Sample Category Title

EUR/USD: Bulls Hold Grip Ahead of Key Event – ECB Policy Decision

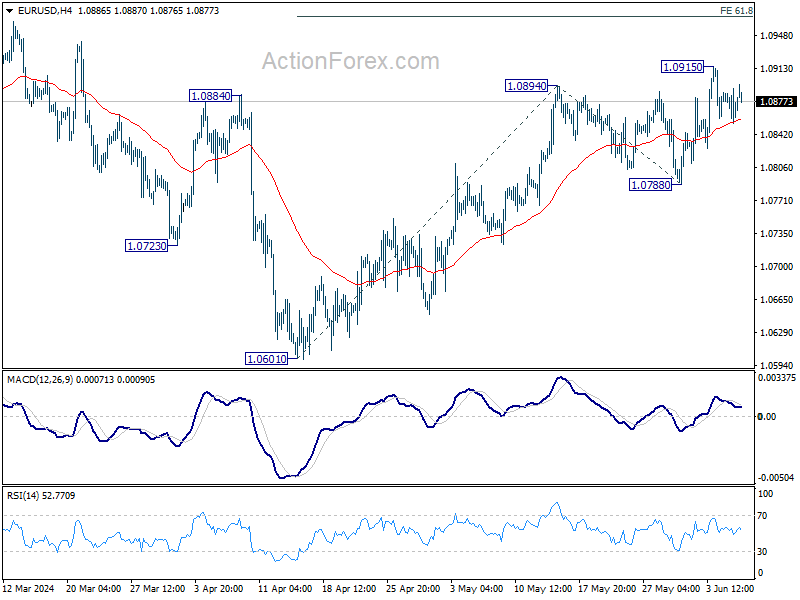

The Euro edged higher on Thursday morning and partially reversed a two-day pullback from new multi-week high (1.0915), but today’s action was so far choppy and lacking direction, as traders await the verdict from the ECB later today.

The European Central Bank policymakers meet today and widely expected to deliver the first rate cut by 25 basis points (3.75% from 4.0%), which will point to progress made in a battle with high inflation, despite the fight is not over yet.

More significant will be the comments from President Lagarde in the following press conference, which will give more details about ECB’s next steps, in light of the impact from high borrowing cost to the economy and sticky services inflation.

Overall, ECB’s hawkish stance (signals that the central bank may not show readiness to continue policy easing but will turn to more cautious mode) is expected to be positive for the single currency, while dovish view would increase pressure on Euro.

The ECB has been criticized for waiting for the Fed to take the first step before starting to cut rates, so today’s action could be seen as reaction to such comments and proof of the central bank’s independence.

But this is not to be the main issue, as the central bank faces much bigger problem of being squeezed by two strong and opposite forces – sticky inflation which still holds away from 2% target and requires tighter monetary policy and weakening economic conditions from high interest rates and persisting reverse impact from a massive economic sanctions on Russia, which hurts the most EU’s largest economy – Germany.

Technical picture on daily chart is bullish, as positive momentum is picking up and MA’s in bullish setup continue to underpin.

Near-term bias is expected to remain with bulls while the price action stays above daily Tenkan-sen (1.0852), while break here would weaken near-term structure and allow for deeper pullback, but larger bulls to remain in play if strong supports at 1.0800/1.0790 zone (psychological / Fibo 38.2% of 1.0601/1.0915 / daily Tenkan-sen) contain extended dips and mark a healthy correction of a larger uptrend.

Conversely, sustained break of recent tops (1.0895/1.0915) to signal bullish continuation and expose key barriers at 1.1000 zone (2024 top / psychological).

Res: 1.0895; 1.0915; 1.0942; 1.1000.

Sup: 1.0852; 1.0841; 1.0795; 1.0758.

