Sample Category Title

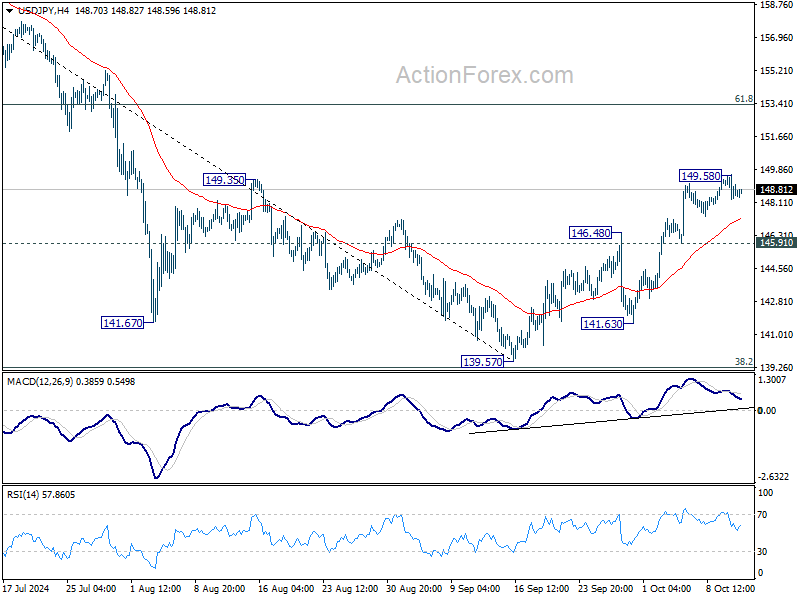

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.04; (P) 148.79; (R1) 149.33; More...

With a temporary top formed at 149.58, intraday bias in USD/JPY is turned neutral first. Further rally is expected as long as 145.91 minor support holds. Rise from 139.57 is s seen as the second leg of the corrective pattern from 161.94. Break of 149.58 will target 61.8% retracement of 161.94 to 139.57 at 153.39.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Disbelief

Oops. Inflation in the US came in hotter-than-expected in September, both on monthly and yearly basis. The headline inflation eased less than expected from 2.5% to 2.4%, while core inflation unexpectedly ticked higher from 3.2% to 3.3%. Nothing looked encouraging in that inflation report for the Federal Reserve (Fed) doves. Some investors found a little comfort in jump in the weekly jobless claims data released at the same time than the CPI report. That triggered a period of hesitation between those who wanted to believe that the Fed’s focus on the health of jobs market could continue even if inflation behaves undesirably. And interestingly, some Fed officials seemed alarmingly little concerned in the face of an uptick in inflation even before the effect of the first – and the jumbo rate cut – is felt. But Raphael Bostic said he’s open to skipping a rate cut. Indeed, if inflation picks up momentum, the Fed’s focus will shift back to containing it – even though it means a weaker jobs market and a slowdown for the US economy. That’s the basis of the economic theory.

The market reaction to yesterday’s US CPI data was mixed. The stock investors’ first reaction was hesitation. There has been an initial selloff, followed by some dipbuying, then a selloff again. At the end, the S&P500 ended the session 0.21% down – which is a surprisingly nice performance given that the combination of higher-than-expected inflation and uglier-than-expected jobs data is simply bad for growth prospects: it means that the Fed must deal with inflation first and let growth slow down while it gets prices under control. So, I am surprised that the S&P500 didn’t show a bigger reaction and even more surprised that the US futures are slightly in the positive this morning.

Due today, the core PPI is expected to print a jump in producer prices from 2.4% to 2.7% y-o-y. Hotter-than-expected figures should – at some point – break the back of the Fed doves.

In the bonds space, the US 2-year yield spiked above 4% post-US CPI but the rebound remained short-lived. The probability of a 25bp cut in the FOMC’s November meeting is slightly higher than no cut bets after the CPI data. There is room for less dovishness when traders get ready to see the truth.

