Sample Category Title

And Suddenly, Fed’s Urge to Cut Rates Evaporates

Federal Reserve’s (Fed) Jerome Powell, who leads a team that started cutting the interest rates with a 50bp point in September by fear that the US jobs market would deteriorate quickly and added another layer of 25bp cut last week, said that ‘the economy is not sending any signals that [they] need to be in hurry to lower the rates’. Maybe, the plans have changed after Trump’s election on rising inflation risks due to pro-growth policies and tariffs.

And beyond Trump, the inflation data released this week wasn’t that encouraging, either. The US headline inflation rebounded from 2.4% to 2.6% parallel to market expectations, while yesterday’s surprised to the upside, with both headline and PPI data printing figures above the market expectations. On top, the initial jobless claims came in lower than expected. All in all, the Fed is coming to the realization that cutting rates hurriedly was not a brilliant idea, and the first thing to do now is to do nothing in December. The probability of a December cut went from 60 to 80%, and is back to around 60% in the aftermath of this week’s data and comments. The US 2-year yield consolidates near 4.35%, the 10-year yield flirted with the 4.50% level, with treasury sceptics eyeing an easy advance to the 5% mark, and the US dollar extended gains to the highest levels in more than a year, supported by the hawkish shift in Fed expectations. The price action makes sense, but the fact that the US dollar has now stepped into the overbought territory will likely slow the short-term demand for the US dollar and could lead to a minor correction. But the price pullbacks should continue to be interesting dip-buying opportunities for the dollar bulls looking for a further extension of gains against majors.

The EURUSD tipped a toe below the chilly 1.05 level yesterday, on the back of a stronger dollar and a 2% decline in Eurozone’s industrial production, but rebounded to 1.0540, as the market hasn’t yet digested the idea that the EURUSD – which was testing the 1.10 offers 6 weeks ago – is now diving below the 1.05 mark. But once the information is digested, the move could materialize. There is a louder call for a 50bp cut in December from the European Central Bank (ECB), and some start talking about a 75bp cut – which I think is clearly not happening. But the Stoxx 600 saw support yesterday, partly thanks to more aggressive ECB rate cut expectations that support valuations and partly thanks to a nearly 3% jump in ASML after the company projected a sales growth between 50 and 100% - yes that’s the prediction range: 50 to 100% growth in sales.

Oil remains offered

Crude oil’s positive attempt yesterday remained short-lived, again, and the barrel of US crude is drilling below the $68pb at the time of writing, despite encouraging retail sales data from China. The USDCAD extends gains above the 1.40 mark and the USDJPY consolidates and extends gains above the 156 mark, with bears eyeing a further rise toward the 160 mark, where authorities would say stop to the bleeding with a direct intervention.

Meli-melo of other news

Disney jumped more than 6% yesterday on better than expected Q3 results, especially for its streaming business, but the rest of the market didn’t look as great. The S&P500, Nasdaq, Dow Jones and Russell 2000, they all fell yesterday on Powell saying – all of a sudden – that there is no need to hurry with the rate cuts. Tesla fell nearly 6% on news that Trump would eliminate the $7500 consumer tax credit for EV. But wait, because Tesla is already profitable, it is better positioned than the rest of the EVs to thrive.

The week will end with the UK GDP, a few more inflation numbers from the Eurozone and US retail sales and industrial production data. The incoming data could give an immediate reason to buy more dollars, or let the dollar soften to buy a dip. But in all cases, the outlook for the US dollar remains comfortably positive as the week comes to an end.

US Retail Sales and Industrial Production to Conclude the Week

In focus today

From the US, October retail sales and industrial production data will provide markets with the latest hard evidence of the health of the US consumer and manufacturing sectors. We expect that with still positive employment and solid wage gains, retail sales should remain on a steady growth path over the coming months.

In the euro area, the European Commission publishes its economic outlooks for 2025 and 2026. It will be interesting to follow their changes in projections as a signal of what we can expect from the ECB at their new projections in December, which will guide the monetary policy.

In Sweden, SCB publishes the October results from the Labor Force Surveys. While a further increase cannot be completely ruled out, we anticipate peak levels will be reached soon, and unemployment should start decreasing during next year. Importantly, the monthly unemployment figures should be assessed with caution due to their relatively high volatility.

Economic and market news

What happened overnight

In China, the monthly batch of data for October gave a mixed picture. Growth in retail sales exceed expectations at 4.8% y/y (cons: 3.8%, prior: 3.2%), reflecting how the country's recent stimulus efforts are kicking in. Conversely, industrial production and fixed asset investments fell short of expectations, printing 5.3% y/y and 3.4% y/y, respectively (cons: 5.6%, 3.5%). New home prices dipped 5.9% y/y, sliding the most in annual terms since October 2015. The monthly figure, however, fell 0.5% m/m, compared to the decline of 0.7% in September, signalling that stimulus measures are starting to support the fragile housing sector.

