Sample Category Title

EUR/CHF Candlesticks and Ichimoku Analysis

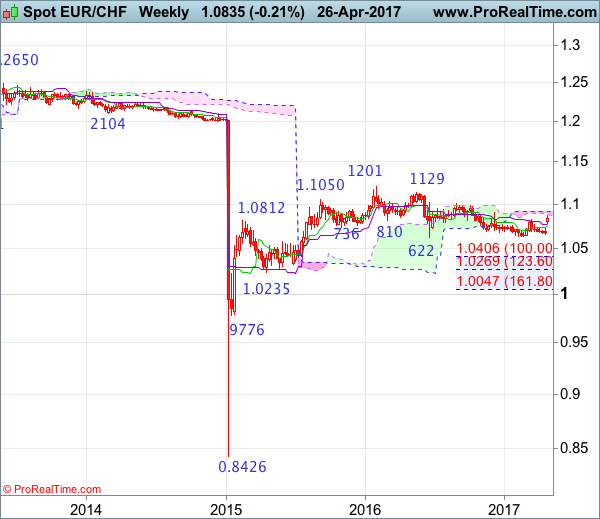

Weekly

• Last Candlesticks pattern: Doji

• Time of formation: 20 Feb 2017

• Trend bias: Up

Daily

• Last Candlesticks pattern: Doji

• Time of formation: 1 Sep 2016

• Trend bias: Near term down

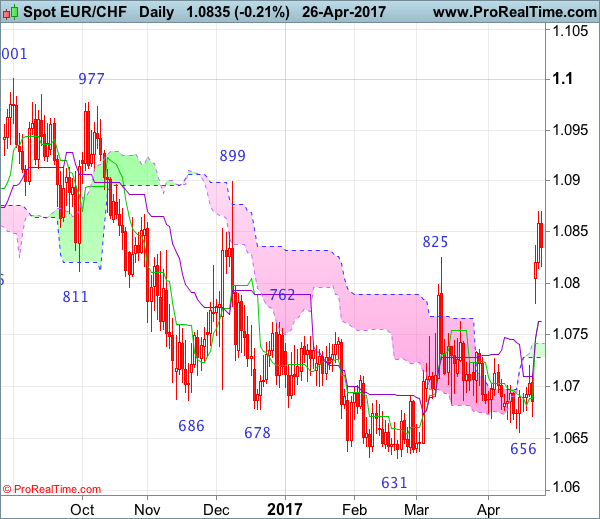

EUR/CHF – 1.0838

The single currency opened higher this week and jumped to as high as 1.0870, the breach of previous resistance at 1.085 signals low has been formed at 1.0631, hence the erratic rise from there may extend further gain to resistance at 1.0899 (Dec high), however, a daily close above there is needed to retain bullishness, then the aforesaid rise may bring at least a stronger correction of early decline to 1.0950-60, then 1.0975-80, having said that, near term overbought condition should prevent sharp move beyond 1.1001 resistance, risk from there has increased for a retreat to take place later.

On the downside, whilst initial downside risk is seen for the pullback from 1.0870 to bring weakness t 1.0800, reckon the Kijun-Sen (now at 1.0763) would limit downside and bring another rise later. A daily close below the lower Kumo (now at 1.0728) would defer and suggest top is possibly formed instead, risk weakness to 1.0671 support but break of indicated support at 1.0656 is needed to add credence to this view and suggest the entire rebound from 1.0631 has ended, bring further fall towards this level later.

Recommendation: Buy at 1.0780 for 1.0980 with stop below 1.0680.

On the weekly chart, although the single currency rebounded initially last week, renewed selling interest emerged around the Kijun-Sen and price should stay above the Tenkan-Sen (now at 1.0753), bring another rise later. Above 1.0870 would extend the erratic rise from 1.0631 low for retracement of recent decline to indicated resistance at 1.0899 but a weekly close above there is needed to retain bullishness and bring a stronger rebound to 1.0970-75, then test of 1.1001. Looking ahead, only a sustained breach above 1.1001 would signal the fall from 1.1201 has ended, bring further gain to 1.1100 but reckon resistance at 1.1129 would hold on first testing.