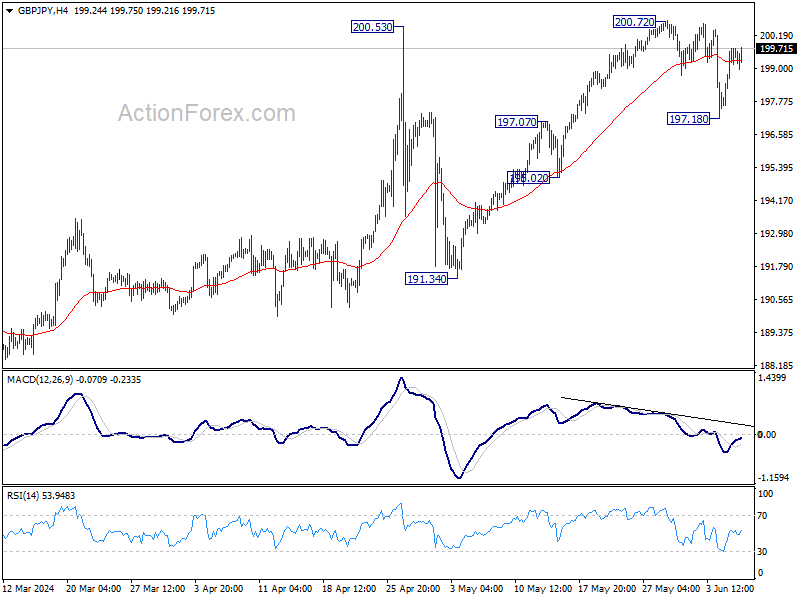

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.08; (P) 198.92; (R1) 200.48; More….

Intraday bias in GBP/JPY remains neutral for the moment. Current development suggests that rise from 191.34 has completed at 200.72 after rejection by 200.53. On the downside, break of 197.18 will resume the fall to 155.02. Further break of 195.02 will target 191.34 support next.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Sustained trading above 200.53 will pave the way to 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

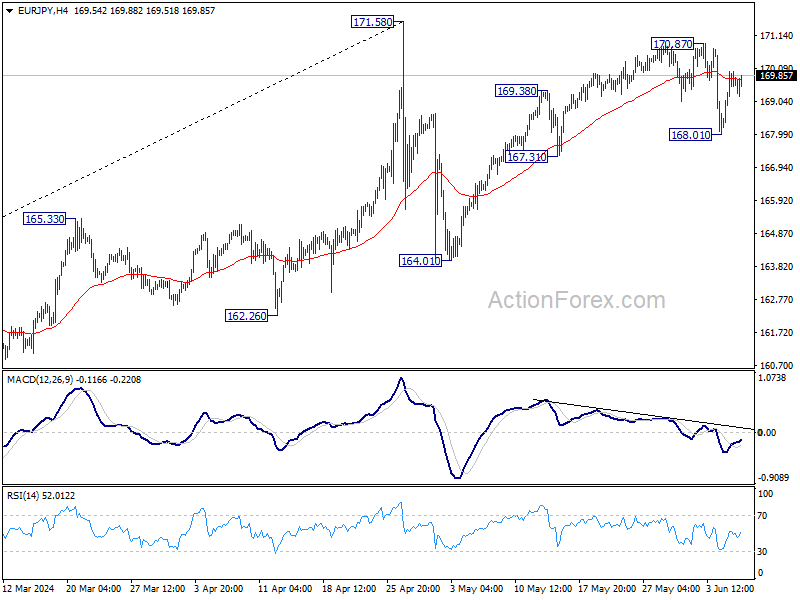

EUR/JPY Daily Outlook

Daily Pivots: (S1) 168.69; (P) 169.36; (R1) 170.35; More….

Intraday bias in EUR/JPY remains neutral for the moment. Current development suggests that rebound from 164.31 has completed at 170.81. Risk will now stay on the downside as long as 170.87 resistance holds. Below 168.01 will target 167.31 support first. Break there will target 164.01 support next.

