Sample Category Title

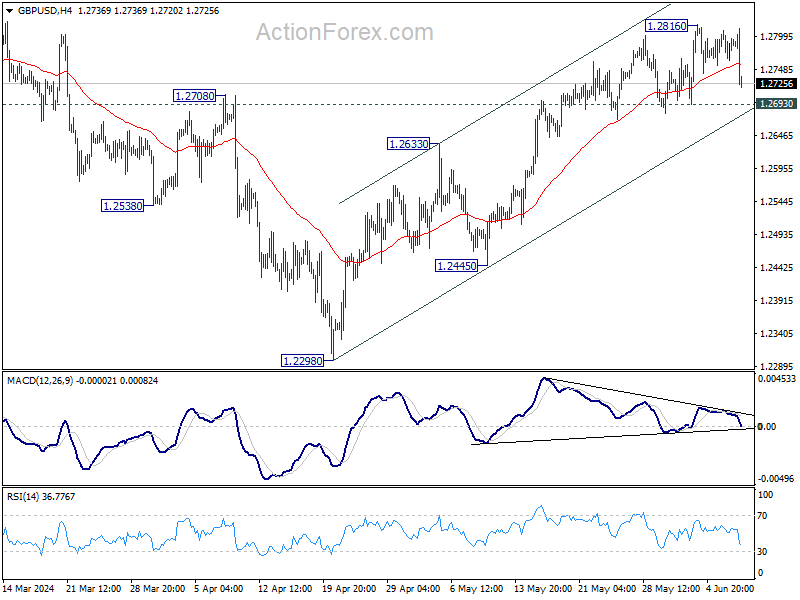

GBP/USD Mid-Day Report

Daily Pivots: (S1) 1.2766; (P) 1.2788; (R1) 1.2812; More…..

GBP/USD dips notably in early US session but stays above 1.2693 support. Intraday bias remains neutral first. Considering bearish divergence condition in 4H MACD, firm break of 1.2693 will turn bias back to the downside for 55 D EMA (now at 1.2646) and possibly below. Nevertheless, break of 1.2816 will resume the rise from 1.2298 to 1.2892 resistance.

