Sample Category Title

ECB Preview – Acknowledging Downside Weakness = A Rate Cut

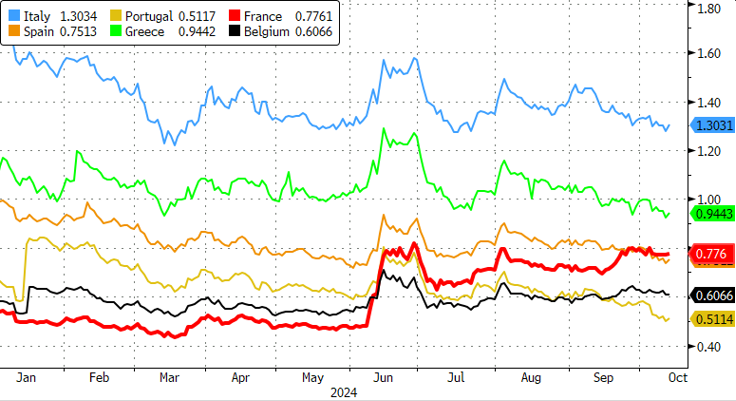

At next week's ECB meeting on 17 October we expect the ECB to deliver yet another rate cut of 25bp, bringing the deposit rate to 3.25%. Weaker-than-anticipated growth indicators, as well as a decline in inflation, support the case for another rate cut from the ECB.

Since the US labour market report last week, markets have significantly repriced expectations for policy easing across central banks, not least the ECB. Markets are now discounting an additional 47bp of rate cuts this year, consistent with a rate cut next week and again in December, and 97bp of rate cuts next year, consistent with our baseline of quarterly rate cuts of 25bp each.

We expect very limited forward guidance at the upcoming meeting, meaning the ECB should stick to the 'meeting by meeting' and 'data dependent' approach that it has been following in the past few quarters. Ahead of the December meeting, where it will give new staff projections, including the 2027 projection, we are set to see very important data points from the euro area (2x PMIs, 2x inflation, wage data, labour data).

Weekly Focus – ECB to Cut Rates Again Next Week

Sentiment has been positive this week as markets continue to digest the strong US jobs report from the previous week, and as the conflict in Middle East has not escalated further. On the latter, Israel could launch its revenge attack against Iran any minute. A decision to target a high-ranking Iranian official or any of the country's oil or nuclear sites, would definitely mark an escalation, and Iran would be forced to respond. However, supply in the oil market remains ample, with substantial volumes of spare capacity in Saudi Arabia, so we see a low risk of higher oil prices even if tensions remain. Israel and Iran's tit-for-tat attacks might lift prices in a knee-jerk fear reaction, but as long as energy flows from the Gulf to the rest of the world are not severely disrupted the impact should be temporary.

Inflation continues to slow down across major economies, see our Global Inflation Watch - Underlying inflation continues to cool gradually, 10 October. The US September CPI signalled headline inflation slowing further in annual terms, while core inflation remained steady. On a monthly level, prices rose slightly more than we had anticipated, but the upside surprise was mostly linked to food and goods prices, which rarely drive persistent inflation. In any case, the resilience in US macro data reduces the chance of the Fed resuming 50bp rate cuts, and short-term rate dynamics favour a lower EUR/USD.

China was an exception to the positive market mood this week, as investors were disappointed with the lack of details on fiscal stimulus measures. China came out with a big monetary stimulus package two weeks ago, and ever since investors have been hungry for details on the fiscal side. This week, the National Development and Reform Commission gave a briefing which lacked concrete measures, leading to a big sell-off in the Chinese equity market. Next, all eyes are on a Finance Ministry briefing on Saturday. We expect Finance Minister Lan Fo'An to announce a clear stimulus plan, but market expectations have become very high, so there is room for disappointment.

Next week's main event will be the ECB meeting on Thursday. Final September HICP data will be released just a few hours before the rate decision, but it is unlikely to be a gamechanger. We expect the ECB to cut the policy rates again by 25bp which would bring the deposit rate to 3.25%, and markets agree with our view. Focus will again be on Lagarde's remarks and especially the Q&A session. Even if ECB's forward guidance has been non-existent, markets seem convinced that rates will be cut at a relatively steady pace from here. We expect another 25bp cut in December and quarterly cuts next year, and see risks tilted towards even lower rates if euro area growth disappoints.

