Sample Category Title

Tech sector propels NASDAQ to new record

The US stock markets continued to display diverged performance. While DOW continued to struggle to bounce, S&P 500 and NASDAQ surged to new record highs. In the background, investor confidence is growing that Fed will begin cutting interest rates in September, with markets currently pricing in nearly 70% odds of this outcome.

A significant driver of this bullish sentiment is the strong performance of the tech sector, which has boosted overall risk appetite. Nvidia's market valuation reached the USD 3T for the first time, surpassing Apple to become the world's second-most valuable company.

Technically, near term outlook will now stay bullish in NASDAQ as long as 16336.07 support holds. A goldilocks non-farm payroll report tomorrow could prompt upside acceleration towards 138.2% projection of 10207.47 to 14446.55 from 12543.85 at 18427.31.

ECB’s Interest Rate Decision and Impact on EUR/USD Exchange Rate

Talking Points

- ECB Main Refinance Rate and EU Inflation

- EUR/USD Technical Analysis – Daily Chart

ECB Main Refinance Rate and EU Inflation

The European Central Bank is scheduled to announce its main refinancing rate on its June 6th, 2024 meeting, traders around the world are looking forward to the central bank’s decision and how it may impact the EURO exchange rate against other currencies. The current main refinancing rate is 4.5%. According to multiple media sources, it is widely anticipated that the central bank will announce a 25 basis point rate cut, taking the main refinance rate down to 4.25%. Should this rate reduction materialize, the ECB would surpass the Federal Reserve (FED) in implementing rate cuts, as the FED remains hesitant to do so. Overall, the ECB’s rate decision is a significant event that is likely to have a number of consequences for the eurozone economy and the foreign exchange market.

According to Bloomberg Analysts surveys, 99.5% of market participants expect a 25 basis points cut on the June 6th meeting, and less than 1% expect a cut for ECB’s July 2024 meeting. The remainder of the year includes mixed views on the ECB’s future rate cuts for 2024. This indecision regarding the 2024 rate cut path may prompt traders to scrutinize the language employed in the forthcoming monetary policy statement as well as the comments and responses of President Christine Lagarde during the ECB’s press conference following the release.

The Euro Zone’s inflation rate experienced an increase in May, with the Consumer Price Index (CPI) reaching 2.6% year-on-year (Y/Y), up from 2.4% in April. Core inflation, based on Eurostat data, also exceeded expectations. This upward trajectory in inflation is a critical factor that could influence the ECB’s future monetary policy decisions. While market sentiment leans toward a potential ECB rate cut in June, the recent increase in EU inflation raises questions about the ECB’s future rate cuts for 2024. The latest CPI increase was primarily driven by rising costs of housing, electricity, gas, and other fuels. However, oil prices have declined in the days following the release of the EU inflation report. The current CPI reading approximates the pre-pandemic average lows.

The EUR/USD exchange rate has witnessed a remarkable increase of nearly 3% since its low of 1.0606 in mid-April 2024, reaching a high of 1.0915 before encountering selling pressure that pushed the price back to the 1.0870 range. The EUR/USD’s recent uptrend persists ahead of the ECB’s meeting. However, several significant resistance levels lie ahead.

The latest COT report for the week ending on May 31st, 2024 (Includes data up to the end of day Tuesday, May 28th, 2024) reflects that the Asset Manager/Institutional and Leveraged Funds categories positioning moved toward long territory after remaining near an intermediate-long extreme level for several weeks. Commercial positioning shifted to shorting, which aligns with recent price action.

EUR/USD Technical Analysis – Daily Chart

- Price action broke out of and closed above the upper border of the narrowing formation; and a throwback took place, along with a shortfall as buyers entered the market above a weekly pivot point of 1.0797 forming an intermediate double bottom formation above the breakout level.

- Price action broke out above the resistance level of the intermediate double bottom formation, and has attempted another throwback to the breakout level.

- A confluence of support represented by the weekly pivot point, a monthly support level, the SMA9, and the EMA9 lies below price action within the range of 1.0840-1.0860 area.

- Price continues to trade above its EMA9, SMA9 and SMA21.

- Non-smoothed RSI7 aligns with price action and currently near its neutral level.

- A potential triple bottom formation lies within the narrowing formation pattern. If the breakout remains intact, we may consider watching for the pattern completion. (Blue circles).

Weekly Chart update

- Price action broke and remained below the lower border of an ascending channel. A pullback has materialized and price action has made it back to the previously broken trendline. It is unchanged from last week, and maybe critical to monitor price behavior at this level.

