Sample Category Title

Markets Shrug Trump’s Tax 1-Page Tax Plan, CAD Rebounds on NAFTA News, Yen Steady after BoJ

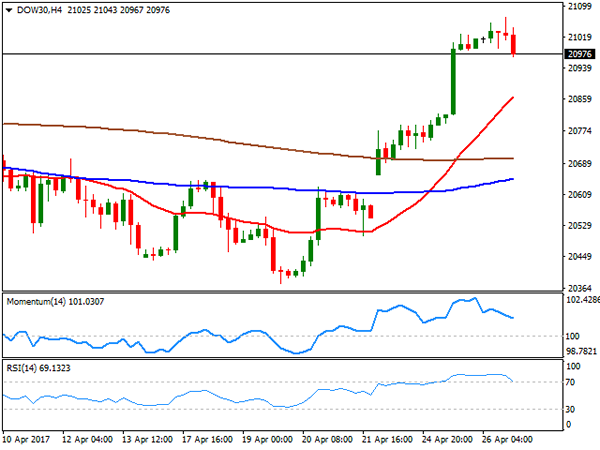

The financial markets had very little reaction to the highly anticipated announcement of tax reforms by US President Donald Trump. DJIA reversed earlier gains and closed slightly lower by -0.1% at 20975.09. S&P 500 also closed down -0.05% at 2387.56. Both were held below record intraday highs of 21169.11 and 2400.98 respectively. 10 year yield also closed lower, losing -0.016, at 2.311. The dollar index struggled to find follow through buying above 99 and is back at 98.90 in Asian session. In the currency markets, Euro remains the strongest major currency for the week, followed by Sterling and Swiss Franc. Yen remains the weakest one after BoJ stands pat, raised growth forecast but lowered inflation projections. Canadian dollar is still trading down for the week but is given a mild boost on news that US will stay with NAFTA for the moment.

Trump delivered a 1-page tax plan

Trump gave a one-page handout to reporters at the White House outlining the tax proposals. The plan includes sections on business and individual reforms. Top corporate tax rate of all businesses will be lowered from 35% to 15%. There will be a "one-time" tax on dollars held by corporations overseas but the rate is not decided yet. Tax breaks for special interests will eliminated. For the individuals, seven tax brackets will be reduced to three of 10%, 25% and 35%. Standard deduction will be doubled and there will tax relief for families with child and dependent care expenses.

Canadian Dollar rebound as NAFTA stays

Canadian Dollar rebounds after the White House said that Trump will not terminate the participation in the North American Free Trade Agreement immediately. The White House said in a statement that there were "pleasant and productive" conversations with leaders of Mexico and Canada. And Trump agreed not to terminate NAFTA at this time and the leaders agreed to "proceed swiftly, according to their required internal procedures, to enable the renegotiation of the Nafta deal to the benefit of all three countries." Commerce Secretary Wilbur Ross said earlier this week that the administration is working with the Congress to start renegotiation of NAFTA as Trump has been openly criticizing the deal. But some Republicans are clearly in objection to scrapping NAFTA.

BoJ raised growth forecast, cut inflation estimate

BoJ left monetary policies unchanged today as widely expected. In the quarterly report of Outlook for Economic Activity and Prices, the central bank lowered inflation forecast for the current fiscal year to 1.4%, down from January's projection of 1.5%. Inflation forecast for fiscal 2018 was held unchanged at 1.7%. On the other hand, growth forecast for fiscal 2017 was revised up to 1.6%, from 1.5%. For fiscal 2018, growth is projected to be at 1.3%, up from prior estimation of 1.1%.

UK PM May held constructive talk with EC President Juncker

UK Prime Minister Theresa May met with European Commission President Jean-Claude Juncker yesterday on a discussion over Brexit. UK's main negotiator David Davis and EU's negotiator Michel Barnier were also present. May's spokesperson said in a statement that the meeting was "constructive" and May "reiterated the UK's commitment to achieving a deep and special partnership with the European Union." EC also said in a statement that the meeting was "constructive" and addressed "issues of strategic interest". No detail about the conversation was released. EU leaders will meet this Saturday to work on their own negotiation plan and official talk will start after UK election on June 8. Barnier noted that the negotiations must be concluded within 18 months to allow time for approval by respective parliaments.

CBI director general warned no trade deal should be Plan Z

CBI director general Carolyn Fairbairn warned that the long term trading relationship between UK and EU is "the real prize", "dwarfing any potential divorce settlement." And, "a one-off EU divorce bill of, some suggest, tens of billions of euros, compared with EU-UK trade worth well over €600bn euros every year, the economic case for making rapid progress on a trade agreement is clear." She urges that "economics cuts through the politics" in the discussions. And, "the business community - in the UK and the EU - is united in wanting an agreement with as few barriers as possible. Yet without an agreement, we'd lose together." And, "for both sides, leaving the negotiating table without a deal shouldn't be 'Plan B' but 'Plan Z'".

ECB to stand pat today

ECB is widely expected to keep monetary policies unchanged today. The first round result of French presidential election, and centrist Emmanuel Macron's high chance of winning the run-off should give ECB much relief. Nonetheless, the central bank is still not ready to hint on any stimulus exit yet. ECB President Mario Draghi has stressed enough that there are much downside risks to the economy, and underlying inflation stayed low. Risks are still tilted much to the downside in spite of the French election results. Meanwhile, various ECB officials have clearly expressed that the course of monetary policies are set for 2017. The central bank will continue with its EUR 60b per month asset purchase till the end of the year. And it's unlikely that policy makers will opt for a rate hike before the asset purchase ends. We'd expect the speculation and debate on exit to start heating up again in June.