As such, the US dollar index was bought then sold and bought and sold again yesterday to end the day near flat after yesterday’s hotter-than-expected inflation report. But the dollar bulls have all the reasons in the world to bet against the Fed doves as the Fed itself could have its back against a wall with the pretty strong jobs, and hotter-than-expected inflation data.

The EURUSD collapsed to 1.09 yesterday as, as opposed to the Fed, the European Central Bank (ECB) rate cut expectations are justified by a Eurozone inflation that fell below the ECB’s 2% target. The pair is better bid this morning but the price rallies are expected to see resistance near the 1.0980 level, the major 38.2% Fibonacci retracement that should keep the EURUSD in the bearish consolidation zone and encourage a further selloff toward the 200-DMA, at 1.0875. A higher-than-expected US PPI print today could back a deeper dive in the EURUSD before the weekly closing bell, and a broader strength of the US dollar against other peers as some components in the PPI report affect the PCE index that the Fed uses as its favourite gauge of inflation to decide what to do with their policy.

Big banks kick off earnings season

Either way, the bank earnings will steal a part of the investor attention to the earnings season today. JP Morgan and Wells Fargo will open the dance, Citi, Morgan Stanley, Goldman and Bank of America will report next week and provide some insights regarding the overall health of the economy. The US bank stocks have performed well this year, they are the second best performers among the S&P500 sub-sectors this year after technology as the Fed rate cuts got delayed to the Q3 while the economic growth remained resilient. Sure, the saving rates and the delinquencies rates rose, but that didn’t have a material impact so far... And if all goes well, the lower net interest income due to the upcoming Fed cuts will be compensated by improved economic activity and a faster loan and deposit growth, while a potential delay in Fed cut rates should keep the net interest income intact. As such, the bank investors have reason to believe that their bank stocks could extend their gains in both scenarios. Let’s see if the expectations match the reality on the field.

China, Mid East tensions keep Oil bulls alert

China will unveil more details about its fiscal stimulus plans on Saturday and their announcement should live up to high market expectations to prevent investors’ enthusiasm from entirely fading. The expectation is a 2 trillion yuan package, ten times the number pronounced by authorities earlier this week.

And tensions in the Middle East will likely keep investors tense into and during the weekend. The barrel of US crude jumped 3% yesterday on possibility that Israel could attack Iran’s oil and nuclear facilities. Short-term risks in oil remain tilted to upside.

UK GDP grows 0.2% mom in Aug, matches expectations

UK GDP grew 0.2% mom in August, matched expectations. Services output grew by 0.1% mom. Production output grew by 0.5% mom. Construction output grew by 0.4% mom.

In the three months to August compared with the three months to May, GDP grew 0.2%. Service output rose 0.1%. Production output showed no growth. Construction output rose 1.0%.

