Sample Category Title

Earnings Season Kicks Off Strong, Oil Markets on Edge

China didn’t pull out the fiscal bazooka on Saturday, but said that there will be a significant bond issuance to help reverse the deepening property crisis and local governments. Israel didn’t attack Iran but some reports hinted that the Israeli army could be narrowing their targets on military and energy infrastructure. As such, crude oil kicked off the week downbeat. The barrel of US crude is trading below the $75pb mark in the early ours of Monday trading, and Brent oil consolidates near $78pb. The short-term risks remain alive; there could be a sudden spike in oil prices in case the Israeli attack on Iranian energy facilities materializes. But the careful steps from the Chinese government regarding their stimulus plans will likely keep the medium to long run investors on hold.

Xi doesn’t like market euphoria and investors don’t like the fact that the ample monetary stimulus may not be channelled toward the right places in the absence of an efficient and comprehensive fiscal package. But both agree that China needs stimulus to overcome the deepening property crisis and fight deflation. The figures released during the weekend showed that consumer price inflation in China was flat in September, while the decline in producer prices accelerated to 2.8% y-o-y. The stock markets gave a mild reaction to the avalanche of news and data. The CSI 300 is up by 1.50% at the time of writing. The index sank last Friday into the bearish consolidation zone on the latest rally triggered by the news of major monetary stimulus. We will probably see the volatility and the latest gains fade. The Hang Seng index, on the other hand, is down by around 0.40% today but holds ground near a minor 23.6% Fibonacci retracement. The index is still in a bullish trend but gains here will probably slow down as well. China related commodities, like copper and iron ore futures are mixed this morning, swinging between hope that China hasn’t got an option but to do whatever it takes to reverse the fortunes, the AUDUSUD is consolidating near the 50-DMA and the major 38.2% Fibonacci retracement, near the 0.6720 level, that should distinguish between the actual bullish trend and a medium-term bearish reversal.

USD extends gains

Friday’s US producer price data came in mixed. The monthly figures were lower than the expectations but the yearly figures were stronger than expected, and the core PPI advanced to 2.8%. The figures didn’t change the November expectations regarding what the Federal Reserve (Fed) would do... the expectation is that the Fed will likely cut its rates by 25bp with a nearly 87% chance assessed to it. But it becomes clearer by the day that the Fed won’t attempt another acrobatic move on its rates in the coming months. The US dollar consolidates and should further extend gains as the other major central banks are set to deliver dovish decisions.

In this context, the European Central Bank (ECB) is expected to announced another 25bp cut on Thursday – as the September CPI should confirm that headline inflation in the Eurozone fell below the bank’s 2% policy target a few hours before the decision. The EURUSD pulled out the major 38.2% Fibonacci support last week and extends losses within the medium term bearish consolidation zone. The next bearish target stands near 1.0875, the 200-DMA, that will either give support to the pair on the back of a cautious cut (due to concerns around sticky core inflation), or clear that support on the back of a dovish cut. Lagarde will tell.

Across the Channel, the British CPI due Wednesday is expected to confirm that the British inflation has also come below the Bank of England’s (BoE) 2% target, but core inflation is still near 3.5%. The BoE Governor Bailey had recently told investors that the bank is about to get ‘more aggressive’ on its rate policy – a comment that had triggered an aggressive selloff in pound sterling. This week’s inflation numbers could give more substance to Bailey’s comments and send Cable below the 1.30 mark, but services inflation will say the last word.

Earnings season kicks off on a positive note

The S&P500 finished last week on a fresh record high as the first big bank earnings came in better than expected. JPM jumped more than 4% and Wells Fargo rallied more than 5% after their Q3 results beat estimates. More bank earnings are due this week along with Netflix, TSM and ASML results.

Elsewhere, Tesla fell nearly 9% on Friday after the company failed to deliver enough details and an encouraging timeline for its robotaxi at last Thursday’s reveal. It’s clear that their robotaxi is not ready to hit the streets yet and that Tesla is not yet bringing any revolution to the world of robotaxis. And provided that the dream of robotaxis was what was keeping investors in appetite since April – as the EV sales are clearly declining across the globe – there is little reason to keep the positive trend going in Tesla. The shares will probably give back to robotaxi gains until further notice. The crumbling robotaxi hopes for Tesla sent Uber and Lyft around 10% higher on Friday.

