Sample Category Title

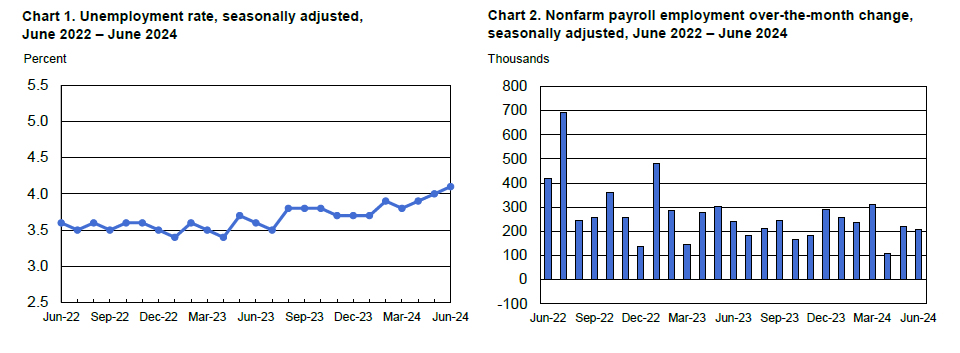

US: Payroll Gains Decelerate in June, While Unemployment Rate Ticks up to 4.1%

Non-farm employment increased by 206k in June, slightly above market expectations for a gain of 190k. However, job gains for the prior two months were revised materially lower by roughly 111k jobs.

Private payrolls rose 136k, with most of the gains concentrated in health care & social assistance (+82.4k) and construction (+27k).

In the household survey, the increase in civilian employment (+116k) lagged the increase in the labor force (+277k), pushing the unemployment rate higher by 0.1 percentage points to 4.1%. Meanwhile, the labor force participation rate ticked up by 0.1 percentage points(ppts) to 62.6%.

Average hourly earnings (AHE) were up 0.3% month-on-month (m/m) – one-tenth below May's gain. On a twelve-month basis, AHE ticked down to 3.9% (from 4.1% in May), with the three-month annualized rate falling 0.4ppts to 3.6%.

Key Implications

Payroll growth remained solid in June, but sizeable revisions to the prior two months reduced the gain in the second quarter to 607k, marking a four-year low. This cooling is consistent with other labor market metrics which have shown that the hiring rate, quit rate, and job opening to unemployed ratio are all at or below their pre-pandemic levels. Softening fundamentals have now pushed the unemployment rate to a new cycle high of 4.1%, which outside of the pandemic has not been seen since early 2018.

The resultant deceleration in average hourly earnings in June will be viewed favorably by the Federal Reserve as they look for signs of waning support to spending which would aid in cooling inflation. Chair Powell noted earlier this week that recent inflation reports have been encouraging, but that more confidence would be needed before the FOMC considers adjusting their monetary policy stance. June's employment report should bolster the Fed's confidence as we await the June CPI inflation report next week.

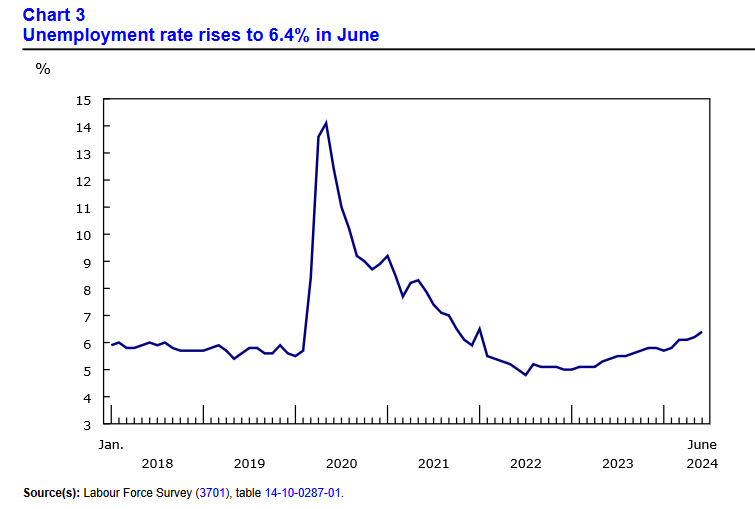

Canada’s Job Market Softens Further in June

Canadian employment was essentially unchanged in June (-1.6k), disappointing expectations for a modest 25k gain. Job losses were once again in full-time positions (-3.4k), while part-time jobs rose only slightly (1.9k).

