Sample Category Title

Gold and Silver bounded in range, awaiting Dollar-driven breakout

Both Gold and Silver are currently still caught in near-term consolidations despite the rally late last week. Both metals have the potential to extend their recent gains, but a more pronounced decline in Dollar may be necessary to provide the needed momentum.

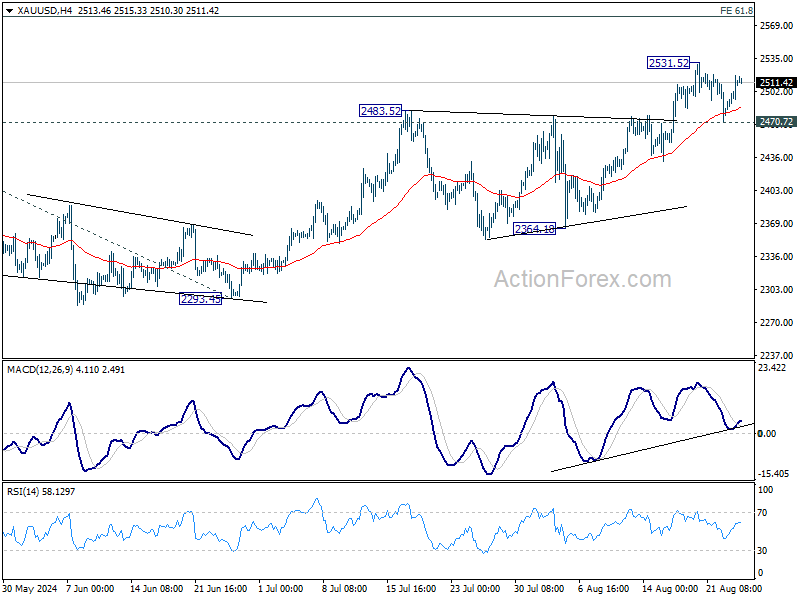

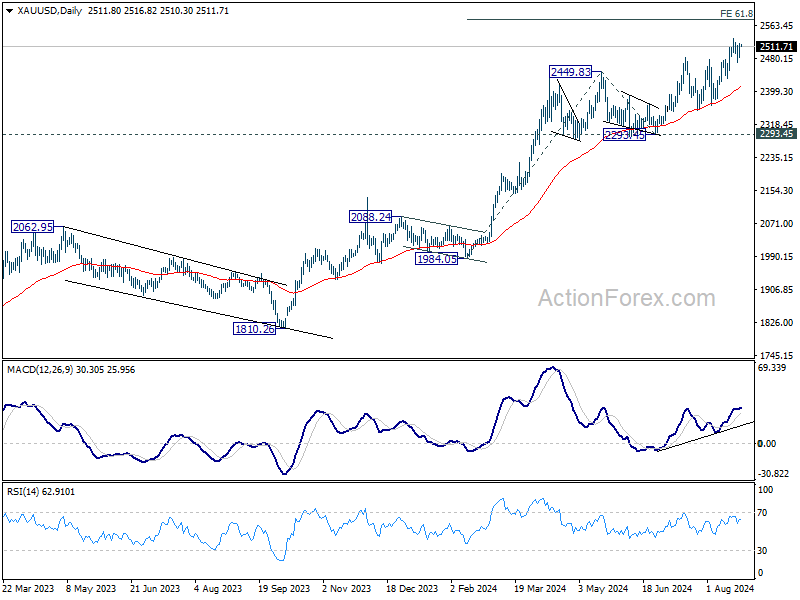

As for Gold, further rally is expected as long as 2470.72 support holds. Firm break of 2531.57 will resume the long term up trend and extend the record run. Next target is 61.8% projection of 1984.05 to 2449.83 from 2293.45 at 2581.30. However, break of 2470.72 will risk deeper pull back to 55 D EMA (now at 2412.87) first.

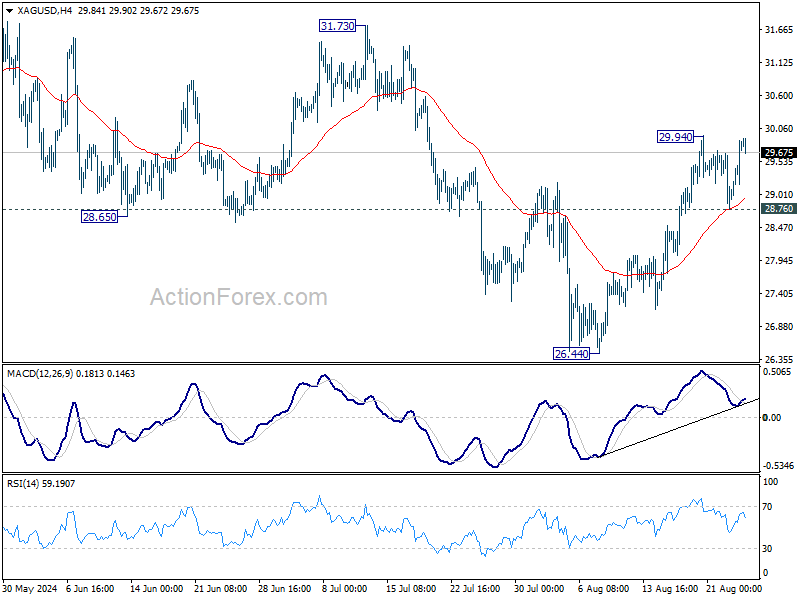

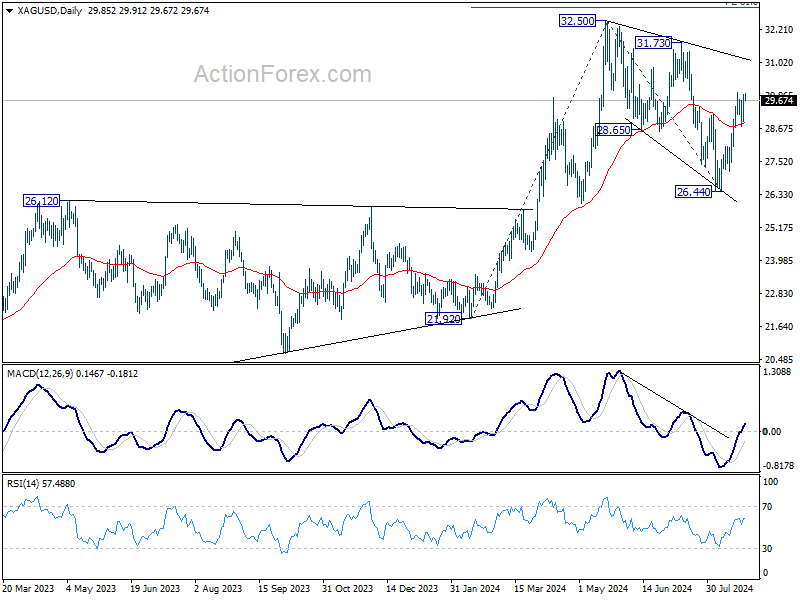

While Silver has been lagging Gold in its run, there is prospect of a catch up ahead. Corrective pattern from 32.50 has likely completed with three waves down to 26.44, after defending 26.12 resistance turned support. For now, further rise is in favor as long as 28.76 support holds. Break of 29.94 will target 31.73 resistance. Decisive break there will solidify this view and target 32.50 and above. However, break of 28.76 will dampen this immediate bullish case.

