Sample Category Title

US ISM services rises to 53.8, activity/production surges

US ISM Services PMI jumped from 49.4 to 53.8 in May, well above expectation of 51.0. Looking at some details, business activity/production rose sharply from 50.9 to 61.2, highest since November 2022. New orders rose from 52.2. to 54.1. Employment rose from 45.9 to 47.1. Prices fell from 59.2 to 58.1.

ISM said, "The past relationship between the Services PMI and the overall economy indicates that the Services PMI for May (53.8 percent) corresponds to a 1.6-percent increase in real gross domestic product (GDP) on an annualized basis."

BoC cuts rate to 4.75%, signals confidence in inflation control

BoC cuts overnight rate by 25 bps to 4.75%, as anticipated. The central bank stated that recent data has bolstered confidence that inflation will continue to move towards 2% target, despite ongoing risks to the inflation outlook.

BoC emphasized its close monitoring of core inflation trends, the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behavior.

Regarding the economy, BoC noted that Q1 GDP growth was slower than forecasted in the Monetary Policy Report. However, recent data suggest that the economy is "still operating in excess supply."

BoC acknowledged that measures of core inflation have slowed, with three-month measures indicating continued downward momentum. Indicators of the breadth of price increases across CPI components have moved down further, nearing their historical average. Despite this, shelter price inflation remains high.

Bank of Canada reduces policy rate by 25 basis points

The Bank of Canada today reduced its target for the overnight rate to 4¾%, with the Bank Rate at 5% and the deposit rate at 4¾%. The Bank is continuing its policy of balance sheet normalization.

The global economy grew by about 3% in the first quarter of 2024, broadly in line with the Bank’s April Monetary Policy Report (MPR) projection. In the United States, the economy expanded more slowly than was expected, as weakness in exports and inventories weighed on activity. Growth in private domestic demand remained strong but eased. In the euro area, activity picked up in the first quarter of 2024. China’s economy was also stronger in the first quarter, buoyed by exports and industrial production, although domestic demand remained weak. Inflation in most advanced economies continues to ease, although progress towards price stability is bumpy and is proceeding at different speeds across regions. Oil prices have averaged close to the MPR assumptions, and financial conditions are little changed since April.

In Canada, economic growth resumed in the first quarter of 2024 after stalling in the second half of last year. At 1.7%, first-quarter GDP growth was slower than forecast in the MPR. Weaker inventory investment dampened activity. Consumption growth was solid at about 3%, and business investment and housing activity also increased. Labour market data show businesses continue to hire, although employment has been growing at a slower pace than the working-age population. Wage pressures remain but look to be moderating gradually. Overall, recent data suggest the economy is still operating in excess supply.

CPI inflation eased further in April, to 2.7%. The Bank’s preferred measures of core inflation also slowed and three-month measures suggest continued downward momentum. Indicators of the breadth of price increases across components of the CPI have moved down further and are near their historical average. However, shelter price inflation remains high.

With continued evidence that underlying inflation is easing, Governing Council agreed that monetary policy no longer needs to be as restrictive and reduced the policy interest rate by 25 basis points. Recent data has increased our confidence that inflation will continue to move towards the 2% target. Nonetheless, risks to the inflation outlook remain. Governing Council is closely watching the evolution of core inflation and remains particularly focused on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is July 24, 2024. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR at the same time.