As a result, the unemployment rate rose two tenths to 6.4%, thanks to healthy growth in the labour force (+40.4k). However, that was not due to rising participation rates, which fell one tenth to 65.3%, but a nearly 100k increase in the working age population (+98.7k).

Students aged 15 to 24 are having a particularly challenging time finding work this summer. The employment rate for returning students was 46.8%, a notable decline from 53.7% in 2022, and marks the lowest level since 1998 (outside of the pandemic in 2020).

Looking across sectors, the public administration lost jobs (-8.8k) for the first time in nearly a year. Losses were seen in eight of 16 industrial categories, with transportation and warehousing (-12k) leading the way. Job gains were led by accommodation and food services, which saw another healthy increase (+17k; +1.5%).

Lastly, total hours declined in June (-0.4% m/m), leaving them up 1.1% over the past year. That is despite employment rising 1.7% over the same period. Wage growth picked up to 5.4% year-on-year in June, impacted by base effects which are expected to peter out next month.

Key Implications

The cooling in Canada's labour market continued in June. The month saw a very slight loss of jobs, though with the standard error on monthly job swings of 32k, it is technically statistically indistinguishable from zero. But, we only need to look at the steady rise in the unemployment rate to see that by nearly all metrics, job market conditions have softened.

The softening labour market likely contributed to the Bank of Canada's confidence that it was time to start lowering interest rates last month. After today's reading, financial markets have increased their odds to greater than 50% that the next cut is coming at their July 24th decision. We still have a couple of very key indicators to go before we reach that point, including inflation and the BoC's Business Outlook Survey, which will help determine whether the next cut is July or September. In either case, Canada's economy is not falling off a cliff and we expect rate cuts will be gradual over the remainder of the year.

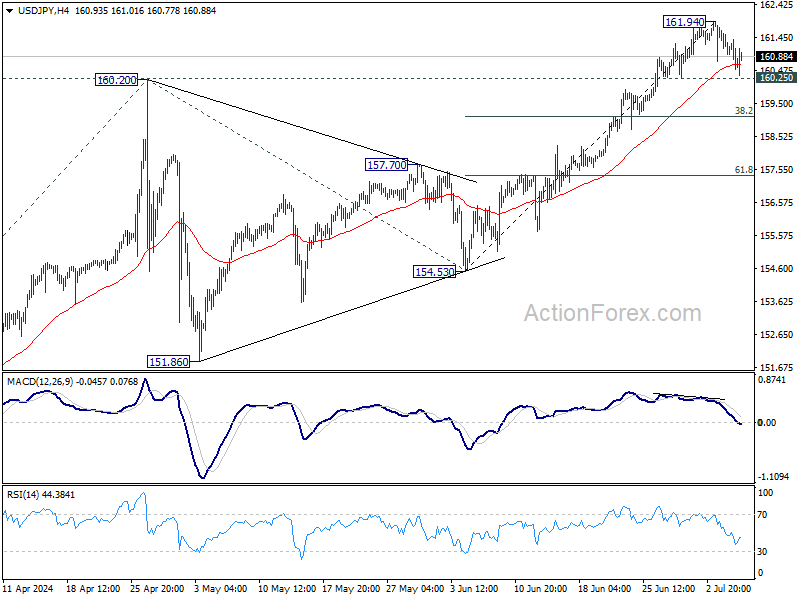

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 160.92; (P) 161.30; (R1) 161.66; More...

Outlook in USD/JPY is unchanged and intraday bias remains neutral at this point. Further rally is expected as long as 160.25 minor support holds. Break of 161.94 will resume larger up trend to 61.8% projection of 146.47 to 160.20 from 154.53 at 163.01. Nevertheless, break of 160.25 will turn bias to the downside for deeper pullback.

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94.

