Sample Category Title

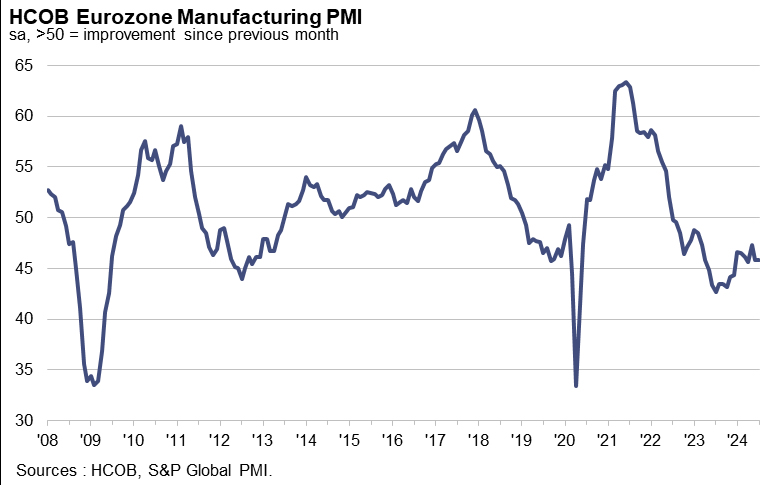

Eurozone PMI manufacturing finalized at 45.8, recovering taking a hit

Eurozone's PMI Manufacturing was finalized at 45.8 in July, unchanged from June, indicating ongoing contraction. PMI Manufacturing Output fell from 46.1 to 45.6, a 7-month low. Input costs increased at the fastest rate in a year and a half.

Among countries, Greece led with a PMI of 53.2, a 7-month low. Spain recorded 51.0, a 6-month low. Ireland reached a 5-month high at 50.1, but the Netherlands fell to 49.2, a 6-month low. Italy showed a 4-month high at 47.4, France hit a 6-month low at 44.0, Germany a 3-month low at 43.2, and Austria a 4-month low at 43.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that the belief in the Eurozone's recovery "is taking a hit." He emphasized that the decline in production has "intensified" doubts, prompting a likely downgrade in GDP growth forecast from 0.8%. Industrial activity weakened broadly, with only Greece and Spain seeing meaningful growth, though momentum there also slowed. Austria and Germany displayed the greatest weakness.

WTT: Top Trade Ideas for August

For the month of August, I have my eyes set on three pairs for my swing trading opportunities during the course of the month. Asides these three, most of my other trade ideas will be executed on lower timeframes, and with more conservative targets in mind. Do note, as always, that these are my personal ideas, and do not serve as a financial advise.