In Japan, GDP growth for Q3 matched consensus, growing a modest 0.2% q/q SA following the 0.7% rebound in Q2. Private consumption was stronger than expected, whereas capital spending and net external demand (exports minus imports) fell 0.2% q/q SA and 0.4% q/q SA, respectively. The decline in net external demand particularly stood out compared to consensus of 0.1% q/q SA growth.

What happened yesterday

In the US, yesterday's data releases had limited market impact. Akin to CPI on Wednesday, October PPI was very much as expected, increasing in October, with headline and core at 0.2% m/m SA and 0.3% m/m SA, respectively. While jobless claims edged slightly lower to 217k, the move was nothing too dramatic.

Fed Chair Powell stressed that the economy is not yielding any signals that the Fed should be in a hurry to slash rates. At the same time, Powell highlighted that the current sound economic backdrop gives the Fed time to approach their decisions carefully, hinting that the Fed likely will cut rates gradually, with inflation coming closer to the 2% target, "but not there yet". We pencil in a rate cut of 25bp cut in December.

In the euro area, industrial production declined by 2.0% m/m in September (cons: -1.4% m/m, prior: 1.5%). Given that the data is quite volatile on a monthly basis and this month was driven by a downtick in Ireland of 11%, we focus more on Q3 as an average. In Q3, industrial production declined 0.3% q/q, highlighting that industry remains weak, likely dragging on activity. The outlook for the coming quarters remains bleak and we do not expect a recovery in the sector before H2 2025 when interest rates likely have declined further.

Euro area employment continued to grow in Q3, increasing 0.2% q/q compared to a downward revised 0.1% in Q2, albeit when judged on the second decimal it was broadly unchanged (from 0.15% to 0.18%). Hence, the euro area labour market remains resilient. The employment situation is heterogeneous across euro area countries. The strength is due to continued increases in employment in Spain, while the picture in Germany is very different with employment declining in Q3. However, we see clear risks of the labour market weakening in the quarters ahead. We expect aggregate euro area employment growth around 0.0-0.1% q/q in the coming quarters as the EU Commission employment expectations index indicates continued mildly positive employment growth in Q4 and indicators of services demand remain positive. The outlook for the euro area is driven by our expectations for employment gains in Southern Europe countered by employment declines in Germany. We see risks as tilted towards the downside due to the weak manufacturing sector, as indicated by the weak wage agreement in German IG Metal for 2025.

Minutes from the ECB's October meeting indicated that risk management considerations were central to its decision to cut rates by 25bp to prevent unnecessary economic strain. Policymakers emphasised that the risks of cutting in October and potentially being too early in the easing cycle were lower than the risks of waiting and potentially acting too late. It was also highlighted that the ECB could pause its cutting cycle in December if activity improves. We believe that the ECB will deliver another 25bp cut in December, bringing the deposit rate to 3.00%.

In Sweden, the final inflation data for October was in line with last week's flash estimates. Decomposing details, the upside deviation seemed to be more broad-based than we had expected and not fueled by higher food prices. There were no worrying developments in the data, however.

Equities: Global equities were lower yesterday, albeit with significant regional variations. European stocks outperformed their US counterparts by approximately 2%, on a day when macroeconomic fundamentals did not provide any material reasons for this divergence. Additionally, the long end of the bond market was more or less moving in sync, and dollar continued to strengthen. In our opinion, this relative movement is a result of some reversal of the massive outperformance the US has demonstrated recently. Indeed, the US has displayed superior macroeconomic and microeconomic data, but not enough to justify the US outperformance we have seen. Hence, the Trump victory/trade has simply caused investors to flock to the US. This trend can be observed in both positioning and flow data, but the real alarm is sounded by relative valuation. Following the post-election movements, the US premium to Europe reached 65% based on a 12-month forward P/E ratio. To put it in perspective, when Trump was elected president back in 2016, the premium stood at 14%. With the movements in equities yesterday, individual stock performance, and for that matter, crypto currencies, it seems that we have put the largest part of the Trump trade behind us. Hence, going forward, both absolute and relative performance should again increasingly be driven by fundamentals. Some of the most extreme Trump trades are also prone to reversal.

In the US yesterday: Dow -0.5%, S&P 500 -0.6%, Nasdaq -0.6%, and Russell 2000 -1.4%.

Asian markets are quite varied this morning, though the major markets are leaning higher. European and US futures are lower.

FI: Global yields generally declined yesterday with the 10y point in Germany down about 8bp. Late in the evening, Powell's remarks on the Fed being in "no hurry to lower rates" spurred a sell-off in USD rates wit 2y treasuries rising 10bp to 4.35% and markets taking out 5bp of December Fed cut pricing. European markets are expected to see some spillover this morning.

