Sample Category Title

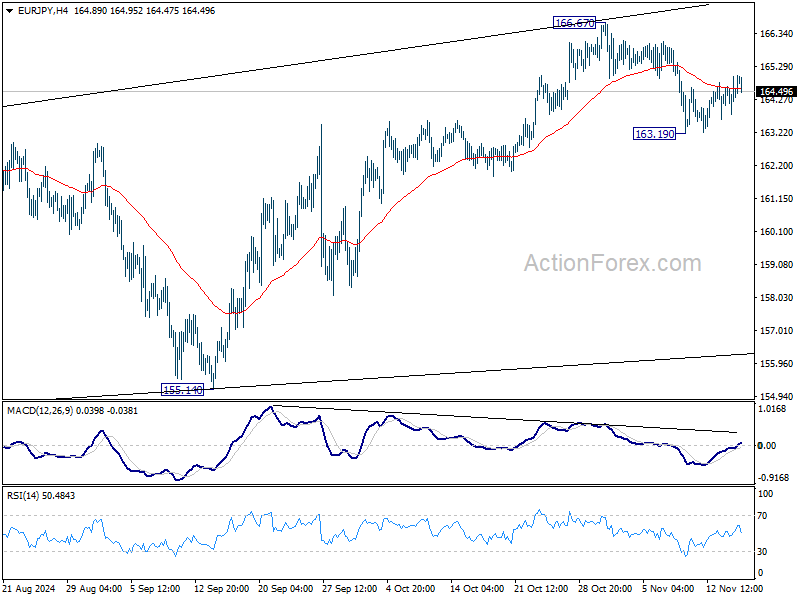

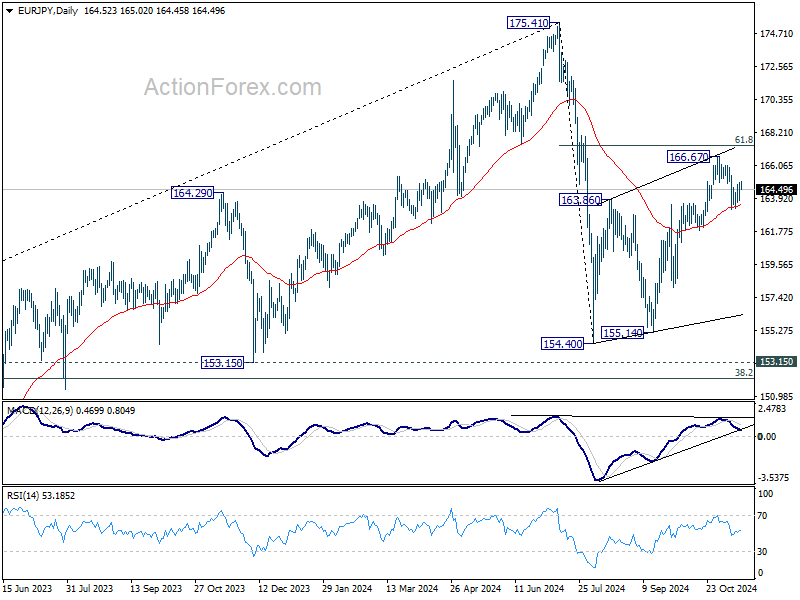

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.91; (P) 164.44; (R1) 165.09; More....

No change in EUR/JPY's outlook and intraday bias stays neutral. On the downside, sustained trading below 55 D EMA (now at 163.48) will argue that whole corrective rise from 154.40 has completed with three waves up to 166.67. Deeper decline should then be seen back to 154.40/155.14 support zone. On the upside, break of 166.67 will target 61.8% retracement of 175.41 to 154.40 at 167.38 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

