Sample Category Title

Fed holds steady at 5.25-5.50%, keeps rate cut plans unclear

Fed kept interest rates unchanged at 5.25-5.50%, as widely anticipated, with a unanimous vote. The accompanying statement closely mirrored June's guidance for future decisions, maintaining that the Fed is "prepared to adjust the stance of monetary policy as appropriate."

Fed emphasized that its assessments will consider a "wide range of information," indicating that it is keeping its plans for potential rate cuts close to the chest for now.

On the economic front, Fed acknowledged that job gains have "moderated" and the unemployment rate has "moved up." Additionally, the statement noted "some further progress" in reducing inflation towards the target. Fed also mentioned that risks to inflation and employment are continuing to "move into better balance."

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have moderated, and the unemployment rate has moved up but remains low. Inflation has eased over the past year but remains somewhat elevated. In recent months, there has been some further progress toward the Committee's 2 percent inflation objective.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals continue to move into better balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Austan D. Goolsbee; Philip N. Jefferson; Adriana D. Kugler; and Christopher J. Waller. Austan D. Goolsbee voted as an alternate member at this meeting.

Bank of Japan Hikes Rates Further, Slows Bond Buying

Summary

- The Bank of Japan (BoJ) sprung a mild surprise at today's announcement, raising its policy rate to around 0.25%, from around 0% to 0.1% previously. The BoJ also said it would reduce the pace of its bond purchases to around ¥3T per month by early 2026. The BoJ's accompanying comments leaned hawkish in tone, and suggested further tightening would likely be forthcoming.

- Given the central bank's apparent willingness to look through subdued activity data, and apparent desire to front load policy normalization, we now forecast faster BoJ rate hikes than previously. We see another 25 bps rate hike to 0.50% in October, while we also now forecast a further 25 bps rate hike to 0.75% in January 2025.

Bank of Japan Delivers Monetary Tightening, Signals More To Come

The Bank of Japan (BoJ) sprung a mild surprise on markets, delivering an earlier than expected rate increase. The central bank also announced a reduction to its monthly bond purchases, though perhaps a slightly more gradual pace of bond purchases than anticipated. Specifically, the BoJ:

- Raised the target for the uncollateralized overnight call rate to around 0.25%, from around 0% to 0.1% previously.

- Signaled it would reduce the pace of its monthly bond purchases by around ¥400B every quarter, to just under ¥3T per month by early 2026.

For August-September 2024, the BoJ said bond purchases would be ¥5.3T per month, and with regular ¥400B reductions each quarter, fall to ¥2.9T per month by Q1 2026. The central bank said it would conduct an interim review of its bond buying plan in June 2025, and in the case of a rapid rise in long term bond yields, respond nimbly, including for example, increasing its purchases.

In addition to the surprise rate hike, the BoJ's announcement and Governor Ueda's post-meeting press conference were notable for several hawkish leaning comments:

- Real interest rates are expected to remain significantly negative after the change in the policy interest rate, and accommodative financial conditions will continue to firmly support economic activity.

- If the outlook for economic activity and prices evolves broadly as expected, the central bank will accordingly continue to raise the policy interest rate and adjust the degree of monetary accommodation.

- Import price inflation has turned positive and upside risks to prices require attention.

- Wage increases have been significantly higher than last year, and have been spreading across regions, industries and firm sizes.

- FX developments are more likely to affect prices than in the past.

- Governor Ueda said another rate hike before year-end was data dependent. Asked about the terminal level of the BoJ's policy rate, Ueda said 0.50% was not considered a particular limit.

With respect to its outlook on price pressures, the Bank of Japan lowered its core inflation forecast for fiscal year 2024 to 2.5% (from 2.8% previously) and increased its forecast for fiscal year 2025 to 2.1% (from 1.9%). The BoJ kept its forecast for core inflation for fiscal year 2026 unchanged at 1.9%.

We see a couple of important takeaways from today's announcement. First, the BoJ appears to be willing to discount subdued economic activity to some extent, given recent weakness in GDP and some other activity data. That suggests that wage and inflation data will remain particularly important for the timing and magnitude of further rate increases. Second, it also appears possible the BoJ is to some extent trying to front load rate increases, such that the Bank of Japan makes progress in normalizing monetary policy ahead of the significant and sustained monetary easing that is anticipated from the Federal Reserve.

