Sample Category Title

Weekly Focus – Geopolitics Back on the Radar

Rising tensions between Russia and Ukraine caused renewed unease in the markets this week. Putin signed an amendment to Russian nuclear doctrine, which allows Russia to use nuclear weapons for retaliating against strikes carried out with conventional weapons, if they were supported by a nuclear state. The change was an obvious response to US allowing Ukraine to use long-range ATACMS-missiles for strikes within Russian territory. Ukraine swiftly performed its first missile strikes to Russia using American and British weapons starting Tuesday, and on Thursday, Russia fired a barrage of missiles including a novel intermediate-range ballistic missile against the city of Dnipro in eastern Ukraine.

While the missile was not an intercontinental ballistic missile like the Ukrainian officials initially claimed, Pentagon reported that similar missiles could be refitted to carry nuclear warheads as well. Both sides have called past week's events an escalation in the war, that has now lasted more than 1000 days. Despite the sabre-rattling on the battlefield, Reuters' sources also reported Putin would be ready to discuss ceasefire when president-elect Donald Trump enters the White House. We remain doubtful that finding common ground around the negotiation table will be as easy as Trump has suggested.

Equity markets traded with a shaky, yet generally positive sentiment in the US, and oil prices rose modestly. Weak set of flash PMIs from the euro area pushed rates lower on Friday, as the composite index plunged back into contractionary territory (48.1; Oct. 50.0). At the time of writing, markets are pricing more than 50% probability for the ECB's 50bp rate cut in December. Broad USD continued its post-election rally supported by solid outlook for the US economy, and EUR/USD is already trading around 1.04. We have been strategically bullish on the greenback for several years, and earlier this week we shifted our 12M EUR/USD forecast even lower to 1.01, read more from FX Forecast Update - Red sweep widens Atlantic FX gap, 18 November.

Next week will be a quiet one in terms of macro data. Main focus will be on November flash HICP data from euro area on Friday, with early signals from German and Spanish country data coming already on Thursday. We expect base effects from weaker reading a year ago to boost headline inflation to 2.3% in y/y terms (from 2.0%) and core inflation to 2.8% y/y (from 2.7%). On a monthly level, inflation momentum has still likely continued moderating, which should further pave the way for ECB cuts in December and beyond. Several ECB officials will be on the wires leading up to the release, including Lane on Monday as well as Villeroy and Nagel on Tuesday.

In the US, focus will be on October's PCE data, which includes the Fed's preferred gauge of inflation. Earlier CPI release suggested that price pressures remained stable on a monthly level in headline and core terms. Markets remain divided over whether the Fed will cut rates in December, and FOMC's November minutes on Tuesday could offer some additional clues on the most likely rate path going forward - we still call for a 25bp cut.

On the other side of the world, Reserve Bank of New Zealand (RBNZ) has become one of the most aggressive central when it comes to rate cuts. We expect another 50bp reduction next week, but markets are speculating with a small chance for an even larger 75bp move.