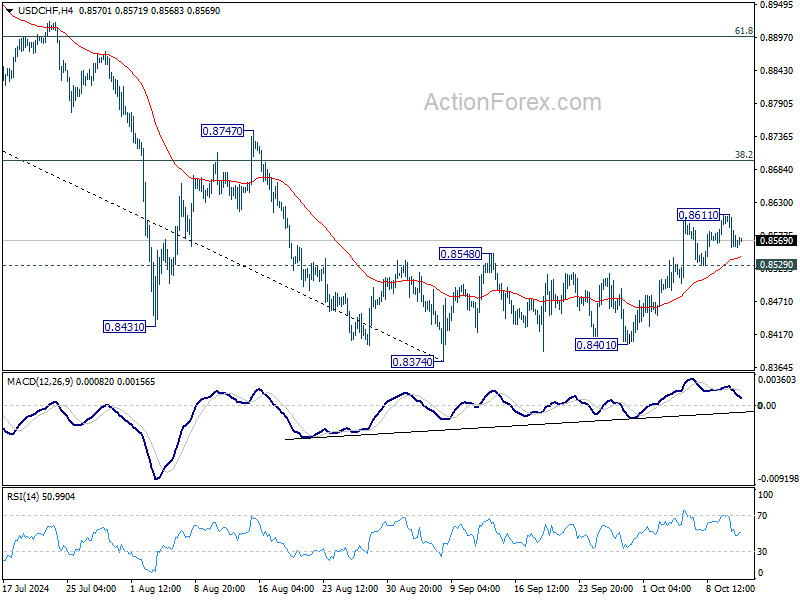

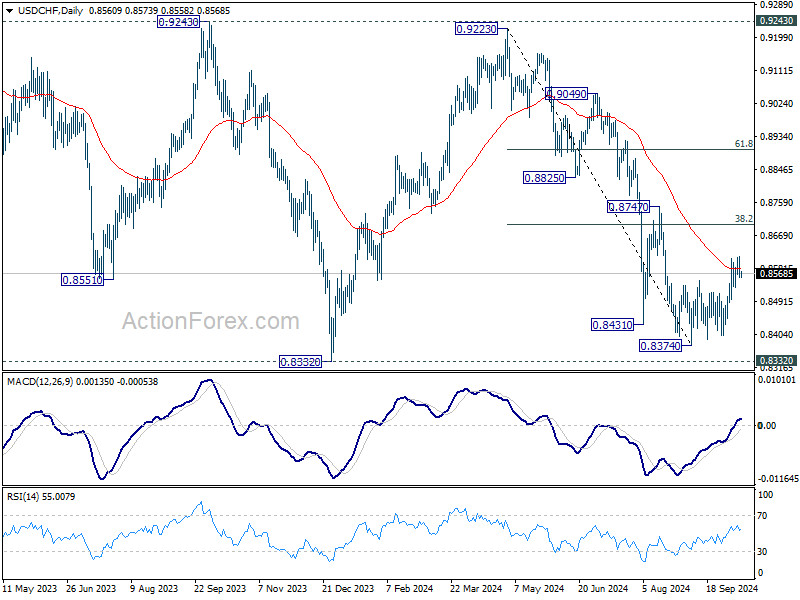

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8542; (P) 0.8578; (R1) 0.8597; More…

Intraday bias in USD/CHF is turned neutral first with current retreat. On the upside, above 0.8611 will resume the rebound from 0.8374 to 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Sustained break there will argue that fall from 0.9223 has completed after defending 0.8332 low. However, firm break of 0.8529 minor support will turn bias back to the downside for retesting 0.8374/8401 support zone instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Risk Sentiment Steadies as Dollar Softens, GBP/CAD Eyes UK and Canada Data

Risk sentiment appears to have stabilized heading into the weekend, despite stronger-than-expected US inflation data released overnight. The report didn’t cause any significant shifts in market expectations regarding Fed's rate cuts. Stock markets also showed resilience, with major US indexes closing only slightly lower.

Dollar, however, has lost some momentum, turning softer against both Swiss Franc and Japanese Yen. Investors are now focused on comments from upcoming Fed officials, particularly on whether any will echo Atlanta Fed President Raphael Bostic’s openness to a potential pause in rate cuts at the November meeting.

For the week so far, Canadian Dollar is currently the weakest performer, followed by New Zealand Dollar and Australian Dollar. On the other hand, Swiss Franc is leading as the strongest currency, followed by Yen, and then Dollar. Euro and British Pound are stuck in the middle.

