Sample Category Title

Crypto Market Looks to Return to Growth

Market Picture

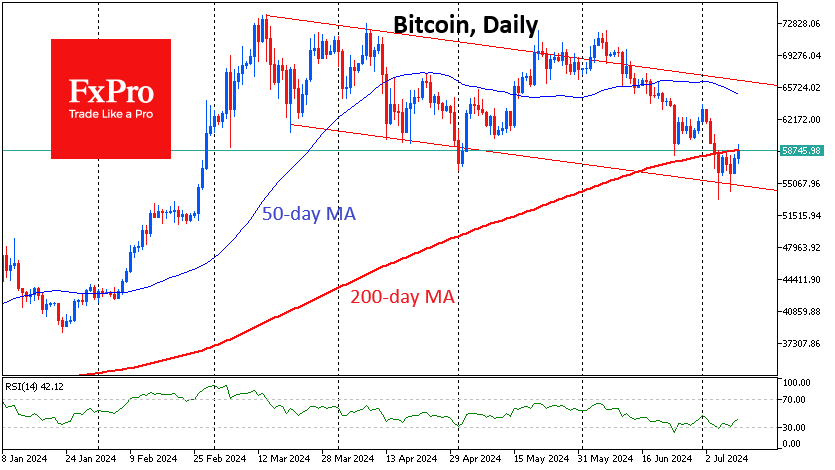

According to the sentiment index, the cryptocurrency market remains in a state of fear at 28. Still, market capitalisation rose for the second day in a row as lower prices attracted buyers. Capitalisation rose 1.9% to $2.16 trillion, surpassing previous local highs, which is promising.

Bitcoin gained 3.2% in 24 hours as it attempted to consolidate above the $59.0K level and the 200-day moving average. These levels are above the local highs, and we have seen the sell-off intensify over the past four days. The next milestones on the way up are seen at $60,000 and then $63,000. However, even after rising to $65.5K this month, bitcoin will remain within the descending channel.

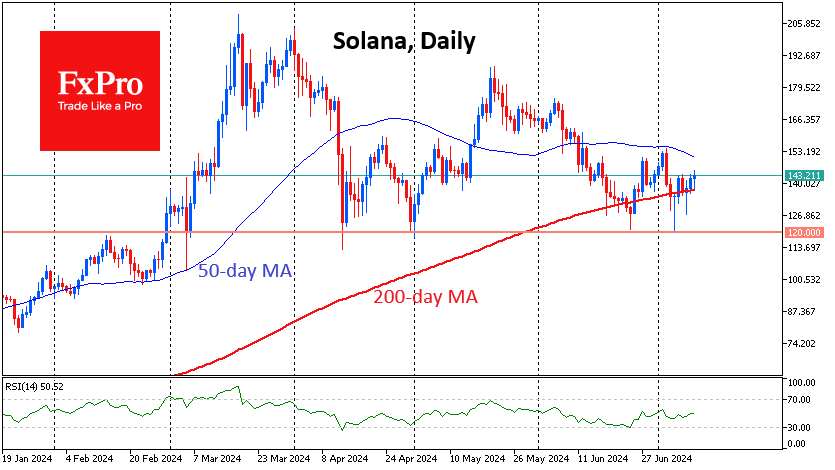

Solana received impressive buyer support at the beginning of the week when it touched the 200-day moving average. This was an important signal that the balance of power was still with the bulls. However, it is too early for them to celebrate, as the crossing of the important curve is still small, and the 50-day average is pointing down and above the price—a bearish signal.

News Background

Demand for crypto instruments was seen against the backdrop of the German government’s maximum coin sales. On the 9th, the German government sent 6,306.9 BTC ($362.12 million) to trading platforms. Since mid-June, the country’s authorities have transferred over 26,200 BTC (~$1.5 billion) to exchanges and market makers. According to Arkham Intelligence, 27,460 BTC (~$1.57 billion) remain in reserve.

Market participants also expect the remaining distribution of 94,771 BTC (~$5.4bn) to Mt Gox customers.

Meanwhile, social media trader sentiment is the most bearish it has been in a year, according to Santiment data. With such a FUD crowd, the chances of a bounce catching most by surprise are at an all-time high.