Sunset Market Commentary

Markets

November EMU PMI’s were one of the final reality checks going into the December 12 policy meeting (and beyond). Last month, there was a glimmer of hope with the overall index at 50. HCOB analyses even saw tentative signs of some light at the end of the (German) tunnel. However, the November data made crystal clear that the tunnel for the EMU economy is much longer and darker than expected. The composite PMI tumbled back in contraction territory (48.1 from 50.0), the lowest level in 10 months. The manufacturing PMI also dropped further to 45.2 from 46.0, but the major negative surprise came from services as it joined the contraction in the manufacturing (49.2 from 51.6) for the first time in 10 months. Intra-EMU divergence persisted with Germany and France seeing even bigger declines in output than in October. France even marked the fastest decline in activity in since January. The rest of the EMU still sees business activity increasing, but at the slowest pace in the current 11-month sequence of growth. The odds for a recovery also aren’t good as new orders decreased for the sixth month running. Employment declined for the fourth consecutive month, but the decline remains limited. HCOB describes the EMU environment as stagflationary as the decline in activity coincides with higher input and output prices, mainly due to higher wage costs in the services sector. In its assessment on Germany, HCOB mentions political uncertainty due to the election of Donald Trump and the announcement of snap elections in Germany. We don’t label it as a glimmer of hope yet, but German expectations for next year improved slightly on hopes that the next government would develop measures to boost the economy, maybe by reforming the debt brake. The market reaction was telling and ‘logical’. German yields are currently ceding between 9 bps (2-y) and 3 bps (30-y), after even bigger losses this morning. Money markets again seen an almost 50/50 chance between a 25 bps and 50 bps ECB rate cut in December. ECB’s Villeroy said he sees inflation reaching 2% earlier in 2025 than expected and is careful of the risk of undershooting the target. ECB’s Centeno also warned on this risk, but still defended a gradual adjustment. US yields were understandably little affected by the decline in EMU. US yields declined 1-2 bps across the curve in the run-up to the publication of the US PMI’s. EUR/USD tumbled in a flash crash post the PMI’s and briefly touched the lowest level since November 2022 (1.0335 area). A close below 1.0448 (currently 1.0425) materially weakens the technical picture with 1.0201 (62% retracement 2022-2023 move) the next target on the charts. At the time of finishing this report, the US PMI’s show ongoing strength in the economy. The composite index improved further to 55.3 from 54.1 on a strong performance of services (55.3 from 54.1). US yields are moving toward unchanged levels. Additional USD gains stay modest (DXY 107.5, EUR/USD 1.041).

News & Views

November UK PMI’s showed a sustained drop in private sector employment amid weaker business optimism and rising cost inflation. The composite PMI slipped from 51.8 to 49.9 (vs 51.7 consensus), the first sub-50 reading since October 2023. New order growth eased to its lowest for one year Details showed a deterioration in both manufacturing (48.6 from 49.9; 9-month low) and services (50 from 52; 13-month low). S&P global market intelligence, responsible for the surveys, commented that companies are giving a clear thumbs down to the policies announced in Labour’s first Budget. Especially the planned increase in employers’ National Insurance contributions hurts. The November PMI is indicative of the economy slipping into a modest decline, with GDP dropping at a 0.1% quarterly rate. The loss of confidence hints at worse to come. Still elevated rates of wage-related price and cost growth limit scope for further BoE rate cuts. It helps explain today’s “modest” fall in UK yields (5 bps across the curve). EUR/GBP initially followed EUR/USD south on weak EMU PMI’s (EUR/GBP 0.8268 intraday low) before rebounding after the UK data to opening levels near 0.8320.

Hungarian gross wages declined by 0.3% on a monthly basis in September, but were still 12.5% higher compared with a year ago. Net earnings increased by 12.3% and real earnings were 9.2% higher than a year earlier. Wage pressure remains stronger in the public sector (+0.5% M/M & 14.1% Y/Y) compared with the private sector (-0.4% M/M & 11.9% Y/Y). The forint remains in the defensive (EUR/HUF 411) as CE FX face a perfect storm of higher USD rates, rising geopolitical tensions and weakness in key trading partner Germany.

US PMI composite jumps to 55.3, accelerating growth and cooling inflation

The US economy showed signs of stronger momentum in November as PMI data highlighted robust activity in the services sector. PMI Manufacturing improved slightly to 48.8 from 48.5, remaining in contraction but showing some stabilization. Meanwhile, PMI Services surged to a 32-month high of 57.0 from 55.0, boosting the Composite PMI to 55.3, up from 54.1, the highest in 31 months.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, noted, "The business mood has brightened in November, with confidence about the year ahead hitting a two-and-a-half-year high." Optimism was fueled by expectations of lower interest rates and a more pro-business stance from the incoming administration, which supported increased output and stronger order book inflows.

Economic growth appears to be accelerating in Q4, with the survey indicating a pickup in overall activity. At the same time, inflationary pressures are cooling. The survey's price gauge pointed to only a marginal increase in prices across goods and services, signaling that consumer inflation is running well below Fed's 2% target.