Dollar Index With Strong Support at 101.80 -102

Today, some traders may still be away due to Columbus Day in the US, though the stock market is open while the bond market is closed. But this could still lead to thinner liquidity. The most important event this week will likely be the ECB interest rate decision on Thursday, but before that, we have UK, CAD and New Zealand inflation reports. In the US, the key focus will be retail sales and a few FOMC speakers.

Regarding the markets, we saw some recovery in stocks last week, and this trend could extend further into the start of this week. It could also mean that sooner or later, the US dollar may enter a corrective phase, as discussed last week. We mentioned that the first impulse from September lows is likely facing resistance around the 103 level on the Dollar Index so pullback wouldn't be surprising. In such a case, the 101.80 to 102.30 zone will be key support to watch for a potential new resumption higher.

https://www.youtube.com/watch?v=tLZvpTEpj2U

Chinese Stock Markets This Morning Trade Volatile

Markets

The US yield curve finished last week with a little steepening. Net daily changes varied between -0.2 bps (2-yr) to +5.2 bps (30-yr), underpinned by second-tier data including decelerating and slightly below-consensus September PPIs. October consumer confidence (U. of Michigan) missed the bar as well. The headline index fell to 68.9 from 70.1 with both the current assessment and outlook deteriorating. The 1-yr ahead inflation gauge picked up from 2.7% to 2.9%, the 5-yr one eased as expected to 3%. German yields closed little changed due to a late-session swoon that erased much of the 4-5 bps gains earlier on the day. Major currencies were little changed against the dollar amid US markets sleepwalking into a long weekend. A healthy risk appetite (stocks 0.3-1% higher) was the main force pushing the likes of the NOK and SEK as well as cyclicals such as the Aussie & kiwi dollar a little higher. China’s yuan strengthened a bit in the run-up to a highly anticipated announced by the country’s finance minister on Saturday. After the economic planning agency underwhelmed earlier in the week, hopes ran high for Lan Fo’an to come big this time – to the tune of CNY 2tn. But while promising further steps to support the property sector and hinting at greater borrowing, investors were left in the dark by not putting a price tag on it. Chinese stock markets this morning trade volatile, swinging from gains to losses back to gains of currently 2.3% (CSI300). After the barrage of (pledged) fiscal and monetary measures in a short period of time, markets seem to give the government the benefit of the doubt. The need for a growth supporting policy pivot is increasingly apparent following another poor inflation reading for September. Consumer prices rose a mere 0.4%, undershooting the August-matching 0.6% consensus. Services inflation came in at only 0.2% y/y while core inflation barely stayed positive (0.1%, lowest since February 2021). Producer prices ventured deeper in negative territory (-2.8% from -1.8% and vs -2.6% expected). Factory inflation has been negative for two years straight (!) now. The yuan gapped lower at the open but pared losses in the meantime to USD/CNY 7.07. US markets are closed today for Columbus Day but a speech by Fed’s Waller on the economic outlook is worth watching. An otherwise empty European calendar paves the way for technically insignificant trading ahead of other events this week, including the ECB policy meeting. A 25 bps cut which was ruled out after the September meeting is now all but certain after disastrous PMIs and inflation numbers confirming ongoing disinflation.

News & Views

Rating agency Moody’s late Friday affirmed Belgium’s credit rating at Aa3 but changed the outlook from stable to negative. The rating agency said the decision to change the outlook reflects the risks that the next government will be unable to implement measures that would stabilize the government debt burden. According to Moody’s, the previous government made some small fiscal consolidation efforts, but they were not structural in nature. In the absence of a large fiscal consolidation programme, Moody’s says that debt will continue to rise due to the material structural increase in expenditures in recent years and persistent spending pressure. It expects the political economy of deficit and debt reduction may become more challenging in the future because of structural headwinds to fiscal consolidation. A large fiscal consolidation effort will require effort at all levels of government. In this respect Moody’s says that Belgium lacks intergovernmental coordination mechanisms to achieve this effort.