On the downside, expect pullback to be limited to the Kijun-Sen (now at 1.0765) and the Tenkan-Sen (now at 1.0753) should contain downside, bring another rise later. Only below previous resistance at 1.0720 would abort and suggest top is possibly formed instead, risk weakness towards support at 1.0656 (last week’s low), once this level is penetrated, this would signal the rebound from 1.0631 has ended, bring retest of this level. Looking ahead, euro needs to penetrate indicated strong support at 1.0622-31 to retain bearishness and confirm recent decline from 1.1201 top has resumed and extend further fall to 1.0550-55, then 1.0500-10 but downside should be limited to 1.0400-10 (100% projection of 1.1201-1.0622 measuring from 1.1001) and price should stay well above previous support at 1.0314.

Currencies: Trump Tax Plan No Help For The Dollar. Focus Turns To Draghi

Sunrise Market Commentary

- Rates: Will Draghi trigger new Bund sell-off?

The ECB is expected to keep its policy unchanged. However, Draghi's language at the press conference might reveal more optimism on economic growth and hints about a future unwinding of the ECB's current very accommodative monetary policy stance. The market reaction could be a copy of the one after the March policy meeting (bear steepening). - Currencies: Trump tax plan no help for the dollar. Focus turns to Draghi

Yesterday, the euro fall prey to modest profit taking. However, the lack of details of the Trump tax plan prevented further USD gains. The BOJ left its policy unchanged with little impact on the yen. Today's focus will be on the ECB meeting. If Draghi would sound more optimistic, he might inspire some further unintended euro gains.

The Sunrise Headlines

- US equities ended marginally weaker as they were not impressed by Trump's tax plan. Overnight, Asian stock markets also correct lower with China marginally underperforming (‐0.5%).

- The Trump administration said it was no longer considering pulling out of NAFTA. Mexico, Canada and the US will soon begin talks over renegotiating the agreement.

- President Trump's top economic team unveiled what they called the biggest tax cut in US history, proposing a sharp reduction in corporate taxes and a simplification of individual rates they said would unleash economic growth.

- The BoJ kept its policies unchanged while lowering its inflation forecast. Any exit from its unprecedented monetary easing remains far away. The central bank made a small increase to its growth forecasts for this fiscal year and next.

- Global oil discoveries fell to a record low in 2016, the International Energy Agency says, raising fresh concerns about the potential for a petroleum‐supply shortage as soon as 2020.

- Profits earned by China's industrial firms rose 23.8% in March from a year earlier, buoyed by a continued construction boom, though the pace of growth eased from multi‐year highs seen in previous months.

- Today's eco calendar heats up with US trade balance, durable goods orders, weekly jobless claims, German Inflation, EMU EC economic confidence and central bank meetings in EMU and Sweden. Italy and the US tap the market

Currencies: Trump Tax Plan No Help For The Dollar. Focus Turns To Draghi

Tax plan no help for USD. Focus turns to Draghi

On Wednesday, the combined rally of EUR/JPY, USD/JPY and EUR/USD continued in Asia, but the post‐Macron risk trade slowed in Europe. This caused some profit taking on the euro as investors reduced positions ahead of the Turmp tax plan and the ECB policy meeting today. The Trump tax plan didn't bring additional info. The announcement triggered a slight setback in US equities and in the dollar. EUR/USD reversed part of intra‐day losses and finished the session at 1.0904 (from 1.0926). USD/JPY closed the session little changed at 111.09.

Overnight, the BOJ as expected left its policy unchanged. The bank is rather upbeat on the economy. Still, It cut its inflation forecast for this fiscal year, suggesting that no policy tightening is to be expected anytime soon. The Bank expects the 2% target to be reached during the fiscal year 2018/19. The reaction of the yen is modest. USD/JPY hovers in the 111.20/25 area. Asian equities trade with limited losses following WS. EUR/USD hovers little changed n the 1.09 area. The CAD and MXN rebound as Trump said he doesn't intend to scrap the NAFTA pact.