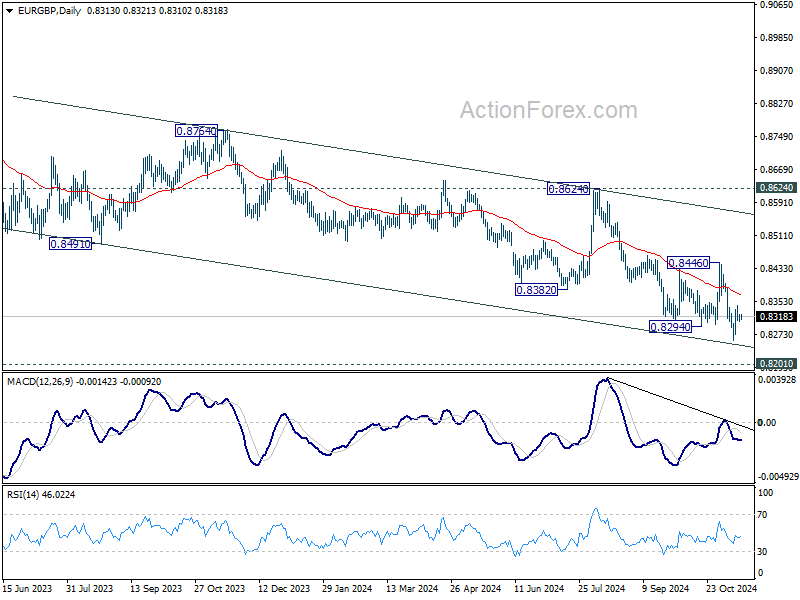

FX: Powell's remarks on the Fed being in "no hurry to lower rates" spurred a second wind for the USD during US hours where EUR/USD briefly touched below 1.05. Scandies recovered some of the previously lost ground vs the euro and NOK/SEK kept above 0.9850 throughout the session. USD/JPY continues to edge higher whereas EUR/GBP defied otherwise elevated G10-volatility and traded remarkably stable between 0.8310-0.8320.

UK GDP shrinks -0.1% mom in Sep; Q3 growth slows sharply to 0.1% qoq

UK economy contracted by -0.1% mom in September, falling short of market expectations for 0.2% mom growth. The contraction was driven largely by declines in manufacturing output and information and communication services, with monthly services output showing no growth. Meanwhile, production sector experienced a notable -0.5% drop, primarily due to a sharp decline in manufacturing. Construction output offered a slight silver lining, rising by 0.1%.

For Q3, GDP grew by a marginal 0.1% qoq, marking a steep slowdown from Q2’s 0.5% qoq growth and missing forecasts of 0.2% qoq. The services sector, which accounts for the largest share of economic activity, expanded by just 0.1%, while construction demonstrated resilience with a 0.8% increase. However, the production sector contracted by -0.2%, reflecting persistent weaknesses in the industrial base.

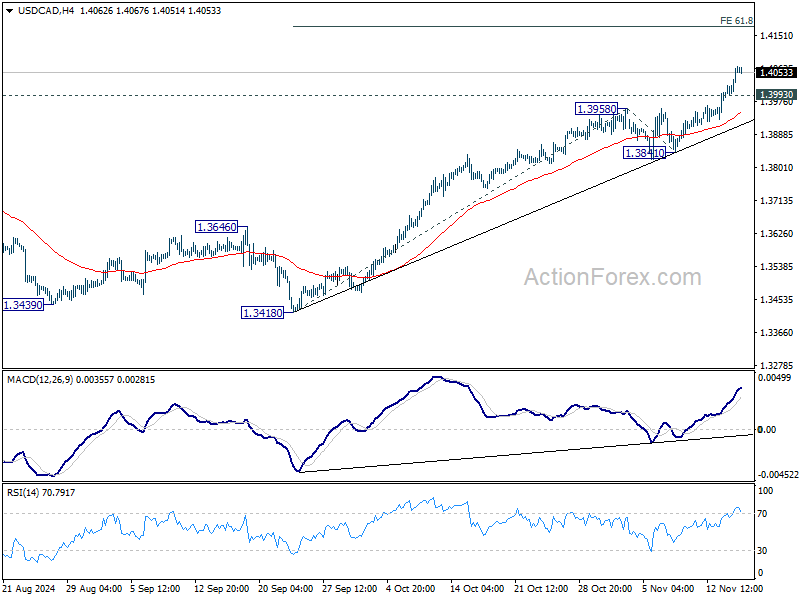

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4010; (P) 1.4038; (R1) 1.4087; More...

Intraday bias in USD/CAD remains on the upside for the moment. Current rally is part of the larger up trend. Next target is 61.8% projection of 1.3418 to 1.3958 from 1.3841 at 1.4175. On the downside, below 1.3993 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 1.3841 support holds, in case of retreat.