Nate Geraci, president of The ETF Store, suggested that the SEC will approve the listing of spot Ethereum ETFs on 15 July. BlackRock, Fidelity, Grayscale, 21Shares, Franklin Templeton, and VanEck submitted updated Forms S-1 to the SEC the day before. Bloomberg analyst Eric Balchunas expects the ETH ETF to launch on 18 July.

Is It Time for Gold to Emerge Above Key Resistance?

- Gold trades higher, but withing a broader sideways range

- RSI and MACD imply strengthening upside momentum

- A break above 2388 could add to the bullish case

- A dip below 2340 may allow declines within the range

Gold is moving higher today, after hitting support near the 2,450 zone yesterday. The precious metal is trading above the short-term uptrend line drawn from the low of June 26, but in the bigger picture, it remains within the sideways range that’s been containing most of the price action since the beginning of April.

The RSI rebounded from near its 50 line, while the MACD, although still below its trigger line, shows signs of bottoming slightly above zero. Both indicators suggest that the precious metal is gaining upside momentum, increasing the chances for a test of the upper bound of the range 2,388 soon.

That said, the move that could solidify the supremacy of the bulls may be a decisive break above 2,388. A move above that obstacle could pave the way towards the high of May 22 at 2,426, or the peak of the day before at 2,434. If the bulls are not willing to stop there either, then they may try reaching the record high of 2,450.

On the downside, a dip below 2,340 could trigger decent declines within the aforementioned sideways range. The bears may initially aim for the 2,320 zone, the break of which could allow extensions towards the lower end of the range at 2,290.

To recap, gold is trending north in the very short-term, but in the bigger picture, it remains within a sideways range that’s been in play since April. For the outlook to brighten, a decisive break above the range’s upper bound of 2,388 may be needed.

Gold Prices Rise Amid Anticipation of Fed Rate Cut

Gold prices continue to experience an upward trend, reaching 2368 USD per troy ounce, fuelled by growing market anticipation of a potential rate cut by the US Federal Reserve. As investors focus on upcoming US inflation data, gold remains a focal point of investment interest.

In his recent testimony before Congress, Federal Reserve chair Jerome Powell highlighted June's improved yet uncertain economic indicators. He noted the need for more comprehensive data to solidify inflation forecasts and hinted at concerns over a slowing economy and a cooling job market. These developments are considered critical drivers for the speculated rate cut in September, currently perceived as likely by 73% of market analysts.

Additionally, increased investment flows into exchange-traded funds (ETFs) bolster gold's appeal, marking a second consecutive month of positive cash inflows. This investment trend underscores gold's role as a safe-haven asset amid financial market uncertainties.

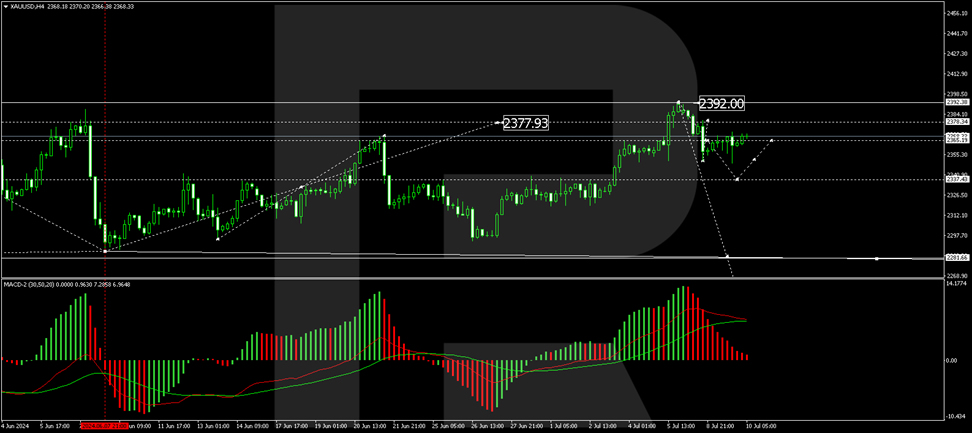

Technical analysis of XAU/USD

Gold's trajectory on the H4 chart shows a potential movement towards the 2337.43 USD level. A rebound to 2365.20 USD could follow, testing this resistance from below. The market may then gear up for a further downward movement towards 2281.66 USD, potentially extending to 2175.00 USD. This bearish outlook is supported by the MACD indicator, which is currently at its peak and poised for a downward adjustment towards the zero level.

