Sample Category Title

German Business Confidence Climbed To Its Highest Level Since July 2011 In April

For the 24 hours to 23:00 GMT, the EUR rose 0.26% against the USD and closed at 1.0867, after Germany’s Ifo business climate index surprisingly jumped to a level of 112.9 in April, strengthening to its highest level in nearly 6 years, indicating that businesses are brushing off concerns about the threat of rising protectionism and uncertainties linked to Brexit as well as major European elections. The index registered a revised reading of 112.4 in the prior month, while markets expected for a steady reading.

Additionally, the nation’s Ifo current assessment index unexpectedly rose to a level of 121.1 in April, defying market expectations of a fall to a level of 119.2 and following a revised level of 119.5 in the previous month. On the other hand, the Ifo business expectations index unexpectedly eased to a level of 105.2 in April, contradicting market consensus for a rise to a level of 105.9, thus suggesting that firms remained cautious about the nation’s future economic outlook. The index recorded a level of 105.7 in the previous month.

Separately, the German Bundesbank indicated in its monthly report that high industrial orders, exceptionally optimistic manufacturing sentiment and a rebound in exports supported German economic growth during the first quarter. However, the bank warned that German GDP potential is likely to fall to 0.75% per year by 2025 from around 1.25% at present due to the nation’s aging labour force.

In economic news, the US Chicago Fed national activity index unexpectedly declined to a level of 0.08 in March, compared to a revised level of 0.27 in the previous month. Investors had envisaged for an advance to a level of 0.50. Further, the nation’s Dallas Fed manufacturing business index surprisingly dropped to a level of 16.8 in April, compared to market expectations of an advance to a level of 17.0. In the previous month, the had registered a reading of 16.9.

In the Asian session, at GMT0300, the pair is trading at 1.0861, with the EUR trading 0.06% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.0828, and a fall through could take it to the next support level of 1.0794. The pair is expected to find its first resistance at 1.0886, and a rise through could take it to the next resistance level of 1.0910.

With no major economic releases in the Euro-zone today, investors will look forward to the US consumer confidence index for April, new home sales for March and house price index for February, all slated to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Pound Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the GBP declined 0.08% against the USD and closed at 1.2785.

On the economic front, UK’s CBI industrial trends total orders decreased more-than-anticipated to a level of 4.0 in April, from a reading of 8.0 in the previous month and compared to market expectations of a drop to a level of 5.0.

In the Asian session, at GMT0300, the pair is trading at 1.2780, with the GBP trading slightly lower against the USD from yesterday’s close.

The pair is expected to find support at 1.2755, and a fall through could take it to the next support level of 1.2731. The pair is expected to find its first resistance at 1.2818, and a rise through could take it to the next resistance level of 1.2857.

Going ahead market participants will focus on UK’s public sector net borrowing data for March, scheduled to release in a few hours.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Weaker Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.18% against the JPY and closed at 109.81.

Macroeconomic data indicated that Japan's final leading economic index fell less than initially estimated to a level of 104.8 in February, compared to a drop to a level of 104.7 in the preliminary print and following a reading of 104.9 in the prior month. Also, the nation's final coincident index was revised higher to a level of 115.3 in February, compared to revised level of 113.3 in the flash estimate. In the previous month, the index had recorded a level of 115.1.

In the Asian session, at GMT0300, the pair is trading at 110.07, with the USD trading 0.24% higher against the JPY from yesterday's close.

The pair is expected to find support at 109.65, and a fall through could take it to the next support level of 109.22. The pair is expected to find its first resistance at 110.42, and a rise through could take it to the next resistance level of 110.76.

Looking ahead, Japan's small business confidence index for April and all industry activity index for February, both set to release tomorrow, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

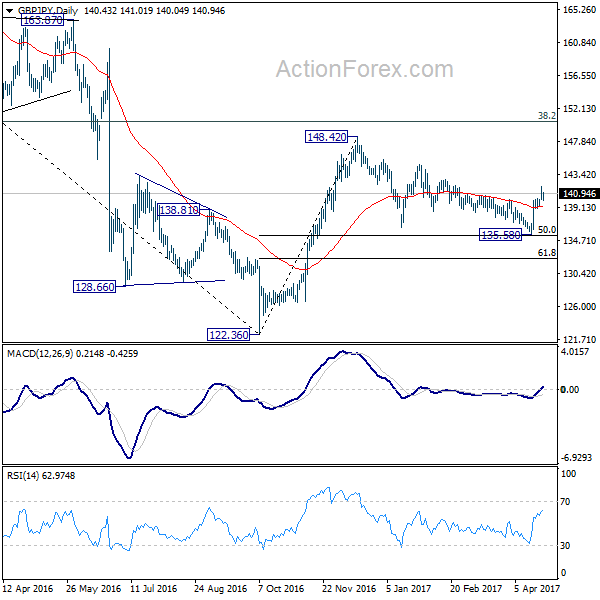

GBP/JPY Daily Outlook

Daily Pivots: (S1) 139.72; (P) 140.88; (R1) 141.58; More....

