Sample Category Title

EUR/USD Turns Red, Are Bears Back In Action?

Key Highlights

- EUR/USD started a major decline below the 1.1000 support.

- A short-term bearish trend line is forming with resistance at 1.0865 on the 4-hour chart.

- GBP/USD extended losses and tested the 1.2965 support zone.

- Bitcoin surged above the $67,500 and $68,000 resistance levels.

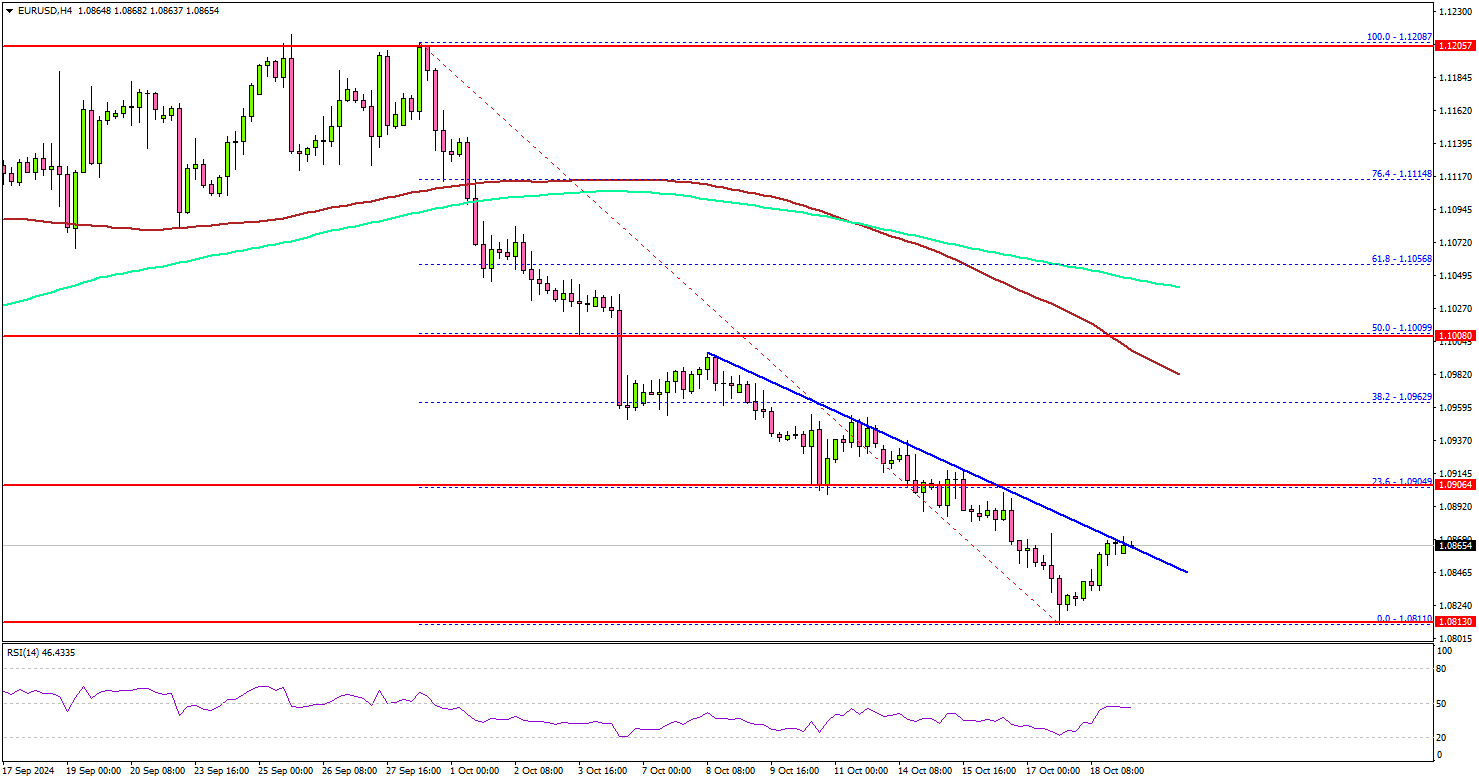

EUR/USD Technical Analysis

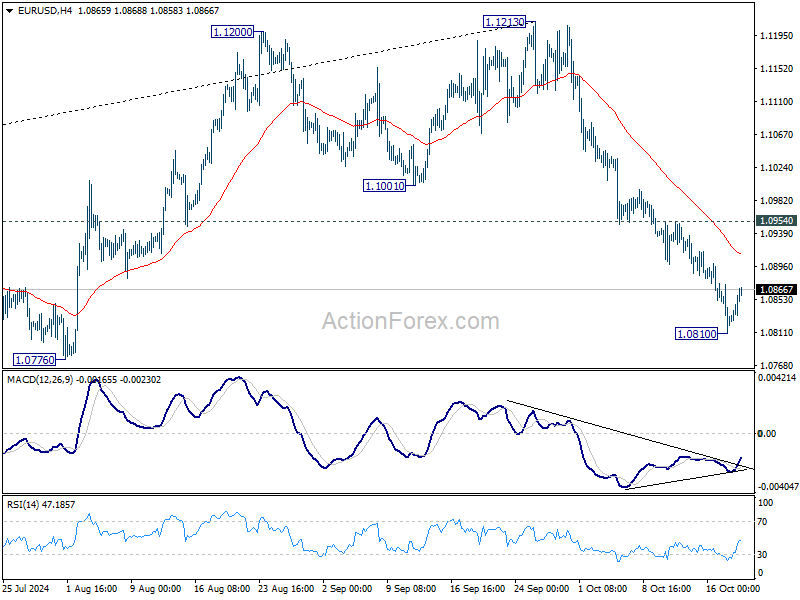

The Euro started a fresh decline below the 1.1050 level against the US Dollar. EUR/USD traded below 1.1000 to move into a bearish zone.

Looking at the 4-hour chart, the pair settled below the 1.0980 pivot level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even tested the 1.0810 level and currently consolidating losses.

There was a minor increase above the 1.0840 level. On the upside, the bears might be active near the 1.0865 level. There is also a short-term bearish trend line forming with resistance at 1.0865 on the same chart.

The first major resistance might be near the 1.0900 level. A close above the 1.0900 level could set the tone for another increase. The next major resistance could be 1.0980.

On the downside, immediate support sits near the 1.0820 level. The next key support sits near the 1.0800 level. Any more losses could send the pair toward the 1.0750 level.

Looking at Bitcoin, the bulls remained in action and pushed the price above the $68,000 resistance zone.

Upcoming Economic Events:

- Fed's Kashkari speech.

PBoC slashes loan prime rates, HSI unmoved

People's Bank of China lowered its one-year loan prime rate to 3.1% and trimmed the five-year LPR to 3.6%, as anticipated by market watchers. This move, at the upper end of the 20-25 basis point range suggested by Governor Pan Gongsheng during a Beijing forum last Friday, impacts a broad spectrum of loans in China. The one-year LPR directly influences corporate and household loans, while the five-year LPR serves as a benchmark for mortgage rates.

While this rate cut signifies some level of monetary stimulus, analysts continue to stress that China's core issue is not the supply of credit, but rather a lack of demand. Many argue that without substantial fiscal stimulus, the impact of these rate adjustments will remain muted.

Hong Kong market barely reacted to the rate cut news. HSI continues to trade in a narrow range between 20k and 21k. However, technically, HSI's up trend from 14794.16 would remain intact as long as 38.2% retracement of 14794.16 to 23241.74 at 20014.76 holds. Break of 21622.65 resistance will indicate that the correction is over, and bring retest of 23241.74 high.

