Sample Category Title

BoE’s Pill warns of uncomfortable strength in underlying inflation

In a speech today, BoE Chief Economist Huw Pill highlighted that while it is "welcome news" that the UK's headline CPI returned to 2% in May, it is crucial for the inflation target to be achieved on a "lasting and sustainable basis."

He emphasized three key indicators of inflation persistence: labor market tightness, pay growth, and services price inflation. Pill noted that recent developments in these areas suggest "some upside risk to my assessment of inflation persistence."

Pill pointed out that annual rates of services price inflation and wage growth, which remain close to 6%, indicate an "uncomfortable strength" in the underlying inflation dynamics.

He also cautioned that the MPC should remain cautious about interpreting any "single data" point as either a "necessary or sufficient trigger" for reassessing their stance.

RBNZ Dovishness Hits Kiwi

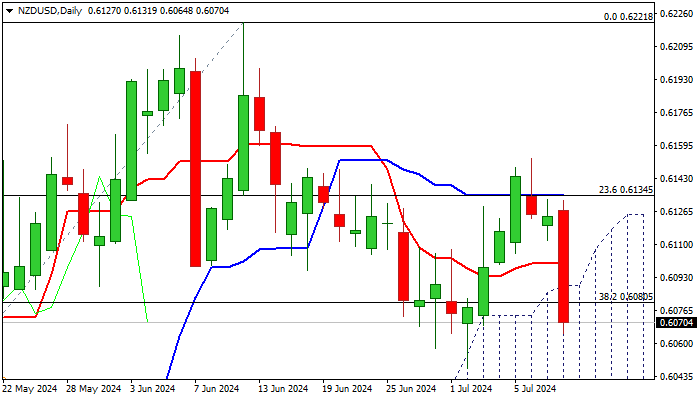

The Reserve Bank of New Zealand kept its benchmark interest rate at 5.5% for the eighth consecutive meeting, which was in line with analyst expectations. However, the central bank’s comments were softer than expected, dragging down NZDUSD by around 1% to 0.6070, a low for the week.

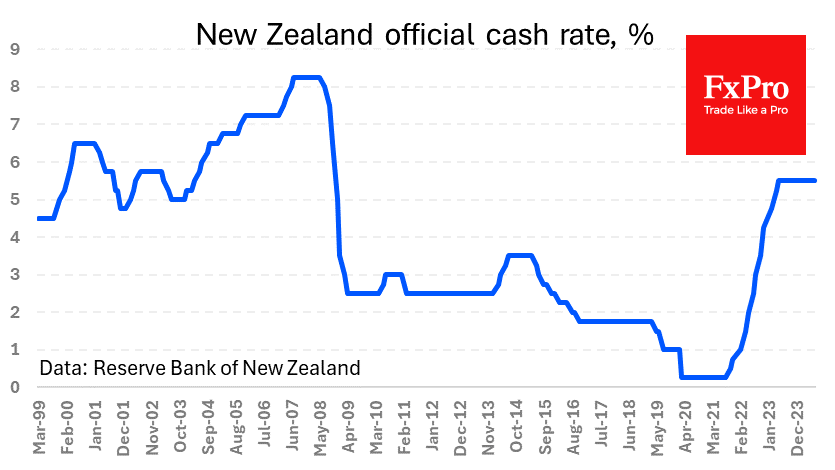

The RBNZ expects inflation to return to the 1-3% target range in the second half of the year and hinted at the possibility of reducing the degree of monetary tightening. At its last meeting in May, the regulator was leaning towards the need for another hike. However, it has now moved into line with the major global central banks, where markets have seen or expect 1-2 rate cuts before the end of the year.

By modern standards, this is a sharp policy reversal that has clipped the Kiwi’s vestigial wings.

The NZDUSD reversed to the downside last Friday from a local high of 0.6150, having broken the upper boundary of the long-term descending channel in place since January 2023. This fits into a broader trend of lower highs since 2014. The recent complete reversal in RBNZ policy is a major fundamental factor keeping the global Kiwi trend in place.

Locally, NZDUSD is testing support in the form of the 200-day moving average after breaking above the 50-day moving average (now at 0.6100) intraday. With fundamentals driving the pair, we expect further declines towards 0.5900 – a key support level over the past 12 months—over the summer months.

The pair’s dips have become increasingly shallow over the past two years, which has increased interest in the New Zealand currency’s momentum, especially near the local extremes of 0.6150 and 0.5900.