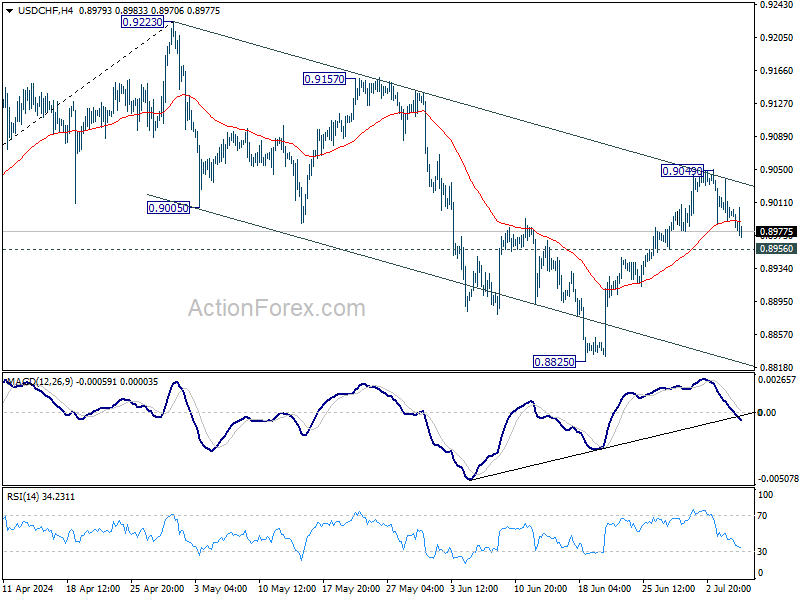

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8983; (P) 0.9012; (R1) 0.9031; More…

Intraday bias in USD/CHF remains neutral first as consolidation from 0.9049 is extending. Further rise is mildly in favor as long as 0.8956 support holds. Above 0.9049 will affirm the case that corrective fall from 0.9223 has completed at 0.8825. Further rally would then be seen to 0.9157 resistance next. However, firm break of 0.8956 will bring retest of 0.8825 support instead.

In the bigger picture, focus remains is now on 0.9223/9243 resistance zone. Decisive break there would complete a head and shoulder bottom pattern (ls: 0.8551; h: 0.8332; rs: 0.8825). That would indicate larger bullish trend reversal. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