Against this backdrop, we now expect earlier and more pronounced rates hikes from the Bank of Japan than previously. We forecast the next 25 bps policy rate hike to 0.50% at the October monetary announcement, a rate hike that will likely be supported by continued firmness in wages and inflation. We also forecast another 25 bps rate increase to 0.75% at the January 2025 announcement. We acknowledge, however, that this 2025 rate increase is less certain, depending on how price trends evolve and whether the BoJ's cumulative rate increases have a more meaningful impact in restraining the economy. Beyond that, we expect the BoJ to hold its policy rate steady through the rest of 2025. Given our outlook for faster Bank of Japan tightening, and ongoing easing from the Federal Reserve over time, we believe conditions remain in place for the yen to strengthen through much of 2025.

FOMC Rate Decision – Potential Impact on EUR/USD, GBP/USD and Dollar Index

- The market anticipates a shift in the Fed’s stance, with three rate cuts now expected in 2024 due to softening economic data.

- A soft landing remains possible as the labor market cools and inflation shows signs of easing.

- Technical analysis suggests GBP/USD is consolidating, EUR/USD maintains a bullish structure, and the Dollar Index (DXY) is at risk of a sharp decline.

FOMC Preview: September Cut Most Likely

Market participants are approaching today’s FOMC meeting with numerous questions. The previous FOMC meeting was bullish for the US dollar as the Fed updated its projections to include one rate cut in 2024.

Since the June meeting, however, economic data has painted a very different picture. The recent changes and softening data in the US have significantly altered the landscape, with markets now pricing in three rate cuts for 2024.

A soft landing remains possible for the US as the labor market continues to cool. Unemployment has already reached 4.1% in June, exceeding the forecasted 4% predicted for the end of 2024.

Regarding inflation, both core CPI and the core PCE deflator were alarmingly high in the first quarter. However, the numbers for May and June appear more promising. Most notably, the “super-core services” excluding housing, food, and energy—that the Fed has heavily emphasized have slowed significantly. Additionally, the key housing components are now reflecting the moderation observed in third-party private rent series.