The next days are busy with Chinese data. On Sunday, China will release CPI for September, but as the data is backward-looking, and given the recent focus on stimulus signals, markets will likely put less emphasis on the numbers. On Monday, China will release trade data for September. Export growth has been trending lower lately as global manufacturing activity has declined. The Chinese data week will be rounded off with a batch of key macro releases (Q3 GDP, retail sales, industrial production) on Friday.

Otherwise, next week's data calendar is very light with German ZEW due on Tuesday and US retail sales out on Thursday.

Sunset Market Commentary

Markets

It’s more of the same today in absence of big events. Slightly below-consensus US PPI data only very briefly triggered a bid in US Treasuries which continued their bear steepening run. Daily changes on the US yield curve range between flat and +4.9 bps (30-yr). German changes add 2 to 3 bps across the curve. French OAT’s underperform. The French-swap spread tests the multiyear high in the wake of yesterday evening’s budget release. The government wants to implement €60.6 bn spending cuts and tax increases to avoid the budget deficit (expected at 6.1% of GDP) from increasing further. Via a 5% deficit next year, they aim to gradually get below the 3% Maastricht threshold by 2029, two years later than asked for by Europe. Lack of parliamentary majority complicates matters. EUR/USD holds steady around 1.0930 with risk sentiment showing no clear direction neither.

Next week’s eco calendar looks interesting. Chinese FM Lan Fo’an holds a press conference tomorrow. He’s expected to announce a new batch of fiscal aid to shore up to economy. It’s a second shot after earlier monetary and fiscal stimulus at the end of September. That triggered a 40%-50% rally on Chinese stock markets, half of which is undone after returning from golden week holidays. On Friday, China reports Q3 GDP data and September retail sales & production numbers. US markets are closed on Monday for Columbus Day Holiday, but a speech by Fed heavyweight governor, and possible successor of Fed chair Powell, Waller is worth watching. He speaks on the economic outlook at an event in Stanford. In the first half of the year, he advocated “what’s the rush?” (in favor of higher for longer). We think he’s still on that boat, but in the other direction. What’s the rush in making monetary policy rapidly less restrictive if inflation remains stuck above 2% and the labour market/economy doesn’t collapse? It’s in line with the mainstream view that the Fed will cut its policy rate by “only” 25 bps at the November policy meeting. Eco data include the Empire Manufacturing business survey (Tuesday), retail sales, Philly Fed business outlook & jobless claims (Wednesday) and housing data. It’s unlikely that they’ll spark the same amount of volatility as September payrolls and September CPI (in combination with jobless claims) did. The European focus simply centers on Thursday’s ECB policy meeting. Unaltered September GDP & CPI forecasts and the brief intermeeting period suggested that bar any surprises, the ECB would sit this meeting out before conducting a new policy rate cut in December. Awful EMU PMI business surveys and a confirmation of the disinflationary trend made Frankfurt changed tack. ECB president Lagarde told European parliament lawmakers that she would take the data into stride when deciding on policy in October. A large majority of ECB governors also backed a (25 bps) October rate cut. Barring any major economic surprises, we think a 25 bps rate cut is the most likely scenario for December as well.

News & Views

The German government earlier this week downgraded the 2024 growth forecasts into a 0.2% contraction. Having done so had the side effect of opening up borrowing (and spending) room under a mechanism enshrined in the country’s constitution that allows for additional spending in times of economic weakness. Bloomberg reported that Germany’s finance minister Lindner plans to take full advantage of that, resulting in a net increase in 2025 borrowing by about €5bn (to €56.5bn). The “windfall” helps close the €12bn budget financing hole for 2025 with the government banking on lower-than-expected outflows of other earmarked funds to close the remaining gap.