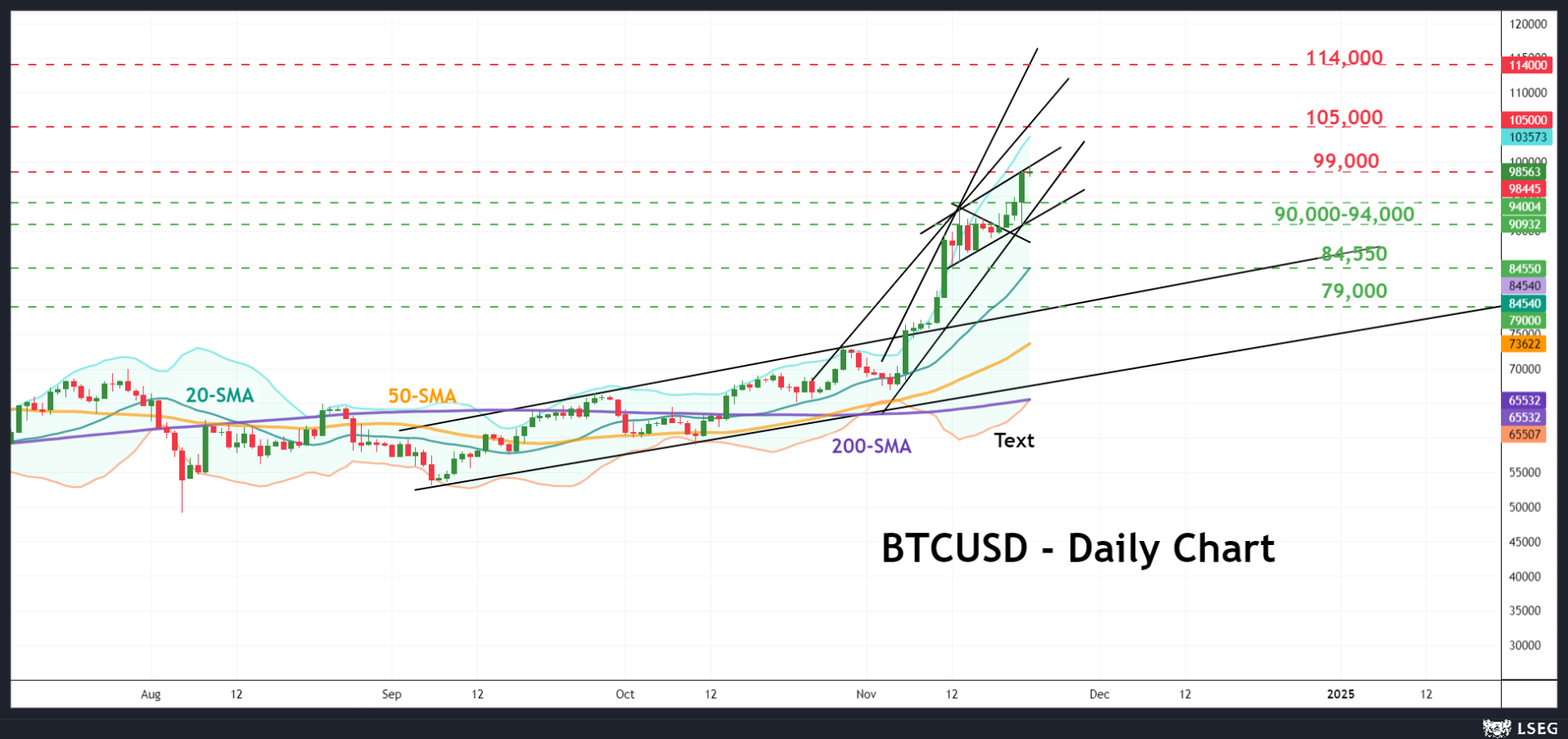

BTCUSD Historic Rally Flirts With 100k

- BTCUSD nonstop rally almost reaches 100k

- Caution needed as market looks overbought

BTCUSD (Bitcoin) is experiencing one of its best moments in its history, having rocketed by 40% to reach an all-time high of 98,670 in just a month as investors swallowed Trump’s promising crypto regulatory pledges and at the same time sought safety against a complex global geopolitical landscape.