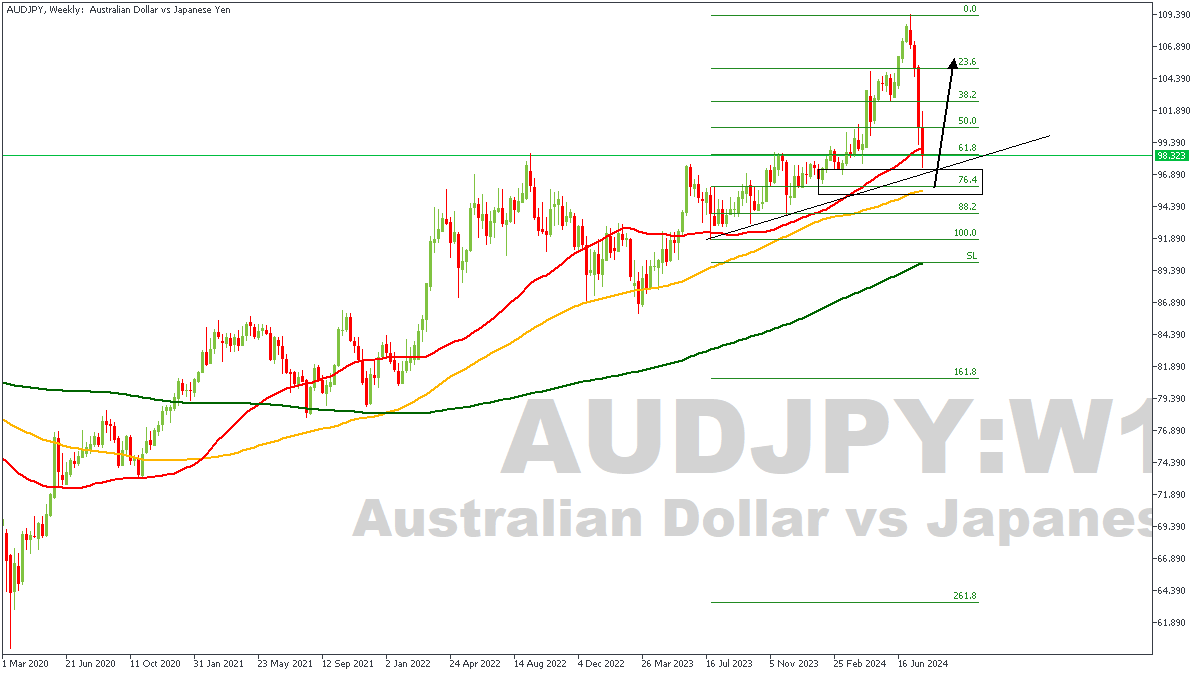

AUDJPY – W1 Timeframe

Without altering or challenging the course of the moving averages and their bullish array, we see price head into the 100-period moving average on the weekly timeframe of AUDJPY as a likely area of support. In line with this, we also see the weekly timeframe demand zone which overlaps the weekly timeframe pivot, and the trendline support that cuts across them both; come within the reach of the price action – implying quite simply that prices may reverse bullish from the area of confluence.

Analyst’s Expectations:

- Direction: Bullish

- Target: 105.246

- Invalidation: 95.165

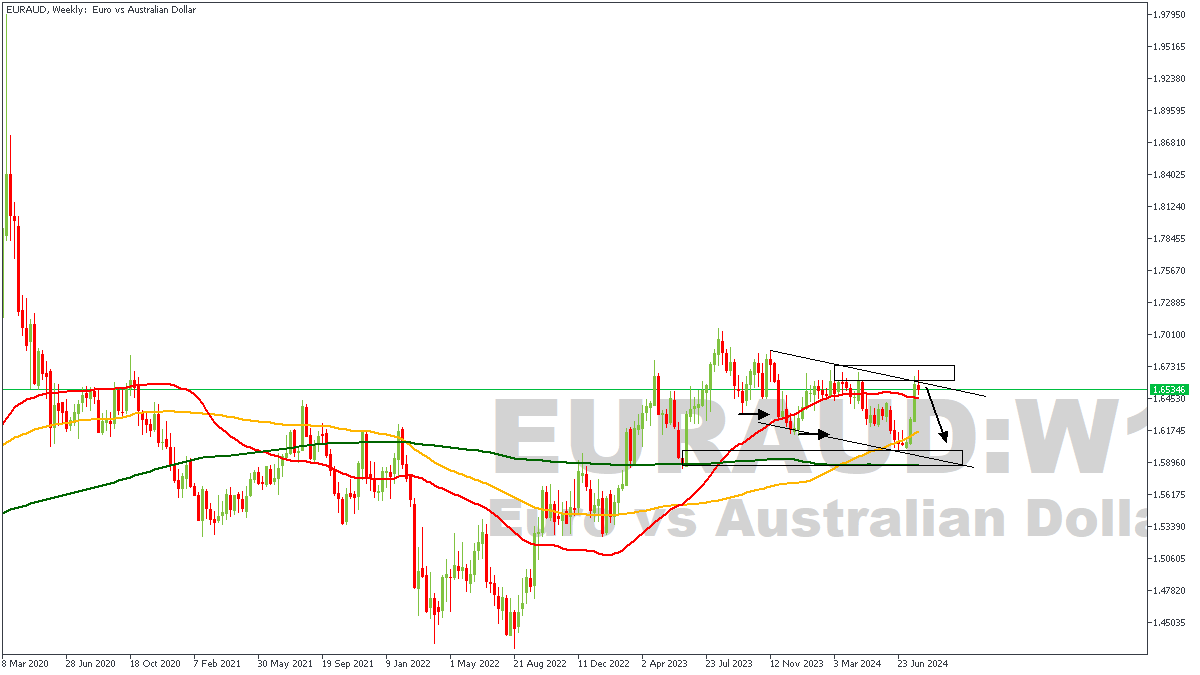

EURAUD – W1 Timeframe

There is a descending channel on the weekly timeframe of EURAUD; which means the outcome could be a breakout, or a formidable rejection. To the left of the current price point, we see price has broken structure downwards a few times in the past, leading me to look for the supply zone responsible for the bearish break of structure. That supply zone, coupled with the trendline resistance, as well as the overbought RSI (Relative Strength Index) are my basis for expecting a bearish outcome from all of this.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.62553