Canadian job growth topped consensus estimates in September. Net gains amounted to 46.7k, picking up from the 22.1k in August and almost double the 27k expected. Full-time jobs (+112k) more than compensated for a setback in part-time work (-65k). The unemployment rate unexpectedly fell back from 6.6% to 6.5%. This first decline since January was accompanied by a drop in the participation rate though, from 65.1% to 64.9%, the lowest since mid-2021. The employment rate, currently at 60.7% (-0.1 ppt), has trended downwards since the peak of 62.4% in early 2023 as labour force growth outpaced employment growth. Average hourly wages among employees increased 4.6%. The report is testament to a solid-to-strong labour market and questions the need for aggressive rate cuts by the central bank. BoC governor Macklem didn’t not want to rule out bigger (than 25 bps) cuts after lowering the policy rate by 25 bps to 4.25% in September. He made the comments back then when market momentum was building for the Fed to kick off with a super-sized 50 bps cut as well. Canadian money markets today pared bets for such a move at the October 23 meeting from 50% to 30% currently. The Canadian dollar clawed back some of the previous losses today but remains on track to print daily losses, extending its losing streak to 8 days. USD/CAD is trading around 1.375. Canadian government bond yields rise between 3.3 and 4.6 bps across the curve.

Graphs

USD/CAD: can Loonie stop the rot following stronger Canadian payrolls?

French OAT’s continue underperforming after 2025 budget proposal

US 10-yr yield: bear flattening trend continues going into long US weekend

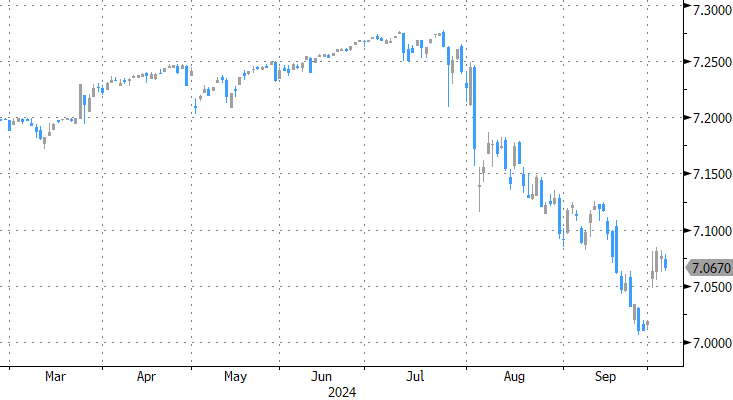

USD/CNY: all (Chinese) hopes on tomorrow’s update from minstry of Finance. More fiscal stimulus ahead?!

Dollar Index – Bulls Pause After US Data and Look for Fresh Direction Signal

The dollar holds in a sideways mode vs the basket of major currencies for the second straight day, as US September CPI data cooled expectations for another Fed jumbo rate cut, though the sentiment is still bullish and keeps the greenback afloat.

Markets digested the latest key economic data which showed slightly hotter than expected inflation in September and warned that Fed’s battle with inflation is still far from the end, but immediate fears were tempered by weekly jobless claims well above consensus.

The dollar index is on track for another weekly gain, although much smaller than the previous week’s 2.1% advance, but initial signal of a stall of recent bull-leg and potential reversal, is developing on daily chart.

The notion is supported by overbought conditions, fading bullish momentum and formation of a bull-trap pattern, although more work at the downside will be still required to generate initial bearish signal.

Rising 5DMA / Thursday’s low mark immediate supports at 102.45, guarding more significant 102.00 zone (broken Fibo 38.2% of 105.78/99.84 / round-figure / rising 10DMA), loss of which would open way for deeper correction of 99.84/102.95 upleg and expose next pivotal supports at 101.76/68 (Fibo 38.2% / daily cloud base / rising daily Tenkan-sen) and 101.40 breakpoint (50% retracement / daily Kijun-sen).