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

Forex Market Pauses Ahead of US Retail Sales, UK GDP

The forex market entered a phase of relative calm during Asian session today, with major currency pairs and crosses having limited movement. The Dollar softened slightly overnight with to retreat in US Treasury yields, but the losses have been minimal. The greenback found support from Fed Chair Jerome Powell's comments that Fed is not in a hurry to cut interest rates. Market are now turning attention to upcoming US retail sales data, which will provide insights into consumer demand and could influence inflationary pressure.

Despite the modest pullback, Dollar remains the clear leader in currency performance for the week. Canadian Dollar holds a distant second place . The Swiss Franc also ranks among the stronger currencies. In contrast, Japanese Ten continues to underperform as the week's worst performer. Political stability in Japan has not translated into currency strength. British pound is the second weakest, with investors awaiting UK's GDP. Australian and New Zealand Dollars are tied as the third weakest currencies while Euro sits in the middle of the performance spectrum.

Technically, EUR/GBP is now in an interesting spot. It's close to 0.8201 key long term support (2022 low). So even in case of another fall, downside potential might be limited. However, there is no clear buying momentum to push it through 0.8446 resistance to confirm short term bottom yet. Hence, in case of some volatility today, quick range trading strategy would be more appropriate.

In Asia, Nikkei rose 0.50%. Hong Kong HSI is up 0.37%. China Shanghai SSE is down -0.71%. Singapore Strait Times is up 0.12%. Japan 10-year JGB yield is up 0.0117 at 1.075. Overnight, DOW fell -0.47%. S&P 500 fell -0.60%. NASDAQ fell -0.64%. 10-year yield fell -0.033 to 4.418.

Fed’s Powell: Rate moving towards neutral, but no rush to cuts

Fed Chair Jerome Powell conveyed in a speech overnight that the central bank sees no immediate need to reduce interest rates quickly. He added that with an "appropriate recalibration" of monetary policy, Fed believes it can sustain economic growth and robust employment while guiding inflation back down to its 2% target in a sustainable manner.

He highlighted that the risks to achieving the Fed's employment and inflation objectives are "roughly in balance," and emphasized that policymakers remain "attentive to the risks to both sides."

Powell noted that Fed is gradually moving policy toward a "more neutral setting". However, he stressed that the path to reaching this neutral rate is "not preset.".

Importantly, Powell remarked that "the economy is not sending any signals that we need to be in a hurry to lower rates." The prevailing economic strength provides Fed with the ability to approach monetary decisions "carefully."

Japan's real GDP growth slows to 0.9% annualized, robust consumption but weak investment

Japan's economy expanded by 0.2% qoq in Q3 2024, aligning with market expectations but indicating a slowdown from the previous quarter's momentum. On an annualized basis, GDP grew by 0.9%, surpassing the anticipated 0.7%, yet decelerating from a downwardly revised 2.2% growth in Q2.

The second straight quarter of expansion was largely propelled by robust private consumption, which accounts for over half of the nation's GDP. Private consumption increased by 0.9% qoq, up from revised 0.7% in the prior quarter, driven by solid demand for automobiles and the influence of wage increases. Despite persistent high inflation, consumers are channeling funds into spending as a result of wage gains.

However, the economy faces challenges as capital investment declined by -0.2% qoq after previous growth, reflecting the impact of a global economic slowdown on sectors like chipmaking equipment. Exports inched up by 0.4% qoq, indicating some resilience in external demand. In contrast, imports surged by 2.1% qoq, which negatively affected GDP by subtracting 0.4 percentage points from growth.

China's industrial growth and investment lag, while retail sales outperform in Oct

China’s economic data for October showed a mixed performance, with retail sales surpassing expectations while industrial production and fixed asset investment slightly underperformed.

Industrial production grew by 5.3% yoy, just shy of the expected 5.4% yoy and holding steady from the prior month. Fixed asset investment also slowed, increasing by 3.4% ytd yoy compared to the forecasted 3.5%.

Real estate investment continued to struggle, declining by -10.3% from the previous year’s level over the January-October period, marking the sharpest annualized contraction since August 2021. This steeper drop reflects ongoing pressures in China’s real estate sector.

In contrast, retail sales surged 4.8% yoy, beating expectations of 3.8% yoy and accelerating from September’s 3.2% yoy. This stronger retail activity was largely driven by a week-long national holiday and an early start to the Singles' Day shopping festival, which boosted consumer spending.

NZ BNZ manufacturing falls to 45.8, further contraction but new orders show signs of recovery

New Zealand’s BusinessNZ Performance of Manufacturing Index dropped from 47.0 to 45.8 in, marking its lowest point since July and extending the sector's contraction for a 20th straight month. The reading underscores continued struggles in the manufacturing sector, despite recent RBNZ rate cuts.

