Sample Category Title

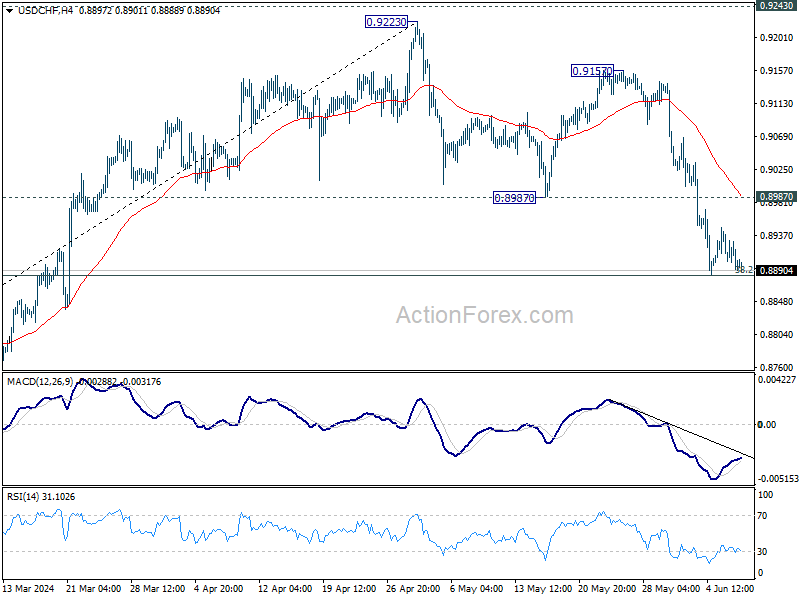

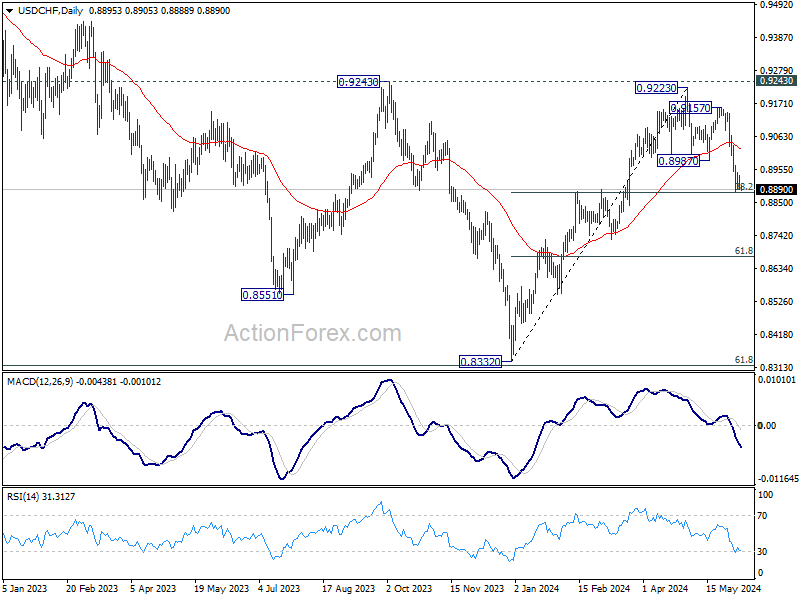

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8874; (P) 0.8911; (R1) 0.8930; More….

Intraday bias in USD/CHF stays neutral with focus on 0.8883 fibonacci level. Strong rebound from current level, followed by break of 0.8987 support turned resistance, will suggest that correction from 0.9223 has completed, and retain near term bullishness. However, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

