Sample Category Title

European Currencies Decline Amid Rising Geopolitical Risks

European currencies are moving into a corrective decline after recent attempts to hold above key levels, with the current move driven by escalating geopolitical tensions and stronger demand for safe-haven assets. The partial closure of the Strait of Hormuz and renewed escalation in the Middle East are weighing on risk assets, supporting the US dollar through capital flows into more liquid instruments and limiting upside potential for both the euro and the pound. Higher energy prices are adding further pressure by increasing inflation risks for the European economy.

At the same time, markets remain cautious ahead of upcoming macroeconomic releases from the US, as well as data from the euro area and the UK. Anticipation of fresh signals on inflation and economic activity is restraining directional moves and increasing the likelihood of tests of key levels amid a mixed fundamental backdrop.

EUR/USD

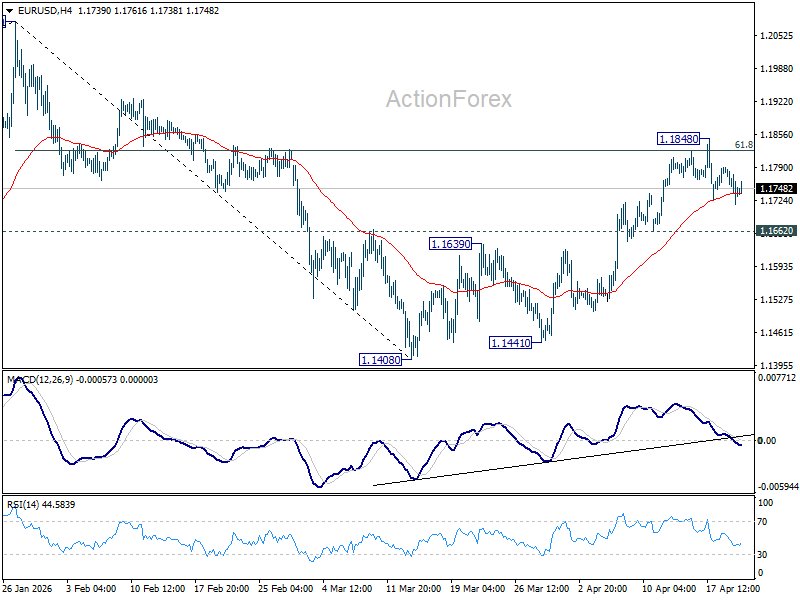

As expected, EUR/USD retested the 1.1800–1.1830 resistance zone but failed to establish a foothold above it. Technical analysis points to the potential for a continued downward correction, with reversal signals forming on the daily timeframe. However, a weaker dollar or an improvement in global risk sentiment could trigger a renewed bullish move towards 1.1830–1.1850.

Key events for EUR/USD:

- today at 13:00 (GMT+3): Bundesbank monthly report

- today at 17:30 (GMT+3): US crude oil inventories

- today at 20:00 (GMT+3): speech by Bundesbank President Nagel

GBP/USD

GBP/USD is also declining and approaching important support levels, reflecting broader pressure on European currencies. Technical analysis suggests a potential retest of 1.3470 and, if broken lower, a move towards 1.3380–1.3430. The bearish scenario could be invalidated by a sustained move above 1.3550.

Key events for GBP/USD:

- today at 09:00 (GMT+3): UK Consumer Price Index

- today at 11:05 (GMT+3): speech by Sarah Breeden (BoE)

- today at 11:30 (GMT+3): UK house price index

The currency market remains in a phase of elevated uncertainty, where a combination of geopolitical developments and macroeconomic expectations is driving subdued price action. In the near term, the news flow will remain the key driver, with the potential either to intensify pressure on European currencies or to trigger short-term corrective rebounds.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

