Sample Category Title

Cliff Notes: Travelling a Bumpy Road with Confidence

Key insights from the week that was.

Australian Q1 GDP printed broadly as expected, rising 0.1% (1.1%yr). There were some surprises for consumption however, a firmer-than-anticipated gain of 0.4% in Q1 – thanks in part to major events like Taylor Swift Era’s Tour and the Formula 1 – and an upward revision to tourism-related spending by Australians abroad, adding $22bn to nominal spending over the past five quarters and 1.0ppt to annual consumption growth. These revisions also appeared as a lift in services imports, and consequently had zero net impact on GDP. In this week’s essay, Chief Economist Luci Ellis explains why these revisions are not a concern for future inflation.

Even with these revisions, Australian per capita consumption is still down 1.1% over the year to March 2024, broadly in line with the experiences of peer economies, excluding the US. Additionally, inflation’s impact on household earnings was material, enough to leave real disposable income flat over Q1 and up just 0.4% versus March 2023. The financial health of Australian consumers is set to remain fragile. The Stage 3 tax cuts and the recently announced 3.75% increase in the minimum wage and awards will provide some relief, but the cumulative impact of elevated inflation will linger.

Other parts of the domestic economy were soft too. The main detractor from domestic demand was new business investment, –0.7% in Q1 as weakness in non-dwelling construction (–4.3%) and infrastructure (–4.8%) outweighed the lift in equipment spending (+2.0%). Housing investment also remains in a downtrend (–3.4%yr). That private demand was near-flat in the quarter (+0.1%) highlights the breadth of current economic weakness, with only the public sector in robust health, up 0.6% and 4.5%yr.

On trade, Australia’s current account balance slid from a surplus of $2.7bn in Q4 to a deficit of –$4.9bn in Q1. As noted earlier, significant revisions to tourism-related services imports were the chief culprit. Accounting for that, the scale of the reduction in the balance between Q4 and Q1 (–$7.6bn) was in line with expectations. Strength in import volumes (+5.1%) was met with only a modest increase in exports (+0.7%), leading net exports to detract a material 0.9ppts from GDP in Q1. The latest data on monthly goods trade suggests a partial unwind of recent import strength is underway in Q2, at least for goods.

Before moving offshore, a final note on housing. The latest data from CoreLogic highlighted a growing divergence by capital city. On a three-month annualised basis, house price growth ranged from –0.9% in Melbourne to 5.0% in Sydney and 17%, 18% and 27% respectively in Brisbane, Adelaide and Perth. It was therefore unsurprising to see housing finance approvals continue to surge in April, up 4.8% (25%yr), as investor activity soared to new heights across the aforementioned smaller capitals. The diversity of conditions across the states will continue to have a significant bearing on nation-wide outcomes. For more housing insights, see our latest Housing Pulse published earlier this week on Westpac IQ.

Offshore, the Bank of Canada cut its policy rate by 25bps to 4.75% at their June meeting. The decision came as the Bank became more confident that inflation will sustainably return to 2%, with inflation’s breadth narrowing to near its “historical average” and wage pressures easing. Wages and housing inflation will remain key determinants of CPI inflation hence. Canada’s labour market is slowing, and supply is sufficient for new demand, allowing wage and services inflation to cool. When questioned about policy divergence with the US, both the Governor and Senior Deputy Governor held that their decisions are based on domestic factors and that, while there are limits to how much Canada can deviate from the US without material implications for the currency, those limits are some way off. Still, the Governing Council remain mindful of residual inflation risks, and so policy is not on a pre-set course. If the economy evolves as expected, further rate cuts will come in time. Updates for GDP and the labour market will be released prior to the Council’s July meeting.

The ECB subsequently cut their policy rates by 25bps at the June meeting, as expected, having kept rates at peak levels for nine months. Over that period, inflation has decelerated 2.5ppts, and President Lagarde made clear that the Council have also become more confident in returning inflation to target in the medium term with inflation expectations having declined "at all horizons". Interestingly, this decision was made and guidance given despite an upward revision to the inflation outlook, headline inflation now seen averaging 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026. The persistence of above-target inflation is a result of domestic inflation, supported by elevated wage growth. The ECB see this wage growth as "making up for the past inflation surge" and believe that wage momentum and services inflation will take time to moderate. However, forward looking wage indicators and profits absorbing some of the "pronounced rise in unit labour costs" give the Council confidence that the deceleration is ongoing and catch-up wage growth will have a limited impact on consumer inflation hence.

The ECB's GDP forecasts point to similar confidence in a return to potential growth, GDP growth to accelerate from 0.9% in 2024, to 1.4% in 2025 and 1.6% in 2026. President Lagarde made clear however that there is an array of risks facing the economy which will need to be assessed carefully. Although GDP growth was robust in Q1 at 0.3% and the unemployment rate is historically low, the downside surprise in April retail sales (-0.5%, 0.0%yr) provides evidence of consumer uncertainty. The restrictive nature of credit conditions also need to be monitored closely. The ECB will maintain a ‘data dependent’ approach to setting policy, taking their time with further easing. But, being a long way from neutral, having had success with inflation and given the immediate uncertainty surrounding economic growth, a series of rate cuts should be expected through 2024 and 2025 – Westpac forecasts a cumulative 150bps (including today's decision) to end 2025.