With 139.19 minor support intact, intraday bias in GBP/JPY remains on the upside for 144.77 resistance. Consolidation pattern from 148.42 should have completed three waves down to 135.58, after hitting 135.39 fibonacci level. Break of 144.77 should extend whole rise from 122.36 through 148.42. On the downside, break of 139.19 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. As long as 50% retracement of 122.36 to 148.42 at 135.39 holds, another rising leg would be seen to 38.2% retracement of 195.86 to 122.36 at 150.42 and possibly above. However, firm break of 135.39 will bring retest of 122.36, with prospect of resuming the larger down trend from 195.86.

Swiss Franc Trading Marginally Lower This Morning

For the 24 hours to 23:00 GMT, the USD slightly declined against the CHF and closed at 0.9958.

In economic news, Switzerland’s total sight deposits rose to a level of CHF569.1 billion in the week ended 21 April, from a level of CHF567.1 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9961, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9933, and a fall through could take it to the next support level of 0.9904. The pair is expected to find its first resistance at 0.9985, and a rise through could take it to the next resistance level of 1.0008.

With no economic releases in Switzerland today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

US To Impose 20.0% Duties On Canadian Softwood Lumber

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the CAD and closed at 1.3514. The Canadian Dollar lost ground after the US announced its first batch of duties on imported wood from Canada.

The US Commerce Secretary, Wilbur Ross, stated that his agency will impose new anti-subsidy tariffs averaging 20.0% on Canadian softwood lumber imports, thus intensifying the long-running trade dispute between the two nations.

In the Asian session, at GMT0300, the pair is trading at 1.3549, with the USD trading 0.26% higher against the CAD from yesterday’s close.

The pair is expected to find support at 1.3452, and a fall through could take it to the next support level of 1.3354. The pair is expected to find its first resistance at 1.3603, and a rise through could take it to the next resistance level of 1.3656.

In absence of any major economic releases in Canada today, trading trend in the CAD is expected to be determined by global macroeconomic events.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

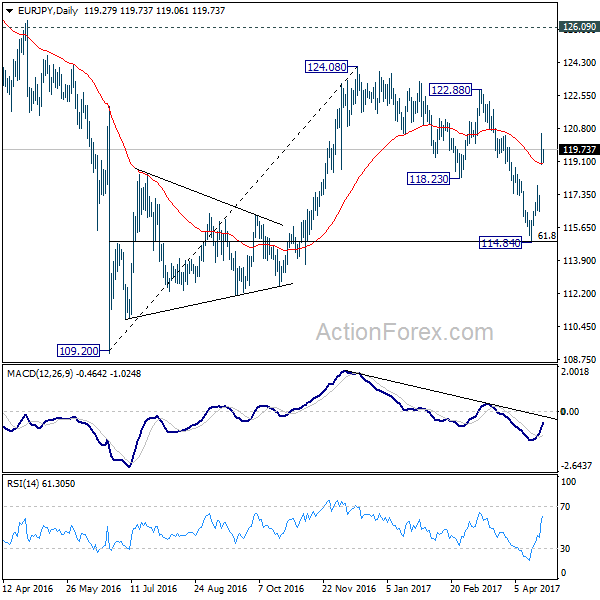

EUR/JPY Daily Outlook

Daily Pivots: (S1) 116.52; (P) 116.91; (R1) 117.37; More...

Intraday bias in EUR/JPY remains on the upside for 122.88 resistance. As noted before, corrective fall from 124.08 has completed at 114.84 already. Break of 122.88 will likely extend the larger rise from 109.20 through 124.08 resistance to 126.09 key resistance level. On the downside, though, 117.81 minor support will turn focus back to 114.84 low instead.

In the bigger picture, price actions from 109.20 is still seen as a corrective move for the moment. But current development suggests that the first leg is finished at 109.20, second leg at 114.84. And rise from 114.84 is possibly developing into the third leg. Further rise will now be mildly in favor through 124.08 resistance. Strong break of 126.09 support turned resistance will confirm completion of whole fall from 149.76 at 109.20. In such case, rise from 109.20 is developing into a medium term move for 141.04 and above.

