Sample Category Title

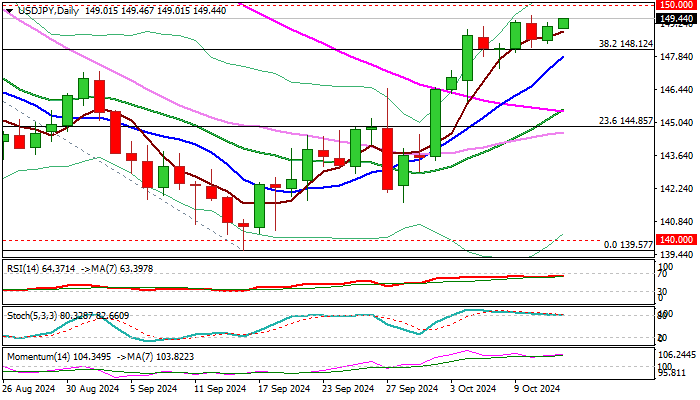

USD/JPY: Holding Above Broken Fibo Level Keeps Bulls in Play for Possible 150+ Acceleration

USDJPY remains constructive and pressuring the top of recent consolidation range in early Monday trading.

The second weekly bullish close, with long tailed last week’s candle, suggests that bulls hold grip for attack at psychological 150 barrier after recent consolidation stayed above broken Fibo pivot at 148.12 (38.2% of 161.95/139.57 descend).

Firm break of 150 to open way for test of 150.74 (50% retracement) and expose key barrier at 151.81 (top of thick daily cloud).

However, bulls may show further indecision and possibly hold in extended consolidation, as technical signals on daily chart are mixed.

Strong bullish momentum, 10/55 and 20/55 bull-crosses underpin the action, while overbought stochastic and formation of 100/200 death cross may produce more headwinds.

Near-term bias is expected to remain with bulls while the price action stays above broken Fibo level at 148.12, reverted to solid support and reinforced by rising 10DMA (147.84).

Break here, on the other hand, to generate initial that recovery leg from 139.57 (2024 low, posted on Sep 16) may be losing traction.

Res: 149.56; 150.00; 150.76; 151.81.

Sup: 148.91; 148.12; 147.84; 145.91.

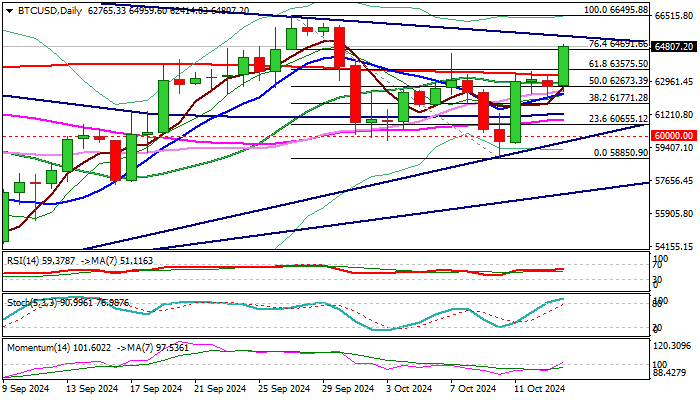

BTCUSD – Fresh Bulls Broke Through 200DMA Which Capped Action for Two Weeks

BTCUSD regained traction on Monday and resumes bull-leg off 58850 (Oct 10 low) after two-day pause.

Fresh advance broke through 200DMA (63302) which capped the action in past two weeks, advancing around 3.5% during Asian and European session.

Bulls cracked Fibo barrier at 64691 (76.4% retracement of 66495/58850) and eye next pivot at 65424 (falling trendline, the upper boundary of larger triangle) which guards key near term barrier at 66495 (Sep 27 peak).

Ascending 14-d momentum broke into positive territory and MA’s turned to bullish setup, contributing to positive near-term outlook, although increased headwinds on approach to the trendline, cannot be ruled out, as stochastic is strongly overbought.

Daily close above 200DMA is seen as minimum requirement to keep fresh bulls in play, with limited dips to find ground above broken Fibo 61.8% (63575) and offer better buying opportunities.