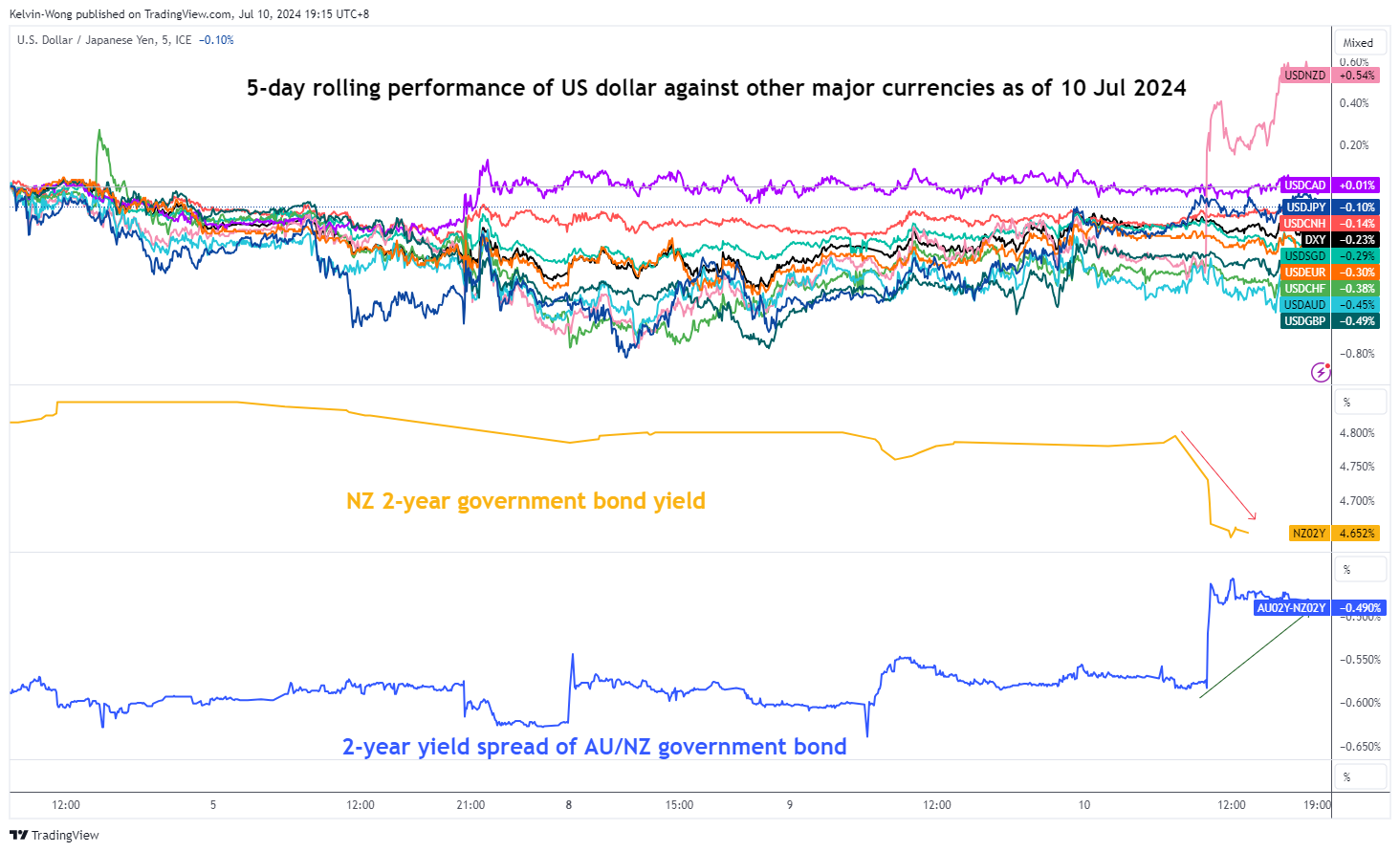

AUD/NZD: Kiwi Torpedoed by Surprise Dovish Tilt from RBNZ

- The Kiwi is the worst intraday performer among the major currencies as it slumped to a 4-week low against the US dollar.

- A dovish tilt in the latest RBNZ monetary policy statement has triggered a narrowing of the yield discount between the 2-year Australian and New Zealand government bonds.

- AUD/NZD has staged a medium-term bullish breakout above 1.1000 key support.

Since our last publication, the price actions of the AUD/NZD have inched lower to break below its 200-day moving average on 4 June and traded lower in the next three days to print an intraday low of 1.0731 on 7 June.

After that, the AUD/NZD staged a bullish reversal of +274 pips/+2.56% in the next four weeks to close at 1.1006 on Tuesday, 9 July which has almost recoupled the prior loss from its 7 May high of 1.1024.

Since the start of today’s Asian session, 10 July, the AUD/NZD has further extended its intraday gains by +96 pips/+0.87% to hit a 52-week high of 1.1103 due to a surprise dovish monetary policy statement released by New Zealand central bank, RBNZ after the conclusion on the outcome of its monetary policy decision.