Rating agency Fitch on Friday cut the outlook on France’s rating from stable to negative. It affirmed the country’s rating at AA-. Moody’s sees a difficult fiscal policy ahead, as fiscal risks have increased since the previous review. This year’s projected fiscal slippage is placing the country in a worse starting position. Fitch expects wider deficits leading to a steep rise in debt toward 118.5% of GDP in 2028. High political fragmentation and a minority government complicate the country’s ability to deliver on sustainable fiscal consolidation. The government presented a sizeable package to bring the deficit to 5.0% of GDP by 2025 but some of the measures are temporary. All measures are worth €60 bn (or 2% of GDP) but the agency included only a part due to political uncertainty and implementation risks. The 2024 deficit is expected to widen to 6.1% GDP which exceeds Fitch’s forecast of 5.1%. Fitch raised the fiscal deficit for 2025 and 2026 to 5.4% and doesn’t expect the government to meet its revised deficit forecast to bring the deficit to 3.0% by 2029. Fitch expects the debt to GDP ratio to rise to 116.3% by end 2026.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) still is a source of concern, but very weak PMI’s and soft comments of Lagarde (and other MPC members) suggest the ECB is likely to step up the pace of easing with an October cut. Spill-overs from strong US data prevented a test of the 2.0% barrier. 2.00-2.35% might serve as a ST consolidation range.

US 10-y yield

The Fed kicked off its easing cycle with a 50 bps move. Turning he focus from inflation to a potential slowdown in growth/employment made markets consider more 50 bps steps. Strong US September payrolls suggest the economy doesn’t need aggressive Fed support for now, but the debate might resurface as the economic cycle develops. 3.60% acted as strong support before a rebound (and resumption of the steepening trend) kicked in.

EUR/USD

EUR/USD twice tested the 1.12 big figure as the dollar lost interest rate support at stealth pace. Bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) partially offset some of the general USD weakness. After solid early October US data, the dollar regained traction, with EUR/USD breaking the 1.1002 neckline. Targets of this pattern are near 1.08.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness was indicated to be further unwound gradually. The economic picture between the UK and Europe also (temporarily?) diverged to the benefit of sterling, pulling EUR/GBP below 0.84 support. Dovish comments by BoE Bailey ended by default GBP-strength. Uncertainty on the UK budget to be released end this month is becoming an additional headwind for the UK currency.