A breakdown of the report reveals broad weakness across production and employment indicators, with production slipping from 47.9 to 44.5, and employment declining from 46.8 to 45.8. Deliveries also fell to 44.6 from 45.6, and finished stocks modestly increased to 47.4. However, new orders provided a rare bright spot, rising from 47.9 to 49.0, the highest level since May 2023.

Encouragingly, the proportion of negative comments from respondents fell to 53.5% in October, a marked improvement from the previous months, where negative sentiment had peaked at 76.3% in June.

BNZ’s Senior Economist Doug Steel noted, “Despite lower interest rates, the manufacturing sector continues to face significant headwinds. Recent business surveys show a sharp contrast between improved expectations for activity and weak current conditions.”

Looking ahead

UK will release GDP, production and trade balance in European session. Swiss will release PPI.

Later in the day, US retail sales will be the main focus. Empire state manufacturing, import prices, industrial production and business inventories will also be published. Canada will release manufacturing sales and wholesale sales.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4010; (P) 1.4038; (R1) 1.4087; More...

Intraday bias in USD/CAD remains on the upside for the moment. Current rally is part of the larger up trend. Next target is 61.8% projection of 1.3418 to 1.3958 from 1.3841 at 1.4175. On the downside, below 1.3993 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 1.3841 support holds, in case of retreat.

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

Cliff Notes: Burgeoning Confidence

Key insights from the week that was.

In Australia, the latest Westpac-MI Consumer Sentiment Survey provided another encouraging update on the health of the consumer. An impressive 11.8% rebound over the past two months has left the headline index at 94.6, the strongest reading in over two-and-a-half years and well within striking distance of a ‘neutral’ reading. Most of the improvement in sentiment has been centred on forward-looking measures, namely year-ahead views on the economy (+23% vs. Sep) and family finances (+7.3% vs. Sep).

While the sub-indexes tracking ‘family finances versus a year ago’ and ‘time to buy a major household item’ have seen some improvement, they both remain at historically weak levels – consistent with evidence from card activity data that points to a limited pick-up in spending following the introduction of the Stage 3 tax cuts. An added complication was the reaction to the US Presidential Election, which saw sentiment deteriorate notably over the course of the survey week – the net effect being greater-than-usual uncertainty about how the rapid recovery in confidence may evolve as the year draws to a close.

Consumers remain confident in the jobs outlook – unsurprising given the strong growth in employment evinced by the labour force survey. Coming off a multi-month above-trend performance, employment growth slowed in October, printing a modest gain of 15.9k. However, that was still enough to keep the employment-to-population ratio unchanged at a record high of 64.4% – a signal employment is still keeping pace with historic population growth. A marginal easing in labour force participation also left the unemployment rate at 4.1% for a third consecutive month. These results, together with little-change in average hours worked and other broader measures of labour underutilisation, imply the labour market remains in robust health, with slack building only at the margin. If sustained, this trend will see nominal wages growth continue to moderate through 2025, but enough momentum persist to deliver further modest real income gains. The outlook for wages, inflation and RBA policy was discussed at length this week by Westpac Chief Economist Luci Ellis.

Before moving offshore, the latest NAB business survey provided further confirmation of a stabilisation in business conditions, the index marking time at +7 points in October. This is consistent with our view that economic growth is current at or near its nadir, having slowed to 1.0%yr mid-year. With consumers having begun to receive their tax cuts and monetary policy easing around the corner, businesses are becoming more optimistic on the outlook, confidence up seven points to +5 in the month. Westpac sees GDP growth accelerating to 1.5%yr by year-end, then 2.4%yr by December 2025.

Globally, financial markets this week continued to assess the implications of a second Trump presidency, attempting to ascertain the President-elect’s priorities through appointment announcements for the incoming administration. The US dollar rallied and longer-dated Treasury yields meanwhile rose as a Republican majority, albeit a slim one, was confirmed for the House of Representatives, giving President Trump more freedom to implement his agenda, centred around lowering taxes, deregulation and reducing immigration.

As we discussed this week, while an extension of the household income tax cuts due to expire next year should be easily achievable, agreement on other tax changes might prove more difficult and/or time-intensive to achieve, with views on next steps for tax policy varied even amongst Republicans. Import tariffs, another critical piece of Trump’s agenda, should support an expansion of domestic manufacturing activity, but only gradually and not without negative effects on consumers, with the price of imported and local production to lift. Note as well there is a timing difference too: tariffs will impact inflation and spending long before investment in new domestic supply can be planned, built and commissioned. We expect these policies to have a meaningful and sustained effect in consumer inflation which the FOMC will have to respond to in late-2026 when we have two 25bp rate hikes forecast – for full detail see Westpac Economics’ Market Outlook November 2024.