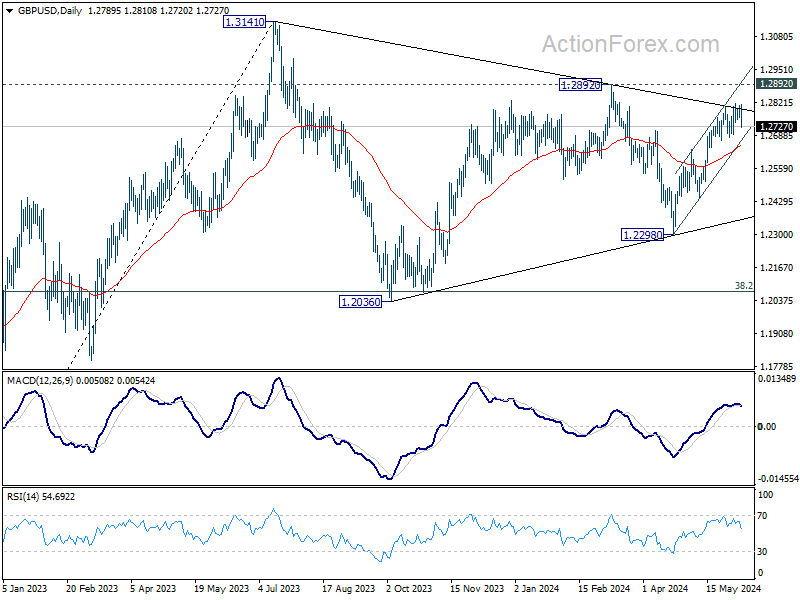

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

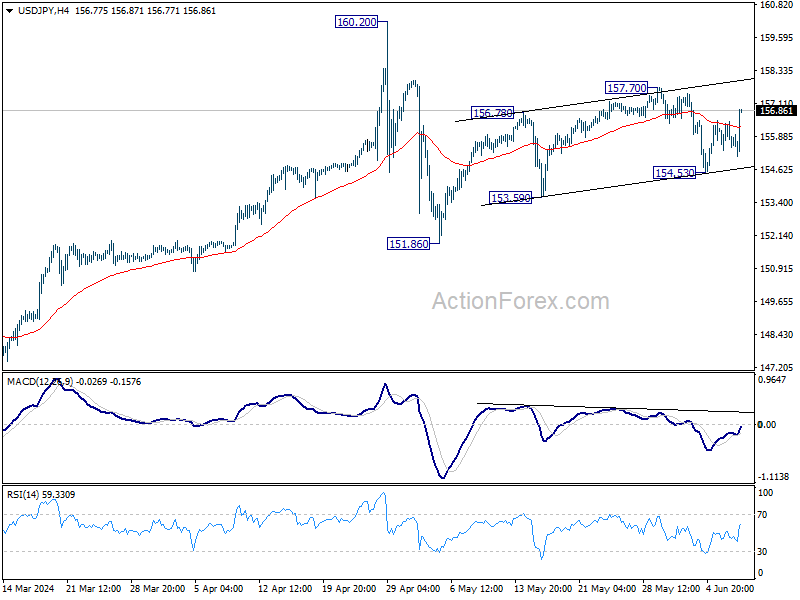

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.19; (P) 155.81; (R1) 156.26; More….

USD/JPY rebounds notably in early US session but stays below 157.70 resistance. Intraday bias remains neutral first. On the upside, break of 157.70 will resume the whole rise from 151.86 and target 160.20 high. Nevertheless, break of 154.53 will turn bias to the downside for 151.86 support and possibly below, as the third leg of the corrective pattern from 160.20.

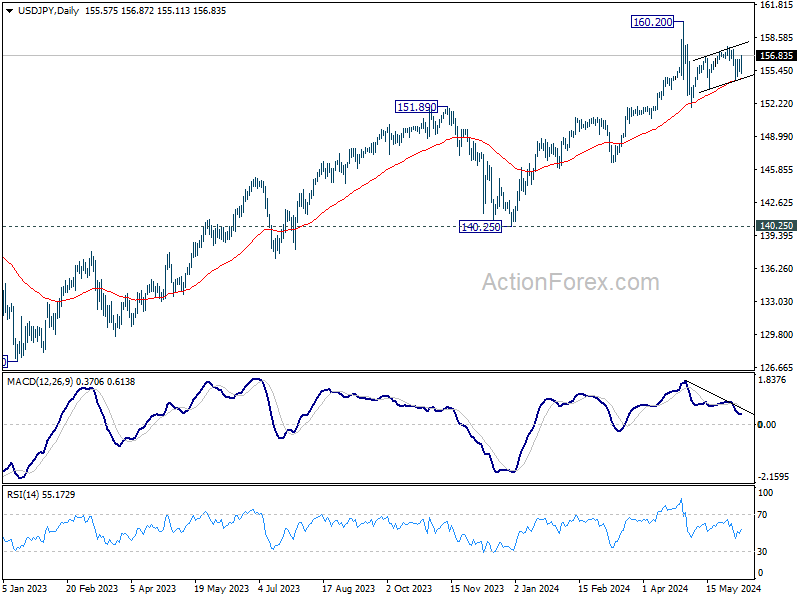

In the bigger picture, a medium term top might be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