Over in the US, the ISM manufacturing PMI surprised to the downside, falling from 49.2 to 48.7 points. New orders jolted lower despite a gain for export orders, pointing to weak domestic demand. Employment gained in the month but is currently only around average levels, while price pressures were reported as benign. The non-manufacturing PMI meanwhile rose 4.4 points to 53.8, supported by a rebound in business activity and new export orders. Price pressures for services were also assessed as benign. Of concern for activity however, the services employment index remained materially below its historic average, pointing to outright job losses. In contrast, the JOLTS survey provided a benign signal for the employment outlook, with job ads slowly converging to their pre-pandemic level, the job opening rate now 4.8% versus 4.5% in 2018 and 2019, and the hiring and separation rates consistent with moderate gains for employment and limited churn. Overall, these data points signal the FOMC have time on their side when assessing policy, but also that downside risks to activity are building. A measured pace of rate cuts from September through 2025 to 3.375% at mid-2026 should manage these concerns and achieve inflation near target over the period. The FOMC’s own view on the outlook will be made clear through next week’s June update to Committee forecasts and Chair Powell’s post-meeting press conference.

USD/JPY Could Soon Rally, US NFP Report Next

Key Highlights

- USD/JPY is eyeing an upside break above the 156.40 resistance.

- A major bearish trend line is forming with resistance at 156.60 on the 4-hour chart.

- EUR/USD is gaining pace above the 1.0880 resistance.

- Gold prices recovered above the $2,350 resistance zone.

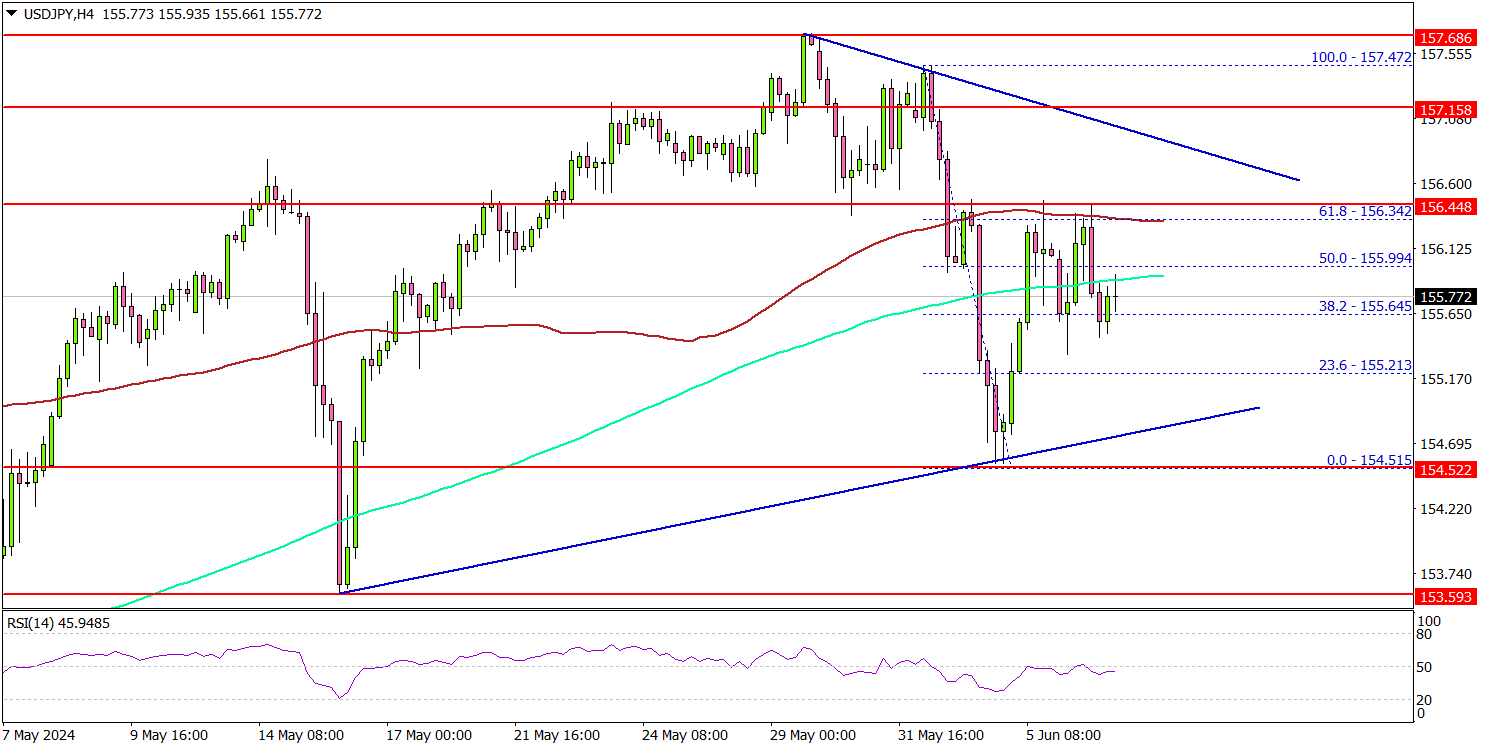

USD/JPY Technical Analysis

The US Dollar remained well- supported above the 154.50 level against the Japanese Yen. USD/JPY formed a base and started a fresh increase above 155.00.