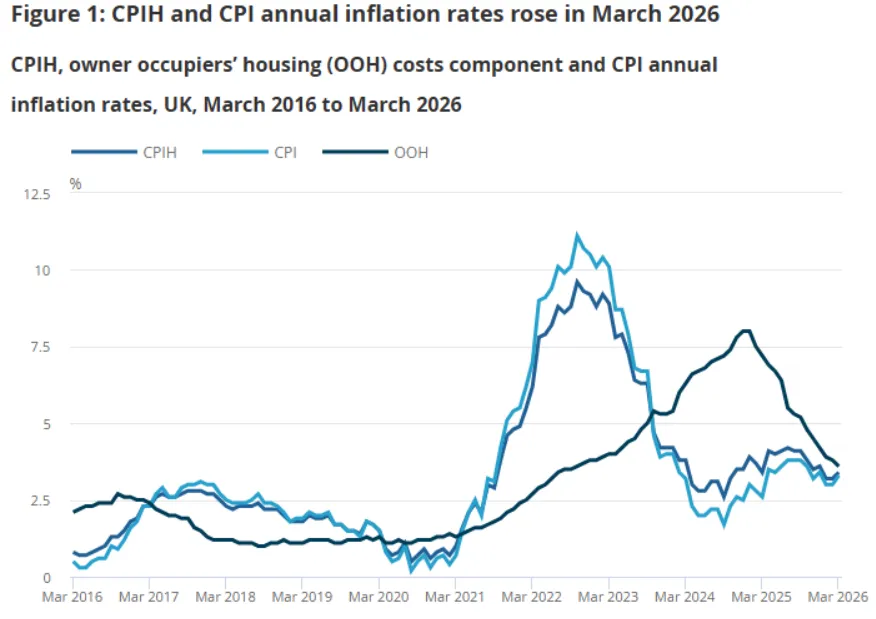

UK Inflation Hits 3-Month High as Energy & Food Pressures Mount

- UK inflation climbed to 3.3% in March 2026

- The inflation surge, linked to geopolitical tensions, reinforces the Bank of England's necessity to maintain a restrictive policy stance

- Second round inflation effects on food and services may only be felt in the months ahead

- The GBP/USD pair has transitioned into a constructive recovery phase after breaking a descending channel

The UK’s inflationary landscape saw a fresh uptick in March 2026, with the annual rate climbing to 3.3%. This print comes after two months of stability at 3%, and while the move was largely anticipated by markets, it marks the highest reading we’ve seen in three months.

From a technical and fundamental standpoint, the primary catalyst remains the volatility in the energy sector. Geopolitical tensions, specifically the ongoing conflict with Iran, continue to ripple through the supply chain. Transport costs surged by 4.7% the fastest pace of growth since late 2022, with motor fuels jumping 4.9%. For consumers at the pump, this translated to a painful 8.6p per litre increase in petrol and a staggering 17.6p rise for diesel.

Source: ONS

Key Data Highlights:

- Housing & Household Services: Rose to 4.3% (up from 4.2%), underpinned by a massive 95.3% surge in domestic heating oil, a level of acceleration not seen since September 2022.

- Food & Beverages: Continued their upward trajectory, hitting 3.7% vs. the previous 3.3%.

Services: Remained sticky at 4.5%, reflecting broader inflationary pressures in the domestic economy. - The Outlier: Clothing prices provided a rare bit of relief, falling by 0.8%, the sharpest decline for the sector since March 2021.

On a month-on-month basis, the CPI increased by 0.7%, signaling that the "inflation storm" may not have fully passed just yet.

While the current data reveals a lot it does not show second round effects of the war in the Middle East on inflation. The impact on food and services may only start to show up in the coming months.

Implications for the Bank of England

For the Bank of England, these figures likely confirm that a restrictive policy stance remains necessary. The surge in energy and food costs offsets the cooling we’ve seen in discretionary items like clothing.

From a trading perspective, keep a close eye on the GBP/USD and FTSE 100, persistent inflation coupled with geopolitical risk often leads to intraday consolidation as markets weigh the likelihood of "higher for longer" rates against slowing growth momentum.

As I’ve noted in previous outlooks, the path to the 2% target remains fraught with external shocks. Until we see a meaningful de-escalation in the Middle East, energy-led volatility will likely remain the dominant theme for the UK economy like many of its peers.

The Initial Market Reaction

Markets seemed to shrug off today's data with GBP/USD remaining largely flat after the release.