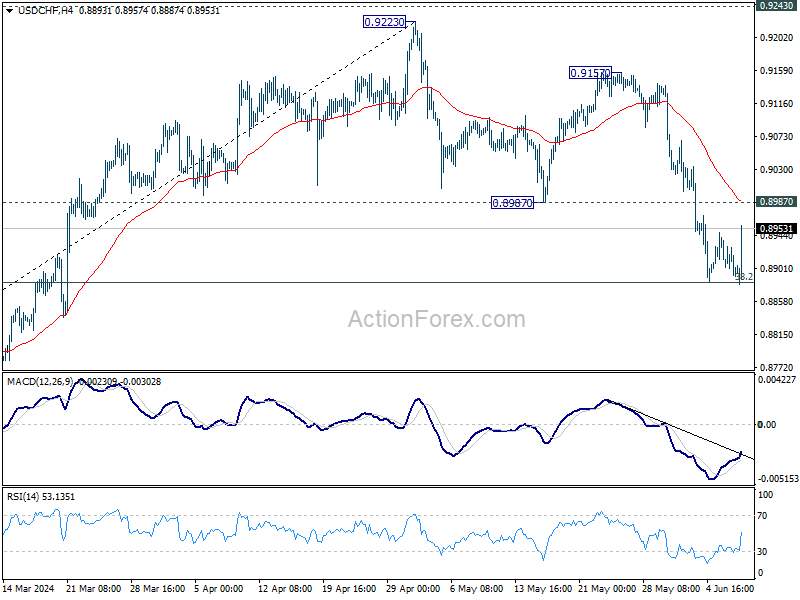

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8874; (P) 0.8911; (R1) 0.8930; More….

USD/CHF recovers after another take on 0.8883 fibonacci level but stays below 0.8987 support turned resistance. Intraday bias stays neutral first. Strong rebound from current level, followed by firm break of 0.8987 support turned resistance, will suggest that correction from 0.9223 has completed, and retain near term bullishness. However, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Strong NFP Report Propels Dollar and Drags Risk Sentiment

Dollar rebounds broadly in early US session following stronger-than-expected employment data. Despite a slight uptick in unemployment rate, robust headline job growth and wage increases highlighted the US job market's continued tightness. This suggests that Fed should remain cautious about premature policy easing.

In reaction to the data, US futures tumbled significantly, pointing to a lower open. A key question now is how much this sentiment will impact the resilient tech sector, with NASDAQ having just reached another record high this week. Additionally, 10-year Treasury yield staged a strong rebound, climbing back above 4.4% mark.

In the broadly currency markets, Canadian Dollar remains the worst performer for the week, despite slightly better-than-expected Canadian job data. Australian Dollar is the second worst and may weaken further before the weekly close due to risk-off sentiment. Euro is currently the third worst. Conversely, Swiss Franc and Yen are the best performers, though their positions could be overtaken by the surging Dollar.

In Europe, at the time of writing, FTSE is down -0.70%. DAX is down -0.86%. CAC is down -0.79%. UK 10-year yield is up 0.0726 at 4.251. Germany 10-year yield is up 0.077 at 2.630. Earlier in Asian, Nikkei fell -0.05%. Hong Kong HSI fell -0.59%> China Shanghai SSE rose 0.08%. Singapore Strait Times closed flat. Japan 10-year JGB yield rose 0.0069 to 0.973.

US NFP grows 272k, average hourly earnings rises 0.4% mom

US non-farm payroll employment grew 272k in May, well above expectation of 180k. That's also higher than the average monthly gain of 232k over the prior 12 months.

Unemployment rate ticked up from 3.9% to 4.0%, above expectation of 3.9%. Labor force participation rate fell from 62.7% to 62.5%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the 12 months period, average hourly earnings rose 4.1% yoy.

Canada employment grows 26.7, unemployment rate up to 6.2%

Canada's employment grew 26.7k in May slightly above expectation of 24.8k. Part-time employment rose 62k while full-time jobs fell -36k.

Unemployment rate ticked up from 6.1% to 6.2%, matched expectations. Average hourly wages increased 5.1% yoy, up from April's 4.7% yoy.

ECB's Nagel: Rate cuts not on autopilot

ECB Governing Council member Joachim Nagel stated today that the decision to cut interest rates yesterday was "logical" given the tendency for inflation to decrease. However, he emphasized that inflation remains "stubborn," particularly in the services sector.

Nagel highlighted that negotiated wages are expected to rise sharply this year and continue strong growth thereafter. He noted, "We on the ECB Governing Council are not driving on autopilot when it comes to interest rate cuts."

Council member Olli Rehn stated that inflation will continue to decline and interest rate cuts will support economic recovery. Rehn suggested that the possible scale of interest rate cuts over the next few years could range from 1 to 2 percentage points, assuming no new economic shocks occur.