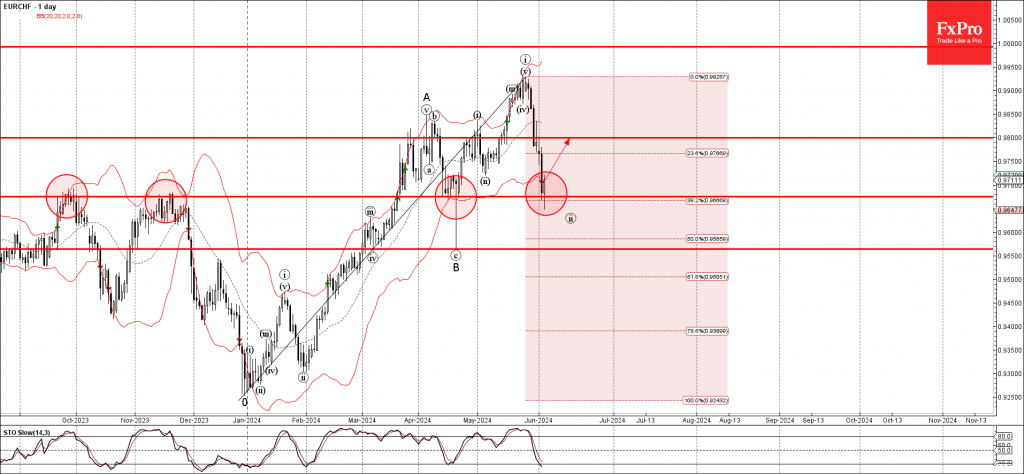

EURCHF Wave Analysis

- EURCHF reversed from support level 0.9675

- Likely to rise to resistance level 0.9800

EURCHF currency pair recently reversed up from the pivotal support level 0.9675 (former resistance from November and strong support from April).

The support level 0.9675 was strengthened by the lower daily Bollinger Band and by the 38.2% Fibonacci correction of the upward impulse from December.

Given the strength of the support level 0.9675 and the oversold daily Stochastic, EURCHF currency pair be expected to rise further to the next resistance level 0.9800.

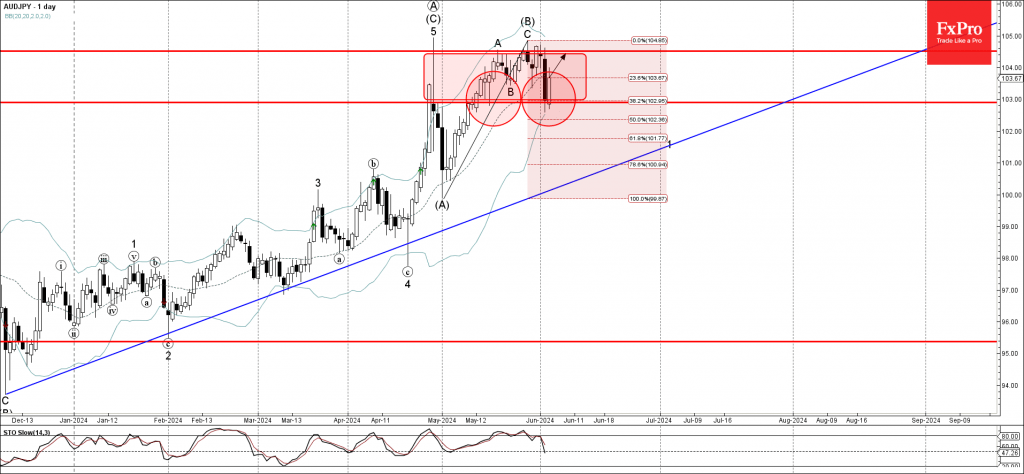

AUDJPY Wave Analysis

- AUDJPY reversed from support level 103.00

- Likely to rise to resistance level 104.50

AUDJPY currency pair recently reversed up from the key support level 103.00 (which has been reversing the price from the middle of May).

The support level 103.00 was strengthened by the lower daily Bollinger Band and by the 38.2% Fibonacci correction of the upward impulse from end of April.

Given the strength of the support level 103.00 and the clear daily uptrend, AUDJPY currency pair be expected to rise further to the next resistance level 104.50, which stopped the previous waves A and (B).

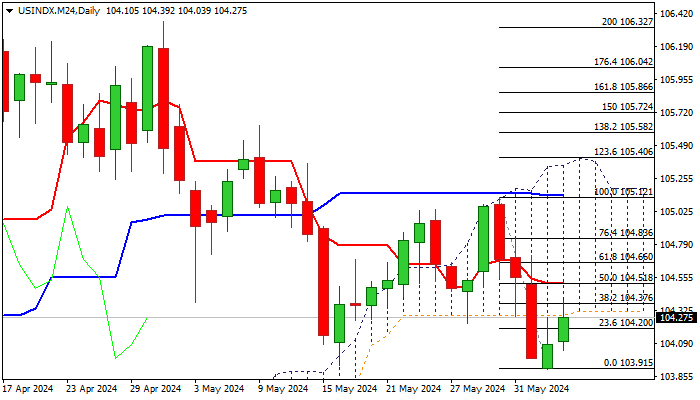

DXY: Upbeat US Services PMI Data Provide Fresh Support to Greenback

The dollar index accelerated higher on Wednesday, following much stronger than expected US services PMI data (May 53.8 vs 51.0 f/c and Apr 49.4) which signaled that services sector returned to growth (May figure hit the highest in nine months) and offset negative signals from downbeat labor reports (JOLTS and ADP).