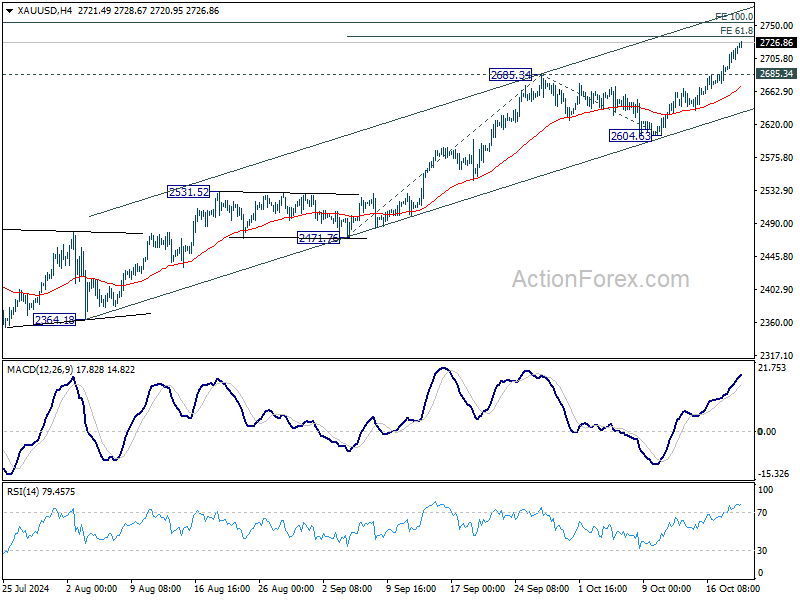

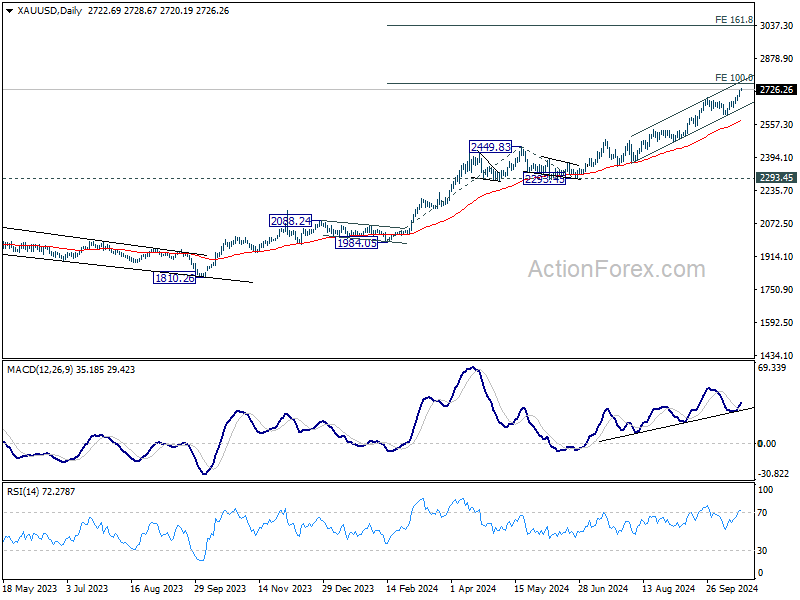

Gold continues record rally amid rising world war fears

Gold prices edged higher in Asian session today, extending their recent record-breaking run. While some market observers attribute the precious metal's rally to uncertainty surrounding the upcoming US presidential election—with no clear frontrunner between Democrat Kamala Harris and Republican Donald Trump—the persistent climb in U.S. stock markets to new record highs suggests that domestic political factors may not be the primary driver. Instead, escalating geopolitical risks appear to be fueling increased demand for Gold as a safe-haven asset.

In the Middle East, Israel has intensified its military operations in both Gaza and Lebanon following recent developments, including the death of a prominent Hamas leader. Reports indicate that Iran-backed Hezbollah has conducted drone attacks targeting areas near Israeli Prime Minister Benjamin Netanyahu's residence. The prospects for a near-term ceasefire seem increasingly remote, raising concerns about broader regional instability.

Even more concerning,, tensions are escalating in Eastern Europe. Thousands of North Korean troops are reportedly preparing to support Russia in its ongoing conflict in Ukraine, with some North Korean military officers already deployed. Ukrainian President Zelenskyy warned this could be the "first step to world war," raising global alarm.

Technically, further rally is expected in Gold as long as 2685.34. Next target is 61.8% projection of 2471.76 to 2685.34 from 2604.53 at 2736.62.

But the a bigger test lies in 100% projection of 1984.05 to 2449.82 from 2239.45 at 2759.23. Strong resistance could be seen there to limit upside initially. However, decisive break above there would prompt upside acceleration. Next medium term target would then be 161.8% projection at 3047.08, which is slightly above 3000 psychological level.

Morning Report

Today's economic developments and market movements.

Key themes: Markets had a relatively quiet finish to the week with little significant market moving data.

US equities finished the week in the green with the S&P 500 posting its sixth consecutive weekly gain.

Rates were slightly lower across the curve in the US and Europe.

The US dollar took a breather from its recent strengthening, giving back a little ground against most of its G-10 counterparts.

Share markets: US equities ended the week in the green, with the S&P 500 posting its sixth consecutive weekly gain. The S&P 500 rose 0.4% on Friday, while the NASDAQ and the Dow Jones were up 0.6% and 0.1%, respectively.

The Eurostoxx 50 and the German Dax were up 0.8% and 0.4%, respectively. While the FTSE 100 slipped 0.3% in London.

The ASX 200 shed 0.9% on Friday but remained 0.8% higher over the week.