A 180-degree turn from RBNZ from hawkish to dovish

The RBNZ has kept its key short-term official cash rate unchanged at 5.50% for the eighth consecutive meeting which is not a surprise to market participants. The big shock came from the tonality of its monetary policy statement where it offered a dovish tilt that implied that the current high interest rate environment in New Zealand has fed through to domestic demand more strongly than expected and a range of business and consumer-based surveys, and high-frequency data have pointed to a decline in economic activities.

That’s a 180-degree change from its prior May monetary policy statement where RBNZ’s stance was mildly hawkish as its officials had discussed the case to consider another interest rate hike and signalled that the first cut on its policy rate to only take place after Q2 2025.

A bad day for the Kiwi as it is the worst performer among the major currencies

Fig 1: 5-day rolling performance of US dollar pairs with 2-year yield spread of AU/NZ government bonds as of 10 Jul 2024 (Source: TradingView, click to enlarge chart)

Today’s “abrupt” change in RBNZ’s monetary policy statement tonality from hawkish to dovish has triggered a significant intraday sell-off of -0.86% in the Kiwi against the US dollar where it slumped the most in almost four weeks, and it is the weakest currency by a far stretch against the US dollar at this time of the writing based on a 5-day rolling performance basis (see Fig 1).

Also, the short-term interest rate swaps market has now priced in two interest rate cuts by RBNZ before 2024 ends which led to the monetary policy-sensitive yield of the 2-year New Zealand government bond to drop by 15 basis points (bps) to 4.65%, its biggest single-day drop since 28 February (see Fig 1).

The current dramatic slide seen in the 2-year New Zealand government bond yield has triggered a further narrowing of yield discount between 2-year Australian and New Zealand government bonds from -0.58% to -0.48% which in turn supports a potential outperformance of the Aussie dollar against the Kiwi.

Potential bullish acceleration in AUD/NZD towards a long-term secular range resistance

Fig 2: AUD/NZD major and medium-term trends as of 10 Jul 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the AUD/NZD cross pair has staged a bullish breakout above its former medium-term range resistance that has capped prior rallies since 20 December 2023.

In addition, the MACD trend indicator has continued to trend upwards steadily above its zero centreline since 27 June which supports a medium-term uptrend phase that is likely to have kickstarted (see Fig 2).

If the 1.1000 key medium-term pivotal support holds, the AUD/NZD may see a further potential upmove within a long-term secular range configuration in place since July 2015 with the next medium-term resistances coming in at 1.1165/1190 and 1.1430/1460 (also the upper limit of the long-term secular range configuration).

On the flipside, failure to hold at 1.1000 suggests a failure bullish breakout and the AUD/NZD may resume its choppy corrective downward drift to expose the next medium-term supports at 1.0890 (also the 50-day moving average) and below it sees 1.0735 next.

New Zealand Dollar Takes a Tumble After RBNZ’s Dovish Tone

The New Zealand dollar is sharply lower on Wednesday. NZD/USD is trading at 0.6081 in the European session, down 0.72% on the day at the time of writing.

RBNZ’s dovish tone raises rate cut expectations

The Reserve Bank of New Zealand held the cash rate at 5.50% at today’s meeting, the eight consecutive time it has maintained rates. No surprise there, but the rate statement was very dovish, which was completely unexpected.

At the previous RBNZ meeting in May, policy makers projected that the Bank would not lower interest rates until the third quarter of 2025. Today’s meeting appears to signal a significant shift away from that hawkish stance.

The heading of the policy statement was “Inflation Approaching Target Range”, in sharp contrast to the “Official Cash Rate to Remain Restrictive” in May. The statement noted that restrictive monetary policy had “significantly reduced consumer price inflation”, language which was more dovish than in the May statement. In the statement, the central bank acknowledged that policy would remain restrictive but added that this could change if, as expected, inflationary pressures eased.

The markets viewed the statement as a signal that the RBNZ might lower rates much sooner than expected, perhaps as early as the August meeting. This has triggered sharp losses for the New Zealand dollar as lower interest rates makes the New Zealand currency less attractive to investors.

The money markets have raised the possibility of an August rate cut to 60%, sharply higher than 33% prior to the rate decision. The inflation report for the second quarter, which will be released next Wednesday, will be a critical factor in the RBNZ rate decision in August.

.