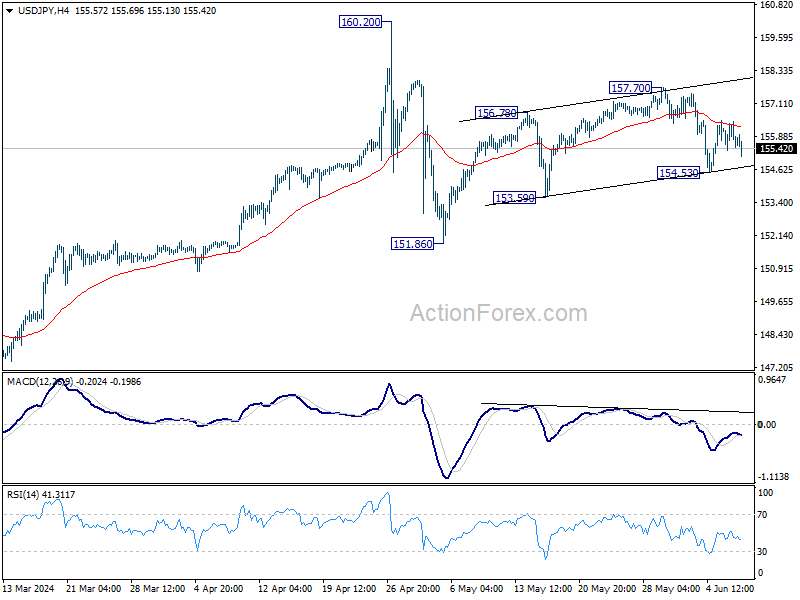

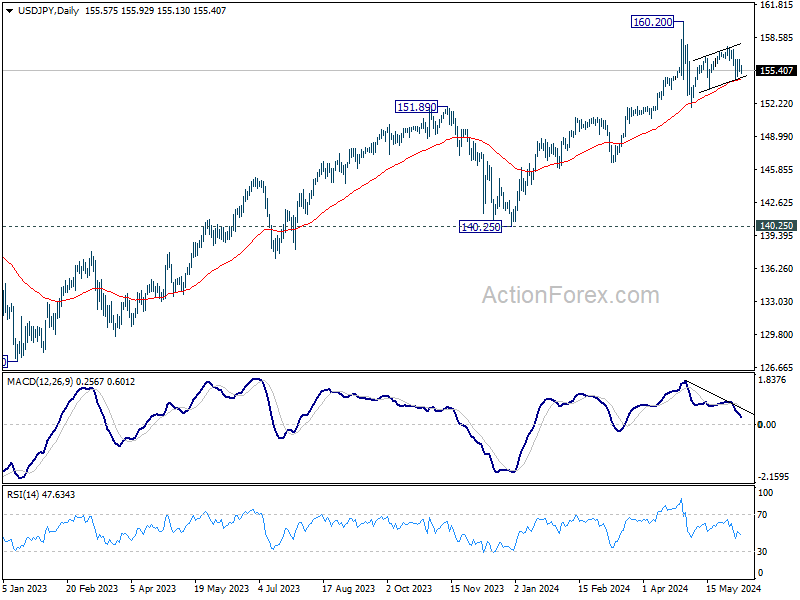

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.01; (P) 155.75; (R1) 156.86; More….

Intraday bias in USD/JPY stays neutral for the moment and outlook is unchanged. Risk will stay on the downside as long as 157.70 resistance holds. Fall from there is seen as the third leg of the corrective pattern from 160.20. On the downside, break of 154.53 will target 153.59 support first. Break there will pave the way to 151.86 support and below.

In the bigger picture, a medium term top might be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

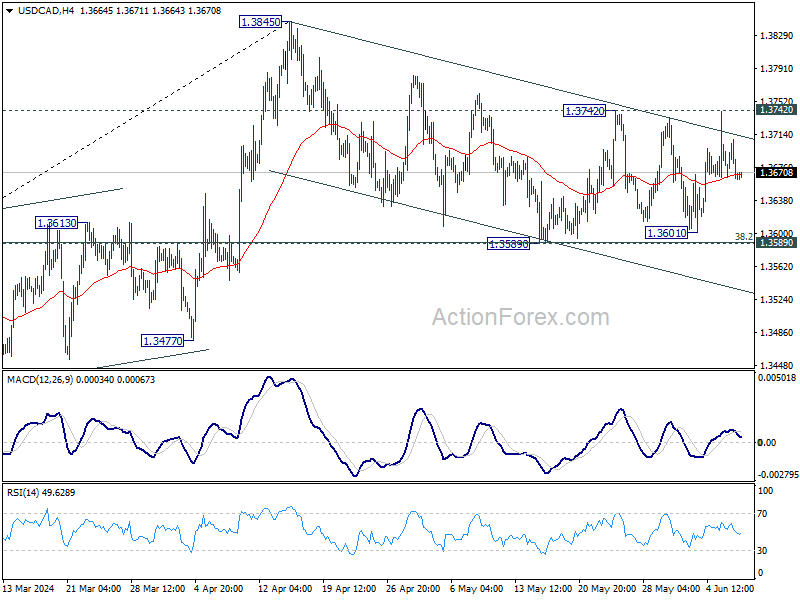

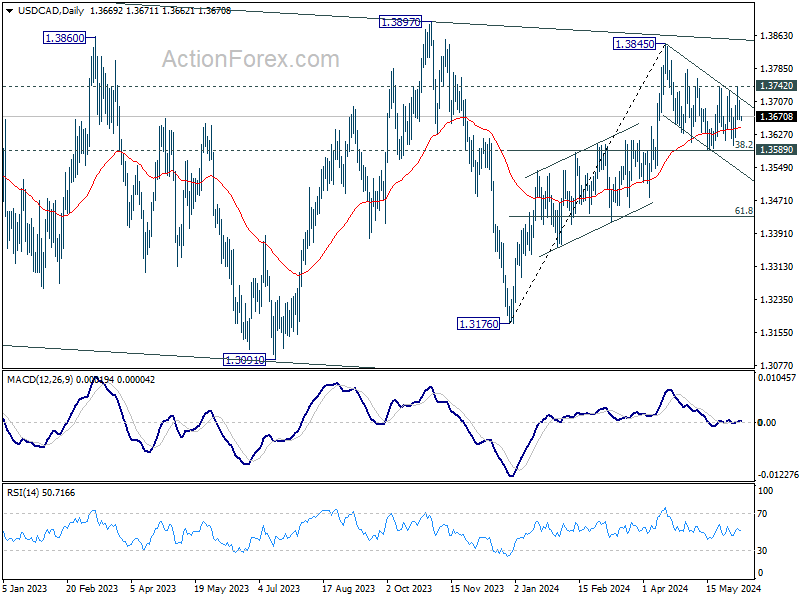

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3653; (P) 1.3682; (R1) 1.3699; More….