From a technical perspective, the recent rally followed the completion of a bullish pennant formation. However, as the RSI is approaching its recent highs in the overbought zone, traders might be inclined to lock in profits. That said, there may still be some extra room for improvement as the price has yet to confirm overbought conditions around the upper Bollinger Band.

Assuming the wall around 99,000 is breached, the next resistance could develop near 105,000. Should the bulls drive above 110,000, the spotlight might turn to 114,000.

Alternatively, if upside forces evaporate immediately, the price could seek protection within the 90,000-94,000 trendline zone. If that base collapses, the price could fall aggressively toward the 20-day simple moving average (SMA) at 84,550 and then to 79,000.

In a nutshell, BTCUSD traders could be sensitive to downside pressures in the short-term following the latest massive rally. If the bulls successfully claim the 99,000 level, the next peak could occur near 105,000.

Canada: Retail Sales End the Third Quarter on a Solid Footing

Retail sales rose by a healthy 0.4% month-over-month (m/m) in September, in line with Statistics Canada’s advance estimate.

Sales were even stronger in real terms. When adjusted for inflation, the volume of retail sales was 0.8% higher on the month.

One weak spot was sales at motor vehicle and parts dealers, which declined by 0.7% m/m after two consecutive months of gains.

Lower gasoline prices also weighed on headline retail sales. Receipts at gas stations and fuel vendors dropped by 2.3% m/m in nominal terms but gained 3.2% m/m in real terms.

Excluding both auto sales and gas station receipts, core retail sales rose by 1.4% m/m in September, driven by food and beverage stores (+3.0% m/m) and building material and garden equipment stores (+3.0% m/m).

E-commerce sales rose by 3.3% m/m, following a 1.5% decline recorded in the previous month.

Statistics Canada’s advance estimate for October points to another solid increase of 0.7% m/m.

Key Implications

Retail sales gained momentum toward the end of the third quarter, rising 3.5% on a quarter-on-quarter (q/q) annualized basis in Q3. This strong finish sets real consumption spending on track for a 1.5-2.0% gain in the third quarter.

The Bank of Canada may have gotten what it wanted: a rebound in consumption growth. Statistics Canada's advance estimate and our internal spending data point to further acceleration in October, particularly in home-related purchases. Additionally, the recent proposed tax holidays could provide a significant boost to consumer spending during the exemption period from mid-December to mid-February. This holiday shopping season may have a bit more sparkle than expected.

Euro and Sterling Under Fire after PMIs, Swiss Franc Reverses Gains

European majors are experiencing significant selling pressure today, with Euro leading the declines. Euro sharply depreciated as traders increased their bets on an aggressive 50 bps rate cut by ECB in December, following dismal PMI data. Market expectations for such a cut have surged to 50%, a substantial rise from around 15% just a day earlier. The region's services sector has now entered contraction, aligning with the manufacturing sector's prolonged recession. This economic downturn is further exacerbated by escalating geopolitical risks, notably the escalation of the Ukraine war, and the looming threat of tariffs from US President-elect Donald Trump. These factors intensify the urgency for ECB to accelerate its monetary easing towards a neutral rate to support the faltering economy.

Sterling is also under substantial strain, weighed down by a larger-than-expected contraction in UK retail sales and disappointing November PMI readings. S&P Global observed that business sentiment in the UK has been declining since the general elections earlier this year. The Labour government's Autumn Budget failed to boost confidence, with sentiment instead plunging sharply. This suggests that the worst may still be ahead for the UK economy, as consumer spending weakens and businesses express growing concern over economic policies.

Swiss Franc initially spiked higher against Euro and Sterling earlier in the day. However, it reversed those gains after SNB Chairman Martin Schlegel emphasized that negative interest rates remain a possibility. The SNB is currently expected to cut interest rates by 25 basis points in December. Yet, the situation is fluid; a larger cut by ECB could prompt SNB to respond similarly to prevent excessive appreciation of the Franc. The complexity of this monetary chess game is heightened by the fact that both central banks will announce their decisions on the same day, December 12.

