Sample Category Title

European Commission forecasts modest recovery and faster disinflation for Eurozone

The European Commission maintains its projection for Eurozone GDP growth at 0.8% in 2024, unchanged from its Spring forecast. However, it has slightly downgraded the 2025 growth projection to 1.3% from the previous 1.4% in Spring forecast, introducing a new projection of 1.6% growth in 2026. For the EU as a whole, GDP is expected to grow by 0.9% in 2024, 1.5% in 2025, and 1.6% in 2026.

Inflation is anticipated to decline significantly. In Eurozone, headline inflation is projected to more than halve from 5.4% in 2023 to 2.4% in 2024, slightly lower than the previous estimate of 2.5%. It is expected to ease further to 2.1% in 2025 and 1.9% in 2026. The EU is forecasted to see an even sharper disinflation, with headline inflation falling from 6.4% in 2023 to 2.6% in 2024, continuing to decrease to 2.4% in 2025 and 2.0% in 2026.

Executive Vice-President Valdis Dombrovskis highlighted that the EU economy is steadily recovering, with growth expected to gain momentum next year. Factors contributing to this acceleration include rising consumption driven by increased purchasing power, sustained record-low unemployment, and anticipated improvements in investment levels.

European Commissioner for Economy Paolo Gentiloni noted that as inflation continues to ease and private consumption and investment growth pick up, supported by unemployment at record lows, growth is set to gradually accelerate over the next two years.

WTI Oil: Will It Break or Bounce?