Intraday bias in USD/CAD remains neutral as it's still bounded in sideway trading. On the upside, break of 1.3742 resistance will revive the case that correction from 1.3845 has completed at 1.3589. Intraday bias will be back on the upside for retesting 1.3845. On the downside, firm break of 1.3589 support will argue that whole rise from 1.3176 has completed at 1.3845 already. Fall from 1.3845 should then resume to 61.8% retracement of 1.3176 to 1.3845 at 1.3432.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Today’s US Payrolls Important for Both Sides of Atlantic

Markets

German bunds underperformed US Treasuries in the wake of yesterday’s ECB policy meeting. Rates rose between 2.2 and 4.4 bps. The central bank cut rates by 25 bps for the first time in five years but still-high domestic price pressures and elevated wage growth mean it has to tread carefully down the easing path. Upwardly revised headline and core inflation forecasts (averaging >2% in 2025) showcase the point. President Lagarde (AKA the lady in charge) referred to the fact that real rates today were much higher than they were before with rates being steady since September but inflation having eased materially. This allowed for some removal of the current restrictiveness without pre-committing to anything nor declaring the central bank has now entered the “dialing back phase”. The hawkish cut meant that markets are no longer sure about a second move this year. Higher-than-expected weekly jobless claims clipped US rates’ cautious upward daily momentum. Yields eventually gained up to 1.2 bps (10-yr). EUR/USD appreciated and went for a test of the 1.09 big figure, supported by the generally positive (especially in Europe) risk environment. Unable to push through, the pair closed the day at 1.089. The trade-weighted dollar index moved south with the 104 barrier in focus.

Today’s US payrolls are important for both sides of the Atlantic in our view. The ECB’s data dependence should be seen broadly, with not only European data important for policy going forward, but also what the likes of the Fed (will) do. And the Fed’s sensitivity to the labour market is high. Consensus expects a job growth of 180k in May, more or less the pace of April. Wages are expected to grow 0.3% (3.9% y/y). US money markets in theory could add some more to a September Fed cut and raise the stakes for 2025 (currently 3.5 cuts) in case of an in line or slightly softer release. Yields at the front end of the US curve (2-yr) are close to support levels though, offering some protection to the downside. A break lower should only occur in case of a significant negative surprise. We also spot some bottoming out in longer maturities, including the 10-yr. Current ECB market pricing makes European rates vulnerable for a downleg in sympathy with the US. But to the extent it filters through to a positive risk (equity) environment, we are biased towards USD rather than euro weakness. EUR/USD continues to flirt with the 1.09 resistance zone and could get tested intensively. A break higher brings 1.0981 on the horizon. The usual slew of ECB speeches in the wake of the decision are worth following up.

News & Views

China foreign trade data for the month of May published this morning still indicated a mixed picture with respect to the country’s growth. Exports (in USD terms) jumped to 7.6% Y/Y indicating foreign demand to support the country’s economic. However, the figure was also supported by favourable base effects. At the same time, import growth slowed more than expected from 8.4%Y/Y in April to 1.4% in May, pointing to still mediocre domestic demand. The trade balance grew from $72.35 bln in April to $82.62 bln in May. Still the data over April and May combined suggest that net exports might provide a positive contribution to the country’s growth in Q2. In the meantime, the yuan hovers within reach of the year-to-date weakest levels near USD/CNY 7.245.

The Reserve Bank of India today kept its policy rate unchanged at 6.50% for the eight straight meeting in 4-2 vote as two members supported a rate cut. The bank kept its inflation forecast of FY 2025 unchanged at 4.5%, but raised its growth forecast from 7.0% to 7.2%. The Bank kept a guarded stance as of withdrawal of accommodation. At least of now, the RBI doesn’t show any intention to move to a more growth supportive policy stance as keeps the focus on bringing inflation back to the 4% target. In this respect, governor Das still warned that uncertainty with respect to food prices still needs close monitoring. The Indian rupee trades little changed near USD/IN 83.45.

Graphs

GE 10y yield

The ECB cut rates in June by 25 bps. But still-high domestic price pressures, elevated wage growth and upgraded inflation forecasts means the central bank cannot pre-commit to anything. Data-dependence remains the buzzword. The German 10y yield bounced off on the upward sloping trendline after a US correction pulled it lower. The backdrop of a recovering European economy should protects its downside.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed Chair Powell indicated that further tightening was unlikely. However, the FOMC Minutes still showed internal debate on whether policy is restrictive enough. Sticky inflation suggests any rate cut will be a tough balancing act while several policy makers hint at a higher neutral rate. The US 10-y yield is correcting lower in the 4.3/4.7% trading range.

