Sample Category Title

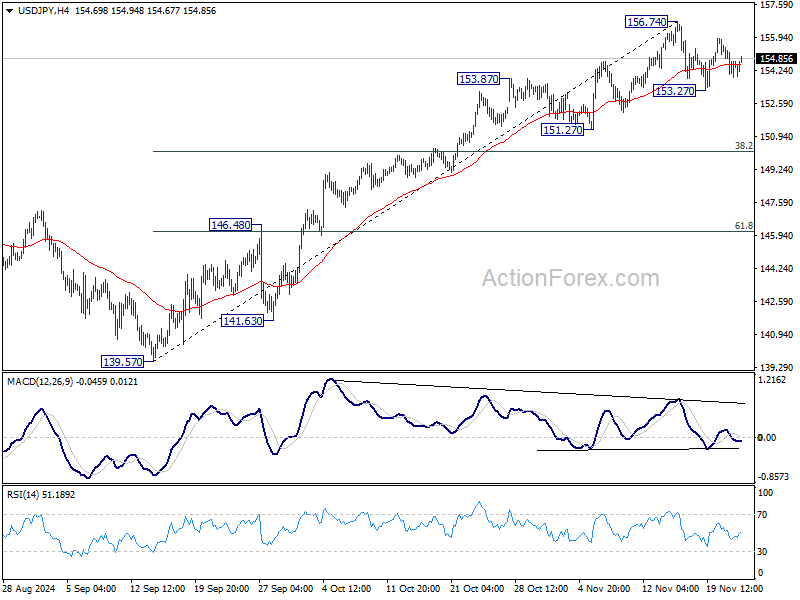

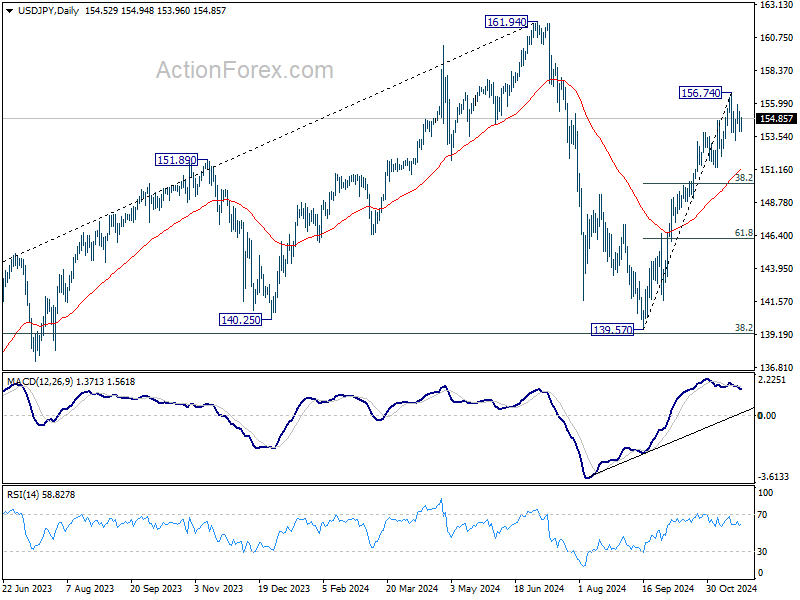

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.82; (P) 154.64; (R1) 155.36; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the upside, break of 156.74 will resume the whole rally from 139.57 towards 161.94 high. On the downside, though, break of 153.27 will resume the correction towards 38.2% retracement of 139.57 to 156.74 at 150.18.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