Council member Gediminas Šimkus indicated that more than one rate cut might be necessary this year. He acknowledged that while data shows clear signs of disinflation, the path ahead will be challenging. Vice President Luis de Guindos added that inflation is expected to be around 2% next year but also noted "huge uncertainty in the economy."

China's exports rises 7.6% yoy in May, trade surplus exceeds expectations

In May, China's exports rose by 7.6% yoy, surpassing the expectation of 6.0% yoy growth. Notably, exports to US increased by 4.8% yoy, marking the highest growth in three months. Exports to ASEAN countries saw a significant jump of 25% yoy, while exports to the EU declined by -0.7% yoy.

On the import side, growth was more subdued, with imports rising by only 1.8% yoy, falling short of the expected 4.2% yoy increase.

China's trade balance for May reported a surplus of USD 82.6B, well above the anticipated USD 72.2B.

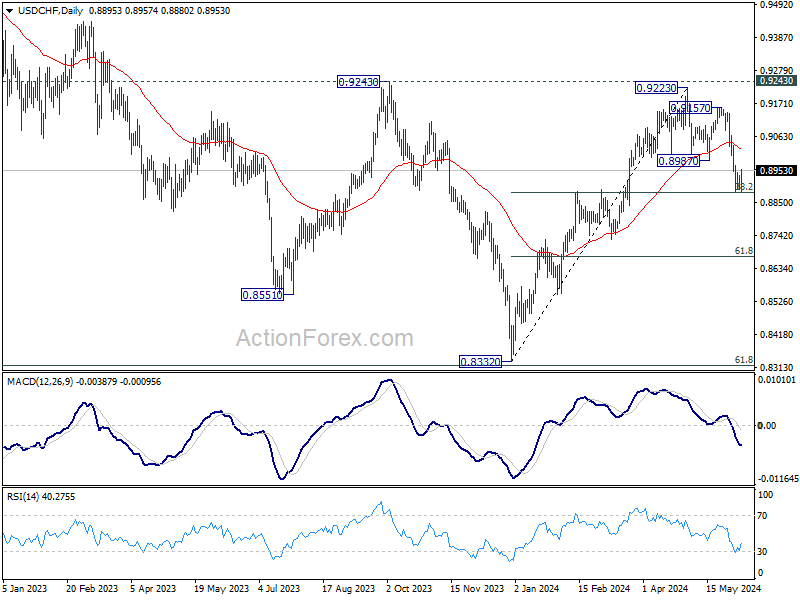

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8874; (P) 0.8911; (R1) 0.8930; More….

USD/CHF recovers after another take on 0.8883 fibonacci level but stays below 0.8987 support turned resistance. Intraday bias stays neutral first. Strong rebound from current level, followed by firm break of 0.8987 support turned resistance, will suggest that correction from 0.9223 has completed, and retain near term bullishness. However, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Sales Q1 | 0.70% | -0.60% | -0.50% | |

| 23:30 | JPY | Household Spending Y/Y Apr | 0.50% | 0.60% | -1.20% | |

| 03:00 | CNY | Trade Balance (USD) May | 82.6B | 71.5B | 72.4B | |

| 06:00 | EUR | Germany Industrial Production M/M Apr | -0.10% | 0.20% | -0.40% | |

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | 22.1B | 25.5B | 22.3B | 22.2B |

| 06:45 | EUR | France Trade Balance (EUR) Apr | -7.6B | -5.4B | -5.5B | -5.4B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | 718B | 720B | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q1 | 0.30% | 0.30% | 0.30% | |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 F | 0.30% | 0.30% | 0.30% | |

| 12:30 | USD | Nonfarm Payrolls May | 272K | 180K | 175K | 165K |

| 12:30 | USD | Unemployment Rate May | 4.00% | 3.90% | 3.90% | |

| 12:30 | USD | Average Hourly Earnings M/M May | 0.40% | 0.30% | 0.20% | |

| 12:30 | CAD | Net Change in Employment May | 26.7K | 24.8K | 90.4K | |

| 12:30 | CAD | Unemployment Rate May | 6.20% | 6.20% | 6.10% | |

| 14:00 | USD | Wholesale Inventories Apr F | 0.20% | 0.20% |

Canada employment grows 26.7, unemployment rate up to 6.2%

Canada's employment grew 26.7k in May slightly above expectation of 24.8k. Part-time employment rose 62k while full-time jobs fell -36k.

