Sample Category Title

BoJ stands pat at 0.25%, sees gradual inflation rise and economic growth

BoJ left its uncollateralized overnight call rate unchanged at around 0.25% during today's meeting, as widely anticipated and decided by unanimously.

In the accompanying statement, BoJ maintained a positive outlook for the Japanese economy, projecting continued growth at a rate above its potential. The central bank expects "overseas economies will continue to grow moderately," further supporting Japan’s economic expansion. Domestically, the "virtuous cycle from income to spending" will gradually intensify, aided by accommodating financial conditions.

On the inflation front, core CPI is forecast to rise through fiscal 2025. BoJ also noted that underlying inflation will "increase gradually" as output gap narrows and medium- to long-term inflation expectations firm up.

However, the central bank also outlined several risks to its outlook, including global economic developments, commodity prices, and the pace at which firms adjust wage and price setting.

Japan’s CPI core rises to 2.8% in Aug, core-core up to 2.0%

Japan's core CPI, excluding fresh food, rose to 2.8% yoy in August, matching expectations and marking the fourth consecutive month of acceleration. This increase is up from 2.7% yoy in July and continues the upward trend from 2.2% yoy in April, keeping inflation above BoJ's 2% target since April 2022.

Core-core CPI, which strips out both fresh food and energy, also rose from 1.9% yoy to 2.0% yoy, highlighting broader inflationary pressures in Japan. Headline CPI, which includes all categories, increased from 2.8% yoy to 3.0% yoy.

Energy prices surged 12.0% yoy, while food prices increased by 2.9% yoy, and household durable goods saw a significant rise of 7.7% yoy. These numbers indicate persistent inflationary pressures across a wide range of goods and services.

UK Gfk consumer confidence plummets to -20 ahead of expected painful budget

UK GfK Consumer Confidence dropped sharply in September, falling from -13 to -20, marking the biggest decline since April 2022. The seven-point drop reflects growing concerns about the economic outlook and personal finances, with households bracing for a difficult budget next month.

Key forward-looking indicators worsened significantly. Expectations for the general economy over the next 12 months dropped by -12 points to -27, while personal finance expectations fell by -9 points to -3. The major purchase index, which gauges consumers' willingness to buy big-ticket items, also dropped -10 points to -23.

GfK noted, “Despite stable inflation and the prospect of further rate cuts, this is not encouraging news for the UK’s new government.” Neil Bellamy, Consumer Insights Director at GfK, linked the drop to concerns over Prime Minister Keir Starmer's warnings of a "painful" budget. Bellamy said, “Consumers are nervously awaiting the Budget decisions on Oct. 30 after the withdrawal of winter fuel payments and warnings of further difficult measures."

