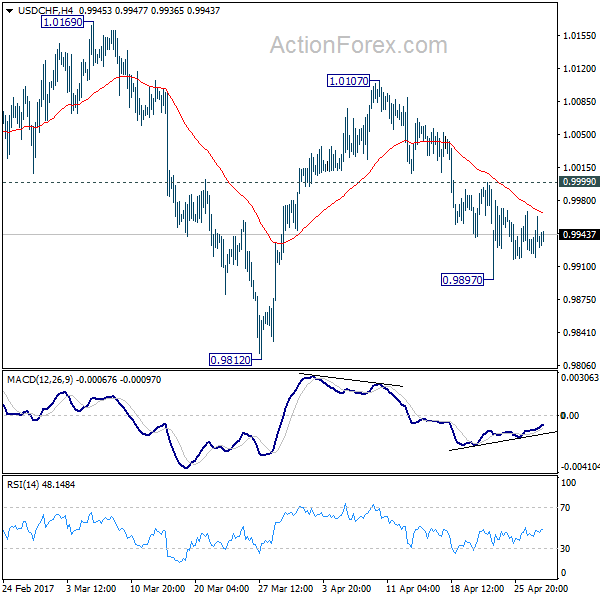

Intraday bias in USD/CHF remains neutral as consolidation form 0.9897 is still in progress. At this point, with 0.9999 minor resistance intact, deeper fall is still in favor. Below 0.9897 temporary low will turn bias to the downside for 0.9812 and possibly below. Nonetheless, whole decline from 1.0342 is seen as a correction. Hence, we'll look for bottoming signal below 0.9812. Meanwhile, on the upside, above 0.9999 minor resistance will turn bias back to the upside for 1.0107 resistance.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.68; (P) 111.23; (R1) 111.60; More....

As long as 109.58 minor support intact, further rise is still expected in USD/JPY. Sustained trading above 111.58 support turned resistance will indicate that fall from 118.65 is merely a corrective move and has completed. Outlook will then be turned bullish for 115.49 resistance and above. However, break of 109.58 will argue that fall from 118.65 is still in progress and will turn bias to the downside for 108.12 and below.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. Current development suggests that it's not completed yet and is extending. In case of deeper decline, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

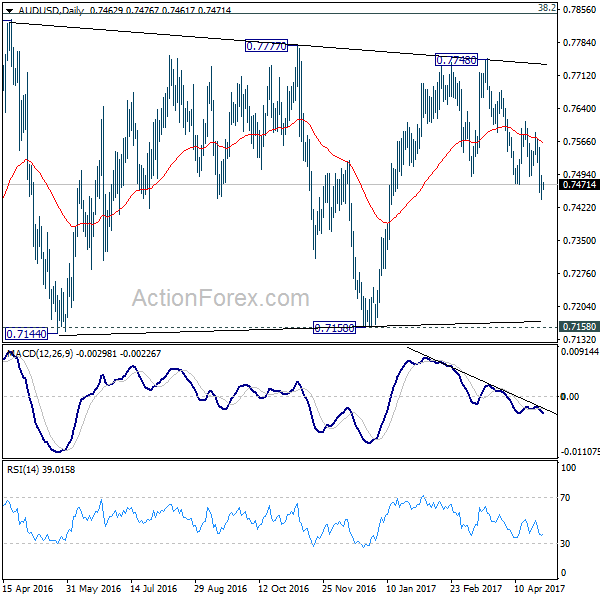

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7440; (P) 0.7466; (R1) 0.7492; More...

Intraday bias in AUD/USD remains on the downside for the moment. Current development suggests that rise from 0.7150 is completed at 0.7748. Deeper decline is expected to test 0.7144/58 key near term support zone. On the upside, break of 0.7609 resistance is now needed to indicate completion of the fall from 0.7748. Otherwise, outlook will stay mildly bearish in case of recovery.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8144) and above.