Unemployment rate ticked up from 6.1% to 6.2%, matched expectations. Average hourly wages increased 5.1% yoy, up from April's 4.7% yoy.

US NFP grows 272k, average hourly earnings rises 0.4% mom

US non-farm payroll employment grew 272k in May, well above expectation of 180k. That's also higher than the average monthly gain of 232k over the prior 12 months.

Unemployment rate ticked up from 3.9% to 4.0%, above expectation of 3.9%. Labor force participation rate fell from 62.7% to 62.5%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the 12 months period, average hourly earnings rose 4.1% yoy.

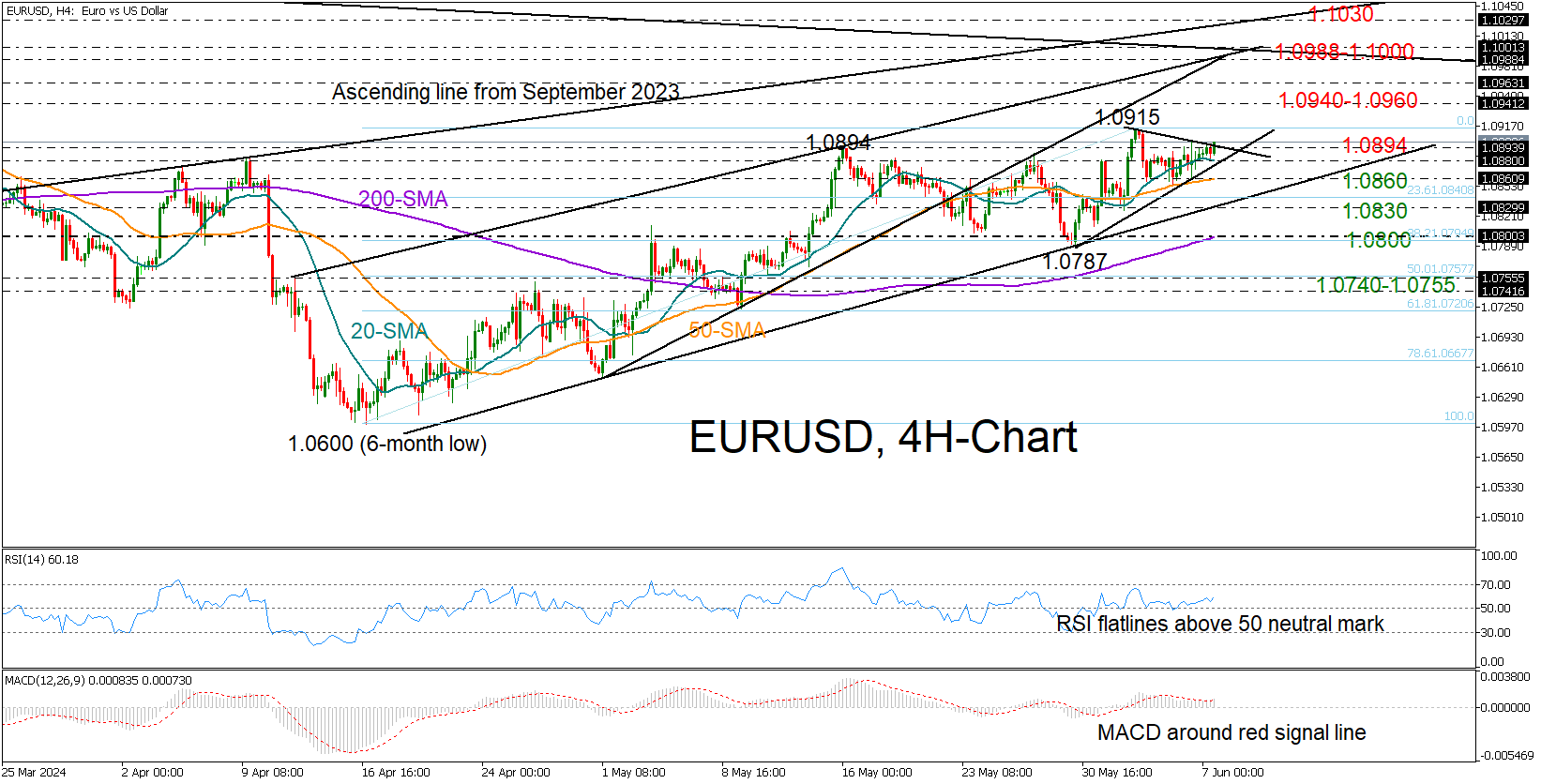

EURUSD Struggles to Close Above 1.0900

- EURUSD constrained below May’s barrier of 1.0894

- Technical signals reflect uncertainty

- Sellers could take control below 1.0830

Despite a false bullish breakout to 1.0915 earlier this week, EURUSD has been struggling to close above May’s bar of 1.0894.

From a technical perspective, traders are indecisive as the RSI in the four-hour chart is lacking direction above its 50 neutral mark and the MACD has stabilized around its red signal line.

On the upside, the price could re-examine the 1.0915 high if the 1.0894 barrier gives way. A continuation higher would bolster buying appetite, likely bringing the March constraining zone of 1.0940-1.0960 next into view. Should the bulls dominate there, the uptrend may expand towards the 1.0988-1.1000 trendline zone. The 1.1030 region, where the ascending line drawn from the September 2023 low is located, could be the next target.

On the downside, the 20-period simple moving average (SMA) has been buffering bearish actions around 1.0880 over the past couple of sessions. Hence, if that base cracks, the 50-period SMA might instantly come to the rescue at 1.0860. If the bears win that battle though, selling pressures could intensify towards the key support trendline at 1.0830 or lower to 1.0800.

All in all, EURUSD is in a wait-and-see mode. A close above 1.0915 would put the pair back on a bullish path, whilst a drop below 1.0830 would question the April-May uptrend.

SILVER (XAGUSD) Buying the Dips at the Blue Box Area