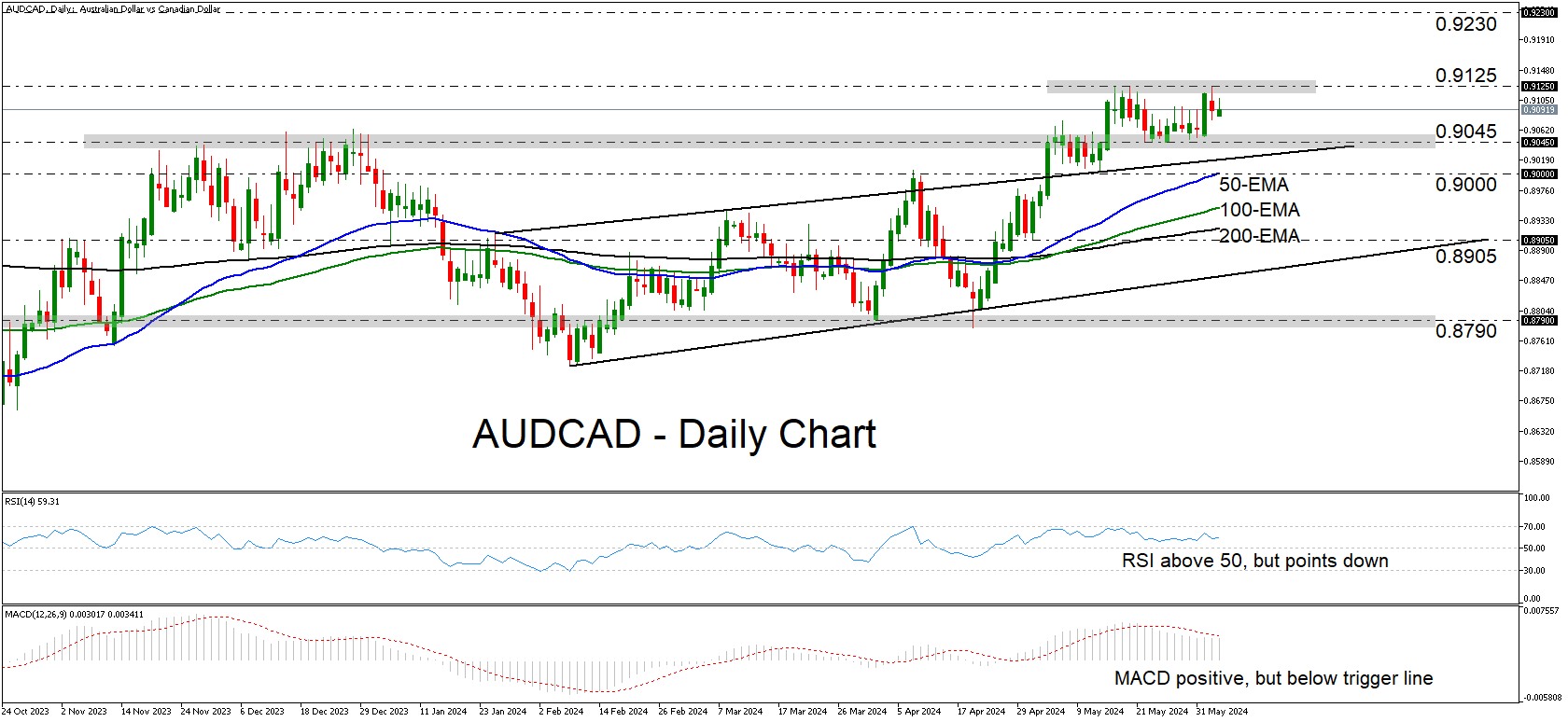

AUDCAD Consolidates Above Key Support Zone

- AUDCAD is trading sideways, above upside channel

- RSI and MACD corroborate the lack of momentum

- A break above 0.9125 could shift the bias to the upside

- A dip below 0.9000 may only confirm a larger correction

AUDCAD has been trading in a sideways manner since May 15, staying between the key support of 0.9045 and the 0.9125 resistance. In the bigger picture, the pair remains above the upper bound of an upward sloping channel, as well as above all three of the plotted moving averages, which means that the bulls could take charge again very soon.

The daily oscillators corroborate the notion that the longer-term uptrend has run out of some steam, at least temporarily. The RSI, although above 50, has turned down, while the MACD, even though positive, has dropped below its trigger line.

A break above 0.9125 could signal that the bulls are back in the driver’s seat. Such a move would confirm a higher high and may see scope for advances towards the 0.9230 zone, a territory last tested more than a year ago, on March 22 and 23, 2023.

On the downside, a break back below the 0.9000 round number may signal the pair’s return within the aforementioned upside channel. Thus, the outlook would still be far from reversing to bearish. For that to happen, AUDCAD may need to drop below the 0.8905 territory.

To recap, AUDCAD is consolidating above the upper bound of a prior bullish channel, which implies that the next directional leg could still be positive.