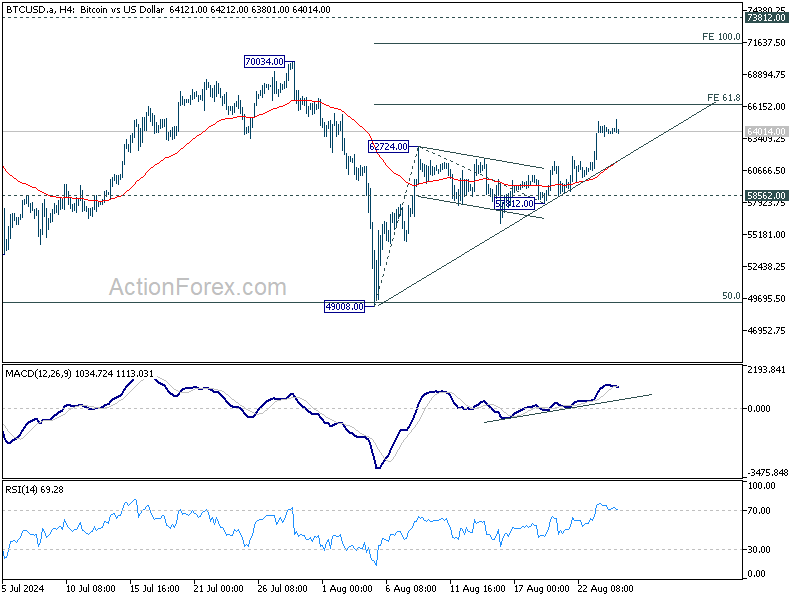

Bitcoin to face 66k hurdle as risk-on rally gains traction

Bitcoin surged last Friday and stayed firm throughout the weekend. The cryptocurrency broke through an important near-term resistance level, fueled by broad risk-on sentiment following Fed Chair Jerome Powell's indication of upcoming monetary easing. It now stands at a critical juncture, where the next move will determine whether it has completed the medium-term consolidation that began in March.

Technically, the break of 62724 confirmed resumption of the rebound from 49008. The strong break of 55 D EMA is also a near term bullish sign. It's possible that the corrective pattern from 73812 has completed 49008, after hitting 50% retracement of 24896 to 73812 at 49354.

However, to solidify the bullish case, Bitcoin will have to overcome the first hurdle at 61.8% projection of 49008 to 62724 from 57812 at 66288. Rejection by this level will keep the rebound from 49008 as just another leg in the corrective pattern from 73812. On the other hand, firm break of 66288 could prompt upside acceleration to 100% projection at 71528, and build up momentum for eventual breakout from the five-month range.

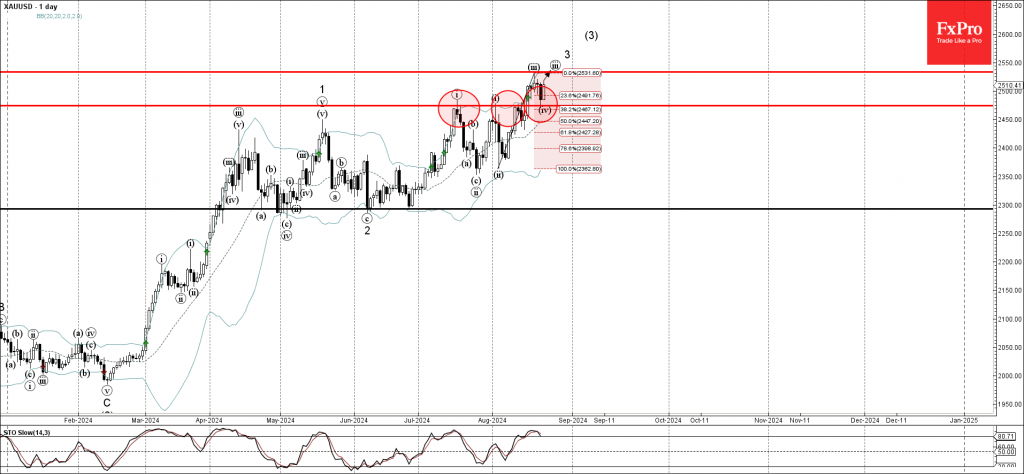

Gold Wave Analysis

- Gold reversed from key support level 2475.00

- Likely to rise to resistance level 2535.00

Gold just reversed up from the key support level 2475.00 (former strong resistance which stopped the previous impulse waves (i) and i) coinciding with the 38.2% Fibonacci correction of the previous sharp upward impulse from the start of August.

The upward reversal from the support level 2475.00 started the sub-impulse wave v of the higher impulse waves 3 and (3).

Given the clear daily uptrend, Gold can then be expected to rise to the next resistance level 2535.00 (top of the previous impulse wave iii).

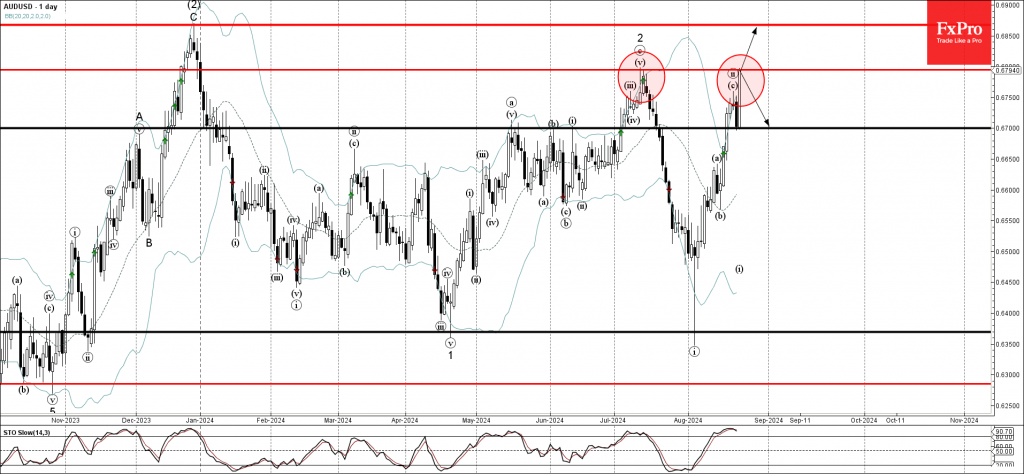

AUDUSD Wave Analysis

- AUDUSD approached key resistance level 0.6795

- Likely to rise to resistance level 0.6865

AUDUSD currency pair just approached the key resistance level 0.6795 (which stopped the previous minor correction 2 at the start of July) standing above the upper daily Bollinger Band.

The subsequent price behavior near the resistance level 0.6795 will affect how this currency pair will move in the coming trading sessions.

If the pair closes above the resistance level 0.6795, AUDUSD can then be expected to rise to the next resistance level 0.6865 (former multi-month high from December). Alternatively, AUDUSD can correct down to 0.6700.

Dollar at Risk of Resuming Medium-Term Downtrend as Fed Confirms Rate Cuts Ahead

Fed Chair Jerome Powell's highly anticipated speech at Jackson Hole didn't disappoint market participants, as he clearly signaled that the time for easing monetary policy has arrived. This declaration provided a notable boost to US stock markets on Friday, with major indexes ending the week on a positive note. Meanwhile, Dollar tumbled across the board, finishing as the worst-performing currency.