NZD/USD Technical

- NZD/USD has pushed below support at 0.6114 and is testing support at 0.6079. Below, there is support at 0.6013

- 0.6180 and 0.6215 are the next lines of resistance

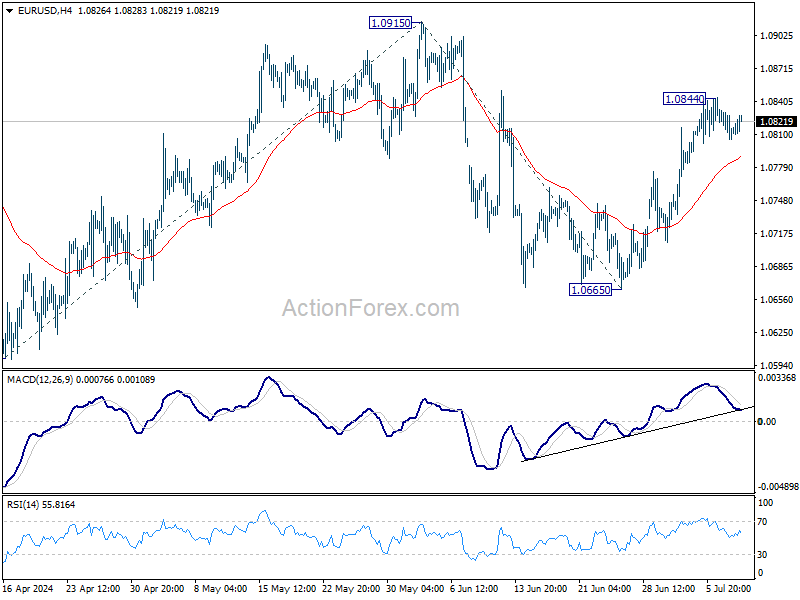

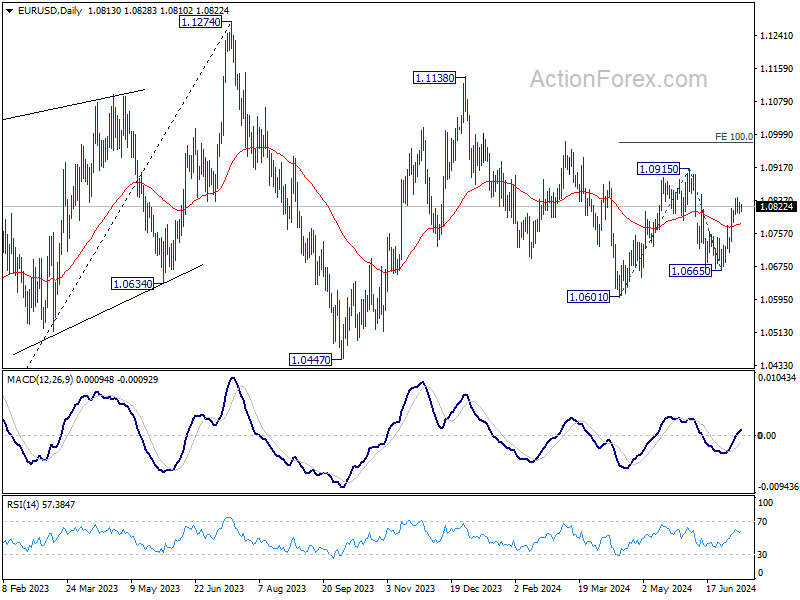

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0802; (P) 1.0824; (R1) 1.0845; More....

Intraday bias in EUR/USD remains neutral as consolidation continues below 1.0844. Further rally is in favor as long as 55 4H EMA (now at 1.0789) holds. On the upside, above 1.0844 will resume the rebound from 1.0665 to retest 1.0915 resistance. Firm break there will target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0919 next. However, sustained break of 55 4H EMA will bring deeper fall back to 1.0665 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.