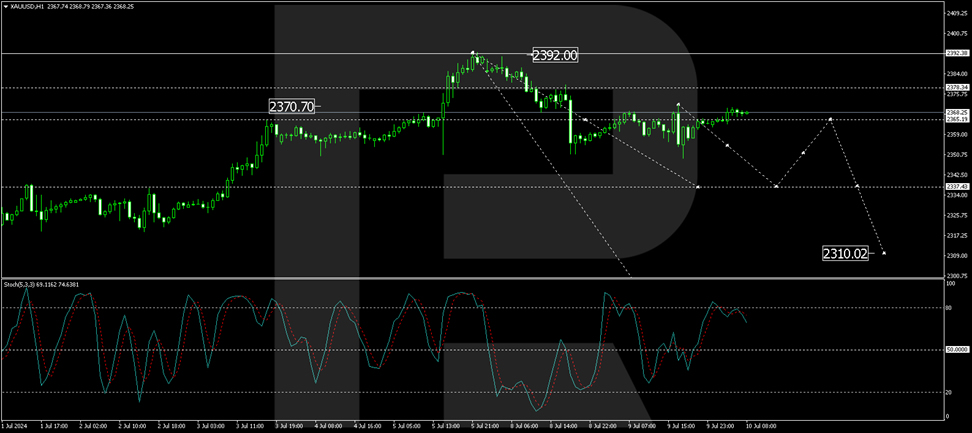

On the H1 chart, gold is consolidating around the 2365.20 USD mark. A downward break is anticipated, targeting 2337.43 USD as the immediate goal. Should this level be reached, a subsequent upward correction back to 2365.20 USD is likely. This scenario is validated by the Stochastic oscillator, which signals a potential decline from its current high position near 80, suggesting a near-term downward correction before further gains.

As the market navigates through these potential movements, investors remain vigilant, watching closely for any new economic data or policy shifts that could influence gold's price dynamics and the broader financial landscape.

NZDUSD Tumbles After RBNZ’s Decision

- NZDUSD finds support at 200-day SMA

- Prices have been heading lower over the last month

- Stochastics and RSI keep downside move

NZDUSD is posting notable losses after the RBNZ’s policy decision to leave interest rates unchanged at 5.5%. The pair is pausing its decline near the 200-day simple moving average (SMA) at 0.6070 and the short-term ascending trend line.

Technically, the stochastic oscillator posted a bearish crossover within its %K and %D lines near the overbought region, while the RSI is heading south below the neutral threshold of 50. Additionally, the 20- and 50-day SMAs are moving lower, with the potential for a downside crossover.

Immediate support could be found near the 0.6050 level before tumbling to the 0.5980 barrier and switching the outlook to a more bearish one.

On the other hand, traders should look to the previous peak at 0.6150 as the first resistance after a successful bounce off the uptrend line, before resting near the 0.6220 obstacle again. A penetration of this level would add optimism for more buying interest until 0.6280, registered in January.

To summarize, NZDUSD has been in a bearish wave since it topped at 0.6220 in the very short term, but over the last three months, it has posted higher highs and higher lows.