Hello fellow traders. In this technical article, we’re going to take a look into the Elliott Wave charts of SILVER (XAGUSD), exclusively presented in the members’ area of our website. As our members know SILVER has recently made pull back that made clear 3 waves down from the May 20th peak . The commodity completed correction right at the Equal Legs zone ( Blue Box Area) . In further text we’re going to explain the Elliott Wave pattern and trading setup.

SILVER Elliott Wave 4 Hour Chart 06.03.2024

The commodity is giving us wave 4 red correction, that can be unfolding as Elliott Wave Zig Zag pattern. The pull back has already reached the extreme zone: 29.82-28.28 (Blue Box- buying zone) . However , we believe another marginal wave down still be seen within Blue Box to complete the pattern.

Despite the expected extension lower, we advise members to avoid selling SILVER. As the main trend is bullish, we expect to see either rally toward new highs or a 3 waves bounce alternatively. Once the bounce reaches the 50% Fibonacci retracement level against the connector high -((b)) black, we’ll secure our position by moving the stop-loss to breakeven. Break of 1.618 fib ext: 28.28 would invalidate the trade.

A quick reminder:

Our charts are designed for simplicity and ease of trading:

- Red bearish stamp + blue box = Selling Setup

- Green bullish stamp + blue box = Buying Setup

- Charts with Black stamps are deemed non-tradable. 🚫

SILVER Elliott Wave 4 Hour Chart 06.06.2024

The commodity made another leg down toward Blue Box area. XAGUSD found buyers within the Blue Box area as expected. We got a nice rally from our buying zone, counting wave 4 correction completed at the 29.33 low. The bounce has exceeded the 50% Fibonacci retracement level against the connector peak. As a result, traders who entered long positions are now enjoying risk-free profits. With the price holding above the 29.33 low, we believe the next leg up can be in progress. We’re looking for a break above the 3 red peak, to confirm next leg up is in progress.

USD/JPY Steady Despite Soft Household Spending

The Japanese yen is calm on Friday. In the European session, USD/JPY is trading at 155.50, down 0.06% on the day at the time of writing.