Dollar's decline seemed more driven by the surge in risk-on sentiment rather than a significant change in expectations for Fed rate cuts, as market pricing for future cuts remained largely unchanged compared to the previous week. While the conditions are now ripe for further depreciation of the greenback, much will hinge on the evolution of risk sentiment, particularly as major stock indexes approach their record highs.

Overall in the currency markets, Canadian Dollar ended as the second-worst performer, but by a distant to the greenback, as weighed down by inflation data that solidified expectations for another rate cut from BoC in the near future. Euro also struggled, becoming the third weakest currency, as weak Eurozone PMI data highlighted underlying fragilities in the region's economy.

On the flip side, New Zealand Dollar stood out as the strongest currency of the week, rebounding from its recent losses. Japanese Yen followed as the second strongest, supported by the determined hawkish tone from BoJ. Swiss franc also showed notable strength, while British Pound and Australian Dollar ended the week with in middle positions.

Dollar's Slide: Is Medium-Term Downtrend Back on as Fed Confirms Cuts are Coming?

Investors seemed pretty satisfied with Fed's communications last week, including insights from the July FOMC minutes and Chair Jerome Powell's speech at the Jackson Hole Symposium. While the messages delivered were largely in line with market expectations and didn't offer any groundbreaking revelations, the reassurance that monetary easing is coming was enough to keep investors content.

FOMC minutes revealed that a "vast majority" of participants viewed a rate cut at the upcoming meeting as likely appropriate, provided the economic data continues to align with expectations. Powell echoed this sentiment, declaring that "the time has come for policy to adjust." However, he refrained from specifying the exact timing or pace of future rate cuts, leaving the markets to speculate.

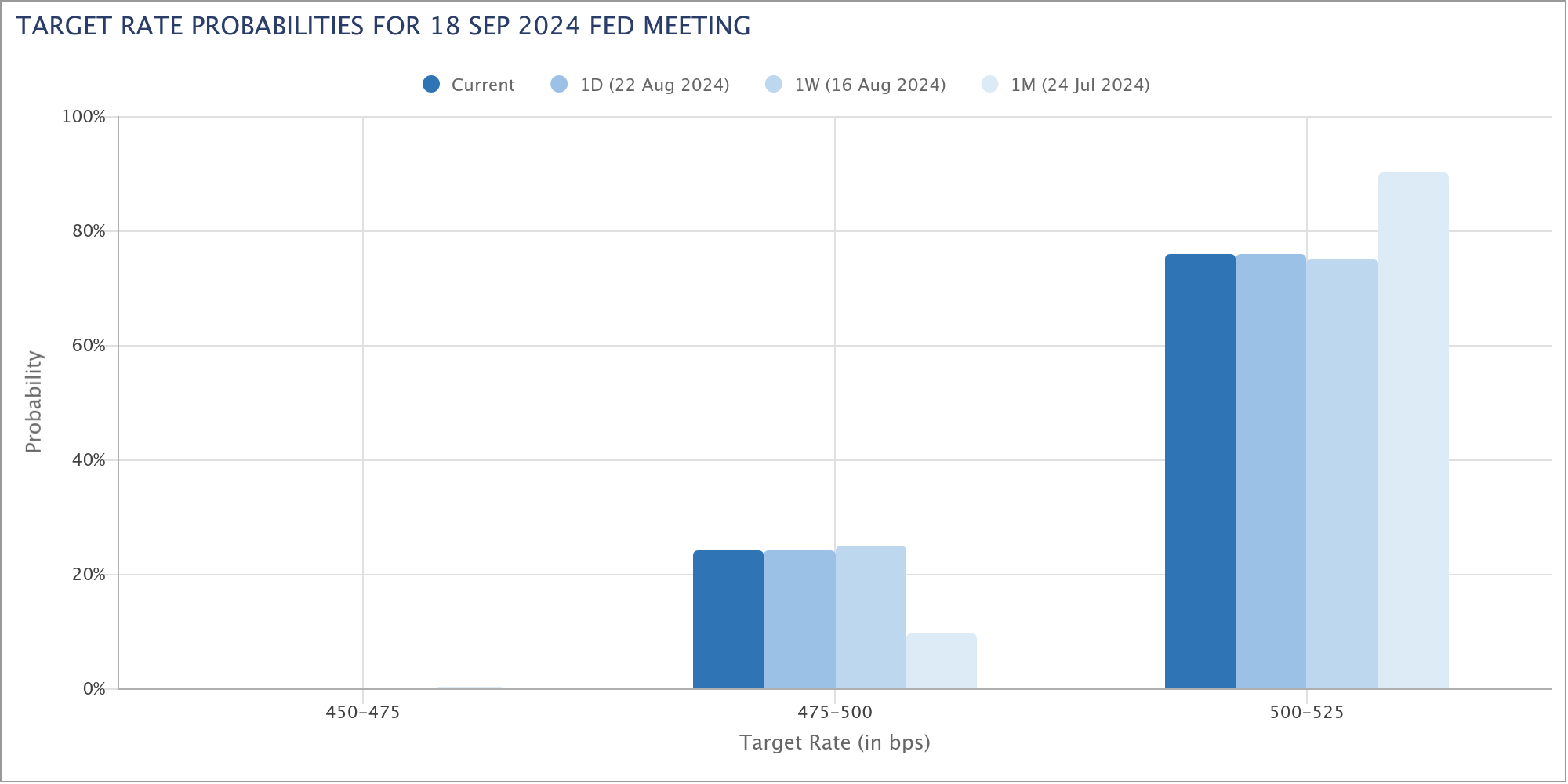

It's important to note that with the lack of new revelations, market pricing remains largely unchanged from the prior week. For the September meeting, a 25bps cut is fully priced in, with 24% chance of a more aggressive 50bps reduction.