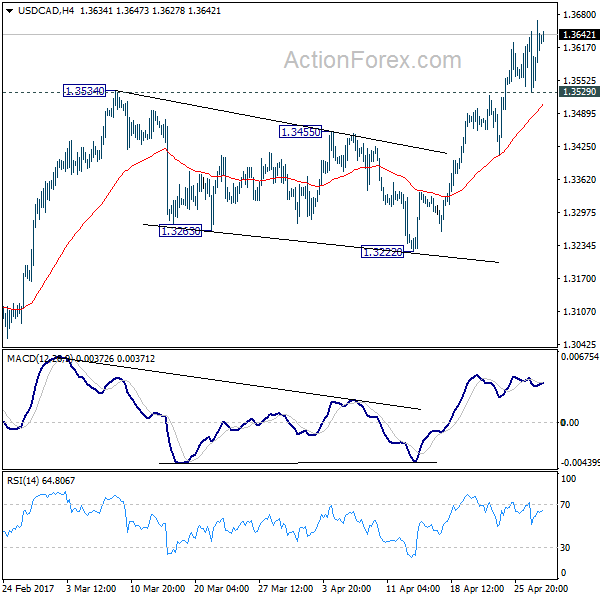

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3568; (P) 1.3568; (R1) 1.3647; More....

USD/CAD's rise resumed after brief consolidation and reaches 1.3669 so far. Intraday bias is back on the upside. Whole medium term rise from 1.2460 is still in progress and should target next medium term fibonacci level at 1.3838. On the downside, below 1.3529 minor support will turn bias neutral and bring consolidation before staging another rise.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.2968 will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Sterling Might Overtake Euro Strength as Traders Look into UK GDP, US GDP also Featured

The financial markets are rather steady as the week is heading for close. Euro remains the strongest major currency for the week even though it's losing some upside momentum. In particular, there is some selling seen in the common currency after ECB press conference yesterday. And on the other hand, Sterling is picking up momentum in Asian session and could overtake Euro's place. Japanese Yen and commodity currencies are generally weak. Canadian dollar got a brief lift on news that US is staying with NAFTA earlier this week. But renewed selling in crude oil is dragging down the Loonie again. Dollar is trading mixed for the moment as markets found little inspiration from US President Donald Trump's tax plan.

In other markets, DJIA closed up 0.03% at 20981.33 overnight. S&P 500 rose 0.06% to close at 2388.77. NASDAQ extended its record run and closed up 0.39% at 6048.94. While DJIA and S&P 500 lost some momentum ahead of record highs, both are still on course to extend the long term up trend. As noted before, the corrective pattern in DJIA from 21169.11 should have completed at 20379.55 already. And we'd anticipate a break of this record high soon, possibly in reaction to Q1 GDP report to be released today.

Yesterday, ECB left the monetary policy and the QE program unchanged. That is, the main refi rate, marginal lending rate and the depo rate stayed unchanged at 0%, 0.25% and -0.40%, respectively. Meanwhile, the asset purchase program would be continued at the pace of 60B euro per month from this month, through to the end of December 2017, or beyond, if necessary. Policymakers acknowledged the increasingly solid economic recovery in the Eurozone. The key message about the economy was that the recovery in the bloc is strengthening and broadening, whilst risks are diminishing. Yet, they refrained from discussing about potential tapering, likely due to concerns over subdued core inflation. More in ECB More Confident on Growth, but Inflation Remains an Overhang

Released from Japan, National CPI core was unchanged at 0.2% yoy in March. But Tokyo CPI core improved to -0.1% yoy in April. Retail sales rose 2.1 yoy in March. Household spending dropped -1.3%. Unemployment rate was unchanged at 2.8%. Industrial production dropped -2.1% mom. From Australia, PPI rose 0.5% qoq in Q1. New Zealand trade balance turned to NZD 332m surplus in March, building permits dropped -1.8% mom.

A number of key economic data will be featured today. UK Q1 GDP will be the main focus in European session. Eurozone will release April CPI flash, M3 money supply. German will release retail sales and import price index. France will release Q1 GDP too. Swiss will release KOF leading indicator. In US session, Q1 GDP will be featured with Chicago PMI. Canada will also released GDP and IPPI & RMPI.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3568; (P) 1.3568; (R1) 1.3647; More....