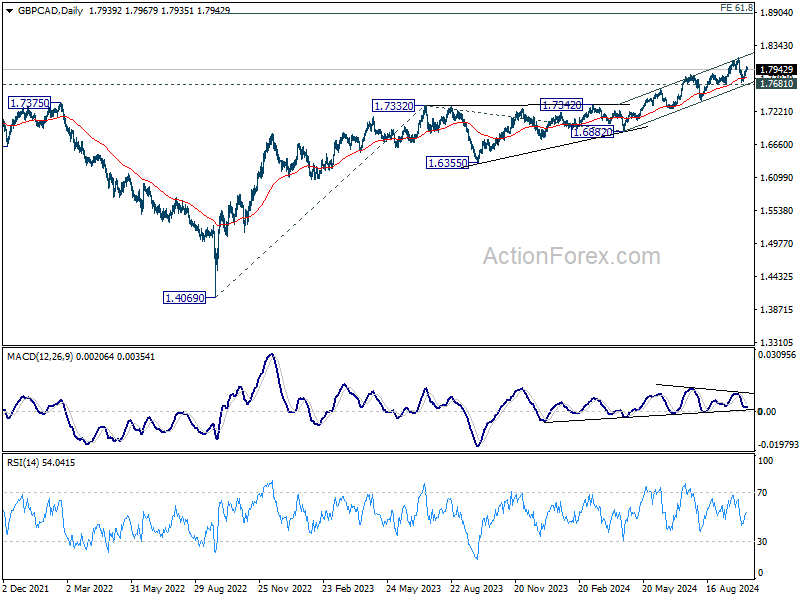

GBP/CAD is worth some attention today given that the UK will release GDP data while Canada will publish employment data. Technically, GBP/CAD's up trend is still in healthy state, supported by the near term rising channel, as well as 55 D EMA. Further rally is expected as long as 1.7681 support holds. The rise from 1.4069 should target 61.8% projection of 1.4069 to 1.7332 from 1.6882 at 1.8899 in the medium term. The speed, however, will depends on how BoE's and BoC's policy paths diverge.

In Asia, at the time of writing, Nikkei is up 0.60%. Hong Kong is on holiday. China Shanghai SSE is down -1.73%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield is down -0.0101 at 0.949. Overnight, DOW fell -0.14%. S&P 500 fell -0.21%. NASDAQ fell -0.05%. 10-year yield rose 0.029 to 4.096.

Fed's Bostic: Comfortable skipping a rate cut if data supports

Atlanta Fed President Raphael Bostic, in an interview with WSJ, indicated that he is open to pausing further rate cuts if economic data warrants it.

"I am totally comfortable with skipping a meeting if the data suggests that’s appropriate," Bostic said.

His view aligns with the more conservative approach seen in Fed's recent projections, where he has penciled in only one more quarter-point rate cut for the remainder of the year.

Bostic’s stance highlights a split among Fed officials regarding the future path of rate cuts. In the latest "dot plot" nine Fed members favor just one more 25bps cut this year, ten officials projected two such cuts.

Fed’s Williams expects gradual move toward neutral policy

New York Fed President John Williams signaled yesterday that monetary policy will continue to shift towards a more neutral stance in the coming months, aligning with ongoing progress toward price stability. He emphasized that while inflation remains above the 2% target, there has been clear movement in the right direction.

Williams noted, “Based on my current forecast for the economy, I expect that it will be appropriate to continue the process of moving the stance of monetary policy to a more neutral setting over time.” He reiterated that this approach will help preserve both the economy’s strength and the health of the labor market.

While acknowledging the work still needed to achieve price stability, he expressed optimism, stating, “The data paint a picture of an economy that has returned to balance.” Despite inflation remaining elevated, the message from Williams was one of cautious confidence, suggesting the Fed’s shift towards less restrictive policy will proceed gradually.

Fed’s Goolsbee expects more close calls ahead on rate decisions

Chicago Fed President Austan Goolsbee, in an interview with CNBC yesterday, highlighted the clear progress made in curbing inflation and cooling the labor market over the past 12 to 18 months.

“The overall trend… is clearly that inflation has come down a lot and the job market has cooled to a level which is around where we think full employment is,” Goolsbee stated.

Looking ahead, he noted there is broad consensus among policymakers that interest rates will need to drop a “fair amount” over the period.

However, in the near-term, Goolsbee expects more “close call” meetings for FOMC as members navigate through sometimes conflicting economic data.