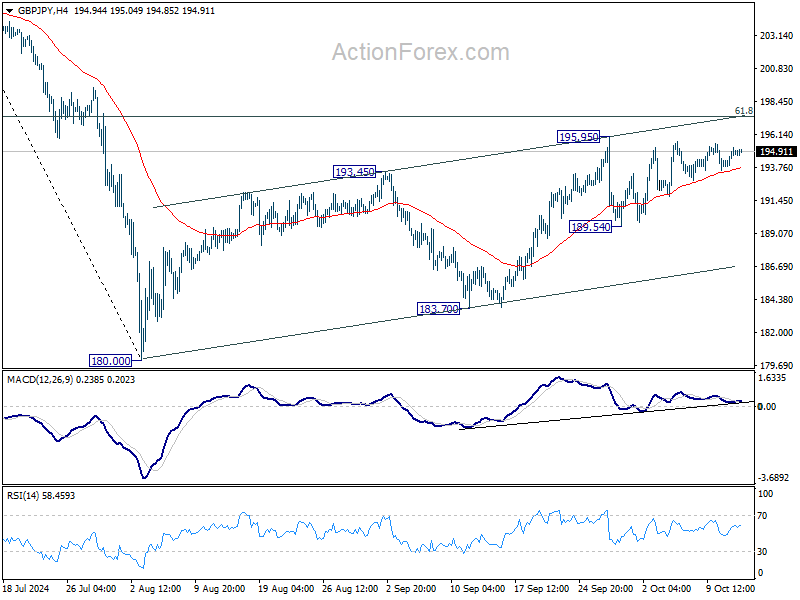

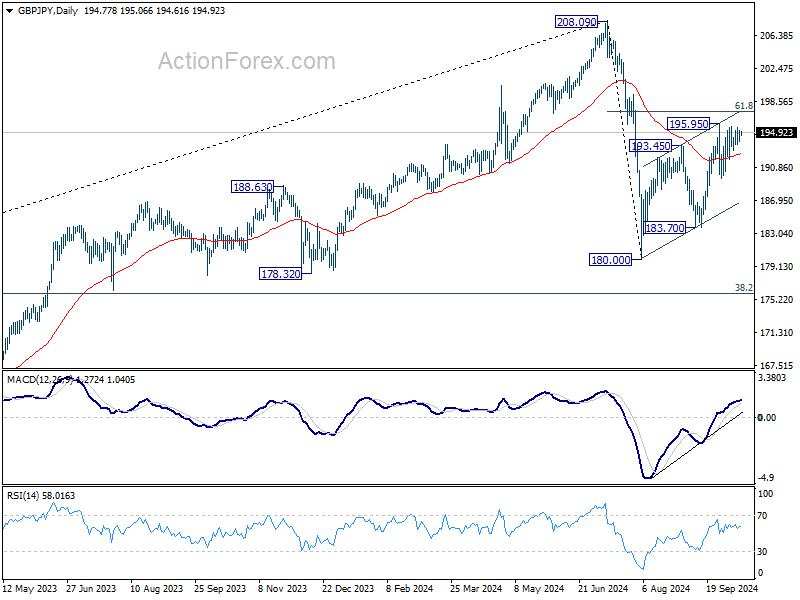

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.07; (P) 194.66; (R1) 195.47; More...

Intraday bias in GBP/JPY stays neutral at this point. On the upside break of 195.95 will resume whole rise from 180.00 to 61.8% retracement of 208.09 to 180.00 at 197.35 next. On the downside, break of 189.54 will turn bias back to the downside for 183.70 support instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

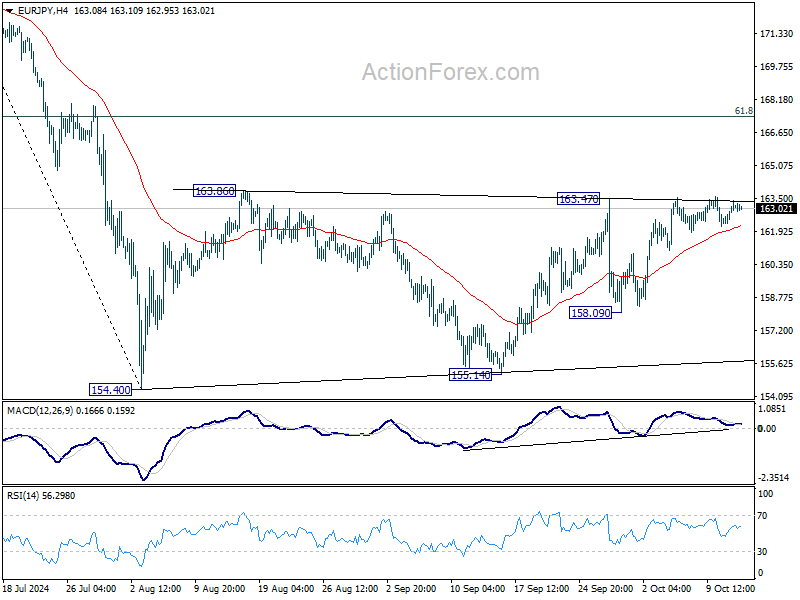

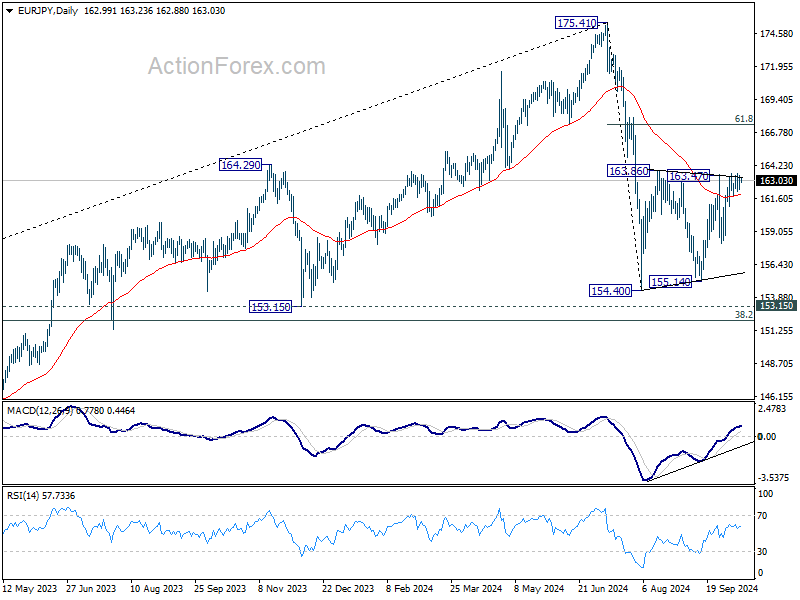

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.40; (P) 162.91; (R1) 163.63; More....