In the bigger picture, a medium top was formed at 171.58 after brief breach of 169.96 (2008 high). But as long as 55 W EMA (now at 166.81) holds, price actions from there is seen as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

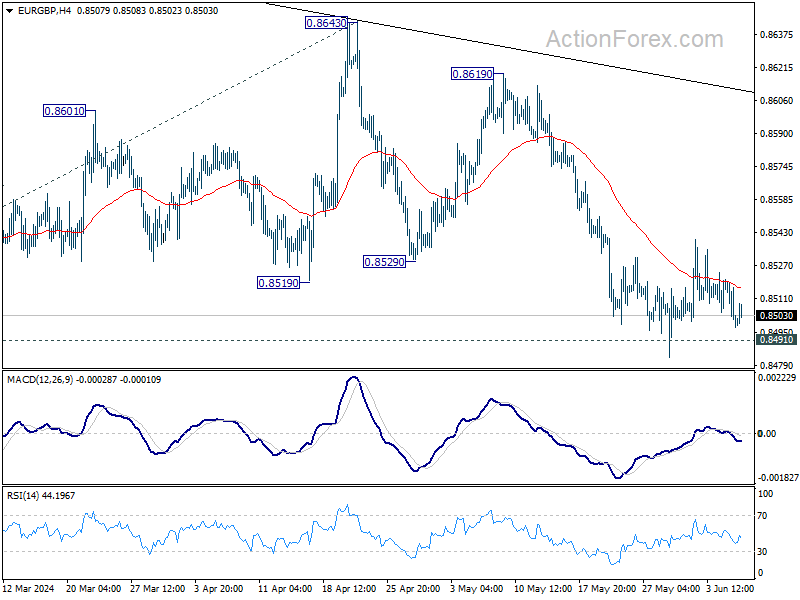

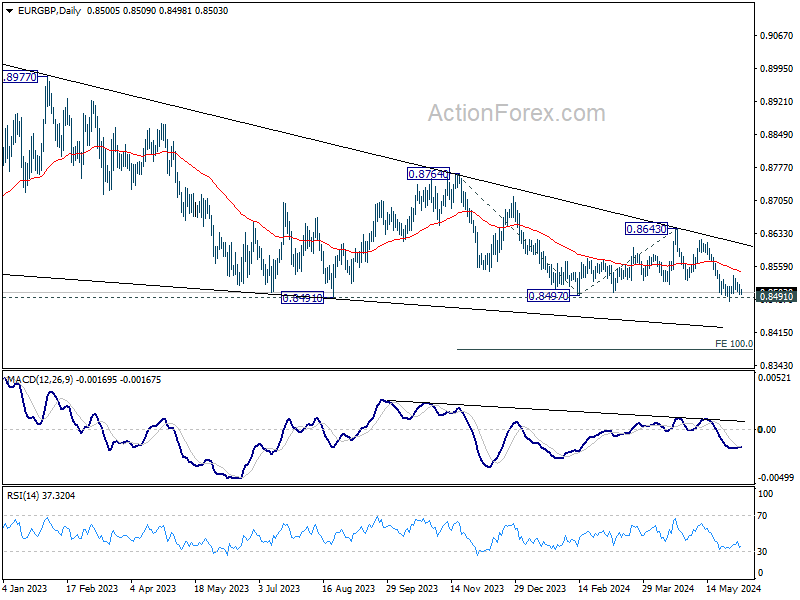

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8492; (P) 0.8507; (R1) 0.8515; More….

Intraday bias in EUR/GBP remains neutral and outlook is unchanged. Further decline is expected as long as 55 D EMA (now at 0.8547) holds. Decisive break of 0.8491/7 will resume larger down trend to 0.8376 projection level next. However, sustained break of 55 D EMA will turn bias back to the upside for 0.9643 resistance instead.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