As the week nears its conclusion, Euro is the worst performer among major currencies, followed by Sterling and Swiss Franc. However, late-week developments could still alter this ranking. On the other hand, Canadian Dollar is firmly in the lead as the strongest currency, supported additionally by robust retail sales data. Australian Dollar and Japanese Yen follow, while Dollar and New Zealand Dollar occupy middle positions.

Canada retail sales rises 0.4% mom in Sep, 0.7% mom in Oct

Canada's retail sales rose by 0.4% mom in September to CAD 66.9B, slightly above market expectations of a 0.3% mom increase. Gains were observed in six out of nine subsectors, with food and beverage retailers leading the growth.

Core retail sales, which exclude gasoline and motor vehicle-related sectors, surged by a robust 1.4% mom, highlighting strength in consumer discretionary spending.

For Q3, retail sales climbed 0.9%, with a 1.3% increase in volume terms, suggesting solid economic activity during the period.

The advance estimate for October indicates a further 0.7% mom rise, reinforcing signs of resilience in consumer demand.

Eurozone PMI signals stagflation as both manufacturing and services contract

Eurozone economic activity weakened sharply in November, with PMI Manufacturing falling to 45.2 from 46.0 and PMI Services dropping to 49.2 from 51.6, pushing Composite PMI to a 10-month low of 48.1, down from 50.0. For the first time since January, both sectors recorded output declines, reflecting broader economic struggles.

Country-level data painted a bleak picture. France saw its Composite PMI drop to 44.8, with Manufacturing PMI at 43.2 and Services PMI at 45.7—both hitting 10-month lows. Germany's Composite PMI fell to 47.3, a 9-month low, with Services PMI sliding into contraction at 49.4 despite a slight improvement in Manufacturing PMI, which edged up to 43.2.

Cyrus de la Rubia of Hamburg Commercial Bank highlighted "stagflationary" conditions, with falling activity alongside rising input and output prices driven by service sector costs and wage growth. He pointed to political instability in France and Germany and global uncertainties, including potential US tariffs, as key contributors.

UK PMI composite fall to 49.9, slips into contraction as post-budget sentiment worsens

UK economic activity weakened in November, with the Composite PMI falling from 51.8 to 49.9, its first contraction in 13 months. Manufacturing PMI declined to a 9-month low of 48.6, down from 49.9, while Services PMI hit a 13-month low at 50.0, down from 52.0.

Chris Williamson of S&P Global Market Intelligence noted that businesses are reporting falling output and employment cuts for the second consecutive month. Post-budget sentiment has deteriorated sharply, with optimism now at its lowest since late 2022. Companies have expressed significant concern over the announced increase in employers' National Insurance contributions.

The November data suggest the economy is contracting modestly, with GDP estimated to decline at a quarterly rate of -0.1%. Williamson warned of the potential for further job losses unless sentiment improves.

On the inflation front, selling price growth slowed to its lowest post-pandemic rate, but elevated wage pressures in services remain a challenge, likely tempering the case for aggressive rate cuts by BoE.

UK retail sales drop sharply by -0.7% mom in Oct, but broader trends show resilience

UK retail sales volumes plunged by -0.7% mom in October, significantly underperforming expectations of a -0.3% mom decline. Also, volumes remained -1.5% below their pre-pandemic level in February 2020.

On a broader basis, retail activity was more encouraging. Sales volumes increased by 0.8% in the three months to October compared to the preceding three months. When measured against the same period last year, sales volumes grew by 2.5%. This represents the strongest annualized growth since March 2022, despite a downward revision of September's annual figure from 2.6% to 2.1%.

Japan's CPI eases to 2.3% in Oct, core-core rises to 2.3%

Japan’s inflation data for October revealed persistent and broadening price pressures. Core CPI (excluding food) eased slightly to 2.3% yoy, down from 2.4% yoy but exceeding expectations of 2.2% yoy. This marked the 31st consecutive month core CPI has stayed at or above BoJ's 2% target.