Elsewhere

Australia import price index rose 1.2% qoq in Q1, much higher than expectation of -0.5% qoq. Swiss will release trade balance in European session. Germany will release Gfk consumer sentiment and CPI. Eurozone will release confidence indicators. UK will release CBI reported sales. From US, trade balance, wholesale inventories, durable goods orders, jobless claims and pending home sales will be featured.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3568; (P) 1.3568; (R1) 1.3647; More....

A temporary top is in place at 1.3647 after USD/CAD fails to sustain above 1.3598 key resistance. Intraday bias is turned neutral first. Some consolidations should be seen but downside of retreat would be contained by 1.3410 support to bring another rally. Break of 1.3647 will extend the whole medium rise from 1.2460 to next medium term fibonacci level at 1.3838. However, break of 1.3410 will turn bias back to the downside for 1.3222 support instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.2968 will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | Monetary Policy Statement | |||||

| 1:30 | AUD | Import Price Index Q/Q Q1 | 1.20% | -0.50% | 0.20% | |

| 6:00 | CHF | Trade Balance (CHF) Mar | 3.01B | 3.12B | ||

| 6:00 | EUR | German GfK Consumer Confidence May | 9.9 | 9.8 | ||

| 9:00 | EUR | Eurozone Economic Confidence Apr | 108.1 | 107.9 | ||

| 9:00 | EUR | Eurozone Business Climate Indicator Apr | 0.82 | 0.82 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Apr | 1.3 | 1.2 | ||

| 9:00 | EUR | Eurozone Services Confidence Apr | 12.9 | 12.7 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Apr F | -3.6 | -3.6 | ||

| 10:00 | GBP | CBI Realized Sales Apr | 6 | 9 | ||

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 11:45 | EUR | ECB Marginal Lending Facility | 0.25% | 0.25% | ||

| 11:45 | EUR | ECB Deposit Facility Rate | -0.40% | -0.40% | ||

| 11:45 | EUR | ECB Asset Purchase Target (EUR) Apr | 60B | 80B | ||

| 12:00 | EUR | German CPI M/M Apr P | -0.10% | 0.20% | ||

| 12:00 | EUR | German CPI Y/Y Apr P | 1.90% | 1.60% | ||

| 12:30 | USD | Advance Goods Trade Balance Mar | -65.2B | -63.9B | ||

| 12:30 | USD | Wholesale Inventories Mar P | 0.30% | 0.40% | ||

| 12:30 | USD | Durable Goods Orders Mar P | 1.30% | 1.80% | ||

| 12:30 | USD | Durables Ex Transportation Mar P | 0.50% | 0.50% | ||

| 12:30 | USD | Initial Jobless Claims (22 APR) | 241K | 244K | ||

| 14:00 | USD | Pending Home Sales M/M Mar | -1.00% | 5.50% | ||

| 14:30 | USD | Natural Gas Storage | 54B |

Market Morning Briefing: Nothing Has Changed Much After The Trump Tax Plan

STOCKS

The tax plan released by Trump yesterday proposed to sharply slash business taxes. It proposed to cut income tax rate from 39.6% to 35% , reduce corporate tax from 35% to 15% and to reduce the seven tax brackets for individuals to 3-tax brackets of 10%, 20% and 35% respectively.

The US stocks have not really moved up at the end f the session. Dow (20975.09, -0.10%) is testing resistance on the daily and 3-day line charts and could possibly come off in the near term. However, when looked at the candle charts, there could be some scope of rising towards 21200-21400 before starting a correction.

Dax (12472.80, +0.05%) could move sideways to create more scope of an upmove. For now 12532 is an important resistance and it could be tested in the next 3-4 sessions.

Shanghai (3112.40, -0.91%) has fallen sharply again coming down to test 3100 levels and looks bearish for the week. A break or bounce from levels near 3100 would decide the next course of direction.

Nikkei (19243.76, -0.24%) is stable just now but could head towards 19620 as mentioned yesterday. Immediate trend is up.

Nifty (9351.85, +0.49%) has been playing out in line with our expectation and could face rejection from resistance near 9400.

COMMODITIES

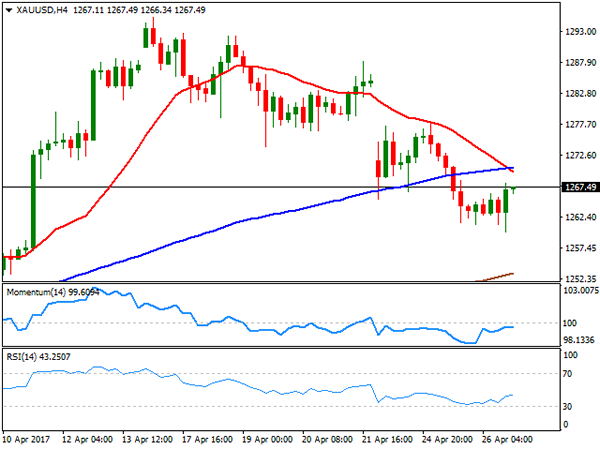

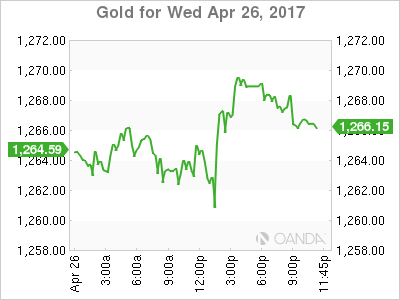

Muted price action had been seen in Gold (1266).Immediate supports are poised at 1260 and 1239 respectively. Buyers will take every dip as a further opportunity for buying while it is trading above 1239. 1285 could be a level where the price action has to be checked to assess the chances of further bounce to 1305 to 1330 levels.