Between now and late-2025, the current disinflationary trend is expected to persist however, allowing the FOMC to reduce the fed funds rate to 3.375% by September 2025, a rate we regard to be broadly neutral for the economy. This week, October’s CPI report again confirmed that inflation pressures are benign, 0.2%mth and 0.3%mth increases in headline and core prices in line with the prior month as well as market expectations. Shelter is now the one significant laggard for inflation, with annualised and annual growth near 5%. The FOMC continue to show little-to-no concern over this item however, given rental growth for current agreements is close to zero. As the shelter component of the CPI factors these results in, annual headline inflation will tend from 2.6%yr currently towards the FOMC’s medium-term target of 2.0%yr.

Turning to Asia, just released October activity data for China showed authorities shift towards pro-active support is paying dividends, but more so that additional stimulus is necessary. Retail sales surprised to the upside, the annual rate accelerating from 3.2%yr in September to 4.8%yr in October, although year-to-date the pickup was considerably more timid, from 3.3%ytd to 3.5%ytd. House prices also responded to authorities’ directives, new and existing home price declines slowing abruptly, from -0.7%mth and -0.9%mth in September to -0.5% in October. Growth in fixed asset investment and industrial production was little changed though, at 3.4%ytd and 5.8%ytd.

Late last Friday, China’s run of policy announcements continued, a debt swap package already mooted detailed to the market. CNY10trn in new special bond issuance will be made available through two programs over 3 and 5 years to local governments to refinance 'hidden debt' onto public balance sheets. The primary benefit is an expected CNY600bn reduction in interest payments over 5 years. The measures will also aid the bring forward of infrastructure spending into late-2024 and early-2025 and ready local governments to buy up housing assets and land from 2025, another initiative previously announced, and intended to provide lasting support to home prices and construction. Authorities clearly remain focused on strengthening the financial position of both the public and private sector, removing impediments to growth and encouraging new activity. But by refraining from announcing outright stimulus, they continue to disappoint the market and, potentially, are putting confidence amongst consumers and business at risk.

Note though, last Friday, Finance Minister Lan Fo'an reportedly promised "more forceful" fiscal stimulus next year and, while discussing today’s data the NBS spokesperson pledged to achieve 2024’s annual growth target of 5.0%. As such, outright stimulus is arguably a matter of time, the length of the waiting period likely to depend on the evolution of US trade policy and global economic uncertainty.

The Real Wage Overhang Hangover

Wages growth has peaked and started declining. At current rates, even quite low productivity growth would be compatible with inflation being sustained at target. So why is the RBA so worried?

The Wage Price Index increased 0.8% in the September quarter and 3.5% over the year. This was in line with our expectations but – as Westpac Economics Senior Economist Justin Smirk pointed out – slightly below consensus expectations. The extent of the step down in the year-ended growth rate was well anticipated, because it reflected the dropping out of the outsized 2023 National Wage Case and related decisions from the calculation.

The RBA does not publish a full quarterly wages forecast profile, only the forecasts for year-ended growth as at June and December quarters. So, we do not know exactly what they expected for the September quarter. However, it would now need to see a bounce back in quarterly growth to around 1% for the December quarter for its end-2024 forecast to come true. Even allowing for some recent health-care agreements, we consider such a bounce to be beyond the bounds of plausibility given how smooth this series tends to be. There are no strong reasons for a change of direction of this kind, either. Surveys, data on awards and enterprise agreements and feedback from our own customers would all suggest that a sudden bounce back in wages growth is not happening.

We therefore expect that the RBA will have to revise down its near-term wages growth forecasts again in February, having already done so in November.

Forecasting is hard, so some revisions and near-term misses are par for the course. Even so, is there something going on with the way some observers think about domestic labour costs, that could be affecting their interpretation of the economic outlook? And in the case of the RBA, could this be affecting its monetary policy decision-making?

Some insights can be gleaned from the following passage from the latest Statement on Monetary Policy:

At current rates of productivity growth, WPI growth remains somewhat above rates that can be sustained in the long term without putting upward pressure on inflation. All else equal, when productivity growth is positive, WPI growth is able to outpace inflation while still being consistent with inflation at the midpoint of the target range. As trend growth in labour productivity is likely below its rate in previous decades, the sustainable WPI growth rate is probably lower than in the past and below the current rate of growth. That suggests it would be difficult to sustain wages growth at its current pace in the longer term without a higher pace of trend productivity growth.

There are a few things worth noting about this passage.

First, this reasoning comes from the markup model for forecasting inflation. As explained in a previous note, this model starts from the presumption that prices are a (roughly stable) markup over costs, including labour costs. A bit of algebra later leads to a relationship that states that wages growth minus productivity growth is approximately equal to inflation (prices growth). As discussed in that previous note, there are a lot of assumptions underlying the use of this relationship for forecasting. But more fundamentally, the WPI is not the measure of labour cost growth that maps most closely to the one implied in that relationship. Rather, the more volatile average earnings measures from the national accounts are more relevant.