Today, the eco calendar is well filled. In EMU, the EC confidence data and the German inflation data take centre stage. German HICP inflation is expected to rebound to 1.9 % Y/Y from a surprise drop to 1.5% Y/Y. We consider the expected rebound as quite strong. A lower than expected figure might be slightly negative for the euro. The US calendar heats up with the trade balance, the durable goods orders and the weekly jobless claims. For the durable orders, we see downside risks. The key feature for the (FX) trading will be the ECB meeting. (see our preview). Given uncertainty about the French elections, we expect the ECB to try to avoid volatility. So, the core of its current policy will be confirmed. It is possible that the risk assessment is upgraded to broadly balanced from tilted to the downside. There is a small chance that the reference to even lower rates is scrapped from the forward guidance. However, we think that the June and the September meetings will be crucial.

In a day‐to‐day perspective, the eco data might be mixed for EUR/USD trading. Market disappointment on the Trump tax plan might be slightly negative for the dollar. As was the case last month, the ECB will try to avoid hints about policy normalisation. However, hints on an improvement in the economic context might be seen as opening the door for a change in policy. In such a scenario, EUR/USD might revisit the recent highs. Even a test of the 1.10 barrier might be on the cards.

This week, FX trading was driven by the global risk trade as (European) political event risk eased. This supported USD/JPY but also EUR/USD and EUR/JPY. Market speculation that the decline in EMU political event risk could bring forward the ECB normalisation process supports the euro, too. ECB's Draghi will downplay this speculation. Question is whether the (FX) market will believe it. At the same time, Trump's tax plan is no immediate support for the dollar. So, for now, a cautiously euro positive momentum might persist. From a technical point of view, This week's rebound of USD/JPY suggests a bottoming out process might have started, but the pair needs to regain the 112.20 level (neckline ST double bottom) to improve the picture. EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) late March. The pair returned to the range top after the French election and set minor new highs. We look out how this test turns out. If EUR/USD would regain the 1.10 barrier, next resistance comes in in the 1.1145/1.13 area (US pre/post‐election swings).

EUR/USD maintains gains. Range top under heavy strain

EUR/GBP

Cable continues to challenge recent top

Yesterday, the focus of sterling trading was on external factors, including on the Trump tax plan. Euro profit taking dominated the price action in EUR/GBP. EUR/GBP closed the session at 0.8487. Initially, the dollar held relatively strong against sterling, but cable regained some ground on USD softness after the Trump Tax plan. The pair closed the session at 1.2848.

Today, the UK calendar contains the CBI retail data/distributive reported sales. A slight decline in the sales momentum is expected. However, the figure will have to be really negative to trigger a meaningful decline of sterling. Sterling took a good start against the euro and the dollar this morning. However, if the euro would stay well bid on the ECB policy statement, it could also help to put a floor for the EUR/GBP. Cable currently profits from USD softness.

Early last week, EUR/GBP dropped below EUR/GBP 0.84 support, (temporary) improving the sterling picture. The pair came within reach of the key 0.8305 support (Dec low), but no real test occurred. After this week's rebound, the range bottom is better protected. Longer term, Brexit‐complications remain a potential negative for sterling. Of late, this was not the focus of sterling trading. Nevertheless on technical considerations we are inclined to reconsider a cautious EUR/GBP buy‐on‐dips approach.

EUR/GBP jumps on French election. 0.83 range bottom looks safe for now. Downside better protected due to euro strength

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9935

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9933

Kijun-Sen level : 0.9944

Ichimoku cloud top : 0.9950

Ichimoku cloud bottom : 0.9936

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although dollar has retreated after meeting resistance at 0.9969 yesterday, a firm break below indicated support at 0.9918 is needed to signal the rebound from 0.9893 (this week’s low) has ended, bring retest of this level, break there would confirm recent decline from 1.0108 has resumed and extend weakness to 0.9865-70 (2 times extension of 1.0108-1.0008 measuring from 1.0067), however, reckon support at 0.9831 would hold from here, bring rebound later

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above 0.9969-75 would prolong consolidation, bring another bounce to 0.9981 but break of 1.0000-08 resistance is needed to signal low is formed instead, bring rebound to 1.0025-30 (61.8% Fibonacci retracement of 1.0108-0.9893), however, price should falter below resistance at 1.0067.