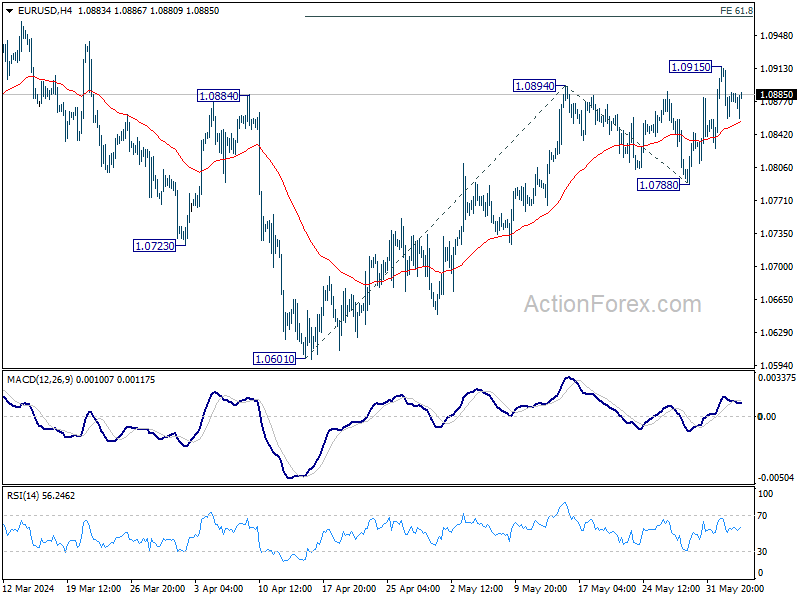

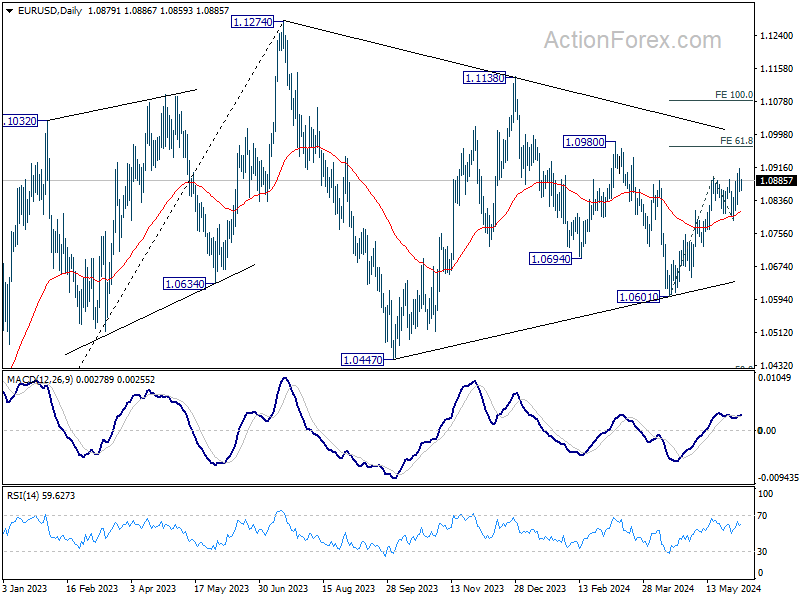

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0853; (P) 1.0885; (R1) 1.0910; More…

Intraday bias in EUR/USD remains neutral for the moment, as consolidation continues below 1.0915. Further rally is expected as long as 1.0788 support holds. Break of 1.0915 will resume the rally from 1.0601 to 61.8% projection of 1.0601 to 1.0894 from 1.0788 at 1.0969. However, firm break of 1.0788 will turn bias back to the downside for deeper decline instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0788 support will extend the corrective pattern instead.