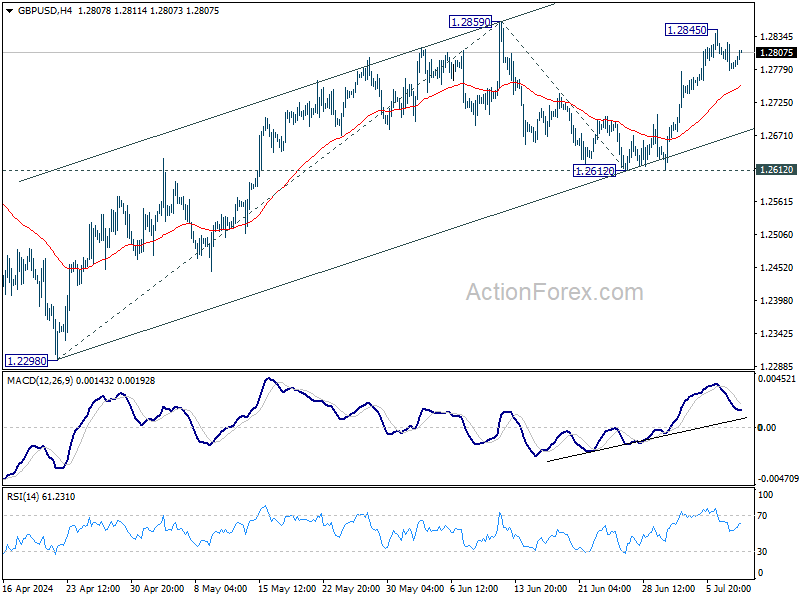

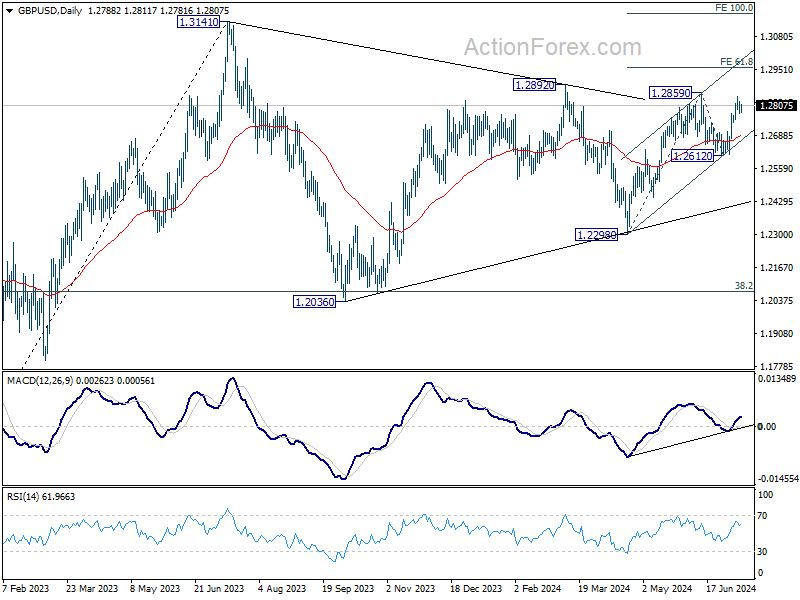

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2768; (P) 1.2797; (R1) 1.2815; More...

Intraday bias in GBP/USD remains neutral as consolidation continues below 1.2845. Further rally is expected as long as 55 4H EMA (now at 1.2752) holds. Firm break of 1.2859 will resume the rally from 1.2298 and target 61.8% projection of 1.2298 to 1.2859 from 1.2612 at 1.2959. However, sustained break of 55 4H EMA will turn bias back to the downside for 1.2612 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern which might still extend. Break of 1.2612 support will bring another fall to 1.2298 support and possibly below. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351 might be ready to resume through 1.3141.