Intraday bias in EUR/JPY remains neutral for the moment. On the upside, firm break of 163.47/86 resistance will resume the rebound from 154.40 to 61.8% retracement of 175.41 to 154.40 at 167.38. On the downside, break of 158.09 will bring deeper fall back to 154.40/155.14 support zone instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

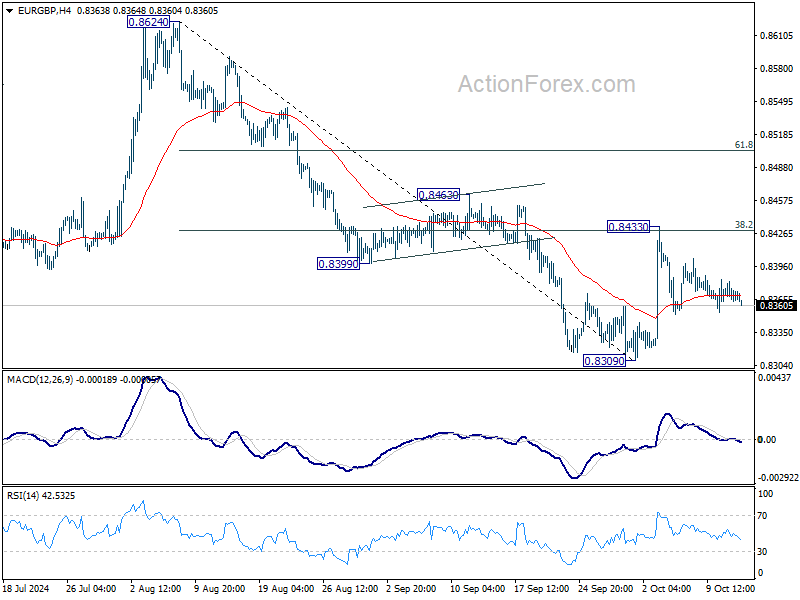

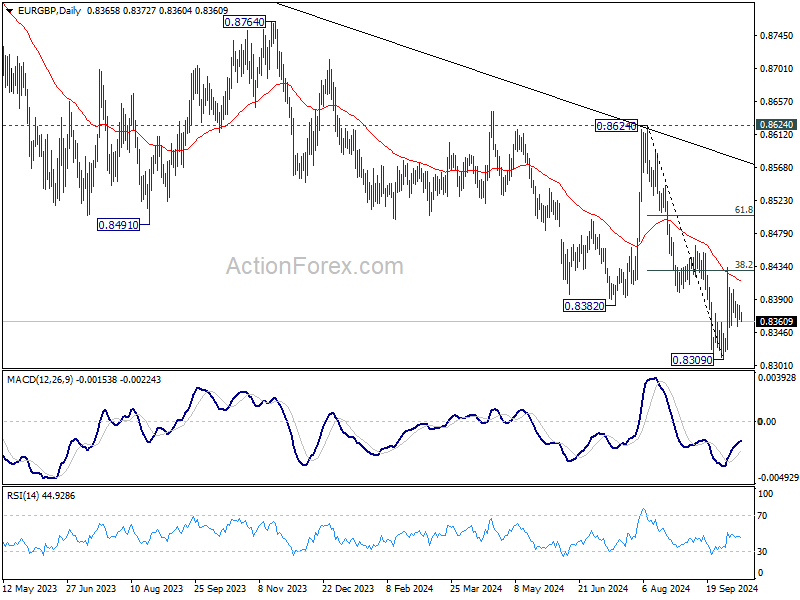

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8362; (P) 0.8372; (R1) 0.8380; More...

Intraday bias in EUR/GBP remains neutral and outlook is unchanged. Further decline is in favor, and firm break of 0.8309 will resume larger down trend to 0.8201 key support next. However, decisive break of 38.2% retracement of 0.8624 to 0.8309 at 0.8429 will pave the way to 61.8% retracement at 0.8504 and possibly above.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound.