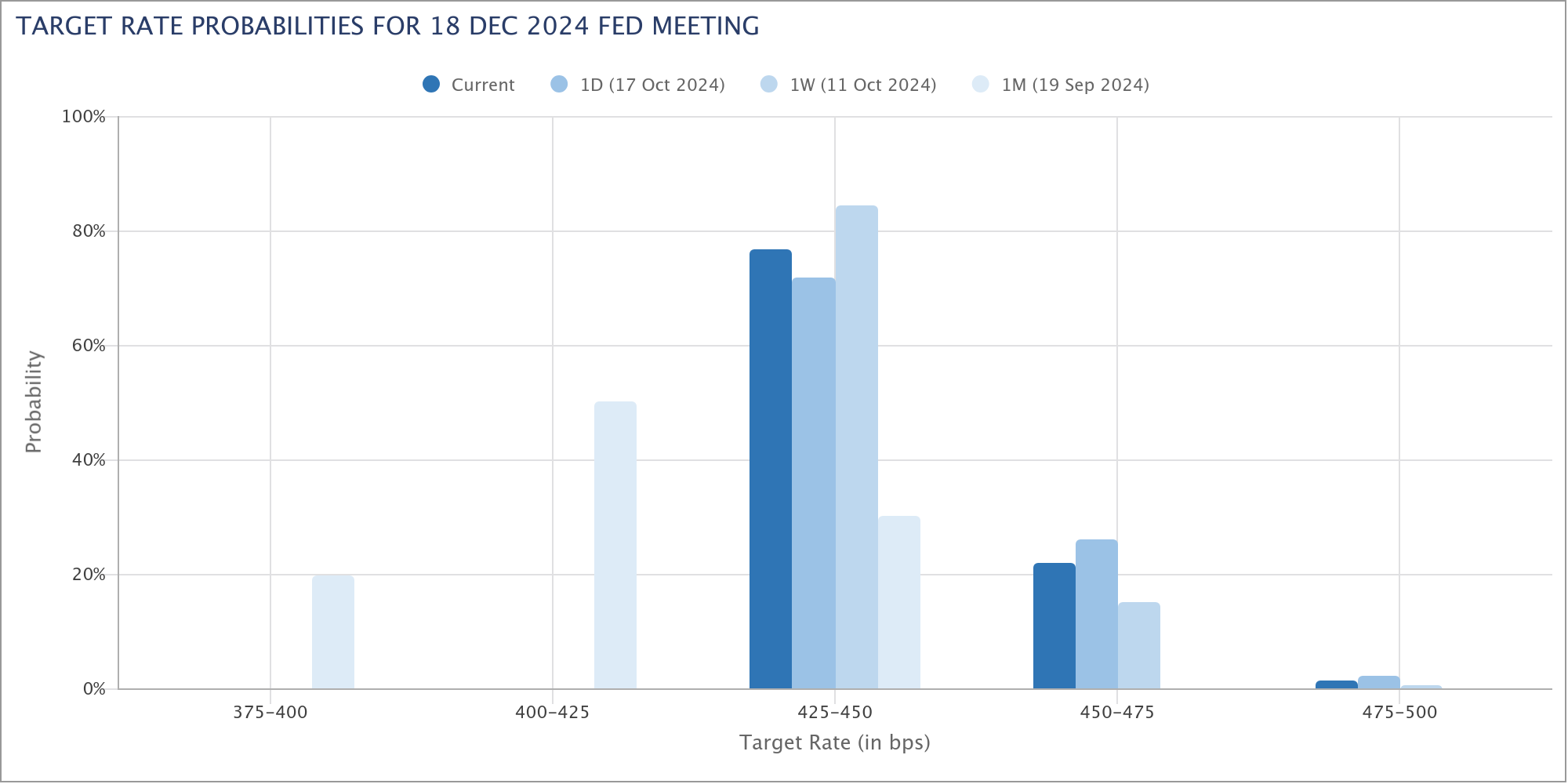

Interest rates: US treasury yields were slightly lower across the curve on Friday. The 2-year yield edged 2 basis points lower to 3.95%, while the 10-year yield was down 1 basis point to 4.08%. A November Fed rate cut remains around 90% priced in with around 40 basis points to cuts priced by the end of the year.

Aussie bond futures mimicked the moves offshore. The 3-and-10-year futures yields were both down 2 basis points to 3.80% and 4.30%, respectively. The odds of an RBA rate cut this year have been trimmed to around 25%, the first rate cut is not fully priced until May 2025.

Foreign exchange: The US dollar pulled back against most of its G-10 counterparts. The DXY slipped from a high of 103.80 to a low of 103.46 and finished only slighty above the days low at 103.49.

The Aussie dollar was a touch firmer and held on above 67 cents despite what was an underwhelming set of announcement from Chinese policymakers last week.

The sell-off in the euro hit a roadblock on Friday with the EUR/USD lifting off a low of 1.0825 to a high of 1.0870, near where it was trading early this morning. However, reassuring inflation data leaves the direction of travel for rates abundantly clear, and the euro on a less supportive yield foundation. After opening above 150 on Friday, the Japanese Yen found some buyers willing to push the USD/JPY back below 150 to around 149.56.

Commodities: Crude markets closed on their lows for the week as Western Leaders called for a ceasefire after the Israeli Defence Force confirmed the killing of Hamas Leader Sinwar. China’s apparent oil demand also fell 7% over the year to September. West Texas Intermediate futures closed down 2.1% at US$69.22.

Metals bounced into the end of the week as slightly better than expected Chinese activity data and the prospect of more stimulus helped stabilise sentiment. Copper was up 1.2% at US$9,553 while aluminium jumped 2.4% at $2,613.

Iron ore markets rebounded Friday despite Chinese steel production seeing the weakest back-to-back output in August and September since November 2021 bar December last year. Futures are up 1.2% at US$101.25. Chinese steel production so far this year is around 3% lower than last year and the lowest year to date total since 2019. At the same time, China has imported 8.5% more iron ore than it has on average over the last 3 years meaning that port inventory levels are close to record highs.

Australia: There were no major economic data releases on Friday.

China: Key economic data reinforced the message that the Chinese government needs to successfully implement stimulus measures if it wants to lift the economic momentum and achieve its growth objective.

GDP increased by 0.9% in the September quarter, up from downwardly revised 0.5% growth in the June quarter, but still below consensus expectations of a 1.1% rise. Compared to a year ago, output was 4.6% higher, which was the slowest annual pace of growth since the start of 2023.

Monthly indicators suggested that after weakening in August, China’s growth was stronger in September. Industrial production rose 0.6% in the month, the firmest in five months, to leave growth annual pace at 5.4%, close to the average over the last twelve months. News on consumer spending was also more positive, as retail sales increased by 0.4% in September and 3.2% over the year, both were the highest in four months.

Investment in fixed assets rose 0.7% in September. While it was the steepest increase in seven months, it was not sufficient to lift the annual growth on a YTD basis from 3.4% seen in August. The breakdown continued to show that state-owned companies fully accounted for the increase this year, while the private sector investment continued to stagnate.

Data on China’s real estate sector remained weak, with residential property sales still down by about 25% so far this year, and house prices maintaining their downward trend.

United Kingdom: Retail sales figures suggested that household consumption gained momentum in recent months. Headline retail sales volumes rose 0.3% in September, significantly higher than consensus forecasts of a 0.4% drop. And given that it followed strong gains July and August, the three-month growth accelerated to 1.8%, which matched the reading in Q1, when household consumption in the national accounts rose a solid 0.6% and was the biggest contributor to GDP growth that quarter. The annual growth in retail sales of 3.9% was the highest since early 2022.

United States: Housing starts declined by 0.5% in September following a sharp 7.8% gain in August. Weakness in the multifamily category accounted for the drop, while single family starts rose to a five-month high. In terms of levels, housing starts remained above the six-month average.

Dollar Extends Winning Streak, Though Momentum Hints at Waning Strength

Dollar continued its reign as the strongest currency for yet another week, bolstered by solidifying expectations around gradual and measured rate cut cycle by Fed. The rate cut from ECB provided some additional tailwind for the greenback. However, momentum behind the Dollar's rise remains tepid. Strong risk-on sentiment, coupled with sluggishness in U.S. Treasury yields, is capping further gains. Additionally, the potential for intervention from Japanese authorities has kept Dollar’s advances against Yen in check.

Sterling ranked as the second-best performer this week, supported by mixed economic data from the UK that leaves BoE's policy outlook uncertain beyond the widely expected November rate cut. Notably, Pound resumed its uptrend against the weaker Euro, reaching its best level since mid-2022. Meanwhile, Swiss Franc ended the week at the bottom of the performance chart, with Euro not far behind.

Australian Dollar also struggled, despite a brief bounce following stronger-than-expected jobs data. The lack of concrete measures in China's recent stimulus announcements continues to weigh on Aussie. Broader risk sentiment in the Asia-Pacific region, in China, Hong Kong, and Japan, is adding further pressure on the currency.