Core-core CPI (excluding food and energy) rose from 2.1% yoy to 2.3% yoy, underscoring renewed strength in underlying inflation. Headline CPI moderated from 2.5% to 2.3%, partly due to slowing energy price gains, which decelerated sharply to 2.3% yoy from 6.0% yoy in September. However, food prices surged 3.8% yoy, accelerating from 3.1% yoy, while services prices edged up to 1.5% yoy from 1.3% yoy.

The combination of steady inflation momentum, recovering consumer spending, and Ten's renewed weakening bolsters the argument for a BoJ rate hike at its upcoming policy meeting in December.

Japan's PMI manufacturing falls to 49.0, services rises to 50.2

Japan’s PMI Manufacturing index edged down to 49.0 from 49.2 in November, signaling a deepened contraction in the sector. In contrast, PMI Services rose slightly to 50.2 from 49.7, indicating a renewed, albeit modest, expansion. PMI Composite improved marginally but remained below the neutral mark at 49.8, up from 49.6.

Usama Bhatti, Economist at S&P Global Market Intelligence, noted that demand conditions were "stagnant," while employment grew at the fastest rate in four months. Price pressures persisted across sectors, driven by rising raw material costs and Yen’s weakness. Firms responded with sharper increases in prices charged for goods and services, aiming to pass on these higher cost burdens to customers.

Australia's PMI composite falls to 49.4, second contraction in three months

Australia’s PMI Manufacturing improved sharply from 47.3 to 49.3 in November, marking a six-month high but remaining in contraction territory. Conversely, PMI Services index dropped from 51.0 to 49.6, hitting a 10-month low and signaling contraction. PMI Composite fell from 50.2 to 49.4, its lowest level in 10 months, indicating a slight overall contraction in private sector output for the second time in three months.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, highlighted the significance of the services sector’s slowdown. “The November S&P Global Flash Australia PMI posted the lowest reading since January, bringing the fourth-quarter average thus far below that of the prior quarter,” Pan said.

The report also noted that easing capacity pressures and subdued activity contributed to slower employment growth, which fell further below the long-term average. In addition, selling price inflation eased as businesses showed caution in raising charges. This combination of softer employment growth and reduced price pressures supports expectations of lower interest rates.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0439; (P) 1.0497; (R1) 1.0532; More...

EUR/USD's decline accelerated to as low as 1.0330 so far and there is no sign of bottoming yet. Sustained trading below 1.0404 key fiboncci level will carry larger bearish implications. Next target will be 161.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0203. Nevertheless, strong rebound from current level, followed by break of 1.0609 resistance, will confirm short term bottoming.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 and below.

Canada retail sales rises 0.4% mom in Sep, 0.7% mom in Oct

Canada's retail sales rose by 0.4% mom in September to CAD 66.9B, slightly above market expectations of a 0.3% mom increase. Gains were observed in six out of nine subsectors, with food and beverage retailers leading the growth.

Core retail sales, which exclude gasoline and motor vehicle-related sectors, surged by a robust 1.4% mom, highlighting strength in consumer discretionary spending.

For Q3, retail sales climbed 0.9%, with a 1.3% increase in volume terms, suggesting solid economic activity during the period.

The advance estimate for October indicates a further 0.7% mom rise, reinforcing signs of resilience in consumer demand.