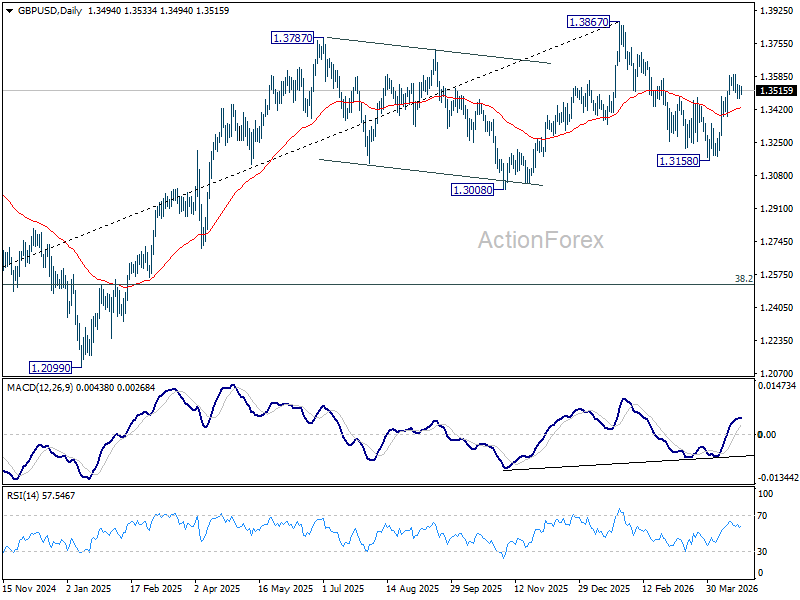

The daily chart for GBP/USD highlights a significant structural shift as we move through April 2026. Following a breakout from a dominant descending channel (dark navy lines) earlier this month, the pair has transitioned from a bearish regime into a constructive recovery phase.

Key Technical Highlights:

- Moving Average Reclaim: Price action remains comfortably above the 100-day SMA (blue) at 1.3455 and the 200-day SMA (black) at 1.3413. This "support sandwich" serves as a foundational floor for the current uptrend.

- The 1.3500 Pivot: GBP/USD is currently consolidating around the 1.3500 psychological level. Bulls must maintain daily closes above this handle to sustain momentum toward the next major resistance at 1.3584.

- Momentum Indicators: The Daily RSI is trending healthily at 57.9, suggesting ample "white space" for further gains before reaching overbought territory.

- Outlook: A decisive break above 1.3584 opens the door for a run toward 1.3700, while a slip below 1.3400 would neutralize the current bullish bias..

GBP/USD Daily Chart, April 22, 2026

Source: TradingView.com

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1708; (P) 1.1750; (R1) 1.1785; More….

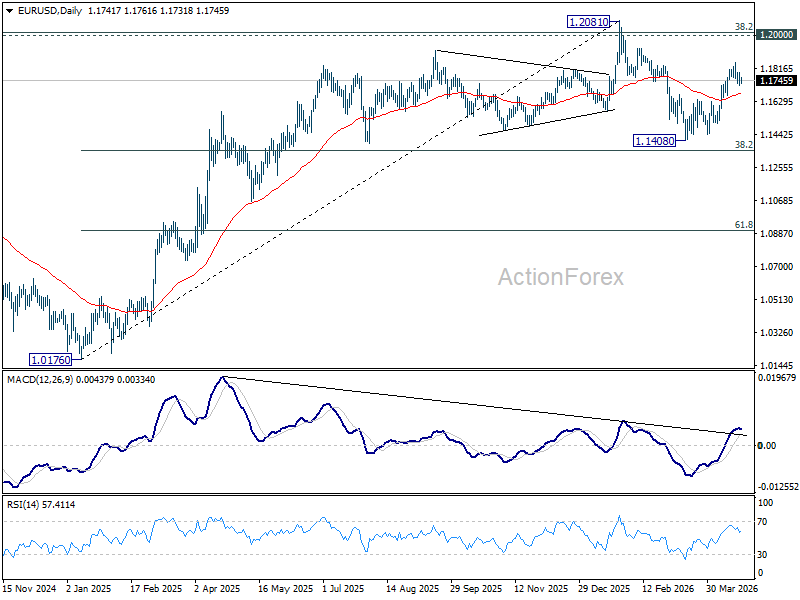

Intraday bias in EUR/USD remains neutral as it's still bounded in consolidations below 1.1848. With 1.1662 support intact, further rally is in favor. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will bring deeper decline back towards 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