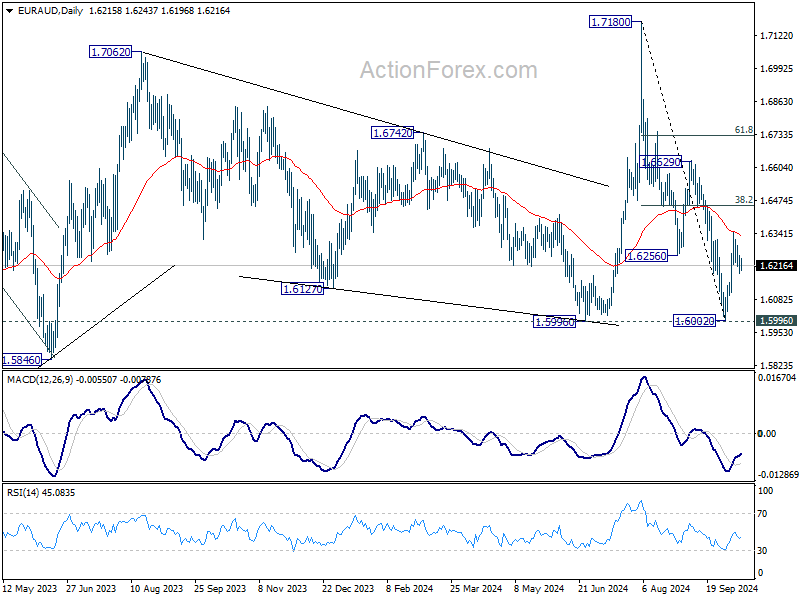

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6172; (P) 1.6214; (R1) 1.6242; More...

Intraday bias in EUR/AUD Is mildly on the downside at this point. Rebound from 1.6002 could have completed at 1.6351. Deeper fall would be seen back to retest 1.6002 low. On the upside, though, above 1.6351 will resume the rebound from 1.6002 to 38.2% of 1.7180 to 1.6002 at 1.6452.

In the bigger picture, as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

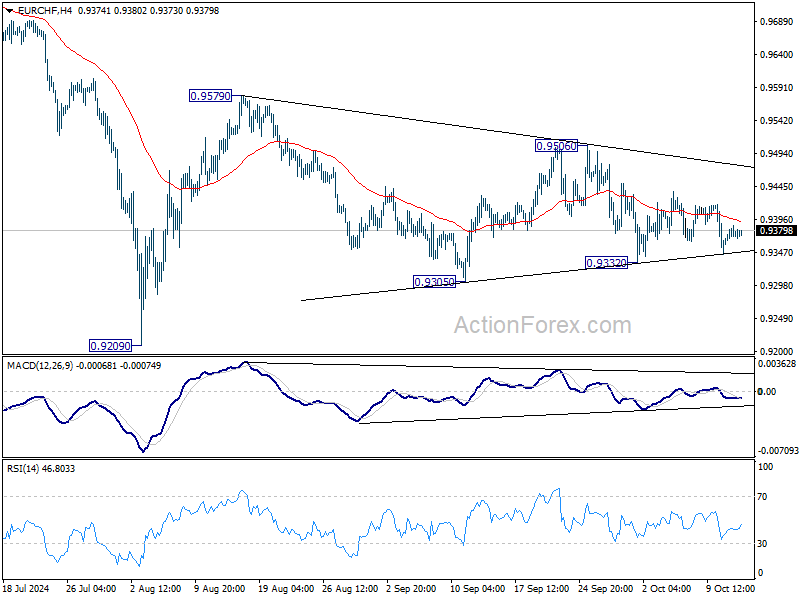

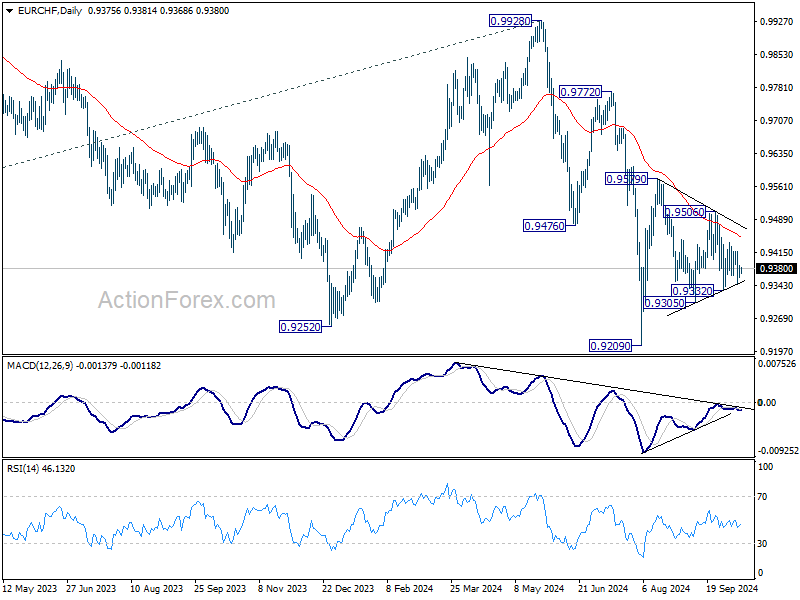

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9357; (P) 0.9373; (R1) 0.9391; More....