USD/CAD's rise resumed after brief consolidation and reaches 1.3669 so far. Intraday bias is back on the upside. Whole medium term rise from 1.2460 is still in progress and should target next medium term fibonacci level at 1.3838. On the downside, below 1.3529 minor support will turn bias neutral and bring consolidation before staging another rise.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.2968 will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Mar | -1.80% | 14.00% | 17.20% | |

| 22:45 | NZD | Trade Balance (NZD) Mar | 332M | 375M | -18M | -50M |

| 23:01 | GBP | GfK Consumer Confidence Apr | -7 | -7 | -6 | |

| 23:30 | JPY | Jobless Rate Mar | 2.80% | 2.90% | 2.80% | |

| 23:30 | JPY | Household Spending Y/Y Mar | -1.30% | -0.50% | -3.80% | |

| 23:30 | JPY | National CPI Core Y/Y Mar | 0.20% | 0.20% | 0.20% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Apr | -0.10% | -0.20% | -0.40% | |

| 23:50 | JPY | Retail Trade Y/Y Mar | 2.10% | 1.50% | 0.10% | 0.20% |

| 23:50 | JPY | Industrial Production M/M Mar P | -2.10% | -0.80% | 3.20% | |

| 1:30 | AUD | PPI Q/Q Q1 | 0.50% | 0.30% | 0.50% | |

| 5:00 | JPY | Housing Starts Y/Y Mar | -2.60% | -2.60% | ||

| 5:30 | EUR | French GDP Q/Q Q1 A | 0.40% | 0.40% | ||

| 6:00 | EUR | German Retail Sales M/M Mar | 0.00% | 1.80% | ||

| 6:00 | EUR | German Import Price Index M/M Mar | -0.10% | 0.70% | ||

| 7:00 | CHF | KOF Leading Indicator Apr | 107.5 | 107.6 | ||

| 8:00 | EUR | Eurozone M3 Y/Y Mar | 4.70% | 4.70% | ||

| 8:30 | GBP | BBA Mortgage Approvals Mar | 42.1K | 42.6K | ||

| 8:30 | GBP | GDP Q/Q Q1 A | 0.40% | 0.70% | ||

| 8:30 | GBP | Index of Services 3M/3M Feb | 0.50% | 0.60% | ||

| 9:00 | EUR | Eurozone CPI Estimate Y/Y Apr | 1.80% | 1.50% | ||

| 9:00 | EUR | Eurozone CPI - Core Y/Y Apr A | 1.00% | 0.70% | ||

| 12:30 | USD | Employment Cost Index Q1 | 0.60% | 0.50% | ||

| 12:30 | CAD | GDP M/M Feb | 0.10% | 0.60% | ||

| 12:30 | CAD | Industrial Product Price M/M Mar | 0.10% | |||

| 12:30 | CAD | Raw Materials Price Index M/M Mar | 1.20% | |||

| 12:30 | USD | GDP (Annualized) Q1 A | 1.10% | 2.10% | ||

| 12:30 | USD | GDP Price Index Q1 A | 2.00% | 2.10% | ||

| 13:45 | USD | Chicago PMI Apr | 56.7 | 57.7 | ||

| 14:00 | USD | U. of Michigan Confidence Apr F | 98 | 98 |

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EUR/USD pair closed the day marginally lower around 1.0880, down for a second consecutive, despite positive macroeconomic data released earlier on the day, as attention centered in the ECB's monetary policy decision. Market players ignored positive figures coming from Germany, where consumer confidence advanced further for May according to the GFK survey, which printed 10.2 against previous 9.8. Inflation in the country is expected to remain flat in April, better than the 0.1% decline forecasted, while yearly basis, is expected to have risen to 2.0% from previous 1.6%. Business sentiment improved in the EU although consumer sentiment remained unchanged at -3.6. As for the ECB, the Central Bank left its monetary policy unchanged, and even indicated confidence in the economic growth, with the risk seen more balanced. The picture however, was not that good for inflation, with policymakers indicating that the accommodative monetary policy will persists amid underlying inflation still being subdued. Additionally, the Central Bank said they did not discuss tapering.