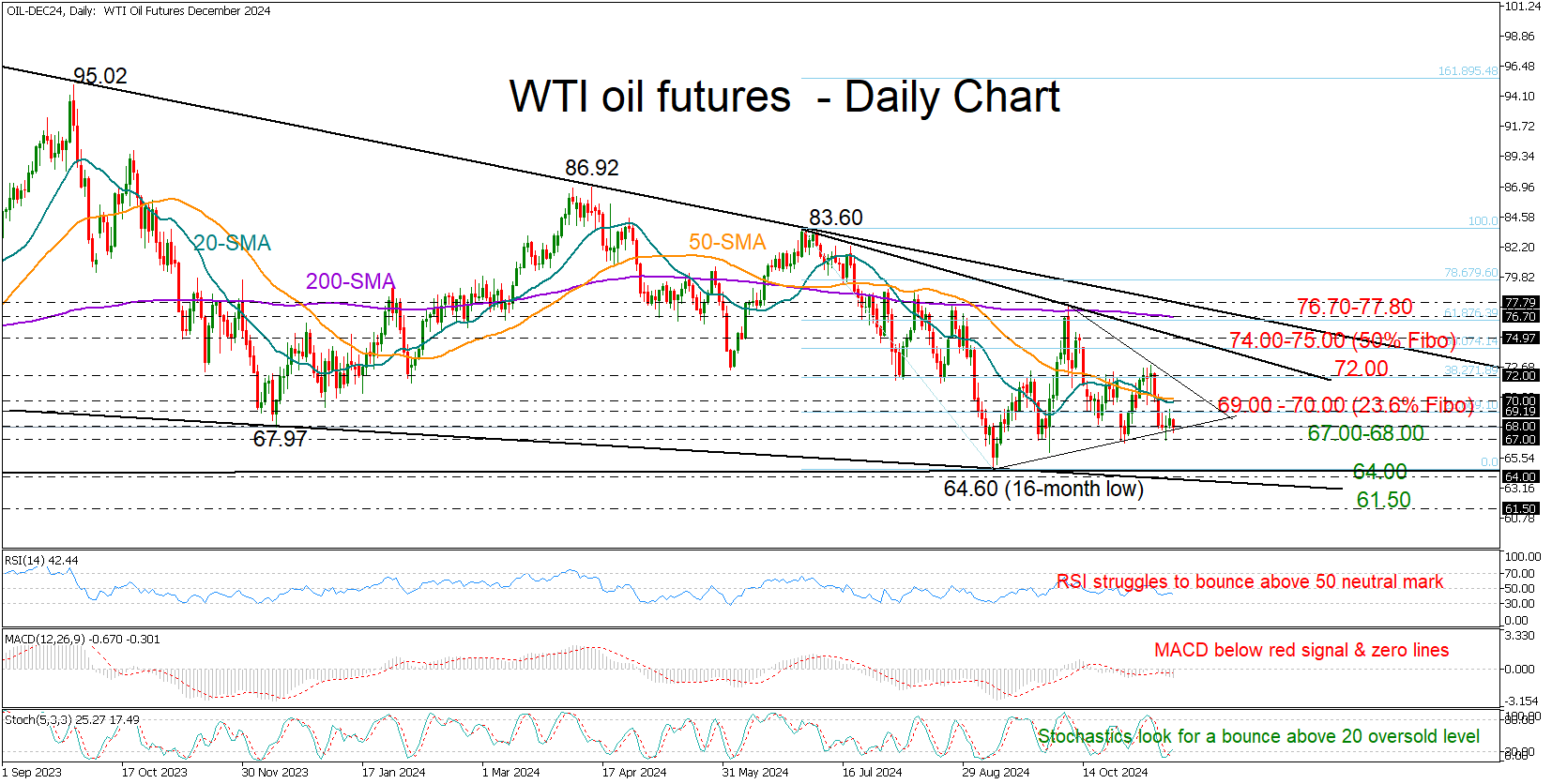

- WTI oil futures continue to flatline near a critical support area

- Bullish trend reversal is a long way above 77.80

WTI oil futures kept their footing above the 67.00-68.00 support region for the third time since the current sideways trajectory began in September. This base has been a strong source of buying in 2021 and 2023 too. Hence, as long as it holds, there’s hope for a bounce back.

But excluding the recent green bullish doji candlestick and the oversold signals coming from the Stochastic oscillator, there are barely any signs of buying enthusiasm. The simple moving averages (SMAs) are still pointing down, and both the RSI and MACD are hovering in the bearish zone, showing that downward pressure is still very much in play.

If the 67.00 floor collapses, the price may seek shelter near the important 64.00 zone, which triggered September’s bounce and helped the bulls twice in 2023. If that doesn’t hold either, we could see a retest of the 2021 base at 61.50. Another failure there could make things get ugly fast, shifting the spotlight straight to the 56.40-57.30 area.

In the event the price crawls above the 69.00-70.00 range and breaks through the 20- and 50-day SMAs, the 72.00 area could block any increases toward the 74.00-75.00 region. A continuation higher could bode well for the market, though for the short-term picture to start looking bullish again the price must close decisively above the 200-day SMA and then rise sustainably above the 2023 resistance trendline at 77.80.

In short, WTI oil futures are at a critical crossroads at the moment. A slip below 67.00 could spell trouble, while a move above 77.80 could upgrade the outlook back to bullish.

Brent Crude Oil Analysis: Bulls Hold the Line at Key Support

The XBR/USD chart reveals that Brent crude oil is trading near its lowest levels of the year.

Several factors are pressuring oil prices:

→ China's uncertain demand outlook: As the world's largest crude oil importer, any signs of weakening demand weigh heavily on the market.

→ A strengthening US dollar: Since Brent is priced in USD, a stronger dollar makes oil more expensive for international buyers, dampening demand.

→ Trump's promises to halt wars, including in the Middle East: This reduces geopolitical risk, which traditionally acts as a bullish factor for oil prices.

Technical Analysis of XBR/USD

From a technical perspective, bears appear to maintain control as a key trendline has shifted from acting as support to resistance (as indicated by the arrows on the chart).

Currently, the price oscillates around this trendline, which serves as the median of a channel marked by blue boundaries:

→ The upper boundary has been tested only once.

→ The lower boundary is under consistent pressure. Bulls, however, have managed to keep the price above the psychological $70.00 level.

How long can demand forces sustain Brent above $70? A fresh bearish breakout below this level could occur, testing whether buyers can prevent the market from extending its downtrend, which has persisted since April 2024.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Aussie Stabilizes, China Retail Sales Rise

The Australian dollar is steady after a five-day slide, which saw the currency fall by 3.5% during that period. In the European session, AUD/USD is trading at 0.6471, up 0.28% on the day.

China retail sales beats expectations

China retail sales, a key indicator of domestic consumption, jumped 4.8% y/y in October, up sharply from 3.2% in September and above the market estimate of 3.8%. This was the fastest pace of growth since February. Retail sales received a boost from a week-long holiday an significant government stimulus measures in September to boost the struggling economy. This included a cut in interest rates and easing restrictions on borrowing for purchases of stocks and houses. These measures are unlikely to be sufficient to turn the economy around, and Bejing is under pressure to take further moves, such as additional monetary easing.

Good news in China is music to the ears of Australian exporters, as China is Australia’s largest trading partner. If Chinese demand for Australian goods increases, it should boost the Australian dollar, which has been hammered by the US dollar and has plunged 6.4% since October 1.

The Reserve Bank of Australia has held its cash rate for 4.35% for eight straight meetings and has become an outlier among the major central banks, most of which have cut rates in response to lower inflation. The RBA is under pressure to cut rates as inflation fell in the third quarter to 2.8%, down from 3.8% in Q2, its lowest rate since the first quarter of 2021.