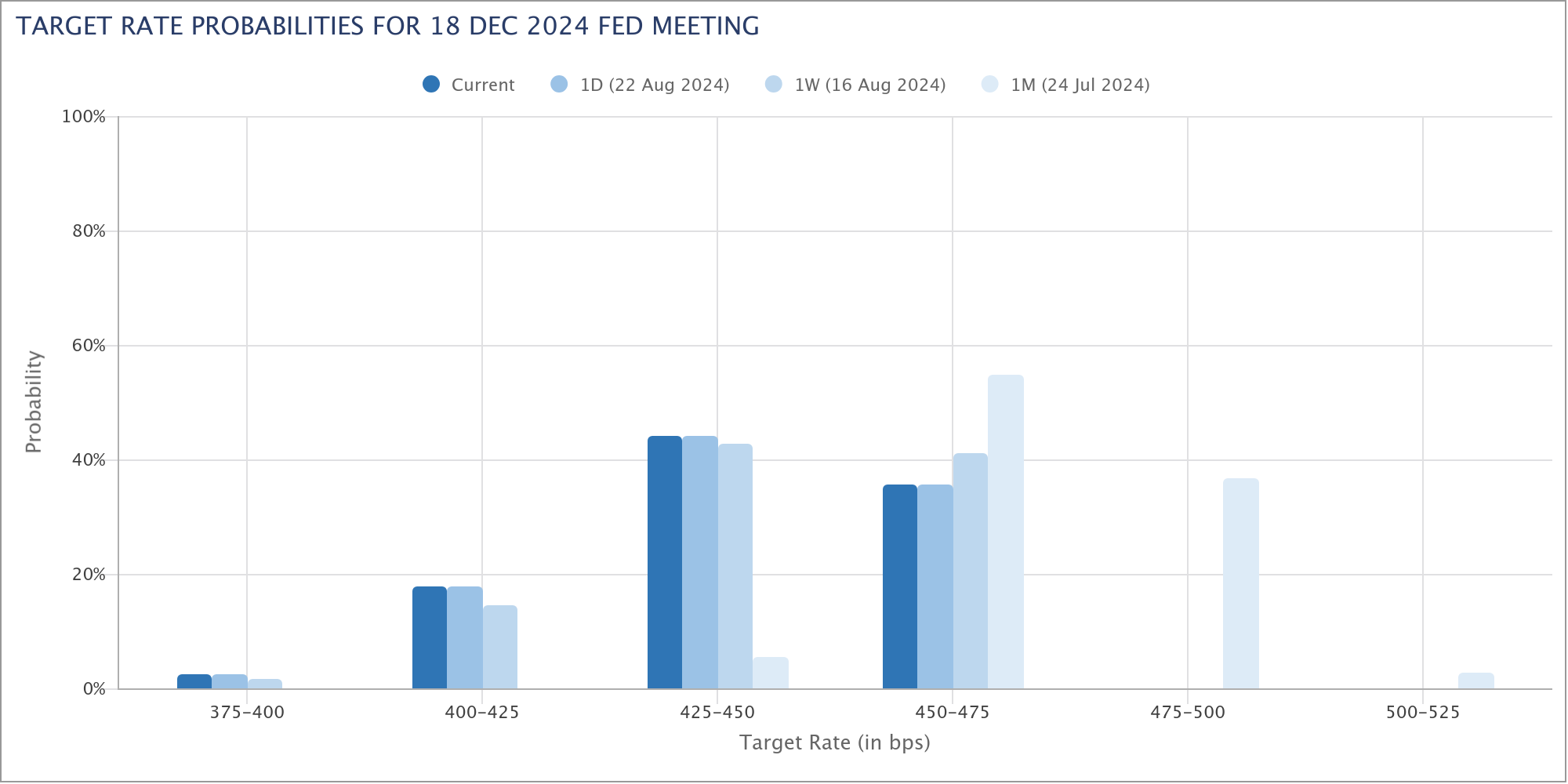

Looking further ahead, by the end of the year, markets are fully pricing in a total of 75bps in rate cuts, with a 65% probability that the total reduction could reach or exceed 100bps.

This outlook has weighed heavily on Dollar, which has tumbled broadly against its peers. The prospect of Fed matching or even surpassing other major central banks in terms of monetary easing this year is putting downward pressure on the greenback. ECB, for instance, is expected to cut rates again in September and possibly once more in December, making a total of 75 basis points in cuts, including the June adjustment. These meetings will also feature updated economic forecasts from the ECB.

Meanwhile, BoE remains a wildcard, with uncertainty surrounding whether it will cut rates in September. A more likely scenario is a single cut in November when new forecasts are released. Including the August reduction, BoE could cut just 50bps this year.

Dollar index's fall from 106.13 continued last week and the strong break of medium term trend line support (as seen in the W chart) argues that down trend from 114.77 might be ready to resume (2022 high).

Near term outlook will stay bearish as long as 103.67 resistance holds. Firm break of 100.61 support will solidify this bearish case. Further break of 99.57 (2023 low) will target 61.8% projection of 114.77 to 99.57 from 106.13 at 96.73, or even further too long term channel support at around 94.61 (M chart) before forming a bottom.

The bearish sentiment surrounding Dollar is also supported by the outlook for 10-year US Treasury yield. Fall from 4.737 is seen as the third leg of the corrective pattern from 4.997. Further decline is expected as long as 4.022 resistance holds, to 100% projection of 4.997 to 3.785 from 4.737 at 3.525.

Indeed, considering that 10-year yield is now correcting whole up trend from 0.398 (2020 low), there is risk of even deeper decline to 3.253 cluster support (38.2% retracement of 0.398 to 4.997 at 3.240) before completing the correction.

However, risk sentiment remains a critical wild card that could shift these developments. While major stock indexes ended higher last week, they remain capped below the record highs set in July. There is skepticism about whether the current momentum can extend or even surpass these records.

Powell's emphasis on supporting the labor market, particularly in the event of significant deterioration, suggests that upcoming job data could have complex impacts on market sentiment.

Strong job data could reduce the urgency for aggressive rate cuts, while weaker data might reignite recession fears but also push the Fed toward faster easing. This raises the question of whether positive economic news will be interpreted as truly positive or whether it might trigger concerns about Fed's next move.

This creates a complex dynamic where good news could be seen as bad news, and vice versa, depending on how markets interpret the data.

Technically, further rally is in favor in DOW as long as 40584.47 support holds. Firm break of 41376.00 would confirm resumption of long term up trend. Nevertheless, break of 40584.47 will indicate initial rejection by 41376.00, and bring deeper pull back to 55 D EMA (now at 39843.95) at least.

Further rise is expected in NASDAQ as long as 55 D EMA (now at 17351.12) holds, for retesting 18671.06 high. However, decisive break of 55 D EMA will argue that the corrective pattern from 18671.06 has already started the third leg, and target 15708.53 support again.

Yen Resilient with BoJ's Commitment to Easing Adjustments,

Japanese Yen ended as one of the top performers last week, as its recent pullback lost steam. The currency found some support from BoJ Governor Kazuo Ueda, who, during a special parliamentary session, reaffirmed the commitment to reduce monetary easing if economic and price trends align with their forecasts. Despite recent market volatility, Ueda made it clear that there is "no change to our basic stance to adjust the degree of monetary easing."

Supporting Ueda's position, IMF Chief Economist Pierre-Olivier Gourinchas emphasized that Japan’s inflation is now above 2%, and expectations are aligning with or even slightly exceeding BoJ's target. Gourinchas noted that Japan’s gradual shift away from its ultra-loose monetary policy is a "good development for Japan". He suggested there is “scope for further normalizations of monetary policy” with potential for gradual increases in policy rates going forward.