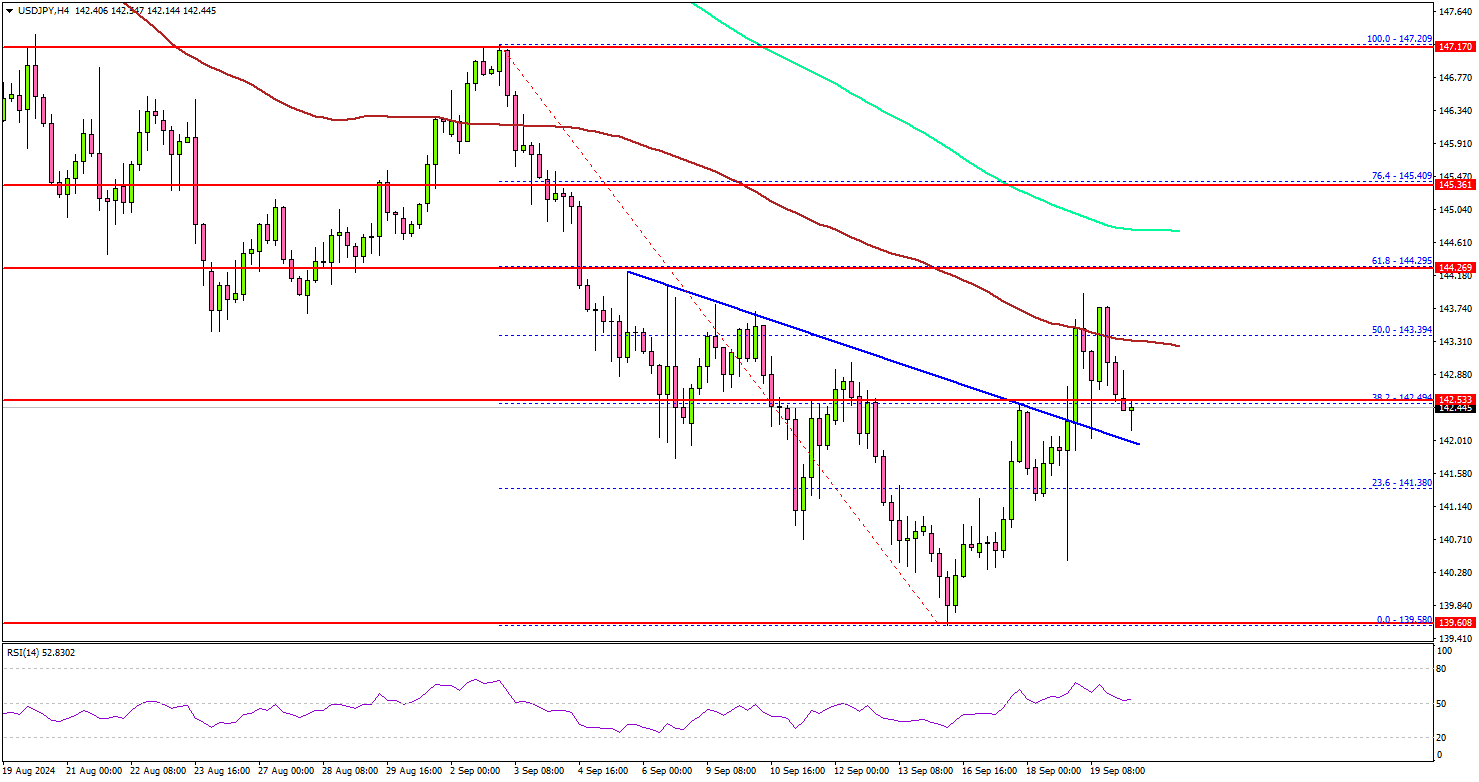

USD/JPY Recovery Eyes Momentum: Will Gains Pick Up?

Key Highlights

- USD/JPY started a fresh increase above the 142.00 resistance.

- It cleared a major bearish trend line with resistance at 142.20 on the 4-hour chart.

- EUR/USD failed to extend gains above the 1.1120 resistance.

- Bitcoin climbed higher above the $61,200 and $62,000 resistance levels.

USD/JPY Technical Analysis

The US Dollar found support near the 139.60 zone against the Japanese Yen. USD/JPY started a decent upward move above the 141.20 and 142.00 resistance levels.

Looking at the 4-hour chart, the pair climbed above the 38.2% Fib retracement level of the downward move from the 147.20 swing high to the 139.58 low. There was a break above a major bearish trend line with resistance at 142.20.

The pair even spiked above the 100 simple moving average (red, 4-hour) and the 50% Fib retracement level of the downward move from the 147.20 swing high to the 139.58 low.

On the upside, the pair could face hurdles near the 144.30 level and the 200 simple moving average (green, 4-hour). A clear move above the 144.30 zone might set the pace for a move toward 145.00. Any more gains might call for a test of the 146.00 zone.

On the downside, immediate support sits near the 142.40 level, below which the pair might test 142.00. The next key support sits near the 141.20 level. Any more losses could send the pair toward the 140.00 support zone.

Looking at Bitcoin, the bulls came into action, and they were able to push the price above the $62,000 resistance zone.

Upcoming Economic Events:

- UK Retail Sales for August 2024 (YoY) - Forecast +1.4%, versus +1.4% previous.

- UK Retail Sales for August 2024 (MoM) - Forecast +0.5%, versus +0.7% previous.

- ECB's President Lagarde speech.