Presumably the RBA has used the smoother WPI measure for ease of exposition. In that case, though, one should be even more circumspect about how tightly the relationship should hold.

Second, there are some interesting implied choices of time period used in that paragraph. For example, it is stated that future trend productivity growth is expected to be slower than the average of previous decades. This is not controversial: the late 1990s was a period of strong productivity growth globally, largely because of the adoption of personal computers and other new technologies. More recent productivity growth was slower, but not zero. The real question is whether future productivity growth will be slower than the average of more recent times, such as the years leading up to the pandemic. Perhaps this is true, but the reasons for a further slowdown have not been elucidated. While any boost from AI and other technology will indeed take time to show up in the productivity figures, just as PCs did, a further decline in global trend productivity growth is not the base case for the profession more broadly.

Third, even granting the reduced noise from using the WPI, and assuming a further slowdown in global productivity, there is the question of why the RBA repeatedly referenced the sustainability of the current rate of growth. At the time of publication, this was the year to the June quarter figure of 4.1%, not the year to September quarter figure of 3.5% just reported. Yet the RBA surely anticipated the step down in growth that was already baked in to awards and many enterprise agreements. Why the focus on the sustainability of a growth rate that everyone knew was not going to be sustained? The question also arises of how we reconcile wages growth having already rolled over, to annualised rates in the low 3s, with the RBA’s view that the labour market is still tight.

Later in the document, the step down in unit labour cost growth from 7% annualised to 3½% annualised in just six months was noted (as we had previously expected and written about). So why the implication that growth in labour costs was much stickier than that?

The deeper question is: with wages growth tracking in the low 3s and productivity growth not being zero, why has the RBA focused so much on the risk that wages growth is unsustainable?

I can’t help thinking that this partly reflects deep-seated narratives about the Australian economy not being competitive. These narratives stemmed from the so-called ‘real wage overhang’ that emerged in the 1970s following the policy-induced wages breakout then. Another bout of this belief system emerged after the mining boom and attendant strong income growth. Since then, restoring competitiveness by crimping wages growth has been a common go-to in the policy discourse in Australia, far more than elsewhere in my observation. It is as if people forget that exchange rates tend to move much faster than domestic labour costs.

In any case, even if productivity growth averages a touch lower than 1% (worse than recent history), then by the RBA’s own figuring, WPI growth averaging 3.2% (the annualised rate of the past three quarters) is well and truly consistent with inflation averaging 2½% or below. Perhaps we need to let go of the pandemic-era hangover.

China’s industrial growth and investment lag, while retail sales outperform in Oct

China’s economic data for October showed a mixed performance, with retail sales surpassing expectations while industrial production and fixed asset investment slightly underperformed.

Industrial production grew by 5.3% yoy, just shy of the expected 5.4% yoy and holding steady from the prior month. Fixed asset investment also slowed, increasing by 3.4% ytd yoy compared to the forecasted 3.5%.

Real estate investment continued to struggle, declining by -10.3% from the previous year’s level over the January-October period, marking the sharpest annualized contraction since August 2021. This steeper drop reflects ongoing pressures in China’s real estate sector.

In contrast, retail sales surged 4.8% yoy, beating expectations of 3.8% yoy and accelerating from September’s 3.2% yoy. This stronger retail activity was largely driven by a week-long national holiday and an early start to the Singles' Day shopping festival, which boosted consumer spending.

Japan’s real GDP growth slows to 0.9% annualized, robust consumption but weak investment

Japan's economy expanded by 0.2% qoq in Q3 2024, aligning with market expectations but indicating a slowdown from the previous quarter's momentum. On an annualized basis, GDP grew by 0.9%, surpassing the anticipated 0.7%, yet decelerating from a downwardly revised 2.2% growth in Q2.

The second straight quarter of expansion was largely propelled by robust private consumption, which accounts for over half of the nation's GDP. Private consumption increased by 0.9% qoq, up from revised 0.7% in the prior quarter, driven by solid demand for automobiles and the influence of wage increases. Despite persistent high inflation, consumers are channeling funds into spending as a result of wage gains.

However, the economy faces challenges as capital investment declined by -0.2% qoq after previous growth, reflecting the impact of a global economic slowdown on sectors like chipmaking equipment. Exports inched up by 0.4% qoq, indicating some resilience in external demand. In contrast, imports surged by 2.1% qoq, which negatively affected GDP by subtracting 0.4 percentage points from growth.