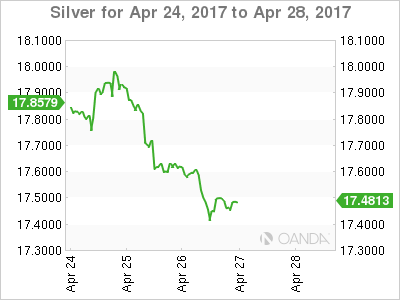

Silver (17.43) is Oversold on the near-term charts and it is hovering around its crucial resistance at 17.45.A close above that could open up 17.80 levels as well. Immediate support is at 17.02 levels.

Copper (2.57) had failed to close above 2.62 levels. A close below 2.55 could open up 2.48 and 2.45 levels respectively. The bias would remain bearish while it is trading below 2.62-67 levels.

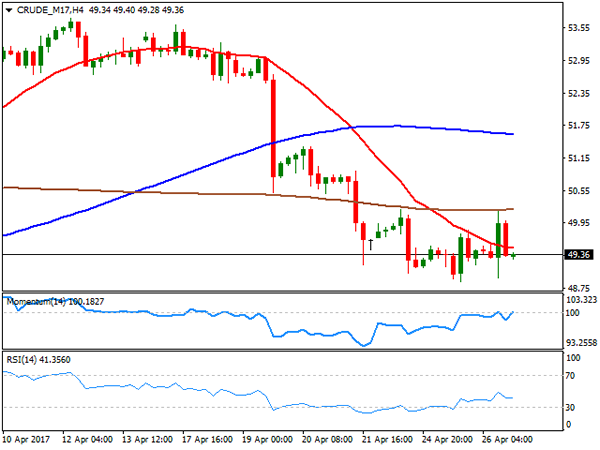

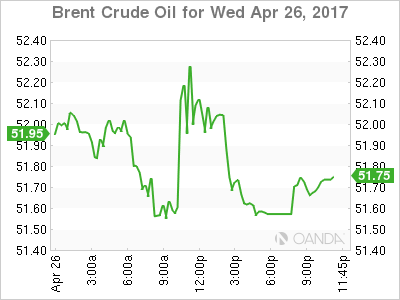

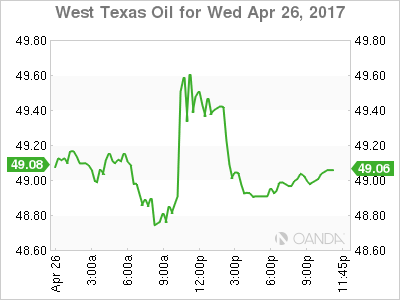

Brent (51.69) and WTI (49.42) have been well supported due to decrease (-3.6M) in U.S crude oil inventory and near term Oversold condition. In a major downtrend like this, the bounces are generally seen as fresh shorting opportunities by the big money with the speculators excited with the fast movement. While we have been expecting a bounce from 51.69 to53.80 in Brent and 49.42 to 51.50 in WTI , we prefer to wait for higher levels to create fresh short positions.

FOREX

Nothing has changed much after the Trump tax plan came out as a page full of bullet points denied all the necessary details to understand anything clearly about it and told of nothing new. It remains to be seen if the BOJ and ECB meet today can trigger any major moves.

Dollar Index (98.89) still hovers just above the make or break support of 98.50 but requires a rise above 99.35 for a confirmed reversal signal and Euro (1.0911) has again come off the highs after being rejected from the major resistance of 1.0950, keeping open the possibility of a downward correction to 1.0840 and 1.0700. Today's ECB meet may turn out to be a market driver.

It has been another quiet session for Pound (1.2870) in 1.2750-1.2900 as expected which may continue for the last 2 sessions of the week too.

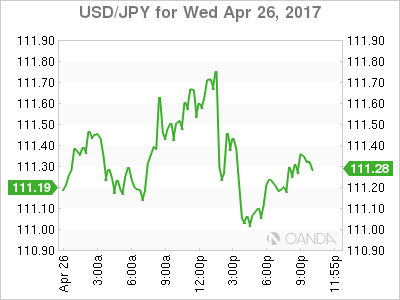

Dollar-Yen (111.22), just as expected, has stalled after hitting a high of 111.77, bang in the middle of our target/resistance area of 111.50-112.00 as it waits for the BOJ meet conclusion due in a few minutes. Support remains unchanged at 110.00.

Aussie (0.7487) has tested and bounced exactly from the lower end of the range of 0.7450-0.7600. The lack of downside momentum may push it up to 0.7550 once again before any large directional move emerges.

Dollar-Rupee (64.12) has resolved the range of 64.20-70 to the downside and now, as long as the resistance of 64.35-45 holds, the path of least resistance points down. Initial support comes at 63.80 which may be revised later to 63.60-50 if needed.