SNB's Martin: Negative rates a possibility, but not on immediate agenda

SNB Vice Chair Antoine Martin indicated that the central bank may consider lowering interest rates, potentially even taking them into negative territory, as a tool to support the economy.

Speaking at an event overnight, Martin said "with inflation being reasonably low in Switzerland and with an economy that could grow faster, that tends in the direction of a lower policy rate,"

He further remarked that negative rates, although not imminent, remain a useful tool in the central bank's arsenal, stating, "There are imaginable scenarios where this is a tool that we would use because it's a particularly useful tool."

"But we're not today in a situation that this is something that we're considering," Martin added.

New Zealand BNZ PMI rises to 46.9, but stays in contraction for 19th month

New Zealand’s BusinessNZ Performance of Manufacturing Index rose slightly from 46.1 to 46.9 in September, marking the third consecutive month of improvement. Despite this, the sector remains in contraction for the 19th straight month, with the index still well below the long-term average of 52.6.

Catherine Beard, Director of Advocacy at BusinessNZ, highlighted that while it’s positive to see the highest PMI result since April, the sector faces a "long and slow road" to recovery.

The components painted a mixed picture: production improved from 46.6 to 48.0, while employment dipped slightly from 46.8 to 46.6. New orders also inched higher from 47.3 to 47.8, but deliveries fell further from 45.8 to 45.6.

Negative sentiment among respondents is gradually improving, with 63.5% expressing pessimism in September, down from 64.2% in August and significantly lower than the 76.3% seen in June. The main concerns continue to revolve around weak demand, with many businesses citing a lack of orders and sales as key issues.

Looking ahead

UK data will take center stage in European session, with monthly GDP, production and trade balance featured. Swiss will release SECO consumer climate while Germany will publish CPI final.

Later in the day, main focus is on Canada employment and US PPI. US will also release U of Michigan consumer sentiment.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8542; (P) 0.8578; (R1) 0.8597; More…

Intraday bias in USD/CHF is turned neutral first with current retreat. On the upside, above 0.8611 will resume the rebound from 0.8374 to 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Sustained break there will argue that fall from 0.9223 has completed after defending 0.8332 low. However, firm break of 0.8529 minor support will turn bias back to the downside for retesting 0.8374/8401 support zone instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

New Zealand BNZ PMI rises to 46.9, but stays in contraction for 19th month

New Zealand’s BusinessNZ Performance of Manufacturing Index rose slightly from 46.1 to 46.9 in September, marking the third consecutive month of improvement. Despite this, the sector remains in contraction for the 19th straight month, with the index still well below the long-term average of 52.6.

Catherine Beard, Director of Advocacy at BusinessNZ, highlighted that while it’s positive to see the highest PMI result since April, the sector faces a "long and slow road" to recovery.

The components painted a mixed picture: production improved from 46.6 to 48.0, while employment dipped slightly from 46.8 to 46.6. New orders also inched higher from 47.3 to 47.8, but deliveries fell further from 45.8 to 45.6.

Negative sentiment among respondents is gradually improving, with 63.5% expressing pessimism in September, down from 64.2% in August and significantly lower than the 76.3% seen in June. The main concerns continue to revolve around weak demand, with many businesses citing a lack of orders and sales as key issues.