The RBA noted at its November meeting that headline inflation has declined considerably but that underlying inflation remains too high. The RBA holds its final meeting of the year on Dec. 10 and is widely expected to maintain rates. If inflation continues to fall, we can expect a rate cut early in 2025.

The US dollar has looked sharp this week against the major currencies and could add to its gains if today’s retail sales report beats expectations. The markets expect October retail sales to rise to 1.9% y/y, up from 1.7% in September. Monthly, retail sales are expected to inch lower to 0.4% from 0.3%.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6465. The next resistance line is 0.6488

- 0.6431 and 0.6408 are the next support levels

EURUSD Faces Decline as Fed Signals Firm Stance

EURUSD plunged to a six-month low of 1.0543 on Friday amid strong support for the US dollar following the US presidential election and recent comments from Federal Reserve officials.

Federal Reserve Chair Jerome Powell's recent statement underscored a cautious approach to cutting interest rates, citing persistent GDP growth, robust employment, and ongoing inflationary pressures. This stance suggests a possible delay or reduction in the anticipated rate cuts, contrasting with earlier market expectations favouring a rate reduction in December.

As Powell indicated a less accommodative monetary policy moving forward, the probability of a December rate cut has notably decreased, bolstering the US dollar's appeal.

Technical analysis of EURUSD

H4 chart analysis: the EURUSD price has reached the 1.0500 level, forming what appears to be the latter half of a downward trend. Today, we expect consolidation range formation above this level. If the price breaks upwards, a corrective wave towards 1.0600 could occur. Subsequently, we expect the continuation of the downward impulse to the 1.0404 level. This bearish EURUSD outlook is supported by the MACD indicator, which remains below zero and is directed downwards.

H1 chart analysis: EURUSD is making a downward move towards 1.0404. After achieving this target, a corrective upward movement towards 1.0600 is possible, suggesting a temporary pause in the bearish trend. The Stochastic oscillator supporting this scenario is close to 80 and signals an imminent fall to 20, in line with the expected continuation of the downward movement.