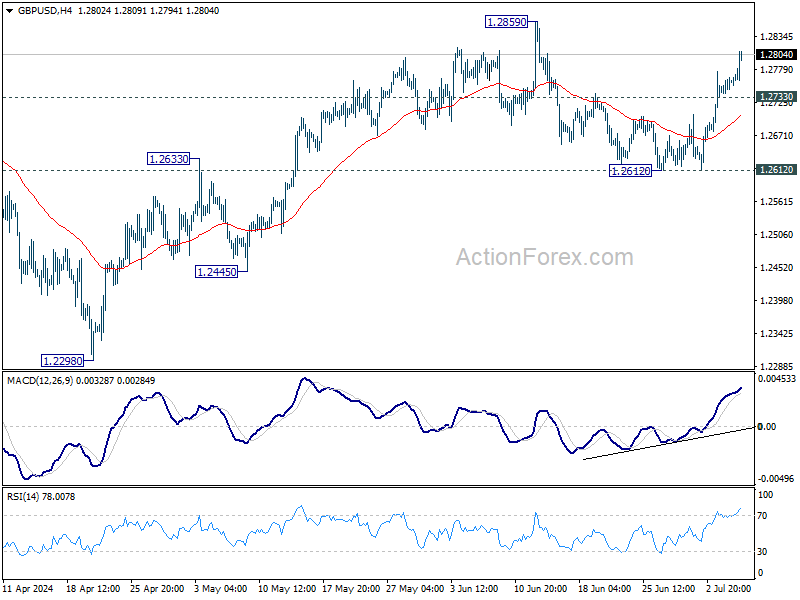

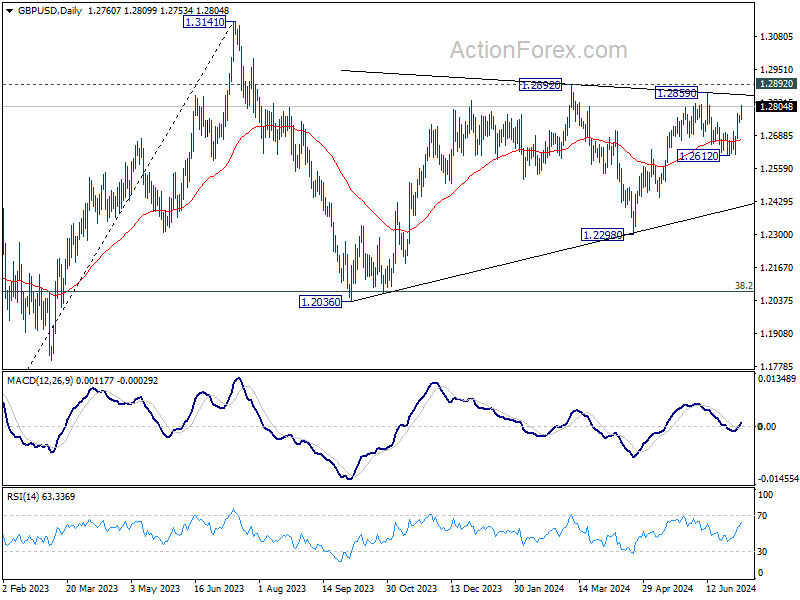

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2744; (P) 1.2756; (R1) 1.2772; More...

Intraday bias in GBP/USD remains on the upside for the moment. Rise from 1.2612 is in progress for retesting 1.2859 high. Firm break there will resume whole rally from 1.2298. On the downside, though, below 1.2733 minor support will dampen the immediate bullish case, and turn intraday bias neutral again first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351 is ready to resume through 1.3141.

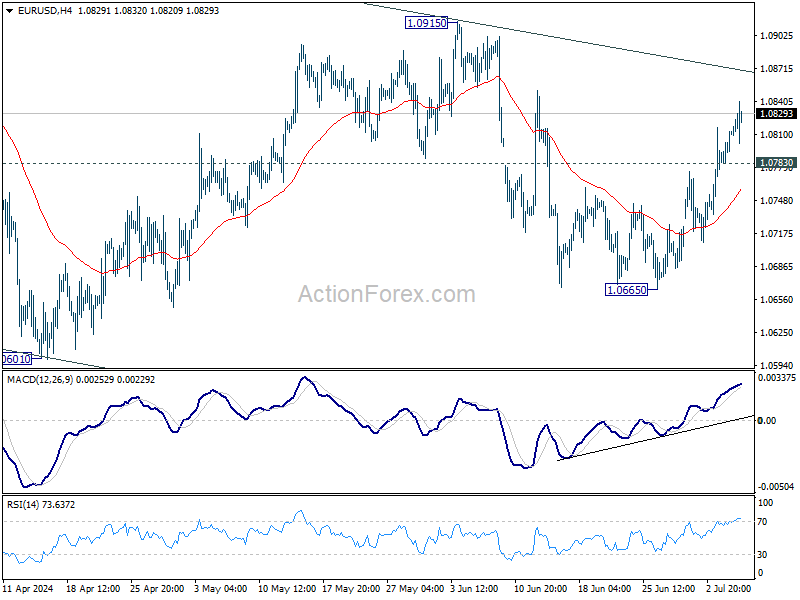

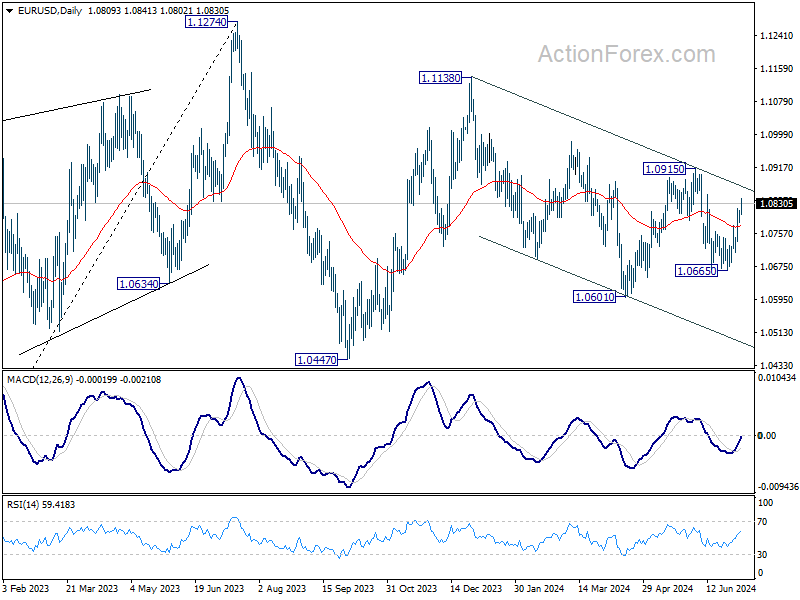

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0791; (P) 1.0804; (R1) 1.0825; More....