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.06/1.09 area might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. We expect this important support level to hold.

All Eyes on US Jobs Data as Two G7 Banks Start Cutting Rates

As widely expected, the European Central Bank (ECB) announced a 25bp rate cut when it met yesterday, but raised its inflation target for this and the next year, warned that the road for easing inflation could be bumpy, and ruled out a July rate cut. The market no longer prices a full rate cut by October. The ECB will remain data-dependent and probably Fed-dependent as well, without saying it aloud, because even though cutting the rates before the Fed was not expected at the start of this year and was courageous, an excessive dovish stance from the ECB could weigh on the euro and jeopardize the bank’s efforts to fight inflation.

Reflation trade is on

The Eurozone yields jumped after the ECB decision, but the Stoxx 600 hit a fresh record. The EURUSD is flirting with the 1.09 level. The ECB meeting wasn’t necessarily conclusive, but at the end of the day, two G7 central banks announced a 25bp rate cut this week, and marked the beginning of the easing cycle for major central banks – even though easing won’t be fast enough.

Elsewhere, the S&P500 reacted positively by hitting a fresh record. Sentiment in energy and metals was cheery yesterday, as the reflation trade saw support following the Bank of Canada (BoC) and the ECB rate cuts and a better-than-expected Chinese export print. The FTSE 100 gained and US crude rebounded past the $75pb despite an unexpected build in US oil inventories last week and could well settle between the $75/78pb level having seen a dip near the $72 support earlier this week, after the OPEC’s announcement to start waning its supply cut policy from the Q3. Copper found support near the 50-DMA while iron ore recovered a part of last week’s losses. Overall, I believe that the reflation environment should continue to give support to the energy and mining-heavy markets, as the major central banks step concretely into the policy easing phase – regardless of how cautious they are and how fast the rates will be pulled lower. It will all depend on inflation…

EUR/USD sees support after hawkish ECB presser, before US NFP data

Looking at the currency markets, the more hawkish than expected ECB stance regarding the future rare cuts is supportive of a further rebound in the EURUSD and I revise my EURUSD outlook to neutral from negative, because look, the ECB remains in a better position to cut rates and should proceed with one more rate cut before the year ends. However, the Euro area surprise index improves although the expectations regarding the Euro area economy remain soft: the Eurozone is expected to revise the Q1 GDP growth from none to 0.3% today. In the meantime, the US data surprises to the downside with the US economic surprise index printing the most disappointing levels since 2019. Atlanta Fed’s GDP Now index rebounded past the 2% this week, but looks choppy. Therefore, the fast deteriorating US outlook, and slightly improving Eurozone outlook narrow the gap between the Fed and ECB expectations, and the latter could throw a floor under the EURUSD at the wake of the first ECB rate cut.

Today, all eyes turn toward the US jobs data. The week was marked by softer-than-expected job openings in April, a significantly lower-than-expected May ADP report, a surprise decline in the pace of unit labour costs from 4.7% to 4% and an unexpected jump in US weekly jobless claims. The consensus of analyst estimates on Bloomberg bet that the US economy may have added around 180K new nonfarm jobs last month, the unemployment rate is seen steady near 3.9% and wages growth may have slightly accelerated on a monthly basis. A soft jobs report should support the dovish Fed expectations and further weigh on the US dollar. The dollar index remains sold at the 100, 200-DMA area this week and has potential to decline with a soft set of data into next week’s FOMC meeting. Whatever today jobs data says, the Fed isn’t expected to cut rates when it meets next week, the Fed members sounded very cautious regarding their inflation expectations, therefore the new dot plot will probably show one or maximum two rate cuts on average this year – down from 3 expected rate cuts at the latest plot. But that’s mostly priced in and could be the peak hawkishness for the Fed this year – if the economic data continues to disappoint.

Do antitrust allegations really matter?

Nvidia eased after hitting a fresh ATH yesterday, and Microsoft consolidated gains above $420 a share on news that the US opened antitrust investigations into two of the world’s most valuable companies due to their dominance in the rapidly emerging field of AI. Nvidia was accused to sell chips to customers that are most likely to use them quickly, and Meta, Amazon and Alphabet stand for about a third of Nvidia’s revenue. But note that these antitrust investigations against the Big Tech companies are common and have not prevented their stock prices from rising thoroughly in the past.

ECB Cuts Rates as Expected, US Jobs Report Today’s Main Event

In focus today

Today's main data event will be the US May Jobs Report. We expect nonfarm payrolls to have grown by 190k, a modest uptick from April when weak public sector jobs growth weighed on the headline figure. Average hourly earnings growth likely remained steady at 0.2% m/m and we think unemployment rate will also remain unchanged at 3.9%. Fed's Cook will be on the wire today.

In the euro area, we receive the important wage growth data for Q1 measured as compensation per employee in the final national accounts. Wages rose 4.6% y/y in the final quarter of last year and recent data suggests that wage growth increased in the first quarter of this year. We also look out for the German industrial production data for May, which has rebounded slightly in the past months. We also have a string of ECB speakers on the wires with Simkus, Nagel, Schnabel, Holzmann, Centeno and Lagarde all set to speak.