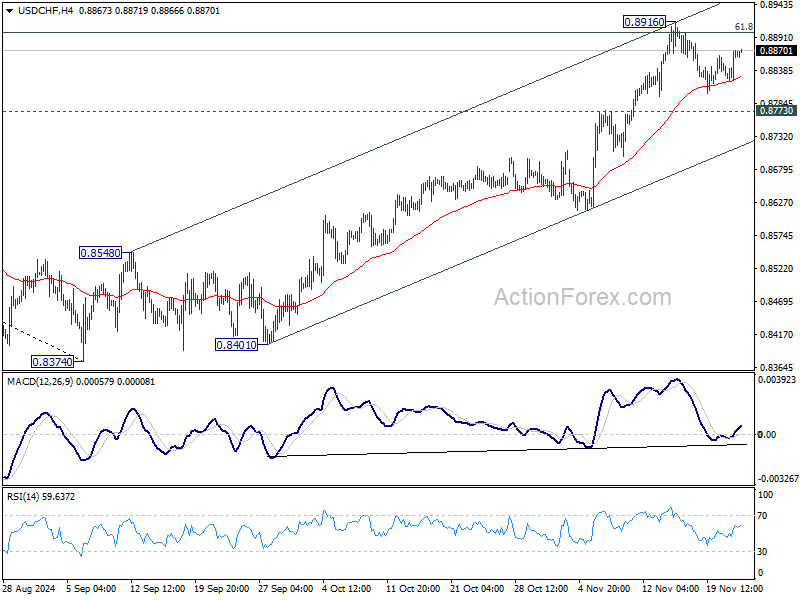

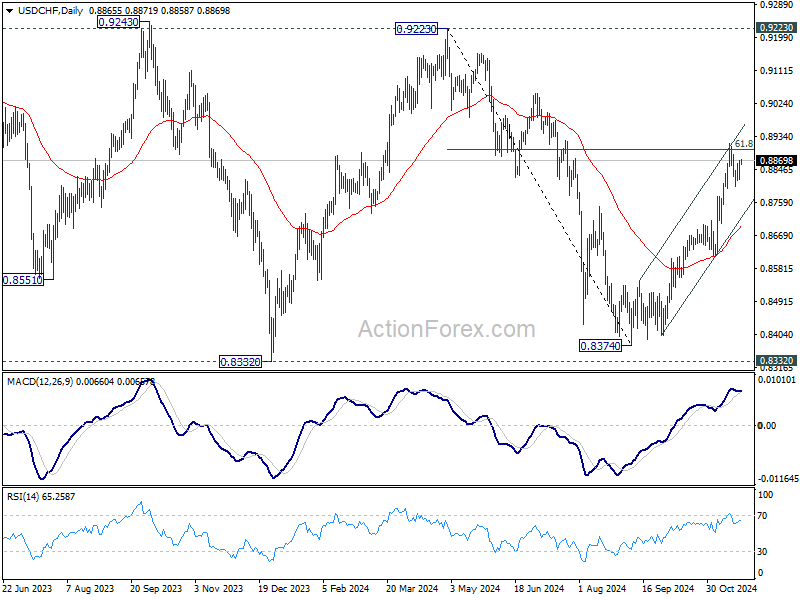

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8835; (P) 0.8854; (R1) 0.8886; More…

Intraday bias in USD/CHF remains neutral as consolidation from 0.8916 is still extending. Further rally is expected as long as 0.8773 resistance turned support holds. On the upside, break of 0.8916 and sustained trading above 61.8% retracement of 0.9223 to 0.8374 at 0.8899 will pave the way back to 0.9223 key resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