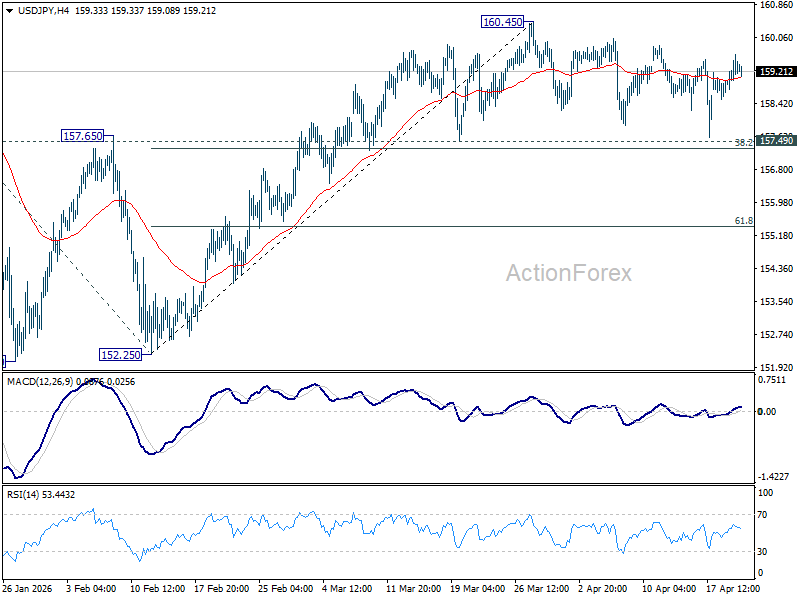

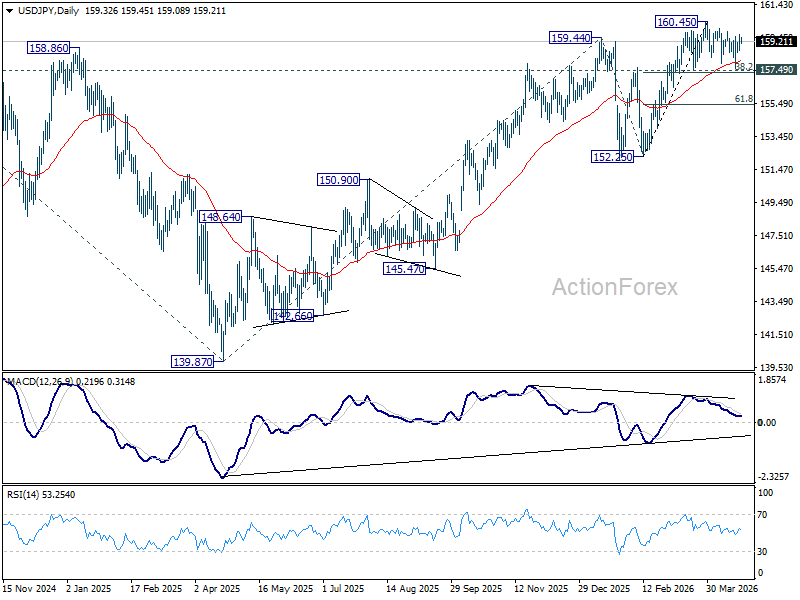

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.80; (P) 159.28; (R1) 159.87; More...