- Invalidation: 1.68862

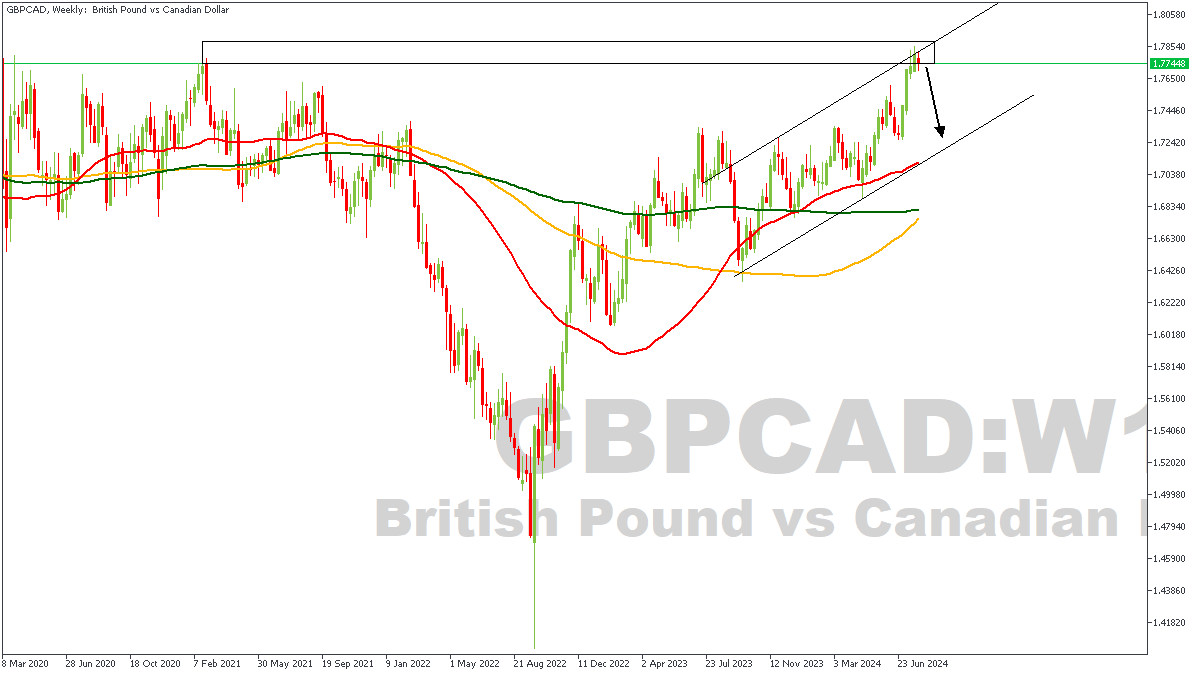

GBPCAD – W1 Timeframe

On the weekly timeframe chart of GBPCAD as shown on the chart, we see price trade into the weekly timeframe supply zone, whilst staying within the confines of a rising channel. Price has initially been rejected off the intersection of the resistance trendline, and the supply zone, and may very well reverse completely from the highlighted zone; albeit, lower timeframes hold the trigger for a bearish scenario.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.73661

- Invalidation: 1.78949

USD/JPY Falls Below 150 Yen Per Dollar

The yen was last this strong in mid-March this year. News from central banks contributed to the decline in USD/JPY.

Yesterday, the Bank of Japan raised interest rates to levels not seen in the past 15 years. Conversely, the Fed kept rates unchanged as expected but "opened the door" for a possible cut in September, according to Reuters. This news weakened the USD and provided a bullish boost to U.S. stock markets.

This shift highlights the collapse of the "carry trade" strategy, where high U.S. rates and low Japanese rates supported the rise of USD/JPY. From early 2023 to the July peak in 2024, USD/JPY rose by about 23%, but it started declining amid news of Bank of Japan's currency interventions.

On July 25, analysing the USD/JPY chart, we:

→ Constructed a descending channel (shown in red);

→ Predicted a scenario with a technical rebound from the lower boundary of the red channel.

Since then, USD/JPY climbed to the psychological mark of 155 yen per dollar on July 30, where the downtrend resumed after a false breakout.

How might the USD/JPY situation develop?