Res: 64959; 65424; 65975; 66495

Sup: 64000; 63575; 63302; 62673

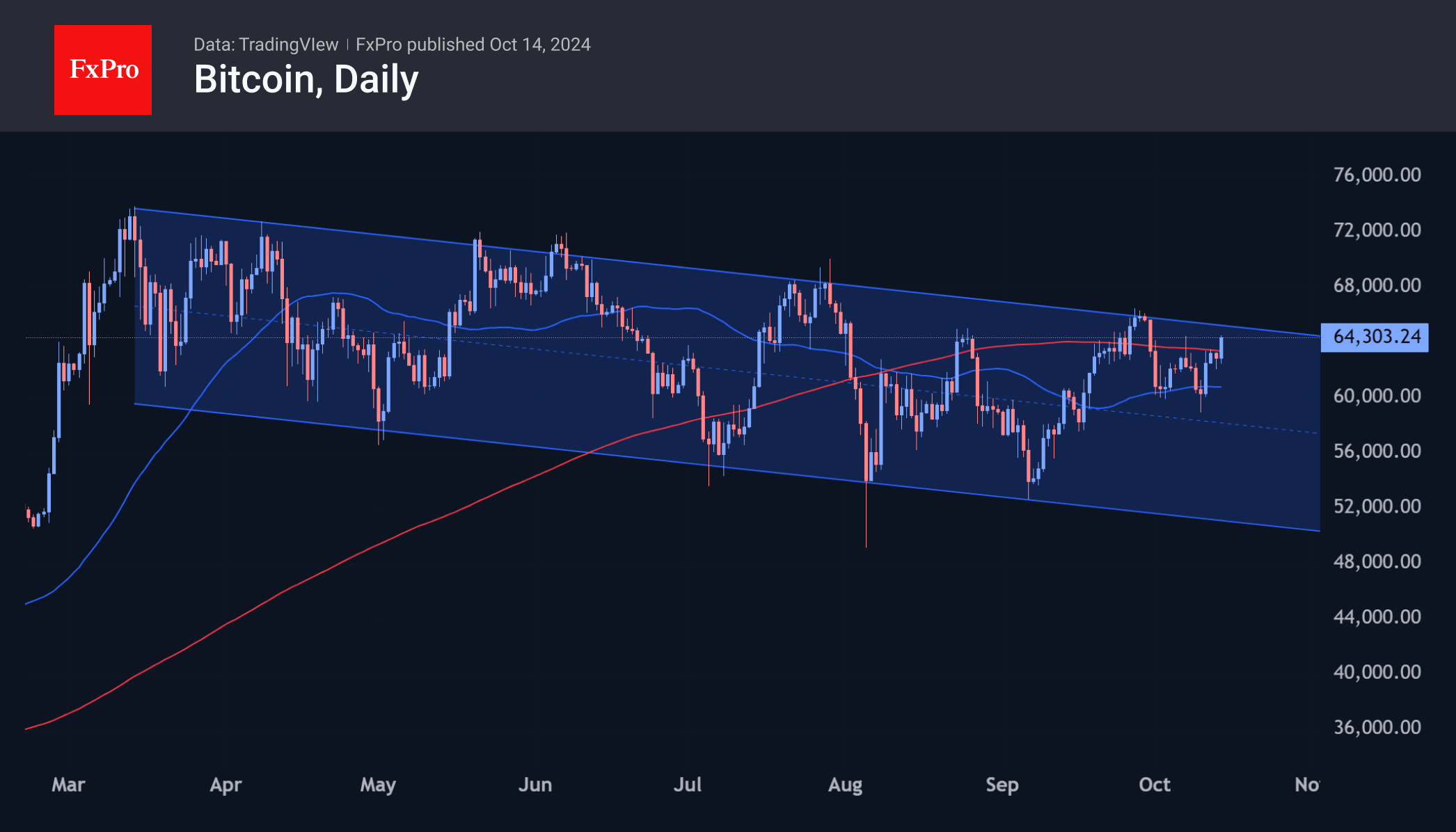

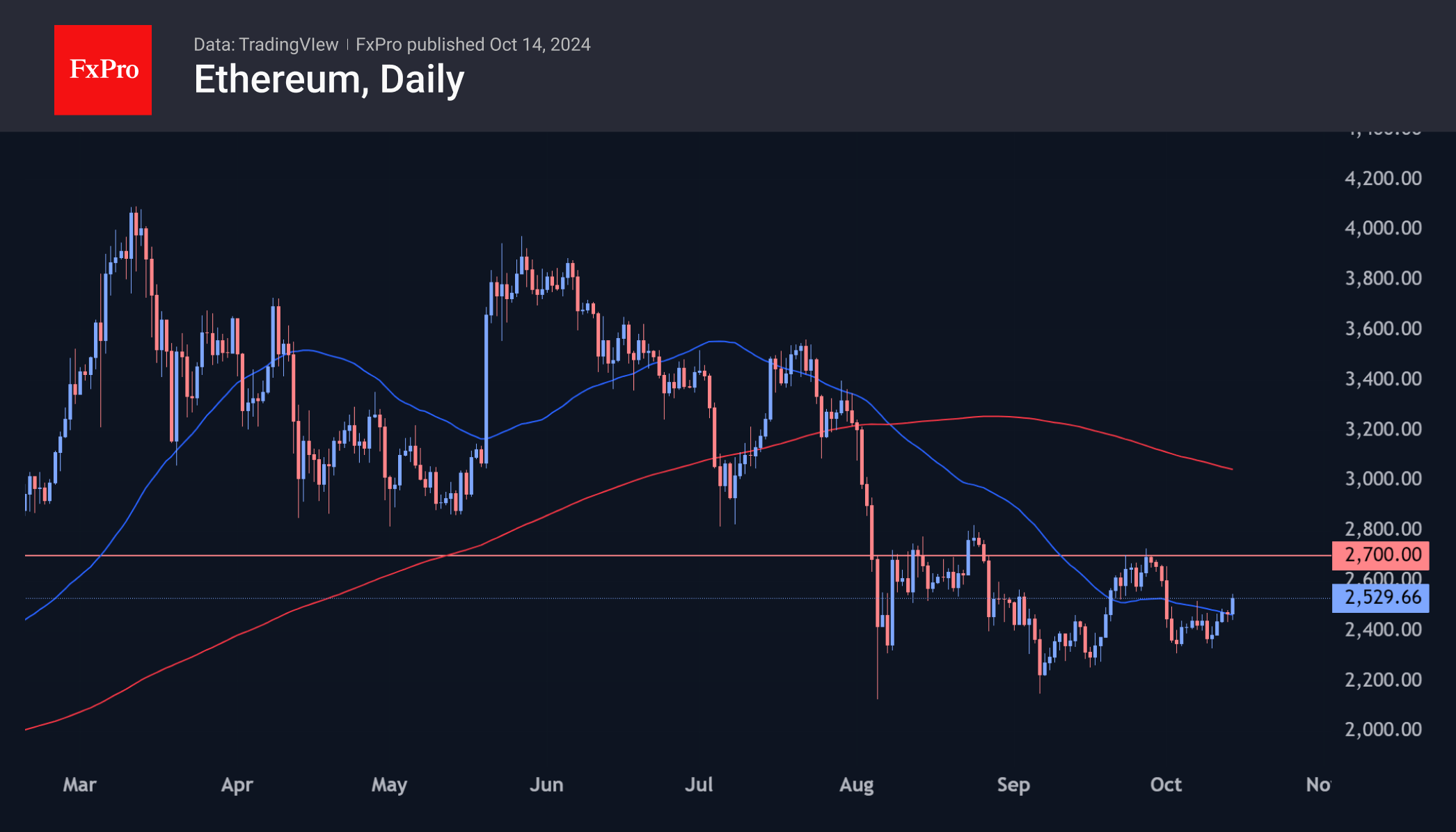

Bitcoin and Ethereum Are Trying to Break Resistance

Market Picture

The crypto market is sitting at $2.23 trillion, roughly back to levels of a week earlier, with two legs of growth—at the end of the day on Thursday and the start of trading on Monday. Sentiment has returned from fear to neutral territory (48), while sentiment in US stock indices is close to extreme greed.

Bitcoin broke above the $64K mark on Monday morning, accelerating intraday gains after breaking through its 200-day MA. This is a repeat of the momentum from a week earlier when the price failed to consolidate above that line. Looking back at the optimism in equities and the strong rally in BTC on the dip under $60K, we give more chances for growth development and a new test of $65K at the intersection of the round level and the upper boundary of the downward channel from March.

Ethereum climbed to $2,500, accelerating gains at the intersection of its 50-day MA on Monday. But this was not such a difficult task as this curve was pointing downwards. Should positive sentiment develop, the target for the bulls looks to be the $2,700 area—the highs at the end of September.

News Background

According to SoSoValue, inflows into the BTC-ETF last week totalled $308.8M after outflows of $301.5M a week earlier. Cumulative inflows since Bitcoin-ETFs were approved in January increased to $18.81bn (+1.7% for the week). In the Ethereum-ETF, net outflows over the past week declined to a paltry $5.2 million after outflows of $30.7 million previously. Net outflows since product approval rose to $558.9 million (+0.9% for the week).

Crypto whales with balances above 1,000 BTC have accumulated an additional 1.5 million coins over the past six months, CryptoQuant noted. Smaller investors have been selling BTC in the meantime. Whale’s growing balance sheet is setting up for a rally sooner rather than later.

The regulator’s attitude toward digital assets ‘is a disaster for the entire industry,’ SEC Commissioner Mark Uyeda said. He continued that the SEC ‘has not developed guidelines. As a result, the courts have done so and have issued various rulings.