Economic and market news

What happened overnight

In China, exports rose more than expected by 7.6% y/y in May (cons: 6.0%, prior: 1.5%). An increase in the annual growth rate was somewhat expected as base effects turned more positive in May. However, the higher-than-expected release is a strengthening signal for the Chinese economy.

What happened yesterday

In the euro area, the ECB decided to cut its three main policy rates by 25bp, which leaves the key policy rate at 3.75%. This cut follows a 9-month period with unchanged policy rates on the back of the rapid hiking cycle since mid-2022. The rate cut was widely expected and thus focus was on the communication. The updated staff projections showed inflation to hit 2% one quarter later (Q4 25) than at the time of the March meeting. With the rate cut fully anticipated, some initial volatility was quickly replaced with markets trading in a tight range, with no commitment on the timing of the next policy rate cut. We continue to look for the next policy rate cut in December in our baseline scenario, although we do not rule out a potential rate cut in September, see Flash: ECB Review - Cutting and keeping, 6 June.

Euro area retail sales fell more than expected by 0.5% m/m in April (cons: -0.3%, prior: 0.8%). Consumers are still cautious with spending despite high employment and rising real incomes. Given the also high savings there is a possibility that growth could be better than expected this year from higher private consumption, but so far, we still see muted spending.

In the US, initial jobless claims increased to 229k (cons: 220k, prior: 221k), showing some signs of the US labour market cooling, even though the claims are still at a low level in a historical context. We saw some USD weakening after the news, with EUR/USD raising from 1.086 to 1.089 after the release.

In Denmark, Nationalbanken cut its key policy rate by 25bp to 3.35%, matching the move by ECB. EUR/DKK trades close to the central rate, which means future rate reductions, will depend on the decisions of the ECB. We expect a 25bp rate cut from the ECB and Nationalbanken in December.

Market movements

Equities: Global equities were mixed yesterday, with an unusual combination of sector and regional rotations. While US indices experienced a downturn, the rest of the world's markets rose. Industrials and utilities underperformed simultaneously, while consumer discretionary and healthcare sectors saw a joint outperformance. The hawkish ECB cut was as sexpected and did not significantly impact the market's direction. In the US yesterday, the Dow increased by 0.2%, while the S&P 500 decreased by 0.02%, the Nasdaq dropped by 0.1%, and the Russell 2000 fell by 0.7%. Asian markets are mixed this morning, with South Korea notably outperforming. Futures in Europe and the US are marginally higher.

FI: Global yields grinded marginally higher through yesterda'’s trading session and the sell-off was largely unaffected by the ECB meeting. The 25bp rate cut was widely expected and with no guidance for the timing or pace of policy rate cuts, the 5y point suffered 1bp more relative to the short end and the long end, on a relatively upbeat growth assessment. 10y Bunds ended 4bp higher on the day at 2.55%.

FX: Overall, only modest reactions in FX space after the ECB cut rates yesterday. The cut was widely anticipated and was followed by small upticks in G10 EUR crosses. But instead of a follow-through they either held on to gains or bounced back down again after the press conference. This morning, ahead of toda'’s NFP key potential market mover, EUR/USD remains in the upper end of the 1.08-1.09 range, EUR/NOK is back at 11.50, EUR/SEK trades just north of 11.30 and EUR/DKK hovers just above 7.46.