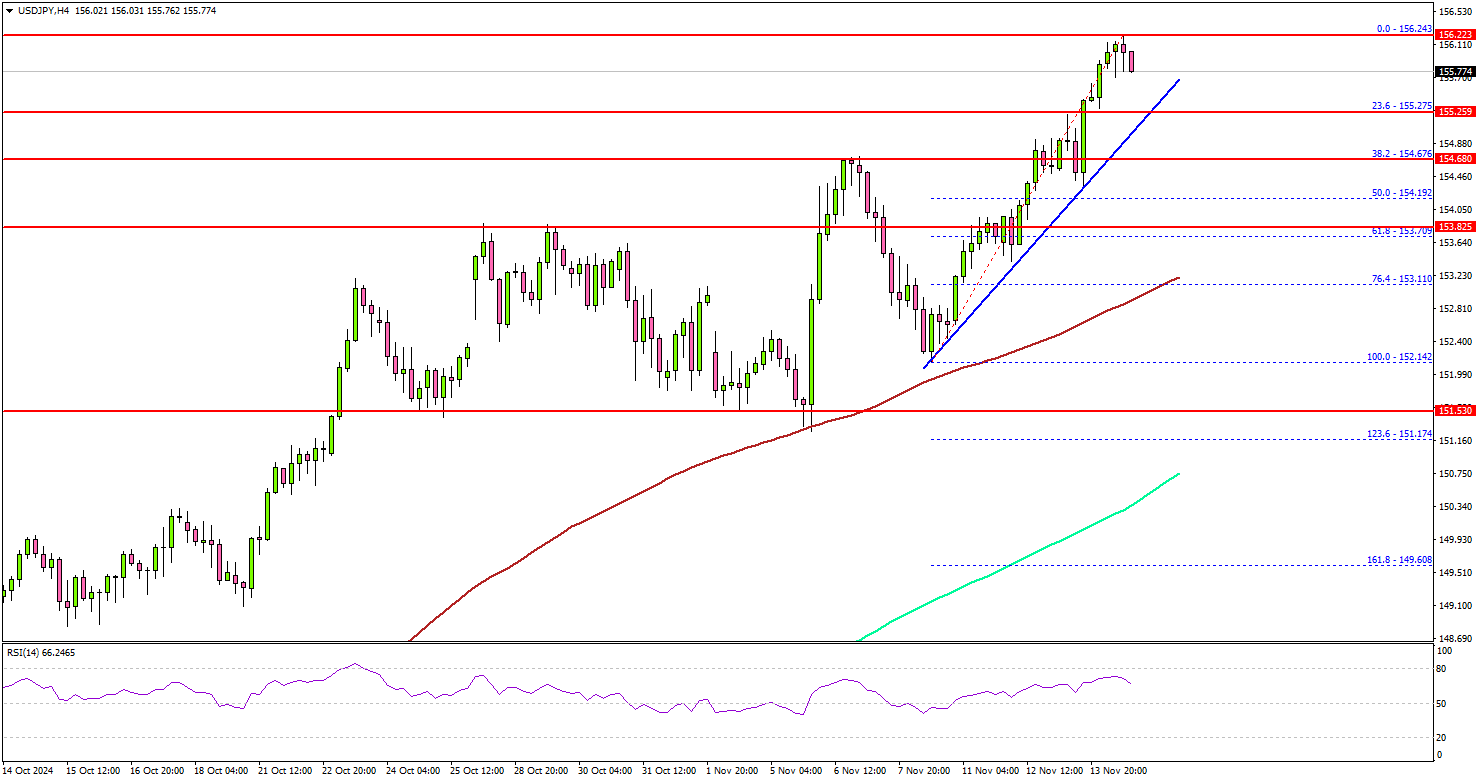

USD/JPY Extends Gains: Is More Upside Ahead?

Key Highlights

- USD/JPY started another increase above the 154.65 resistance.

- A key bullish trend line is forming with support at 155.25 on the 4-hour chart.

- Gold extended losses and traded below the $2,600 support.

- Oil is consolidating and facing hurdles near the $70.00 resistance.

USD/JPY Technical Analysis

The US Dollar started a fresh increase from the 152.35 zone against the Japanese Yen. USD/JPY cleared the 153.50 and 154.50 resistance levels to move into a positive zone.

Looking at the 4-hour chart, the pair settled above the 155.65 barrier, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). There was also a move above the 156.00 level.

The pair is now showing signs of strength and might continue to rise above 156.25. On the upside, the pair could face resistance near the 156.85 level.

The first key resistance is near the 157.50 level. A close above the 157.50 level could set the tone for another increase. The next major resistance could be 158.80, above which the price could accelerate higher toward the 160.00 resistance.

On the downside, immediate support sits near the 155.25 level. There is also a key bullish trend line forming with support at 155.25 on the same chart.

The next key support sits near the 154.65 level. Any more losses could send the pair toward the 153.80 level or even 152.50 in the near term.

Looking at Gold, the bears gained strength, and they were able to push the price below the $2,620 and $2,600 support levels.

Upcoming Economic Events:

- US Retail Sales for Oct 2024 (MoM) – Forecast +0.3%, versus +0.4% previous.

- NY Empire State Manufacturing Index for Nov 2024 – Forecast -0.7, versus -11.9 previous.