Record-Breaking Stocks, Yield Momentum Fades, Dollar Stalls at Key Resistance

U.S. equity markets continued their impressive ascent last week, with both DOW and S&P 500 closing at new record highs, marking six consecutive weeks of gains. This streak represents the longest series of weekly advances in 2024 for these major indices. Specifically, DOW gained 0.96% for the week, S&P 500 rose by 0.85%, and NASDAQ Composite added 0.80%. Investors are showing robust confidence, seemingly embracing the expectation that Fed will proceed with monetary policy easing only in a gradual and measured fashion.

While the consensus still anticipates two additional 25bps rate cuts by Fed before the end of the year, recent comments from Fed officials suggest that a single rate cut may also be a plausible outcome. Markets are adjusting to these possibilities well as reflected in fed fund futures, which now prices in a 77% chance of a total of 50 bps of rate cuts by year-end, down from approximately 84% a week earlier.

While Dollar ended the week as the strongest performing currency, its momentum was somewhat constrained by risk-on environment, as well as loss of momentum in US Treasury yields. Technically, Dollar Index is capped by a significant medium-term resistance, which could continue to limit further appreciation in the near term.

As for DOW, near term outlook will remain bullish as long as 41831.74 support holds. Next target is 100% projection of 32327.20 to 3989.05 from 38000.96 at 45562.81. Also, while it's still a bit far, we'd pencil in 100% projection of 1821365 to 36952.65 from 28660.94 as the next medium term target first.

10-year yield is starting to face strong resistance from 38.2% retracement of 4.997 to 3.603 at 4.135 and 55 W EMA (now at 4.074) zone. This is seen as an important hurdle that's difficult for TNX to overcome. Firm break of 3.981 support should confirm rejection by the mentioned resistance zone and bring pullback to 55 D EMA (now at 3.935) and possibly below. However, decisive break of this zone will carry larger bullish implications, and open up the case for long term up trend resumption through 4.997.

Dollar index is also pressing 55 W EMA (now at 103.47). Break of 102.76 minor support will indicate initial rejection by 55 W EMA and bring pull back to 55 D EMA (now at 102.36) and possibly below. However, considering that DXY has just bounced of 55 M EMA (now at 99.85). Sustained break of 55 W EMA will raise the chance that whole corrective fall from 114.77 has completed, and bring stronger rally to 106.13/107.34 resistance zone.

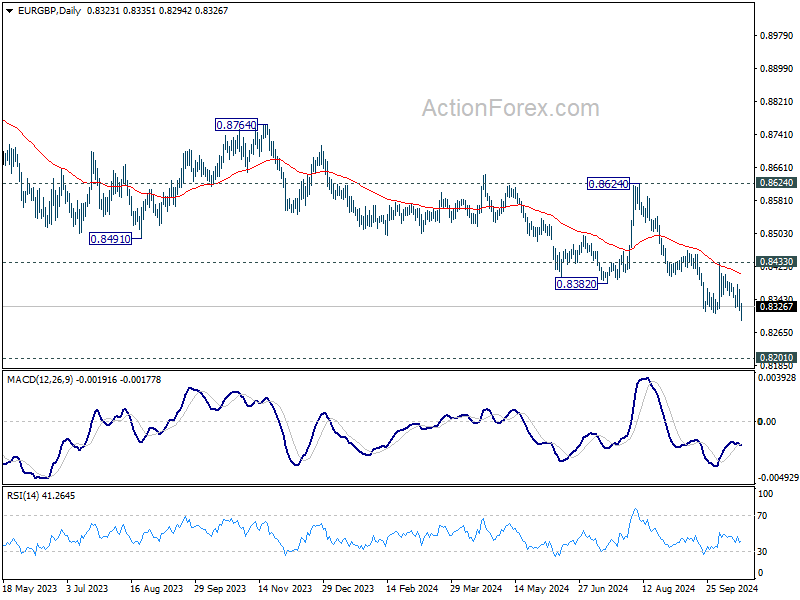

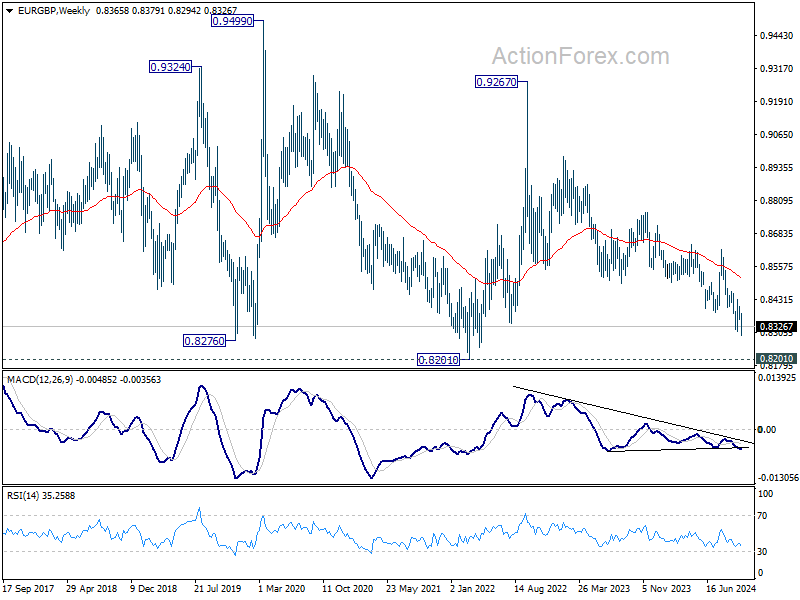

DAX at Record But Faces Resistance, EUR/GBP Targets Crucial Support After Breakout

ECB unanimously lowered deposit rate by 25bps to 3.25%, aligning with widespread expectations. The key takeaway from President Christine Lagarde's statement was the acknowledgment that the disinflationary process is "well on track." The inflation outlook has been hit by "downside surprises" in economic activity, signaling that the ECB's path to further easing may continue.

While Lagarde did not provide explicit guidance on future policy moves, it's evident that policymakers are increasingly surprised and concerned by the deterioration in economic indicators since their previous meeting. A further rate cut in December appears to be on the table, and only a significant improvement in incoming data might deter ECB from proceeding. The pace at which ECB intends to lower interest rates to a neutral level, however, remains uncertain and will likely depend on the new economic projections scheduled for release in December.

ECB's accelerated easing measures seem timely for European investors, as reflected by the DAX index reaching new record highs last week. However, DAX is now approaching a critical resistance zone around the psychological level of 20k, which may pose a significant hurdle that's proved difficult to break unless the European economic outlook improves significantly under the ECB's support.

Technically, DAX is now close to 100% projection of 8255.65 (2020 low) to 16290.19 (2021 high) from 11862.84 (2022 low) at 19897.38, which is close to 20k psychological level. Break of 18911.72 support will indicate initial rejection by this resistance zone, and bring break deeper pullback towards 17024.82 support.

Nevertheless, firm break of 20k will be a sign of strong underlying momentum. Next near term target will be 100% projection of 14630.21 to 18892.92 from 17024.82 at 21287.52.

Euro concluded the week on a weaker footing, notably breaking lower against Sterling. The UK's economic data painted a mixed picture last week. CPI dropped more than anticipated to 1.7% in September, the lowest level since April 2021. This significant decline strengthens the argument for BoE to resume policy easing with a 25 basis point rate cut in November. However, robust employment figures and strong retail sales suggest that consumer demand may not be cooling sufficiently to ensure continued disinflation. While another BoE rate cut in December remains a possibility, it is by no means certain, which is helping to keep the Pound relatively buoyant.