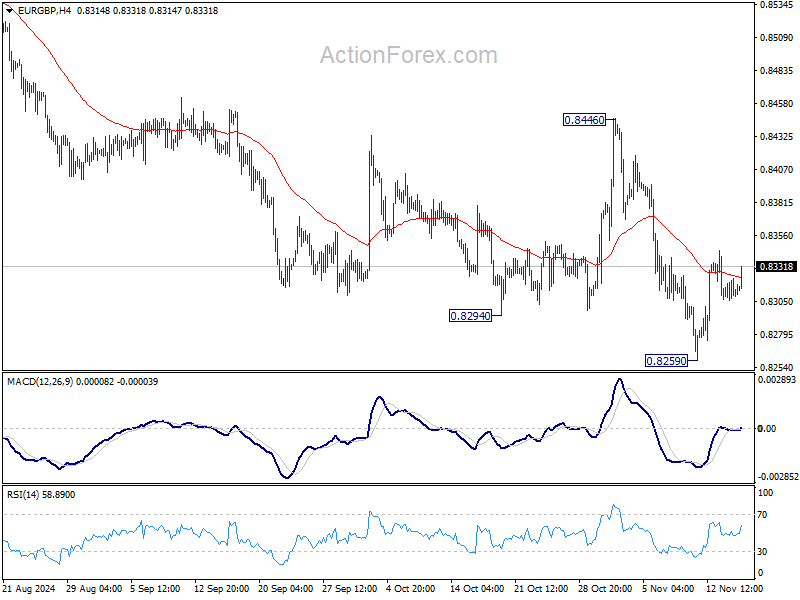

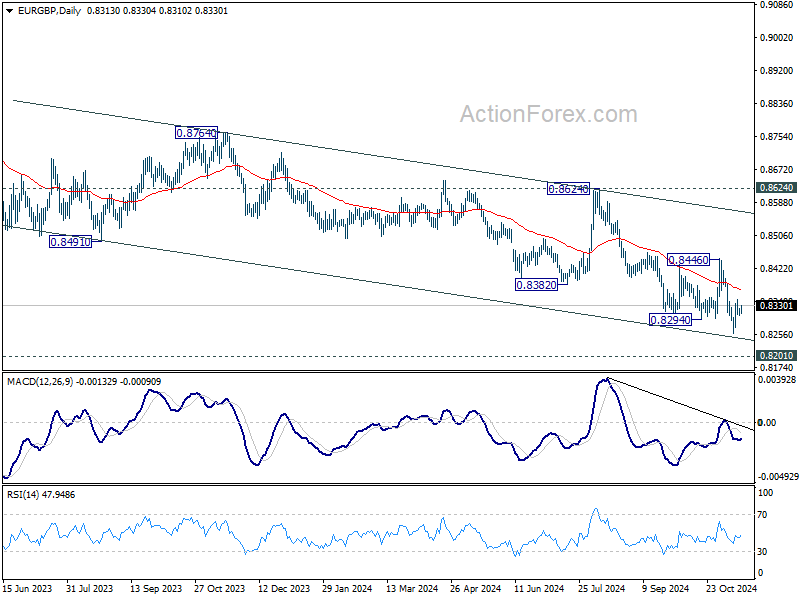

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8305; (P) 0.8315; (R1) 0.8322; More...

Intraday bias in EUR/GBP remains neutral for the moment. More consolidations could be seen above 0.8259 but further decline is expected as long as 0.8446 resistance holds. Break of 0.8259 will resume larger down trend to 0.8201 key support.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