Intraday bias in USD/JPY stays neutral as consolidation continues below 160.45. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.80) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

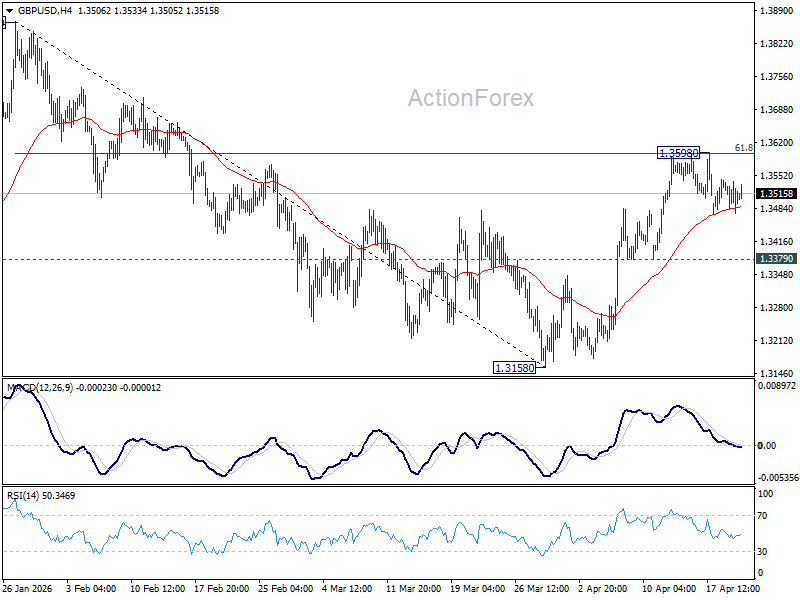

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3475; (P) 1.3508; (R1) 1.3542; More...

GBP/USD is still bounded in consolidations below 1.3598 and intraday bias stays neutral. With 1.3379 support intact, further rise is favor. On the upside, sustained break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will pave the way to retest 1.3867 high. However, firm break of 1.3379 will bring deeper fall back to 1.3158 low instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

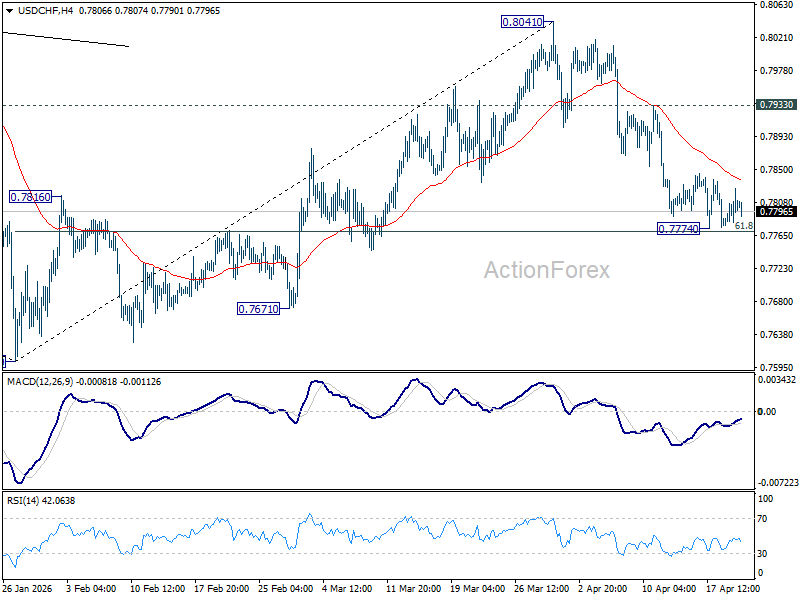

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7782; (P) 0.7805; (R1) 0.7830; More….

USD/CHF is still extending consolidations above 0.7774 and intraday bias remains neutral. Upside of recovery should be limited below 0.7933 resistance to bring another fall. Sustained break of 61.8% retracement of 0.7603 to 0.8041 at 0.7770 will resume the decline from 0.8041 to retest 0.7603 low.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8059) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