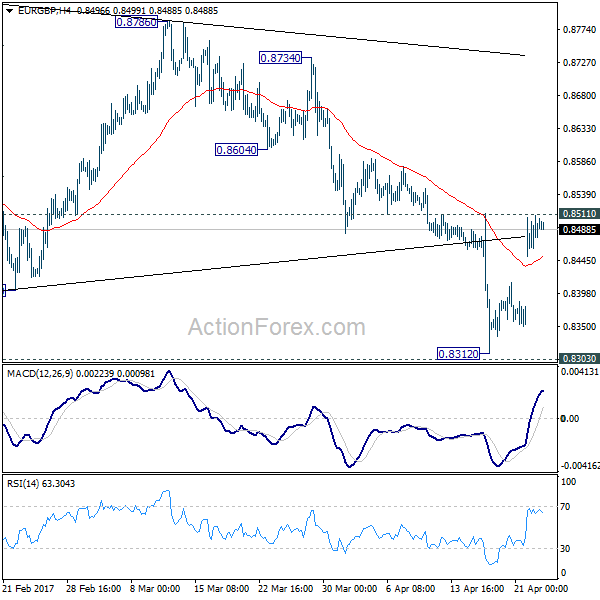

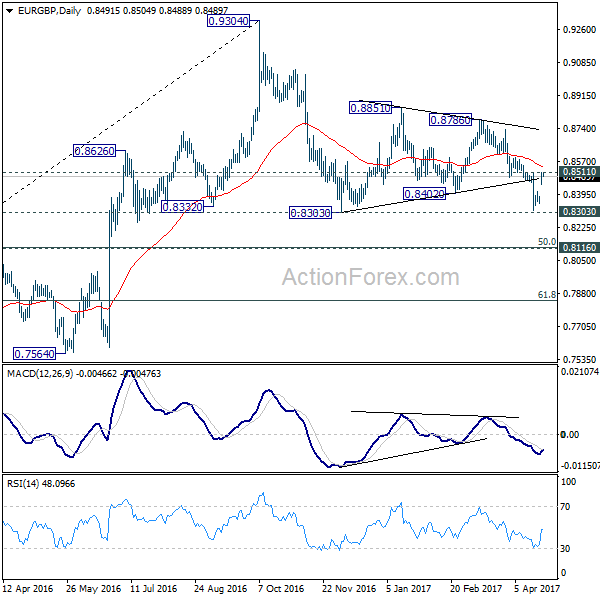

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8459; (P) 0.8484; (R1) 0.8518; More...

Intraday bias in EUR/GBP remains neutral as, at this point, it's still staying below 0.8511 resistance. Break of 0.8303 will extend the corrective fall from 0.9304 to 0.8116/20 key cluster support. We'd expect strong support there to completion the correction and bring rebound. Meanwhile, on the upside, break of 0.8511 will turn bias back to the upside for 0.8786 resistance instead.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is possibly ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

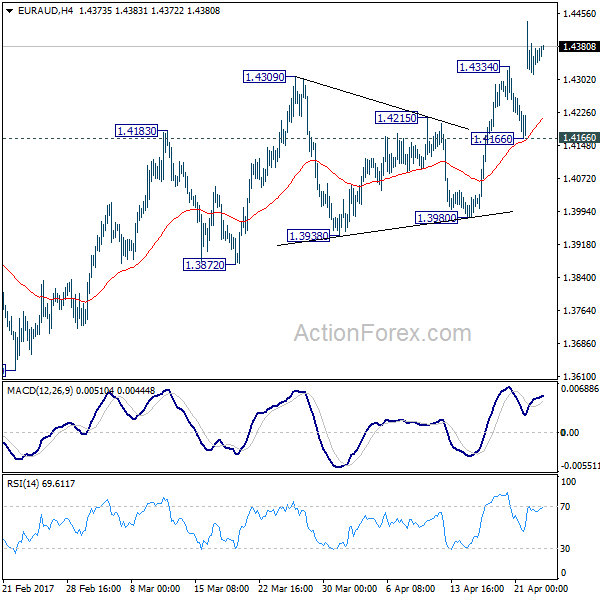

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4301; (P) 1.4370; (R1) 1.4423; More...

Intraday bias in EUR/AUD remains on the upside as rise from 1.3624 is in progress. Further rally would be seen to 1.4721 key resistance. As noted before, we're holding on to the case off trend reversal after defending 1.3671 key support. Decisive break of 1.4721 should confirm. On the downside, break of 1.4166 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after defending 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

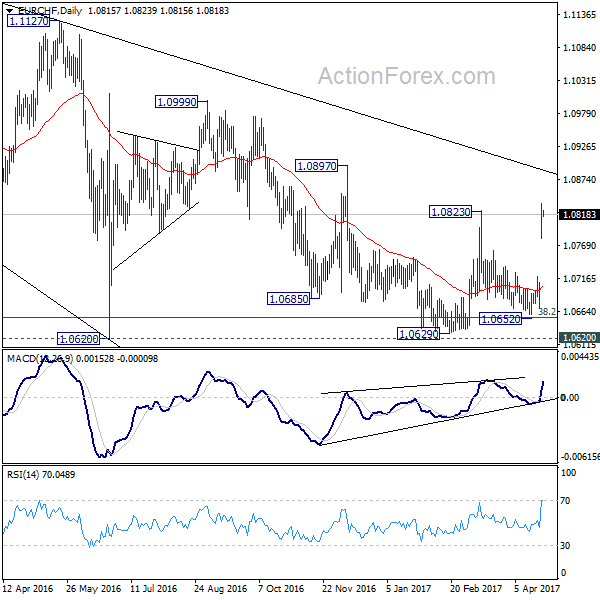

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0788; (P) 1.0812; (R1) 1.0844; More...

Intraday bias in EUR/CHF remains on the upside for the moment. The break of 1.0823 resistance indicates resumption of rise from 1.0629 and carries larger bullish implication. Further rise should now be seen to 1.0897 resistance next. On the downside, below 1.0781 minor support will turn intraday bias neutral and bring retreat first, before staging another rally.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0823 resistance will affirm this bullish case. Further break of 1.0999 will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0652 support holds.