Res: 102.81; 103.01; 103.34; 103.54

Sup: 102.45; 102.11; 101.90; 101.40

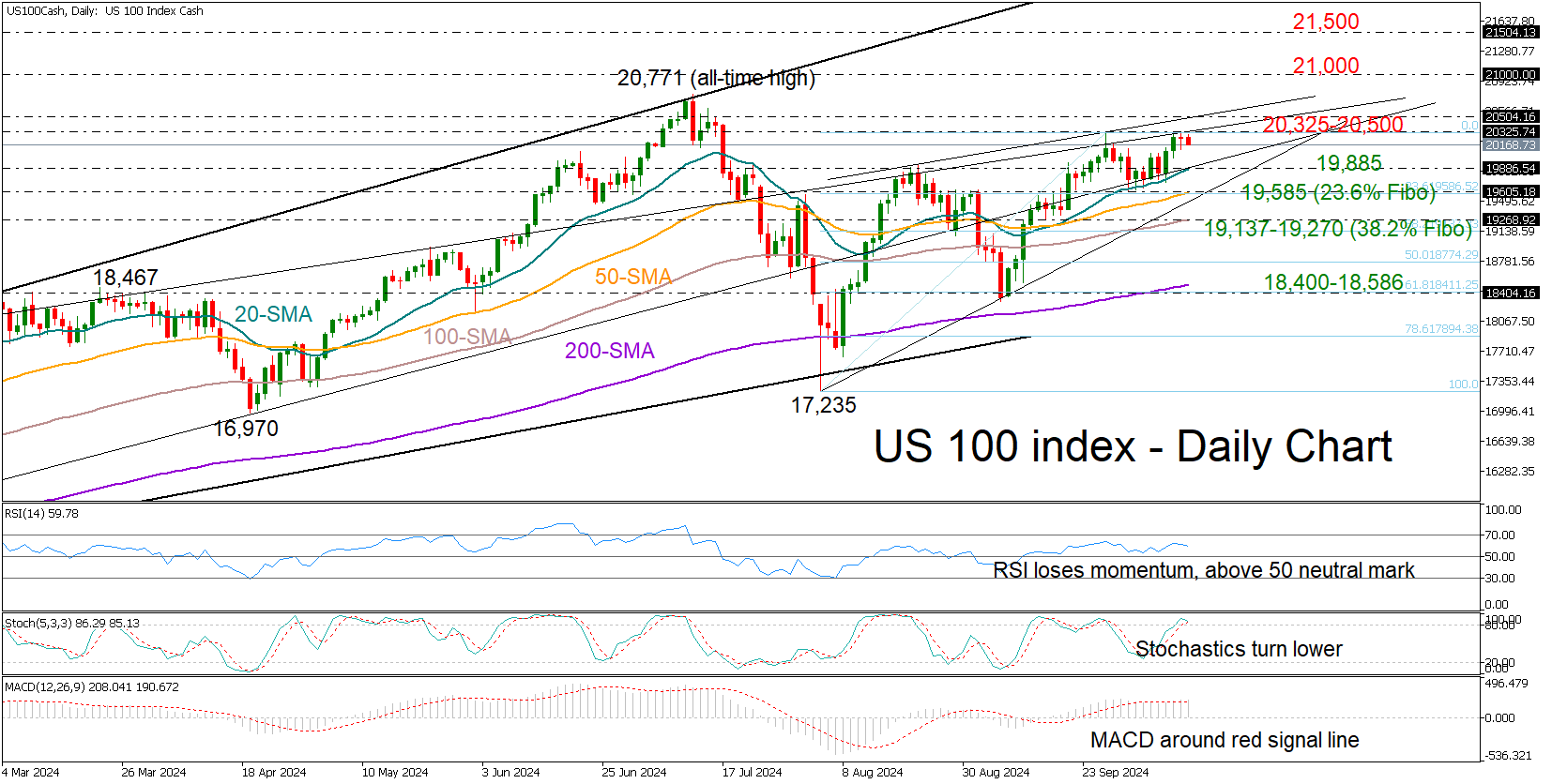

US 100 Index Slows Down Near September’s High

- US 100 index holds within bullish area but lacks steam

- Bulls need a close above 20,325-20,500 to strengthen uptrend

The US 100 stock index is about to open mildly lower on Friday despite upbeat US banking earnings, weighed by Tesla’s disappointing guidance on its self-driving robotaxis.

The index stabilized around September’s high and near the constraining ascending line from September 2022 at 20,316 following its bounce off the 20-day exponential moving average (EMA). Technically, the price could enter a consolidation phase as the stochastic oscillator is looking for a negative pivot and the RSI is losing momentum, though with the latter holding comfortably above its 50 neutral mark, buying appetite could stay alive.

The price could gain fresh impetus towards the all-time high of 20,770 if a close above the 20,325-20,500 is achieved. Stretching into uncharted territory, the bulls may face some congestion around the 21,000 psychological mark and then near 21,500.