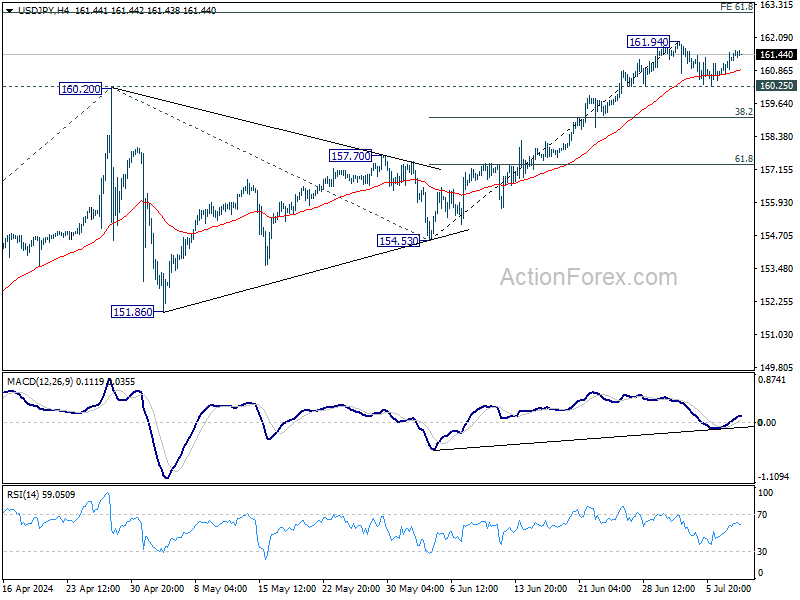

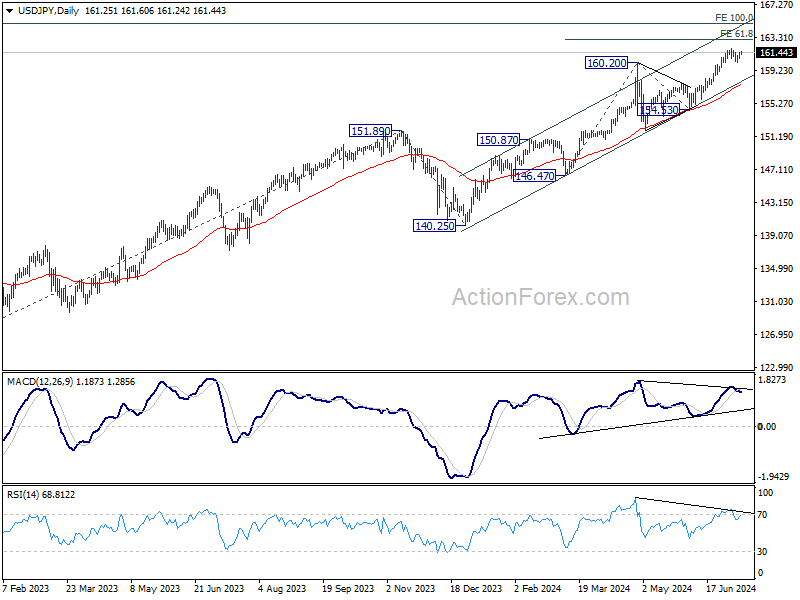

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 160.85; (P) 161.18; (R1) 161.63; More...

USD/JPY is still staying in range below 161.95 and intraday bias remains neutral. Further rally is expected with 160.25 minor support intact. On the upside, break of 161.94 will resume larger up trend to 61.8% projection of 146.47 to 160.20 from 154.53 at 163.01. Nevertheless, break of 160.25 will turn bias to the downside for deeper pullback.

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94.

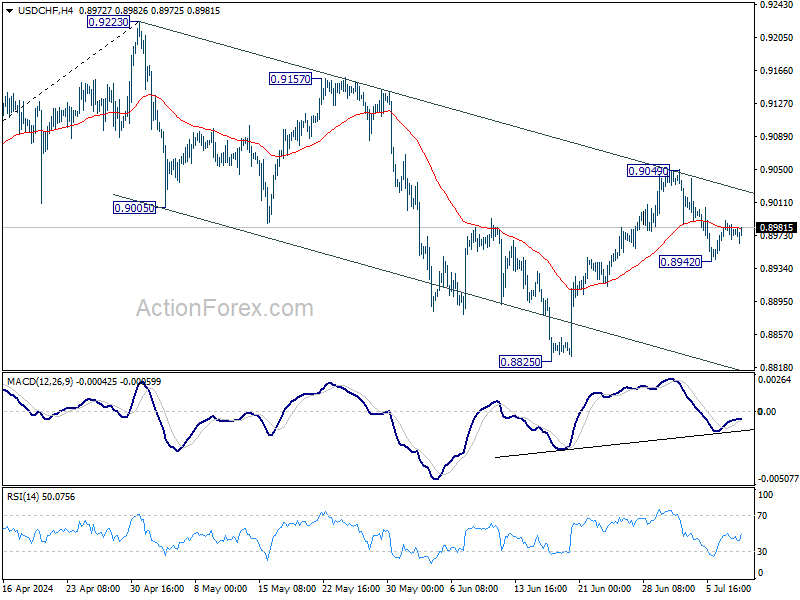

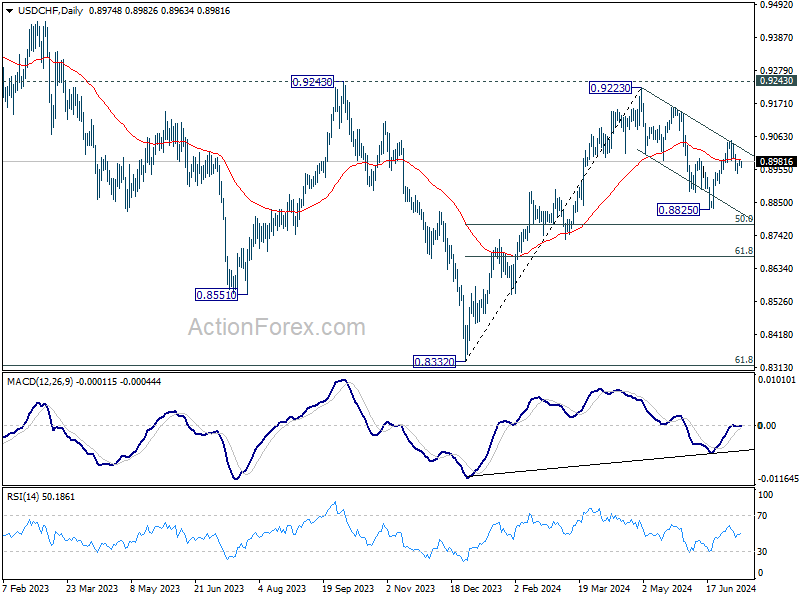

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8965; (P) 0.8978; (R1) 0.8991; More…

USD/CHF is staying in range of 0.8942/9049 and intraday bias remains neutral. As noted before, rebound from 0.8825 could have completed at 0.9049, after rejection by falling channel resistance. Below 0.8942 will bring deeper fall to 0.8825 support. Nevertheless, break of 0.9049 will revive near term bullishness and resume the rebound from 0.8825 instead.