Looking at the 4-hour chart, the pair was able to clear the 155.80 and 156.00 resistance levels. However, the bears are currently active near the 100 simple moving average (red, 4-hour). The pair is now consolidating near the 200 simple moving average (green, 4-hour).

Immediate support is near the 155.20 level. The next major support is near the 155.00 zone. A downside break and close below the 155.00 support zone could open the doors for a larger decline. In the stated case, the pair could decline toward the 154.20 level.

On the upside, immediate resistance is near the 155.20 zone. The first major resistance is near the 155.40 level. There is also a major bearish trend line forming with resistance at 156.60 on the same chart.

A clear move above the 155.60 resistance might send it toward the 157.20 level. Any more gains might call for a move toward the 158.00 level in the near term.

Looking at EUR/USD, the pair is showing bullish signs, and the bulls might soon aim for a move toward the 1.0950 level in the near term.

Economic Releases

- US nonfarm payrolls for May 2024 – Forecast 185K, versus 175K previous.

- US Unemployment Rate for May 2024 - Forecast 3.9%, versus 3.9% previous.

Attention Shifts to US NFP as Dollar Index Seeks Fresh Momentum

As the week draws to a close, market attention is squarely on the upcoming US non-farm payroll employment report. The sluggish Dollar is in need of a catalyst from the jobs report to spark a meaningful and sustainable breakout from its recent range against major currencies.

Market expectations are set for NFP to show 180k growth o May, with the unemployment rate steady at 3.9%. Average hourly earnings are expected to increase by 0.3% mom.

Recent related economic data offers mixed signals. ISM Services employment index rose from 45.9 to 47.1, but still indicating contraction. Conversely, ISM Manufacturing employment index turned to expansion, rising from 48.6 to 51.1. ADP private employment showed a growth of only 152k. Additionally, the four-week moving average of initial jobless claims rose from 210k to 222k, suggesting some softening in the labor market.

While there may be some upside surprises in headline job growth, it is unlikely to significantly exceed expectations. The critical variable remains wage growth, which is essential for gauging underlying domestic inflation pressures, and an important factor influencing the timing of Fed's first rate cut.

Dollar index dipped to 103.99 this week but struggled to find decisive selling momentum. Further decline is still in favor as long as 105.18 resistance holds. Fall from 106.51 is seen as developing into the third leg of the pattern from 107.34. Any downside acceleration could push DXY through 102.35 support towards 100.61.

However, strong bounce from current level followed by break of 105.18 will revive near term bullishness. Rise from 100.61 would then be ready to resume through 106.51 before reversing.

NFP: Markets Consolidate Ahead of Big News

Analysts are predicting a softer May Non-Farm Payroll (NFP) report, with expectations set at 151,000 new jobs, down from 175,000 in the previous month. This conservative forecast follows a recent trend of underestimating the US job market's strength, with the previous miss restoring analysts' confidence in issuing more cautious projections. If the actual NFP figures surpass this modest expectation, it could positively impact the markets. Generally, an NFP above 180,000 is seen as bullish, so meeting the forecast would indicate a slowing but still growing labor market. While the pace of job creation may be decelerating, the expected figures are not indicative of a significant downturn.