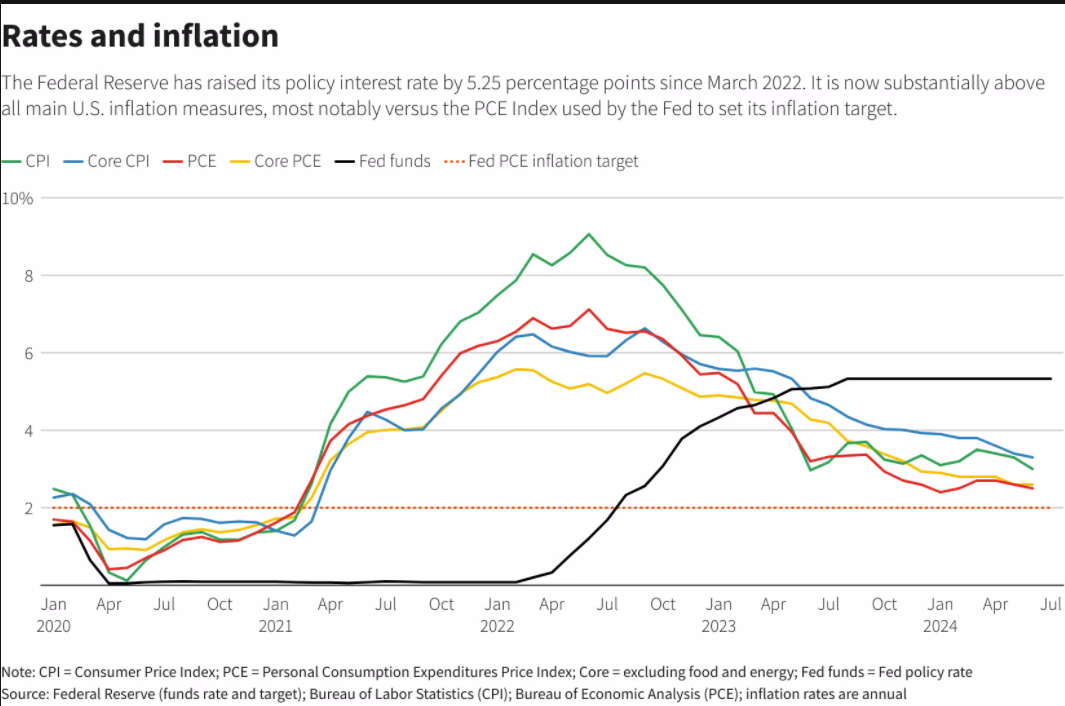

US Rates and Inflation Chart, July 31, 2024

Source: LSEG (click to enlarge)

This creates a slight dilemma for the Fed, as rising unemployment could heighten recession concerns. With income growth slowing and pandemic-era savings depleting, the Fed may be pushed to implement the three rate cuts currently anticipated before the year’s end.

Given this dilemma and the multitude of factors the Fed must consider, today’s forward guidance will be crucial. The rhetoric in June about one rate cut in 2024 is likely to change. If Fed Chair Powell maintains his outlook, it could lead to a short-term bounce for the US dollar.

Conversely, a pivot from Powell and a more bearish tone would theoretically lead to US dollar weakness. However, the recent selloff in the US dollar may indicate that much of the “pivot” is already priced in.

Technical Analysis

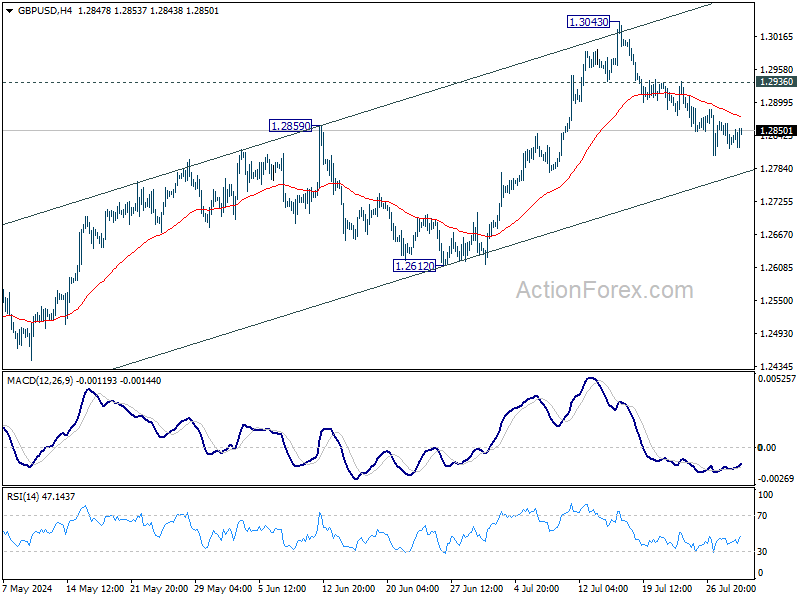

GBP/USD

From a technical perspective, GBP/USD has been consolidating over the past three days since hitting support at 1.2850. Both bulls and bears have attempted to move the price away from this level, but each effort has been countered by buying or selling pressure. This underscores the current uncertainty surrounding the upcoming Central Bank meetings.

Immediate support below the 1.2850 area lies at the 1.2800 and 1.2750 levels. A break below these support zones could shift focus back to the psychological 1.2500 mark. Conversely, an upward movement will face resistance at 1.2950 before the psychological 1.3000 level becomes crucial again.

Support

- 1.2800

- 1.2750

- 1.2680

Resistance

- 1.2950

- 1.3000

- 1.3040

GBP/USD Daily Chart, July 31, 2024

Source: TradingView (click to enlarge)