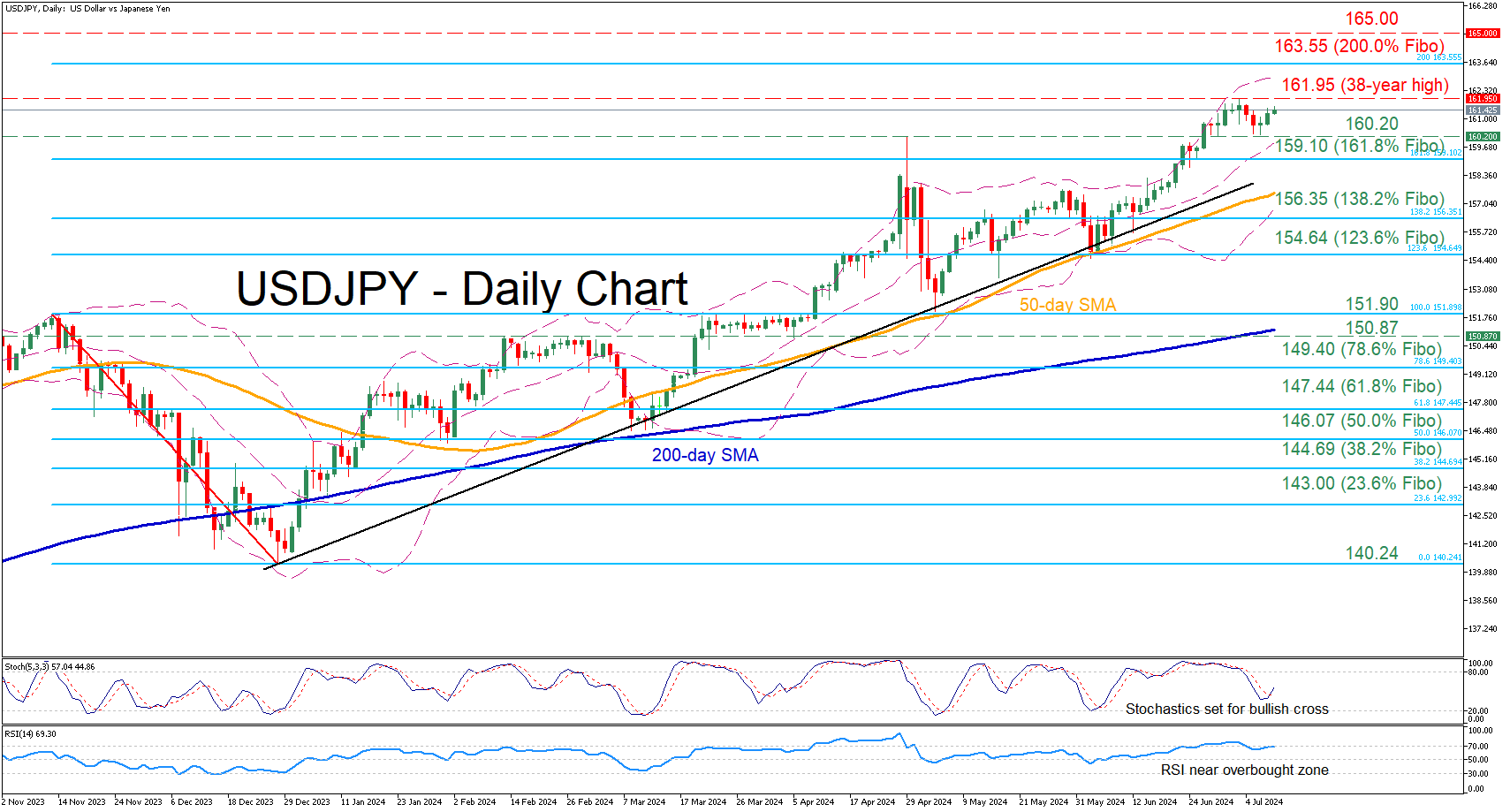

USDJPY Reapproaches Multi-Year Highs

- USDJPY edges higher after the pullback from 38-year high pauses

- The risk of a Japanese intervention is active at current levels

- Momentum indicators provide overbought signals

USDJPY experienced a minor setback from its 38-year high of 161.95, which quickly came to a halt at the April peak of 160.20. The pair is on track to revisit its recent multi-year high, but traders should be cautious as the market has approached levels that the Japanese side might be willing to defend.

Should bullish pressures persist, the price could initially challenge the 38-year high of 161.95, registered on July 3. Further advances could then cease at 163.55, which is the 200.0% Fibonacci extension of the 151.90-140.24 downleg. A break above that territory could pave the way for the 165.00 psychological mark.