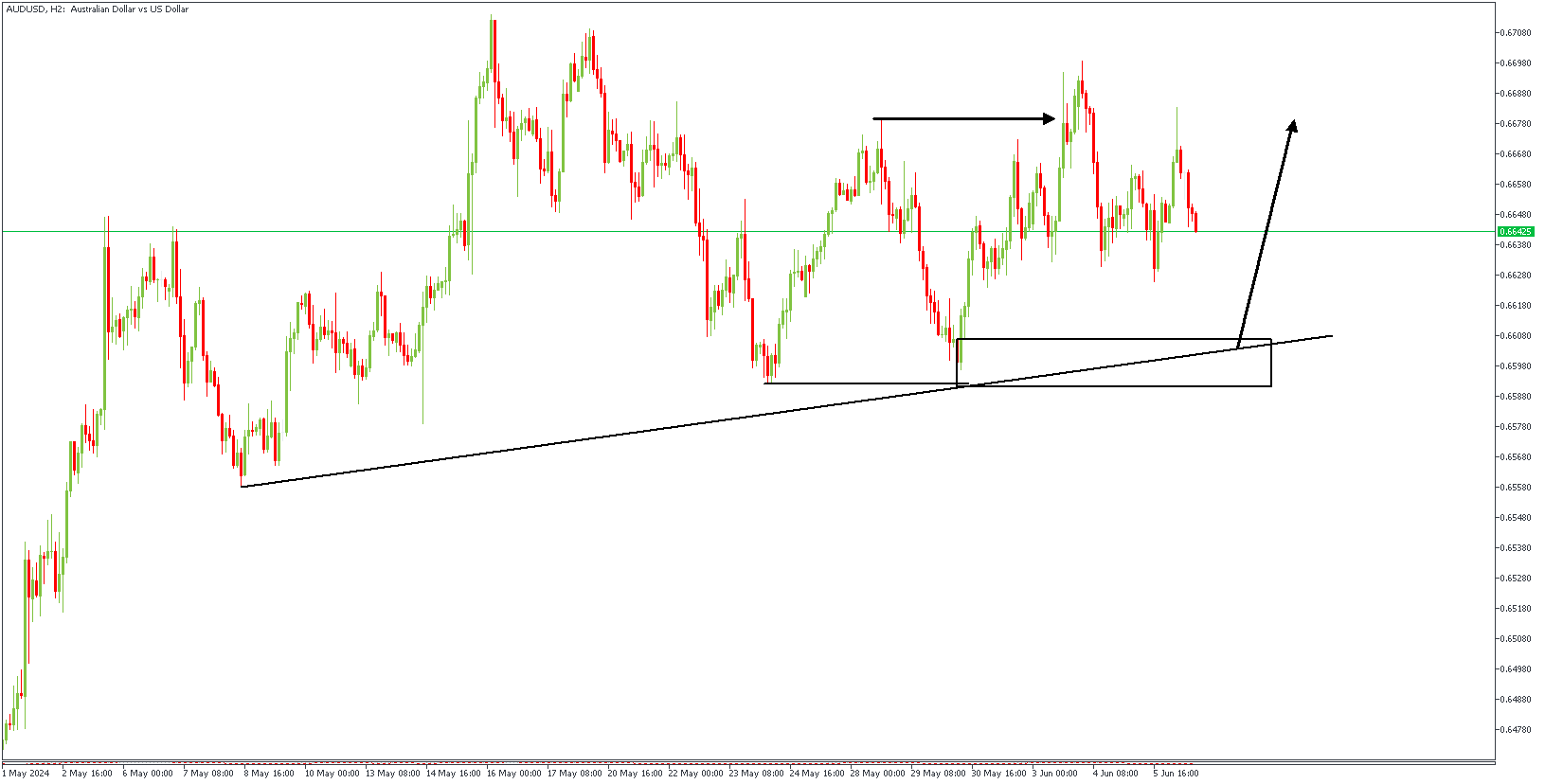

AUDUSD – H2 Timeframe

AUDUSD on the 2-hour timeframe is gradually sliding towards an area of demand that aligns with the demand zone from a previous low that raided liquidity. The previous swing high has also been broken and exceeded, creating a break of structure. The trendline support is expected to complement the bullish pressure, and serving as a confluence to the bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 0.66840