Intraday bias in EUR/CHF remains neutral at this point. On the downside, break of 0.9332 will resume the fall from 0.9579 towards 0.9209 low. On the upside, break of 0.9506 will turn intraday bias to the upside for 0.9579 resistance and above.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Thursday’s ECB Meeting Main Event This Week

In focus this week

Today is set to be a quiet start of the week, without major market movers on the data front.

We continue to await Israel's response to the Iranian missile attack on 1 October, which will determine whether we will see a further escalation of the conflict in the region. According to the American news channel NBC, unidentified US officials believe that Israel will be targeting Iranian military and energy infrastructure. Tensions continue as Hezbollah stroke Israel with a drone bombing south of Haifa where four IDF soldiers were killed and about 67 people injured. Israel made attacks in Gaza near a school which is housing internally displaced persons. Minimum 15 people were confirmed dead.

On the data front we receive final inflation data from Sweden on Tuesday and the ZEW index from Germany. On Wednesday UK CPI is due for release. On Thursday, focus will be on the ECB meeting where we expect the ECB to deliver yet another rate cut of 25bp, bringing the deposit rate to 3.25%. Also on Thursday, we will receive the final September inflation data from the euro area, and the Central Bank of Turkey will announce their rate decision. To round off the week, we get Japanese inflation data and GDP data out of China on Friday.

Economic and market news

What happened overnight

China began large-scale military exercises around Taiwan. This comes after Taiwanese President Lai Ching-te's National Day speech last week, where he asserted his country's sovereignty. China calls the exercises a "stern warning". Officials from the US government condemned the drills and said that there was no justification for them.

What happened over the weekend

Fitch downgraded the outlook of France from 'stable' to 'negative' on the back of the fiscal risks and the more negative view on the fiscal situation in France made by the new French government, where the budget deficit for 2024 is expected to be 6.1% and the budget deficit for 2025 is expected to be 5% resulting in rising debt to GDP, which Fitch expects to be more than 118% of GDP by 2028. However, they have not downgraded France from AA- yet, but has affirmed the rating although their model rating suggests an A+ rating. The 10Y spread between France and Germany is testing the 80bp level and the risk is that it would go towards 90bp even though this is a very wide level seen in a historical context.

In China, September CPI inflation came in lower than expected at 0.0%|0.4% m/m|y/y (consensus: 0.4%|0.6%, prior: 0.4%|0.6%). Core inflation came in at 0.1%, down from 0.3% in August. The print suggests that deflationary pressures increased further in September, which comes from weak domestic demand. The Chinese finance minister Lan Fo'An spoke about fiscal stimulus at an awaited press conference Saturday, saying that the government is looking at additional ways to boost the economy, but failed to speak about size or timing of the measures, which investors and analysts were hoping for. The market reaction in Chinese equities were mixed as CSI 300 increased by 0.3%, however the Hang Seng index declined 1.7% in early trading Monday. Brent Crude oil fell 1.8% in Early trading Monday, which could be a reaction to deflation fears in China.

What happened on Friday

In the US, September PPI came out slightly below expectations, but core PPI (which excludes the decline that we saw in energy prices during September) was close to consensus expectations. There was some moderation across both goods and services producer price inflation. Overall, this week's CPI and PPI data was, at the very least, not alarming for the Fed and the disinflationary process remains well underway.

The University of Michigan consumer sentiment survey fell to 68.9 in October from 70.1 in September, in contrast to expectations of a rise to 70.8. The one-year inflation expectations ticked slightly higher to 2.9% from 2.7%, which could likely be driven by the latest up-tick in oil/gasoline prices.

In Germany, we got the final inflation data from September, which showed still elevated underlying inflation. The 'LIMI' measure of domestic inflation fell to 4.82% y/y from 4.95% in August, which is another move in the right direction, but the level remains high.

FI: 10Y US Treasury yields continued to rise last week and are once again trading above 4% as the market has been repricing monetary policy expectations in the US. This has had a spillover effect on Europe, where there has also been a solid repricing and a rise in yields, where the 10Y German government bond yield has risen almost 25bp since early October. Furthermore, the Bund ASW-spread ended below 25bp on Friday. The 10Y spread between France and Germany is testing the 80bp level and given the negative rating action last week there is risk for a further widening.