Alternatively, if the pair comes under selling pressure, immediate support could be found at the April peak of 160.20, which also provided downside protection in July. Failing to halt there, the price could descend towards the 161.8% Fibo of 159.10. Even lower, the 138.2% Fibo of 156.35 could prove to be a tough barricade for the bears to overcome.

In brief, despite some near-term weakness in the aftermath of a fresh 38-year peak, USDJPY has been inching back higher. Therefore, we could see some heightened volatility moving forward as the price is trading near levels that could trigger another intervention by the Japanese authorities.

Analysis of NZD/USD: “Kiwi” Sharply Fell After Central Bank’s Decision

The Reserve Bank of New Zealand (RBNZ) kept the interest rate unchanged at 5.5% on Wednesday.

The decision to maintain the interest rate was anticipated. However, market participants noted a shift in the tone of the RBNZ's official statements. In May, the bank indicated that the tight policy would continue as long as necessary, but now it is open to easing the restrictive monetary policy if inflation slows down.

As a result, market participants are now considering the possibility of a nearer-term rate cut, which led to a decline in the New Zealand dollar relative to other currencies.

Specifically, against the US dollar, the "kiwi" fell by approximately 0.75%.

Will the decline continue as the situation develops?

According to the technical analysis of the NZD/USD chart today:

→ In 2024, the exchange rate dynamics are significantly influenced by interactions with the levels: 0.62150 (resistance), 0.58850 (support), and 0.60500 (which acts as a pivot between support and resistance, as indicated by the black arrows).

→ Bullish sentiment prevailed in the market since May, resulting in the formation of an upward blue channel on the chart. However, the bulls were unable to break through the 0.62150 resistance, and now the median of the blue channel serves as resistance (indicated by the blue arrow).

Considering the prospect of further NZD/USD price decline, it is important to note obstacles in the path of the bears in the form of supports: → from the lower boundary of the blue channel; → from the 0.60500 level, around which the price has fluctuated since the beginning of the year; → from the psychological level of 0.6.

Therefore, technically, it is possible that the downward momentum created today due to the RBNZ decision may weaken when attempting to break through these supports.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Fed Chair Explicitly Said He Didn’t Intend to Give Any Rate Timing Signals

Markets

Fed Chair Powell before Congress yesterday reiterated that the US economy is coming into better balance. It made considerable progress toward the Fed’s 2% target. The labour market has cooled but remains strong. Even so, data still have to provide the MPC greater confidence that inflation is sustainably moving to target. Recent readings showed some progress but more good data are still needed. However, from now inflation is not the only risk the Fed is facing. As the labour market is cooling, reducing policy restrain too late or too little also can unduly weaken activity and employment. Even so, the Fed Chair explicitly said that he didn’t intend to give any rate timing signals as the Fed stays in a data-dependent mode. This absence of any guidance on timing also prevented any meaningful market reaction. US yields hardly changed (2-y easing 0.2 bps while the 30-y added 2.3 bps). Even as there was little economic news on this side of the Atlantic, German yields added between 1.8 bps (2-y) and 4.2 bps (30-y). Intra-EMU spreads (vs Germany) after a mild easing on Monday, yesterday again widened (France +4 bps) as markets realized that any fiscal improvement in France, but also any many other EMU countries, will be a difficult political process. Risk premia are here to stay. The EuroStoxx 50 declined 1.33%. In the US, the S&P 500 (+ 0.07%) and the Nasdaq (+0.14%) held at record levels. Changes in the major USD cross rates were limited, with the dollar gaining on points (DXY close 105.13, EUR/USD 1.0813, USD/JPY 161.33).

This morning, Asian equities show no clear trend and mostly are little changed as are US Treasuries. EUR/USD gains marginally (1.0819). The yen weakens further beyond USD/JPY 161.(5). Today, there are no important data on both sides of the Atlantic. The market focus will mainly go to tomorrow’s US June CPI inflation. A mild 0.1% M/M & 3.1% Y/Y (headline) and 0.2%/3.4% (core) is expected. After Powell not pre-committing and with markets already discounting 2 cuts this year, a sub-consensus figure is probably needed for ST US yields to decline further (US 2-y support at 4.55%/4.59%). In this context, it also won’t be that easy for EUR/USD to break to 1.0916 resistance.