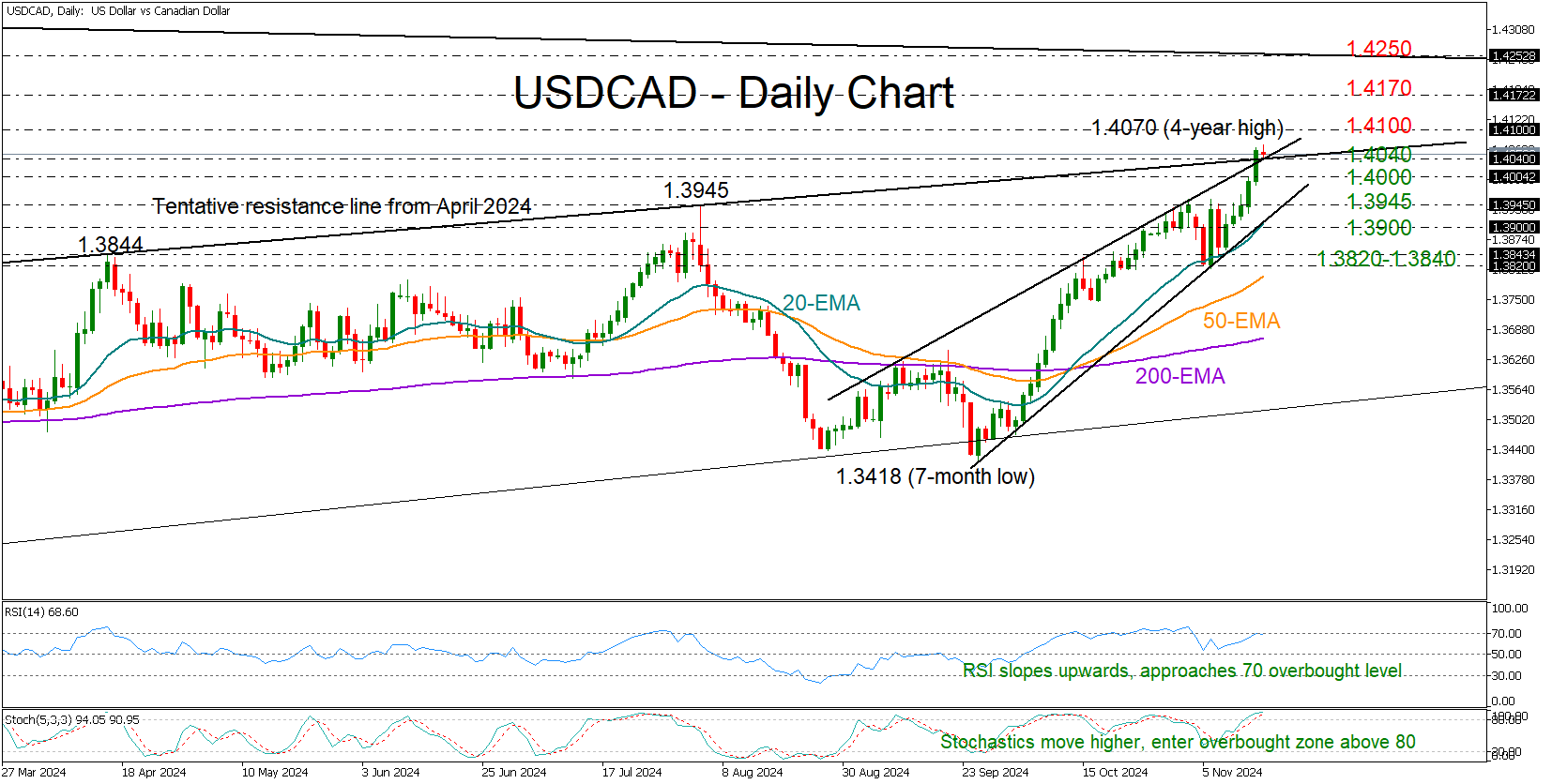

USDCAD: What’s Next After a Four-Year High?

- USDCAD snaps long-term range above 1.4000

- Bulls may take a breather; overall outlook remains bullish

USDCAD enjoyed a lovely session on Thursday, and it even found fresh buying interest to tick to a new four-year high of 1.4070 on Friday after a four-day nonstop rally.

Technically, the pair broke through the trendline resistance zone around 1.4040, now acting as support, sparking renewed optimism that a new bullish cycle is underway. However, some consolidation could be on the horizon as both the RSI and stochastic indicators hover in overbought territory, signaling the current bull run may be overstretched.

Looking to the upside, the psychological 1.4100 level is the next hurdle, followed by the 1.4170 mark from May 2020. If the bulls maintain momentum, it would be interesting to see if they can successfully breach the tentative resistance line at 1.4250, which connects the 2002 and 2020 highs.

On the flip side, if the price slides below 1.4040, support could immediately emerge around the 1.4000 round level. The former resistance of 1.3945 and the 2022 high of 1.3976 could provide the next line of defense, while a break below the 20-day exponential moving average (EMA) and the 1.3900 number could send stronger bearish signals, threatening a deeper pullback to the 1.3820-1.3840 support region.

Overall, the pair has exited its two-year consolidation phase, suggesting the start of a new bullish cycle. That said, a brief pause or pullback is possible before the next leg higher.