If downside pressures strengthen, the 20-day EMA could come back into view within the 19,885-20,000 region. A step below this floor may press the price towards the 50-day EMA, which overlaps with the 23.6% Fibonacci retracement of the latest upleg near 19,585. Another failure there could send stronger bearish signals, confirming additional declines towards the 100-day EMA and the 38.2% Fibonacci of 19, 137.

In summary, although the US 100 index hasn't lost its shine yet, it could shift to the sidelines if the 20,325-20,500 resistance territory proves solid.

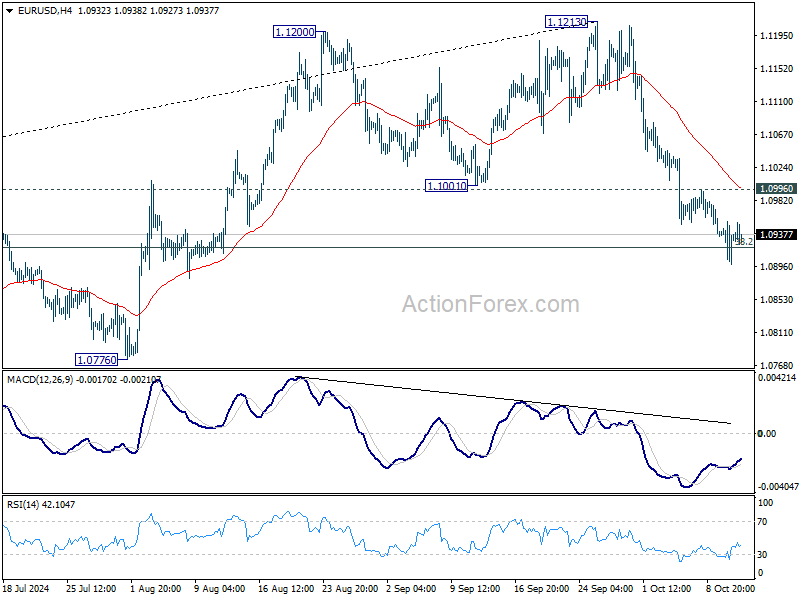

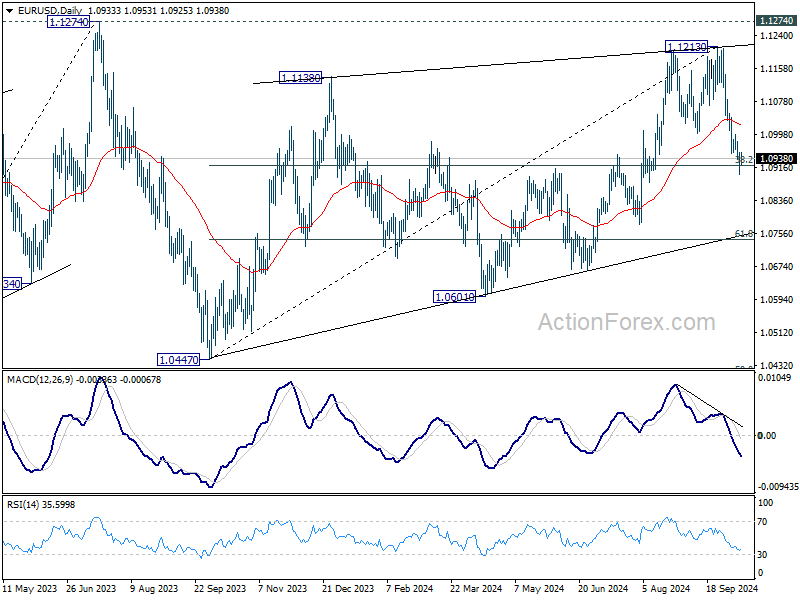

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0906; (P) 1.0931; (R1) 1.0961; More....

No change in EUR/USD's outlook and intraday bias stays on the downside. Sustained break of 38.2% retracement of 1.0447 to 1.1213 at 1.0920 will argue that fall from 1.1213 is the third leg of the corrective pattern from 1.1274. In this case, deeper decline would be seen to 61.8% retracement at 1.0740 next. On the upside, above 1.0996 minor resistance will turn intraday bias neutral again first.

In the bigger picture, rejection by 1.1274 resistance suggests that corrective pattern from 1.1274 (2023 high) is not completed yet. Instead, decline from 1.1213 might be another falling leg. Sustained break of 55 W EMA (now at 1.0877) will validate this case, and bring deeper fall towards 1.0447 support again.