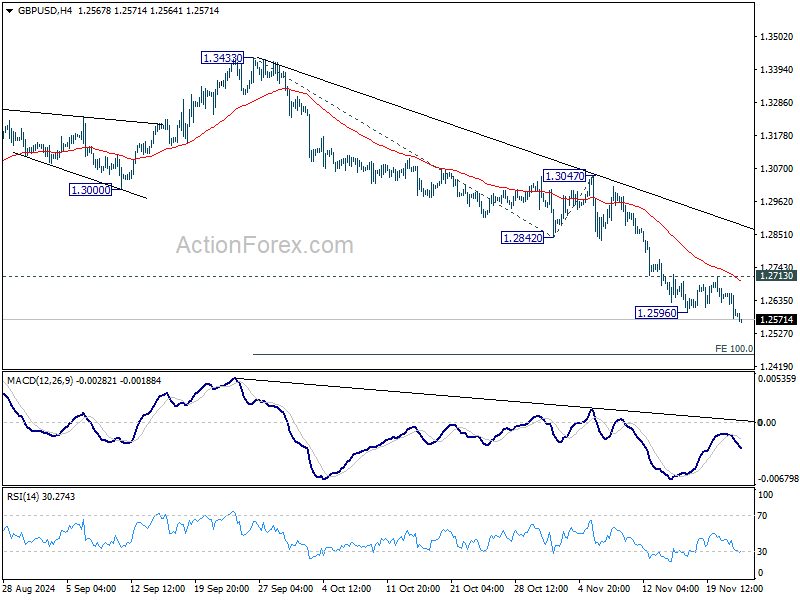

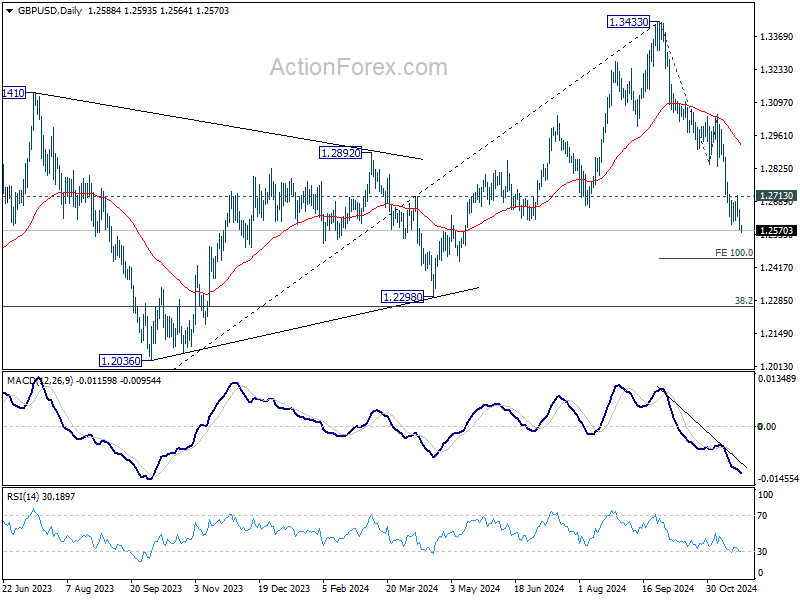

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2557; (P) 1.2609; (R1) 1.2641; More...

GBP/USD's fall from 1.3433 resumed by breaking through 1.2596 and intraday bias is back on the downside. Deeper fall should be seen to 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456. For now, risk will stay on the downside as long as 1.2713 resistance holds, in case of recovery.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