- Invalidation: 0.65848

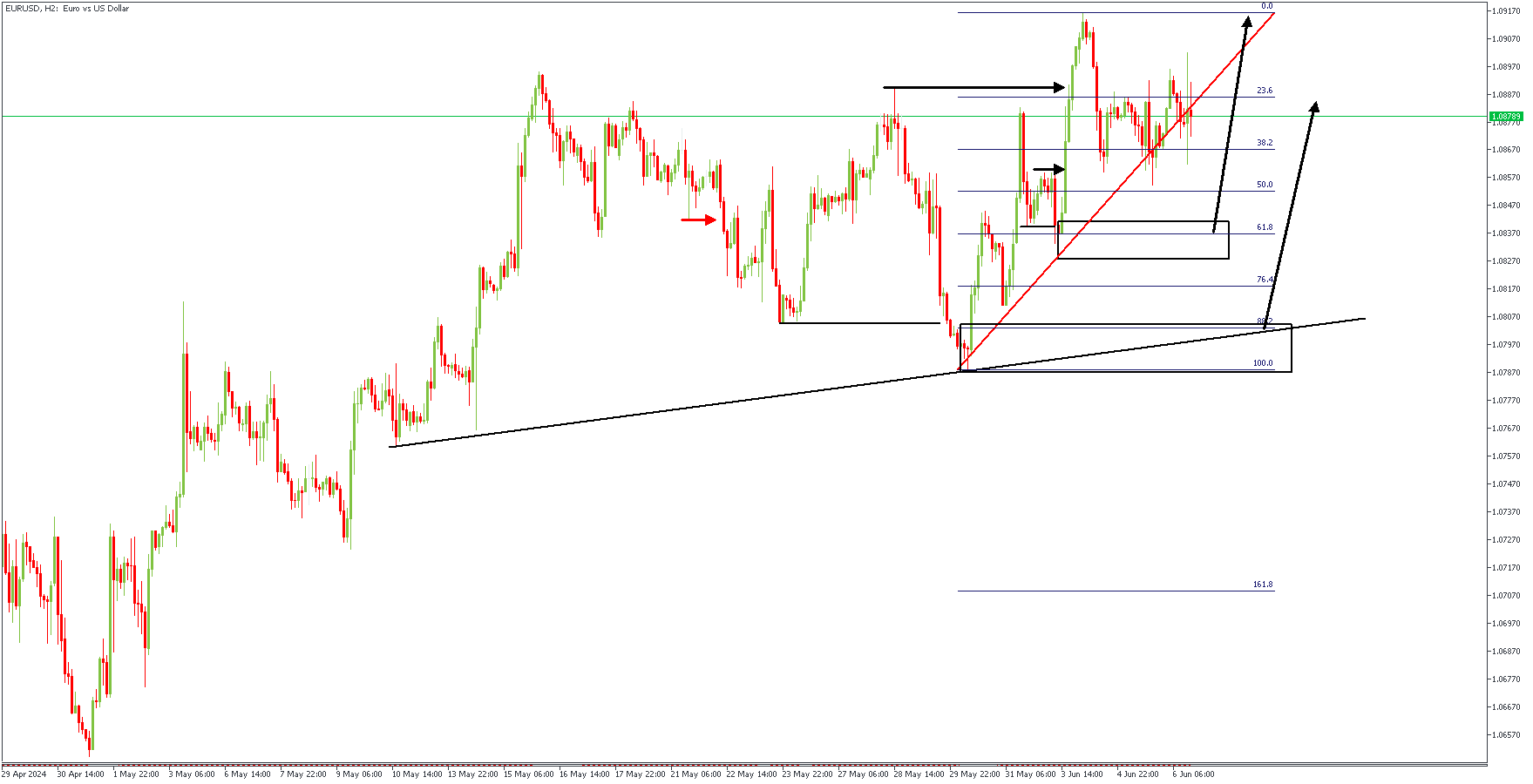

EURUSD – H2 Timeframe

On the 2-hour timeframe chart of EURUSD, we can see a clear sweep of the previous low, followed by the bullish break of structure (which I believe you should be familiar with now as a QMR pattern). The 88% of the Fibonacci retracement tool, the drop-base-rally demand zone, and the trendline support are my confluences in favour of a bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.09158