Japan’s household spending slips

Japan’s economic activity has been sluggish and household spending, a key driver of economic growth, declined by 1.2% m/m in April. This followed a 1.2% gain in March and was well short of the market estimate of 0.2%. On a yearly basis, household spending rose 0.5%, up from -1.2% but short of the market estimate of 0.6%.

Japanese households have been curbing spending as inflation is high and economic conditions remain gloomy. On Monday, we’ll get a look at Japan’s GDP for the first quarter and the forecast is not looking good. The economy is expected to have contracted by 0.5% q/q in Q1 after no growth in the fourth quarter of 2023. This would point to the economy barely avoiding a recession. On an annualized basis, the economy is expected to have declined by 2% after a gain of 0.4% in the fourth quarter.

The Bank of Japan meets on June 14th and a weak GDP report could complicate plans to tighten policy. The BoJ has hinted that it will continue on the path to normalization but if the central bank doesn’t make any moves at the June meeting, the weak Japanese yen could lose more ground.

In the US, the week wraps up with the nonfarm payrolls report for May. This release is one of the most important events on the data calendar but has found itself overshadowed by inflation releases. Still, nonfarm payrolls is a market-mover that can have a significant impact on the US dollar. The market estimate stands at 185,000 for May, little changed from the 175,000 gain in April.

USD/JPY Technical

- USD/JPY tested resistance at 155.81 earlier. Above, there is resistance at 156.21

- 155.19 was tested in support earlier. The next support level is 154.74

Week Ahead – Fed and BoJ Decide on Monetary Policy

- US CPI data and Fed to determine the dollar’s fate

- Will the BoJ signal that another rate hike is looming?

- Pound traders await UK employment and GDP numbers

- RBA hike bets shrink ahead of AU jobs and China CPI data

Mind the dots

With US inflation resuming its downtrend in April and the ISM manufacturing PMI for May disappointing, investors remained convinced that the Fed will begin lowering interest rates at some point this year. Currently, they are penciling in nearly two quarter-point reductions by December, assigning around an 80% probability for the first one to be delivered in September.

Ergo, as they try to figure out when Fed officials will hit the rate cut button, traders are likely to lock their gaze on Wednesday’s FOMC decision next week. This will be one of the more significant meetings that is accompanied by updated economic projections and a new dot plot.

Bearing in mind policymakers’ ‘higher for longer’ mantra, market participants are nearly certain that the Committee will refrain from acting at this gathering. Therefore, the spotlight will fall on the statement and especially the new interest rate projections. The March plot pointed to three 25bps cuts this year and another three in 2025.

So, with most policymakers signaling that they are in no rush to start lowering borrowing costs, there is the possibility of an upward revision. Nonetheless, a median dot pointing to two rate cuts this year may not be enough to lift the dollar, as this is what the market is already anticipating. For the dollar to stage a strong recovery, the majority of Fed officials may need to signal only one quarter-point reduction for 2024.

The US CPI data for May are due to be released just a couple of hours ahead of the decision, and a set of sticky numbers could allow the dollar bulls to start the party earlier, even if the Fed decision does not meet their expectations. After all, market participants will be aware that the CPI numbers will not be incorporated into policymakers’ projections. That said, Fed Chair Powell may receive questions about the data at the press conference. The PPI figures are scheduled for Thursday.

When is the next BoJ rate hike coming?

On Friday, the central bank torch will be passed to the Bank of Japan (BoJ). At its latest gathering on April 26, this Bank kept the range for its benchmark rate between 0% and 0.1% as was widely expected. Although the Bank upgraded its inflation projection, it did not signal a reduction of its bond purchases and refrained from signaling a strong intention to raise interest rates again soon. This resulted in a weakening yen and two intervention episodes by Japanese authorities in the following days.

However, the currency resumed its slide soon after the episodes, with the larger-than-expected economic contraction for Q1 putting obstacles in the road for the next rate increase. Investors are still assigning a strong 67% chance for another 10bps hike in July, but should the Bank avoid communicating that clearly, traders may get disappointed, and the yen could extend its slide and retest its recent lows.