Technically, while EUR/GBP's down trend resumed last week it's now heading towards an important support at 0.8201 (2022 low). Strong support is expected there to contain downside and bring rebound, at least on first attempt. Break of 0.8433 resistance should turn the cross into sideway trading first. But medium term outlook will remain bearish as long as 0.8624 resistance holds.

Yen Slide Halted by Verbal Intervention and Political Risks: Will It Bounce Back?

In Japan, Yen briefly slipped past the critical 150 level against Dollar, but it quickly regained ground as verbal interventions from Japanese officials made traders wary of pushing the currency lower. At this same time, this stabilization of Yen comes amid a broader shift in investor sentiment, as Nikkei Index experiences a selloff fueled by growing political uncertainty ahead of the snap general election scheduled for October 27.

Recent polls suggest that the ruling Liberal Democratic Party may struggle to secure the 233 seats needed for an outright majority in the 465-seat lower house. According to a Nikkei newspaper report, the LDP's grip on power—held since 2012 after a brief period in opposition—could be at risk. Further adding to the political unease, a separate survey by Jiji Press revealed that support for new Prime Minister Shigeru Ishiba's cabinet has fallen to just 28%, marking the lowest approval rating for a new government since records began in 2000. This sharp decline raises serious doubt about the stability of Ishiba's leadership.

Technically, Nikkei's rise from 31156.11 is seen as the second leg of the corrective pattern from 42426.77 high. Target of 61.8% projection of 31156.11 to 39080.64 from 40257.34 has already be reached.

Notably, Tuesday's trading session formed an "Abandoned Baby" candlestick pattern, a rare and potent bearish reversal signal. Break of 37651.07 support will argue that whole rebound from 311156.11 has completed, and turn outlook bearish for 35254.43 and below.

Extended selloff in Nikkei could drag USD/JPY lower. Break of 146.47 resistance turned support will indicate that the rebound from 139.57 has completed, and turn near term outlook bearish for retesting this low.

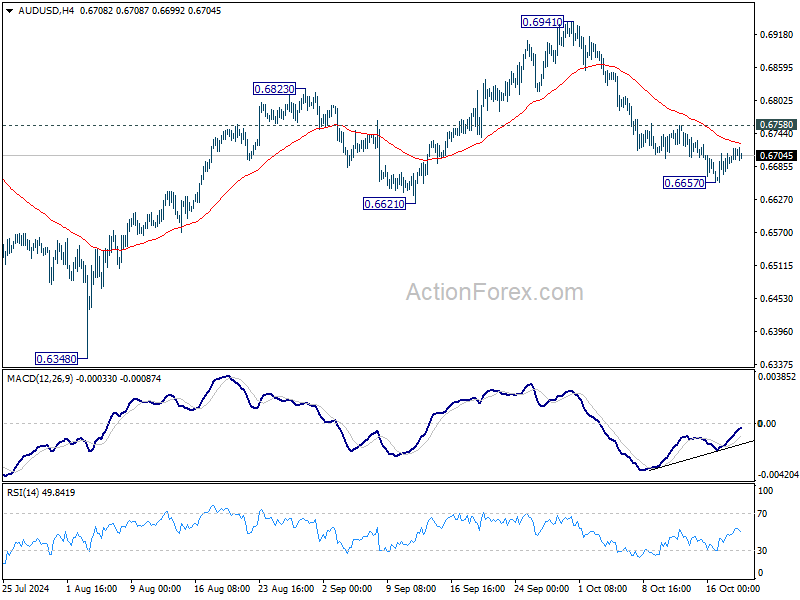

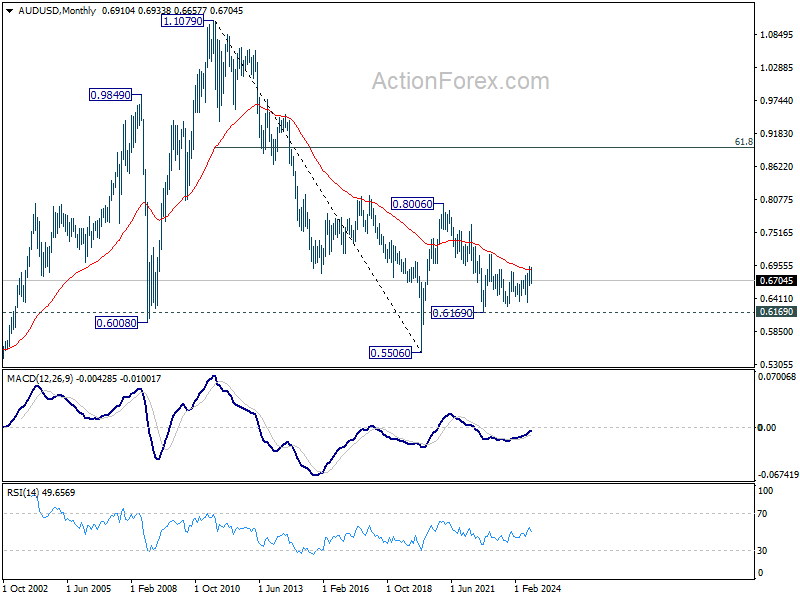

AUD/USD Weekly Report

AUD/USD edged lower to 0.6657 last week but recovered since then. Initial bias stays neutral this week for some more consolidations. Further decline is expected as long as 0.6758 resistance holds. Below 06657 will target 0.6621 first. Firm break there will confirm bearish reversal. However, break of 0.6758 will suggest that pullback from 0.6941 has completed and turn bias back to the upside.

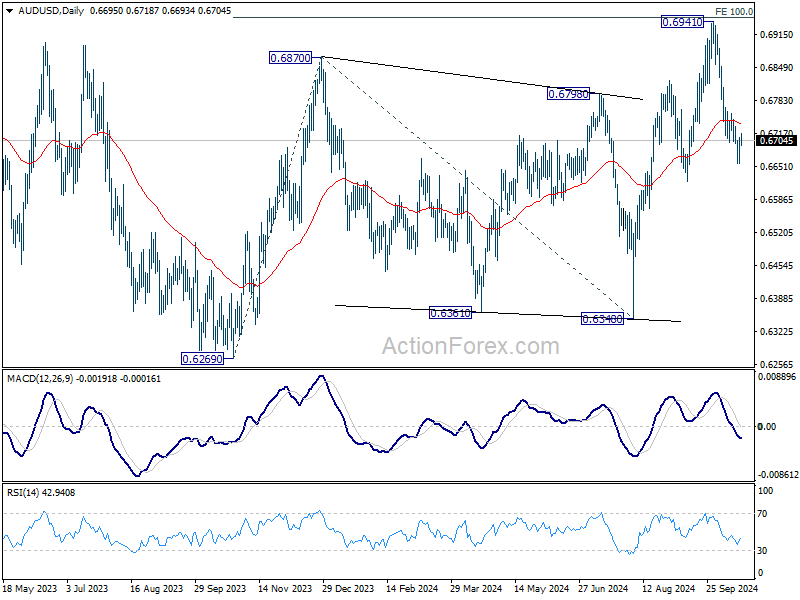

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.