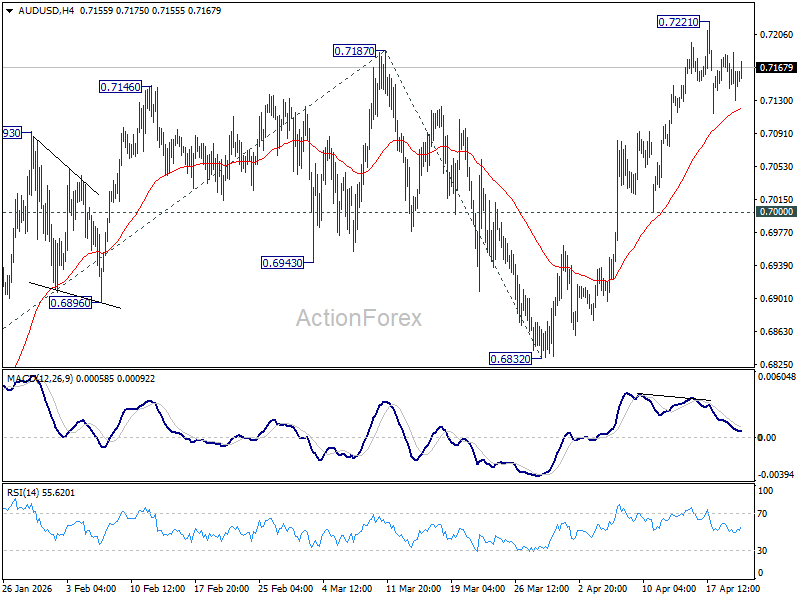

AUD/USD Daily Report

Daily Pivots: (S1) 0.7128; (P) 0.7157; (R1) 0.7184; More...

AUD/USD is extending consolidations from 0.7221 and intraday bias remains neutral. In case of deeper retreat, downside should be contained above 0.7000 support. On the upside, above 0.7221 will extend the larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. However, break of 0.7000 will bring deeper fall back to 0.6832 support instead.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