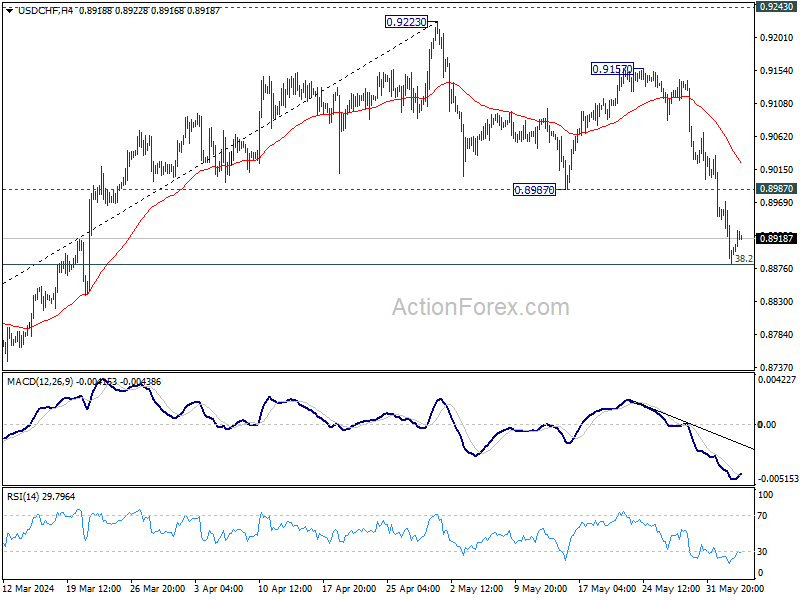

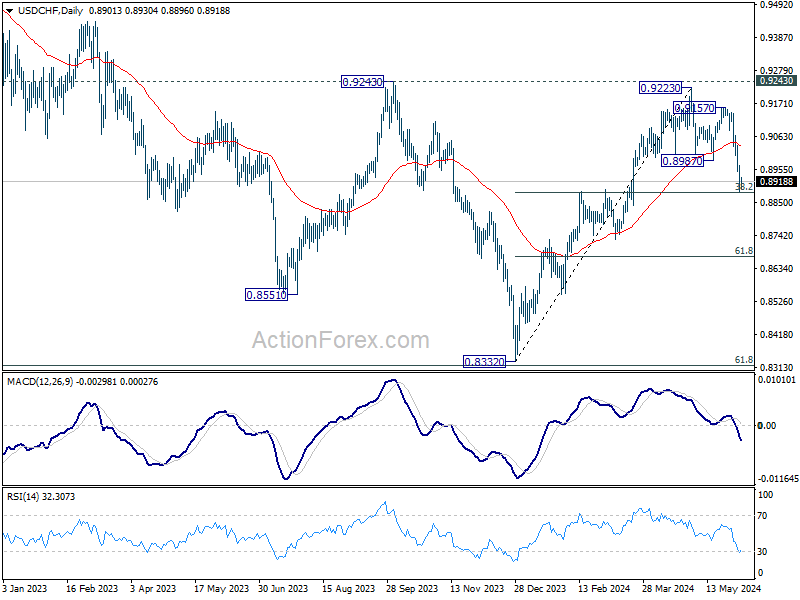

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8867; (P) 0.8919; (R1) 0.8954; More….

Intraday bias in USD/CHF is turned neutral with 4H MACD crossed above signal line. Strong rebound from current level, followed by break of 0.8987 support turned resistance, will suggest that correction from 0.9223 has completed, and retain near term bullishness. However, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