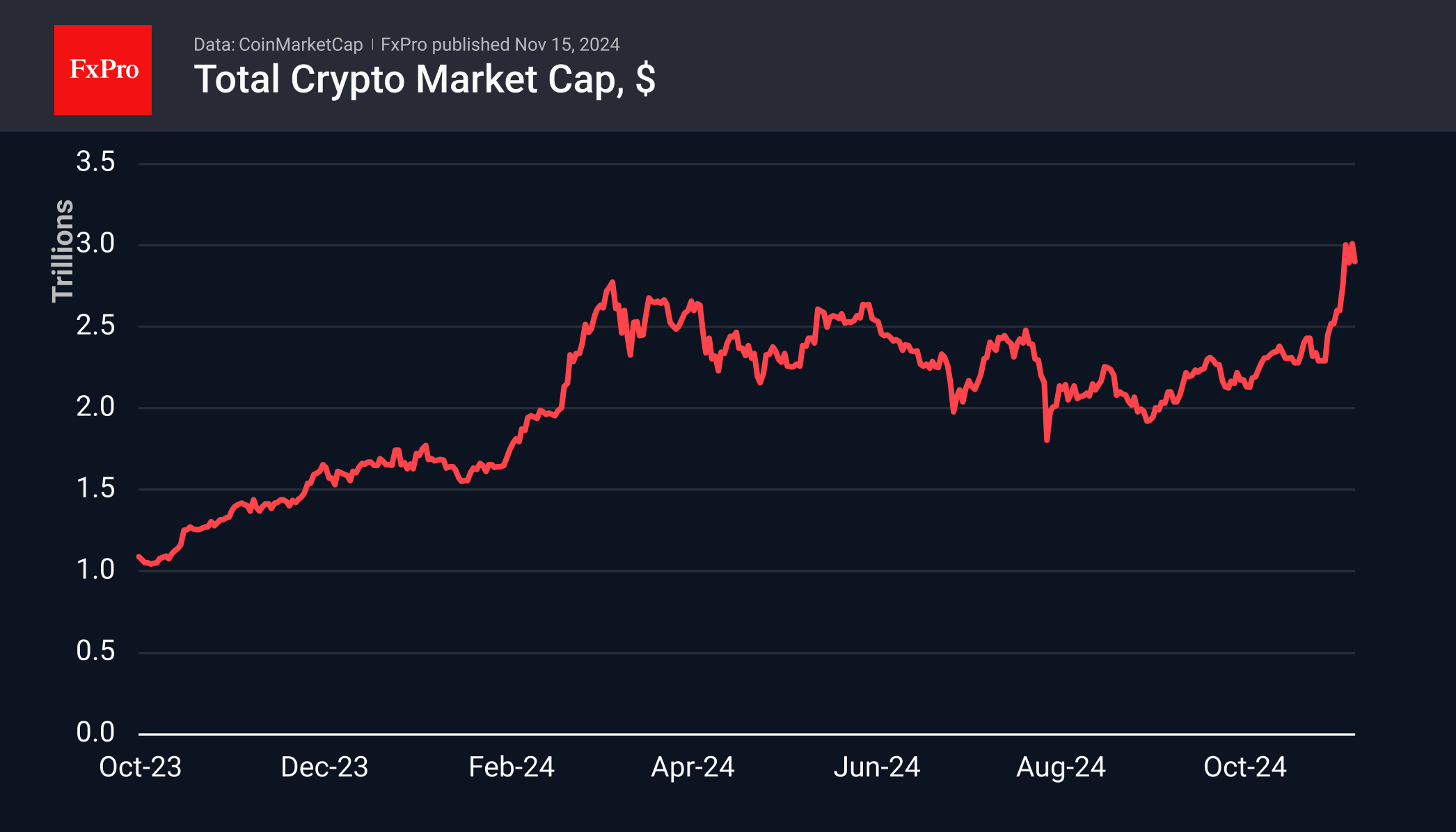

The Third Day of Crypto Cooling Off

Market Picture

The cryptocurrency market continues to cool for the third day in a row, falling 1.7% in the last 24 hours to $2.92 trillion. This is a retest of the lower end of a range that is seeing serious position shake-offs. This dynamic is also in line with the general risk-off sentiment that has prevailed in the markets this week. By the end of the week, we cannot rule out a deeper correction to the overall level of $2.73 trillion, which is the 61.8% level of the last growth impulse and the consolidation area of 10-11 November.