INTEREST RATES

ECB Policy meet is due today. Markets await to watch if there is any indication of an eventual stimulus reduction that Draghi may signal today. The German yields could come off in the near term as they are headed towards near term resistances. The 10Yr (0.35%) could move up towards 0.40% in the coming sessions.

The US yields have fallen slightly. The 5Yr (1.84%), 10YR (2.31%) and the 30YR (2.97%) are down from previous levels of 1.86%, 2.33% and 2.98% respectively. The yields could start coming off again in the near term.

The German-US 2Yr (-1.98%) has come off and is testing the earlier resistance turned support near current levels. A bounce from here could trigger some more strength in Euro in the near term. We need to keep a close watch for further directional cues.

Elliott Wave View: USDCAD Flat Correction

Short term Elliott Wave view in USDCAD suggest the decline to 1.322 ended Intermediate wave (X). The rally from there is unfolding as a double three Elliott Wave structure where Minute wave ((w)) ended at 1.3525 and Minute wave ((x)) ended at 1.3406. Minute wave ((w)) is subdivided as a Flat Elliott wave structure where Minutte wave (a) ended at 1.3338 and Minutte wave (b) ended at 1.3258. Near term, pair is within Minutte wave (x) Flat pullback to correct the cycle from 4/24 low towards 1.346 – 1.3498 area before the rally resumes. We don’t like selling the proposed pullback and expect buyers to appear once wave (x) pullback is complete in 3, 7, or 11 swing as far as pivot at 1.3406 stays intact.

USDCAD 1 hour Elliott Wave Chart

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

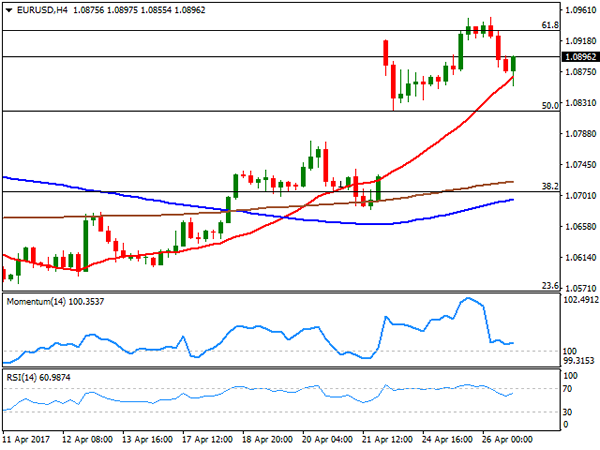

EUR/USD

The greenback closed the day higher against its major rivals, bolstered by hopes the US White House will announce the so long promised tax reform somehow during the day, rather than on the "official" release. The American dollar advanced ahead of Trump unveiling its plan, easing modestly afterwards, as the US administration failed to clarify how they plan to pay for these tax deductions, although higher taxes to imports have been mentioned. Furthermore, the plan presents different scales of reduction, benefiting the most high-income taxpayers that would receive the biggest cuts, both in dollar terms and as a percentage of income. Additionally, the actual administration is considering an executive order on withdrawing the US from the NAFTA, hitting particularly the Mexican Peso and the CAD. Market's attention is now centered on Thursday's ECB monetary policy meeting, with mounting speculation that Mr. Draghi will present a change in the bank's guidance towards future moves, as growth continued to be solid in the region.

The EUR/USD pair fell down to 1.855 its lowest for the week, but bounced modestly from the level, ending the day around the 1.0900 threshold, maintaining the positive tone, despite the intraday decline. In the 4 hours chart, technical readings support additional recoveries, as indicators have corrected extreme overbought conditions, but pared their decline within positive territory, turning modestly higher ahead of Wall Street's close, whilst the intraday decline was quickly reversed after the price briefly slide below a bullish 20 SMA. Still, the price needs to surpass the 1.0930/50 region, where the pair presents the 61.8% retracement of the post-US election decline and the recently achieved yearly high, to be able to extend its gains towards the critical 1.1000 level.

Support levels: 1.0865 1.0820 1.0785

Resistance levels: 1.0950 1.1000 1.1045

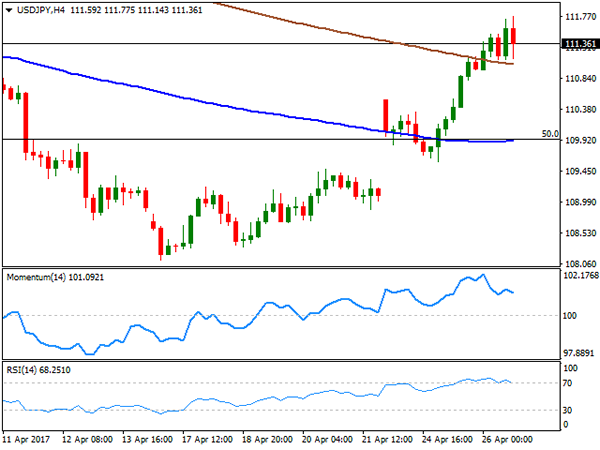

USD/JPY

The USD/JPY pair surged to its highest for this April, printing 111.77, before giving up some its daily gains, still closing in the green. The pair got a boost from a recovery in US Treasury yields, although they later give up after the US government announcement on the tax reform. The 10-year yield benchmark traded as high as 2.33% intraday, but pulled back to 2.31% after ahead of the close, weighing on the pair by the end of the US afternoon. The Bank of Japan will have its monthly monetary policy meeting during the upcoming Asian session, but is expected to maintain the status quo unchanged, with the pair's traders more focused on Thursday's US Durable Goods Orders for March. The positive tone of US equities, helped the pair to hold on to gains by the end of the day, although it's not enough to guarantee a similar advance in Asian equities. From a technical point of view, the 4 hours chart shows that the price held above its moving averages, with buying interest aligned around the 200 SMA, currently around 111.00, whilst technical indicators retreated modestly from extreme overbought readings, but are far from turning lower. Still, the pair needs to regain the 112.00 threshold to be able to extend its advance towards the 113.00 region.