Fed Starts at a Sprint, But the Finish Line is Uncertain

The US Federal Reserve has chosen a ‘sprint first, then dawdle’ approach to rates normalisation. Dawdling makes sense given the neutral rate is uncertain and probably higher than pre-pandemic.

The US Federal Reserve has started its cutting cycle with an outsized 50 basis point move. This was larger than what we had expected, though the direction and timing was obvious. Starting with 50 basis points is what you do when you want to get to where you need to go as soon as you reasonably can. The counterargument to this approach is that you might not want to risk scaring the horses with an outsized move that hints you think something is seriously wrong with the US economy. These are matters of judgement. Not all the FOMC members were persuaded, with Michelle Bowman dissenting.

The former central banker in me expected that Fed policymakers would not want to risk another episode of market volatility and economic catastrophising like the one seen a few months ago, and so would choose the more conservative approach. It turns out that you can word up key people in the media to soften the surprise factor. (This is another thing that does not sit well in the Australian context, where a media leak would be a conduct issue.)

For the record, the Fed’s outsized cut has no implications for the RBA’s decision next week or at subsequent meetings. As we have noted in the past, because Australia has a floating exchange rate, the RBA can set monetary policy here according to domestic circumstances. We continue to expect the RBA to hold rates next week and for the rest of the year.

Sprint first, then dawdle

The Federal Reserve does not need to be in a hurry. The US economy is not slowing precipitously, and growth in US real consumer spending remains robust. Indeed, the median FOMC member only expects to cut a further 50 basis points over the next two meetings, and a notable fraction of members expect only 25 basis points.

Central banks are characterising their rate cutting cycles as normalisation cycles. Policy had needed to be tight to address the high inflation stemming from the pandemic supply shocks and the policy-related demand shock that occurred in response to the pandemic. Now that inflation is close to target in many economies, policy does not need to be as tight as it was. And as we have explained before, because policy works with a lag, central banks need to start normalising before inflation is all the way back to target.

If the objective is to normalise, typically that would call for a measured initial response. By moving more quickly initially, the Federal Reserve has broken the mould to an extent. And they took this approach despite the exuberant equity market and other measures that suggest US financial conditions are not that tight. The FOMC members have also taken this approach to the early phase of the rate-cutting cycle even though the ‘dot plots’ that accompanied the announcement suggest the Fed funds rate will not return to neutral levels until 2026.

This ‘sprint first, then dawdle’ implied future path for the US can be reconciled by the considerable uncertainty implied by the members’ projections for the long-run level of the Fed funds rate, a proxy for their view of neutral. If you know exactly how far you need to go, you can get there quickly. But if you are unsure of your destination, tread more carefully. A rapid reversion to a level still a bit above neutral and slow from there makes sense in that situation. It is also consistent with our existing expectations that the pace of decline in the Fed funds rate would be faster in the first six months of the cycle than the second.

Many forces are lifting neutral

The FOMC’s uncertainty about the level of the neutral policy rate is warranted, more to the upside than down. Their latest forecasts upgraded their estimate, but it is not clear if they have gone far enough; the methods central banks use to estimate neutral policy rates are inherently incremental. A deeper look at underlying developments suggests that there are a range of global factors pushing in the direction of the global rate structure being higher than it was in the period between the Global Financial Crisis and the pandemic.

Among these factors are the geopolitical and sociological forces that are pushing towards larger public sectors in advanced economies. The IMF has recently noted political support coalescing behind greater government spending. The root causes are multifaceted. Geopolitics is now more multipolar, with the United States and China treating each other as strategic rivals rather than purely as trade partners. This pushes governments to boost spending on defence and national security, as well as expanding strategic manufacturing capability. Population ageing is also necessitating more health-related spending. Governments are also heavily involved in investing in the energy transition, along with the private sector.

More broadly, we see a sociological shift towards greater demand for – or at least tolerance of – government intervention in the economy to forestall risks and harms that sections of the community perceive. The pandemic may have amplified that shift. In Australia, at least, higher public demand and taxation have become a trend in recent years.