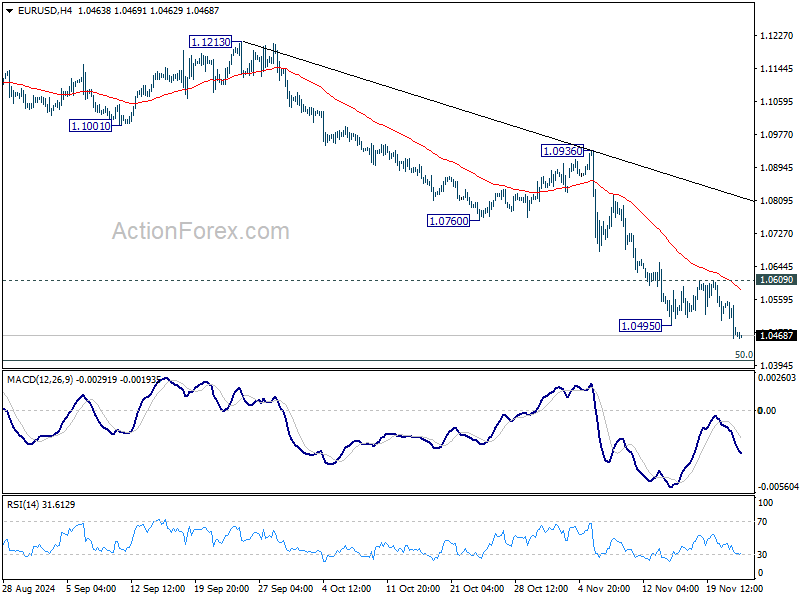

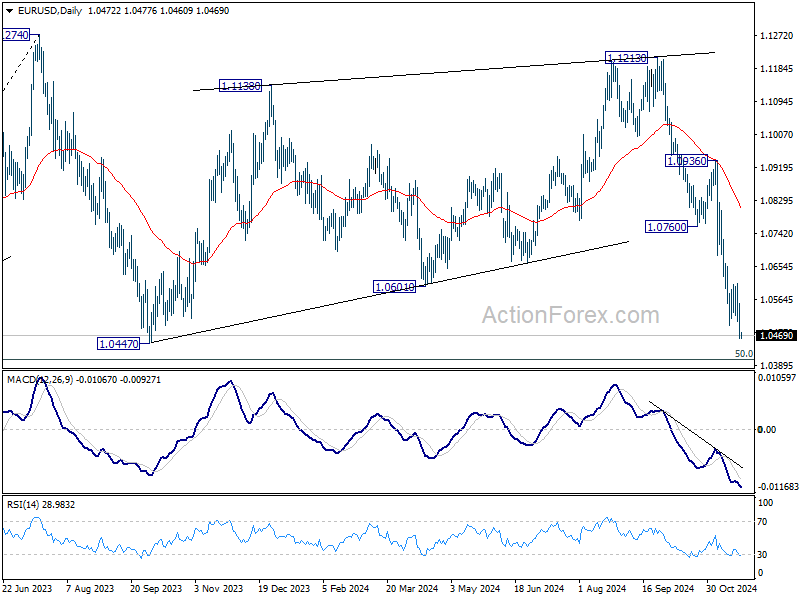

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0439; (P) 1.0497; (R1) 1.0532; More...

EUR/USD's fall from 1.1213 resumed by breaking through 1.0495 temporary low. Intraday bias is back on the downside for 1.0447 support and then 1.0404 key fibonacci level next. Strong support could be seen from this zone to bring rebound. But risk will stay on the downside as long as 1.0609 resistance holds. Decisive break of 1.0404 will carry larger bearish implications.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

Swiss Franc and Dollar Gain as Putin Warns of Global War Escalation, Euro Awaits PMIs

Swiss Franc and US Dollar appreciated broadly today as investors sought safe-haven assets in response to escalating geopolitical risks. Gold extended its near-term rebound, while Bitcoin surged to a new record high, reflecting heightened demand for alternative stores of value.

The catalyst for this shift was a warning from Russian President Vladimir Putin that the conflict in Ukraine is escalating toward a global scale. Putin stated that Russia responded to Ukraine's use of US and British-supplied missiles by launching a new hypersonic medium-range ballistic missile at a Ukrainian military facility. He indicated that additional actions could follow, intensifying concerns about a broader confrontation involving major powers.

Despite these developments, the risk-off sentiment was not uniformly reflected across global markets. DOW closed significantly higher overnight, while NASDAQ edged lower. In Asia, market performance was mixed; Japan's Nikkei 225 advanced whereas Hong Kong's HSI and China's SSE trade in red.

Australian Dollar pulled back slightly but remains one of the week's strongest performers, despite mixed PMI data. Meanwhile, Yen continued to trade within familiar ranges, showing limited reaction to both the geopolitical developments and stronger-than-expected Japanese CPI data.

Attention is now turning to the Eurozone's PMI data scheduled for release today. This data will be particularly significant after Euro's broad-based decline yesterday, breaking key support levels against several major currencies.