- Invalidation: 1.08162

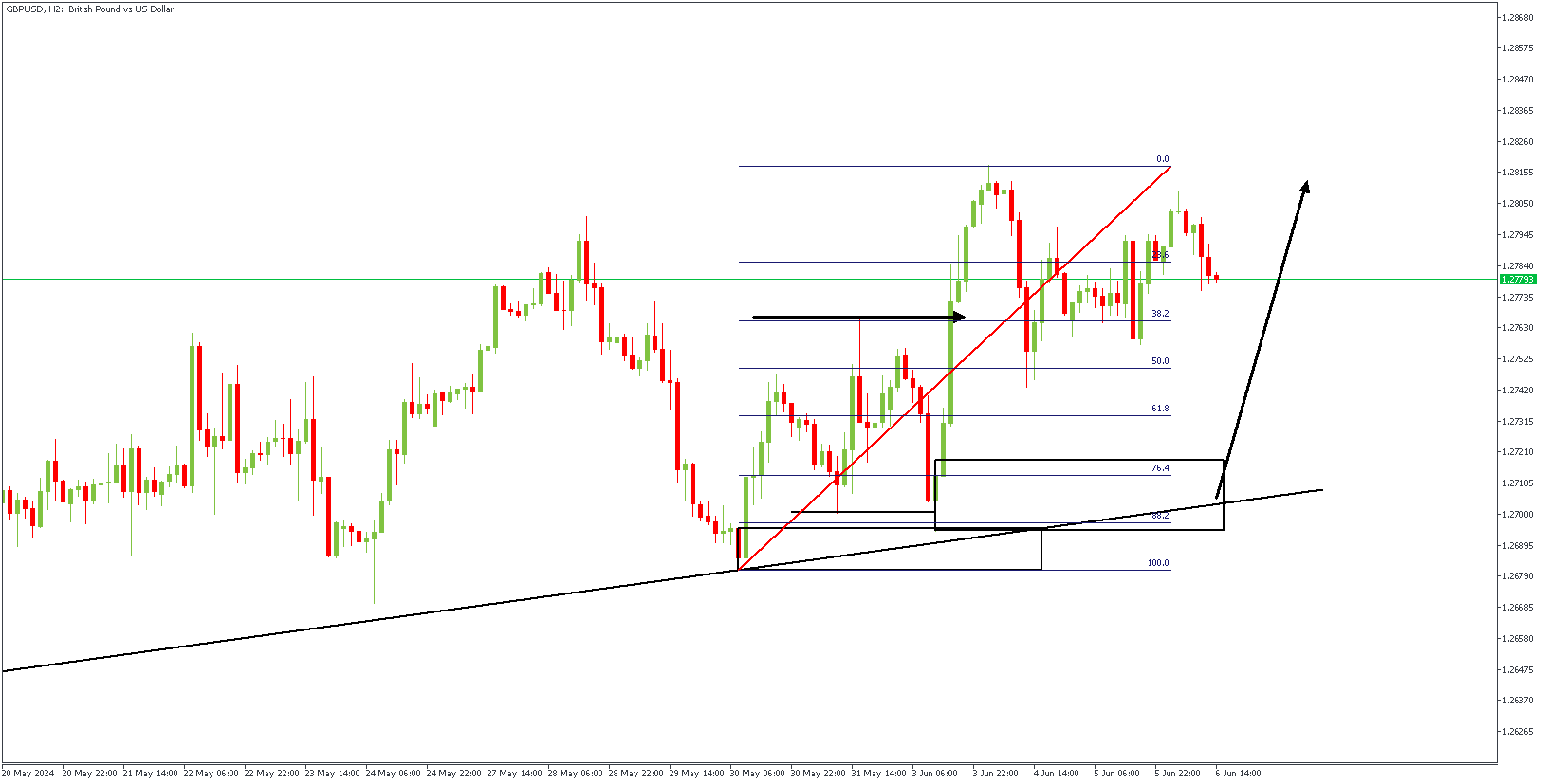

GBPUSD – H2 Timeframe

Quite similar to what we had on EURUSD, we can see GBPUSD on the 2-hour timeframe also printing a clear QMR pattern, however, this time with an added confirmation from the demand zone that birthed the reaction. Following the break above the previous swing high, I expect to see price retrace into the 88% of the Fibonacci, and thereafter pump higher. The trendline support can be considered the final piece of the puzzle that puts the bullish sentiment altogether.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.28093

- Invalidation: 1.26786

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

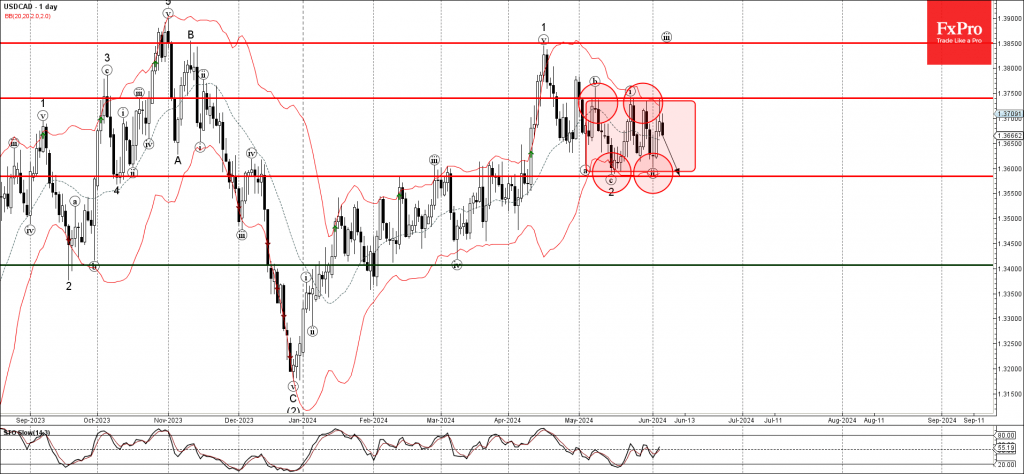

USDCAD Wave Analysis

- USDCAD reversed from resistance level 1.3740

- Likely to fall to support level 1.3600

USDCAD currency pair recently reversed down from the key resistance level 1.3740 (upper boundary of the narrow sideways price range inside which the pair has been moving from the start of May).

The resistance level 1.3740 was strengthened by the upper daily Bollinger Band – which created the daily Shooting Star.

Given the strength of the resistance level 1.3740, USDCAD currency pair be expected to fall further to the next support level 1.3600, lower boundary of this sideways price range.

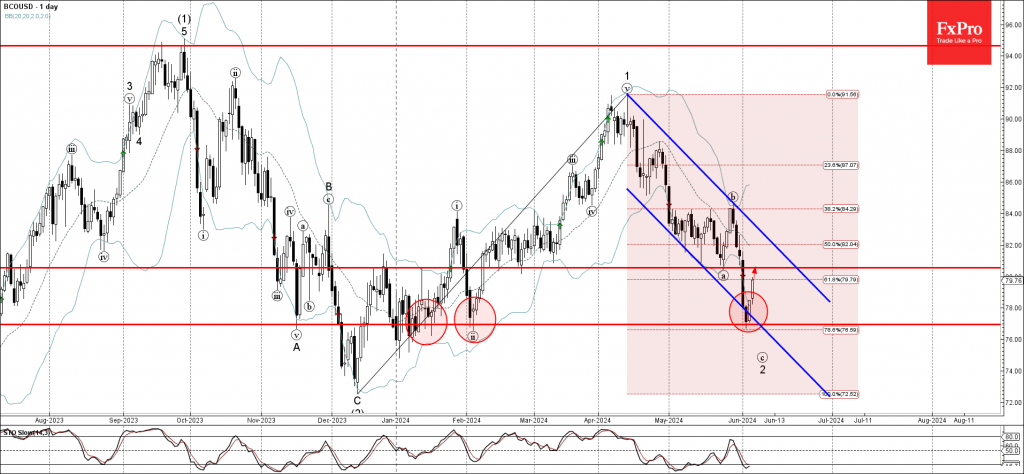

Brent Crude Oil Wave Analysis

- Brent Crude oil reversed from support level 76.95

- Likely to rise to resistance level 80.55

Brent Crude oil recently reversed up from the key support level 76.95 (which has been repeatedly reversing the price from the start of this year).