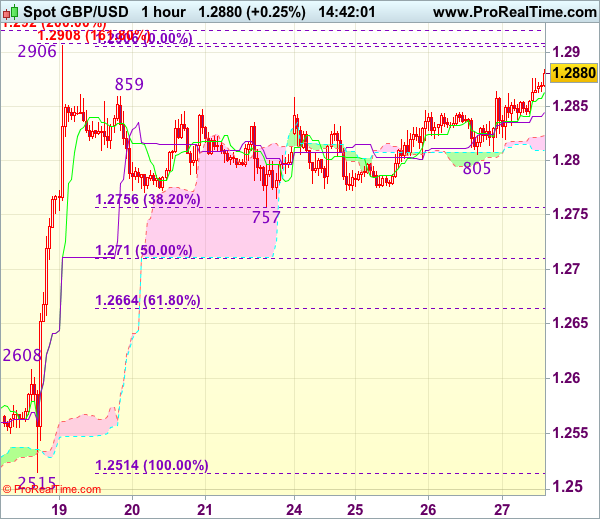

Trade Idea : GBP/USD – Buy at 1.2845

GBP/USD - 1.2884

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2863

Kijun-Sen level : 1.2845

Ichimoku cloud top : 1.2823

Ichimoku cloud bottom : 1.2809

New strategy :

Buy at 1.2845, Target: 1.2945, Stop: 1.2810

Position : -

Target : -

Stop : -

As cable has risen again after finding renewed buying interest at 1.2805, signaling the pullback from 1.2906 has ended at 1.2757 earlier and retest of this level would be seen, break there would confirm recent upmove has resumed for headway o 1.2920-30 (2 times extension of 1.2365-1.2575 measuring from 1.2500), then 1.2950 but reckon 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance) would hold on first testing.

In view of this, would not chase this rise here and would be prudent to buy cable on pullback as downside should be limited to 1.2840-45. Below said support at 1.2805 would abort and prolong consolidation, then risk another corrective fall to indicated previous support at 1.2757 but price should stay well above 1.2710 (50% Fibonacci retracement of 1.2515-1.2906), bring another rise.

Post-Rout Rally Likely For Oil But OPEC Concerns Remain In Place

Key Points:

- Buying pressure should be returning this week.

- Multiple technical reading suggestive of a reversal.

- Fundamentals likely to cap upsides around the 51.55 handle.

Following a much larger than anticipated drawdown in US Crude Inventories, the recent oil rout is levelling out which means buying pressure is likely to be coming down the line in the immediate future. Moreover, both the near and medium-term technical biases are indicating that a bottom has been reached which will also be adding to bullish sentiment. Despite this, overall upsides may be limited which is worth taking into account.

Starting with the long-term technicals, the key structure to keep in mind is that rising wedge which began approximately 12 months ago. Notably, the recent rout has brought oil prices into conflict with the downside of this pattern, which would typically necessitate some upside action, moving ahead. Indeed, this shift in momentum is already becoming apparent given the rather muted moves made by oil over the prior 3 sessions.

This shift in bias comes as little surprise given the developments in a number of near-term technical readings. In particular, a potential ascending triangle or bullish pennant is shaping up which will be reinforcing the effects of the long-term wedge. However, in addition to this, we can also see that stochastics have been pushed into oversold territory around a historical reversal point which will be spurring the bulls into action.

If enough support can be recruited, we expect to see oil prices make their way higher over the next few weeks, potentially even back to above the $50 handle. Although, overall gains are likely to be capped around the 51.55 level as this represents the intersection of the upside of the near-term triangle and the 50.0% Fibonacci retracement. What's more, even getting to this price involves closing back above the 100 day EMA which may prove rather difficult this time around as a result of uncertainty regarding OPEC.

Speaking of the cartel, it's slipping grip on the market is becoming evident for a number of reasons but one recently reported statistic stands out. Specifically, we saw a record uptick in global Oil shipments by tanker to 50.3M barrels last month which can't be a good sign for those wanting to see oil well above the $50 handle. Additionally, Russia is proving reluctant to sign on for an extension of the freeze which will reinforce resistance substantially.

Ultimately, the combination of both the technical and fundamental biases illustrate that, while we can expect to see buoyancy return moving ahead, the 51.55 level should remain a robust zone of resistance. As a result, we may have to see a break out of some form or another in June to resolve the developing disconnect between technicals and fundamentals and this is worth watching out for.