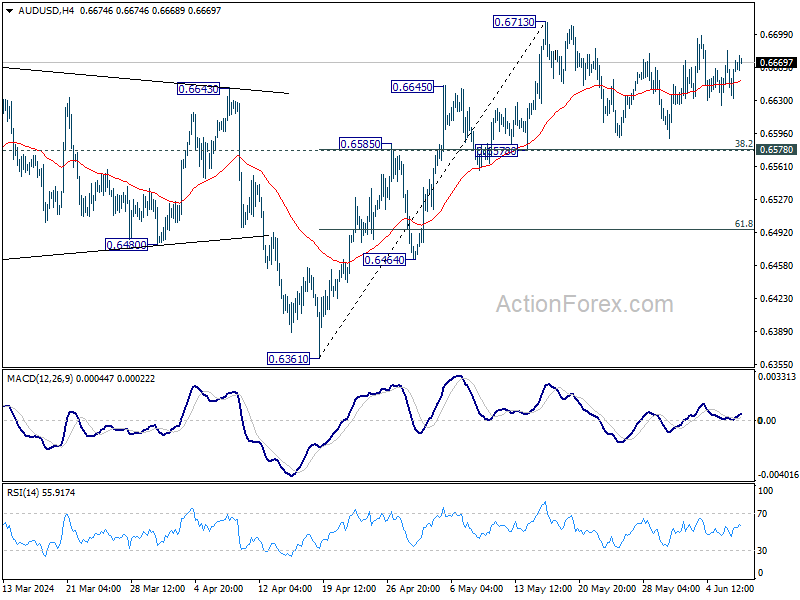

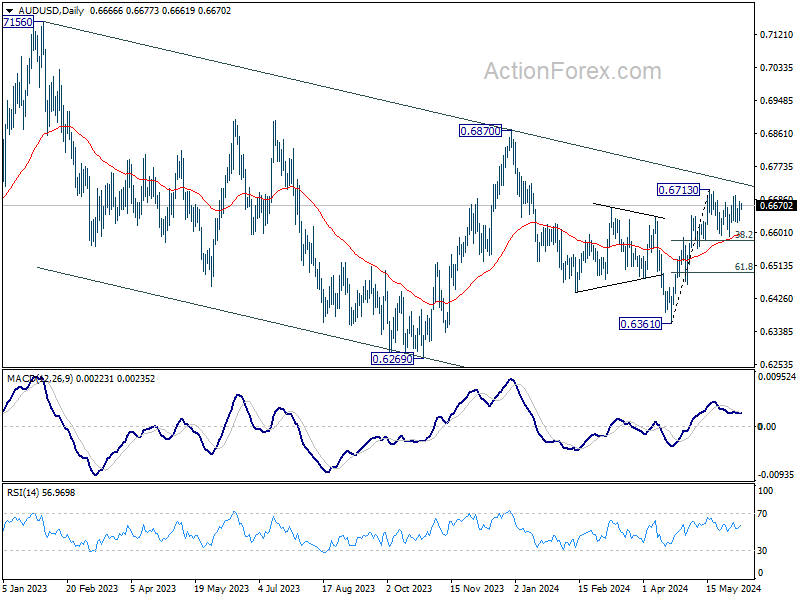

AUD/USD Daily Report

Daily Pivots: (S1) 0.6639; (P) 0.6661; (R1) 0.6689; More….

AUD/USD is still extending sideway trading below 0.6713 and intraday bias stays neutral. As long as 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) holds, further rally remains in favor. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Sluggish Forex Markets on Hold for Direction from US Non-Farm Payrolls

Forex markets remain directionless as the week's highly anticipated central bank activities. The rate cuts by both BoC and ECB failed to provide the expected catalysts for significant currency movements. Neither Canadian Dollar nor Euro managed to break out of their recent trading ranges following these policy adjustments. Similarly, Dollar continues to gyrate within its familiar boundaries. All eyes are now on the upcoming non-farm payroll report, which market participants hope will provide the momentum needed for more sustainable movements.

As we approach the week's end, the Swiss Franc remains the standout performer among major currencies, closely followed by Japanese Yen and New Zealand Dollar. On the other end of the spectrum, Canadian Dollar finds itself as the week's weakest link, exacerbated by BoC's dovish turn. Euro and British Pound continue to hover in middle positions

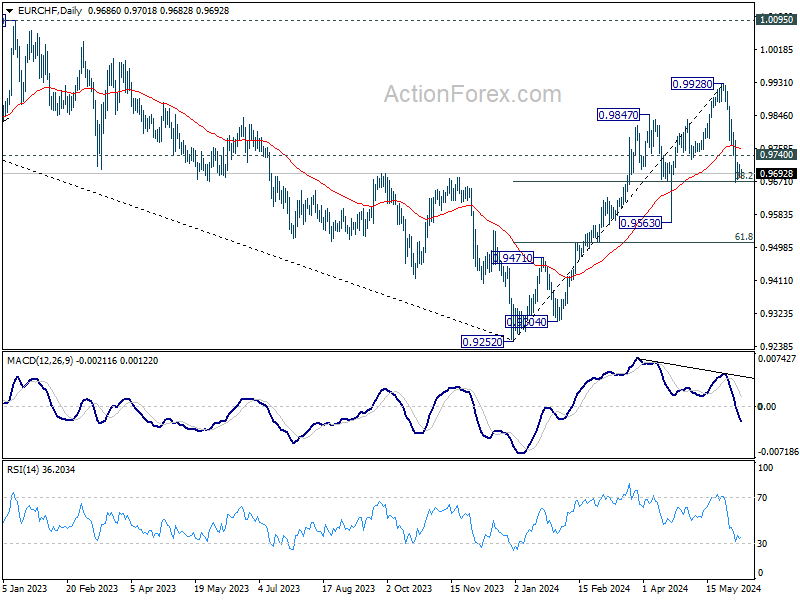

From a technical analysis standpoint, the Swiss Franc's impressive run might soon encounter a significant challenge. As it approaches a key Fibonacci resistance level in the EUR/CHF pair at the 38.2% retracement of 0.9252 to 0.9928 at 0.9670, a crucial juncture is at hand. A potent rebound from this level, particularly if it surpasses the 0.9740 mark, could signal a short-term bottoming out. This would potentially lead to a pronounced recovery. Such a technical move could precipitate a broader selloff in the Franc across various currency pairs, dramatically altering its current position as a top performer.

From a technical perspective, while the focus remains predominantly on Dollar due to today's non-farm payroll report, Swiss Franc also deserves attention. Franc is currently facing critical Fibonacci resistance level after its near term rally.