The balance of investment and saving in the private sector has also tilted towards more investment. Like governments, the private sector needs to execute on the energy transition, adopt energy-intensive innovations in AI and adapt to changing patterns of trade. There also might be more scope to fund investment, noting that the global banking sector is no longer in the mode of building up capital to meet new Basel requirements, as it was in the period between the GFC and the pandemic.

All these forces mean that investment demand is stronger relative to the past. While the Asian region remains an important source of saving, it is not an even bigger source than it was during the period of the so-called ‘global savings glut’. The net is therefore likely to be a tilt towards investment relative to saving. The way that the demand for and supply of funding for investment equilibrates is through a higher structure of global interest rates. This implies a higher risk-free ‘neutral’ rate. It might also have implications for things like average term premia and risk premia.

There are some forces pushing in the other direction. For example, global goods inflation is likely to remain low given weak domestic demand in China and the approach the authorities there are taking to growth and development, principally by boosting manufacturing supply capacity. The additional investment involved would tend to boost the global neutral real rate. However, the disinflationary impact means that actual nominal rates could be lower than otherwise, even if neutral rates are not.

Also working in this direction, population ageing is tending to boost participation and labour supply rather than reduce it in most western economies – though not the United States; we saw more evidence of this in the rising trend in participation here in Australia this week. As well as being disinflationary, abundant labour supply relative to population means less incentive to invest in labour-saving technologies. This is not so great for global productivity but could help offset increases in investment demand from other sources.

At this stage, though, we think the net of all these forces takes the global structure of interest rates higher than it was pre-pandemic. Indeed, we think neutral rates are more likely to in the low to mid 3% range than the high 2% level implied by the Federal Reserve’s current projections.