MicroStrategy’s ultimate goal is to transform into a leading Bitcoin bank with a market value of $1 trillion, founder Michael Saylor said. MicroStrategy’s crypto reserves are valued at 252,220 BTC, with assets of approximately $15.5 billion.

Payment service Stripe has added USDC and USDP stablecoins as payment options on its checkout page. The launch of the service was made possible thanks to the cooperation with Coinbase, which was signed in June.

NZ Dollar Under Pressure as Services Data Disappoints

The New Zealand dollar is lower on Monday. In the European session, NZD/USD is trading at 0.6082, down 0.44%.

Services PMI contracts for seventh straight month

New Zealand’s economy has been struggling, and a key factor has been the contraction in the services sector. The services PMI remained steady in September at 45.7 following an upward revision in August. The PMI has now been stuck in contraction for seven straight months, with readings below the neutral 50 level.

The Reserve Bank of New Zealand chopped interest rates by 50 basis points last week, as the weak economy is in danger of tipping into a recession due to elevated rates. The RBNZ has been hawkish and even warned at recent meetings about possibly raising rates, but pivoted sharply in delivering an oversized cut.

The RBNZ had projected that it would not start lowering rates until mid-2025 but the weak economy and falling inflation were the drivers behind the rate cut. New Zealand releases third-quarter inflation on Tuesday with a market estimate of 2.3% y/y, compared to 3.3% in the second quarter.

Lower inflation is welcome news for the RBNZ, but weak inflation in China is not. In September, inflation dropped to 0.4% y/y, down from 0.6% in August and below the market estimate of 0.6%. Monthly, inflation eased to 0.0%, down from 0.4% and below the market estimate of 0.4%. Core CPI rose only 0.1%, its lowest level since February 2021.

China has a deflation problem, which could result in weaker economic growth and higher unemployment. That would dampen consumer demand and New Zealand would feel the pinch, as China is New Zealand’s largest export market.