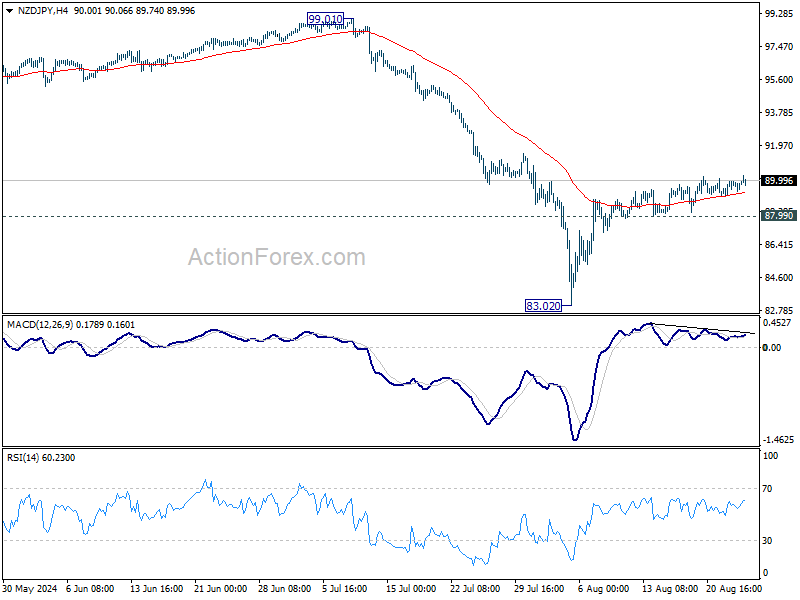

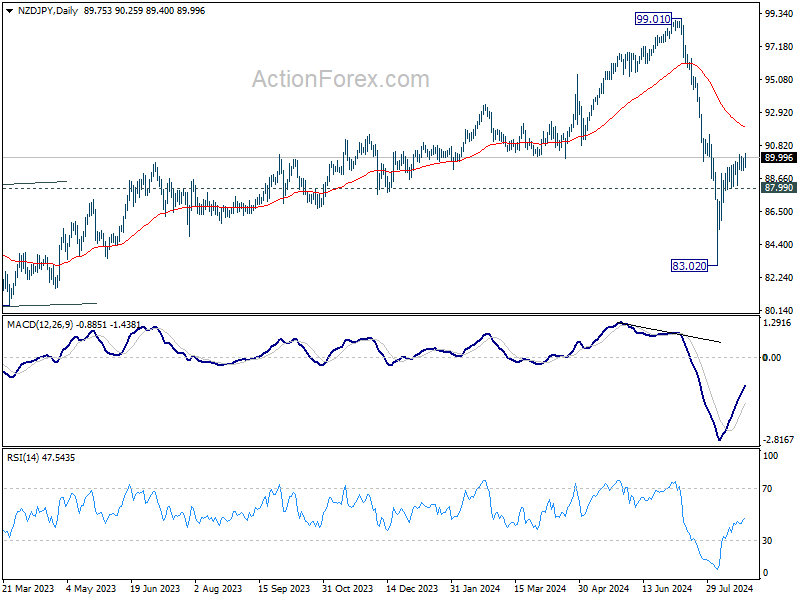

While New Zealand was on paper the best performer last week, it just outperformed Yen slightly. For now, further rise is in favor as NZD/JPY as long as 87.99 minor support holds, towards 55 D EMA (now at 91.44). However, considering bearish divergence condition in 4H MACD, break of 87.99 will argue that the rebound from 83.02 is over, and bring retest of this low.

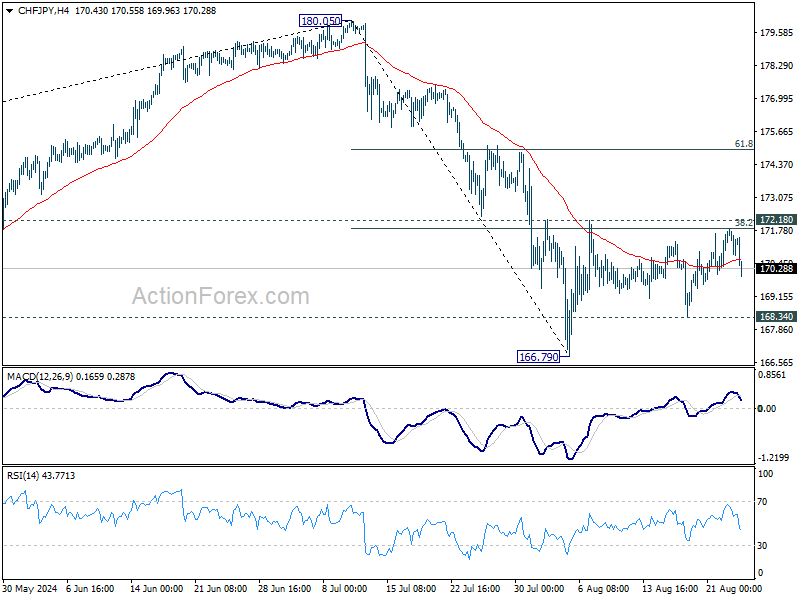

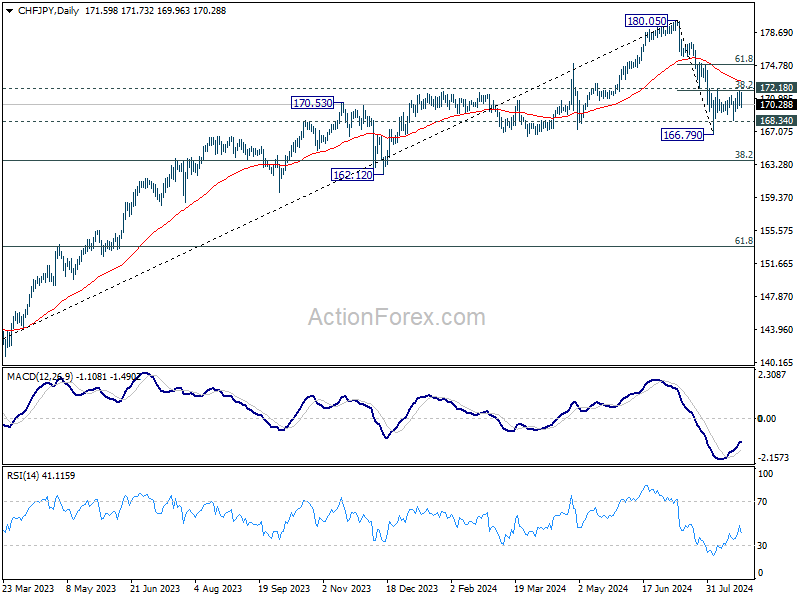

CHF/JPY has failed to break through 172.18 resistance and 38.2% retracement of 180.05 to 166.79 at 171.85 for the second time. Break of 168.34 support will argue that fall from 180.05 is ready to resume through 166.79, as a correction to up trend from 137.40.

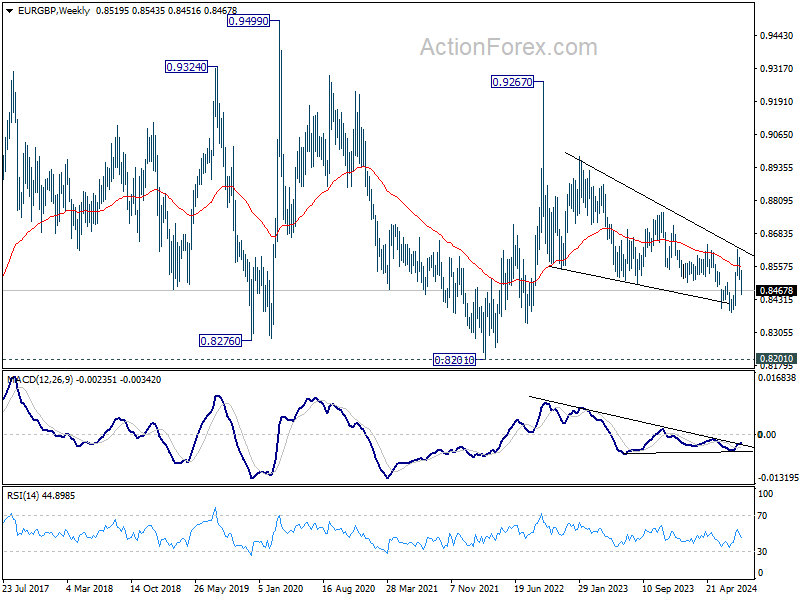

EUR/GBP Accelerates Down as PMIs Highlight Contrasting Economic Outlook

EUR/GBP accelerates down as PMI highlights contrasting economic strength Sterling outshined Euro last week, supported by stronger PMI data that highlighted solid expansion across both the UK manufacturing and services sectors in August. The UK economy demonstrated a combination of stronger growth and improved job creation. While the decline in inflation pressure as indicated in the PMI report might provide BoE with an opportunity to consider another rate cut, the robustness of the underlying economy also allows the central bank some leeway to hold off on such a move for the next meeting. This is particularly relevant given the tight divide within the MPC between hawks and doves.