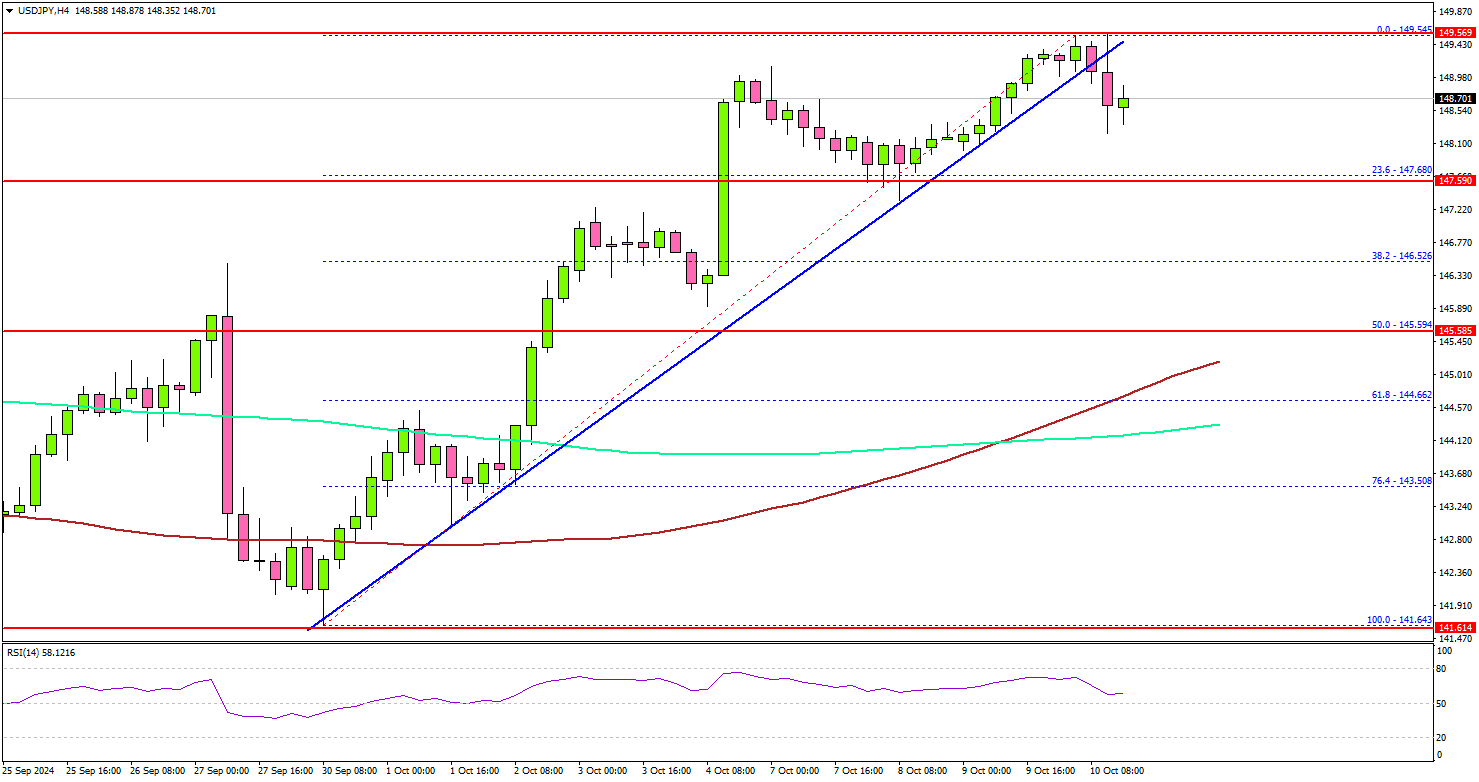

USD/JPY Signals Possible Pullback: Will Bulls Lose Momentum?

Key Highlights

- USD/JPY rallied above 149.20 before the bears appeared.

- It traded below a major bullish trend line with support at 149.35 on the 4-hour chart.

- EUR/USD extended losses and traded below the 1.0950 support.

- GBP/USD is at risk of more downsides below the 1.3000 support.

USD/JPY Technical Analysis

The US Dollar gained pace above the 147.50 and 148.50 levels against the Japanese Yen. USD/JPY even surpassed 149.20 before the bears appeared.

Looking at the 4-hour chart, the pair traded as high as 149.54 and recently corrected some gains. There was a move below a major bullish trend line with support at 149.35. If the bears remain in action, the pair could drop toward the 148.00 level.