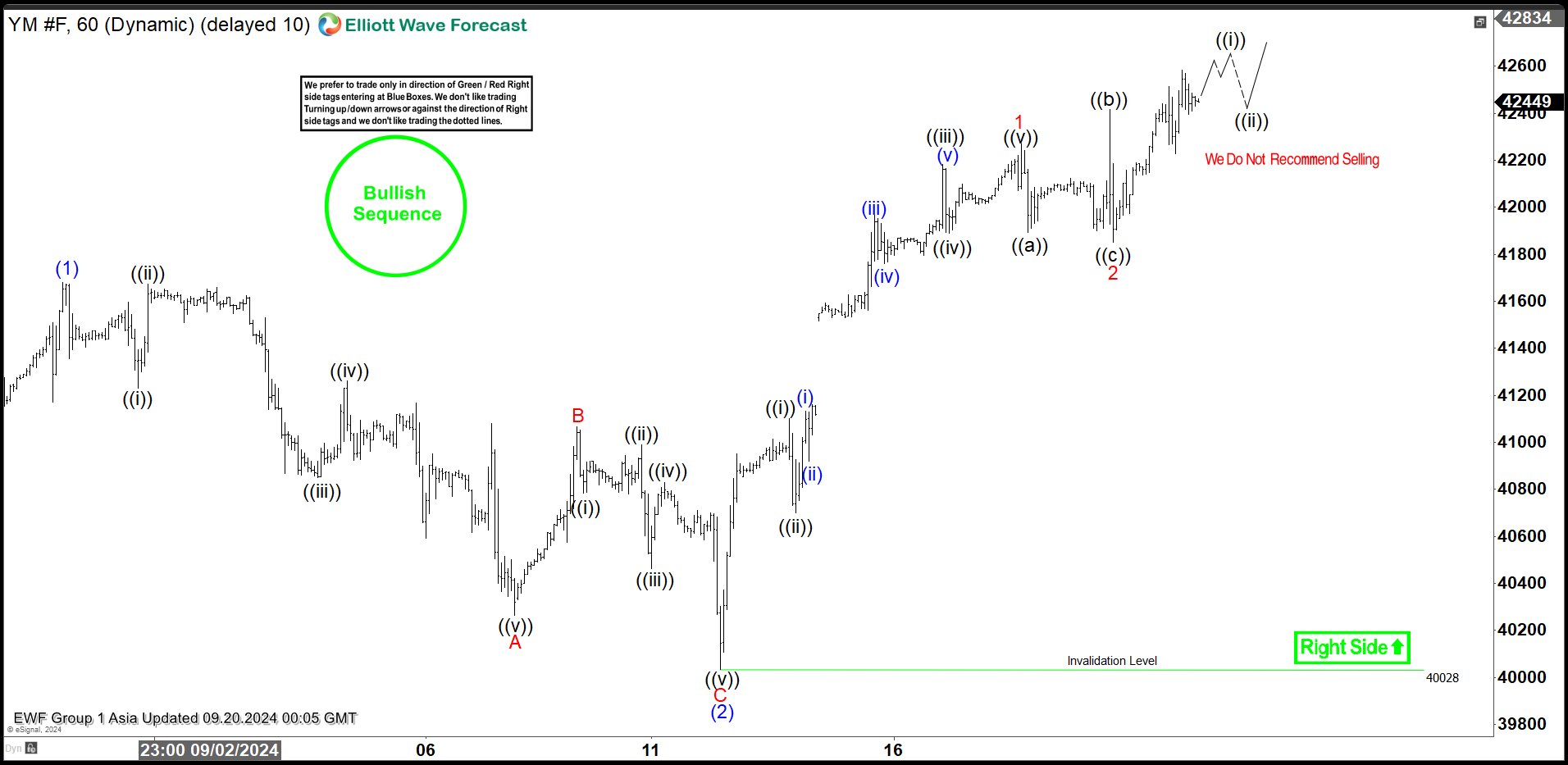

Intraday Elliott Wave View on Dow Futures (YM) Favors the Bullish Side

Short term Elliott Wave view on Dow Futures (YM) suggests that cycle from 8.8.2024 low is in progress as an impulse. Up from 8.8.2024 low, wave (1) ended at 41682 and wave (2) pullback ended at 40028 as the 1 hour chart below shows. Internal subdivision of wave (2) unfolded as a zigzag Elliott Wave structure. Down from wave (1), wave A ended at 40264 and rally in wave B ended at 41065. The Index then extended lower in wave C towards 40028 which completed wave (2) in higher degree.

Index has turned higher in wave (3). Internal subdivision of wave (3) is unfolding as a 5 waves impulse. Up from wave (2), wave ((i)) ended at 41100 and wave ((ii)) pullback ended at 40701. Wave ((iii)) higher ended at 42184, and wave ((iv)) pullback ended at 41890. Final leg wave ((v)) ended at 42270 which completed wave 1 in higher degree. Pullback in wave 2 unfolded as an expanded flat where wave ((a)) ended at 41893, wave ((b)) ended at 42416 and wave ((c)) ended at 41850. Index has resumed higher in wave 3 of (3). Near term, as far as pivot at 40028 low stays intact, expect dips to find support in 3, 7, or 11 swing for further upside.

Dow Futures (YM) 60 Minutes Elliott Wave Chart

Dow Futures (YM) Elliott Wave Video

https://www.youtube.com/watch?v=dTf2w_6XBRc

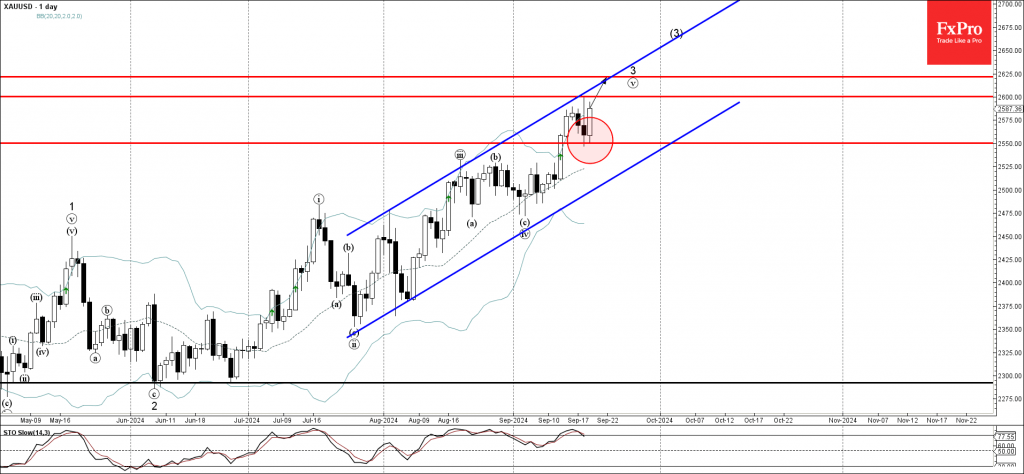

Gold Wave Analysis

- Gold reversed from support level 2550.00

- Likely to rise to resistance level 2600.00

Gold continues to rise inside the minor impulse waves v and 3, which belong to the intermediate impulse wave (3) from the start of June.