FX: Last week in FX markets was characterised by USD strength and underperformance in the cluster of commodity and cyclically sensitive currencies with CAD and NZD leading the losses. In the Scandies, both SEK and NOK staged a late-week comeback although EUR/NOK and EUR/SEK still entered the weekend around 11.70 and 11.35, respectively. Finally, the JPY has come under renewed pressure amid the rise in global yields and USD/JPY is now back close to the 150-mark.

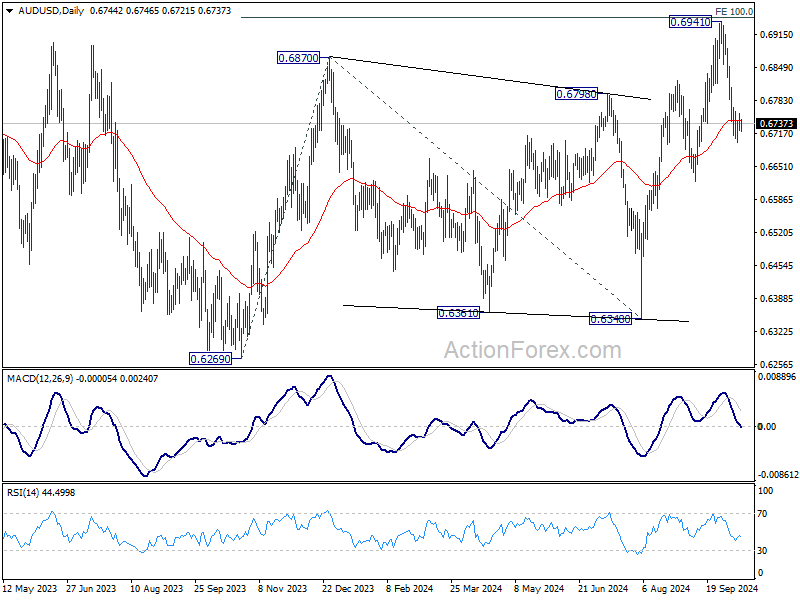

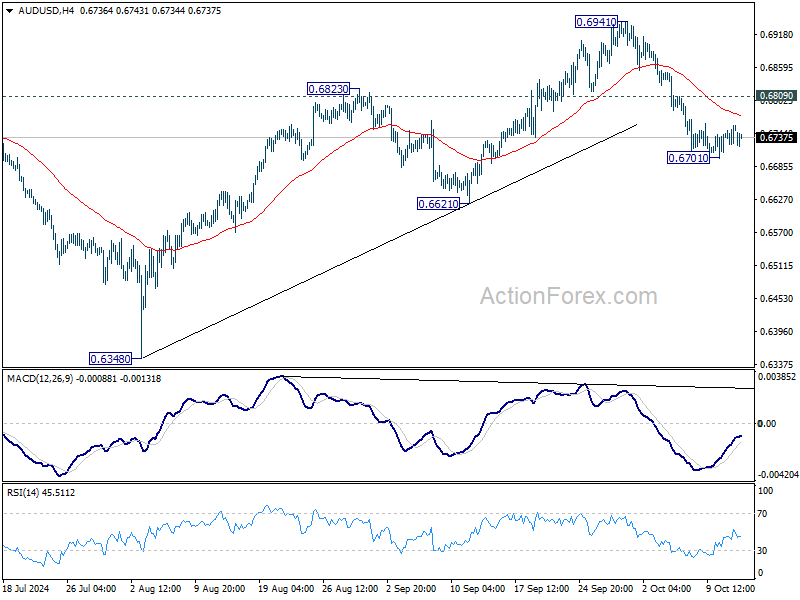

AUD/USD Daily Report

Daily Pivots: (S1) 0.6731; (P) 0.6745; (R1) 0.6766; More...

Intraday bias in AUD/USD remains neutral for consolidations above 0.6701 temporary low. Further decline is expected as long as 0.6809 minor resistance holds. On the downside, break of 0.6701 and sustained trading below 55 D EMA (now at 0.6743) should confirm rejection by 0.6941 fibonacci level. Intraday bias will be back on the downside for 0.6621 support next. On the upside, however, break of 0.6809 minor resistance will bring retest of 0.6941 high instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.