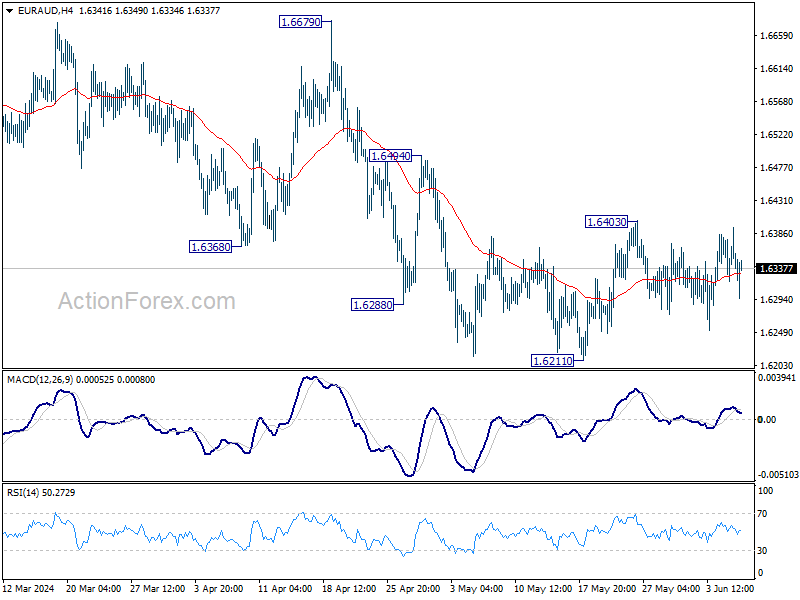

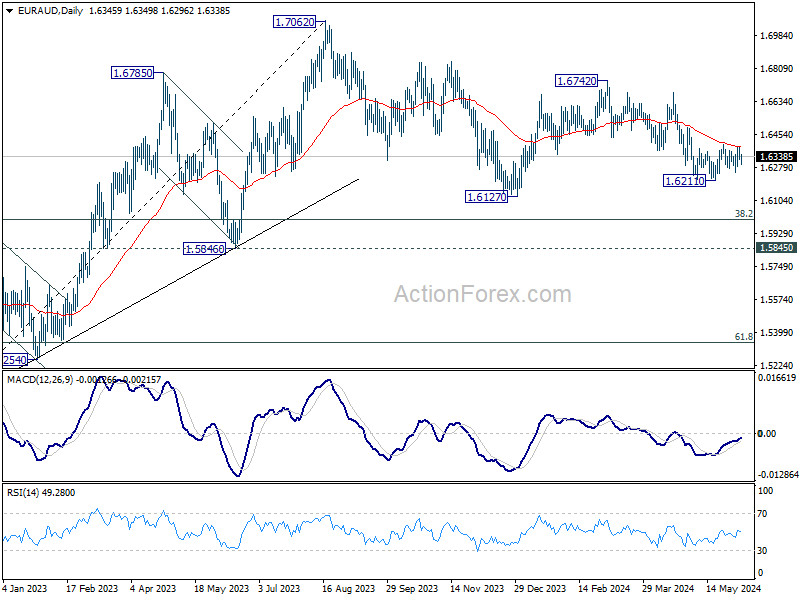

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6317; (P) 1.6356; (R1) 1.6391; More….

Intraday bias in EUR/AUD remains neutral as sideway trading continues. On the downside, firm break of 1.6211 support will resume the whole decline from 1.6742, as the third leg of the correction from 1.7062. On the upside, above 1.6403 will resume the rebound from 1.6211 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