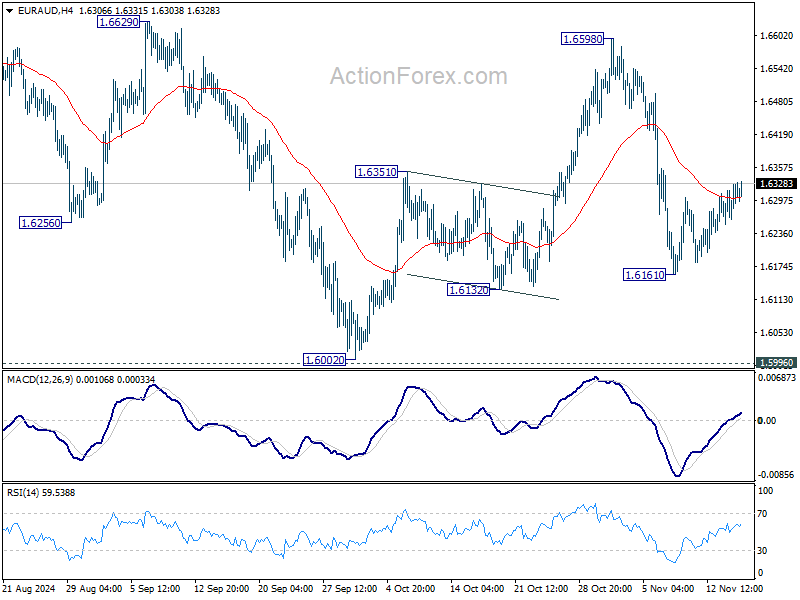

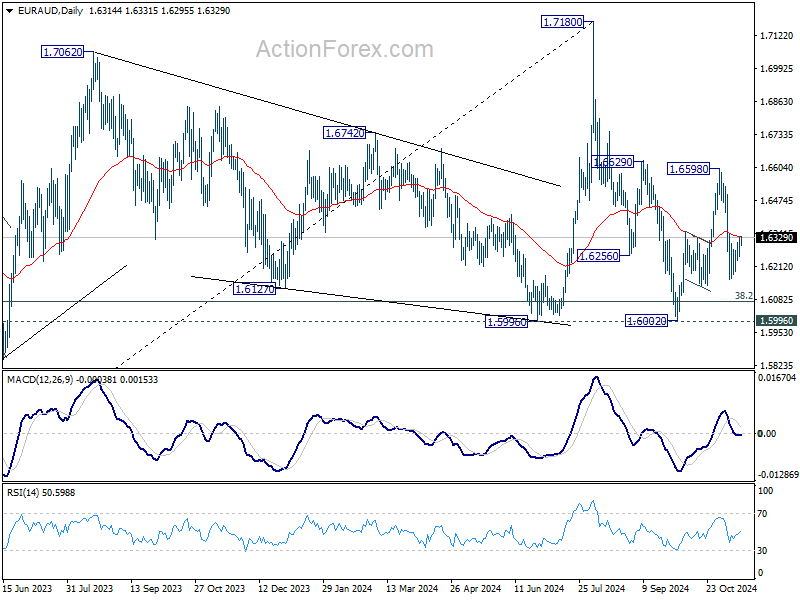

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6268; (P) 1.6299; (R1) 1.6345; More...

Intraday bias in EUR/AUD stays neutral as consolidations continues above 1.6161 temporary low. Risk will stay mildly on the downside as long as 1.6598 holds. On the downside, break of 1.6161 will resume the decline from 1.6590 to target a test on 1.5996/6002 key support zone.

In the bigger picture, as long as 1.5996 cluster support , up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.

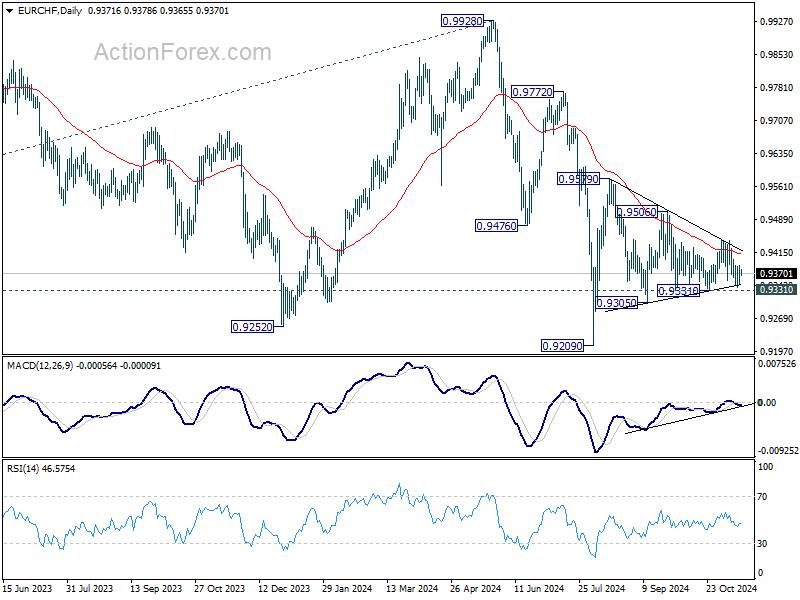

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9352; (P) 0.9370; (R1) 0.9395; More....