On the downside, immediate support sits near the 147.70 level. It is close to the 23.6% Fib retracement level of the upward move from the 141.64 swing low to the 149.54 high.

The next key support sits near the 146.50 level. Any more losses could send the pair toward the 50% Fib retracement level of the upward move from the 141.64 swing low to the 149.54 high at 145.60.

On the upside, the bears might be active near the 149.40 level. The first major resistance might be near the 149.50 level. A close above the 149.50 level could set the tone for another increase.

The next major resistance could be 150.00. A clear move above the 150.00 level might send USD/JPY toward 152.00. Any more gains might call for a test of the 153.20 zone.

Looking at EUR/USD, the bulls failed to defend more downsides, and the pair declined below the 1.0950 support zone.

Upcoming Economic Events:

- Canada’s Net Employment Change for Sep 2024 – Forecast 27K, versus 22.1K previous.

- Canada’s Unemployment Rate for Sep 2024 - Forecast 6.7%, versus 6.6% previous.

- US Producer Price Index for Sep 2024 (MoM) – Forecast +0.1%, versus +0.2% previous.

- US Producer Price Index for Sep 2024 (YoY) – Forecast +1.6%, versus +1.7% previous.

Fed’s Bostic: Comfortable skipping a rate cut if data supports

Atlanta Fed President Raphael Bostic, in an interview with WSJ, indicated that he is open to pausing further rate cuts if economic data warrants it.

"I am totally comfortable with skipping a meeting if the data suggests that’s appropriate," Bostic said.

His view aligns with the more conservative approach seen in Fed's recent projections, where he has penciled in only one more quarter-point rate cut for the remainder of the year.

Bostic’s stance highlights a split among Fed officials regarding the future path of rate cuts. In the latest "dot plot" nine Fed members favor just one more 25bps cut this year, ten officials projected two such cuts.

SNB’s Martin: Negative rates a possibility, but not on immediate agenda

SNB Vice Chair Antoine Martin indicated that the central bank may consider lowering interest rates, potentially even taking them into negative territory, as a tool to support the economy.

Speaking at an event overnight, Martin said "with inflation being reasonably low in Switzerland and with an economy that could grow faster, that tends in the direction of a lower policy rate,"

He further remarked that negative rates, although not imminent, remain a useful tool in the central bank's arsenal, stating, "There are imaginable scenarios where this is a tool that we would use because it's a particularly useful tool."

"But we're not today in a situation that this is something that we're considering," Martin added.

700 Reasons to Expect Higher Real Rates on Average

Now that central banks are cutting rates, the question of where they will stop comes into focus. Real rates have trended down for decades, but a very long-term view supports our thesis that rates will average higher in future than they did pre-pandemic.

Most peer central banks are already cutting rates and some are front loading the cuts. The Fed and the RBNZ have seemingly declared 50 to be the new 25, though it is not clear that the FOMC will continue at that pace. The ECB may also want to pick up the pace to offset fiscal consolidation, as Westpac economics colleague Illiana Jain points out in her piece in our latest Market Outlook report released this week.

Steep hiking phases followed by equally steep cutting phases may well be a general pattern when an inflation surge is largely driven by supply shocks that unwind of their own accord. Unlike the more organic sources of strong demand that central banks usually contend with, the demand component of the current inflation shock has also been partly self-correcting, driven as it was by pandemic-era stimulus. It should be no surprise then that the economies with some of the sharpest rate cycles – the United States and New Zealand – had ongoing fiscal stimulus after the pandemic.

While the need to reduce the restrictiveness of policy in these economies is clear, it is less obvious where policy might need to land to no longer be restrictive. The so-called neutral rate is uncertain. And as the FOMC ‘dot plot’ estimates for the long-run fed funds rate show, policy makers are even less sure about its level than in the past. While their views have diverged, all FOMC members are agreed that it is probably higher than was believed before the pandemic. This lines up with our long-standing house view that the global structure of interest rates is likely to be higher on average than it was between the GFC and the pandemic. The era of negative yields is over.