NZD/USD Technical

- NZD/USD has support at 0.6051 and 0.5991

- There is resistance at 0.6112 and 0.6172

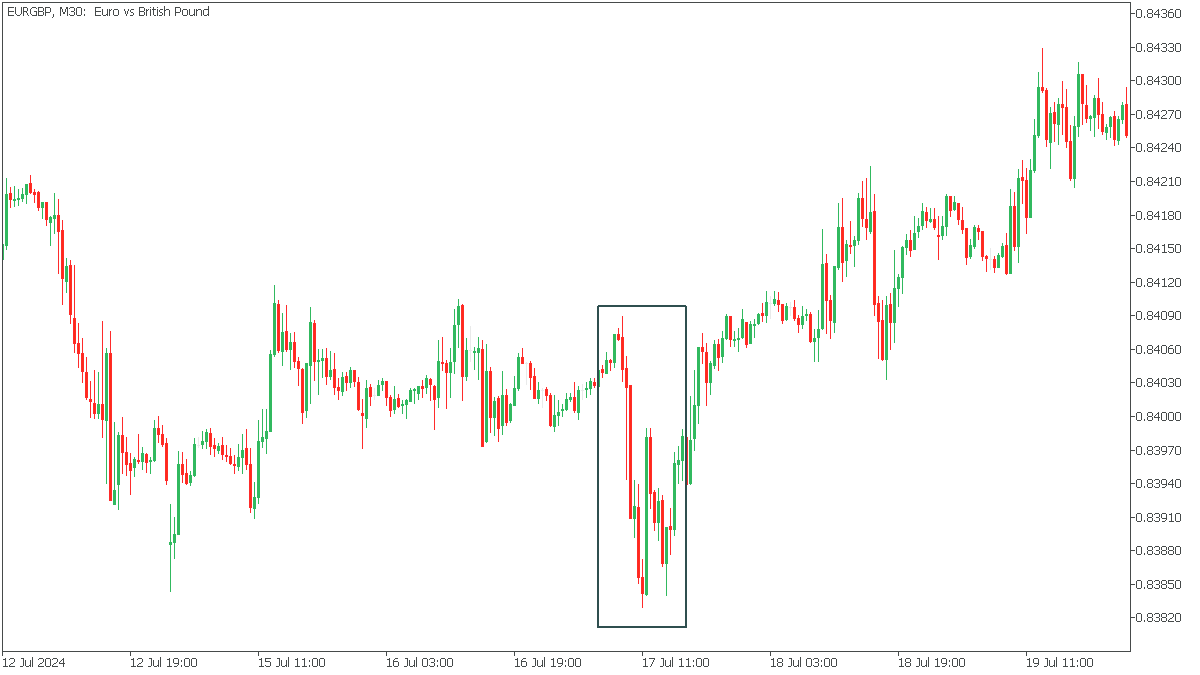

News of the Week (October 14—October 18): EURGBP Market Analysis

Watch EURGBP closely—key data could drive a big move!

The EURGBP pair, also known as the “Chunnel” by traders, is a widely traded currency pair that reflects the economic relationship between the Eurozone and the United Kingdom. The euro is mainly influenced by economic data from the major Eurozone countries such as Germany, France, and Italy, as well as the European Central Bank's interest rate and monetary policy decisions.

Conversely, the British Pound is shaped by UK domestic economic indicators such as inflation, employment, and GDP data. The Bank of England plays a key role in setting interest rates, and its decisions significantly impact the strength of the Pound.

UK Consumer Price Index (CPI) YoY, Oct 16, 8:00 (GMT+2)

The UK CPI is forecast to remain unchanged at 2.2% year-on-year. If the actual figure exceeds expectations and is higher, it will indicate that inflationary pressures in the UK are growing. This may prompt the Bank of England to consider keeping the rate at the current level, which will probably strengthen the GBP, and as a result, the EURGBP pair will decline.

On the other hand, if CPI data comes in worse than forecast and shows lower-than-expected inflation, this could indicate a slowdown in the UK economy, leading to a weaker Pound. This is likely to lead to an upward movement of the EURGBP pair.

The last time UK inflation beat analysts' expectations was July 17, 2024, causing EURGBP to fall sharply.

Eurozone Interest Rate Decision, Oct 17, 14:15 (GMT+2)

The upcoming Eurozone interest rate decision will result in a small cut from 3.65% to 3.4%. If the ECB cuts rates more than forecast, it could signal a cautious approach to economic recovery, signaling that the central bank is more concerned about the risks of stagnation or deflation. The euro will likely weaken in such a scenario, pushing the EURGBP pair lower.

However, if the ECB decides to cut rates less than expected or not at all, this could signal confidence in the resilience of the Eurozone economy. In this case, the euro could strengthen, leading to a rise in EURGBP.

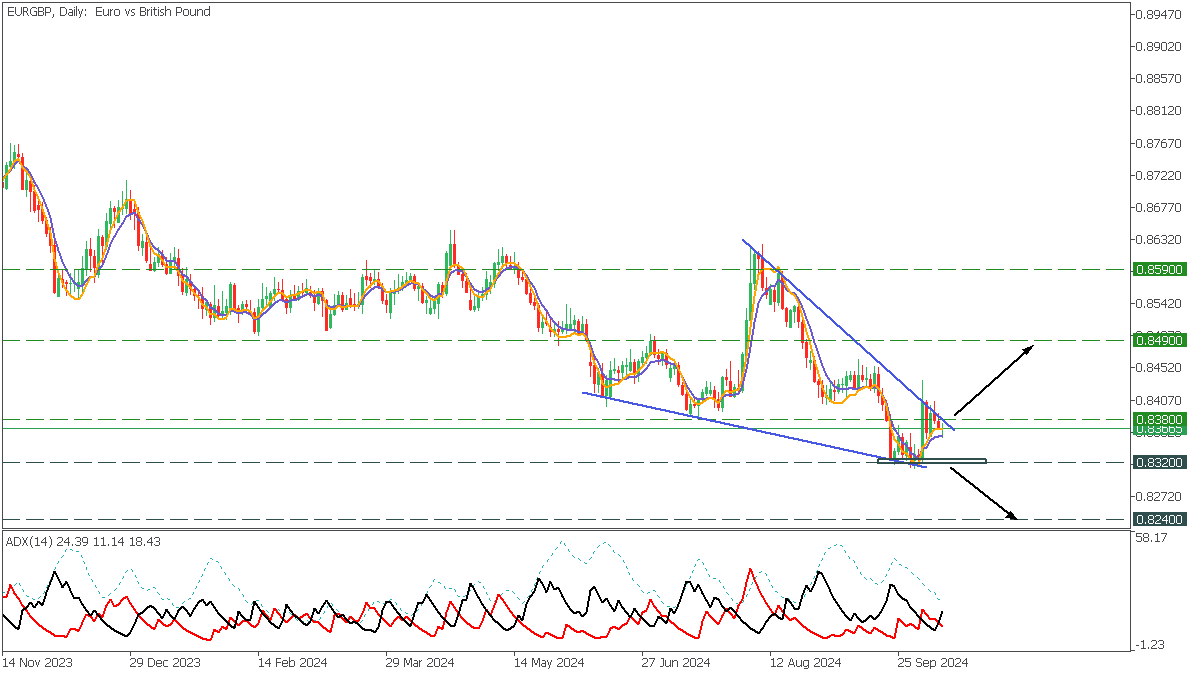

In the daily timeframe, the EURGBP formed a falling wedge pattern with a long-term bearish trend. The price reached crossed DEMA and TEMA but bounced off the upper trend line. At the same time -DI crossed +DI on the ADX Indicator, which is a bearish signal.