Intraday bias in EUR/USD remains on the upside for the moment. Rise from 1.0665 is in progress to 1.0915 resistance first. Firm break there will resume whole rebound from 1.0601. Nevertheless, on the downside, below 1.0775 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.

NFP Revisions Hits Dollar; But September Fed Cut Still Uncertain

Dollar weakened broadly after the release of the US Non-Farm Payroll report, though the initial selloff was far from decisive. June's employment data showcased a robust labor market with near-average job and solid earnings growth , coupled with just a slight uptick in unemployment rate. However, significant downward revisions to April and May's job growth numbers (-111k) suggest the labor market may not be as robust as initially reported. These mixed signals add some weight to the argument for a Fed rate cut in September, but they are not conclusive enough to cement such expectations.

At the same time, Canadian Dollar faced pressure after weak employment data for June revealed contraction in jobs and a spike in the unemployment rate. Meanwhile, Sterling continues to ride high, maintaining broad firmness as political uncertainties clear up following the UK general elections, with Labour's landslide victory injected a sense of stability. Yen is attempting a recovery but lacks consistent buying momentum. Euro is mixed as traders look forward to French election runoff on Sunday.

In Europe, at the time of writing, FTSE is up 0.01%. DAX is up 0.82%. CAC is up 0.37%. UK 10-year yield is down -0.039 at 4.164. Germany 10-year yield is down -0.010 at 2.578. Earlier in Asia, Nikkei fell -0.00%. Hong Kong HSI fell -1.27%. China Shanghai SSE fell -0.26%. Japan 10-year JGB yield fell -0.0126 to 1.070.

US NFP rises 206k in Jun, but May and Apr revised sharply lower

US Non-Farm Payroll employment increased by 206k in June, above expectation of 180k. Growth was slightly lower than average monthly gain of 220k over the prior 12 months.

However, prior month's growth was revised sharply lower from 272k to 218k. April's figure was also revised sharply lower by -57k to 165k. That is, April and May's combined downward revision was -111k.

Unemployment rate ticked up from 4.0% to 4.1%, above expectation of holding steady at 4.0%. Unemployment rate also rose slightly from 62.5% to 62.6%.

Average hourly earnings rose 0.3% mom, matched expectations. Annual hourly earnings growth slowed from 4.0% yoy to 3.9% yoy.

Canada's employment falls -1.4k in Jun, unemployment rate rises further to 6.4%

Canada's employment contracted -1.4k in June, much worse than expectation of 25.0k growth.

Unemployment rate rose from 6.2% to 6.4%, above expectation of 6.3%. It has now risen 1.3% since April 2023. Employment rate fell -0.2% to 61.1%.

Total hours worked were down -0.4% mom, up 1.1% yoy. Average hourly wages rose 5.4% yoy, up from May's 5.1% yoy.

Eurozone retail sales rises 0.1% mom in May, EU up 0.1% mom too

Eurozone retail sales volume rose 0.1% mom in May, below expectation of 0.2% mom. Sales volume, increased by 0.7% mom for food, drinks, tobacco, and by 0.4% mom for automotive fuel in specialized stores. Sales volume fell -0.2% mom for non-food products (except automotive fuel).

EU retail sales also rose 0.1% mom. Among Member States for which data are available, the highest monthly increases in the total retail trade volume were recorded in Denmark (+2.3%), Lithuania (+1.8%) and Luxembourg (+1.7%). The largest decreases were observed in Slovakia (-1.0%), Ireland (-0.9%), Bulgaria and Malta (both -0.8%).

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0791; (P) 1.0804; (R1) 1.0825; More....