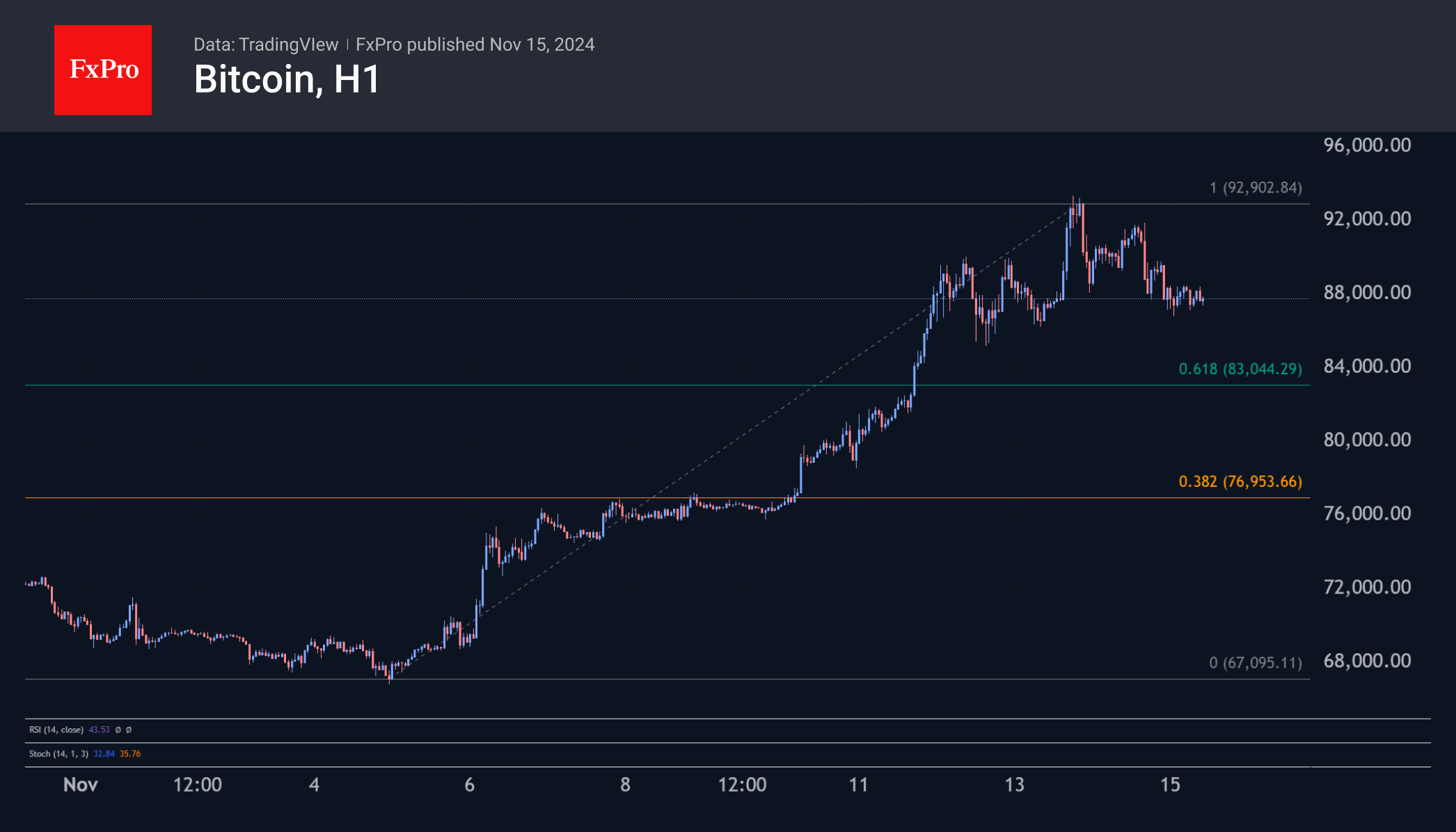

Bitcoin is consolidating below $88K, opening and closing within the $88K–$89K range for the fourth day. On the daily timeframe, the RSI is about to fall below the 80 level, which could trigger a deeper shakeout with a pullback to $83K.