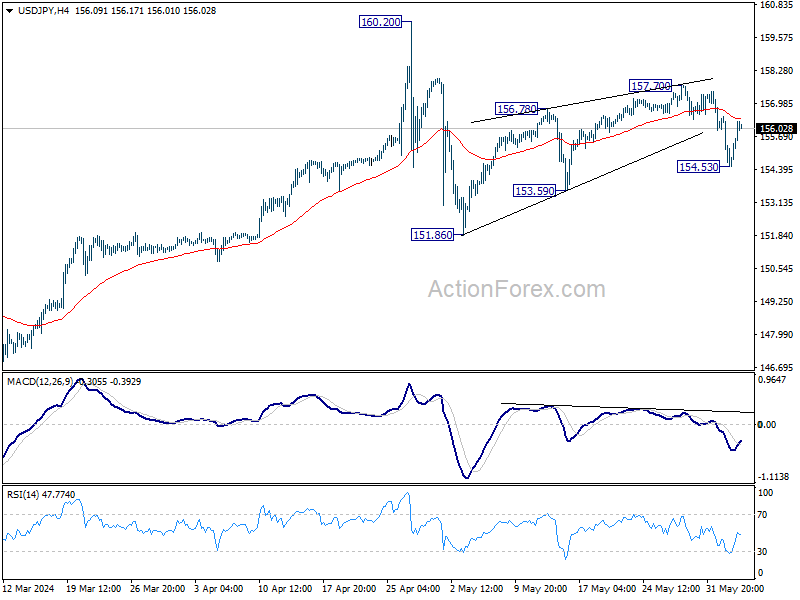

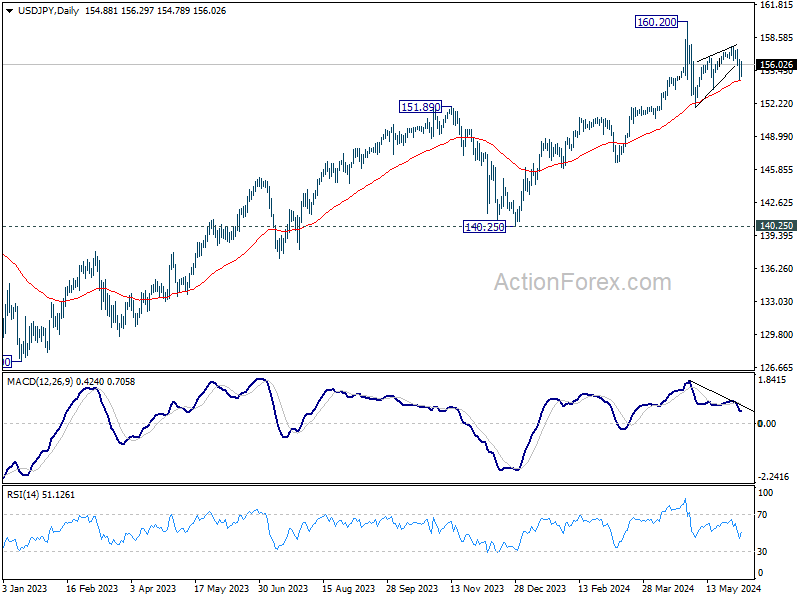

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.13; (P) 155.31; (R1) 156.07; More….

Intraday bias in USD/JPY remains neutral for the moment. Risk will stay on the downside as long as 157.70 resistance holds. Fall from there is seen as the third leg of the corrective pattern from 160.20. On the downside, break of 154.53 will target 153.59 support first. Break there will pave the way to 151.86 support and below.

In the bigger picture, a medium term top might be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

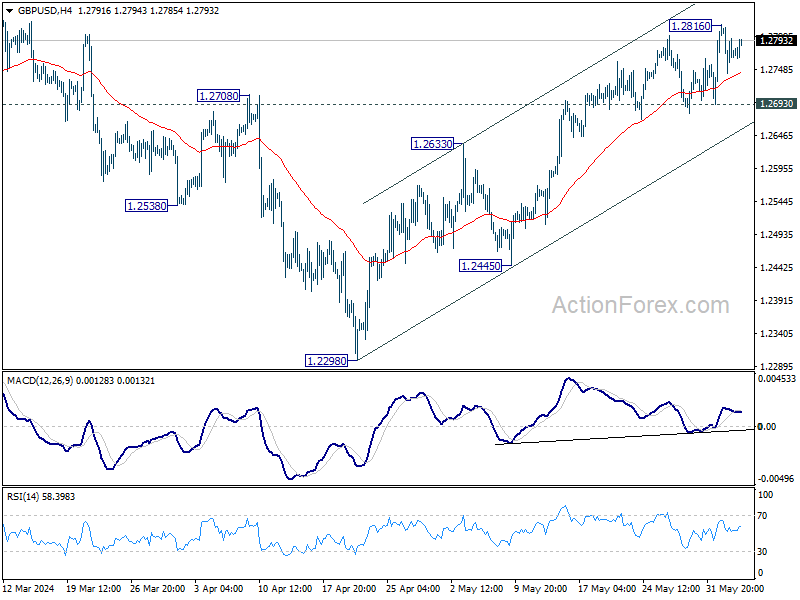

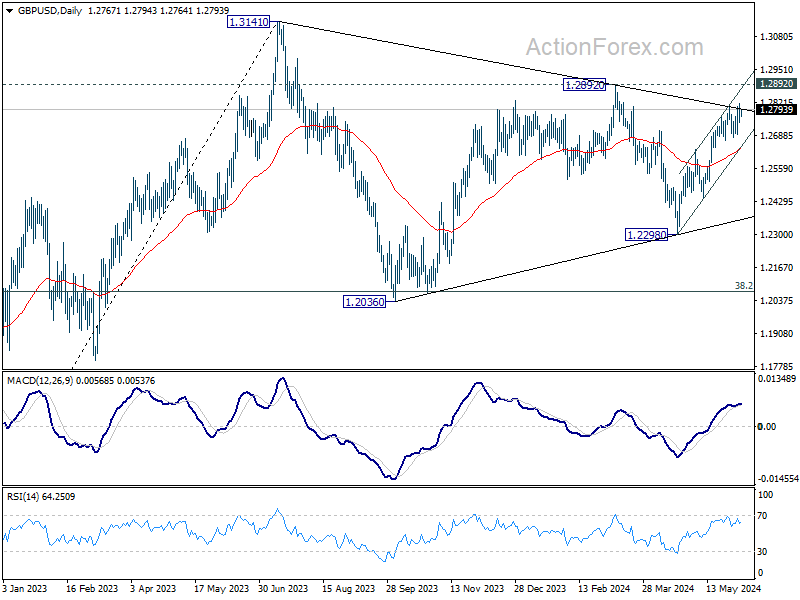

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2737; (P) 1.2777; (R1) 1.2810; More…..