After surging to 1.0932, the pair fell down to 1.0851, as disappointing US data kept the greenback in check across the board. Initial jobless claims rose to 257K worse than the 241K expected in the week ending April 21st, whilst eh goods trade deficit expanded to $65 billion in March. Durable Goods Orders for the same month rose just by 0.7%, missing expectations of a 1.2% advance, while the core figure fell by 0.2%, against the 0.4% forecasted. Finally, pending home sales fell in March by 0.8%, less than market's forecast of a 1.0% decline.

From a technical point of view, the pair continues consolidating its recent gains, although the upward potential has somehow faded, after another failed attempt to surpass the key resistance around 1.0930, the 61.8% retracement of the post-US election slide. The 4 hours chart, shows that the price settled below its 20 SMA for the first time this week, while technical indicators continued retreating, now flat around their mid-lines. Sellers stand in the area between the mentioned Fibonacci resistance and the weekly high of 1.0950, this last the level to surpass to confirm an upward extension, while below the weekly low of 1.0820, the weekly low and another Fibonacci support, the risk will turn towards the downside, with the pair targeting then 1.0730, the unfilled weekly opening gap.

Support levels: 1.0855 1.0820 1.0785

Resistance levels: 1.0910 1.0950 1.1000

USD/JPY

The USD/JPY pair traded uneventfully for a second consecutive day, erasing its intraday gains in the US afternoon, and settling pretty much flat around 111.20. The Bank of Japan monetary policy meeting barely affected the pair, as the ongoing policy was maintained unchanged. Policy makers raised the economic forecast, increasing its real GDP growth forecast for the 2017-18 fiscal year to 1.6% from the 1.5% projected in January, butt lowered its core inflation growth forecast to 1.4% from 1.5% in the same period. The yen found some support on falling US yields, following Draghi's statement, with the 10-year benchmark down to 2.29% from 2.31%. The pair traded within Wednesday's range, lacking directional strength ahead of Friday's opening. Japan will release a batch of first-tier data including National and Tokyo inflation, unemployment, industrial production and retail sales. The 4 hours chart shows that approaches to the 200 SMA continued to attract buying interest, but that the Momentum indicator extended its decline within positive territory, indicating decreasing buying interest. The RSI indicator in the mentioned chart remains flat around 60. The downside potential seems limited as long as the price holds above the mentioned SMA, currently around 110.95, while only beyond 112.00 the pair will be poised to resume its advance.

Support levels: 110.95 110.60 110.20

Resistance levels: 111.60 112.00 112.45

GBP/USD

The GBP/USD pair surpassed its previous 2017 by a few pips, printing 1.2916 at the beginning of the European session, and settling above 1.2900. Grinding slowly higher, the absence of first-tier data or fresh Brexit headlines prevented the pair from advancing further, but the outlook remains bullish for the pair, although it will suffer a macroeconomic challenge this Friday, when it will release the first estimate of the Q1 GDP. The economy is expected to have grew by 0.4% in the three months to March, following a 0.7% advance in the previous quarter. In the meantime the pair remains near the mentioned high, and the 4 hours chart shows that the price remains above a recovering 20 SMA, whilst the RSI indicator continues consolidating near overbought levels and the Momentum indicator within positive territory. An acceleration through 1.2920, should favor additional gains, towards 1.2960 first, and up to 1.2710 afterwards.