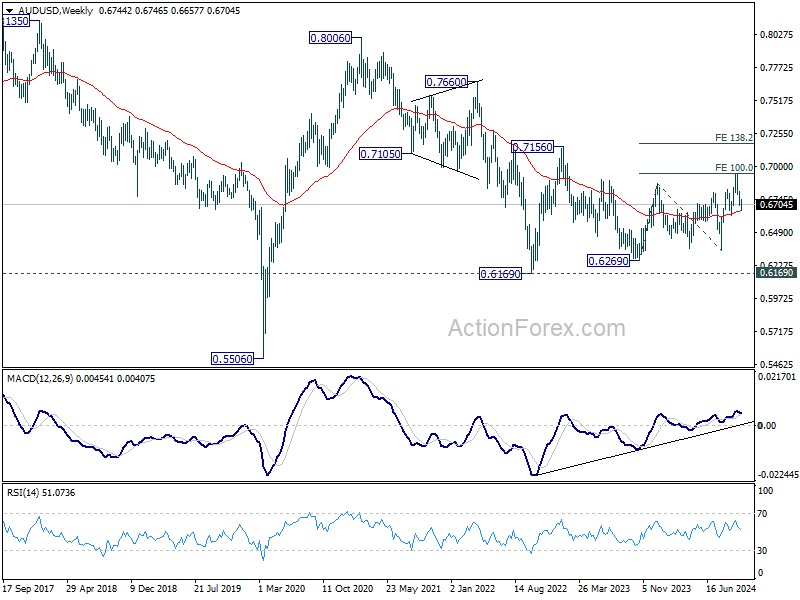

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen as the second leg of the pattern. Firm of 0.7156 resistance will argue that the third leg has already started towards 0.8006.

EUR/USD Weekly Outlook

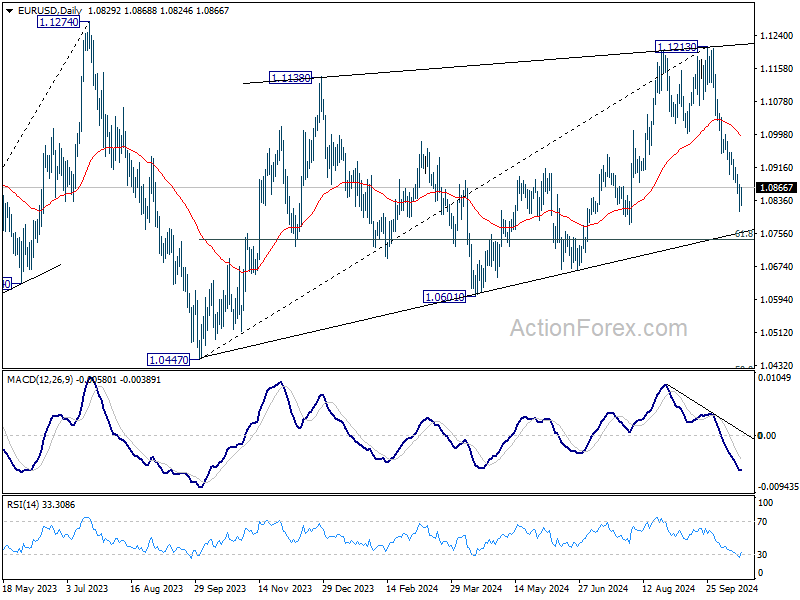

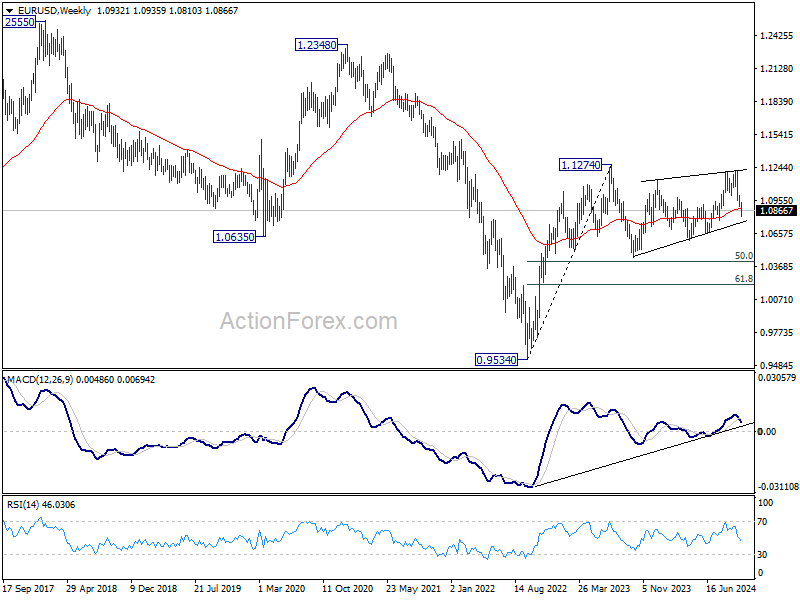

EUR/USD's decline from 1.1213 continued last week but recovered after hitting 1.0810. Initial bias remains neutral this week for consolidations. But outlook will stay bearish as long as 1.0954 resistance holds. Below 1.0810 will resume the fall from 1.1213 to 61.8% retracement of 1.0447 to 1.1213 at 1.0740. Firm break there will target 1.0601 support next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

In the long term picture, a long term bottom is in place at 0.9534 (2022 low). But for now, EUR/USD is struggling to sustain above 55 M EMA (now at 1.1011). Outlook is neutral at best at this point.