News & Views

Chinese June inflation came in at the low end of expectations again. This happening despite favorable 2023 base effects suggests ongoing (very) weak consumer demand. Prices rose 0.2% y/y (-0.2% m/m), only half of the 0.4% expected and a further deceleration from the 0.3% in May. Consumer goods deflated by 0.1% y/y while services CPI eased to 0.7% from 0.8%. The core gauge (excluding food & energy) pared May’s 0.6% (-0.1% m/m). There seems to be little improvement on the way for CPI to pick up anytime soon with factory-gate inflation (PPI) still venturing in negative territory. The -0.8% y/y outcome was in line with expectations, though, and also meant a further bottoming out from the -1.4% in May and the trough of -5.4% in June 2023. The Chinese yuan set a new 9-month low in the wake of the release. USD/CNY trades at 7.275, slowly but steadily nearing the September 2023 16-yr low of 7.35.

The Reserve Bank of New Zealand kept the policy rate unchanged at 5.5% this morning but dialed back its hawkish tone from the May meeting. Back then, persistent domestic inflation (amongst others) made policymakers discuss a rate increase before eventually deciding to keep rates high for longer and signaling no cuts before 2025Q3. There was no mention whatsoever of a potential hike in the statement today. Instead, the RBNZ expects headline inflation to return to the 1-3% target range in the second half of this year while strong domestically generated price pressures will ease. This follows a fall in capacity pressures, which the recently weaker higher frequency economic indicators suggest is coming. While agreeing that monetary policy needs to be restrictive still, the statement in another dovish twist added that “The extent of this restraint will be tempered over time consistent with the expected decline in inflation pressures.” New Zealand swap yields tank up to almost 20 bps at the front end of the curve. The RBNZ pivot triggered a strong shift in markets’ rate cut expectations. They now fully price in a first move in October (vs November yesterday) with a 60% chance discounted for a start at the next meeting in August (vs October). The kiwi dollar loses against all G10 peers this morning, including the US dollar, though losses could have been bigger. NZD/USD slips to 0.609.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Meanwhile, much of the save haven bids were reversed after the (first round in) the French elections. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed needs more evidence than just one slower-than-expected (May) CPI provided. June dots suggest one move in 2024 and four next year. The long end of the curve was also supported by increased odds of a Trump presidency after the debate with Biden. At the same time, softer US labour market data are fuelling the debate on the September Fed rate cut, steepening the curve.

EUR/USD

EUR/USD is stuck in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB taking the lead and a swing to the right in European elections pulled the pair to the 1.0665 area. However, the dollar also lost some momentum as the Fed is turning its focus to a potential softening of the labour market, potentially opening the way for policy easing in September.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. This might cap further sterling gains. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 is solid support.