In the bigger picture, focus remains on 0.9223/9243 resistance zone. Decisive break there would suggest larger bullish trend reversal and turn outlook bullish. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

Yen Weakness Persists in Calm Trading; Dollar Range-Bound

Yen continues its extended selloff today, except against New Zealand Dollar, in an otherwise subdued forex market. Reports indicate that BoJ may lower its economic growth forecasts for this year at its meeting later in July, while predicting that inflation will hover around 2% target in the coming years. These updated forecasts could keep the BoJ on track for another rate hike, potentially as soon as this meeting.

Additionally, BoJ's plan to taper its bond purchases is drawing attention. This week, the central bank is meeting with institutional investors to discuss its strategy. One of the megabanks has suggested significantly reducing monthly bond purchases to JPY 1T. However, opinions vary, with life insurance firms and asset managers offering diverging views—some advocating for gradual reductions, while others call for an immediate halt to purchases.

Despite these discussions, Yen is receiving little support and is likely to remain weak until BoJ's next meeting on July 30-31. Traders seem to be waiting for concrete actions rather than relying on speculative reports.

In the broader currency markets, New Zealand Dollar is the worst performer of the week so far, following today's sharp decline after RBNZ hinted at future monetary easing. This dovish shift has led markets to anticipate the first rate cut could occur in November, earlier than previously expected. Yen is the second weakest currency, followed by Swiss Franc.

On the flip side, Canadian Dollar is currently the strongest performer. Dollar is the second strongest but is on edge ahead of tomorrow's crucial US CPI release, which could significantly influence market movements. British Pound ranks third in performance, while Euro and Australian Dollar are trading in middle positions.

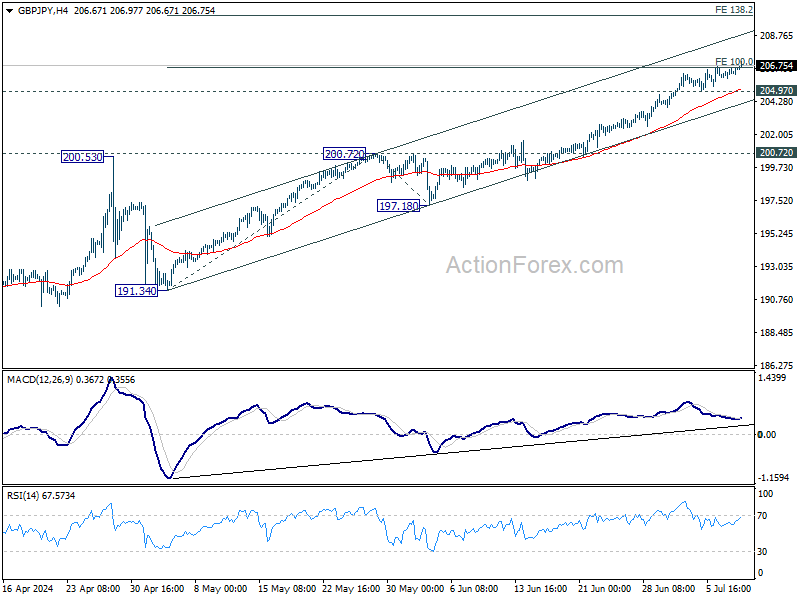

Technically, GBP/JPY's recent up trend is trying to resume today and momentum appears to be picking up slightly, as seen in 4H MACD. Near term outlook will stay bullish as long as 204.94 support holds. sustained break of 100% projection of 191.34 to 200.72 from 197.18 at 206.56 will target 138.2% projection at 210.17. The cross will be closely watching tomorrow's UK GDP release for further direction.

In Europe, at the time of writing, FTSE is up 0.61%. DAX is up 0.63%. CAC is up 0.64%. UK 10-year yield is down -0.0505 at 4.112. Germany 10-year yield is down -0.0586 at 2.528. Earlier in Asia, Nikkei rose 0.61%. Hong Kong HSI fell -0.29%. China Shanghai SSE fell -0.68%. Singapore Strait Times rose 0.99%. Japan 10-year JGB yield rose 0.0129 to 1.089.