Technical Analysis of USD/JPY Today:

→ The chart forms a structure of swing extremes A-B-C-D-E-F-G. Notably, each subsequent recovery is about 50% of the previous downward impulse, indicating dominant supply forces. The expanding channel, shown in purple, also confirms this.

→ The psychological level of 150 yen per dollar may act as support, mirroring the resistance at 155 yen. Today's price action shows signs of demand activation below 150.

Therefore, it's possible that:

→ After a decline of over 8% from peak A, bears may want to take profits;

→ A corrective move H→I towards the upper purple boundary could form.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

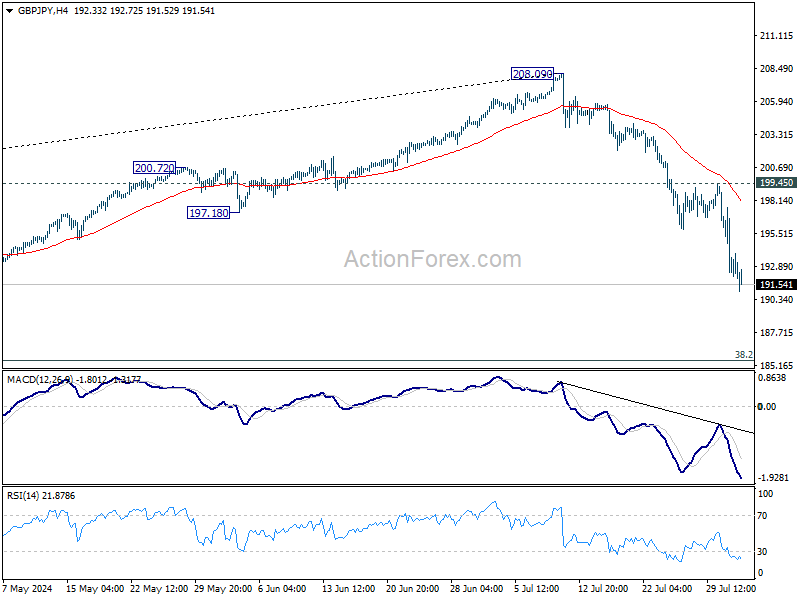

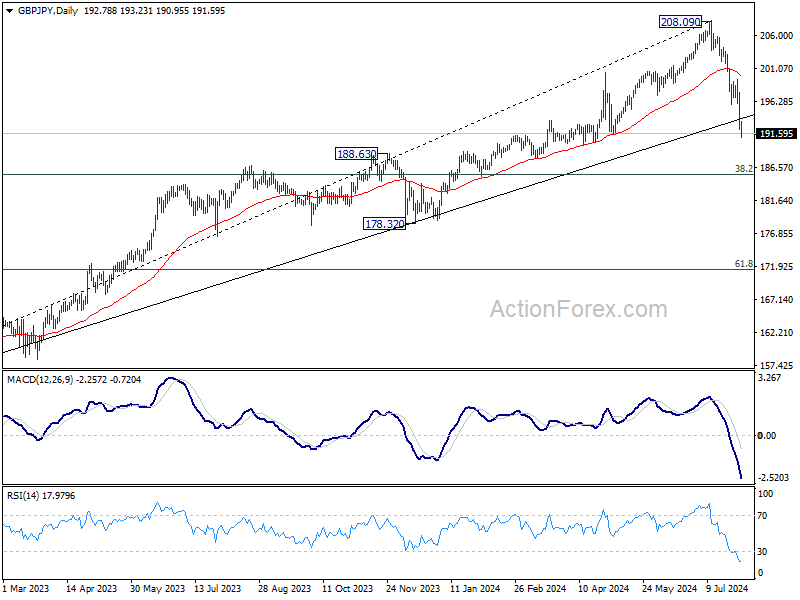

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.80; (P) 194.20; (R1) 196.23; More...

GBP/JPY's fall from 208.09 continues today and intraday bias stays on the downside. Current decline is a larger scale correction and should target 185.49 fibonacci level. For now, outlook will continue to stay bearish as long as 199.45 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in W MACD, 208.09 might be a medium term top and fall from there could already be correcting whole up trend from 148.93 (2022 low). Risk will now stay on the downside as long as 55 D EMA (now at 199.93) holds. Deeper fall would be seen to 38.2% retracement of 148.93 to 208.09 at 185.49.