In contrast, Eurozone’s economic picture is showing signs of strain as seen in their PMIs. While French services sector received a temporary boost from the Olympic Games, this appears to be an outlier rather than a sign of sustained strength. The broader Eurozone fundamentals remain shaky, with Germany’s economic troubles at the forefront. The country’s manufacturing sector continues to struggle, and these difficulties are beginning to spill over into the services sector. The increased likelihood of Germany experiencing a second consecutive quarter of negative growth raises the specter of a renewed recession in Europe’s largest economy.

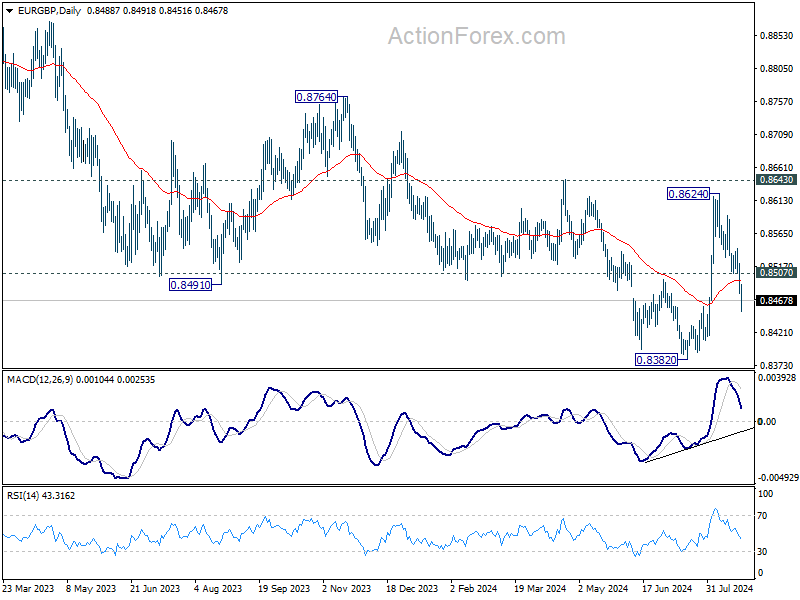

EUR/GBP's downside acceleration last week suggests that rebound from 0.8382 has completed at 0.8624 Rejection by 0.8643 resistance keeps the medium term down trend intact. Also, the break below both 55 D and 55 W EMA are also bearish signal. Retest of 0.8382 low should be seen next. The question now is whether EUR/GBP would accelerate downward through 0.8382 to resume the larger down trend from 0.9267 (2022 high).

EUR/USD Weekly Outlook

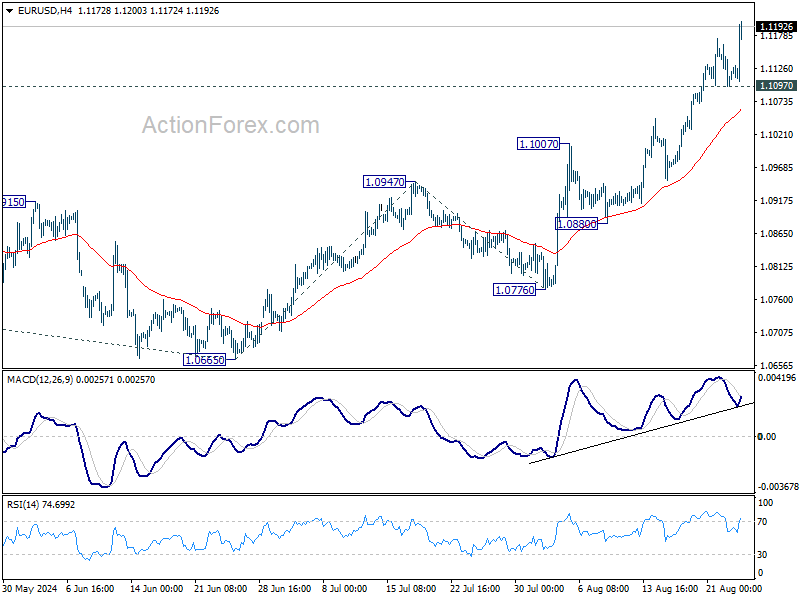

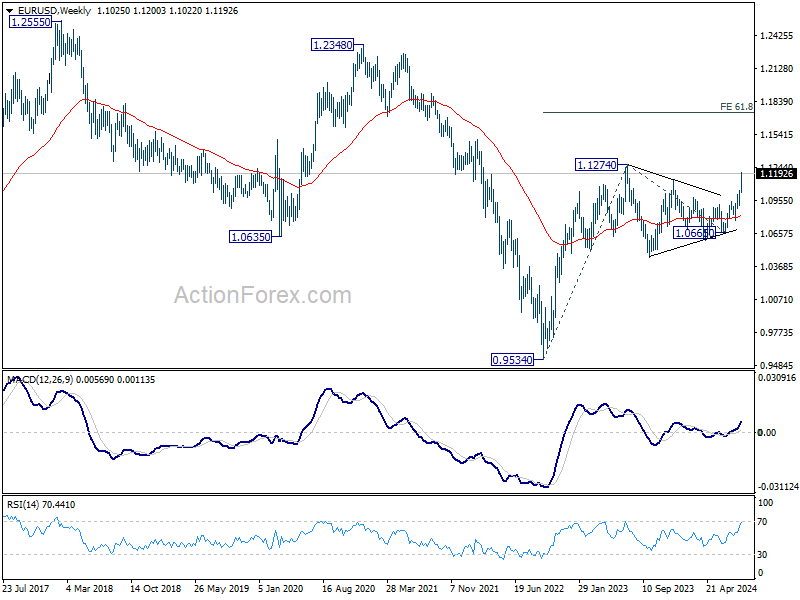

EUR/USD's rally continued last week and the strong break of 1.1138 resistance argues that larger up trend may be resuming. Initial bias is on the upside this week for t 161.8% projection of 1.0665 to 1.0947 from 1.0776 at 1.1232, and then 1.1274 high. On the downside, below 1.1097 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

In the long term picture, a long term bottom is in place at 0.9534 (2022 low). The strong break of 55 M EMA (now at 1.1018) is taken as the first sign of bullish trend reversal. But still, firm break of 1.2348 structural resistance is needed to confirm. Otherwise, price actions from 0.9534 could still develop into a consolidation pattern.

EUR/USD Weekly Outlook

EUR/USD's rally continued last week and the strong break of 1.1138 resistance argues that larger up trend may be resuming. Initial bias is on the upside this week for t 161.8% projection of 1.0665 to 1.0947 from 1.0776 at 1.1232, and then 1.1274 high. On the downside, below 1.1097 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

In the long term picture, a long term bottom is in place at 0.9534 (2022 low). The strong break of 55 M EMA (now at 1.1018) is taken as the first sign of bullish trend reversal. But still, firm break of 1.2348 structural resistance is needed to confirm. Otherwise, price actions from 0.9534 could still develop into a consolidation pattern.