Support levels: 1.2870 1.2830 1.2795

Resistance levels: 1.2920 1.2960 1.3010

GOLD

The GBP/USD pair surpassed its previous 2017 by a few pips, printing 1.2916 at the beginning of the European session, and settling above 1.2900. Grinding slowly higher, the absence of first-tier data or fresh Brexit headlines prevented the pair from advancing further, but the outlook remains bullish for the pair, although it will suffer a macroeconomic challenge this Friday, when it will release the first estimate of the Q1 GDP. The economy is expected to have grew by 0.4% in the three months to March, following a 0.7% advance in the previous quarter. In the meantime the pair remains near the mentioned high, and the 4 hours chart shows that the price remains above a recovering 20 SMA, whilst the RSI indicator continues consolidating near overbought levels and the Momentum indicator within positive territory. An acceleration through 1.2920, should favor additional gains, towards 1.2960 first, and up to 1.2710 afterwards.

Support levels: 1.2870 1.2830 1.2795

Resistance levels: 1.2920 1.2960 1.3010

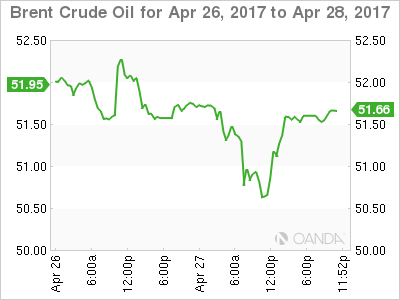

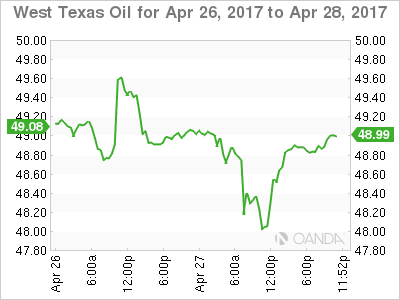

WTI CRUDE OIL

Crude oil prices plunged at the beginning of the day, with West Texas Intermediate crude futures printing a fresh 4-week low of $48.21 a barrel on news that Libya have resumed oil pumping for export in two key oilfields. The commodity, however, trimmed most of its intraday losses ahead of Wall Street's close, ending the day at $49.20 a barrel, as the dollar weakened in the US session following the release of soft local data. WTI retains a negative outlook, as in the daily chart, the price continued developing well below all of its moving averages, whilst technical indicators head south within bearish territory. In the 4 hours chart, the price is also below its moving averages, with the 20 SMA acting as an immediate resistance at 49.30, while technical indicators recovered within negative territory, but pared gains and turned flat around their mid-lines.

Support levels: 48.85 48.20 47.70

Resistance levels: 49.30 49.80 50.30

DJIA

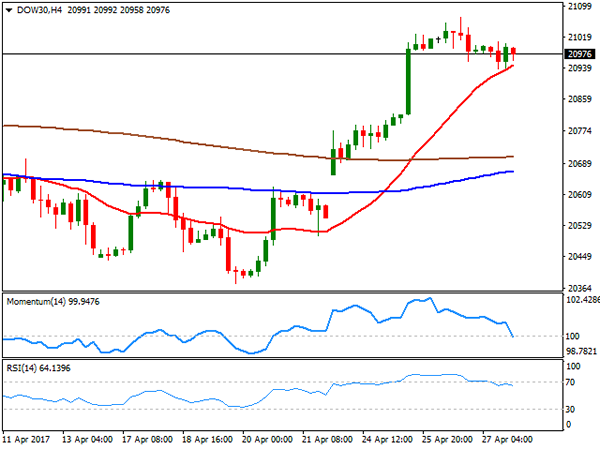

Wall Street posted modest gains this Thursday, with the DJIA up 6 points, to 20,981.33 and the S&P surging by 0.06% to 2,388.77. The Nasdaq Composite out-stood, adding 23 points to 6,048.94, a record close. Amazon released its earnings report right after the close, hitting record highs after a positive statement, although Microsoft edged lower in the same scenario. Within the Dow, Home Depot was the best performer, adding 1.21% followed by Intel that added 1.18%. El du Pont lead declines with a 1.90% decline, followed by Caterpillar that shed 1.73%. Technically, the daily chart for the index shows that indicators lost directional strength within positive territory, but also that it holds above its moving averages, with the risk still towards the upside. In the shorter term, and according to the 4 hours chart, the index is barely holding above a bullish 20 SMA, this last at 20,945, while technical indicators head lower, indicating a possible downward corrective move on a break below the mentioned SMA.