Support levels: 111.05 110.65 110.20

Resistance levels: 112.00 112.45 112.85

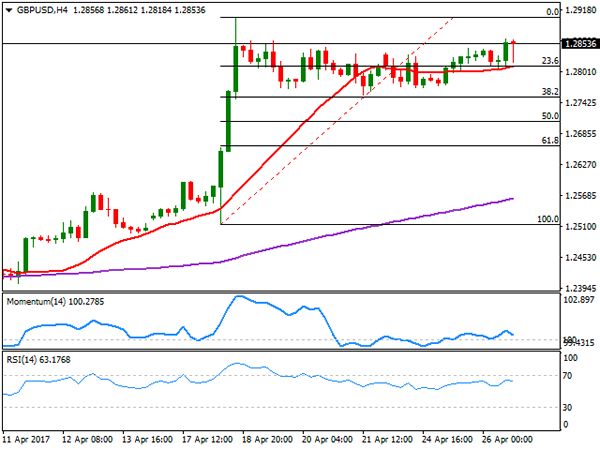

GBP/USD

The British Pound closed the day higher against its American rival, indifferent as usual to broad dollar's intraday demand. The GBP/USD pair traded as low as 1.2804 before recovering, still confined to a tight 60 pips range daily basis, amid the absence of UK macroeconomic news. In fact, UK's calendar will remain light until Friday, when the kingdom will release its preliminary Q1 GDP, with the economy expected to have grew just 0.4% in the three months to March. Trading at its highest for the week, the pair presents a neutral-to-bullish stance in the short term, given that in the 4 hours chart, the price held above the 1.2810 price zone, where the pair has is 20 SMA and the 23.6% retracement of its latest bullish run. In the same chart, technical indicators hold within positive territory, albeit with no certain directional strength, not enough to confirm further gains at the time being. The daily high was set at 1.2863, with further gains beyond it probably resulting in an advance towards 1.2903, this month high, en route to 1.2960.

Support levels: 1.2810 1.2775 1.2730

Resistance levels: 1.2865 1.2910 1.2660

GOLD

After printing a fresh 2-week low of $1,259.99 a troy ounce, spot gold managed to end the day with modest gains at 1,267.45. The mentioned low was achieved during the first half of the day, when hopes ahead of Trump's tax reform plan announcement led the dollar higher, although the momentum of the American currency faded after the official news. Limited physical demand in Asia also weighed on gold. Despite the late recovery, further weakness is expected for the bright metal, amid easing political woes around the world. From a technical point of view, the daily chart shows that the price is below a still bullish 20 SMA, this last at 1,270.90, whilst technical indicators turned flat within neutral territory. In the shorter term, and according to the 4 hours chart, however, the risk is towards the downside, given that the 20 SMA is crossing below the 100 SMA above the current level, while technical indicators lost upward strength within bearish territory, turning south ahead of the Asian opening.

Support levels: 1,259.90 1,250.70 1,242.50

Resistance levels: 1,270.90 1,278.10 1,288.20

WTI CRUDE OIL

West Texas Intermediate crude oil futures closed flat around $49.30 a barrel for a second consecutive gains, unable to hold on to intraday gains beyond the 50.00 threshold. The commodity surged up to 50.18 following the release of US stockpiles data, as the EIA reported a drawdown of 3.6 million barrels for the week ending April 21st. According to the same report, US crude inventories stood at 528.7 million barrels at the end of last week, near the upper seasonal limit, whilst gasoline inventories rose by 3.4 and distillates by 2.7 million barrels, these last denting the positive headline. The daily chart for US oil shows that the advance was contained by selling interest around the 200 DMA, whilst technical indicators have lost their bearish momentum, but remain within negative territory, maintaining the risk towards the downside. In the 4 hours chart, the price is below all of its moving averages, whilst the Momentum indicator stands in neutral territory and the RSI flat around 41, also favoring further slides, despite the current absence of directional strength.

Support levels: 48.85 48.30 47.70

Resistance levels: 49.80 50.30 51.00

DJIA

Having traded within positive territory for most of the day, US major indexes were unable to hold on to gains after Trump's announcement on a tax reform, closing marginally lower. The Dow Jones Industrial Average lost 21 points, to settle at 20,975.09, whilst the S&P lost 0.05%, to 2,387.45. The Nasdaq Composite closed flat at 6,025.23. Stocks eased after Treasury Steven Mnuchin and National Economic Director Gary Cohn released a one-page outline of the plan, failing to provide much detail, somehow disappointing investors. Among the DJIA, United Technologies was the best performer, adding 1.27%, followed by Verizon Communications that gained 1.24%, while Procter & Gamble led decliners, shedding 2.53%. The Dow maintains a positive tone daily basis and despite the intraday decline, as its well above its moving averages, whilst technical indicators have barely lost upward strength within positive territory, but are far from anticipating a downward move. In the shorter term, the 4 hours chart technical indicators head south within positive territory, still correcting overbought readings, but the index holds well above a bullish 20 SMA, this last at 20,863.