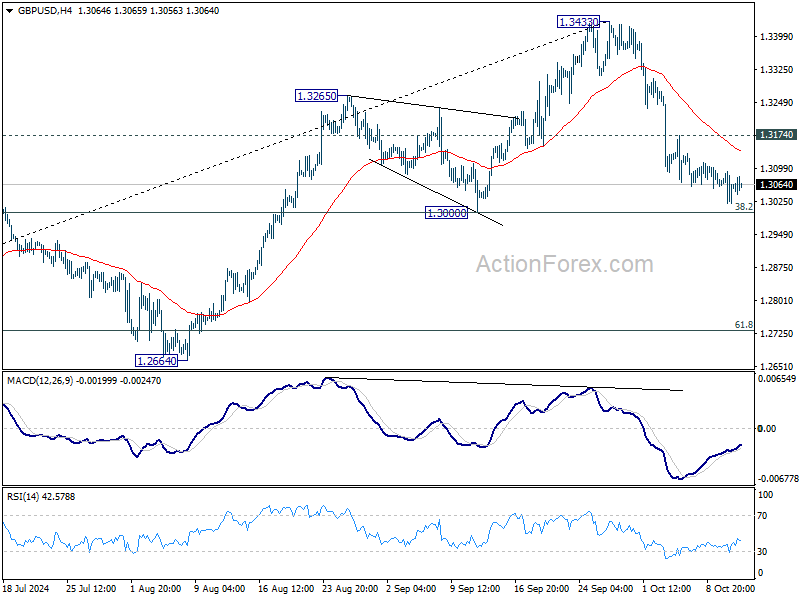

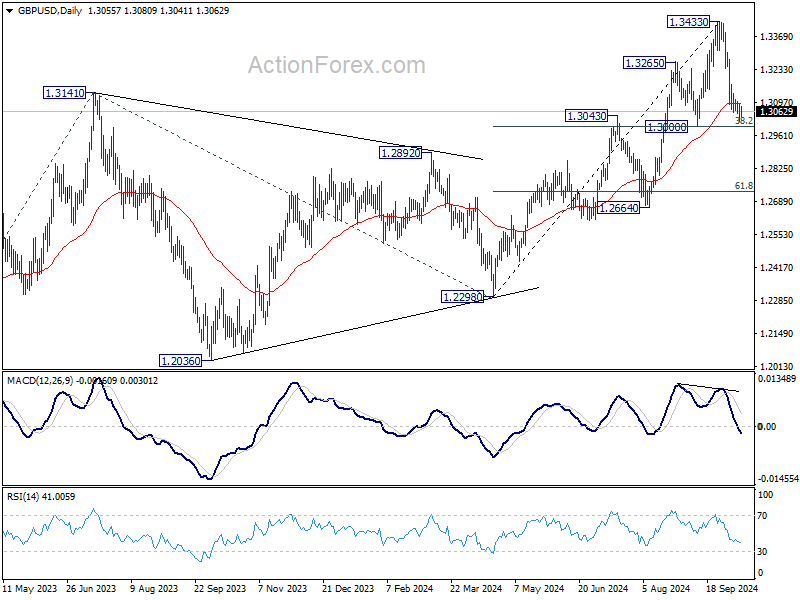

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3023; (P) 1.3058; (R1) 1.3095; More...

Outlook in GBP/USD remains unchanged and intraday bias stays neutral. While corrective fall from 1.3433 might extend lower, strong support should be seen from 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999) to contained downside. Above 1.3174 minor resistance will turn bias back to the upside for stronger rebound. However, decisive break of 1.3000 will carry larger bearish implications.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