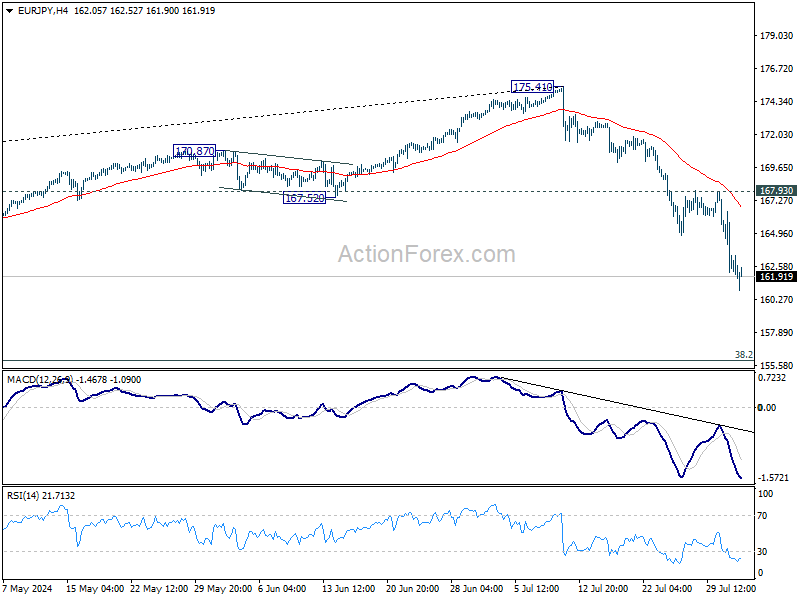

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.76; (P) 163.65; (R1) 165.29; More...

EUR/JPY's fall from 175.41 is in progress and intraday bias remains on the downside. This decline should be a larger scale correction and should target 155.91 fibonacci level next. On the upside, break of 167.93 resistance is needed to confirm short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, break of 164.29 resistance turned support indicates that fall from 175.41 medium term top is at least correcting the rise from 124.73, with risk of bearish trend reversal. Deeper decline would be seen to 38.2% retracement of 124.37 to 175.41 at 155.91. This will now remain the favored case as long as 55 D EMA (now at 169.17) holds, even in case of strong rebound.