Support levels: 20,954 20,914 20,869

Resistance levels: 21,035 21,071 22,010

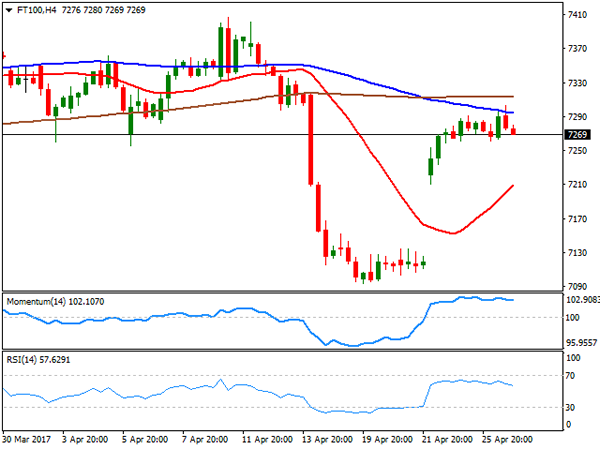

FTSE100

The FTSE 100 added 13 points or 0.18% to close at 7,288.72, but eased in after hours trading, heading into the Asian session at 7,263. The London benchmark benefited by a sharp advance in Standard Chartered that gained 4.01% after the release of its quarterly profit that nearly doubled from a year ago. The second best performer was chemical Croda International that gained 3.77%, also following the release of positive financial figures. Mining-related equities traded lower, after Fresnillo said that gold quarterly production decreased by 3.3%, ending the day 0.7% lower, although the worst performer was GlaxoSmithKline, down by 2.06%. Daily basis, the index is poised to fall further, as it remained contained below its 20 DMA, while technical indicators retreated from their mid-lines, although with limited bearish momentum. In the 4 hours chart, the index is below its 100 and 200 SMAs, but above a bullish 20 SMA, whilst technical indicators are correcting overbought conditions, heading lower within positive territory.

Support levels: 7,254 7,210 7,173

Resistance levels: 7,303 7,340 7,385

DAX

European equities posted a modest advance this Wednesday, with the German DAX ending the day at 12,472.80, up by 0.05%. A cautious stance prevailed ahead of the US President Trump announcement of a tax reform, with the index entering Asia with a soft tone amid easing positive mood. Deutsche Bank was the best performer, up by 2.05% followed by Infineon Technologies that added 1.05%. E.ON on the other hand, led decliners, ending the day down 1.37%. The daily chart shows that the index holds near its recent high and within a tight range, far above bullish moving averages, but with technical indicators easing within positive territory. In the 4 hours chart, technical indicators are barely correcting from extreme overbought readings, whilst the 20 SMA maintains its strong upward slope far below the current level, indicating that while the decline could extend short term, the long term outlook remains positive.

Support levels: 12,418 12,366 12,312

Resistance levels: 12,430 12,495 12,530

Commodities Tread Water In Asia

Trump's tax plans see the greenback strengthen and both oil and precious metal's rallies fizzle out.

Crude Oil

The turkey shoot that is the U.S. Crude Inventories produced another surprise overnight, with a drawdown of 3.6 million barrels against 1.75 million expected. This initially sent both Brent and WTI higher by over one dollar, with the spot levels failing just shy of 52.50 and 50.00 respectively.

The rally, however, was short-lived as traders noted that higher refinery demand had driven most of the drawdown and not end-user demand. Both contracts quickly fell back to close around 51.50 and 48.90 respectively on a spot basis.

For now, though, it is clear that the world has plenty of oil 'in stock,' making OPEC's life that much harder ahead of its June production cut rollover date.

Brent

Brent spot opens slightly higher in Asia at 51.70 with resistance at 52.50 and support at 51.20.

WTI

WTI spot opens at 49.00 with support clearly denoted at 48.70, its 200-day moving average and then 48.50 close behind. Resistance lies at the key 50.00 region, which it has tested and failed near two times this week already.

Precious Metals

Gold

Gold continued its recent trend of lower daily highs overnight, failing at the 1270 level to trade in early Asia around 1266. With the U.S. dollar resurgent after President Trump's tax announcements alongside equities, gold has struggled to make effective rallies as the previous week's geopolitical tensions fade from traders' minds.

From a technical perspective, gold still appears to be setting itself up for a meaningful correction lower with nearby support at 1254, the 200-day moving average, and then the key 1240 level. Gold has resistance at 1280 and then the 1296 area.

Intra-day, gold is locked in a 1260/1270 range with a break of either level probably seeing some stop-loss driven extension.

Silver

Following Tuesday's bearish outside reversal day silver continues to tread water. Like gold, it attempted a rally back over 17.6000, but this soon fizzled out. Silver is trading in Asia around its New York close at 17.4290 with support at 17.3850, the 100-day moving average. Behind this is yesterday's low at 17.3280 and then 17.2600.

Resistance lies at 17.6550 and then the 200-day moving average at 17.9660.

From a charting perspective, a daily close under the 100-dma would confirm the bearish outside reversal from Tuesday and imply that silver may see lower levels ahead.