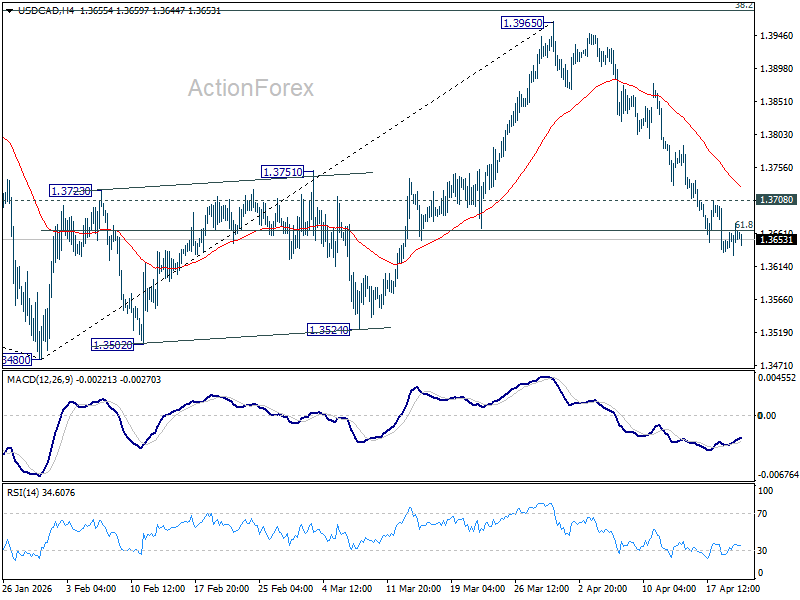

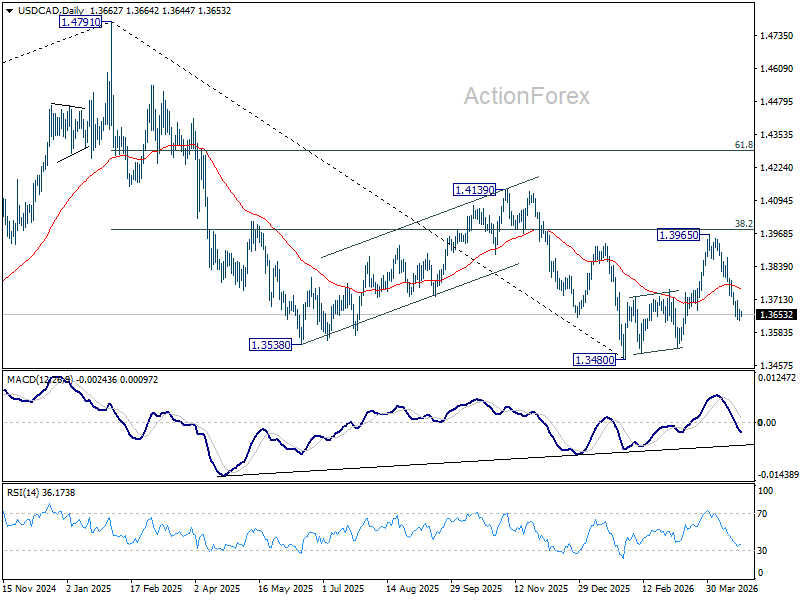

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3638; (P) 1.3658; (R1) 1.3683; More...

Intraday bias in USD/CAD remains on the downside despite loss of momentum. Sustained trading below 61.8% retracement of 1.3480 to 1.3965 at 1.3665 will pave the way to retest 1.3480 low. On the upside, above 1.3708 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

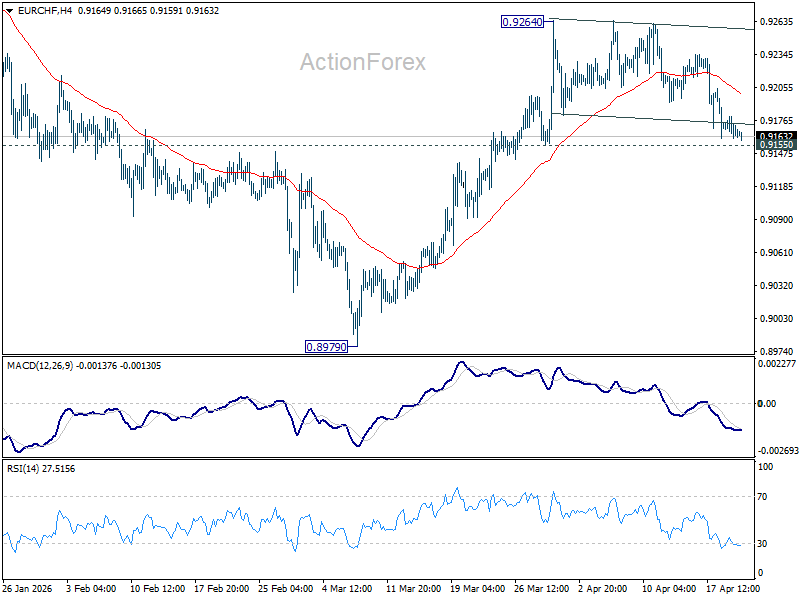

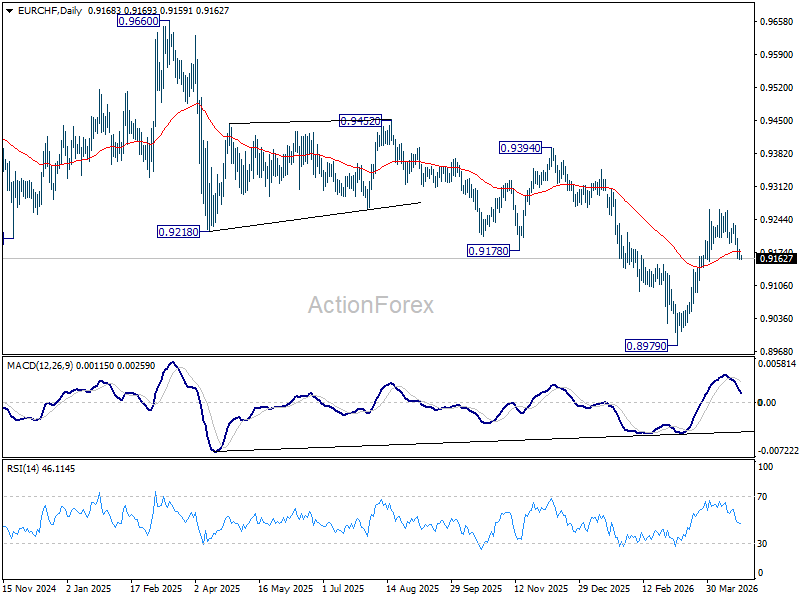

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9157; (P) 0.9174; (R1) 0.9186; More....