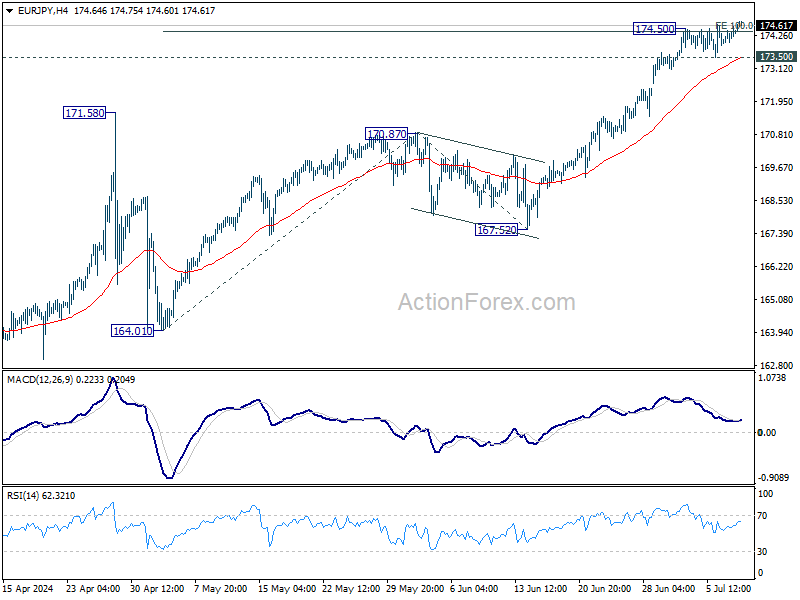

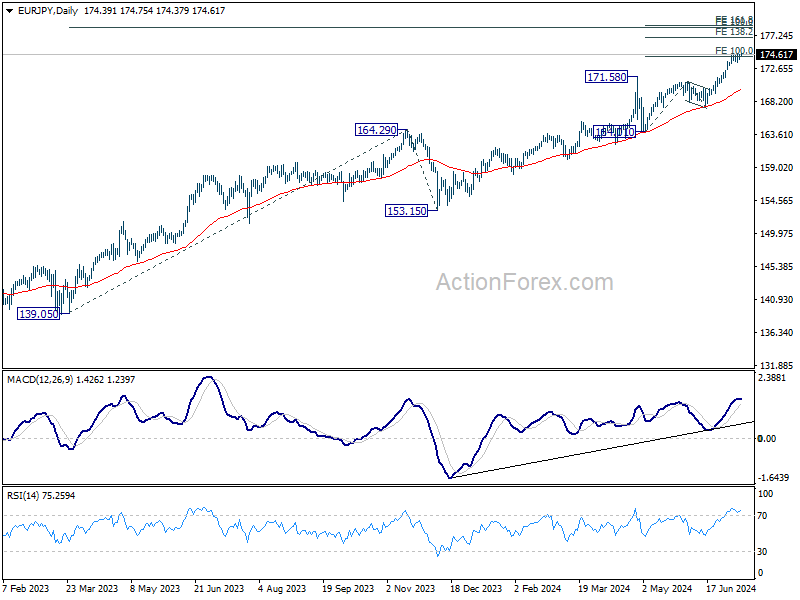

EUR/JPY Daily Outlook

Daily Pivots: (S1) 174.06; (P) 174.33; (R1) 174.70; More...

Intraday bias in EUR/JPY is back on the upside as recent up trend is trying to resistance. Sustained trading above 174.50 will target 138.2% projection of 164.01 to 170.87 from 167.52 at 177.00. On the downside, however, break of 173.50 minor support will turn bias to the downside for deeper pullback.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 139.05 to 164.29 from 153.15 at 178.38. For now outlook will stay bullish as long as 170.7 resistance turned support holds, even in case of deep pullback.