Emerging Market Asia

Yuan

USDCNY fixed at 6.8896 today, +51 pips from last fixing and -12 pips from the previous closing at 6.8908 at 16:30 Beijing time. While the US Tax reform details remain elusive, the bottom line should be dollar positive. We’ve seen a move higher for the dollar on regional currencies as dollar demand is starting to perk up. Investor confidence in China will be fraught with uncertainty through 2017 as US interest rates are expected to rise, and mainland officials deal with the perils of deleveraging the China money ball. Restoring financial stability will be high on the politburo’s agenda.

Ringgit

The Ringgit opened lower against the US dollar this morning as the greenback picked up steam after the US tax reform announcements on Wednesday. While the Ringgit continues to benefit from the BNM proposed liberalisation of onshore markets, the currency will continue to feel the headwinds from oil price uncertainty. Regardless of the oil patch musing, outflows have subsided, and I suspect the market will re-engage the MYR for no other reason than the domestic capital markets are very much undervalued about its ASEAN counterparts.

Rupee

Inflow remains steady, and with rating upgrades perking up, we expect an increase in flow into the India Capital market that should keep the INR on a positive footing. However, with short dollar positioning a bit over stretched we could see some profit taking ahead of next week’s FOMC. With a positive interest rate carry environment, the short USDINR should remain favourable.

Won

Geopolitical headlines are weighing on the Won, and expectedly dealers were inclined to trim short dollar position. With Trump quashing the NAFTA chatter, it lessens the likelihood of Trade barrier escalation, which should be perceived as risk friendly for regional currencies

A ‘Taxing’ Day For Dealers

A 'Taxing' Day for Dealers

As expected, the Trump administration rolled out the Tax reform roadshow on Wednesday. Given the market’s lofty expectations, traders are viewing it as little more than a road map, rather than the much ballyhooed 'big announcement', because the statement did not provide any comprehensive details. While the essence of the proposal is reflationary and indeed, dollar bullish in a very market friendly positive way, the argument remains for, and further clarity is required on how the tax cut’s deficit ramifications will be offset. Fiscal reforms present a real revenue drain amidst disquieting concerns of the current trajectory for the US deficit. Look for the US administration to revisit the contentious repeal of Obamacare, which also will present another hurdle for risk. Overall, an incredibly Taxing day for traders.

As for the government shutdown, chatter in the Foggy Dew suggests that the legislators will need another week to settle their differences to avoid a shutdown, this despite reports suggesting otherwise. It is all a bit confusing and will likely go down to Friday’s deadline.

While dealers were connecting the tax reform dots, commodity currencies were sideswiped by a report in Politico that the Trump Administration is weighing an executive order to withdraw from NAFTA by officially starting a six-month review period. Predictably, the CAD and MXN have weakened notably on this, but there has been lots of foreshadowing of this move, dating back to mid-March.

Amid all the soundbites, FOMC members have reiterated that they respond to data, rather than Trump uncertainty; yet the market is responding to latter.

Canadian Dollar

Another tough day on the Canada post. While the CAD initially benefited from a larger drop in crude inventories, it was steamrolled by the NAFTA headlines. The bounce in WTI was then unwound after a Bloomberg report that stated Saudi Arabia was losing market share to Iran and Iraq. Traders now think that maybe production cuts may not be extended, and so the balancing act goes on.

Japanese Yen

Despite the USDJPY move overnight, the currency of choice remains the EURJPY, which should underpin the USDJPY near term. We again find ourselves caught in a vortex of headlines driven trade, which tends to muddy the fundamentals. But with risk sentiment expected to reassert itself, it is challenging not to view the USDJPY higher in this environment.

On the BoJ front, no changes are expected, and it is far too early to expect any hawkish delivery from a BOJ that is likely erring on an inflation overshoot before signalling any hike.

Australian Dollar

The AUD has been beaten down after yesterday’s CPI report, which suggests that the RBA will remain accommodative for the foreseeable future and the acute bid that transpired on the USD post-US Tax rhetoric. The NAFTA talk has not only weighed on USDCAD overnight but commodity currencies, as the market re-visits US protectionism and possible announcements on import tax policy.

Dollar Rises Ahead Of Japanese And European Central Bank Announcements

BOJ and ECB expected to stand pat despite improving economic indicators

The USD is higher across the board on Wednesday after US Treasury Secretary Steve Mnuchin and Chief Economic Adviser Gary Cohn presented the outline of the Trump tax reform. Billed as the biggest tax cut in US history its main goal is to unlock growth. The Trump administration had squandered its honeymoon period in Washington by introducing controversial policies on immigration and healthcare instead of the pro-growth reforms signalled right after Trump was victorious in the November elections. A return to pushing those policies could spark the return of the reflation trade, also known as the Trump trade.

The Bank of Japan (BOJ) will publish its Monetary Policy Statement on Wednesday, April 26 at 11:30 pm EDT. The central bank is not likely to update its policy during the April meeting. BOJ Governor Haruhiko Kuroda said on April 20 that the current quantitive easing (QE) program would remain in place for some time. The strength of the JPY has been an obstacle in reaching the central bank’s goal of 2 percent inflation. The BOJ is expected to lower its inflation forecast and upgrade its economic growth outlook.