No change in EUR/CHF's outlook as range trading continues. Intraday bias bias stays neutral. On the downside, break of 0.9331 will target 0.9305 support first. Firm break there will bring retest of 0.9209 low. On the upside, break of 0.9444 will bring stronger rally to 0.9506 resistance next.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9419) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

EUR/USD Closed at New YTD Low

Markets

Markets tried to extend the Trump trade yesterday after higher US October producer price inflation and solid (low) weekly jobless claims. They sparked a reaction higher in the dollar and lower in US Treasuries. However those moves didn’t go far and even started a modest correction move on this month’s one-way traffic. Enter Fed Chair Powell. After European close he spoke on the economic outlook at a Dallas Fed event. He labelled the recent performance of the US economy as “remarkably good” in an echo to last week’s press conference following the Fed’s 25 bps rate cut. While he shied away from commenting on US politics, he did admit that the economy is not sending any signals that they need to be in a hurry to lower rates. These comments first of all indicate that the Fed embraces the recent market repricing on a landing zone for the policy rate next year (3.75%-4%; clearly above neutral). Secondly Powell seems to be closer to already pausing the interest rate cycle lower. While we stick to the view that we’ll see another 25 bps rate cut in December, it won’t take much to hold in January. US money markets are already contemplating the possibility of a skip at the final meeting of this year with a 25 bps rate cut only 60% discounted. Earlier on the day, dovish Fed governor Kugler said that the Fed must focus on both inflation and jobs goals. “If any risks arise that stall progress or reaccelerate inflation, it would be appropriate to pause our policy rate cuts,” she said. “But if the labor market slows down suddenly, it would be appropriate to continue to gradually reduce the policy rate.” Kugler’s comments seem to be skewing to the upside inflation risks (stubborn housing inflation and high inflation in certain goods and services) which obviously carries some weight given her more dovish status. Daily US yield changes eventually ranged between +5.9 bps (2-yr) and -4.9 bps (30-yr). This flattening move contrasts with the bull steepening in Europe where German yields shed 6.4 bps (5-yr) to 0.9 bps (30-yr). EUR/USD closed at a new YTD low (1.0530) after testing the 1.05 mark during the day. The range bottom and 2023 low stands at 1.0448. Today’s US retail sales have the potential to trigger a test if they showcase more strength. We think risks are becoming asymmetric though. If it weren’t for Powell’s intervention, the dollar and US Treasuries would have already corrected on the strong trend. It’s our preferred scenario going into the weekend.

News & Views

The Central Bank of Mexico yesterday cut its policy rate by 25 bps to 10.25%. Annual headline inflation rebounded to 4.76% in October while core inflation continued decreasing to 3.80% .The central bank forecasts headline and core inflation to converge to the 3% inflation target (with a tolerance band of +/- 1.0%) by the end of next year and stay there in 2026. Upside risks to this scenario remain. Looking ahead, the board expects that the inflationary environment will allow further reference rate adjustments, supported by expectations of ongoing weakness in the economy. The Mexican peso (MXN) since Q2 is on a downward trajectory against the dollar with recent political events in the US confirming this trend. USD/MXN currently trades at 20.48, compared to a low of 16.26 early April.

Japanese growth slowed from 0.5% Q/Q in Q2 to 0.2% Q/Q in Q3 (0.9% Q/Qa). The outcome was marginally stronger than expected (0.7% Q/Qa). The details show a mixed picture. Private consumption printed much stronger than expected at 0.9% Q/Q (from 0.7% in Q2 and 0.2% expected). On the negative side, capital spending was weak at -0.2% Q/Q (from 0.9% in Q2). Net exports also unexpectedly contributed negatively (-0.4%) to Q3 growth. In the previous quarter this negative contribution was only -0.1%. From a monetary policy point of view, the solid performance of domestic demand probably is the more important factor for the BOJ to gradually continue policy normalization. Recent weaking of the yen also points in the same direction. Markets are now looking forward to a speech and press conference of BOJ governor Ueda next Monday. Analysts currently are divided whether a next step should already take place in December or only come at the January meeting. USD/JPY tentatively extends its gain trading north of 156, to be compared to sub 140 levels mid-September.