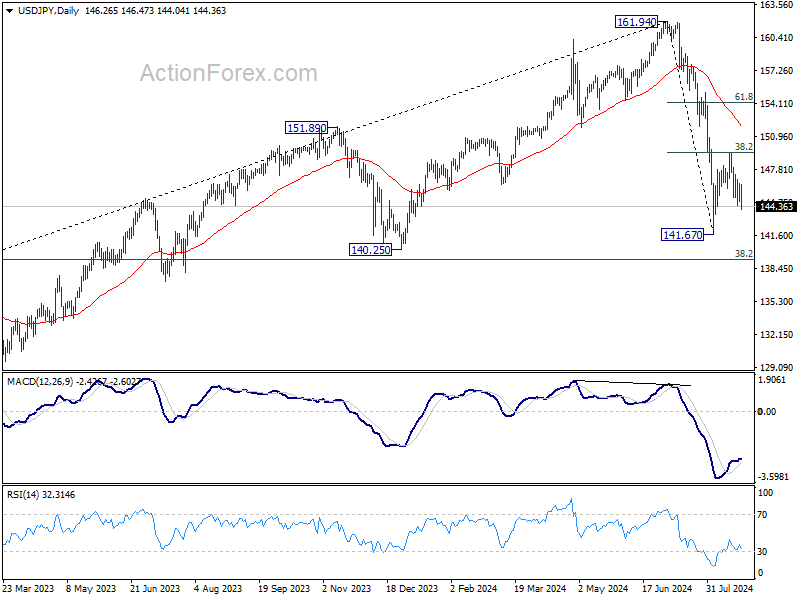

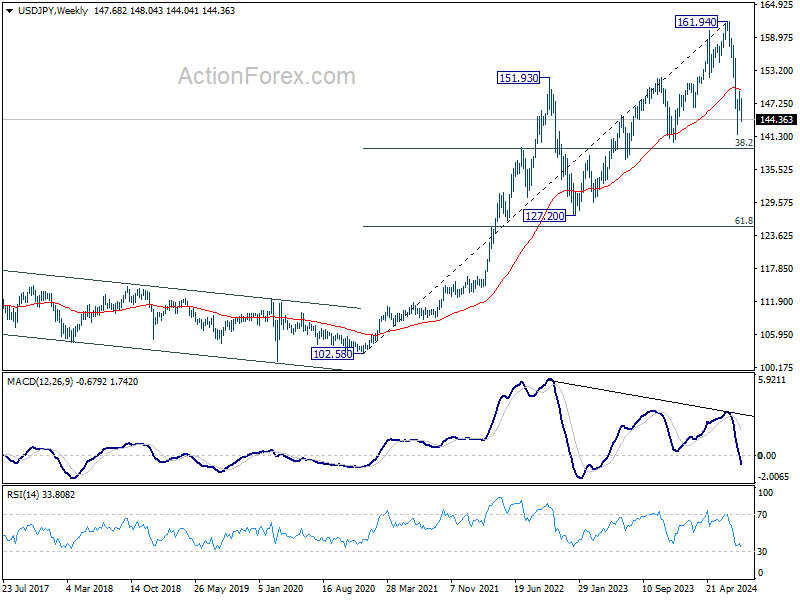

USD/JPY Weekly Outlook

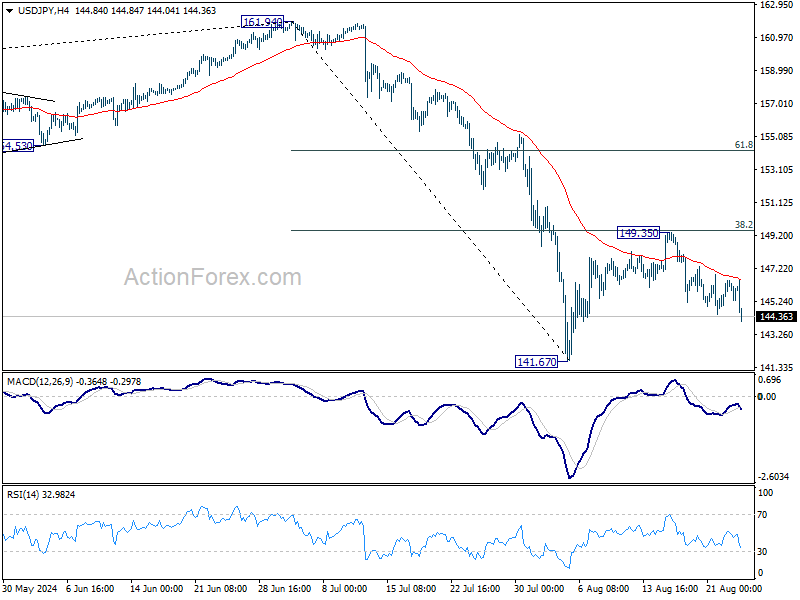

USD/JPY gyrated lower last week even though momentum is a bit unconvincing. Still, the development suggests that rebound from 141.67 has completed at 149.35, after rejection by 38.2% retracement of 161.94 to 141.67 at 149.41. Initial bias is on the downside this week for retesting 141.67 low. Firm break there will resume the whole fall from 161.94 to 140.25 support next. For now, risk will stay on the downside as long as 149.35 resistance holds, in case of recovery.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.59) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. However, a medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 132.73).