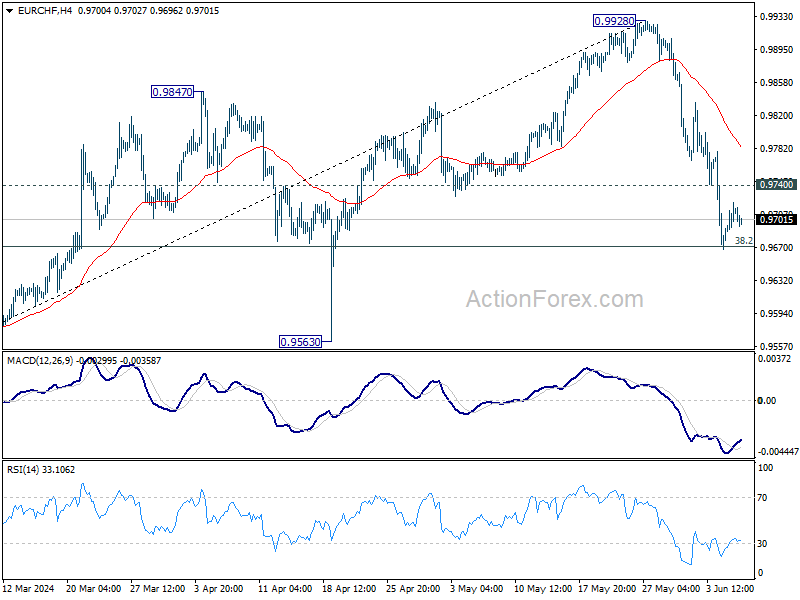

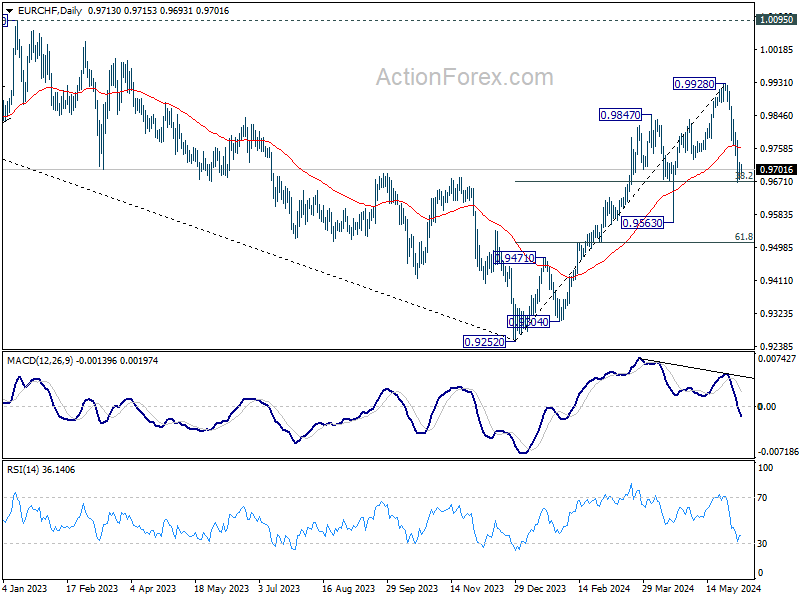

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9687; (P) 0.9704; (R1) 0.9729; More….

Intraday bias in EUR/CHF is turned neutral with 4H MACD crossed above signal line. Strong support is still expected from 38.2% retracement of 0.9252 to 0.9928 at 0.9670 to bring rebound. Break of 0.9740 minor resistance will turn intraday bias back to the upside. Nevertheless, sustained break of 0.9670 will bring deeper fall to 0.9563 support instead.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004.

Focus Turns to Europe and to ECB Today

Markets

Make it five. Five consecutive days of rallying US Treasuries on the (consequences of) the same theme: fading growth momentum and what it might mean to the Fed. At the front end of the curve, we’ve seen the obvious swing back from a first cut in December to the Fed pulling the trigger already in September. The US 2-yr yield lost 25 bps on a weekly basis. The long end of the curve outperformed, shedding up to 34 bps for the US 10-yr yield as real rates drove the move lower. The US 10-yr yield closed just below 4.31% support yesterday as the balance between a slightly below consensus ADP employment report (+152k vs +175k) and the Bank of Canada leaving the door open for follow-up action after their first rate cut this cycle on the one hand and a stronger-than-hoped for rebound in the services ISM (53.8 from 49.4 vs 51 expected) and bullish risk sentiment (WS up to +2% for Nasdaq) on the other hand, eventually fell in favour of the former. It’s telling about very short term bond market sentiment given broad-based strength in ISM subcomponents. Business activity surged (61.2) and new order growth accelerated (54.1), also for export orders (61.8). Firms still cut jobs, but at a slower pace (47.1). The prices paid component softened somewhat compared to April, but at 58.1 still suggests abundant inflationary pressures. Today is this week’s odd one out from a data point of view unless we see a significant surprise in Q1 (final) productivity and labor cost data. Tomorrow, May payrolls have the final say.

Focus turns to Europe and to the ECB today. They’ll join the Bank of Canada in making monetary policy less restrictive with a well-flagged 25 bps rate cut for all policy rates. The bigger question remains whether the central bank commits to any guidance for the following meetings, something they refused to do so far. Back in March when presenting their new operational framework, they did already flag to narrow the corridor between the main refinancing rate and the deposit rate from currently 50 bps to 15 bps. The penalty rate (MLF) will remain 25 bps above the MRO. Sticky Q1 wage growth, the bumpy inflation path ahead, recovering economic growth, and the Fed’s reaction function all suggest limited scope for genuine follow-up rate cuts. We nevertheless think that the ECB will keep the option open and that the market will anticipate. Current market pricing (2.5 rate cuts discounted for this year) seems prone for a dovish repositioning at the front end of the curve in a steepening move. This should keep EUR/USD below 1.09 resistance and will trigger (at least) a test of EUR/GBP 0.85 support.