Intraday bias in EUR/CHF remains neutral and range trading continues below 0.9264. Further rise is in favor with 0.9155 support intact. Firm break of 0.9264 will resume the rise from 0.8979 to 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9280) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

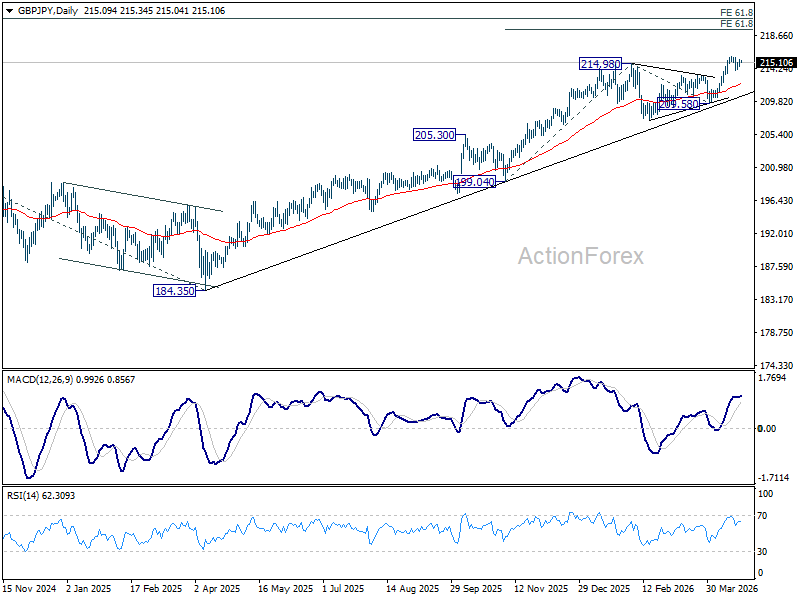

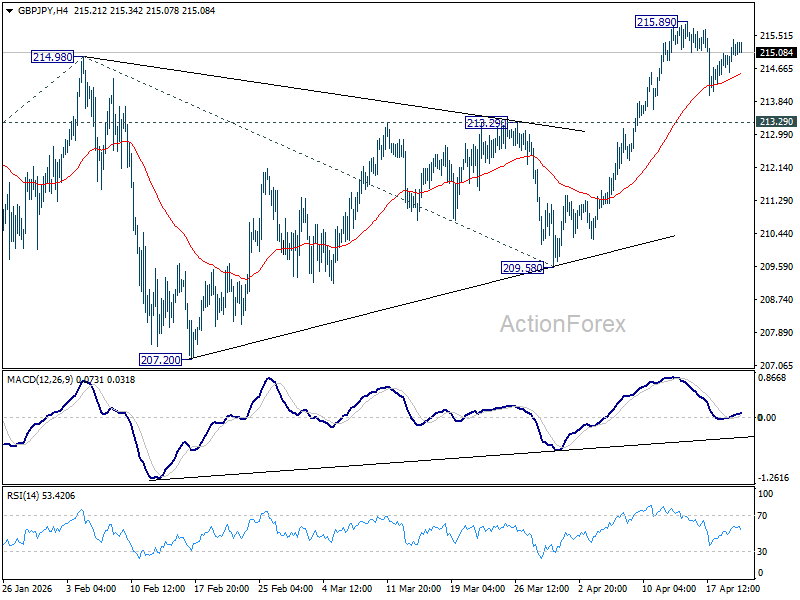

GBP/JPY Daily Outlook

Daily Pivots: (S1) 214.80; (P) 215.12; (R1) 215.62; More...

Intraday bias in GBP/JPY stays neutral as consolidations continue below 215.98. Further rise is expected as long as 213.29 resistance turned support holds. Firm break of 215.89 will resume larger up trend to 61.8% projection of 199.04 to 214.98 from 209.58 at 219.43.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 204.83) holds, even in case of another deep pullback.