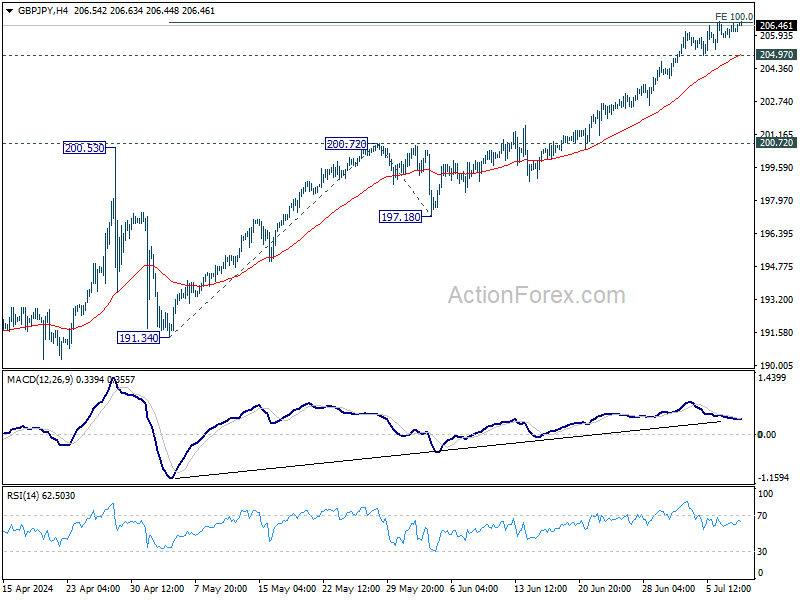

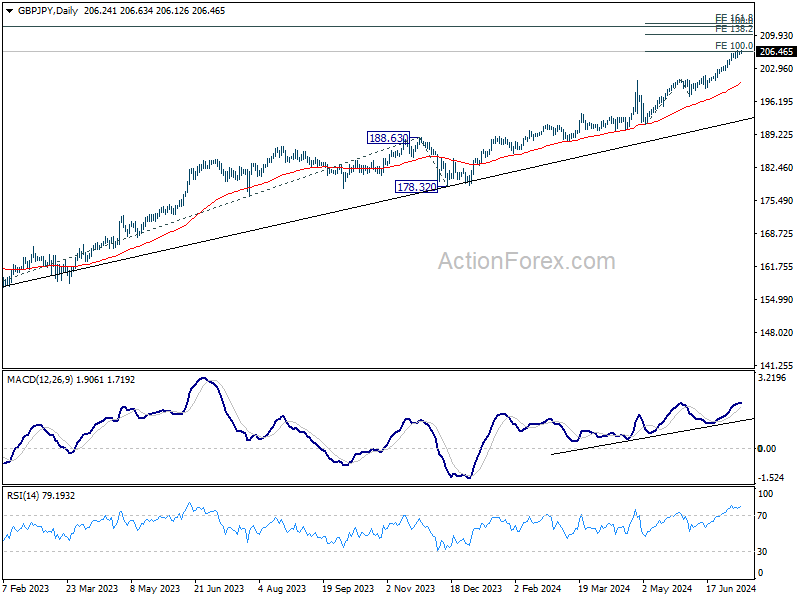

GBP/JPY Daily Outlook

Daily Pivots: (S1) 205.88; (P) 206.24; (R1) 206.60; More...

Intraday bias in GBP/JPY remains neutral at this point. Further rise is expected with 204.97 minor support intact. On the upside, sustained break of 100% projection of 191.34 to 200.72 from 197.18 at 206.56 will target 138.2% projection at 210.17. On the downside, below 204.97 minor support will turn bias to the downside for deeper pull back.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 197.18 support holds, even in case of deep pullback.

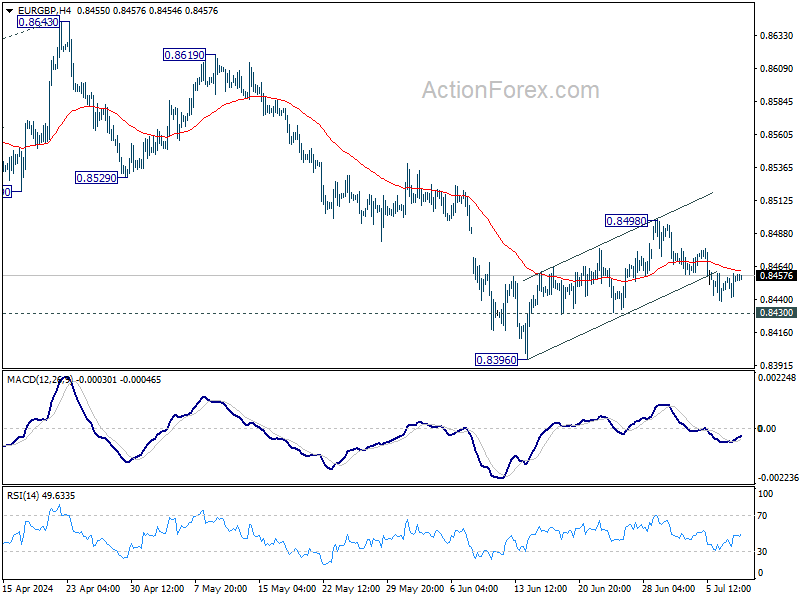

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8446; (P) 0.8453; (R1) 0.8464; More...

Intraday bias in EUR/GBP remains neutral and outlook is unchanged. On the upside, sustained trading above 55 D EMA (now at 0.8495) will extend the rise from 0.8396 short term bottom to 0.8529 support turned resistance. Nevertheless, On the downside, break of 0.8493 support will suggest that the corrective recovery has completed. Intraday bias will be back on the downside for retesting of 0.8396 low. Firm break there will resume larger down trend.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.