Support levels: 20,945 20,914 20,869

Resistance levels: 21,035 21,071 22,010

FTSE100

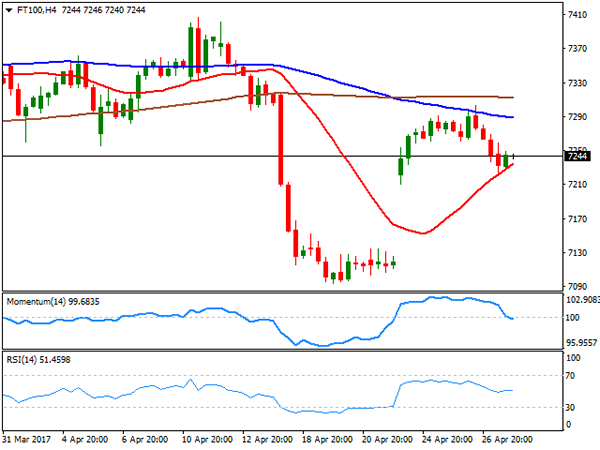

London shares followed the lead of European indexes, with the Footsie down 51 points daily basis to end at 7,237.17, undermined by persistent Pound's strength and weaker base metals. Despite banks were under pressure, Lloyds Banking group was among the best performers, ending the day up 2.31% after a positive earnings report. BHB Billiton led decliners, down 4.75%, followed by Glencore that shed 3.15% and Fresnillo that closed down 2.73%. Daily basis, the index is contained to the upside by a bearish 20 DMA, but holding above a bullish 100 DMA, this last at 7,218, the level to break to see further declines. Indicators in the mentioned time frame hold within negative territory, with the RSI turning modestly lower. In the 4 hours chart, a bullish 20 SMA attracted some short term buying interest, but the recovery has been limited, while technical indicators are biased lower within neutral territory, in line with the longer term perspective.

Support levels: 7,218 7,173 7,126

Resistance levels: 7,259 7,303 7,340

DAX

European major benchmarks closed mostly lower this Thursday, with the German DAX settling at 12,443.79, down by 29 points or 0.23%, with banks and automotive shares leading the way lower in the country. Despite an encouraging earnings report, Deutsche Bank plunged at the beginning of the day, ending 3.41% lower amid the increased earnings were achieved on the back of revenues around 9.0% lower, at 7.3 billion Euros. Bayer on the other hand, was the best performer, adding 4.33%. The daily chart shows that the index continued to consolidate at the upper end of its weekly range, maintaining a positive technical outlook given that it remains far above bullish moving averages, whilst technical indicators have resumed their advances within positive territory. In the 4 hours chart, the Momentum retreated towards its 100 level, but the RSI indicator holds around 66 as the 20 SMA maintains a strong bullish slope well below the current level, supporting some additional gains on a break above 12,495, the weekly high.

Support levels: 12,418 12,366 12,312

Resistance levels: 12,495 12,530 12,585

Market Morning Briefing: Almost All Stocks Are Stable And Could Consolidate For A Few Sessions

STOCKS

Almost all stocks are stable and could consolidate for a few sessions. Resistances are visible not very far from current levels and a sharp corrective dip thereafter is possible.

Dow (20981.33, +0.03%) was almost stable yesterday with and is not attempting t rise above 21000.Similarly Dax (12443.79, -0.23%) is also stable near 12500. Both the indices could consolidate for a few sessions and ty to move a little higher to test respective resistances near 21400 and 12600-12700 before coming off from there. However, upside is limited for the near term.

Shanghai (3141.63, -0.33%) could trade within the 3180-3100 region for at least the next 2-3 sessions before deciding the further course of direction. On the 3-day candles support is visible just below 3100 and is expected to hold in the medium term.

Nikkei (19213.09, -0.20%) has potential to test 19620 in the next week in case it breaks above 19300. Thereafter a corrective dip towards 18800 is possible.