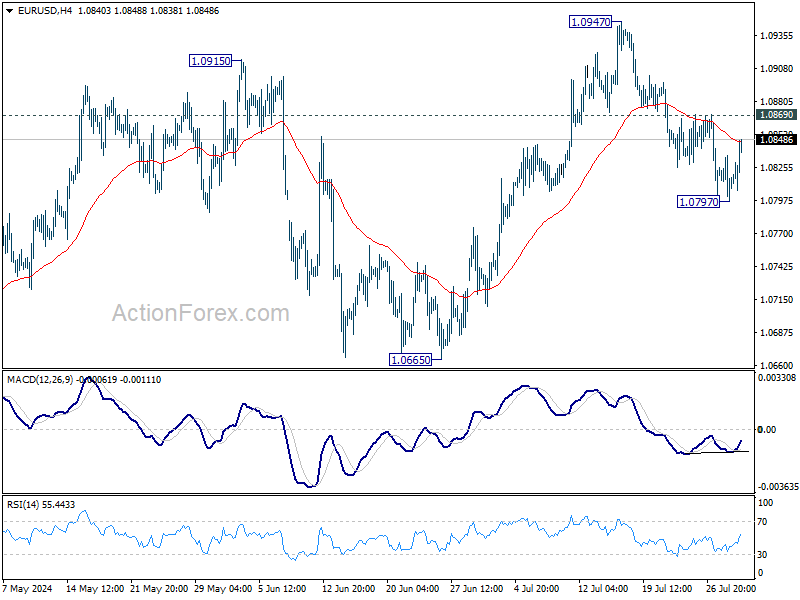

EUR/USD

From a technical perspective, EUR/USD has risen today following a slight uptick in the Euro Area’s inflation print.

On a broader scale and daily timeframe, EUR/USD maintains a bullish structure. A daily candle close below the 1.0680 level would be necessary to alter this structure. The 100-day moving average around the 1.0800 level is currently providing support, with immediate resistance at 1.0860 and 1.0900.

Conversely, a decline from the current price may find support at 1.0755 before the key swing low at 1.0680 comes into focus.

EUR/USD Daily Chart, July 31, 2024

Source: TradingView (click to enlarge)