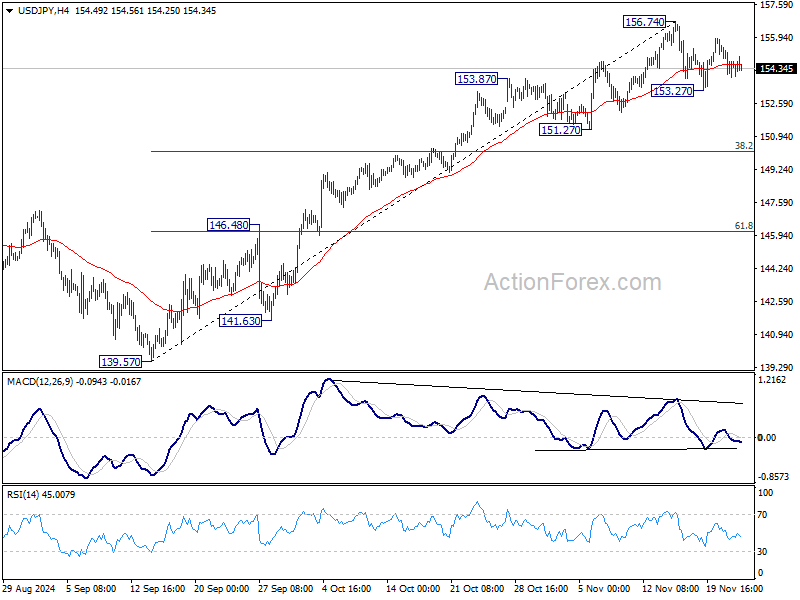

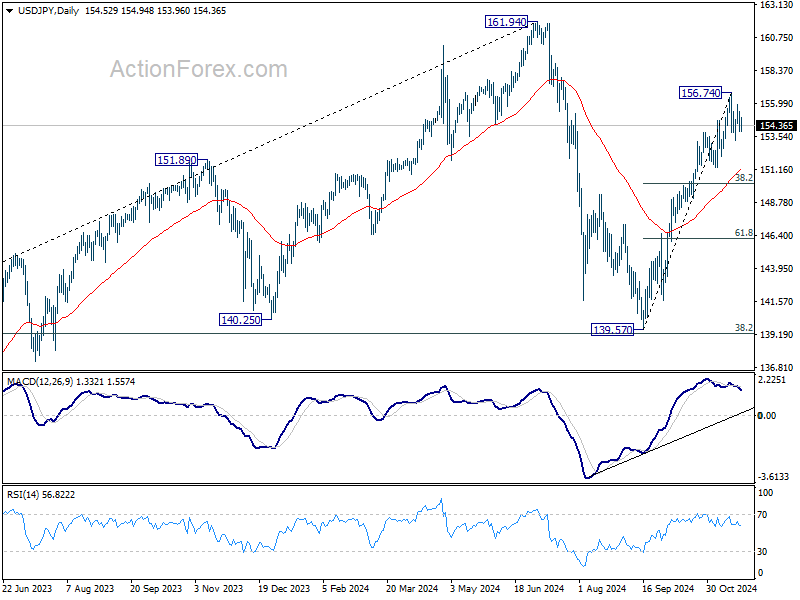

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.82; (P) 154.64; (R1) 155.36; More...

USD/JPY is still bounded in range trading and intraday bias stays neutral. On the upside, break of 156.74 will resume the whole rally from 139.57 towards 161.94 high. On the downside, though, break of 153.27 will resume the correction towards 38.2% retracement of 139.57 to 156.74 at 150.18.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

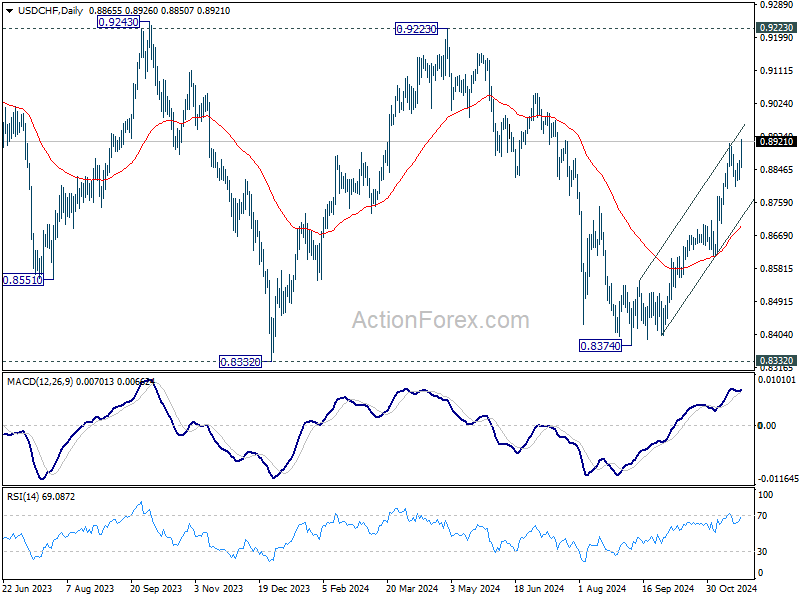

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8835; (P) 0.8854; (R1) 0.8886; More…