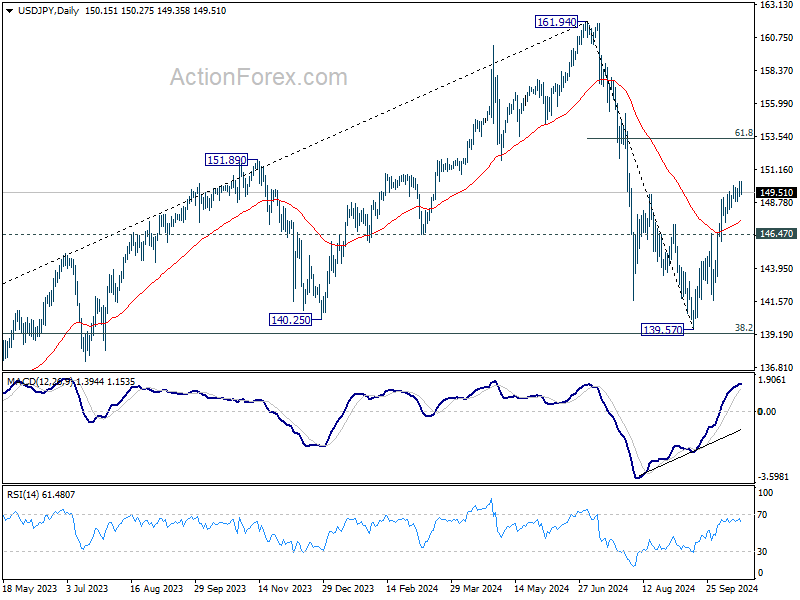

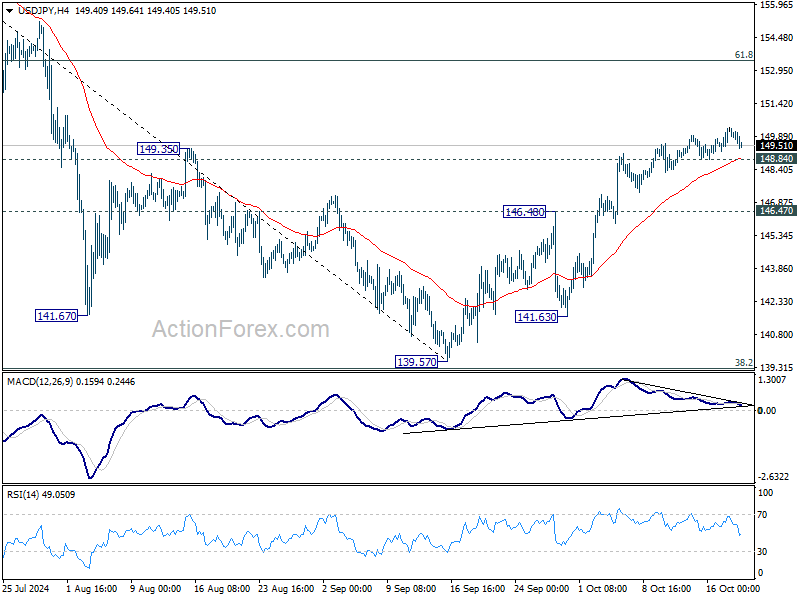

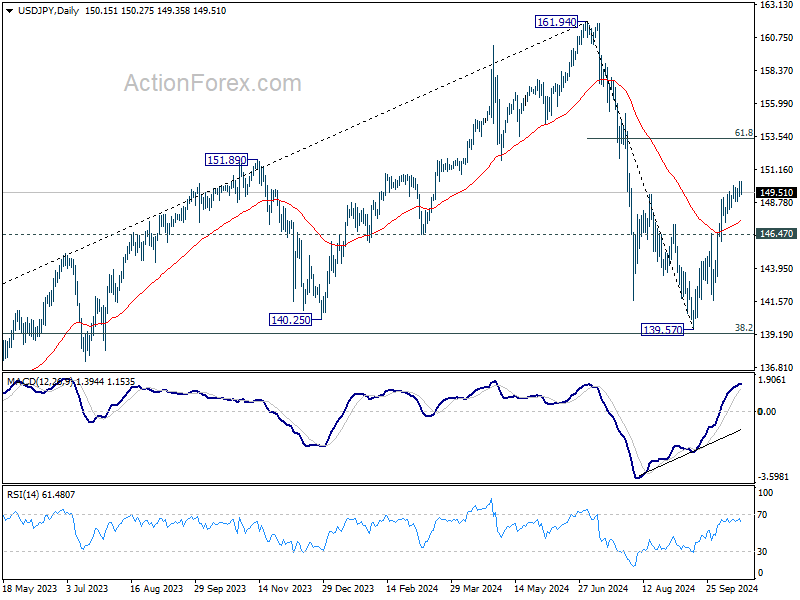

USD/JPY Weekly Outlook

USD/JPY edged higher last week even though it continued to lose upside momentum, as seen in 4H MACD. Further rally is expected as long as 148.84 minor support holds, towards 61.8% retracement of 161.94 to 139.57 at 153.39. However, break of 148.84 will turn intraday bias neutral first. Further break of 146.48 resistance turned support will indicate that rebound from 139.57 has already completed.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. However, a medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 133.73).

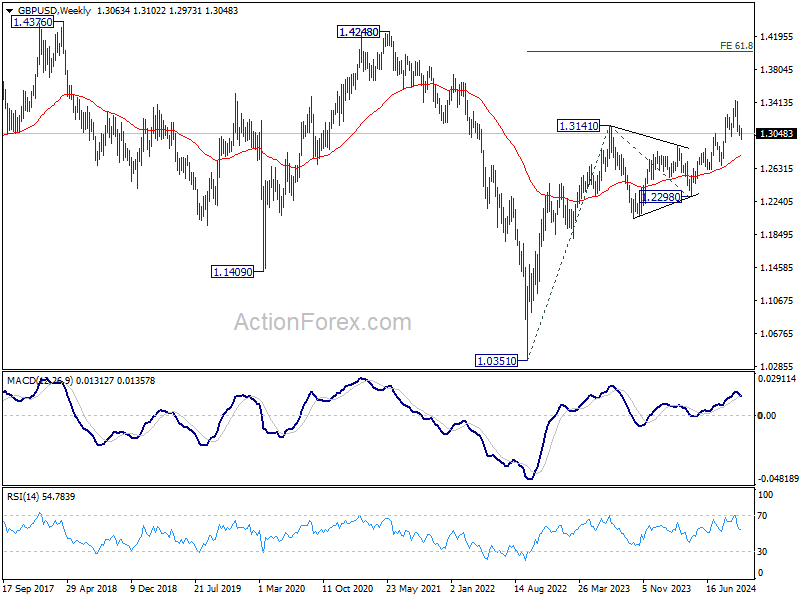

GBP/USD Weekly Outlook

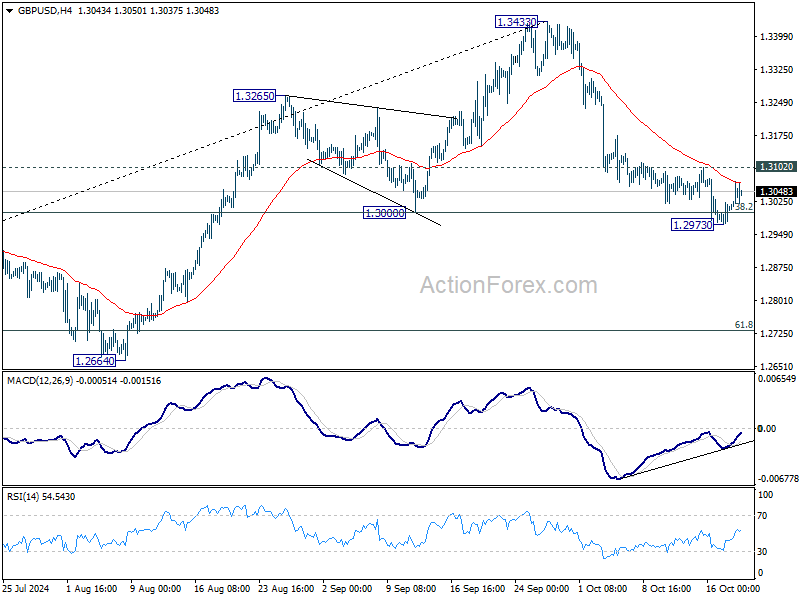

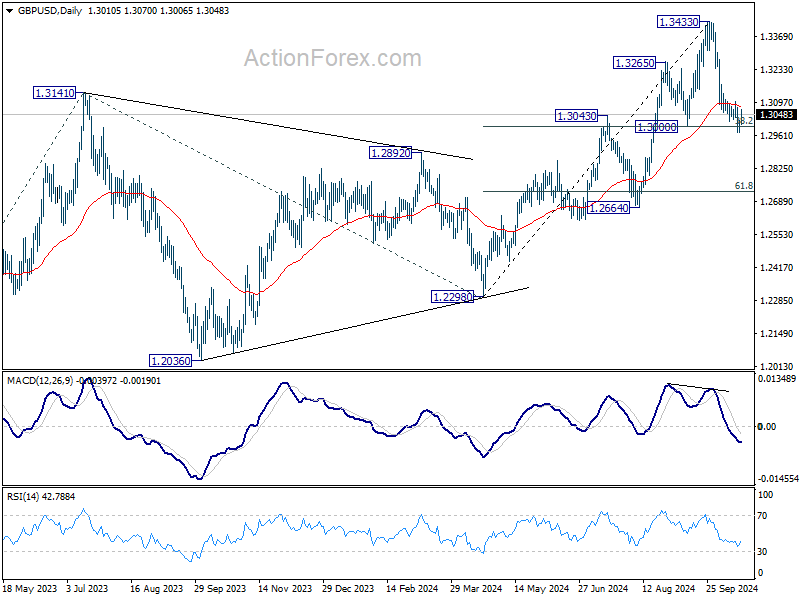

GBP/USD edged lower to 1.2973 last week but recovered after drawing support from 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999). Initial bias remains neutral this week first. On the upside, firm break of 1.3102 resistance will argue that pullback from 1.3433 has completed, and turn bias back to the upside for stronger rebound. However, sustained trading below 1.3000 will argue that whole rise from 1.2298 has completed and bring deeper fall to 61.8% retracement at 1.2732.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

In the long term picture, as long as 1.2298 support holds, rise from 1.0351 long term bottom is expected to continue. The strong break of 55 M EMA (now at 1.2811) is a sign of bullish trend reversal. Yet, break of 1.4248 structural resistance is needed confirm. Otherwise, price actions from 1.0351 could just be part of a consolidation pattern.