Support

- 1.0800

- 1.0755

- 1.0680

Resistance

- 1.0860

- 1.0900

- 1.0948

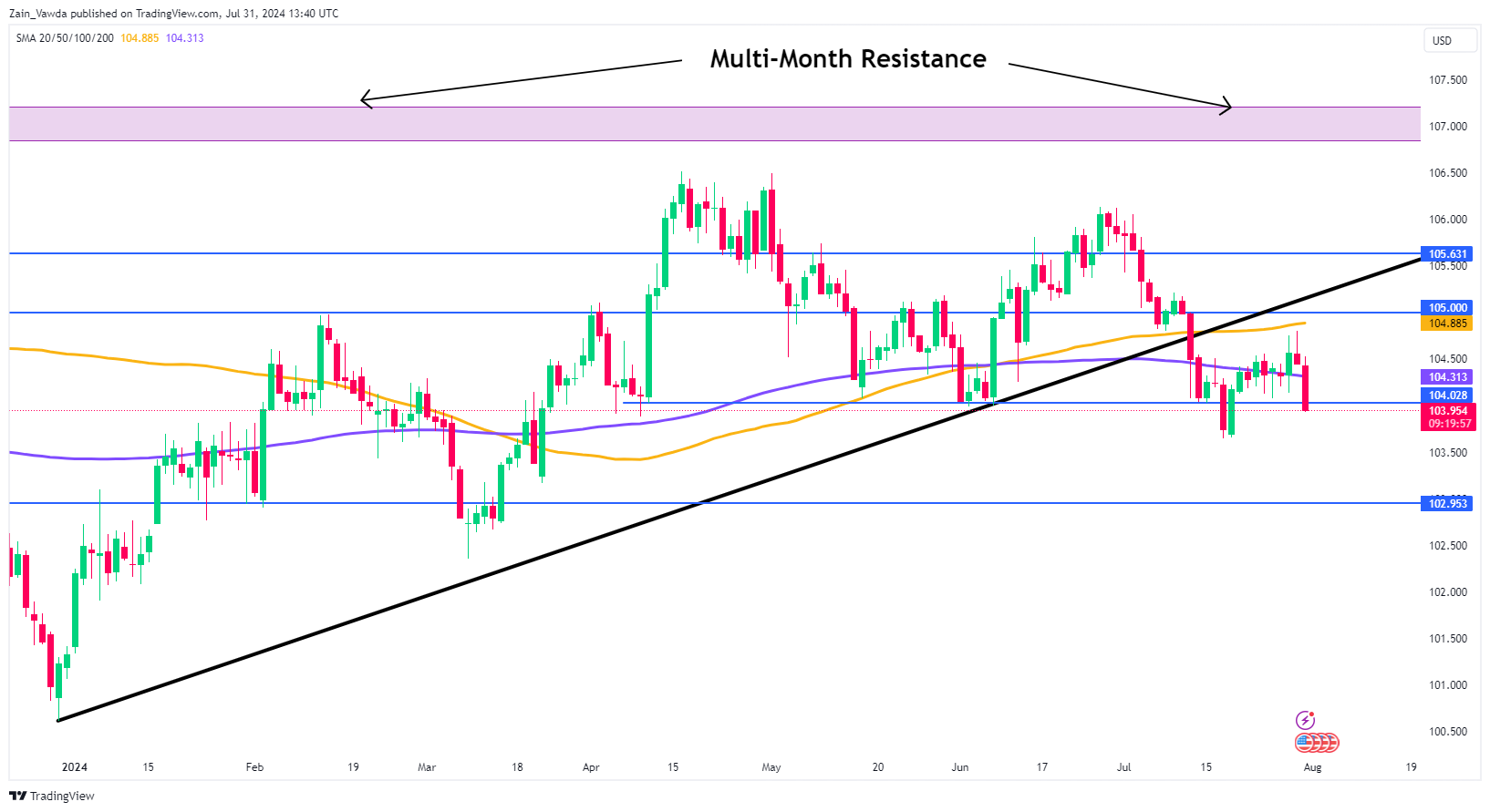

US Dollar Index

The Dollar Index (DXY) is at risk of a sharp decline following the FOMC meeting, with much depending on the Fed’s rhetoric. However, the technical outlook appears concerning.

After breaking the long-term ascending trendline, the DXY experienced some consolidation and a brief retracement earlier in the week. As the FOMC meeting approaches, the selloff has resumed.

The DXY is currently breaking through support at the 104.00 level, with further support found at the recent lows of 103.65. Should it break lower, the 103.00 level comes into focus.

Conversely, a move higher from this point faces immediate resistance at 104.313, followed by the resistance level at 104.88 (100-day moving average), which is just below the psychological 105.00 mark.

US Dollar Index Daily Chart, July 31, 2024

Source: TradingView (click to enlarge)

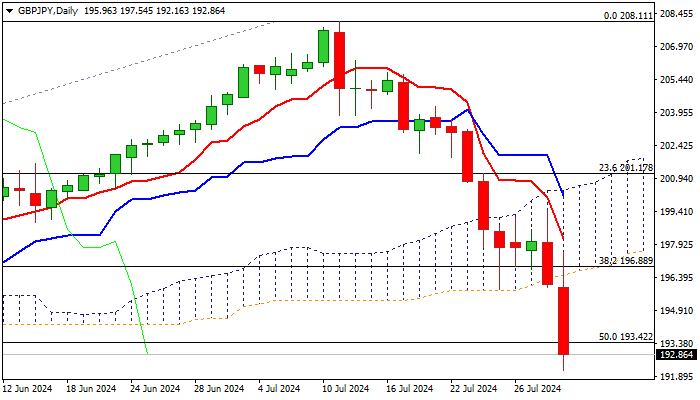

GBP/JPY Accelerates Lower After BoJ Rate Hike

GBPJPY extends steep downtrend by dropping 1.7% on Wednesday and on track for the biggest daily drop since 12 July 2023, after BOJ rate hike further boosted yen, while sterling remains deflated by growing expectations that BoE would deliver a 25 basis points rate cut tomorrow.

Markets also focus on today’s Fed rate decision at the end of two-day policy meeting, expecting Chair Powell to add to expectations for three rate cuts by the end of the year, with cycle likely to start in September.

Fresh acceleration lower brought the price well below ascending daily cloud (spanned between 196.50 and 200.39) and broke below 50% retracement of 178.73/208.11 (193.42) to hit the lowest since early May.