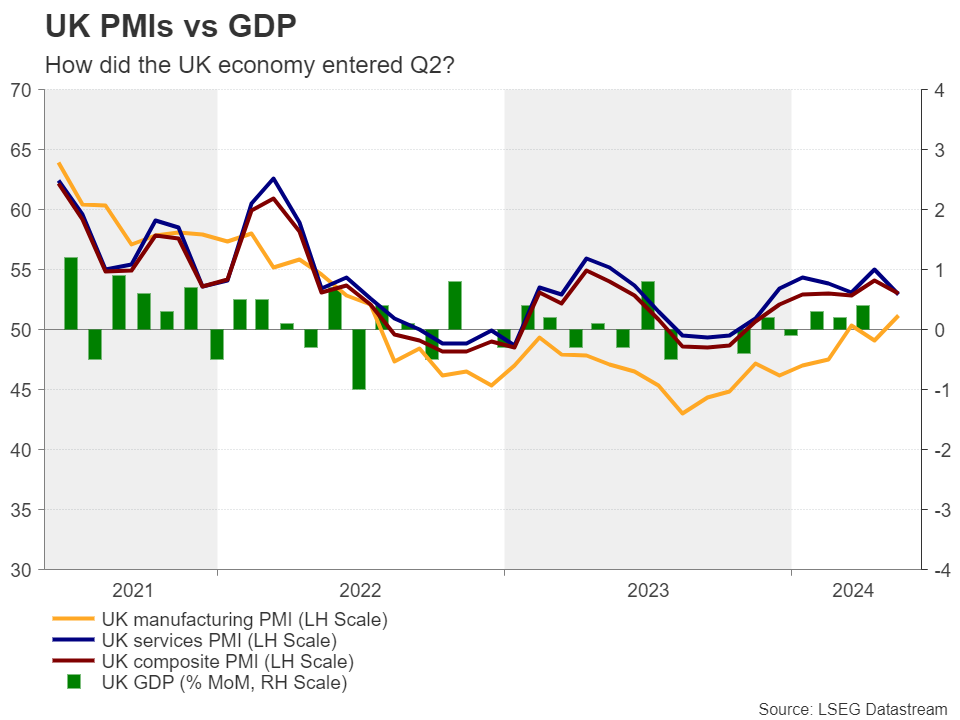

UK jobs and GDP data to shake the pound

The pound is also likely to be a protagonist next week, as the UK employment report and the monthly GDP rate, both for April, are due to be released on Tuesday and Wednesday respectively.

The hotter-than-expected UK inflation numbers for April, and especially the stickiness in underlying price pressures, prompted investors to scale back their BoE rate cut bets. Currently, they are pricing in around 40bps worth of rate reductions by December, with the probability of a first quarter-point cut in September resting at around 65%.

Another month of elevated wage growth and a GDP figure corroborating the view that the UK economy entered Q2 on a solid footing may lessen the September probability and thereby help the pound trade higher.

Nonetheless, with general elections scheduled for July 4, pound traders may become more careful closer to that date. The Labor party has been portraying itself as the party of fiscal responsibility and thus, if they win, they could make the BoE’s work easier, allowing it to cut interest rates much earlier than currently expected.

China inflation, AU jobs, EU elections

Elsewhere, China’s CPI and PPI numbers are scheduled for Wednesday, while Australia’s employment report is due out on Thursday.

Although Australia’s weaker-than-expected GDP data for Q1 eliminated the few bets about a rate hike by the RBA, the Australian central bank is still seen as one of the most hawkish among the major ones, as investors seen only a 50% chance for a quarter-point reduction by the RBA this year.

Thus, a rebound in Australia’s employment combined with hotter-than-expected Chinese inflation may allow the aussie to trade higher as investors become more confident that the RBA is unlikely to press the cut button this year.

It is also worth mentioning that this Sunday is the last day of the EU Parliamentary elections. Although the outcome may not be a game changer for financial markets, a surge in right-wing support could make it more difficult for lawmakers to agree and push through reforms and policies that give the EU more power. This could weigh somewhat on the euro.