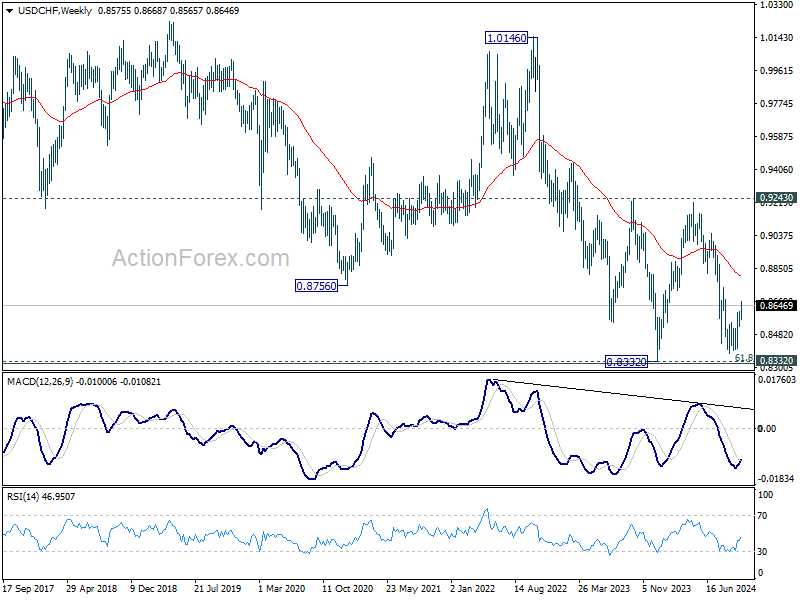

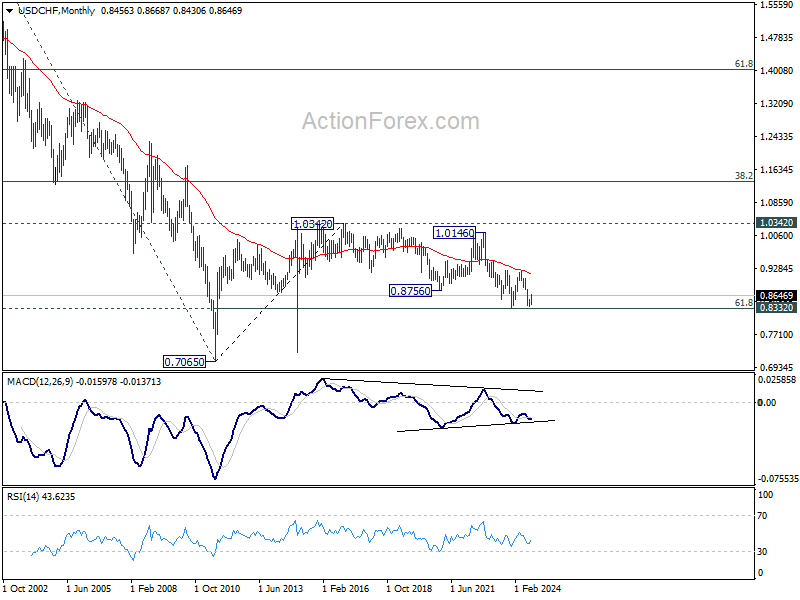

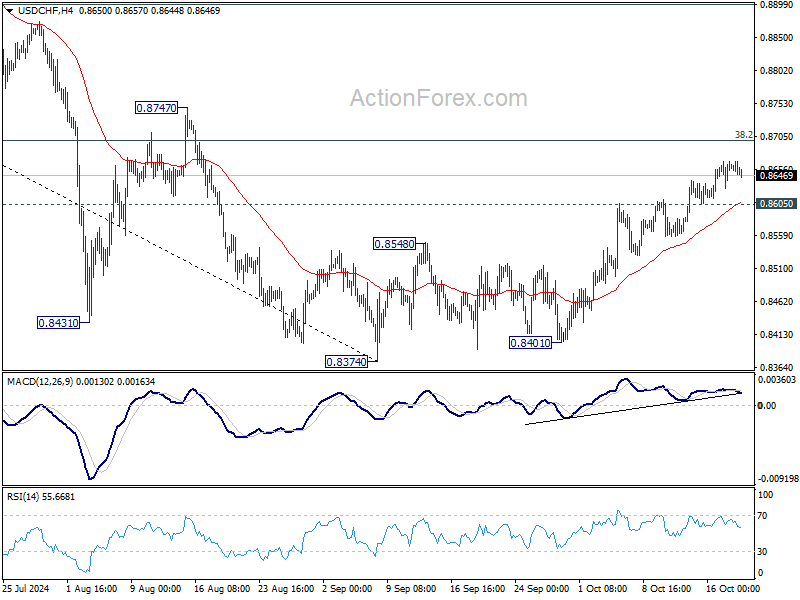

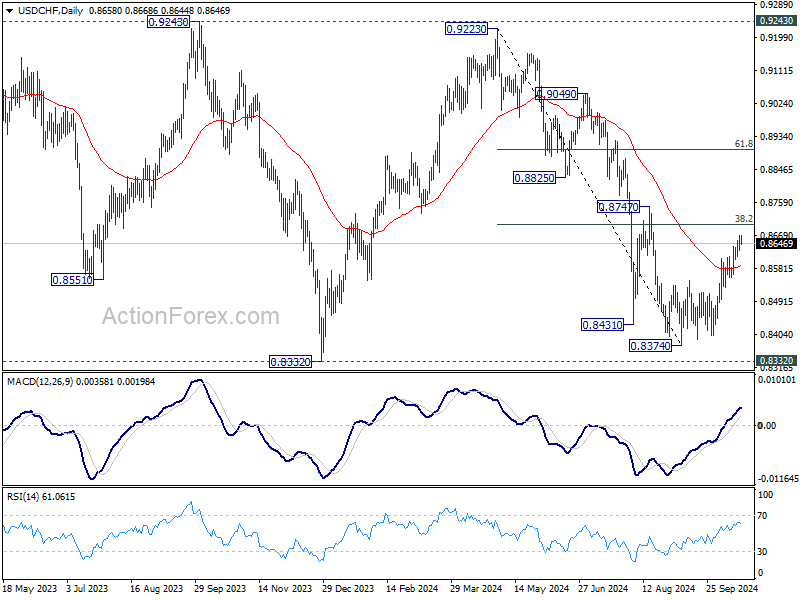

USD/CHF Weekly Outlook

USD/CHF's rebound from 0.8374 continued last week and there is no clear sign of completion yet. Initial bias stays on the upside this week for 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Sustained break there will argue that fall from 0.9223 has completed after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next. On the downside, below 0.8605 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Rejection by 55 M EMA suggest that this fall is in progress. Break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317 will pave the way back to 0.7065.