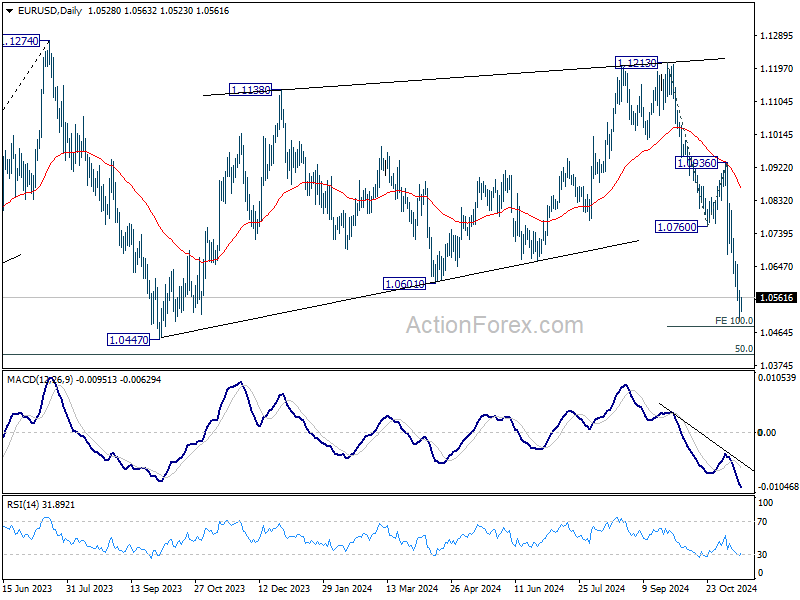

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0490; (P) 1.0536; (R1) 1.0576; More...

A temporary low is formed at 1.0495 in EUR/USD, just ahead of 100% projection of 1.1213 to 1.0760 from 1.0936 at 1.0483. Intraday bias is turned neutral for consolidations first. But outlook will remain bearish as long as 1.0760 support turned resistance holds. Firm break of 1.0495 will target 1.0404 key fibonacci level.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