Nifty (9342.15, -0.10%) has been slowly moving up towards 9400. Yesterday was a quiet day and we could soon expect a sharp fall in the medium term.

COMMODITIES

Gold (1266) is trading within the narrow range of 1265-1300.Buyers will take every dip as a further opportunity for buying while it is trading above 1260-65 levels. 1275-80 could be the levels where the price action has to be checked to assess the chances of further bounce to 1305 to 1330 levels.

Silver (17.28) is Oversold and trading within the range of 17-17.45.A close above that could open up 17.80 levels as well. Copper (2.58) has shown some strength as it manages to trade above its crucial support at 2.57. But only above 2.65-67, higher resistances of 2.72 -80 can come into consideration. If copper will manage to close above 2.65 levels then we might see sharp upside rally in silver too.

Muted price action had been seen in Brent (51.74) and WTI (49.31). While we have been expecting a bounce from 51.69 to 53.80 in Brent and 49.31 to 51.50 in WTI and we prefer to wait for higher levels to create fresh short positions.

FOREX

Dollar Index (99.04) still hovers just above the make or break support of 98.50 but requires a rise above 99.35 for a confirmed reversal signal and Euro (1.0867) has again come off the highs after being rejected from the major resistance of 1.0950, keeping open the possibility of a downward correction to 1.0824 and 1.0700.

Dollar-Yen (111.16) is holding below immediate resistance near 112 and could trade in the 112-111 zone for 1-2 sessions before coming off towards 110.50. Immediate support visible near 110 as mentioned yesterday.

Pound (1.2913) has moved up after initial consolidation in the 1.2864-1.27730 region and now while the upward momentum continues, we could see a rise towards 1.30 in the near term.

Aussie (0.7475) is almost stuck near support at 0.7450. ther could be a short bounce towards 0.75 in the next 2-sessions.

Dollar-Rupee (64.19) is trading higher and hovering around its crucial resistance at 64.20/25. It it will hold then we could see trade within the 63.90-64.20/25 region with a possible extension to 64.35. However, a dip towards 63.80 is on the cards possibly next week before a bounce back towards 64.25-35 is expected.

INTEREST RATES

The US yields are down as expected. . The 5Yr (1.82%), 10YR (2.29%) and the 30YR (2.96%) are all down 2bps and looks bearish in the enar term. The 10yr could come down to test 2.20% while the 30Yr may test 2.9% in the coming sessions.

The German-US 2Yr (-2.00%) and the 10YR (-1.99%) has shown some signs of reversal and if it sustains in the coming week, we could see a fall in Euro towards 1.07.

The US-Japan 10YR (2.27%) has fallen and could move towards 2.2% in the near term indicating a slight dip in Dollar-yen and Nikkei in the next 2-3 sessions.

Elliott Wave View: USDCAD Extending Higher

Short term Elliott Wave view in USDCAD suggest the decline to 1.322 ended Intermediate wave (X). The rally from there is unfolding as a double three Elliott Wave structure where Minute wave ((w)) ended at 1.3525 and Minute wave ((x)) ended at 1.3406. Minute wave ((w)) is subdivided as a Flat Elliott wave structure where Minutte wave (a) ended at 1.3338 and Minutte wave (b) ended at 1.3258. Pair is currently within Minute wave ((y)) which is unfolding as a double three Elliott Wave structure where Minutte wave (w) ended at 1.3626 and Minutte wave (x) FLAT ended at 1.3526. Near term, while pullbacks stay above 1.3406, expect pair to extend higher towards 1.3714 – 1.3787 area to end cycle from 4/13 low before a larger pullback in 3 waves can be seen at minimum to correct cycle from 4/13 low. We don’t like selling the proposed pullback.