Bears pressure next significant support at 191.66 (200DMA), where stronger headwinds could be expected, as daily studies are oversold.

Upticks should be capped under daily cloud base (196.50) to keep bears intact for fresh push lower and possible probe below 190 mark, as BoJ’s fresh hawkishness and dovish BOE, would continue to weigh on the pair.

Res: 193.42; 195.04; 196.50; 197.37

Sup: 191.66; 191.35; 190.29; 189.95

Sunset Market Commentary

Markets

The biggest moves in markets ahead of tonight’s Fed policy meeting happened in the Japanese yen. A not completely expected rate hike to 0.25% by the Bank of Japan this morning, accompanied by a bond taper programme, took some investors off guard. In a hawkish presser afterwards, governor Ueda said that if the economy evolves according to the outlook, more rate hikes will follow, possibly beyond neutral (+/-0.5%). Ueda added that the weak currency was an argument to raise the rate today, along with increased confidence of a consumer-driven sustained return to the 2% inflation target. USD/JPY is testing the 150 barrier, the lowest level since mid-March on JPY strength (rather than USD-weakness that drove much of the recent USD/JPY decline). European markets eyeballed the EMU inflation print. Prices in July evolved in a not so comfortable way for the ECB. The headline figure was flat m/m, allowing the y/y figure to unexpectedly pick up from 2.5% to 2.6%. Core inflation stood at a June-matching 2.9%, defying expectations for a minor deceleration. And services inflation, lastly, barely eased from the 4.1% in June to 4% this month – a level deemed too high to reconcile with the ECB’s overall 2% target. An attempt of European/German yields to reverse earlier declines quickly faded to nothing and returned towards intraday lows. Net daily changes vary between 3.2-3.8 bps. The euro did hold on to some minor gains against the dollar (EUR/USD around 1.084) as the former was weighed down by a drop in US yields as well (2-4 bps)-. Q2 Employment Cost Index – the Fed’s preferred wage measure - came in a tad below consensus, ie 0.9% vs 1% (4.1% y/y, the slowest advance since 2021). Both wages & salaries (the base compensation component) as well as benefits eased compared to the previous quarter, suggesting moderating wage growth in a ditto labour market. The latter was also confirmed by the ADP job report printing at sub-par 122k.

We are now headed towards tonight’s FOMC meeting. The Fed’s status quo at 5.25-5.5% is widely anticipated. The central question is whether the recent string of beneficial CPI outcomes and mostly below-consensus economic outcomes will prompt clearer clues towards a first cut (in September) in either the statement or the presser. We think there’s a possibility of that to happen, be it subtle in order to prevent the recent sharp yield correction go much further against the background of thinner liquidity circumstances and technical support zones at the verge of breaking. Complementing the case for (short-term) yields not to drop much lower from current levels is the current pricing in money markets (almost three cuts priced in for 2024). The four cuts for 2025, as things currently stand, seem appropriate as well. First support for the dollar kicks in at EUR/USD 1.09. That should hold.

News & Views

Polish inflation in July came in to the soft side of expectations. While the monthly reading quickened sharply from 0.1% to 1.4%, it fell short of a 1.6% consensus estimate. On a yearly basis, the number picked up from 2.6% to a 2024 high of 4.2%. That undershot expectations by 0.2 ppts but is nevertheless well above the central bank’s 2.5% +/- 1 ppt target. The few details made available by Poland Statistics showed that electricity, gas and other utilities drove the dramatic increase (+11.8% m/m). This was the result of the government’s decision to raise the energy cap for the second half of 2024. This will affect all upcoming readings on a similar basis and is one of the reasons for the hawkish monetary policy stance. The majority of the MPC council agrees that no cuts are appropriate this year with governor Glapinski at some point ruling out 2025 as well. Council member Wnorowski in a first reaction after the release said that inflation at the beginning of next year could pick up further but said he sees reasons for discussions about cuts to start in 2025Q2. The Polish zloty trades little chanced around EUR/PLN 4.29.