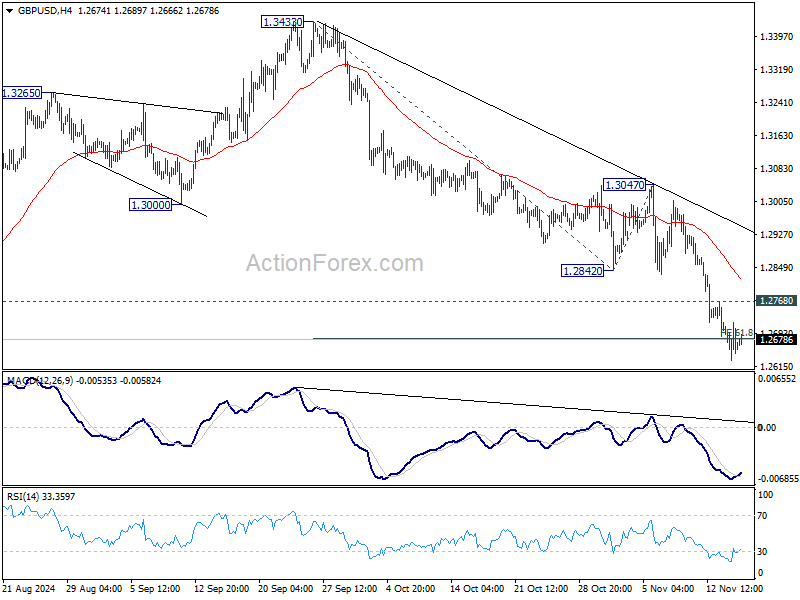

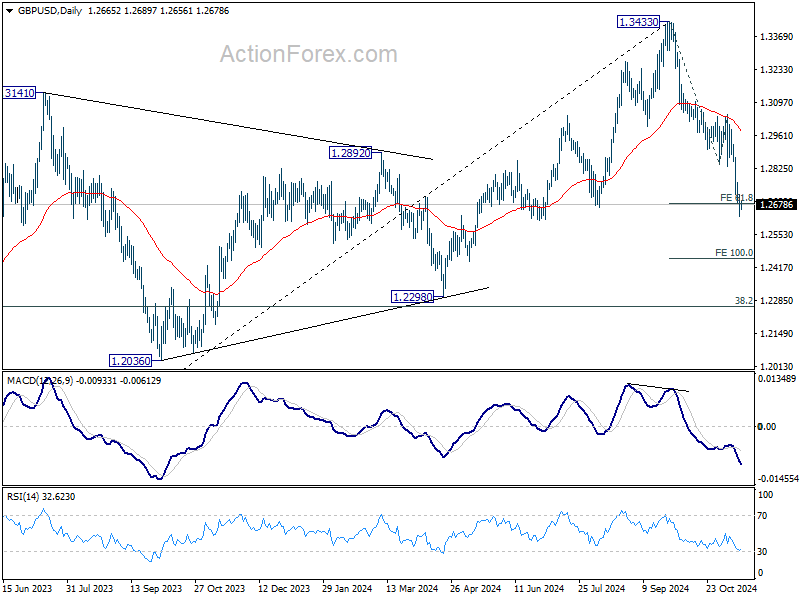

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2623; (P) 1.2674; (R1) 1.2719; More...

GBP/USD's fall from 1.3433 is still in progress and intraday bias stays on the downside. Next target is 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456. On the upside, above 1.2768 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 13047 resistance holds, in case of recovery.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