The support level 76.95 was strengthened by the lower daily Bollinger Band and by the support trendline of the daily down channel from April.

Given the strength of the support level 76.95 and the oversold daily Stochastic, Brent Crude oil be expected to rise further to the next resistance level 80.55, former low of wave a from the end of May.

US Dollar Index Needs to Hold Above 104

- US dollar index pauses downleg near important support trendline

- Technical signals are uncertain; sellers wait below 104

The US dollar index is trading at an attractive level around the protective trendline that joins the lows from December 2023 and March 2024 near 104.00. The index could enter a new bullish phase, though the technical outlook cannot guarantee an immediate rebound.

Although the stochastic oscillator is near its 20 oversold level, the RSI keeps fluctuating below its 50 neutral mark and the MACD remains negatively charged below its red signal line. The price itself has yet to climb above its simple moving averages (SMAs,) adding to the negative risks.

A step below the 104.00 round level is expected to trigger the next bearish action, squeezing the price towards the 103.60 constraining territory. A continuation lower could stabilize around May’s support line at 103.18, while the 23.6% Fibonacci retracement of the September 2022-July 2023 downtrend could tackle steeper declines along with the long-term descending line drawn from September 2022 at 102.70.

Alternatively, the bulls might attempt to climb above the restrictive 20-day SMA at 104.54. The tentative descending trendline from May’s peak could limit bullish actions ahead of the 38.2% Fibonacci mark of 105.12. If the rally continues, the spotlight will fall on the 105.50 area.

Overall, despite the discouraging technical signals, the US dollar index might have another opportunity to rotate higher if the 104.00 floor holds.

ECB Review: Cutting and Keeping

Today, the ECB decided to cut its three main policy rates by 25bp, which leaves the key policy rate at 3.75%. This cut follows a 9-month period with unchanged policy rates on the back of the rapid hiking cycle since mid-2022. The rate cut was widely expected and thus focus was on the communication.

The updated staff projections showed inflation to hit 2% one quarter later (Q4 25) than at the time of the March meeting.

With the rate cut fully anticipated, some initial volatility was quickly replaced with markets trading in a tight range, with no commitment on the timing of the next policy rate cut, although the meeting with staff projections (September, December, March, and June) seems preferable with a lot more information provided.

We continue to look for the next policy rate cut in December in our baseline scenario, although we do not rule out a potential rate cut in September.

Acknowledging the progress – not confirming the dialling back phase

The ECB’s decision to cut rates was widely expected by market participants and did not come as a surprise. The decision itself was agreed by most GC members, except one member (Reuters sources reported this to be Holzmann). The staff projections showed an upward revision of growth and inflation this year with a direct reference to inflation still above 2% next year. Coupled with guidance of “keeping” the policy rates restrictive to bring inflation to the target, we maintain our call for the next policy rate cut to occur in December, contrary to market pricing and consensus among analysts who expect a September rate cut.

As discussed in COTW: staying restrictive - not yet entering the dialling back phase, we did not expect Lagarde to confirm that they have entered the dialling back phase, which in our reading would be a commitment to a string of policy rate cuts. When asked about it, she did ‘volunteer’ that we have entered the dialling back phase, although she pointed to a “strong likelihood” of this being the dialling back phase, but she would not confirm this. To us this means that the ECB does not want to pre-commit to a specific meeting or policy rate path. The ECB kept its meeting-by-meeting and data-dependent approach for its threetiered reaction function (inflation outlook, underlying inflation, and strength of the monetary policy). Markets are now pricing an additional 36bp of rate cuts by year-end (on top of today’s rate cut, which takes effect on Wednesday next week).

Staff projections show higher inflation and growth

The ECB expects the economy to continue its recovery as the manufacturing sector stabilises, exports pick up, and monetary policy will exert less of a drag on activity. The updated staff projections show higher inflation both this year and next year due to the persistent pressure from domestic inflation and elevated wage growth. HICP is now expected to average 2.5% in 2024 and 2.2% in 2025, which is 0.2pp. higher than the March projections in both years. Likewise, expectations for core inflation were revised up to 2.8% in 2024 and 2.2% next year from 2.6% and 2.1%, respectively. Lagarde noted that inflation will fluctuate around the current levels for the rest of the year before settling towards the 2% target next year.