Following up on the US Treasury announcing the updated borrowing estimates for the running (and upcoming) quarter, the agency today released quarterly refunding statement detailing the borrowing strategy. The US Treasury expects that, based on current projected borrowing needs, it does not have to increase auction sizes for at least the next several quarters. With the exception of the August refinancing round (temporary $3 bn uptick in the 7-yr, 10-yr and 30-yr auction size), all other auction sizes were left unchanged at least through October 2024. That means the financing strategy remains tilted towards short(er) maturities with monthly sizes ranging from $58 to $70bn.

Graphs

US 2-yr yield reaches make or break moment

AUD/USD: Aussie dollar erases much of the CPI-driven weakness as US counterpart remains unconvincing

Brent ($/b) snaps losing streak as geopolitical concerns flare up (Israeli retaliatory attack in Lebanon)

Japanese 2-yr yield shoots to highest level in 15 years as central bank hiked and flags more to come, conditional on eco developments

EUR/USD Outlook: Rises on EU CPI and US Labor Data, Bear-Trap Forming on Daily Chart

EURUSD bounced on Wednesday after a triple rejection at 1.0800 support zone (50% retracement of 1.0666/1.0948 rally/daily Kijun-sen) signals formation of a bear-trap.

Fresh gains were sparked by higher than expected EU inflation numbers in July which improved Euro’s sentiment and below expectations US ADP private sector payrolls signaling softening in US labor market and adding to Fed rate cut narrative.

Markets shift focus to the key event of the day – FOMC rate decision. The US central bank is expected to stay on hold in July policy meeting, but to provide more hints about their next steps at Chair Powell’s press conference.

The Fed is widely expected to start cutting interest rates from September, with more signals from the central bank, to deflate dollar and further boost the single currency.

Technical picture on daily chart is mixed (conflicting MA’s, negative momentum and north-heading RSI) and lacks clearer technical signal, although fresh gains point to development of reversal signal on daily chart.

However, such scenario will need confirmation, with lift and close above 1.0850 zone (falling 10DMA / Fibo 38.2% of 1.0948/1.0798 bear-leg) seen as minimum requirement to validate bullish signal and expose upper pivots at 1.0870 zone (lower platform / 50% retracement).

Only sustained break below 1.0800 pivot would neutralize fresh bulls and signal continuation of larger downtrend from 1.0948 (July 17 top).

Res: 1.0850; 1.0870; 1.0890; 1.0902.

Sup: 1.0807; 1.0800; 1.0773; 1.0732.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0797; (P) 1.0816; (R1) 1.0835; More.....

Intraday bias in EUR/USD is turned neutral with current recovery. But further decline is expected with 1.0869 resistance intact. Sustained break of 55 D EMA (now at 1.0815) will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947. Deeper decline should then be seen to 1.0601/0665 support zone next. Nevertheless, break of 1.0869 minor resistance will bring retest of 1.0947 instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

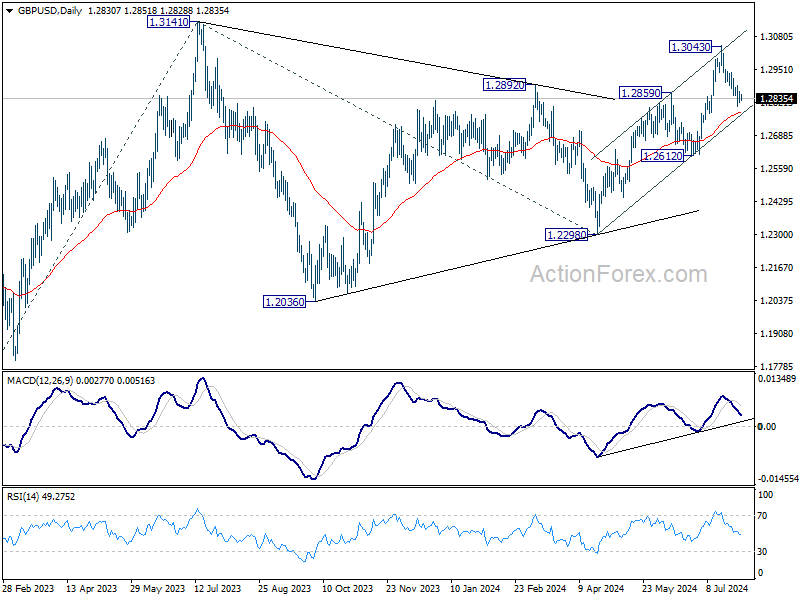

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2815; (P) 1.2841; (R1) 1.2863; More...