News & Views

The National Bank of Poland (NBP) left its main policy rate unchanged at 5.75% yesterday. Headline inflation printed at 2.5% in May, exactly touching the NBP’s inflation target. Core inflation (4.1% in April) is also expected to have decreased further. A further decline in producer prices (-8.6% Y/Y in April) confirms the fading of most external supply shocks and a reduction of cost pressures. Together with relatively low economic growth, it limits inflation. The strong zloty also helps. The NBP expects that Q2 annual CPI growth will run consistent with the its inflation target. Core CPI is also seen declining further, but due to elevated services inflation, it will stay above the headline inflation. Despite current favorable inflation developments, the NBP continues to see a high degree of uncertainty for inflation beyond Q2 related to the impact of fiscal and regulatory price policies which might also affect inflation expectations. Higher domestic demand due to rising wages is mentioned as a potential factor for higher inflation in H2 as well. Governor Glapinski will comment the policy decision in a press conference later today.

The Bank of Canada (BoC) cut its policy rate by 25 bps to 4.75%. The Canadian economy returned to growth (1.7%) in Q1, but this was softer than the BOC expected even as consumption was solid. Wage pressures remain but look to be moderating gradually. Overall, recent data suggest the economy is still operating in excess supply. CPI inflation eased to 2.7%. Core inflation also slowed and is expected to hold a downward momentum. The Governing Council agreed that monetary policy no longer needs to be as restrictive as it was. Going forward governor Macklem indicated that "If inflation continues to ease, and our confidence that inflation is headed sustainably to the 2% target continues to increase, it is reasonable to expect further cuts to our policy interest rate," Macklem admitted that there are limits to how far the BoC can diverge from the US, but that they are not close to those limits yet.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a June rate cut which has broad backing. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. The German 10y yield set a new YtD top at 2.7% before following the US correction lower on growth worries

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed Chair Powell indicated that further tightening was unlikely. However, the FOMC Minutes still showed internal debate on whether policy is restrictive enough. Sticky inflation suggests any rate cut will be a tough balancing act while several policy makers hint at a higher neutral rate. The US 10-y yield is correcting lower in the 4.3/4.7% trading range.

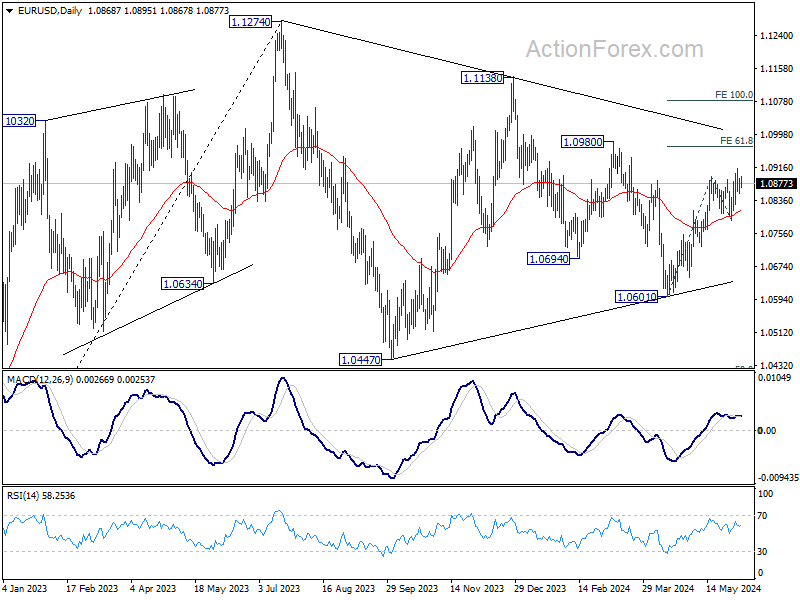

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.06/1.09 area might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. We expect this important support level to hold.