EUR/CHF is now pressing 38.2% retracement of 0.9252 to 0.9928 at 0.9670. Strong rebound from current level, followed by break of 0.9740 support will indicate short term bottoming, and bring stronger rebound. If realized, that could be accompanied by selloff in the Franc in other pairs, and push it down the performance ladder notably.

In Asia, at the time of writing, Nikkei is down -0.21%. Hong Kong HSI is down -0.48%. China Shanghai SSE is down -0.35%> Singapore Strait Times is up 0.45%. Japan 10-year JGB yield is up 0.0131 at 0.979. Overnight, DOW rose 0.20%. S&P 500 fell -0.02% NASDAQ fell -0.09%. 10-year yield fell -0.008 to 4.281.

Attention Shifts to US NFP as Dollar Index Seeks Fresh Momentum

As the week draws to a close, market attention is squarely on the upcoming US non-farm payroll employment report. The sluggish Dollar is in need of a catalyst from the jobs report to spark a meaningful and sustainable breakout from its recent range against major currencies.

Market expectations are set for NFP to show 180k growth o May, with the unemployment rate steady at 3.9%. Average hourly earnings are expected to increase by 0.3% mom.

Recent related economic data offers mixed signals. ISM Services employment index rose from 45.9 to 47.1, but still indicating contraction. Conversely, ISM Manufacturing employment index turned to expansion, rising from 48.6 to 51.1. ADP private employment showed a growth of only 152k. Additionally, the four-week moving average of initial jobless claims rose from 210k to 222k, suggesting some softening in the labor market.

While there may be some upside surprises in headline job growth, it is unlikely to significantly exceed expectations. The critical variable remains wage growth, which is essential for gauging underlying domestic inflation pressures, and an important factor influencing the timing of Fed's first rate cut.

Dollar index dipped to 103.99 this week but struggled to find decisive selling momentum. Further decline is still in favor as long as 105.18 resistance holds. Fall from 106.51 is seen as developing into the third leg of the pattern from 107.34. Any downside acceleration could push DXY through 102.35 support towards 100.61.

However, strong bounce from current level followed by break of 105.18 will revive near term bullishness. Rise from 100.61 would then be ready to resume through 106.51 before reversing.

China's exports rises 7.6% yoy in May, trade surplus exceeds expectations

In May, China's exports rose by 7.6% yoy, surpassing the expectation of 6.0% yoy growth. Notably, exports to US increased by 4.8% yoy, marking the highest growth in three months. Exports to ASEAN countries saw a significant jump of 25% yoy, while exports to the EU declined by -0.7% yoy.

On the import side, growth was more subdued, with imports rising by only 1.8% yoy, falling short of the expected 4.2% yoy increase.

China's trade balance for May reported a surplus of USD 82.6B, well above the anticipated USD 72.2B.

Looking ahead

Germany industrial productions and trade balance; Frane trade balance; Swiss foreign currency reserves, and Eurozone GDP revision wil be released in European session. Later in the day, Canada employment data is another important one beside US NFP.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6639; (P) 0.6661; (R1) 0.6689; More….

AUD/USD is still extending sideway trading below 0.6713 and intraday bias stays neutral. As long as 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) holds, further rally remains in favor. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | 6.55B | 5.50B | 5.02B | 4.84B |

| 05:45 | CHF | Unemployment Rate May | 2.40% | 2.30% | 2.30% | |

| 06:00 | EUR | Germany Factory Orders M/M Apr | -0.20% | 0.50% | -0.40% | |

| 08:00 | EUR | Italy Retail Sales M/M Apr | -0.10% | 0.30% | 0.00% | |

| 08:30 | GBP | Construction PMI May | 54.7 | 52.5 | 53 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | -0.50% | -0.20% | 0.80% | 0.70% |

| 12:15 | EUR | ECB Rate On Deposit Facility | 3.75% | 3.75% | 4.00% | |

| 12:15 | EUR | ECB Main Refinancing Operations Rate | 4.25% | 4.25% | 4.50% | |

| 12:30 | USD | Trade Balance (USD) Apr | -74.6B | -69.8B | -69.4B | -68.6B |

| 12:30 | USD | Initial Jobless Claims (May 31) | 229K | 215K | 219K | |

| 12:30 | USD | Nonfarm Productivity Q1 | 0.20% | 0.30% | 0.30% | |

| 12:30 | USD | Unit Labor Costs Q1 | 4.00% | 4.70% | 4.70% | |

| 12:30 | CAD | Trade Balance (CAD) Apr | -1.05B | -2.2B | -2.3B | |

| 12:45 | EUR | ECB Press Conference | ||||

| 14:00 | CAD | Ivey PMI May | 65.2 | 63 | ||

| 14:30 | USD | Natural Gas Storage | 89B | 84B |

China’s exports rises 7.6% yoy in May, trade surplus exceeds expectations

In May, China's exports rose by 7.6% yoy, surpassing the expectation of 6.0% yoy growth. Notably, exports to US increased by 4.8% yoy, marking the highest growth in three months. Exports to ASEAN countries saw a significant jump of 25% yoy, while exports to the EU declined by -0.7% yoy.