Trump Administ Ration Agreed Not To Terminate NAFTA

Market movers today

Today's main eventis the ECB meeting . Following the latesteCB meeting in early March, market participants have speculated about the sequencing of the ECB's exit st rategy and some weeks ago, the market priced in a 10bp deposit rate hike from the ECB at the end of this year. Since then, the communication from prominenteCB members has signalled a more dovish stance and in the most recent speech from Mario Draghi he concluded 'a reassessment of the current monetary policy stance is not warranted at this stage' . We expect the ECB to send the same dovish message at the coming meeting, while we believe it will stick broadly to its currentint roductory statement without removing some of the soft wording.

Ahead of Draghi 's press conference at 14.30 CET, the German inflation figures are released.

In the US, core capital goods orders are released. Although the oil price has notincreased in 2017, manufacturing confidence is very high, indicating tail winds to core capital goods orders.

Selected market news

Asian equity markets are more or less unchanged this morning following the US administ ration announcement on its tax plans and the Bank of Japan meeting this morning. Regarding the US tax plans, there was no major news, as the Trump administ ration repeated thatit wants to both cutand simplify taxes for individuals (7 to 3 tax brackets) and corporates (15% corporate tax, one-off tax on dollars held overseas " homeland investmentact 2", territorial tax (did not use the words border adjustment tax) financed by removing most tax deductions and higher GDP growth (" 3% or higher"). We still believe Trumponomics will come later and be smaller than previously pledged and thata deal is unlikely to be reached until after Congress's August recess. US equity markets finished flat while the USD weakened slight ly overnightagainst the EUR. Focus in US politics is now on avoiding a U.S. government shutdown, which requires a spending bill to be passed by both houses of the US Congress and signed by President Donald Trump by tomorrow at midnight .

This morning, the Bank of Japan (BoJ) keptits monetary policy measures unchanged as widely expected. No noteworthy reaction in USD/JPY afterwards suggesting that unchanged policy from the BoJ was widely expected. We still expect that the BoJ is likely to keep its policy unchanged for the rest of Koruda's current term as governor, which ends in April 2018.

On trade related issues, the Trump administ ration agreed not to terminate NAFTA at this time and the leaders from Mexico, Canada and the US agreed to proceed swift ly, according to their required internal procedures, to enable the renegotiation of the NAFTA deal to the benefit of all three count ries according to a Bloomberg story ({NSN OP1TGZ6S972H }). The Mexican Peso, which has already st rengthened the most (9.25%) among emerging market currencies against the USD this year, gained another 1.4% this morning. Also the CAD st rengthened by 0.55%.

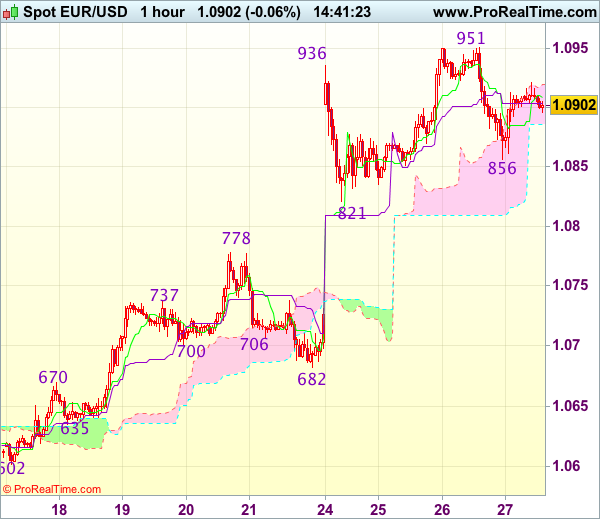

Trade Idea : EUR/USD – Stand aside

EUR/USD - 1.0902

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0909

Kijun-Sen level : 1.0904

Ichimoku cloud top : 1.0919

Ichimoku cloud bottom : 1.0886

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s marginal rise to 1.0951, lack of follow through buying and the subsequent retreat to 1.0856 suggest consolidation below this level would be seen and below said support at 1.0856 would bring correction of recent rise to 1.0835-40 but reckon support at 1.0821 would hold from here, bring another rise later.

In view of this, would be prudent to stand aside for now. Only above said resistance at 1.0951 would extend recent upmove from 1.0340 low to 1.0975-80 and possibly towards 1.1000 which is likely to hold on first testing due to loss of momentum, risk from there is seen for a retreat later.