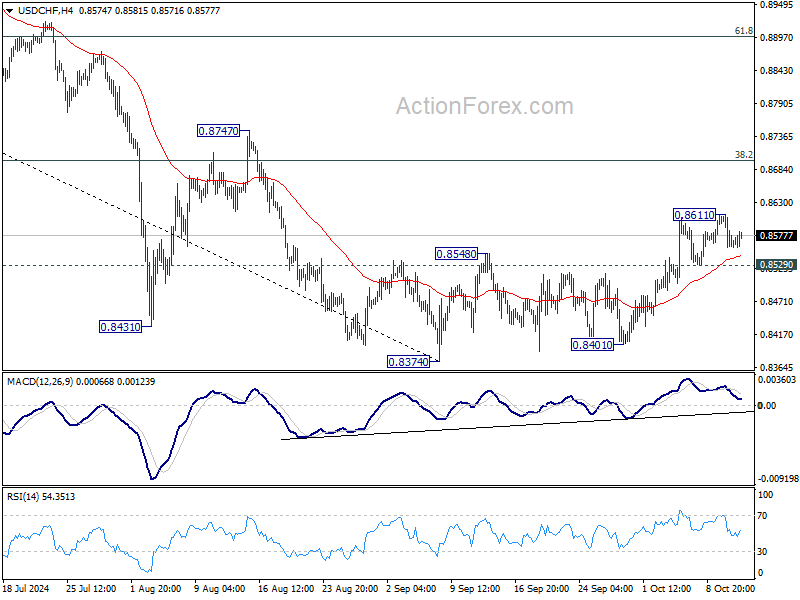

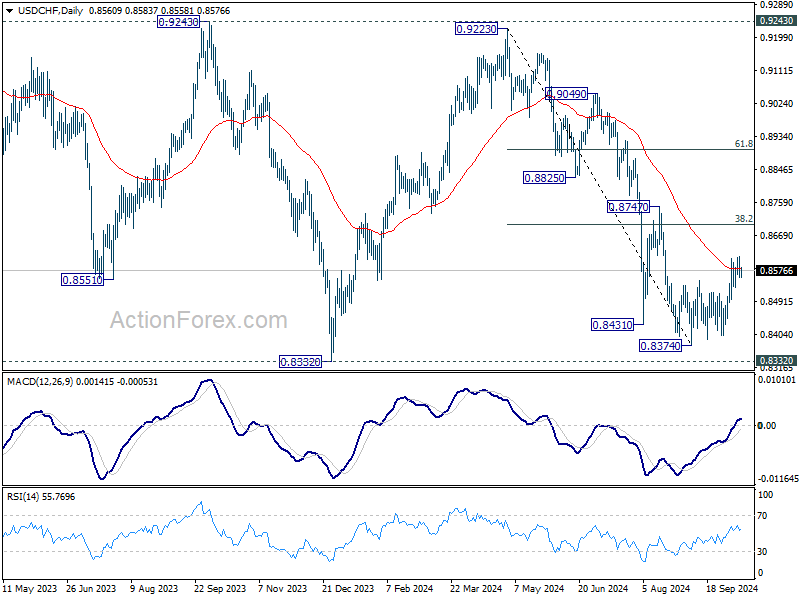

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8542; (P) 0.8578; (R1) 0.8597; More…

Intraday bias in USD/CHF stays neutral for consolidation below 0.8611 temporary top. On the upside, above 0.8611 will resume the rebound from 0.8374 to 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Sustained break there will argue that fall from 0.9223 has completed after defending 0.8332 low. However, firm break of 0.8529 minor support will turn bias back to the downside for retesting 0.8374/8401 support zone instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