The sticky expected inflation outlook is largely driven by the elevated wage growth. The ECB staff expect wage growth of 4.8% this year (previously 4.5%), 3.5% in 2025 (previously 3.6%), and 3.2% in 2026 (previously 3.0%). Lagarde noted that wages will remain elevated, but this is largely due to catching up with previous inflation, while the forward-looking wage tracker shows declining wage pressures. Rising economic activity also adds to inflationary pressures. The GDP growth expectation for 2024 was increased to 0.9% y/y from 0.6%, reflecting stronger-than-expected growth in Q1, as well as marginally higher future growth expectations. The ECB now sees balanced risks to the growth outlook in the short-term, which are changed from downside in March, while all expectations for 2026 were unchanged (see chart).

European Central Bank Kicks Off Its Rate Cut Cycle

Summary

- The European Central Bank (ECB) today joined the growing group of advanced economy central banks that have begun their monetary easing cycles, lowering its Deposit Rate by 25 bps to 3.75%.

- ECB policymakers cited the past drop of inflation and the improving inflation outlook as key factors behind their decision to lower interest rates. There were some elements of caution, however, as the ECB said domestic price pressures remain strong as wage growth is elevated, and revised up its near-term inflation forecasts.

- We view the ECB's statement as consistent with further rate cuts, albeit at a measured pace. The ECB said it will continue to follow a “data-dependent and meeting-by-meeting approach” in determining its interest rate decisions.

- Over the rest of 2024, our base case is for the ECB to pause in July before cutting rates again in September, October and December. However, we suspect ECB policymakers would prefer to see a return to an overall downward trend in wage growth and domestic inflation to be fully comfortable in lowering interest rates further, and thus view the risks as tilted toward lesser easing.

European Central Bank Kicks Off Its Rate Cut Cycle

The European Central Bank (ECB) today joined the growing group of advanced economy central banks (including the Swiss National Bank, Riksbank and Bank of Canada) that have begun their respective monetary policy easing cycles. The ECB lowered its benchmark interest rates by 25 bps, bringing its Deposit Rate to 3.75%, and offered several perspectives in support of its decision to ease monetary policy, saying:

- Inflation has fallen more than 2.5 percentage points since September 2023 (when the policy rate reached its peak), and the inflation outlook has improved markedly.

- Underlying inflation has also eased, and inflation expectations have declined at all horizons.

- Monetary policy has kept financing conditions restrictive. By dampening demand and keeping inflation expectations well anchored, this has made a major contribution to bringing inflation back down.

While clearly acknowledging the improving inflation situation, the ECB's announcement was balanced by some cautious and hawkish elements, saying domestic price pressures remain strong as wage growth is elevated, and that inflation is likely to stay above target well into next year. Indeed, near-term core inflation projections (CPI excluding food and energy) have been revised higher to 2.8% for 2024 (previously 2.6%) and to 2.2% for 2025 (previously 2.1%). The core inflation forecast for 2026 was unchanged at 2.0%. The ECB also raised its GDP growth forecast for 2024 to 0.9%, from 0.6% previously.

In terms of policy guidance, we view the ECB's statement as consistent with further rate cuts, albeit at a measured pace. The ECB said it will “keep policy rates sufficiently restrictive for as long as necessary to achieve” a timely return to the 2% inflation target. Use of “sufficiently” restrictive does, in our view, allow for some further reduction in interest rates given their currently elevated levels. The ECB added however that it “will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction.” Finally, the ECB said it is not committing to a particular rate path.

Today's interest rate reduction was clearly signaled ahead of time by ECB policymakers and widely forecast, including by ourselves. Going forward, we have also forecast the ECB will hold rates steady in July before delivering another 25 bps rate cut in September. By the fourth quarter we expect Eurozone wage growth and underlying inflation may have slowed sufficiently for the ECB to deliver rate cuts at its October and December meetings, especially if the Federal Reserve begins lowering interest rates as well. If realized, that would see the Deposit rate lowered by a cumulative 100 bps this year to end 2024 at 3.00%.

We view today's announcement as very much consistent with the ECB keeping interest rates unchanged at its July meeting, while the optionality embodied in today's statement would allow for a resumption of rate cuts in September. That said, we view the risks around our ECB easing outlook for this year as tilted toward a lesser 75 bps of rate cuts, compared to our base case for a cumulative 100 bps of rate reduction. ECB policymakers are likely wary of the modest uptick in Eurozone wage growth reported for Q1, and the uptick of core inflation and particularly services inflation in May. Over the next few months ahead of the ECB's 12 September monetary policy announcement we will get CPI inflation data for June, July and August, and both the Q2 Indicator of Negotiated Wages along with Q2 compensation per employee (the most comprehensive wage measure) will be available in time for the September meeting. We suspect ECB policymakers would prefer to see a return to an overall downward trend in wage growth and domestic inflation to be fully comfortable in lowering interest rates further. Against that backdrop, a further interruption to the disinflation progress could put one of our expected September or October rate cuts at risk.