The price earlier reversed up from the support level 2550.00, which stopped the previous short-term correction yesterday.

Given the prevailing daily uptrend, Gold can be expected to rise further to the next resistance level 2600.00 – the breakout of which can lead to the next resistance at 2625.00.

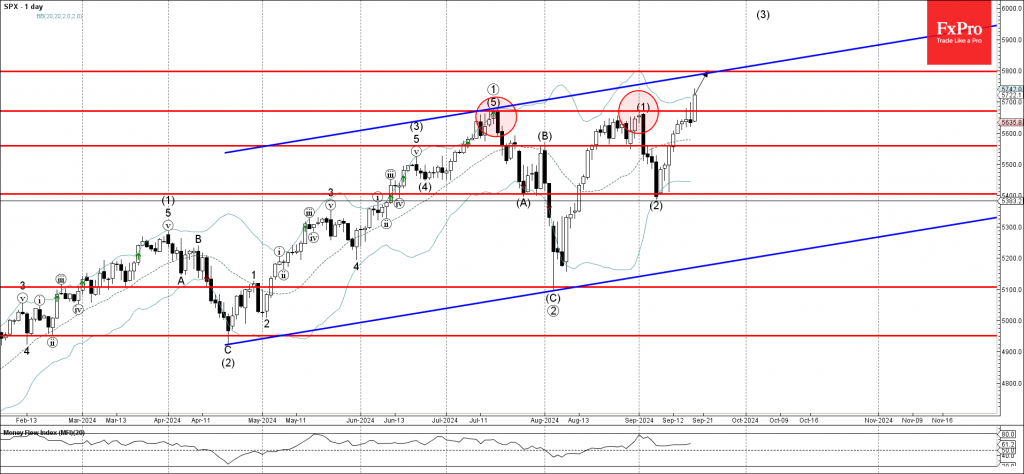

S&P 500 Wave Analysis

- S&P 500 broke key resistance level 5670.00

- Likely to rise to resistance level 5800.00

S&P 500 index today broke above the key resistance level 5670.00 (which stopped the previous impulse waves (5) and (1), as can be seen below).

The breakout of the resistance level 5670.00 continues the active intermediate impulse wave (3) from the start of September.

Given the clear daily uptrend, S&P 500 index can be expected to rise further to the next resistance level 5800.00 (intersecting with the weekly up channel from April).