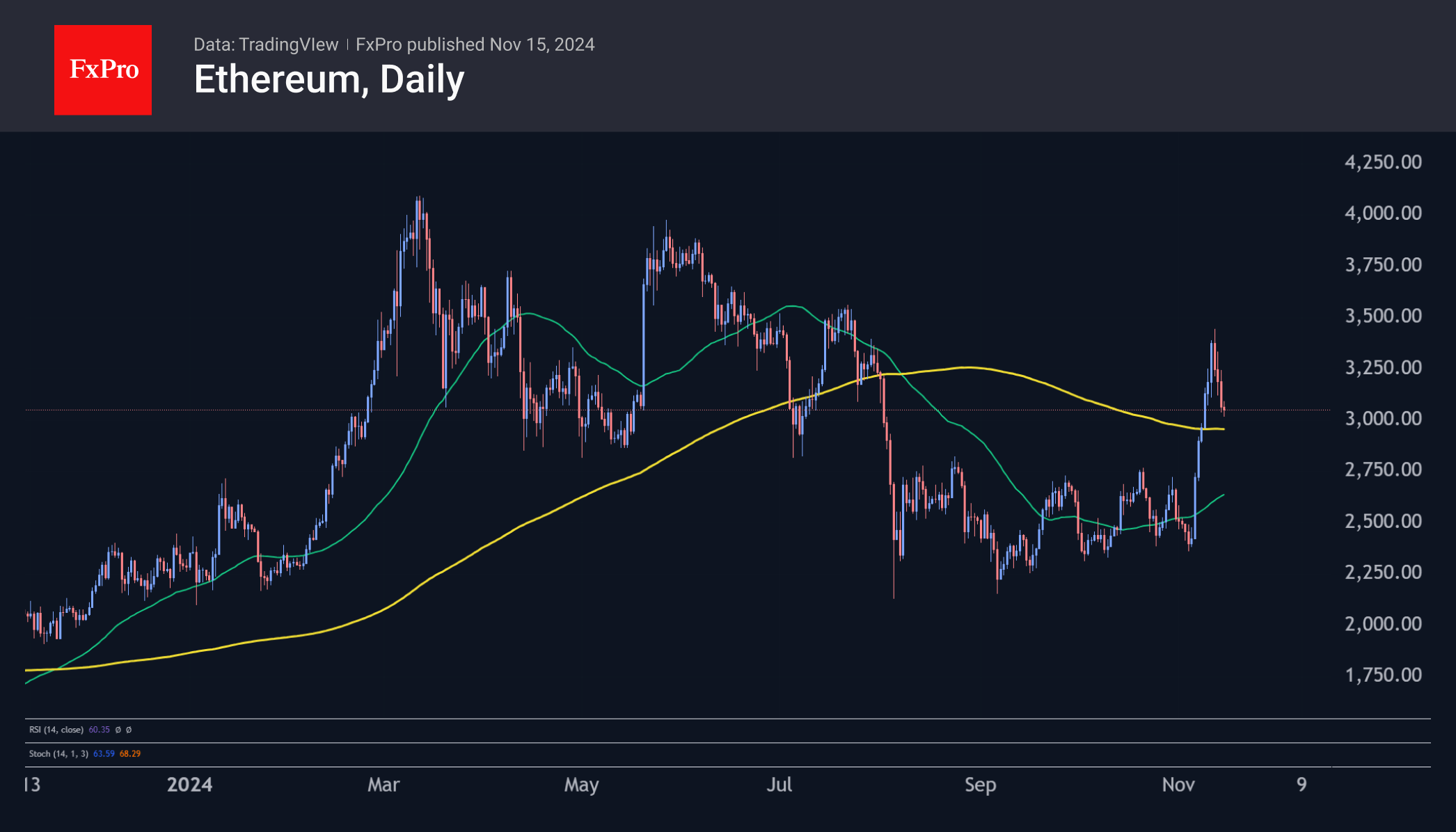

Ethereum has pulled back to $3,000, losing 12% from its peak in a four-day correction. Local support could come from the 200-day average at $2,950, which coincides with the coin’s support area from April to July this year.

News Background

The PEPE meme token has soared over the past two days, reaching a record capitalisation of over $9.6 billion and the 15th spot in the CoinMarketCap ranking. The coin surged after listing on several crypto platforms, including Robinhood and Coinbase.

K33 Research notes that bitcoin’s correlation with gold fell to an 11-month low (-0.36). The divergence occurred after Trump won the presidential election. Since then, bitcoin has rallied 20% to a new ATH, while the precious metal has fallen 5% on the back of a stronger dollar and rising US Treasury yields.

According to a survey by digital bank Sygnum, 57% of institutional investors intend to increase their investments in cryptocurrencies. 65% of respondents are optimistic about the crypto market. According to 69% of respondents, high price volatility is the main barrier to entry into the crypto market.

Mike Novogratz, CEO of Galaxy Digital, said Bitcoin will reach $500,000 if the US creates a strategic reserve in the first cryptocurrency. US President-elect Donald Trump made a similar proposal during his election campaign.

According to HashKey Group, the Trump administration’s friendly attitude towards cryptocurrencies will be one factor forcing China to lift restrictions on the cryptocurrency market.

Ethereum developers have unveiled the concept of ‘smart transactions’, bringing the realisation of the ‘world computer’ closer. Due to a more dynamic set of features, Smart Transactions (STXN) will significantly expand the range of applications and protocols.

UK Economy Contracts in September, Pound Shrugs

The British pound has stabilized on Friday after four straight losing sessions. In the European session, GBP is trading at 1.2666, up 0.02%. It has been a miserable week for the pound, which is down 1.9%. The pound fell as low as 1.2629 on Thursday, its lowest level since early July.

UK GDP declines 0.1%

The UK economy surprised on the downside with a contraction of 0.1% m/m in September, after a 0.2% gain in August and below the market estimate of 0.2%. This was the first decline in five months. Quarterly, the economy expanded by only 0.1% in the third quarter, its weakest pace in three quarters. This followed the 0.5% gain in Q2 and missed the market estimate of 0.2%. The services sector grew by just 0.1%.

The GDP data will be a major disappointment to the new Starmer government, which has promised to kick-start the UK economy. After solid growth in the first half of the year, the economy fell with a sharp thud, with weak consumer and business confidence dampening economic activity.

The Bank of England will be keeping a close eye on the GDP data, with its next meeting on Dec. 19, the last meeting of the year. The BoE shaved rates by a quarter-point earlier this month and weak GDP will support the case for a rate cut at the December meeting.

US retail sales expected to improve

The US closes the trading week with retail sales, which are expected to have improved in October. The market estimate is 1.9%, compared to 1.7% in September. Monthly, retail sales are expected to inch up to 0.4% from 0.3%. Consumer spending has been generally strong and consumer confidence should improve now that the uncertainty over the US election is over.

GBP/USD Technical

- GBP/USD tested resistance at 1.2674 earlier. The next resistance line is 1.2719

- 1.2578 and 1.2527 are the next support levels

Japan GDP Beats Forecast, Yen Ends Skid

The Japanese yen is in positive territory today, putting the brakes on a four-day skid. In the European session, USD/JPY is trading at 155.54 down 0.45% on the day.

Japan GDP climbs 0.9%

Japan’s economy expanded by 0.9% in the third quarter, below the revised 2.2% gain in Q2 but above the market estimate of 0.7%. Quarterly, GDP rose 0.2%, lower than the 0.5% gain in Q2 and matching expectations.