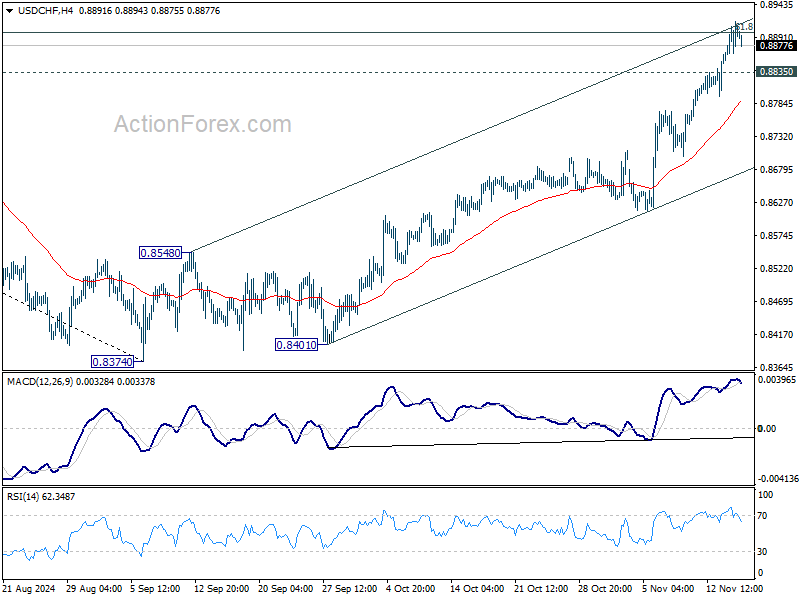

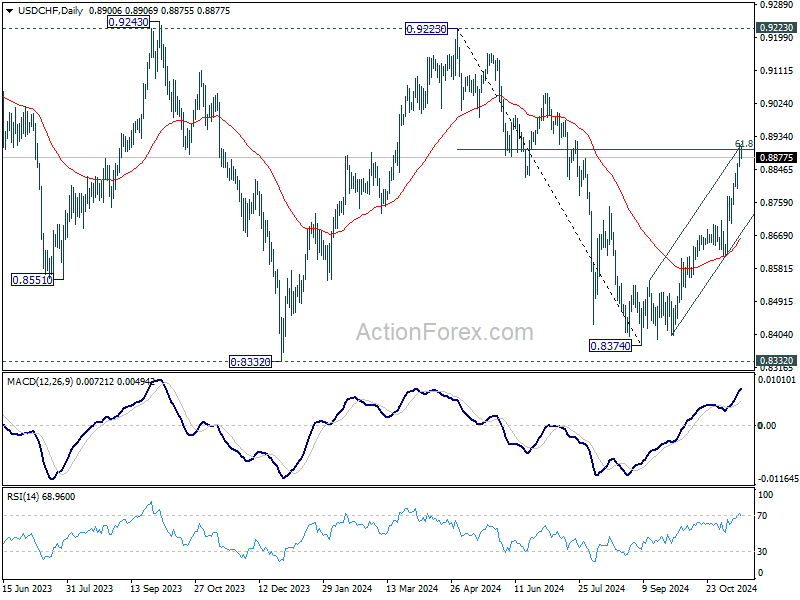

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8861; (P) 0.8890; (R1) 0.8932; More…

USD/CHF's rally is still in progress and intraday bias stays on the upside. Sustained break of 61.8% retracement of 0.9223 to 0.8374 at 0.8899 will pave the way to 0.9223 high. On the downside, below 0.8835 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

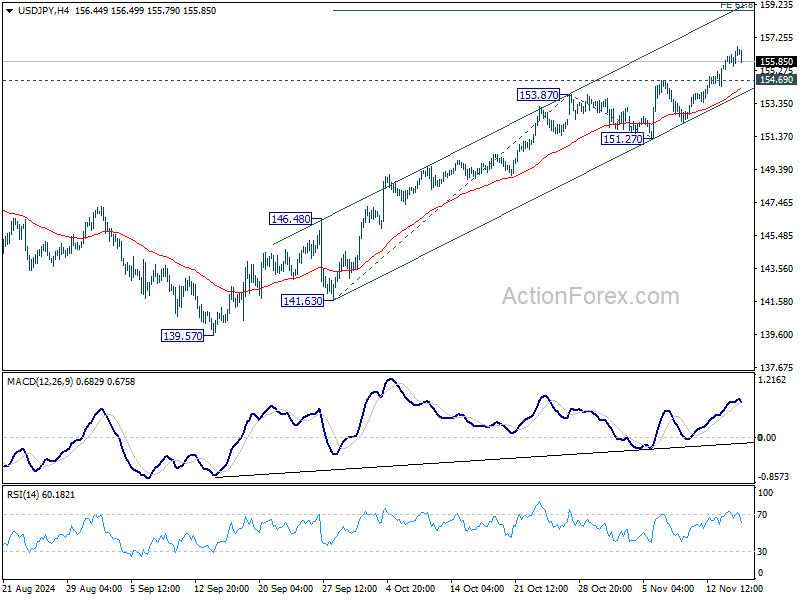

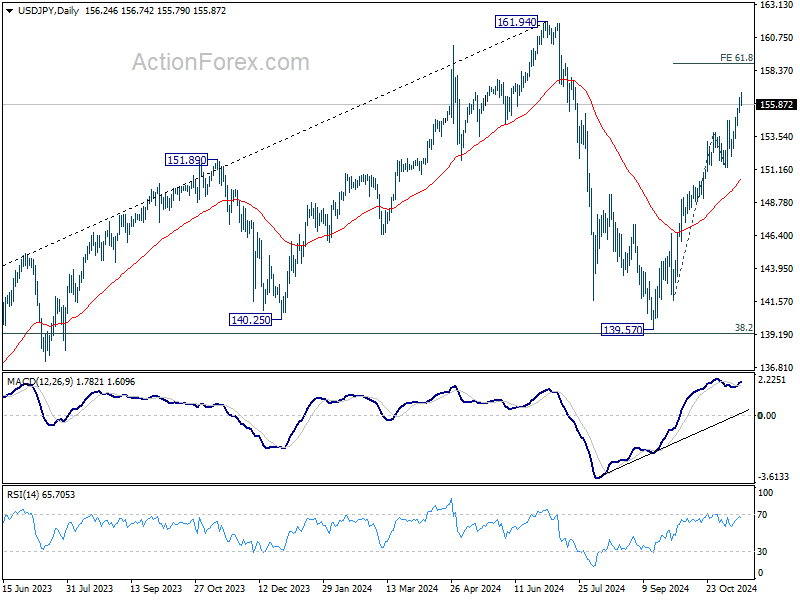

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.60; (P) 156.01; (R1) 156.68; More...