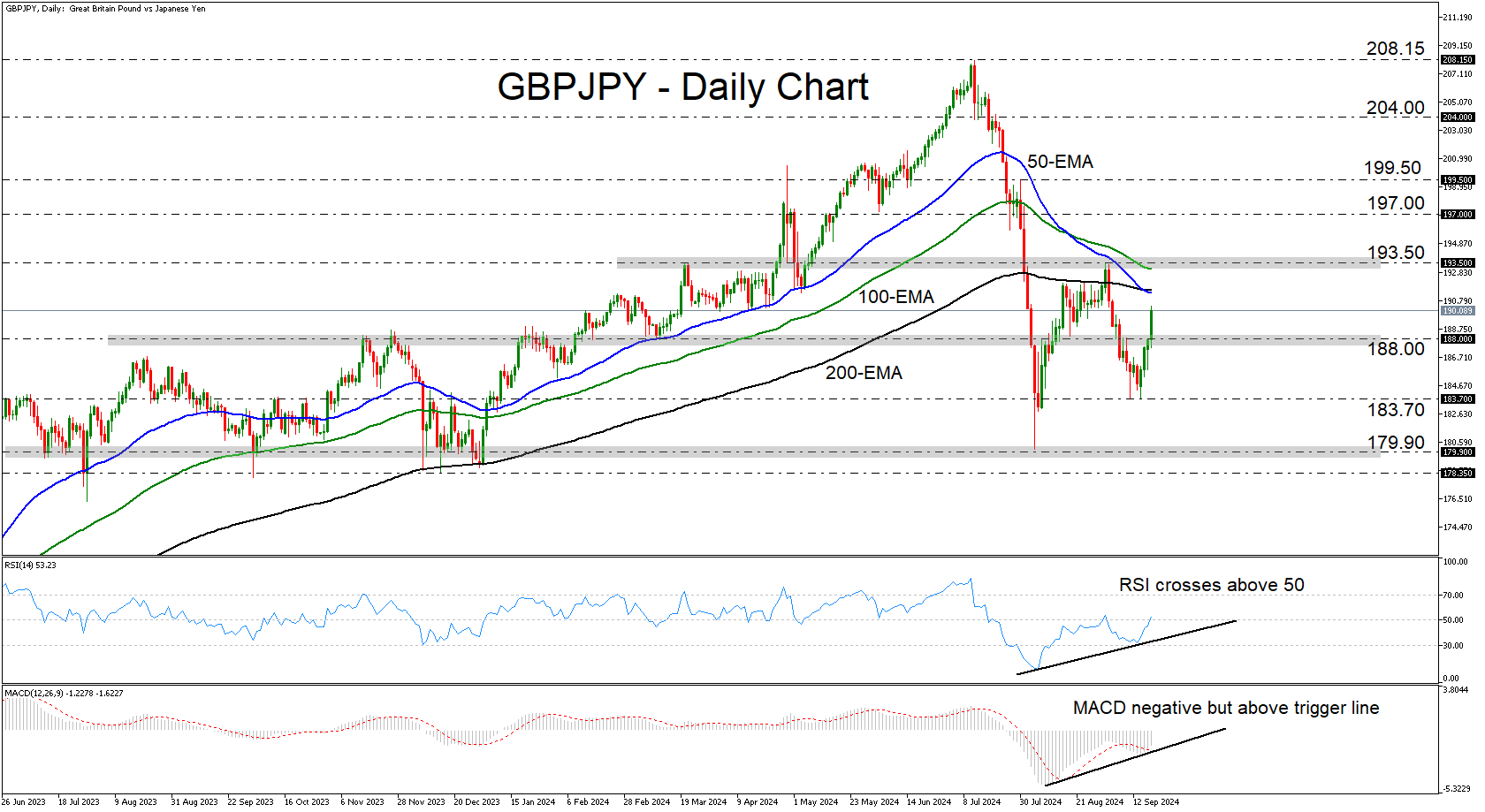

GBPJPY Surges Above 188.00 Key Barrier

- GBPJPY jumps above 188.00, confirming a higher low

- A break above 193.50 could brighten the picture

- A move below 183.70 may turn the outlook back to bearish

GBPJPY traded higher on Thursday, clearing the key resistance (now turned into support) barrier of 188.00. The move confirmed the higher high at 183.70, which cancels the bearish picture. However, the fact that the price remains below the important zone of 193.50 suggests that the outlook has not turned bullish either.

The oscillators are corroborating the notion that the bears may have jumped off the boat, at least for now. Similarly to the price action, both the RSI and the MACD have formed higher highs, with the former poking its nose above its equilibrium 50 line. The MACD, although negative, has moved above its trigger line.

For the outlook to brighten, the bulls would have to prove they are strong enough to push the action above the 193.50 barrier, a move that could take the pair above all the plotted moving averages as well. This could initially pave the way towards the 197.00 area, the break of which could see the bulls aim for the high of July 30 at 199.50.

The move signaling that the bears are back into the game may be a dip below the latest trough of 183.70. This may see scope for declines towards the low of August 5 at 179.90, or the 178.35 territory, which acted as a floor between July 2023 and January 2024.

To sum up, GBPJPY confirmed a higher low on the daily chart, but it has yet to form a clear uptrend structure. This means that the outlook has turned neutral for now.