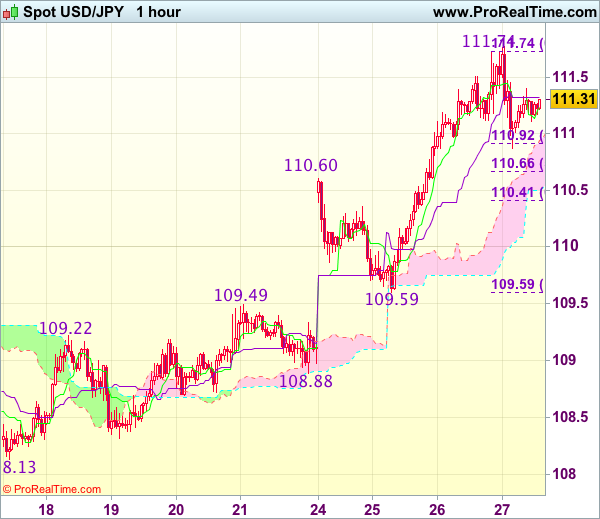

Trade Idea : USD/JPY – Buy at 110.70

USD/JPY - 111.30

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.24

Kijun-Sen level : 111.33

Ichimoku cloud top : 110.94

Ichimoku cloud bottom : 110.50

Original strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

As the greenback retreated after rising to 111.78 yesterday, suggesting consolidation below this level would be seen and pullback to 110.60-69 (previous resistance and 50% Fibonacci retracement of 109.59-111.78) cannot be ruled out, however, reckon downside would be limited and 110.40-45 (61.8% Fibonacci retracement) should hold, bring another rise later, above said resistance at 111.78 would signal recent rise from 108.13 low has resumed and extend further gain to 111.90-00 but overbought condition should prevent sharp move beyond another previous resistance at 112.20.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as previous resistance at 110.60 should limit downside, bring another rally. Below 110.40-45 (61.8% Fibonacci retracement of 109.59-111.78) would defer and suggest top is possibly formed, risk weakness to 109.80 but break of support at 109.59 is needed to provide confirmation.

Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.85% against the USD and closed at 0.7474.

LME Copper prices rose 0.4% or $25.0/MT to $5677.5/MT. Aluminium prices rose 0.8% or $14.5/MT to $1957.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7486, with the AUD trading 0.16% higher against the USD from yesterday's close.

Early morning data showed that Australia's import price index registered an unexpected rise of 1.2% on a quarterly basis in 1Q 2017, defying market expectations for a fall of 0.5% and following a gain of 0.2% in the previous quarter. Further, the nation's export price index climbed 9.4% QoQ in 1Q 2017, higher than market consensus for an increase of 8.0%. In the previous quarter, the index had advanced 12.4%.

Elsewhere, in China, Australia's largest trading partner, industrial profits increased 23.8% on an annual basis in March, after registering a rise of 2.3% in the previous month.

The pair is expected to find support at 0.7451, and a fall through could take it to the next support level of 0.7415. The pair is expected to find its first resistance at 0.7523, and a rise through could take it to the next resistance level of 0.7559.

Moving ahead, traders will look forward to Australia's private sector credit data for March, scheduled to be released in the early hours of tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Euro Trading Marginally Higher, Ahead Of ECB’s Monetary Policy Decision

For the 24 hours to 23:00 GMT, the EUR declined 0.19% against the USD and closed at 1.0907.

On the economic front, French consumer confidence index remained steady at a level of 100.0 in April, meeting market expectations.

In the US, data revealed that MBA mortgage applications rebounded 2.7% in the week ended 21 April 2017, following a drop of 1.8% in the prior week.

In the Asian session, at GMT0300, the pair is trading at 1.0910, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.0860, and a fall through could take it to the next support level of 1.0810. The pair is expected to find its first resistance at 1.0955, and a rise through could take it to the next resistance level of 1.1000.

Going ahead, all eyes will be on the European Central Bank's (ECB) interest rate decision, scheduled to be announced later today. Also, the Euro-zone's final consumer confidence index and Germany's flash consumer price inflation, both for April, will be on investors' radar. Moreover, the US advance goods trade balance, durable goods orders and pending home sales data, all for March coupled with weekly jobless claims data, slated to release later in the day, will garner a significant amount of market attention.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.