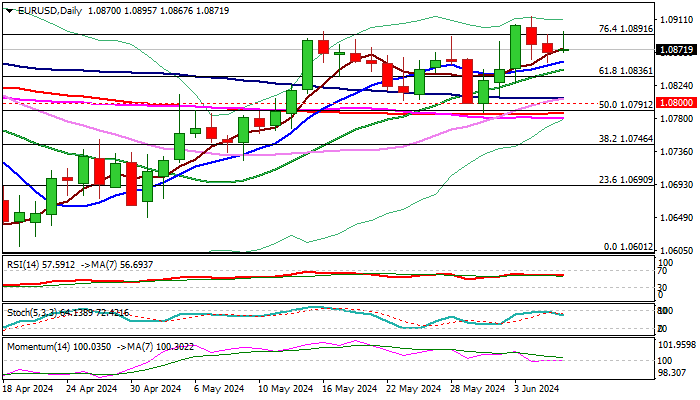

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0851; (P) 1.0872; (R1) 1.0889; More…

Range trading continues in EUR/USD and intraday bias stays neutral at this point. Further rally is expected as long as 1.0788 support holds. Break of 1.0915 will resume the rally from 1.0601 to 61.8% projection of 1.0601 to 1.0894 from 1.0788 at 1.0969. However, firm break of 1.0788 will turn bias back to the downside for deeper decline instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0788 support will extend the corrective pattern instead.

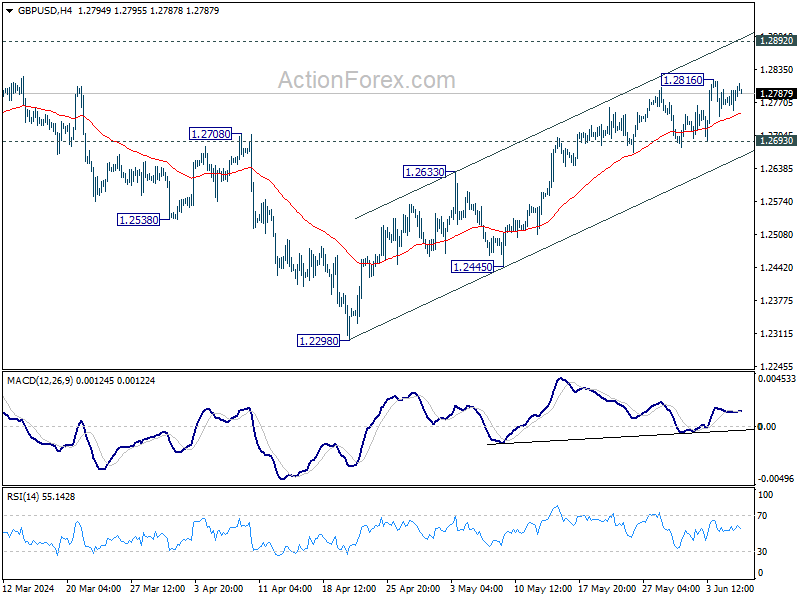

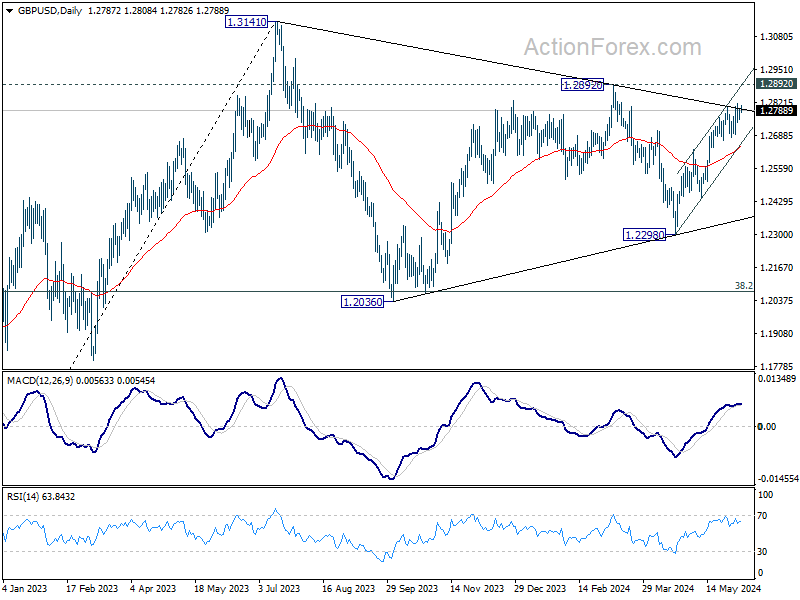

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2763; (P) 1.2779; (R1) 1.2803; More…..