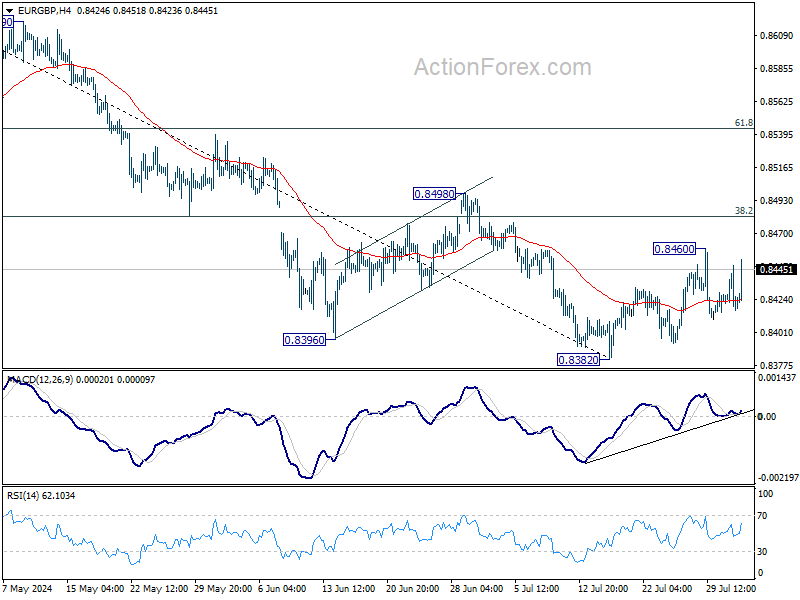

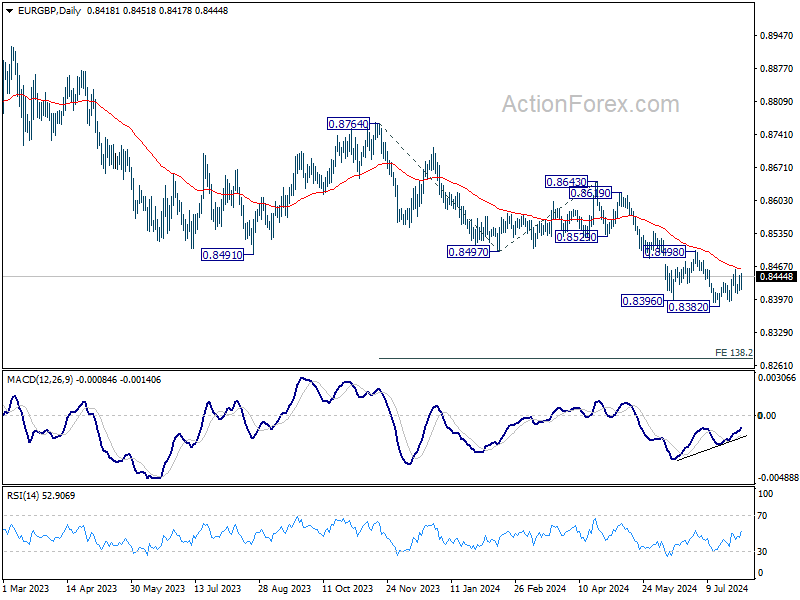

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8409; (P) 0.8429; (R1) 0.8441; More....

Intraday bias in EUR/GBP remains neutral for the moment. Consolidation from 0.8382 might extend with stronger recovery. But outlook continues to stay bearish with 0.8498 resistance intact. Firm break of 0.8382 will resume larger down trend next target will be 138.2% projection of 0.8764 to 0.8497 from 0.8463 at 0.8274.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 key support (2022 low). For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of strong rebound.

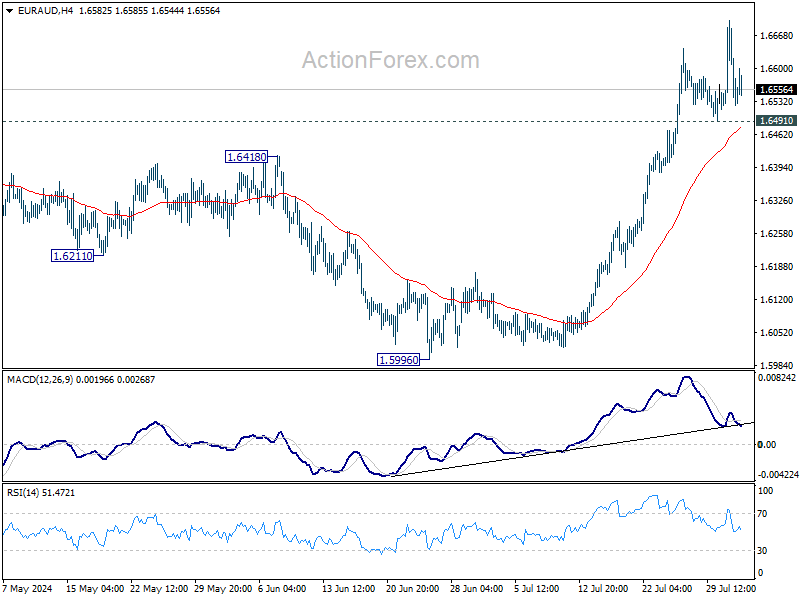

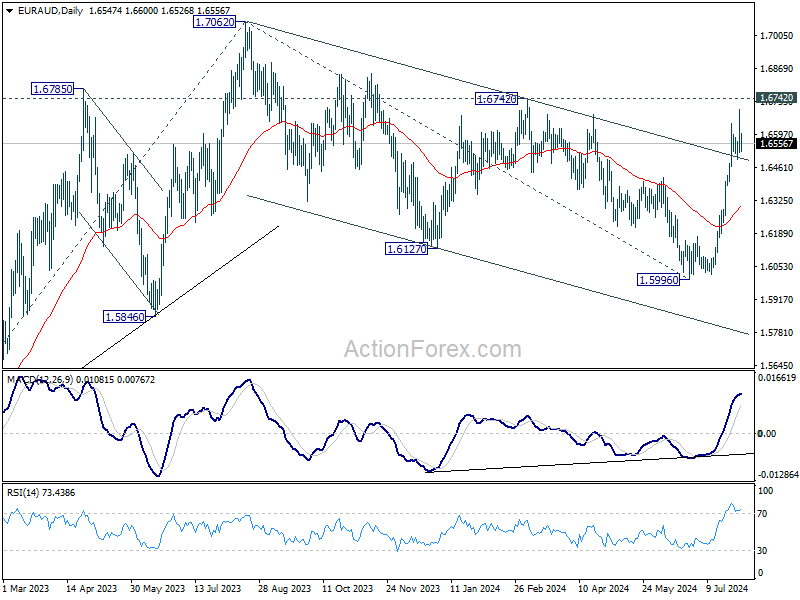

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6482; (P) 1.6592; (R1) 1.6659; More...