Intraday bias in EUR/USD remains on the upside for the moment. Rise from 1.0665 is in progress to 1.0915 resistance first. Firm break there will resume whole rebound from 1.0601. Nevertheless, on the downside, below 1.0775 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Household Spending Y/Y May | -1.80% | 0.20% | 0.50% | |

| 05:00 | JPY | Leading Economic Index May P | 111.1 | 111.1 | 110.9 | 0.10% |

| 06:00 | EUR | Germany Industrial Production M/M May | -2.50% | 0.20% | -0.10% | |

| 06:45 | EUR | France Trade Balance (EUR) May | -8.0B | -7.2B | -7.6B | |

| 06:45 | EUR | Industrial Output M/M May | -2.10% | -0.20% | 0.50% | 0.60% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | 711B | 718B | ||

| 08:00 | EUR | Italy Retail Sales M/M May | 0.40% | 0.20% | -0.10% | |

| 09:00 | EUR | Eurozone Retail Sales M/M May | 0.10% | 0.20% | -0.50% | |

| 12:30 | USD | Nonfarm Payrolls Jun | 206K | 180K | 272K | 218K |

| 12:30 | USD | Unemployment Rate Jun | 4.10% | 4.00% | 4.00% | |

| 12:30 | USD | Average Hourly Earnings M/M Jun | 0.30% | 0.30% | 0.40% | |

| 12:30 | CAD | Net Change in Employment Jun | -1.4K | 25.0K | 26.7K | |

| 12:30 | CAD | Unemployment Rate Jun | 6.40% | 6.30% | 6.20% | |

| 14:00 | CAD | Ivey PMI Jun | 53 | 52 |

Canada’s employment falls -1.4k in Jun, unemployment rate rises further to 6.4%

Canada's employment contracted -1.4k in June, much worse than expectation of 25.0k growth.

Unemployment rate rose from 6.2% to 6.4%, above expectation of 6.3%. It has now risen 1.3% since April 2023. Employment rate fell -0.2% to 61.1%.

Total hours worked were down -0.4% mom, up 1.1% yoy. Average hourly wages rose 5.4% yoy, up from May's 5.1% yoy.

US NFP rises 206k in Jun, but May and Apr revised sharply lower

US Non-Farm Payroll employment increased by 206k in June, above expectation of 180k. Growth was slightly lower than average monthly gain of 220k over the prior 12 months.

However, prior month's growth was revised sharply lower from 272k to 218k. April's figure was also revised sharply lower by -57k to 165k. That is, April and May's combined downward revision was -111k.

Unemployment rate ticked up from 4.0% to 4.1%, above expectation of holding steady at 4.0%. Unemployment rate also rose slightly from 62.5% to 62.6%.

Average hourly earnings rose 0.3% mom, matched expectations. Annual hourly earnings growth slowed from 4.0% yoy to 3.9% yoy.

UK Election: Labour Wins in a Landslide

The UK national election on Thursday propelled the Labour Party to a sweeping victory and Labour leader Keir Starmer will become the next Prime Minister. In the six-week election campaign of the election, Labour had a massive lead in the polls and there was no doubt it would win a huge majority in parliament. The latest update indicates that Labour has won 412 seats and the Conservatives had plunged to 121 seats. This gives Labour a massive 160-seat majority in the House of Commons.

The Labour victory ends fourteen years of Conservative rule and with power comes the responsibility to revive the weak UK economy, which fell into a recession in the second half of 2023. Productivity and wages have been stagnant and the national debt is now larger than the size of the economy. Inflation has finally dropped to the 2% target but the Bank of England hasn’t lowered interest rates and that has taken a toll on businesses and households.

How will the financial markets react?

Traditionally, the Conservatives have been more business-friendly than Labour. The latter have favoured raising taxes on the highest earners and large corporations in order to fund public services and reduce inequality. Labour has, however, shifted more to the centre and Labour leader Keir Starmer has pledged to show fiscal restraint in order to lower the UK’s massive debt levels. If as Prime Minister Starmer delivers on this promise, it would preclude higher taxes or raising government spending.

The financial markets will be watching carefully but investors didn’t shown any jitters ahead of the Labour landslide. The FTSE 100, the benchmark UK stock market index, is up 0.68% this week and the British pound has climbed 1.1% against the US dollar this week. With a huge majority in parliament, Starmer will have an easier time pushing through legislation, which means that political uncertainty should not be a factor that the markets have to worry about.