Range trading continues in GBP/USD and intraday bias stays neutral for the moment. Further rise is in favor as long as 1.2693 support holds. Above 1.2816 will resume the rally from 1.2298 to 1.2892 resistance next. On the downside, break of 1.2693 minor support will turn intraday bias to the downside for deeper pullback instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

Subdued Trading Continues as Markets Shrug US ADP Disappointment

Trading in the forex markets is subdued US session gets underway, with weaker-than-expected U.S. ADP private job data failing to stir significant movement in the Dollar. Despite the slowdown in job gains and pay growth, the job market remains robust. US futures are pointing to a flat open, and the 10-year yield is down slightly. Market focus is now shifting towards the upcoming US ISM Services data and BoC's rate decision.

For the week, the Franc stands out as the strongest performer at this point, significantly outpacing other currencies. The second placed Japanese Yen is seeing some reversal of its gains from yesterday. New Zealand Dollar holds its position as the third strongest, in stark contrast to Canadian and Australian Dollars, which are among the weakest. Dollar, Euro, and Sterling are exhibiting mixed performances, with the Greenback trending slightly softer.

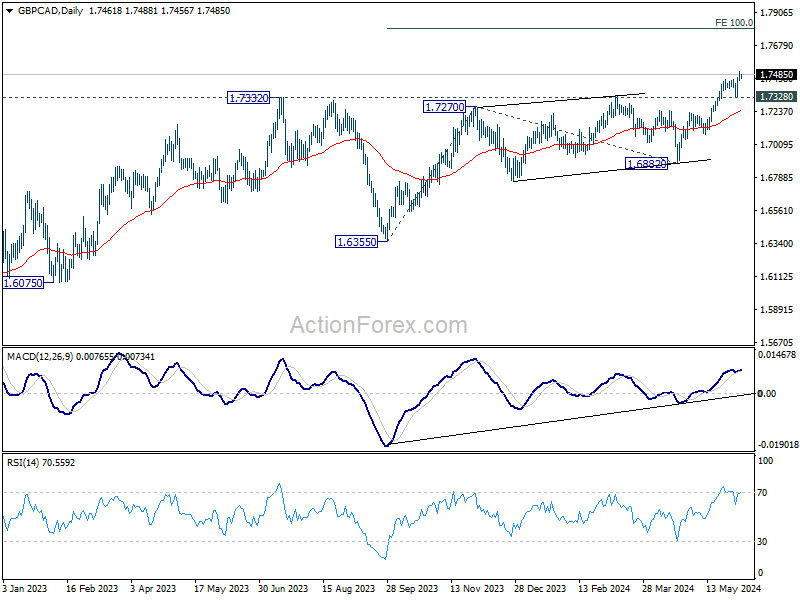

Technically, GBP/CAD's up trend resumed this week and edged higher to 1.7504. While some volatility might be seen today, near term outlook will stay bullish as long as 1.7328 support holds. Current rise should continue to 100% projection of 1.6355 to 1.7270 from 1.6882 at 1.7797.

In Europe, at the time of writing, FTSE is up 0.50%. DAX Is up 1.15%. CAC is up 1.19%. UK 10-year yield is up 0.004 at 4.186. Germany 10-year yield is down -0.0153 at 2.521. Earlier in Asia, Nikkei fell -0.89%. Hong Kong HSI fell -0.10%. China Shanghai fell -0.83%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield fell -0.0323 to 1..005.

US ADP employment roses 152k, below expectation 175k

US ADP private employment grew 1252k in May, below expectation of 175k increase. By sector, goods-producing jobs rose 3k while services-providing jobs rose 149k. By establishment size, small companies lose -10k jobs. Medium companies added 79k while large companies added 98k.

Pay gains for job-stayers held steady for the third month at 5.0% yoy. Meanwhile, for job-changes, median change in annual pay was at 7.8% yoy.

“Job gains and pay growth are slowing going into the second half of the year," said Nela Richardson, chief economist, ADP. “The labor market is solid, but we're monitoring notable pockets of weakness tied to both producers and consumers."

Eurozone PPI down -1.0% mom, -5.7% yoy in Apr

Eurozone PPI fell -1.0% mom in April, below expectation of -0.5% mom. Over the 12-month period, PPI fell -5.7% yoy. For the month, industrial producer prices increased by 0.3% for intermediate goods, 0.2% for capital goods, 0.2% for durable consumer goods, 0.1% for non-durable consumer goods. PPI decreased by -3.6% for energy.