Further rise is expected in EUR/AUD with 1.6491 support intact. As noted before, corrective fall from 1.7062 should have completed with three waves down to 1.5998. Firm break of 1.6742 will argue that larger up trend is going to resume through 1.7062 high. On the downside, however, break of 1.6491 support will delay the bullish case and bring retreat first.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) and could have completed after hitting 38.2% retracement of 1.4281 to 1.7062 at 1.6000. On resumption next target will be 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. This will now remain the favored case as long as 55 D EMA (now at 1.6296) holds.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9480; (P) 0.9522; (R1) 0.9549; More....

EUR/CHF's fall from 0.9928 resumed by breaking through 0.9476 support. Intraday bias is now on the downside. Further decline should be seen to 100% projection of 0.9928 to 0.94767 from 0.9772 at 0.9320. On the upside, break of 0.9605 resistance is needed to confirm short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, with 1.0095 key medium term resistance intact, price actions from 0.9252 (2023 low) are seen as a corrective pattern. Fall from 0.9928 is seen as the second leg that's in progress to retest 0.9252 low. But strong support should be seen there to extend the corrective pattern with another rising leg. In any case, medium term outlook will be neutral at best as long as 1.0095 structural resistance holds.

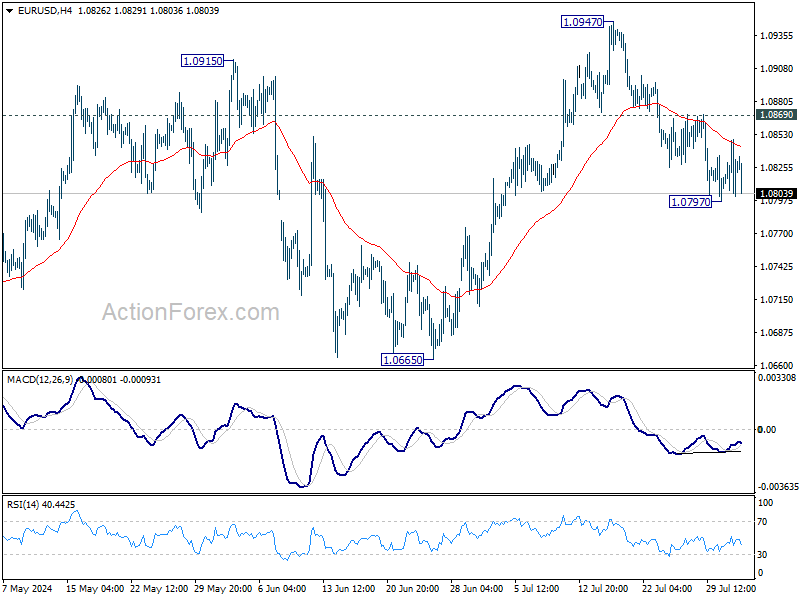

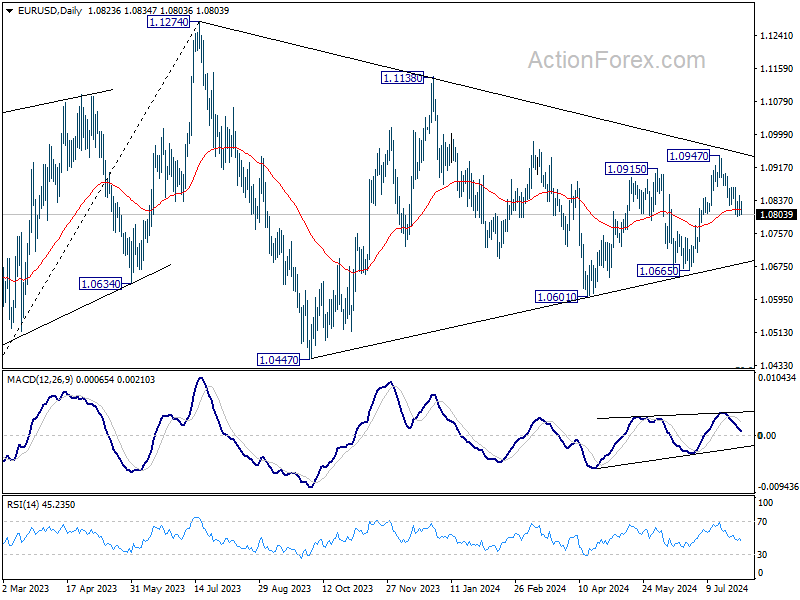

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0802; (P) 1.0826; (R1) 1.0849; More.....