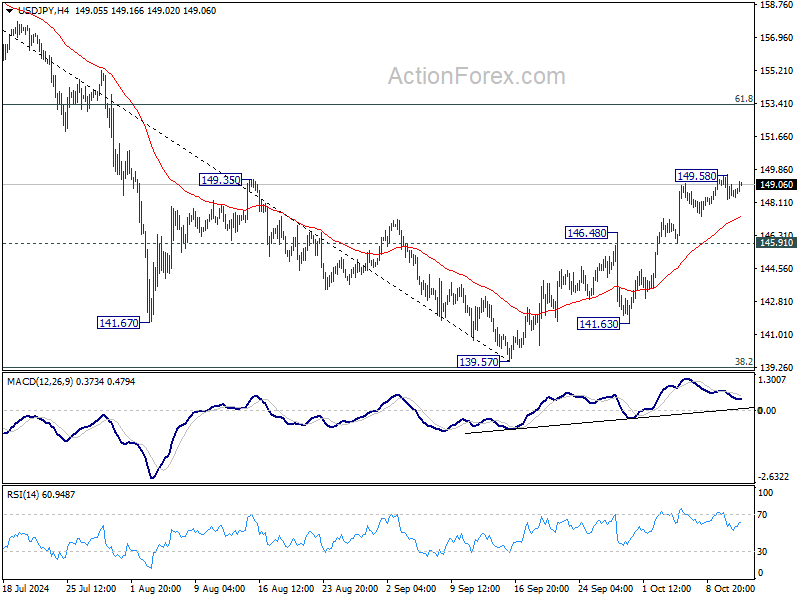

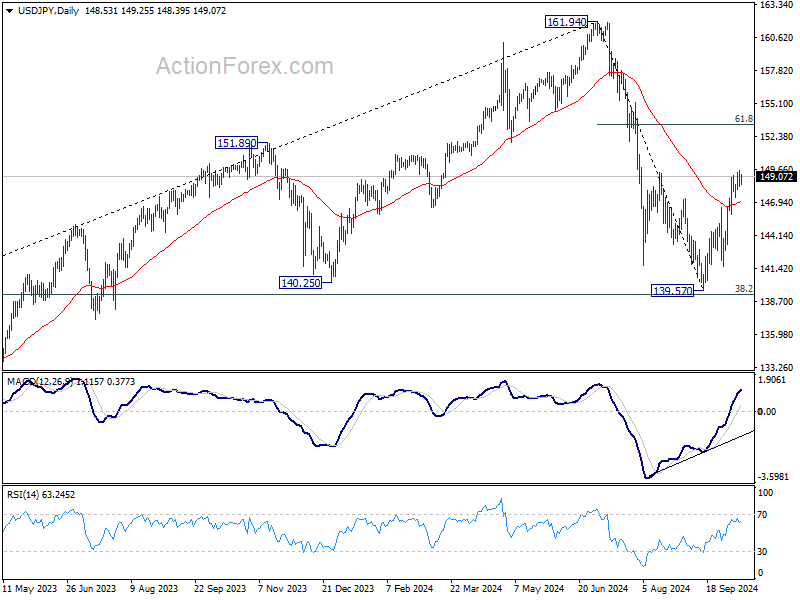

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.04; (P) 148.79; (R1) 149.33; More...

Intraday bias in USD/JPY remains neutral for consolidation below 149.58 temporary top. Further rally is expected as long as 145.91 minor support holds. Rise from 139.57 is s seen as the second leg of the corrective pattern from 161.94. Break of 149.58 will target 61.8% retracement of 161.94 to 139.57 at 153.39.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Canada’s Labour Market Takes a Break from its Cooling Trend in September

Canada's labour market bucked its weakening trend in September, adding 47k new jobs. Adding to the good news, the gains were entirely full-time (+112k), and in the private sector (+61k). Meanwhile part-time positions gave back their August gains (-65k).

Job gains were strong enough to push the unemployment rate down a tenth to 6.5%, the first improvement since January. Labour force growth was modest in September (+16k), as the participation rate fell two tenths to 64.9%.

Looking across sectors, job gains were concentrated in information, culture and recreation (+22k, 2.6%), wholesale and retail trade (+22k, 0.8%) and professional, scientific and technical services (+21k, 1.1%).

The unemployment rate ticked down in September, driven entirely by youth. The unemployment rate for those aged 15-24 fell a full percentage point to 13.5%, but is still 2.8 percentage points higher than a year ago. Perhaps more telling is that the share of the core working age population (25-54 years) with a job continued to tick down. It has fallen 1.6 percentage points relative to the start of 2023.

In one gray cloud in the report, total hours worked fell again in September (-0.4% month-on-month), and are up 1.2% over the past year. Wage growth cooled to 4.6% year-on-year in September.

Key Implications

A move down in Canada's unemployment rate is good news, and the two year bond yield is up a few tenths on the news. However, September's jobs report does not change the picture of a labour market that has cooled notably since the Bank of Canada started raising interest rates. Data rarely moves in a straight line, and we would need to see a few more months of strength before we declare an improving trend.

The Bank of Canada's next interest rate decision is in less than two weeks, and another cut is widely expected. Some market participants are leaning towards a larger half point move after the Fed's larger cut, but September's job data will likely pare those bets back a bit. We look for another quarter-point interest rate cut on October 23rd.