USD/CHF's rally from 0.8374 resumed by breaking 0.8916 resistance. Intraday bias is back on the upside. Further rise should be seen towards 0.9223 key resistance next. For now, outlook will stay bullish as long as 0.8800 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

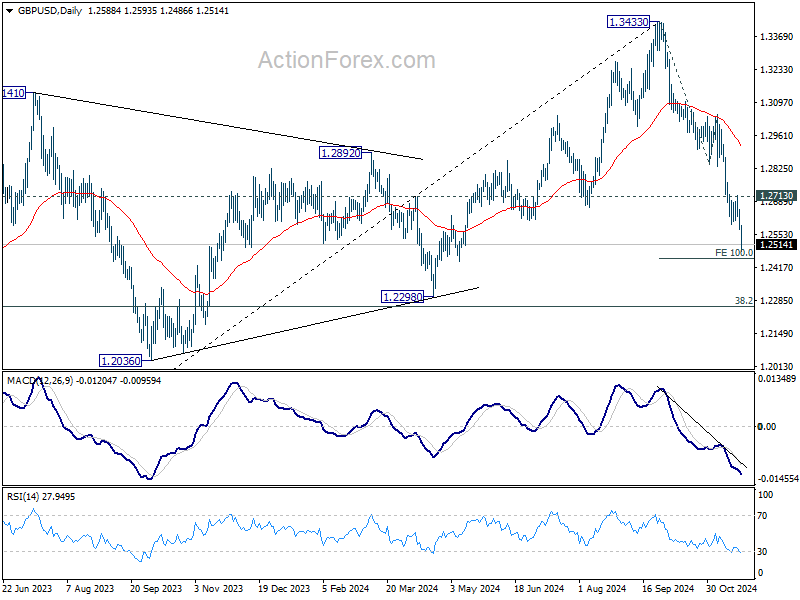

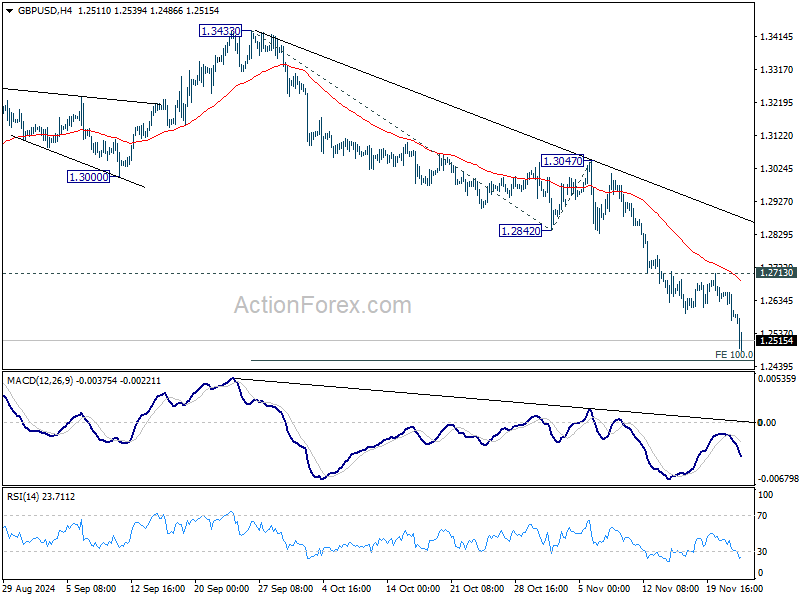

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2557; (P) 1.2609; (R1) 1.2641; More...

GBP/USD's accelerates lower today and intraday bias stays on the downside for 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456. Decisive break there will extend the fall from 1.3433 to 1.2298 cluster support zone. For now, risk will stay on the downside as long as 1.2713 resistance holds, in case of recovery.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.