Intraday bias in EUR/USD remains neutral for consolidation above 1.0797 temporary low. Further decline decline is expected with 1.0869 resistance intact. Sustained break of 55 D EMA (now at 1.0815) will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947. Deeper decline should then be seen to 1.0601/0665 support zone next. Nevertheless, break of 1.0869 minor resistance will bring retest of 1.0947 instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

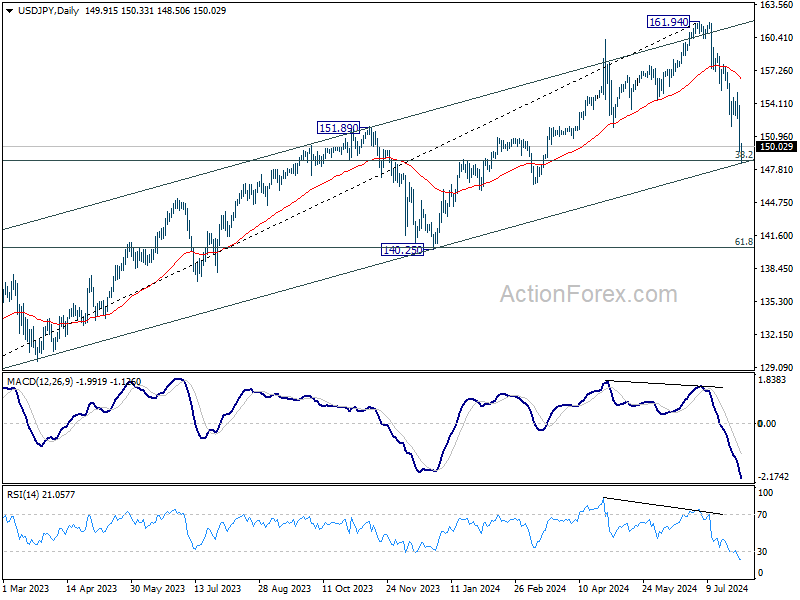

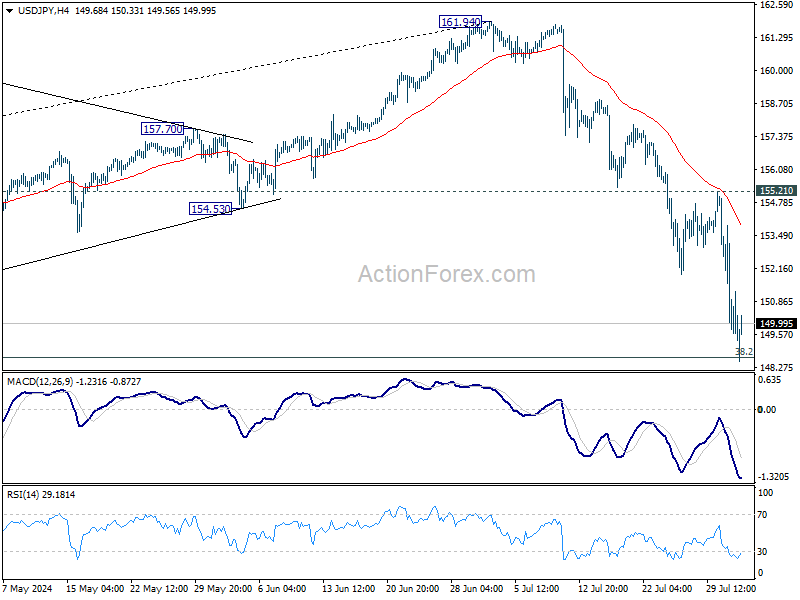

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.42; (P) 151.16; (R1) 152.72; More...

USD/JPY's fall from 161.94 is still in progress and hit 148.66 fibonacci level already. Strong support could be seen from the current level, which is close to medium term channel support (now at 148.22) to bring rebound. However, break of 155.21 resistance is needed to confirm short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Next target is 38.2% retracement of 127.20 to 161.94 at 148.66. Decisive break there will pave the way to 140.25 support next. Risk will now stay on the downside as long as 55 D EMA (now at 156.42) holds, in case of rebound.