EU PPI fell -0.1% mom, -5.5% yoy. The largest monthly decreases in industrial producer prices were recorded in France (-3.6%), Croatia (-1.9%) and Greece (-1.8%). The highest increases were observed in Denmark (+2.8%), Ireland (+0.8%) and Finland (+0.3%).

Eurozone PMI composite finalized at 52.2, a 12-month high

Eurozone PMI Services was finalized at 53.2 in May, slightly down from April's 53.3. PMI Composite was finalized at 52.2, up from prior month's 51.7, a 12-month high. Also, business confidence surged to 27-month high. Inflation rates cooled but remained above pre-pandemic averages.

A closer look at individual countries reveals varying levels of economic activity. Spain leads with a robust Composite PMI of 56.6, marking a 14-month high. Germany follows with a Composite PMI of 52.4 and hitting a 12-month peak. Conversely, Italy's PMI dipped to a three-month low of 52.3, and France lagged with a Composite PMI of 48.9 and marking a two-month low.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, commented on the broader implications of these figures: "The spectre of recession is off the table." He highlighted the crucial role of the service sector in driving this positive shift, noting, "In Germany, we can now talk of an upward trend, Italy's business activity remains solid, and Spain has improved from an already strong position." However, he also acknowledged the challenges facing France, which has seen a recent dip in economic performance.

UK PMI services finalized at 52.9, expansion slows, price pressures ease

The latest PMI data from the UK indicates a deceleration in the service sector for May, with the Services PMI dropping to 52.9 from April's 55.0, marking the slowest growth rate since November. The Composite PMI, which aggregates both services and manufacturing, also experienced a downturn, finishing at 53.0 compared to 54.1 the previous month.

Joe Hayes, Principal Economist at S&P Global Market Intelligence, provided insights into the broader implications of these figures, stating that the PMI survey reflected a "reasonable rate of expansion" in the UK service sector. Coupled with data from the manufacturing sector, the PMIs collectively suggest an approximate GDP growth of around 0.3% for the second quarter.

A significant development from the PMI surveys is the moderation in price increases for UK services, which have risen at the slowest pace in over three years. This marks the third consecutive month of diminishing selling price inflation in the service sector, a trend that will likely be welcomed by BoE. According to Hayes, this trend suggests that "the trajectory of services prices is moving in the right direction," potentially easing concerns about persistent inflationary pressures.

Japan's nominal labor earnings rise 2.1% yoy, real wages still declining

Japan's nominal labor cash earnings increased by 2.1% yoy in April, surpassing the expected 1.7% and marking the 28th consecutive month of growth. Excluding bonuses and nonscheduled payments, average wages climbed by 2.3% yoy. However, overtime and other allowances were down by -0.6% yoy.

Despite the rise in nominal wages, real wages fell by -0.7% yoy, continuing a 25-month streak of declines, the longest on record. Nonetheless, the rate of decline was smaller than the revised -2.1% yoy drop in March, as many major companies implemented salary increases during the latest spring annual wage negotiations.

Japan's PMI composite hits highest since August 2023

Japan's PMI Services index was finalized at 53.8 in May, slightly lower than April's 54.3. Meanwhile, PMI Composite index rose to 52.6 from 52.3 in April, marking its highest level since August 2023 and staying above 50 neutral mark for the fifth consecutive month.

Trevor Balchin, Economics Director at S&P Global Market Intelligence, noted that the Japanese service sector's "strong upturn was sustained," with only slight easing in growth rates for activity and new work. New export business expanded the most since this metric was introduced in September 2014. Both the future activity and employment indices increased since April and were among the highest on record.

Balchin also highlighted that while costs continued to rise sharply, the strong demand for services led firms to be confident in raising prices. In May, average prices charged for services increased at the third-fastest rate on record, following only April 2014 and April 2024.

RBA's Bullock discusses plan A and two backups amid inflation concerns

RBA Governor Michele Bullock addressed a senate panel today, emphasizing the importance of controlling inflation despite balanced risks. She underscored the necessity of bringing inflation back down to the target band, warning that if inflation doesn't appear to be heading in the right direction, "we'll have to take action.”

In her elaboration on the RBA's rate-setting approach, Bullock described a "Plan A," which involves a data-driven methodology, keeping all options open without committing to a specific course of action prematurely. That is, RBA does “not rule anything in or out.”