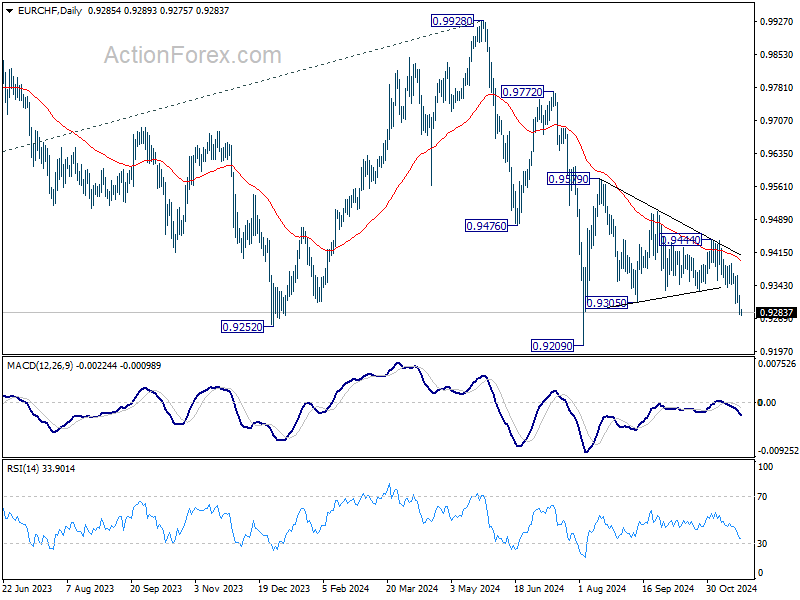

Technically, EUR/CHF's near term decline resumed and breaks through 0.9305 support. Attention is now on whether it picks up downside momentum for breaking through 0.9209 low decisively.

In Asia, at the time of writing, Nikkei is up 0.76%. Hong Kong HSI is down -1.70%. China Shanghai SSE is down -1.58%. Singapore Strait Times is up 0.07%. Japan 10-year JGB yield is down -0.0101 at 1.086. Overnight, DOW rose 1.06%. S&P 500 rose 0.53%. NASDAQ rose 0.03%. 10-year yield rose 0.026 to 4.432.

Japan's CPI eases to 2.3% in Oct, core-core rises to 2.3%

Japan’s inflation data for October revealed persistent and broadening price pressures. Core CPI (excluding food) eased slightly to 2.3% yoy, down from 2.4% yoy but exceeding expectations of 2.2% yoy. This marked the 31st consecutive month core CPI has stayed at or above BoJ's 2% target.

Core-core CPI (excluding food and energy) rose from 2.1% yoy to 2.3% yoy, underscoring renewed strength in underlying inflation. Headline CPI moderated from 2.5% to 2.3%, partly due to slowing energy price gains, which decelerated sharply to 2.3% yoy from 6.0% yoy in September. However, food prices surged 3.8% yoy, accelerating from 3.1% yoy, while services prices edged up to 1.5% yoy from 1.3% yoy.

The combination of steady inflation momentum, recovering consumer spending, and Ten's renewed weakening bolsters the argument for a BoJ rate hike at its upcoming policy meeting in December.

Japan's PMI manufacturing falls to 49.0, services rises to 50.2

Japan’s PMI Manufacturing index edged down to 49.0 from 49.2 in November, signaling a deepened contraction in the sector. In contrast, PMI Services rose slightly to 50.2 from 49.7, indicating a renewed, albeit modest, expansion. PMI Composite improved marginally but remained below the neutral mark at 49.8, up from 49.6.

Usama Bhatti, Economist at S&P Global Market Intelligence, noted that demand conditions were "stagnant," while employment grew at the fastest rate in four months. Price pressures persisted across sectors, driven by rising raw material costs and Yen’s weakness. Firms responded with sharper increases in prices charged for goods and services, aiming to pass on these higher cost burdens to customers.

Australia's PMI composite falls to 49.4, second contraction in three months

Australia’s PMI Manufacturing improved sharply from 47.3 to 49.3 in November, marking a six-month high but remaining in contraction territory. Conversely, PMI Services index dropped from 51.0 to 49.6, hitting a 10-month low and signaling contraction. PMI Composite fell from 50.2 to 49.4, its lowest level in 10 months, indicating a slight overall contraction in private sector output for the second time in three months.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, highlighted the significance of the services sector’s slowdown. “The November S&P Global Flash Australia PMI posted the lowest reading since January, bringing the fourth-quarter average thus far below that of the prior quarter,” Pan said.