USDCAD 1 hour Elliott Wave Chart

Oil And Gold Slip Sideways Into Friday

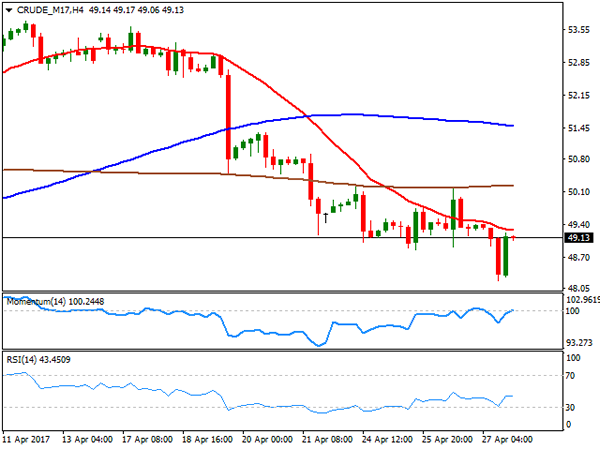

Crude oil staged a dead cat bounce overnight after an initial sell-off, whilst gold flat-lined into Friday.

Both Brent and WTI fell a dollar overnight to make new lows for the week but rebounded aggressively to finish unchanged from Wednesday at 51.50 and 48.90 respectively. Although the talk was of renewed Libyan production, the price action looks suspiciously stop loss driven in our opinion as both broke weekly lows flushing out yet more long-suffering bulls.

Oil’s recovery was probably helped by the International Energy Agency announcing that final investment decisions in new fields had dropped to the lowest level since the 1940’s. That will be a story for another day, more interestingly from a technical standpoint was that both contracts broke their 200-day moving averages intra-day, only to close back then as the New York session ended. Although crude has had something of a dead cat bounce, it may imply we have seen the worst of the sell-off for this week at least.

BRENT

Brent spot opens at 51.50 this morning with support at the 200 DMA at 50.90 followed by the overnight low at 50.0 and then 49.50. Resistance lies just above at 51.80 and then 52.50.

WTI

WTI spot trades at 48.85 with its 200 DMA just below at 48.70, followed by its overnight low at 47.90 and then 46.50. Resistance is just above at 49.00 and then the 50.00 a barrel region.

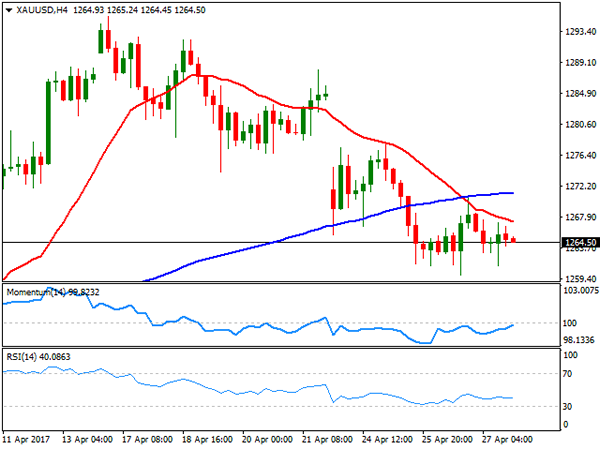

GOLD

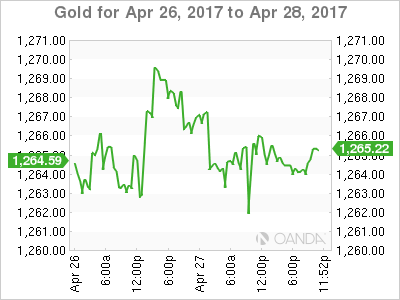

Gold heads into the end of the week with more of a whimper than a roar after a deadly quiet session overnight, closing almost unchanged at 1264.50 where it presently trades in Asia. The price action though continues to suggest that gold is treading water before another move down rather than a rally.

With the world an apparently more certain place, the safe haven bid is dissipating which could slowly but surely erode gold’s pricing premium, and a stronger U.S. dollar against the G10 currencies will not be helping.

From a technical perspective, gold has continued to make lower highs on a daily basis over the last two weeks. Gold has initial support at 1259.50 and then the 200-day moving average at 1253.70. The key support region follows this at 1240, a break of which would imply possibly much lower levels.

Resistance lies at 1270 followed by 1280 and then the April highs at 1295.70.