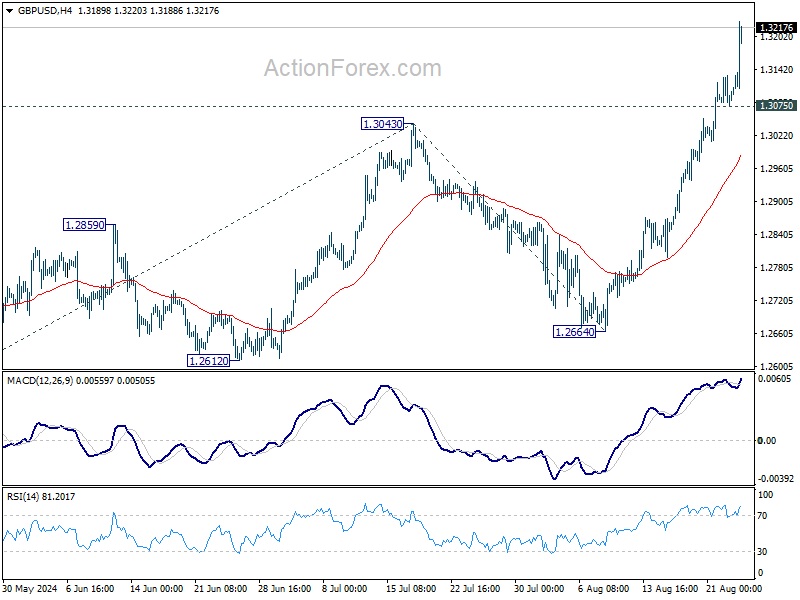

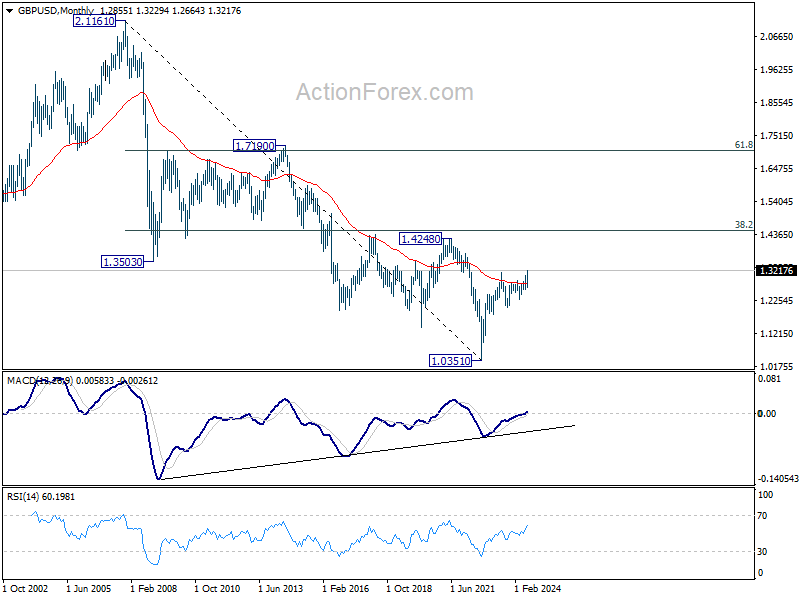

GBP/USD Weekly Outlook

GBP/USD's rally accelerated higher last week and the break of 1.3141 resistance confirms larger up trend resumption. Initial bias remains on the upside this week for 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. On the downside, below 1.3075 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, up trend from 1.0351 (2022 low) is resuming. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

In the long term picture, as long as 1.2298 support holds, rise from 1.0351 long term bottom is expected to continue. The strong break of 55 EMA (now at 1.2814) is a sign of bullish trend reversal. Yet, break of 1.4248 structural resistance is needed confirm. Otherwise, price actions from 1.0351 could just be part of a consolidation pattern.

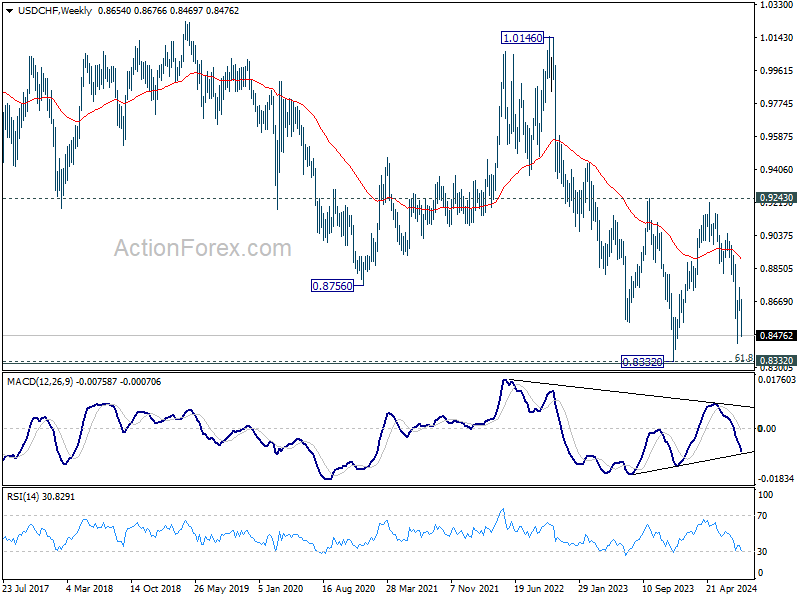

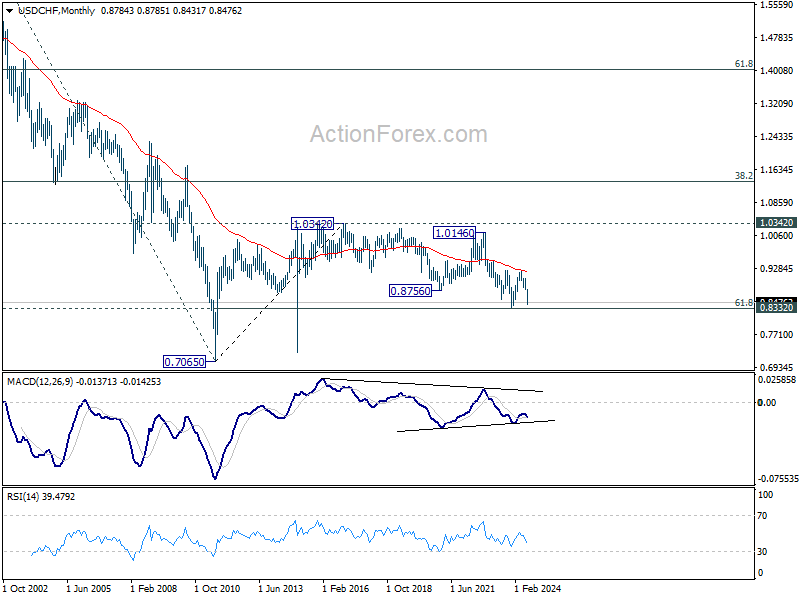

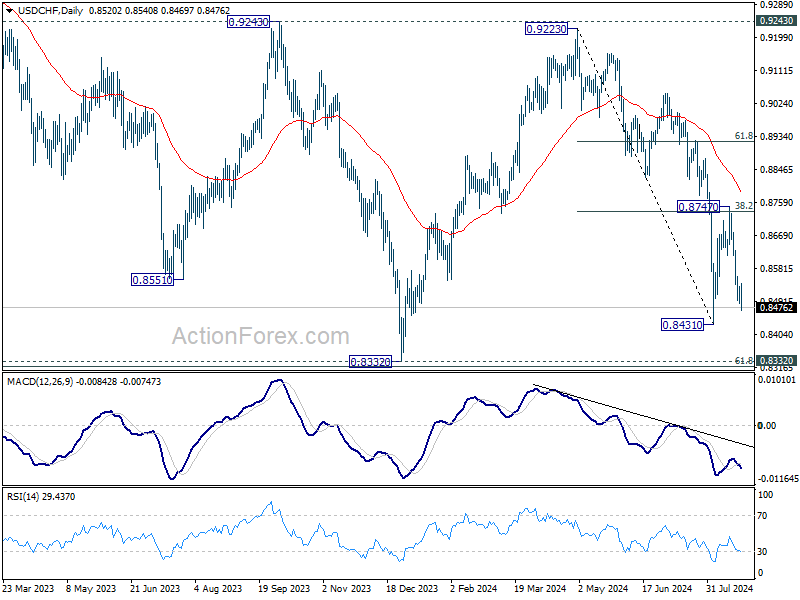

USD/CHF Weekly Outlook

USD/CHF's extended decline last week suggests that rebound from 0.8431 has completed at 0.8747, after rejection by 38.2% retracement of 0.9223 to 0.8431 at 0.8734. Initial bias is on the downside this week for retesting 0.8431 support first. Firm break there will resume whole decline from 0.9223 towards 0.8332 low. On the upside, above 0.8540 minor resistance will turn intraday bias neutral.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Rejection by 55 M EMA suggest that this fall is in progress. Break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317 will pave the way back to 0.7065.