The report also noted that easing capacity pressures and subdued activity contributed to slower employment growth, which fell further below the long-term average. In addition, selling price inflation eased as businesses showed caution in raising charges. This combination of softer employment growth and reduced price pressures supports expectations of lower interest rates.

Looking ahead

UK will release retail sales and PMI flash in European session. Germany will release GDP final. Eurozone will also release PMI flash. Later in the day, Canada will release retail sales. US will also release PMI flash.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0439; (P) 1.0497; (R1) 1.0532; More...

EUR/USD's fall from 1.1213 resumed by breaking through 1.0495 temporary low. Intraday bias is back on the downside for 1.0447 support and then 1.0404 key fibonacci level next. Strong support could be seen from this zone to bring rebound. But risk will stay on the downside as long as 1.0609 resistance holds. Decisive break of 1.0404 will carry larger bearish implications.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

Japan’s CPI eases to 2.3% in Oct, core-core rises to 2.3%

Japan’s inflation data for October revealed persistent and broadening price pressures. Core CPI (excluding food) eased slightly to 2.3% yoy, down from 2.4% yoy but exceeding expectations of 2.2% yoy. This marked the 31st consecutive month core CPI has stayed at or above BoJ's 2% target.

Core-core CPI (excluding food and energy) rose from 2.1% yoy to 2.3% yoy, underscoring renewed strength in underlying inflation. Headline CPI moderated from 2.5% to 2.3%, partly due to slowing energy price gains, which decelerated sharply to 2.3% yoy from 6.0% yoy in September. However, food prices surged 3.8% yoy, accelerating from 3.1% yoy, while services prices edged up to 1.5% yoy from 1.3% yoy.

The combination of steady inflation momentum, recovering consumer spending, and Ten's renewed weakening bolsters the argument for a BoJ rate hike at its upcoming policy meeting in December.

Japan’s PMI manufacturing falls to 49.0, services rises to 50.2

Japan’s PMI Manufacturing index edged down to 49.0 from 49.2 in November, signaling a deepened contraction in the sector. In contrast, PMI Services rose slightly to 50.2 from 49.7, indicating a renewed, albeit modest, expansion. PMI Composite improved marginally but remained below the neutral mark at 49.8, up from 49.6.

Usama Bhatti, Economist at S&P Global Market Intelligence, noted that demand conditions were "stagnant," while employment grew at the fastest rate in four months. Price pressures persisted across sectors, driven by rising raw material costs and Yen’s weakness. Firms responded with sharper increases in prices charged for goods and services, aiming to pass on these higher cost burdens to customers.

Australia’s PMI composite falls to 49.4, second contraction in three months

Australia’s PMI Manufacturing improved sharply from 47.3 to 49.3 in November, marking a six-month high but remaining in contraction territory. Conversely, PMI Services index dropped from 51.0 to 49.6, hitting a 10-month low and signaling contraction. PMI Composite fell from 50.2 to 49.4, its lowest level in 10 months, indicating a slight overall contraction in private sector output for the second time in three months.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, highlighted the significance of the services sector’s slowdown. “The November S&P Global Flash Australia PMI posted the lowest reading since January, bringing the fourth-quarter average thus far below that of the prior quarter,” Pan said.

The report also noted that easing capacity pressures and subdued activity contributed to slower employment growth, which fell further below the long-term average. In addition, selling price inflation eased as businesses showed caution in raising charges. This combination of softer employment growth and reduced price pressures supports expectations of lower interest rates.

Cliff Notes: Calm Conditions

Key insights from the week that was.

In Australia, the RBA’s November Meeting Minutes provided a deep dive into the Board’s baseline views and assessment of risks. Chief Economist Luci Ellis subsequently discussed a number of noteworthy developments, one being the statement that the Board “would need to observe more than one good quarterly inflation outcome to be confident that such a decline in inflation was sustainable.” This is in line with the Board’s policy strategy to take and signal a patient and careful approach to assessing current disinflation. It should also be noted that the RBA’s economic and policy forecasts incorporate technical assumptions on the cash rate path based on market pricing. Of late, market pricing has shifted the start date for cuts back and also reduced the expected quantum of easing; the RBA have expressed a greater degree of comfort with such a view, considering known risks at this time.