In Europe, at the time of writing, FTSE is up 0.61%. DAX is up 0.63%. CAC is up 0.64%. UK 10-year yield is down -0.0505 at 4.112. Germany 10-year yield is down -0.0586 at 2.528. Earlier in Asia, Nikkei rose 0.61%. Hong Kong HSI fell -0.29%. China Shanghai SSE fell -0.68%. Singapore Strait Times rose 0.99%. Japan 10-year JGB yield rose 0.0129 to 1.089.

RBNZ holds rates at 5.50%, softens hawkish tone

RBNZ left OCR unchanged at 5.50%, as widely expected. The central bank softened its hawkish stance in the accompanying statement, indicating that the extent of monetary restriction "will be tempered over time consistent with the expected decline in inflation pressures." Markets interpreted this as a signal that RBNZ is moving closer to lowering interest rates.

RBNZ also acknowledged that its restrictive monetary policy has "significantly reduced consumer price inflation," with headline inflation expected to return to the 1-3% target band "in the second half of this year." This decline in inflation reflects both receding domestic pricing pressures and lower inflation for imported goods and services. Additionally, labor market pressures have eased.

While domestically generated price pressures "remain strong," RBNZ said there are signs that "inflation persistence will ease in line with the fall in capacity pressures and business pricing intentions."

China's CPI slows to 0.2% in Jun, PPI negative for 21st month

China's CPI slowed to 0.2% yoy in June, down from 0.3% yoy in May, missing expectations of a 0.4% yoy increase. Core CPI, which excludes volatile food and energy prices, rose by 0.6% yoy, unchanged from May, but slightly slower than the 0.7% increase observed in the first half of the year.

On a month-on-month basis, inflation remained negative in June, with CPI falling by -0.2%, following a -0.1% decrease in May. This continued negative trend reflects ongoing deflationary pressures in the economy.

PPI fell by -0.8% yoy, improving from the prior month's -1.4% yoy decline and matching market expectations. Despite the slight improvement, PPI has remained negative for the 21st consecutive month, indicating persistent weakness in industrial prices.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8965; (P) 0.8978; (R1) 0.8991; More…

USD/CHF is staying in range of 0.8942/9049 and intraday bias remains neutral. As noted before, rebound from 0.8825 could have completed at 0.9049, after rejection by falling channel resistance. Below 0.8942 will bring deeper fall to 0.8825 support. Nevertheless, break of 0.9049 will revive near term bullishness and resume the rebound from 0.8825 instead.

In the bigger picture, focus remains on 0.9223/9243 resistance zone. Decisive break there would suggest larger bullish trend reversal and turn outlook bullish. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jun | 2.90% | 2.90% | 2.40% | 2.60% |

| 01:30 | CNY | CPI Y/Y Jun | 0.20% | 0.40% | 0.30% | |

| 01:30 | CNY | PPI Y/Y Jun | -0.80% | -0.80% | -1.40% | |

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 08:00 | EUR | Italy Industrial Output M/M May | 0.50% | 0.20% | -1.00% | |

| 14:00 | USD | Wholesale Inventories May F | 0.60% | 0.60% | ||

| 14:30 | USD | Crude Oil Inventories | 0.7M | -12.2M | ||

| 18:00 | USD | Fed's Beige Book |

NZD/USD Outlook: Kiwi Dollar Down 1% on Dovish RBNZ

NZDUSD was sharply lower during Wednesday morning (down almost 1% for the session) deflated by the Reserve Bank of New Zealand’s dovish stance.

The central bank left interest rates unchanged at 5.5%, as widely expected, but signaled that the door for possible rate cut remains open, should inflation continue to ease in line with expectations.

Fresh weakness broke through important technical supports at 0.6100 and 0.6089/80 (daily Tenkan-sen / daily Ichimoku cloud top /Fibo 38.2% of 0.5851/0.6221) and pressuring pivotal support at 0.6047 (July 2 higher low).

Daily close within a cloud to confirm bearish signal, with violation of 0.6047 trigger to complete a failure swing pattern on daily chart and open way for test of next targets at 0.6036/25 (50% retracement / daily cloud base), with break below thickening daily cloud to further weaken near-term structure.

Rising negative momentum on daily chart and daily Tenkan/Kijun-sen in bearish setup, add to negative near-term outlook.

Corrective upticks should be ideally capped by cloud top and not exceed daily Tenkan-sen, to keep bears intact and offer better selling opportunities.

Res: 0.6089; 0.6100; 0.6134; 0.6153.

Sup: 0.6047; 0.6036; 0.6025; 0.6000.