- If the price breaks the upper trendline above 0.8380, the upside will be to 0.8490;

- However, in case of a break below 0.8320 support, EURGBP will fall to 0.8240;

Copper Futures (HG_F) Elliott Wave Forecasting the Path

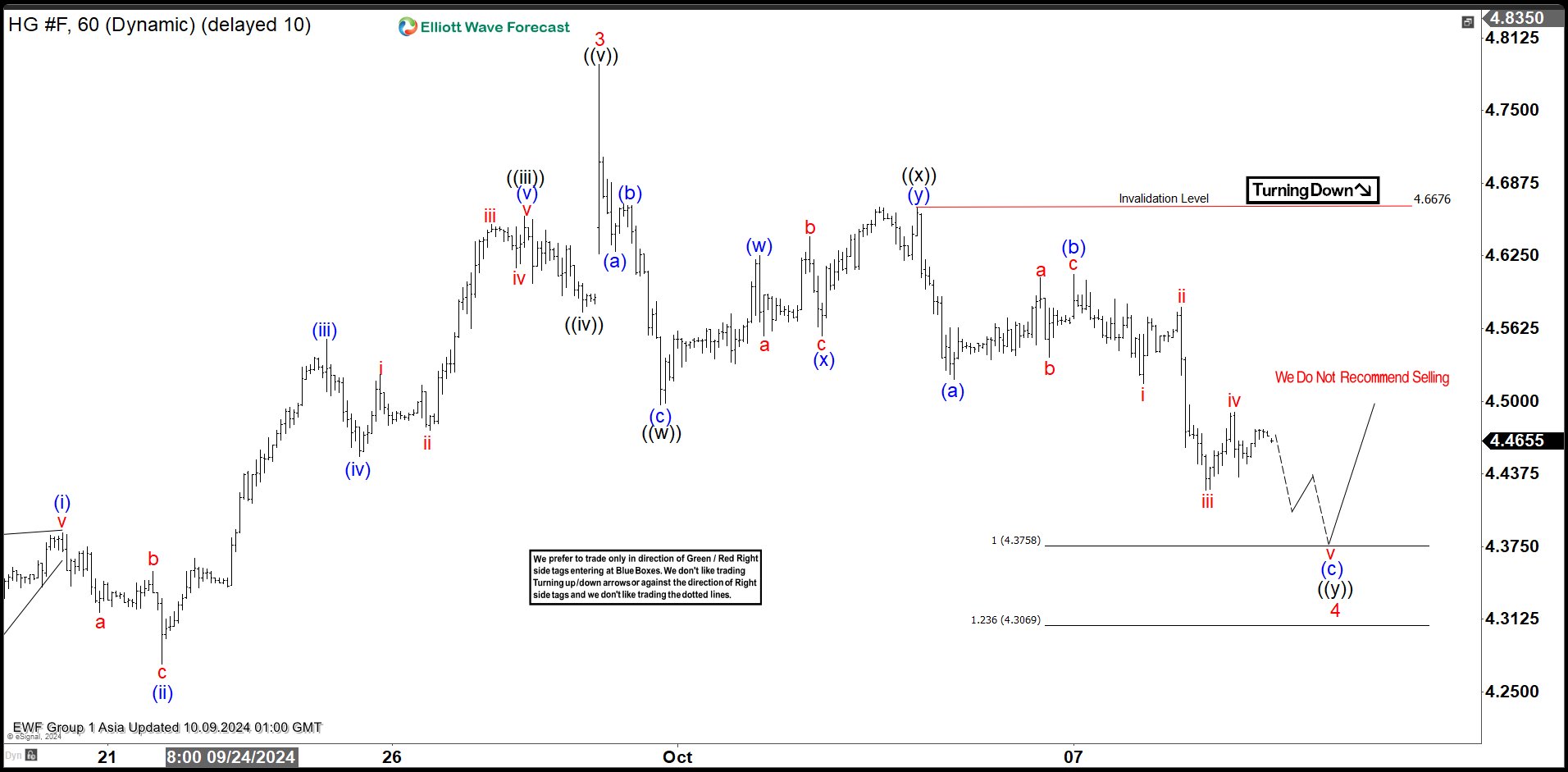

In this technical article we’re going to take a quick look at the Elliott Wave charts of Copper Futures HG_F, published in members area of the website. As our members know, Copper is showing impulsive sequences in the cycle from the 3.9230 low. Consequently we are favoring the long positions at this stage. The commodity has recently given us a 3-waves pull back, when buyers appeared right at the equal legs zone. We are going to explain Elliott Wave forecast further in this article.

Copper H1 Asia Update 10.09.2024

The current view suggests that the Copper commodity is doing a 4 red pullback. Structure of the correction is still incomplete, suggesting more short term weakness. We expect to see another leg down toward equal legs : 4.3758-4.3069 ( buyers zone). Once extreme zone is reached , we expect potential buyers to appear in that area, which could lead to a further rally towards new high or a three-wave bounce at least.