Following these developments, we adjusted our view on the most probable path for monetary policy. We have moved back the start date for the cutting cycle from February to May, but have retained 100bps of easing in 2025, with a terminal rate of 3.35% still forecast for the December quarter. We see risks to the timing of the first cut in May as broadly balanced. Some of the more notable risks include the pace of the expected recovery in consumer spending following Stage 3 tax cuts – the hit to real incomes in prior years and caution shown by consumers towards spending in recent months leads us to expect a slower recovery in consumption growth than the RBA – and the tightness of the labour market. Both of these uncertainties have important implications for inflation’s trajectory. Next week’s October monthly inflation gauge will be another important update on Australia’s immediate inflation pulse and the risks (see here for our preview).

Over in the UK, annual inflation accelerated to 2.3% in October as electricity price rebates from 2023 cycled out. Core inflation was unaffected by this development, but edged higher to 3.3%yr in the month as services inflation remained sticky around 5.0%yr. Inflation is on track to overshoot the Bank of England’s 2.0%yr target for 2024 overall – the CPI needs to rise just 0.1% in the next two months for annual inflation to print at 2.25%yr come December 2024. The BoE’s more cautious tone around back-to-back cuts hence speaks to the lingering uncertainty for inflation.

In Japan meanwhile, while the data has not pushed rate hikes off the table, it is also yet to convince that the virtuous cycle of prices and wages is being sustained. Governor Ueda noted this week that the December meeting would be ‘live’ and that data between now and December would dictate their decision. CPI ex. fresh food came in slightly above expectations at 2.3%yr in October, below September’s 2.4%yr and August’s 2.8%yr, but above the 2.0%yr policy target. Services inflation has shown greater momentum in the past three months. RENGO leader Tomoko Yoshino has called on the new Prime Minister to support small businesses in raising wages ahead of the union’s wage negotiations in March. RENGO will be targeting another 5.0% increase in wages for FY25 after it secured a 5.1% increase in FY24. Persistence in inflation will help make the union’s case, as will support from the government. Large businesses in Japan have been quieter this year about their wage plans. Arguably, the BoJ will want to see evidence that businesses intend to maintain wage growth in FY25 before they raise rates again.