The rate that neither stimulates nor weighs on inflation at any point is also the rate that balances desired saving and investment. It will depend on whatever else is going on, including the drag or stimulus from fiscal policy. It is because of these other things that we expect a higher average rate structure. European governments need to consolidate, but as Iliana points out, by less and in a less abrupt manner than in the early 2010s. Western governments more generally are facing greater demands to spend on defence, energy transition and to meet the needs of an ageing population. The private sector, too, has more need to invest now, on energy transition and the energy demands of AI. It also has a bit more scope to do so given that Western banking systems are less constrained by the need to build up capital to meet the requirements of the Basel 3 rules. Asian economies remain an important source of saving, but not more than they were in the first two decades of the century. They might even be less of a saving source, depending on how large the stimulus is in China.

All of this is a guide to what central banks need to do to achieve their desired policy stance in the moment. It says less about where the rate structure is likely to gravitate to in the long run, when all the current shocks have played out. The answer to that question is also often labelled the ‘neutral rate’, a little confusingly. (Some researchers attach an extra star to their notation distinguish between these concepts.) This longer-term version is less of a guide to central bank decision-making now, and more of an anchor for pricing very long-term debt securities.

A plague on all your 20th century trend estimates

This long-term anchor concept still boils down to the rate that balances global saving and investment on average. But now we must consider the deeper and more structural drivers of those forces, and whether there are structural trends. A large body of research notes the downward trend in both short-term and long-term real interest rates. So far, though, there has been no consensus on the reasons for this.

Some recent research by Kenneth Rogoff, Barbara Rossi and Paul Schmelzing might provide some insights. They have compiled data on real long-term bond yields going all the way back to the year 1311, more than 700 years. An achievement in itself, their dataset shows that there has indeed been a slight downward trend over this longer period. Crucially, though, the period between the GFC and the pandemic was in fact a downward deviation from that trend. The authors therefore expect some reversion to trend in coming years. This contrasts with papers using shorter data sets, where the downward trend is less precisely estimated.

It is important not to take this purely empirical observation as gospel. We do not yet know why there is a downward trend, or what might be the cause of the recent downward deviation. There are, however, some reasonable hypotheses. Recall that these are long-term real bond yields not the short-term rates used by central bankers to set policy. The market and policy apparatus the shorter rate applied to came in many centuries later than long-term sovereign bonds. It may be that the trend comes from a trend in the term premium or risk premium, rather than from the neutral short-term rate as we think of it now. For example, it could be that as experience with long-term debt markets increased, and governments became better at keeping their financial promises, investors among Europe’s Early Modern elites became more trusting over time and demanded a smaller term/risk premium over the (unobserved) ‘true’ risk-free rate.

Some other suggestive possibilities can be inferred from the fact that there was a break upwards in the trend following the Black Death in the 1340s, when one-third to a half of the population of Europe perished. If the underlying trend in interest rates reflects people’s willingness to wait until tomorrow, their need to be compensated for waiting will reflect their beliefs about how likely it is that they will even survive until tomorrow. Events like the Black Death surely shifted that subjective belief.

More broadly, rising longevity – or more precisely, greater certainty about your adult longevity – could be one of the reasons why people have seemingly become more patient and willing to accept less compensation for waiting, that is, a lower long-term interest rate. (The authors cite other research suggesting that elite males – the segment of the population who would have cared about yields on sovereign debt back then – were less likely to die in battle from the 1400s. That would have helped start the downtrend after the increase following the Black Death.) That is a reason to expect a slow downward trend, and to not assume that a lurch down after the GFC was permanent. There is a common thread here with other literature, including work from the Bank of Canada that focused on the need to save for longer (and more certain) retirements.

The academic debate remains unresolved. For anyone thinking about pricing bonds or planning fiscal policy, though, some of the latest research suggests it would be foolhardy to assume that the low-rates world of the GFC-to-pandemic period will continue.