She also outlined two contingency "Plan Bs" depending on economic developments: one for persistently high inflation, and another for a significant economic downturn.

"If it turns out that inflation is starting to head higher again or it’s much stickier then we won’t hesitate to move and raise interest rates again," Bullock declared. Conversely, she noted that a weaker-than-expected economy would prompt considerations for easing rates to mitigate deflationary pressures.

Australia's Q1 GDP rises 0.1% qoq, lowest annual growth since late 2020

Australia's GDP grew by 0.1% qoq in Q1, below the anticipated 0.2% growth. On a year-over-year basis, GDP increased by 1.1%.

Katherine Keenan, head of national accounts at ABS, remarked that GDP growth was weak in March, marking the lowest annual growth rate since December 2020. She also highlighted that GDP per capita fell for the fifth consecutive quarter, declining by -0.4% in March and -1.3% over the past year.

China's Caixin PMI services rises to 54, highest level since July 2023

China's Caixin PMI Services index jumped from 52.5 to 54.0 in May, exceeding expectations of 52.6. This marks the 17th consecutive month of expansion and the highest reading since July 2023. Similarly, PMI Composite rose from 52.8 to 54.1, indicating expansion for the 7th straight month and at the fastest pace in a year.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that growth in supply and demand in both the manufacturing and services sectors picked up pace, with a particularly strong increase in services demand. He mentioned that exports in both sectors improved amid market optimism. Additionally, employment in the services industry shifted from a decline to an increase, driving the composite index into expansion for the first time in nine months.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2737; (P) 1.2777; (R1) 1.2810; More…..

Range trading continues in GBP/USD and intraday bias stays neutral for the moment. Further rise is in favor as long as 1.2693 support holds. Above 1.2816 will resume the rally from 1.2298 to 1.2892 resistance next. On the downside, break of 1.2693 minor support will turn intraday bias to the downside for deeper pullback instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q1 | 5.10% | 2.80% | -7.80% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Apr | 2.10% | 1.70% | 0.60% | 1.00% |

| 00:30 | JPY | Services PMI May F | 53.8 | 53.6 | 53.6 | |

| 01:30 | AUD | GDP Q/Q Q1 | 0.10% | 0.20% | 0.20% | 0.30% |

| 01:45 | CNY | Caixin Services PMI May | 54 | 52.6 | 52.5 | |

| 06:45 | EUR | France Industrial Output M/M Apr | 0.50% | 0.50% | -0.30% | |

| 07:45 | EUR | Italy Services PMI May | 54.2 | 54.5 | 54.3 | |

| 07:50 | EUR | France Services PMI May F | 49.3 | 49.4 | 49.4 | |

| 07:55 | EUR | Germany Services PMI May F | 54.2 | 53.9 | 53.9 | |

| 08:00 | EUR | Eurozone Services PMI May F | 53.2 | 53.3 | 53.3 | |

| 08:30 | GBP | Services PMI May F | 52.9 | 52.9 | 52.9 | |

| 09:00 | EUR | Eurozone PPI M/M Apr | -1.00% | -0.50% | -0.40% | -0.50% |

| 09:00 | EUR | Eurozone PPI Y/Y Apr | -5.70% | -5.10% | -7.80% | |

| 12:15 | USD | ADP Employment Change May | 152K | 175K | 192K | 188K |

| 12:30 | CAD | Labor Productivity Q/Q Q1 | -0.30% | 0.40% | 0.40% | |

| 13:45 | CAD | BoC Interest Rate Decision | 4.75% | 5.00% | ||

| 13:45 | USD | Services PMI May F | 54.8 | 54.8 | ||

| 14:00 | USD | ISM Services PMI May | 51 | 49.4 | ||

| 14:30 | USD | Crude Oil Inventories | -2.1M | -4.2M |

US ADP employment roses 152k, below expectation 175k

US ADP private employment grew 152k in May, below expectation of 175k increase. By sector, goods-producing jobs rose 3k while services-providing jobs rose 149k. By establishment size, small companies lose -10k jobs. Medium companies added 79k while large companies added 98k.

Pay gains for job-stayers held steady for the third month at 5.0% yoy. Meanwhile, for job-changes, median change in annual pay was at 7.8% yoy.

“Job gains and pay growth are slowing going into the second half of the year," said Nela Richardson, chief economist, ADP. “The labor market is solid, but we're monitoring notable pockets of weakness tied to both producers and consumers."