The GDP numbers were not sparkling but point to a second straight quarter of growth. August economic activity was dampened due to a “megaquake” alert and a fierce typhoon which caused widespread destruction and disruption.

Private consumption, which comprises more than half of the country’s GDP showed strong growth of 3.6% y/y, despite the weather issues. This is an encouraging sign for the Bank of Japan, which wants to see inflation rise to demand and consumption. The BoJ has been vague about the timing of a rate hike but the markets are looking at December or January as likely dates. The yen has been wobbly and is down 2.3% in November. If the yen’s downswing continues, the BoJ could decide to hike rates at the Dec. 19 meeting.

The US wraps up the week with retail sales for October and the markets are expecting a slight gain. Retails sales eased to 1.7% y/y in September, which was an 8-month low. The forecast for October is 1.9%. Monthly, retail sales are expected to inch up to 0.4% from 0.3%. Consumer spending has been generally strong and consumer confidence should improve now that the uncertainty over the US election is over.

USD/JPY Technical

- USD/JPY has pushed below support at 1.5601 and is testing 1.5560. The next support line is 1.5493

- 1.5668 and 1.5709 are the next resistance lines

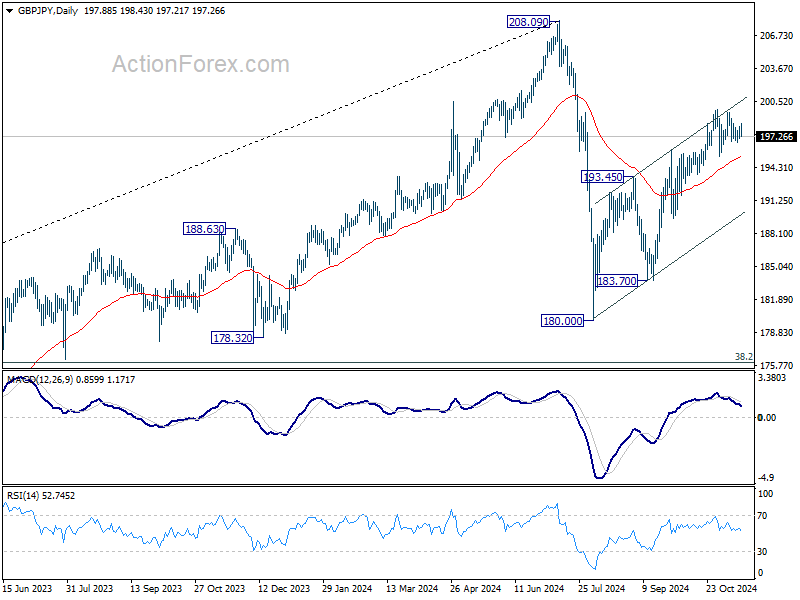

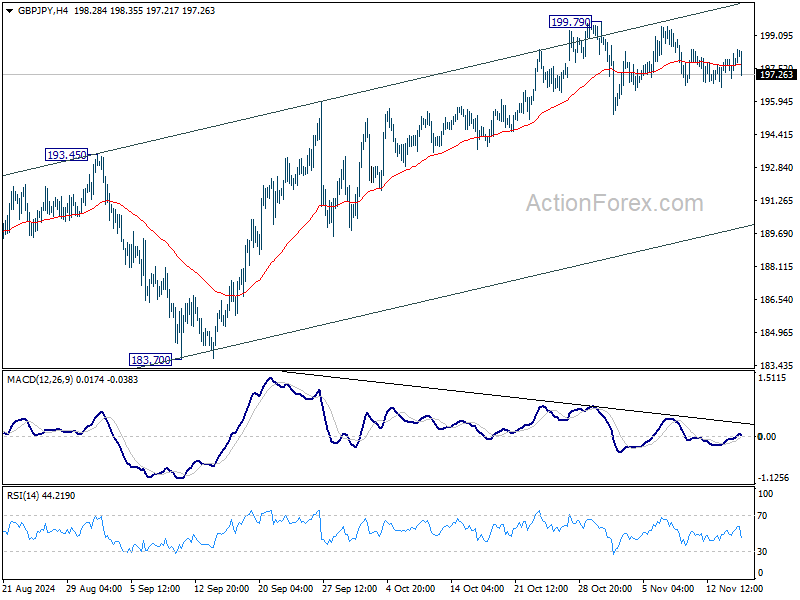

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.28; (P) 197.76; (R1) 198.45; More...

GBP/JPY is still bounded in sideway trading below 199.79 and intraday bias stays neutral. Further rally is expected as long as 55 D EMA (now at 195.24) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.