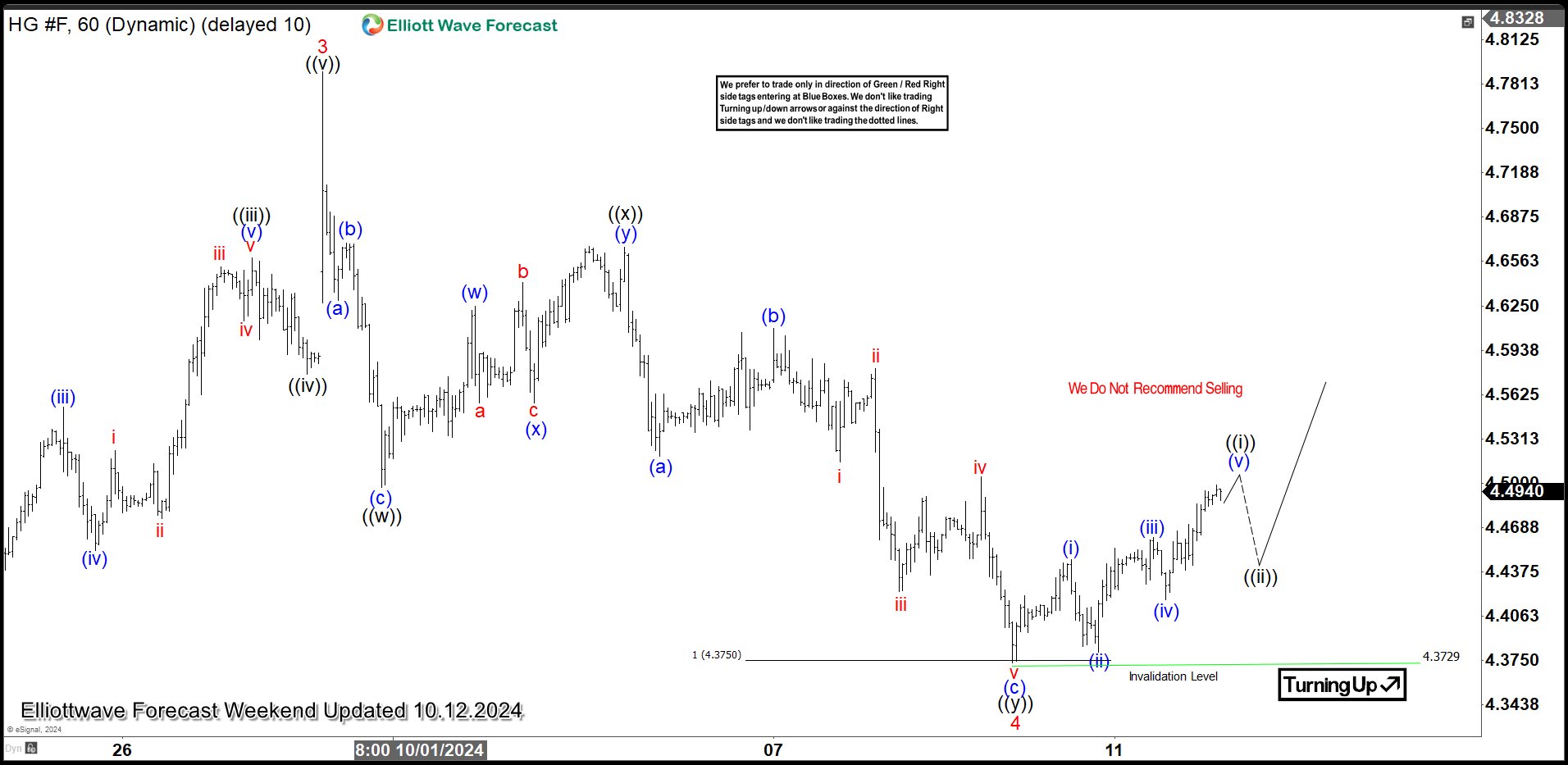

Copper H1 Asia Update 10.12.2024

The commodity made another wave down as we expected. The price has reached the extreme zone at 4.3758-4.3069 area. The commodity found buyers and made a rally from the Equal Legs-Buyers zone, completing pull back at the 4.3729 low. Copper can remain supported as far as the price stays above 4.3729 low.