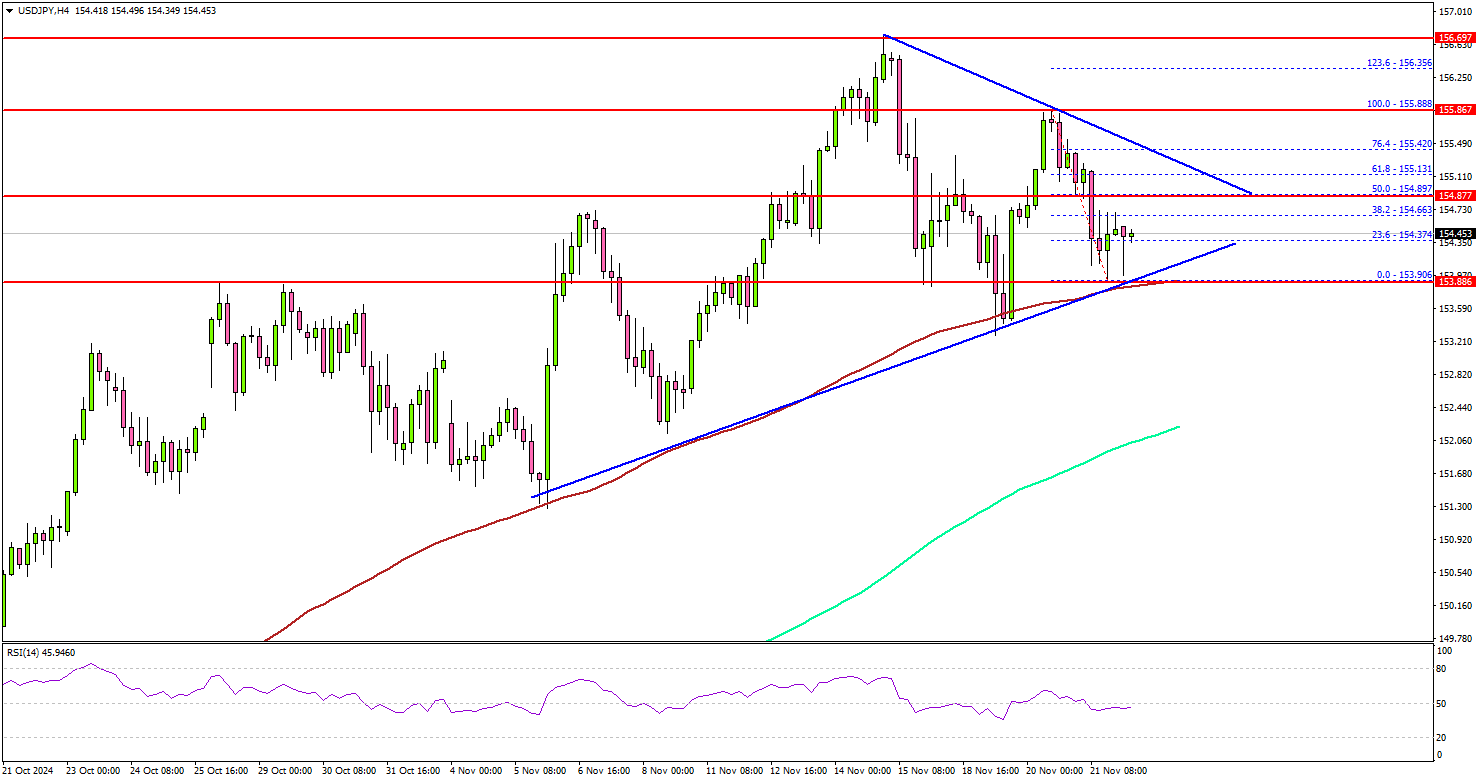

USD/JPY Consolidates: Is a Fresh Upside Move Ahead?

Key Highlights

- USD/JPY started a consolidation phase above the 154.00 zone.

- A major contracting triangle is forming with resistance at 155.30 on the 4-hour chart.

- Bitcoin remains in a strong uptrend and traded to a new all-time high above $95,000.

- EUR/USD dipped further and traded below the 1.0500 support zone.

USD/JPY Technical Analysis

The US Dollar started a downside correction below 156.00 against the Japanese Yen. USD/JPY traded below the 155.50 support to enter a short-term bearish zone.

Looking at the 4-hour chart, the pair dipped below the 154.20 support and tested the 100 simple moving average (red, 4-hour). The pair remained stable above 154.00 and is currently well above the 200 simple moving average (green, 4-hour).

A low was formed at 153.90 and the pair is now trading in a range. On the upside, the pair could face resistance near the 154.90 level.

The first major resistance is near the 155.30 level. There is also a major contracting triangle forming with resistance at 155.30 on the same chart. A close above the 155.30 level could set the tone for another increase.

The next major resistance could be 155.85, above which the price could climb higher toward the 156.50 resistance. Any more gains might send USD/JPY toward 158.00.

On the downside, immediate support sits near the 154.00 level. The next key support sits near the 153.60 level. Any more losses could send the pair toward the 153.00 level or even 152.40 in the near term.

Looking at Bitcoin, the price extended gains, traded to a new all-time high above $94,000 and might continue to move up.

Upcoming Economic Events:

- Euro Zone Manufacturing PMI for Oct 2024 (Preliminary) – Forecast 46.0, versus 46.0 previous.

- Euro Zone Services PMI for Oct 2024 (Preliminary) – Forecast 51.8, versus 51.6 previous.

- US Manufacturing PMI for Oct 2024 (Preliminary) – Forecast 48.8, versus 48.5 previous.

- US Services PMI for Oct 2024 (Preliminary) – Forecast 55.3, versus 55.0 previous.