Intraday bias in GBP/USD remains neutral at this point. As long as 1.2693 support holds, further rally is in favor. Above 1.2816 will resume the rally from 1.2298 to 1.2892 resistance next. On the downside, break of 1.2693 minor support will turn intraday bias to the downside for deeper pullback instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

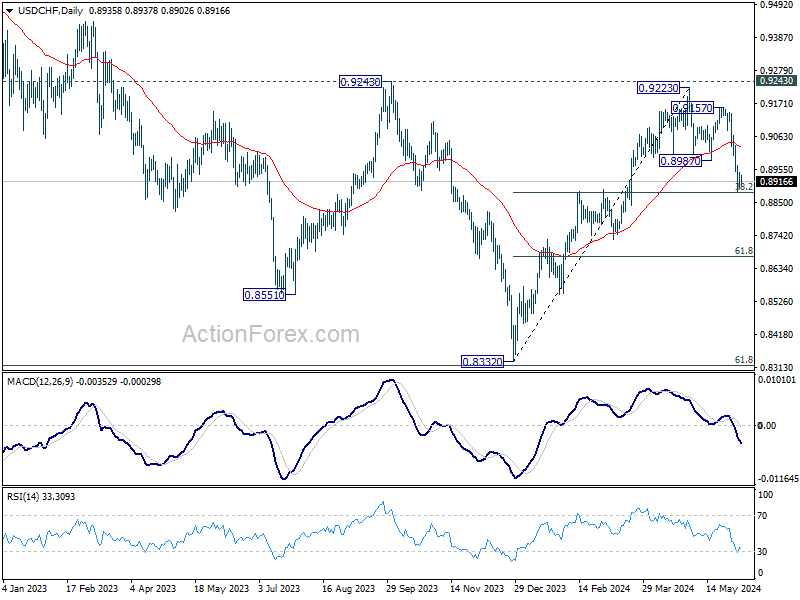

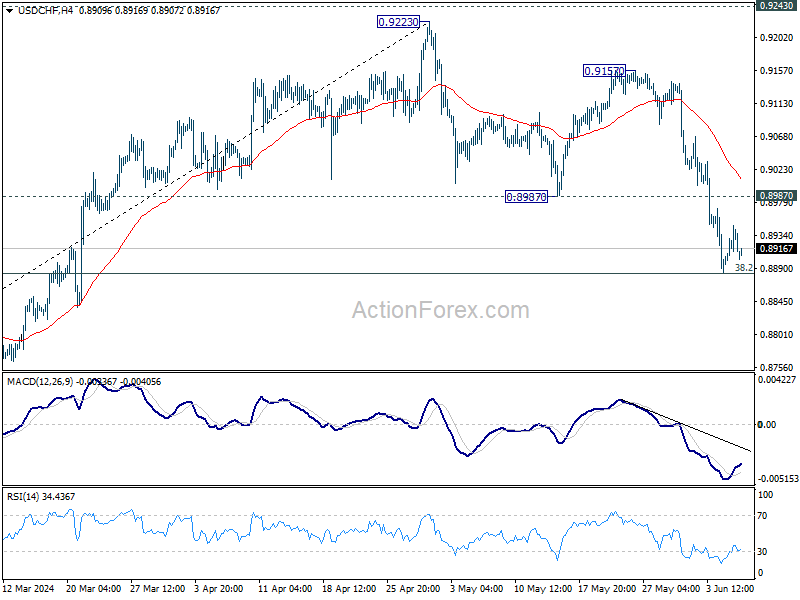

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8901; (P) 0.8925; (R1) 0.8959; More….

Intraday bias in USD/CHF remains neutral for the moment. Strong rebound from current level, followed by break of 0.8987 support turned resistance, will suggest that correction from 0.9223 has completed, and retain near term bullishness. However, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.