On the import side, growth was more subdued, with imports rising by only 1.8% yoy, falling short of the expected 4.2% yoy increase.

China's trade balance for May reported a surplus of USD 82.6B, well above the anticipated USD 72.2B.

Time for the Spakfilla?

The national accounts confirmed that demand growth remained soft. Revisions to past tourism spending have no implications for future inflation but underline that weak supply is still an issue.

This week’s national accounts confirm that the Australian economy is still soft. Domestic demand has limped along at a quarterly pace of 0.1–0.2% for a couple of quarters. Real household income was flat in the quarter and again lagged population growth over the year.

Consumption over the past two years was not as weak as previously stated. This is because the ABS has revised its assessment of past overseas tourism spending by Australians. This counts as consumption and has resulted in a lower estimated household saving ratio. But because outbound tourism counts as imports, this had no implications for GDP.

With the revisions, Australia no longer looks like such a downside outlier on the performance of consumption per capita relative to peer economies. The United States is still clearly an outlier on the upside, though.

Some observers have speculated that these revisions might imply that households are more willing to spend than previously thought. They might therefore spend more out of the forthcoming tax cuts than predicted. This possibility needs to be weighed against both the

Westpac–Melbourne Institute survey results suggesting the opposite, (PDF 156KB) and the reduced ability to spend implied by the lower savings buffer remaining.

Indeed, the revisions remove some of the puzzle about household saving remaining as high as it had appeared. Some resilience in saving could be reconciled because higher interest rates encourage higher saving, and lower consumption, even when incomes are not outright falling. But household disposable income growth has been unusually weak in Australia. The fiscal consolidation and drag from higher taxation have been larger in Australia than in some peers. It seems these factors have offset each other, and the overall boost to saving has not been material.

At its May meeting, the RBA Board assessed that demand was coming back into line with supply quite quickly. Key to its assessment of the inflation outlook, though, is where the level of demand stands relative to the level of supply. This is harder to assess. It is also important to remember that in an environment of large and more frequent supply shocks, demand outstripping supply does not necessarily imply that demand is strong. It could instead be a case of weak demand and even weaker supply, hampered by various constraints. This interpretation becomes more plausible as high inflation rates become confined to a smaller range of categories of consumption. Recent increases in shipping costs suggest that disruptions are ongoing.

Monetary policy works by hammering down demand to make it in line with supply. In recent years, though, part of the issue is that the demand ‘nail’ is only sticking out because the supply ‘wood’ around it has been eroded away. Some of the supply disruptions related to the pandemic have taken a long time to unwind.

Outbound tourism is a good example of this. According to data from the Bureau of Infrastructure and Transport Research Economics (BITRE), in February 2024 – the latest available data – there were around 2.15 million outbound airline seats available going to 65 cities. This compares with around 1.6 million seats for 52 cities the previous February and just 440,000 seats to 37 cities in February 2022, soon after the borders reopened. The expansion over the latest year occurred partly because China’s borders only opened in early 2023. Most of the destinations added since February 2023 are in China.

There is an element of two-way interaction, too. As tourism demand recovered, airlines would have been willing to put on more flights. That said, most of what we saw was supply recovering and the relative price of overseas travel normalising. It is only since the beginning of this year that available seats have returned to the levels seen in the corresponding month of 2019. For most of 2023, flight capacity was 10–15% short of 2019 levels.

It should be noted that this rebound in the number of available seats and travellers was already in the data. The latest revision to consumption relates to the average amount of spending Australians did when they were overseas. While it is hard to be sure on the basis of available information, it seems reasonable to suppose that the Australians who did go overseas on holiday in 2022/23 ¬– when flights were still constrained and expensive – were disproportionately the ones who could spend up big when they did travel. There might also have been an element of ‘revenge spending’ following the years when overseas travel was not possible.

The key point, though, is that the revision is for several quarters ago. Unlike the long and variable lags of monetary policy, the effect of extra demand on inflation comes through quickly. Whatever effect this extra spending had on inflation, it has already happened. Past inflation data already incorporated the effects of this extra spending, though we did not know this at the time. And since this spending occurred overseas, it did not involve domestic supply capacity in any case.

We therefore regard these revisions as having no material implications for the inflation outlook.

There is a broader point here about how we should interpret and respond to an excess of demand over supply when supply shocks are so prevalent. Instead of only hammering down the demand nail, policymakers and businesses also need to consider what they can do to rebuild the supply of wood surrounding the nail.

Time for some Spakfilla? Simplifying and fast-tracking approval processes, and ensuring skilled migration is directed to activities that add to supply would be a start. At the least, what is needed is some understanding that the ripple effects of the pandemic are not yet over. It also needs to be understood that high inflation concentrated in a few categories is not the same thing as generalised high inflation. Tight monetary policy might still be needed. The assessment of the outlook should, however, allow for these differences.