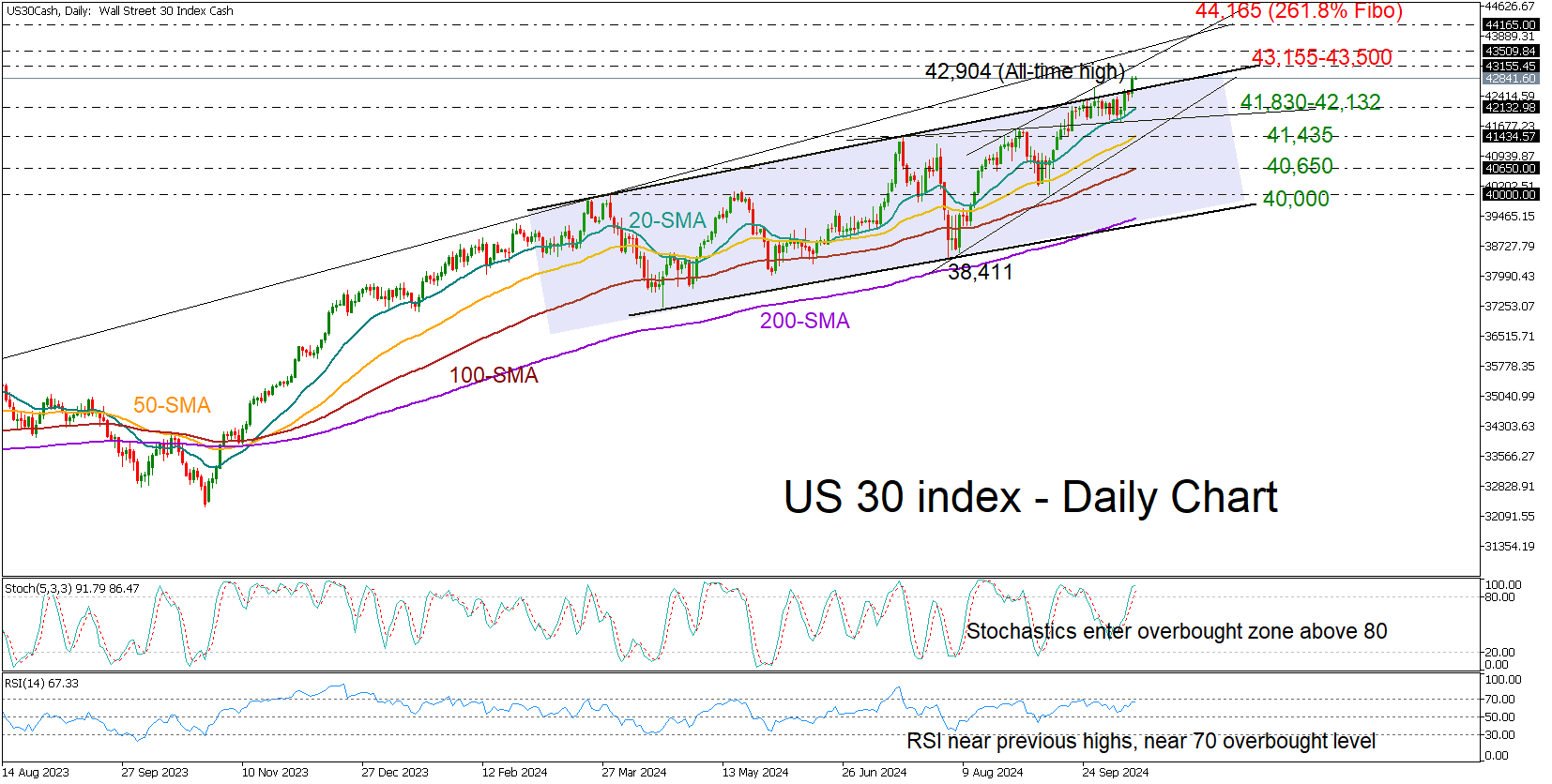

US 30 Index Celebrates Another Record High

- US 30 index strengthens uptrend to all-time high of 42,904

- Short-term bias is positive, but the way up may not be straight

The US 30 index (cash) hit an all-time high of 42,904 in less than a month on Friday and closed above the constraining line at 42,550, raising confidence that its record rally has more room to go.

Having bounced off its 20-day simple moving average (SMA), the bulls may face immediate resistance within the 43,155-43,500 constraining region given the overbought signals coming from the RSI and the stochastic oscillator. If not, then the uptrend could accelerate towards the 44,165 zone, where the 261.8% Fibonacci extension of the previous downfall is placed.

Alternatively, if upside forces fade out, the 20-day SMA could provide extra fuel near 42,132 with the help of the 41,830 territory. Slightly lower, the 50-day SMA might also act as support as it did back in September near 41,435. Should the bears win the battle there, the decline could continue towards the 100-day SMA at 40,650.

In brief, the latest bounce in the US 30 index reflected that the bulls are still in town, though there are still some barriers nearby, with the next challenge expected to emerge near 43,155-43,500.

China’s export grow slows to 2.4% yoy, imports edge up 0.3% yoy

China's export and import data for September painted a weaker-than-expected picture of the nation's trade performance. Exports grew by just 2.4% yoy to USD 303.7B, well below expectations of 6.0% yoy and down from the 8.7% yoy rise in the previous month. Imports edged up a modest 0.3% yoy to USD 222B, missing expectations of 0.9% yoy increase and lower than August's 0.5% yoy rise. Trade surplus narrowed to USD 81.7B, smaller than the expected USD 89.8B and down from USD 91.0B in August.

Breaking down the data by region, exports to the US, China’s largest trading partner, rose by 2.2% yoy, while imports saw a stronger 6.7% yoy growth. Trade with ASEAN remained more robust, with exports up 5.5% yoy and imports climbing 4.2%yoy. However, exports to the EU edged up by only 1.3%, while imports from the bloc fell by -4% yoy. Trade with Russia was mixed, with exports surging by 16.6% yoy, but imports declining by -8.4% yoy.

Customs spokesman Lu Daliang attributed the weaker export growth to “short-term incidental factors,” including frequent typhoons in key port cities, a high base from last year, and ongoing global shipping congestion. Lu noted that the peak export season for some Chinese products typically seen in Q3 had been moved forward by more than a month this year due to the shipping delays.