GBP/USD is losing downside momentum as seen in 4H MACD. But further decline is still expected with 1.2936 resistance intact. Decisive break of 55 D EMA (now at 1.2781) will suggest that rise from 1.2298 has completed with three waves up to 1.3043. Deeper fall would be seen to 1.2612 support and below. On the upside, above 1.2936 resistance will bring retest of 1.3043 resistance instead.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022. However, break of 1.2612 support argue that this corrective pattern is extending with another falling leg.

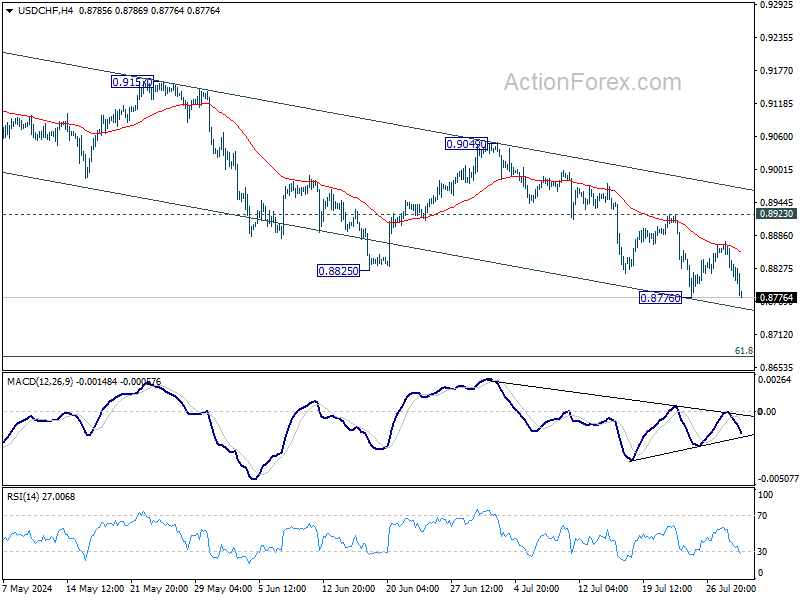

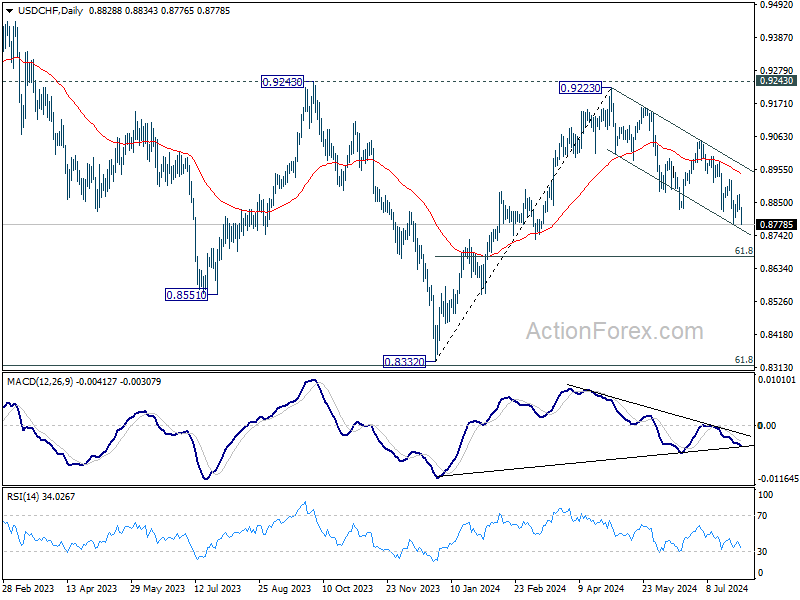

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8810; (P) 0.8843; (R1) 0.8860; More…

USD/CHF is holding above 0.8776 support despite today's dip and intraday bias remains neutral. More consolidations could still be seen but further decline is expected as long as 0.8923 resistance holds. On the downside, break of 0.8776 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. However, break of 0.8923 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.