The European Central Bank (ECB) will release its minimum bid rate on Thursday, April 27 at 7:45 am EDT. ECB President Mario Draghi was active last week talking down a premature tapering as there remain multiple downsides risks to the economy. The market was optimistic after the results of the first round of presidential elections in France. With a Macron and Le Pen second round the worst case scenario was avoided and the EUR rose but until May 7 there are still a lot that could change despite the polls pointing to a healthy Macron lead. After the results of Brexit and the US elections polls do not command the same trust that they used to.

The EUR/USD lost 0.378 percent in the last 24 hours. The single currency is trading at 1.0895 after the Trump administration got back on track with their pro-growth policies. Too early to call the return of the Trump trade, specially with a possible disappointment on Friday as the first estimate of the Q1 GDP will be released.

European economic indicators have been light this week. The German Ifo business climate index rose to 112.9 a six year high as executives are more optimistic about the current state of the German economy. The ECB press conference will be a highlight for investors looking for insights into its QE program after it scaled it back to 60 billion euros a month (from 80 billion euros). The EUR has benefited from a reduction in risk after the first round of the French elections, but there is still more to come not only in the second round, but with the end of the two party system the parliamentary elections are now even more relevant.

The USD/JPY gained 0.232 percent on the Wednesday trading session. The pair is trading at 111.37 as the USD got a boost from the Trump administration’s announcement of its tax reform plans. The BOJ will stand pat on rates and the size of its massive QE program even as there are some positive signs of economic growth. The inflation benchmark of 2 percent remains out of reach however as the current rate hovers around 0.3 percent.

The JPY has been used as a safe haven during volatile times, working against the work of the BOJ. US military actions and the French election made it a natural refuge as the USD and EUR were sold in favour of the Japanese yen. With the return of risk appetite and a reversal of fortune for the greenback it has advanced more than 2 percent against the JPY after touching weekly lows of 108.72.

Market events to watch this week:

Wednesday, April 26

11:50pm JPY Monetary Policy Statement

Thursday, April 27

Tentative JPY BOJ Outlook Report

Tentative JPY BOJ Policy Rate

2:30am JPY BOJ Press Conference

7:45am EUR Minimum Bid Rate

8:30am EUR ECB Press Conference

8:30am USD Core Durable Goods Orders m/m

8:30am USD Unemployment Claims

Friday, April 28

4:30am GBP Prelim GDP q/q

8:30am CAD GDP m/m

8:30am USD Advance GDP q/q

Does Geopolitical Risk Require A Shift In Thinking On Gold?

Up until recently, we had been speaking about shorting gold on the blog. Price was sitting at a major higher time frame resistance level and the opportunity was there to manage our risk around it.

But then the US launched missiles into Syria, tensions on the Korean peninsula escalated and most recently, the French elections all threw a metaphorical spanner in the works.

So does this shift in the geopolitical landscape to a more risk off environment mean that gold becomes a buy?

XAU/USD Daily:

Taking a look at the daily chart, you can see that price has broken above the higher time frame resistance level that we were looking to use as a risk management level for potential shorts.

With this level now gone, should our thinking change with it? If you're in the ‘trade a level until it's broken' camp, then the answer would be yes.

XAU/USD Hourly:

Zooming in to the hourly chart, you can see that after breaking above the higher time frame resistance level, price has now pulled back to retest it this time as support.

This could be viewed as confirmation that the level has in fact held as support and now you would look to buy any short term pullbacks. One such pullback that I've marked in green on the hourly chart above.

Tax Plan Follows The Script

As we anticipated, the trade was to sell-the-fact on the Trump tax plan. The bulk of currencies finished the day unchanged despite some volatility, the only real movers were the commodity currencies, which lagged. The Asia-Pacific calendar is quiet as we count down to the ECB. A new USD trade has been posted alongside supproting charts moments ago.

Yesterday we wrote about the Trump trading plan: to react to the first hints of action, then exit when he delivers. The market followed the script on Wednesday as he delivered his long-touted tax plan.

As anticipated, it wasn't a plan. It was a one-page, bullet point draft of a dozen principles that he hopes to achieve. It mirrored his campaign pledged and much of it was leaked.

The market's response was to unwind a portion of the rally in risk assets since Friday in anticipation of the news. USD/JPY sagged 70 pips to 111.00. The US dollar fell by a smaller margin elsewhere and the S&P 500 gave up an 8 point gain to finish down 1 point.

We will look for more opportunities to trade Trump in the future.

One continues to be CAD and MXN. The White House will likely announce its intention to pull out of NAFTA in the days ahead, according to reports. The Mexican peso was especially hit hard because it would leave the nations without a trade deal. Canada would fall back on the 1987 FTA if no new deal is reached, and that's similar to NAFTA.But if it's similar to NAFTA, Trump could hate it as well. Certainly the door is now open to a radically different trading relationship between the three nations.

USD/CAD didn't break Tuesday's high on the news but it's nearby and the close above 1.3600 is a bullish technical signal. The pair didn't break higher in part because Canadian Feb retail sales ex-autos were slightly better than expected and with a big upward revision to the prior. Also notable for the pair is that oil couldn't hang onto a gain despite a bullish inventory report.

Also on the commodity front, AUD/USD was cut down on yesterday's CPI report. In US trading, it broke below the April lows and that could set up more technical trouble.The only possible catalyst in today's Asia-Pac session is Q1 import/export prices at 0130 GMT but that's a longshot. The consensus on imports is -0.5% and exports is +8.0%.

The bigger story will come Thursday with the ECB decision. Sources reports suggest references to downside risks will be removed and that may help the euro maintain its upside momentum.