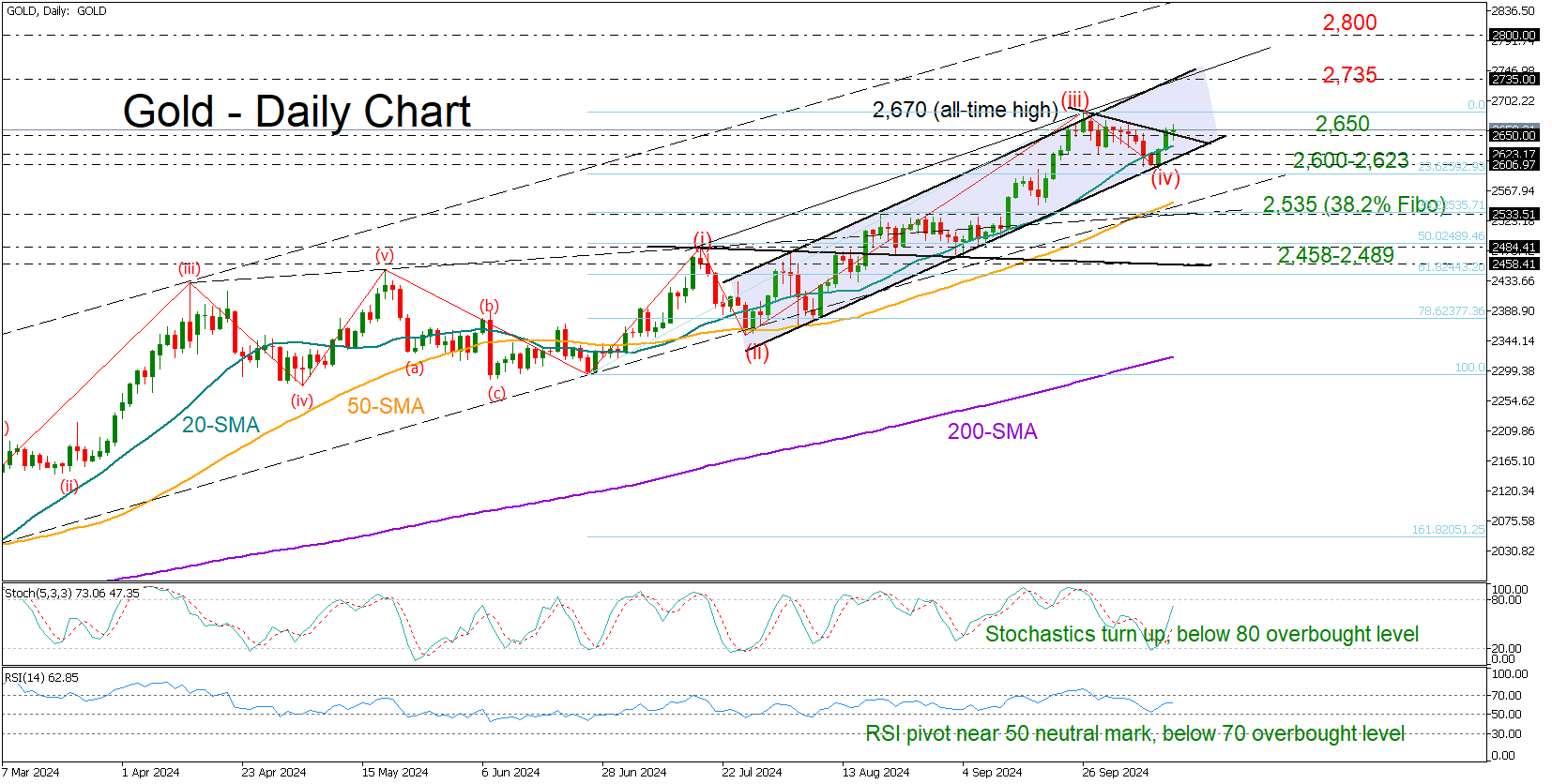

Gold Might Take Another Bullish Shot

- Gold enters a new bull run; shifts spotlight to all-time high

- Technical signals point to more upside; close above 2,650 needed

Gold started a new bullish corrective phase near the 2,600 level last week, adding extra credence to its upward trend that has been active for more than two months.

On Monday, the price climbed to 2,666, surpassing the short-term falling trendline from September’s peak that the bulls must break to reach the top of 2,670 or achieve a new record high near the upper band of the channel at 2,735. The latter coincides with the 161.8% Fibonacci extension of the previous downfall. If the rally continues above it, the next barrier could occur within the 2,800-2,850 region and near the resistance line of the broad upward-sloping channel.

Based on the RSI and stochastic oscillator, it appears that the current rebound is still at an early stage. Encouraging trend signals persist as well. If the Elliot pattern in the chart is correct, the precious metal might have one more upleg to complete before it shifts to the sidelines.

However, if the price doesn’t close above 2,650, it may drop and find support near the 20-day SMA and the channel’s support trendline at 2,623. The 2,600 area may also be scrutinized, and if the bears break through that level, the sell-off could accelerate towards the 50-day SMA and the 38.2% Fibonacci retracement of the June-September uptrend at 2,535. Failure to pivot there could cause another rapid fall towards the 50% Fibonacci mark of 2,489 and the flat constraining line at 2,458.

Summing up, gold is expected to continue its bull run in the short-term. In the meantime, a close above 2,650 might be necessary to bolster buying appetite towards the top of the bullish channel.

S&P 500 Reaches Another Record High

As shown by the S&P 500 chart (US SPX 500 mini on FXOpen), the leading US stock index set its 45th record of the year, closing above 5800 on Friday. This marks the fifth consecutive week of growth, with the index up more than 22% since the start of the year.

According to Reuters, the bullish market sentiment is driven by the start of Q3 earnings season, with companies possibly issuing bolder forecasts due to the beginning of the Fed’s rate-cutting cycle.

What are the prospects for the index until the end of 2024?

A technical analysis of the daily S&P 500 chart (US SPX 500 mini on FXOpen) shows:

In 2024, price action has been contained within three relatively narrow ascending channels (shown in blue), where:

→ The first two channels remained valid for at least 80 candles, and the third has now reached 30 candles;

→ The channels have similar slopes and widths;

→ Drawing lines through the high of Channel 1, the high and low of Channel 2, and the low of Channel 3 forms a larger channel (shown in orange).

If the bullish sentiment persists, the S&P 500 (US SPX 500 mini on FXOpen) may continue to rise within the third blue channel towards the upper orange line.

However, several factors could significantly impact the market before the year's end: → Labour market data, as well as Fed decisions and comments;

→ US presidential elections and budget approval;

→ Company earnings and forecasts that fall well below market expectations.

Goldman Sachs analysts predict that the S&P 500 could reach 6,000 by the end of 2024.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.