USD/JPY's rally is still in progress and intraday bias stays on the upside. Current rise from 139.57 should target 61.8% projection of 141.63 to 153.87 from 151.27 at 158.8. On the downside, below 153.40 minor support will turn intraday bias neutral again first. But near term outlook will remain bullish as long as 151.27 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

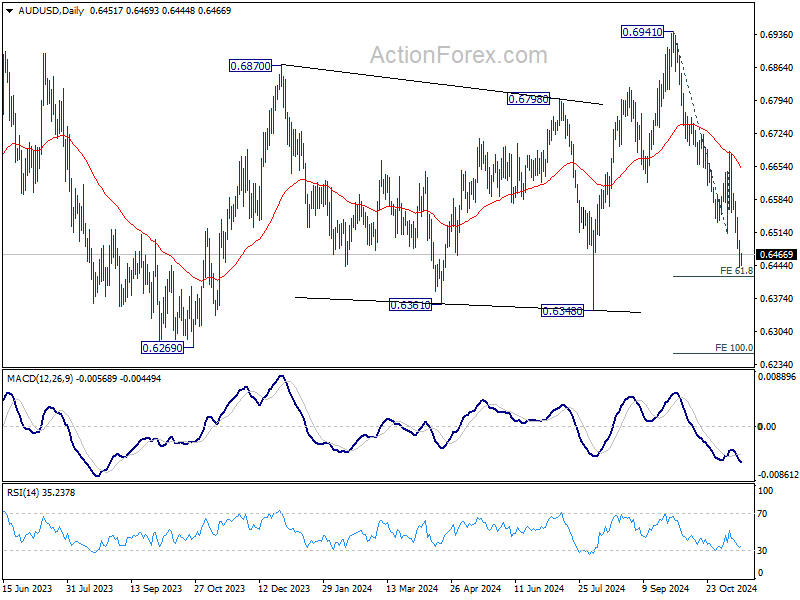

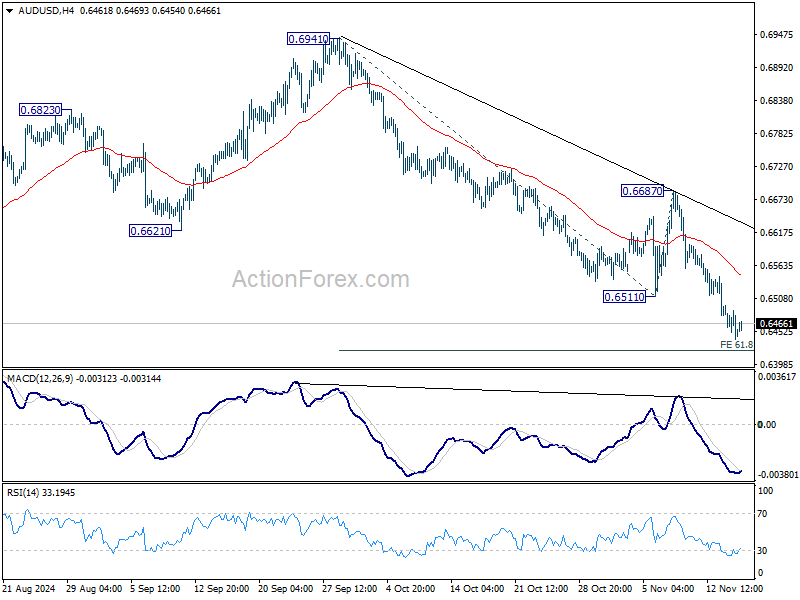

AUD/USD Daily Report

Daily Pivots: (S1) 0.6431; (P) 0.6465; (R1) 0.6488; More...

Intraday bias in AUD/USD remain son the downside for the moment. Current fall from 0.6941 should target 61.8% projection of 0.6941 to 0.6511 from 0.6687 at 0.6421. Firm break there will target 100% projection at 0.6257 next. On the upside, above 0.6511 support turned resistance will turn intraday bias neutral and bring consolidations first. But outlook will stay bearish as long as 0.6687 resistance holds, in case of recovery.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.