Fresh advance cracked strong barriers in the 104.24/37 zone (converged 100/200DMA’s / base of thick daily cloud / Fibo 38.2% of 105.12/103.91 bear-leg) but needs close above these levels to confirm initial reversal signal, generated by Tuesday’s inverted hammer candlestick.

Sustained break higher to expose next pivot at 104.51 (50% retracement / 10DMA) and open way for further recovery on violation.

Caution on possible recovery stall, as 14-d momentum is still in the negative territory and a massive daily clouds weighs.

Res: 104.77; 104.51; 104.66; 104.83

Sup: 104.20; 103.91; 103.82; 103.65

Could Stronger US Data Force a Fed Rate Cut?

- Markets crave weaker US data to support their rate cut expectations

- Strong data this week could cause an acute market reaction

- The Fed might find it easier to act if financial stability is under threat

The key question in the market participants’ minds is when the Fed is going to start easing its monetary policy stance. The year started with the market pricing in at least five rate cuts by the Fed in 2024, but with inflation remaining above 3% since July 2023, expectations have tanked.

With the ECB expected to cut rates this week and the BoE possibly following suit in early August, the pressure is on the Fed to turn dovish and cut rates in September ahead of the November US Presidential elections. Otherwise, it might have to wait until December when either the Fed would potentially be significantly behind the curve, or the US economy might not need a more accommodative monetary policy stance.

Two main reasons for Fed to cut rates

Based on the Fed's mandate, there are two key reasons for the Fed to start cutting rates: (a) weak economic data, and particularly lower inflation, and (b) a severe risk-off episode in stock markets that threatens the stability of the system.

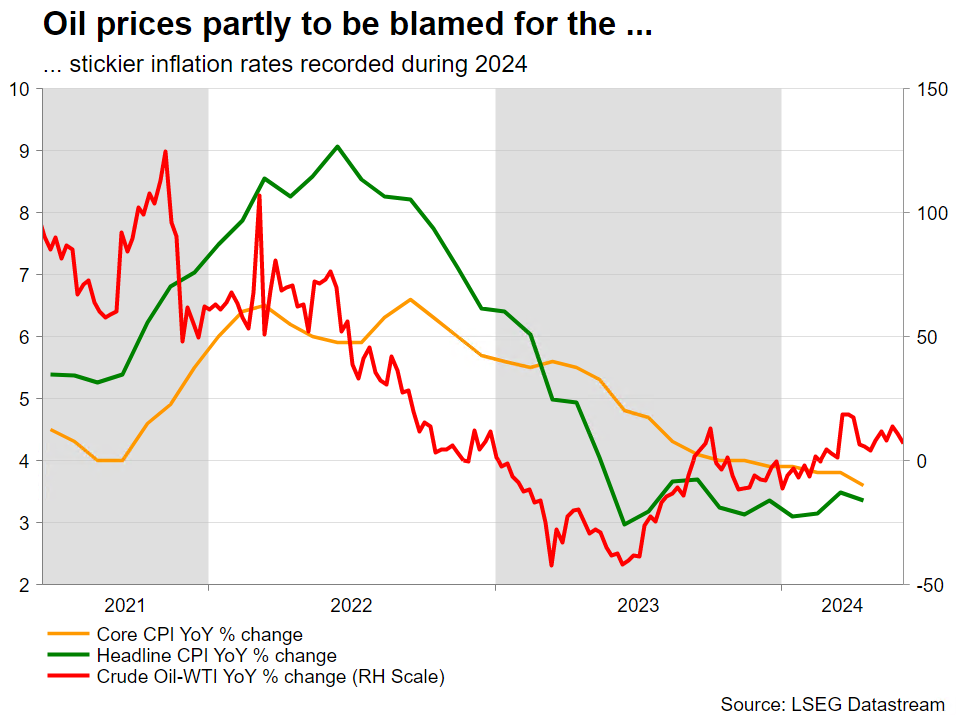

(a) Oil prices and US domestic demand hold the key for lower inflation

Higher inflation during 2024 has been attributed to the elevated oil prices and the strong domestic demand. Encouragingly for the Fed doves, oil prices have suffered severe selling in the past few sessions and hence opened the door to lower inflationary pressures ahead.

Similarly, increased wage earnings have been fuelling consumer appetite and cancelled out most of the impact of the higher cost of money. However, both the consumer confidence index and the University of Michigan consumer sentiment survey have been recently showing signs of weakness.

Focusing on this week's key data calendar and an array of weaker prints, for example a sub-100k increase in non-farm payrolls led by weaker private payrolls, and a decent jump in the unemployment rate, could increase exponentially the pressure on the Fed to turn dovish at next week's gathering and prepare for a rate cut in September.

(b) US yields, stock markets matter for the Fed

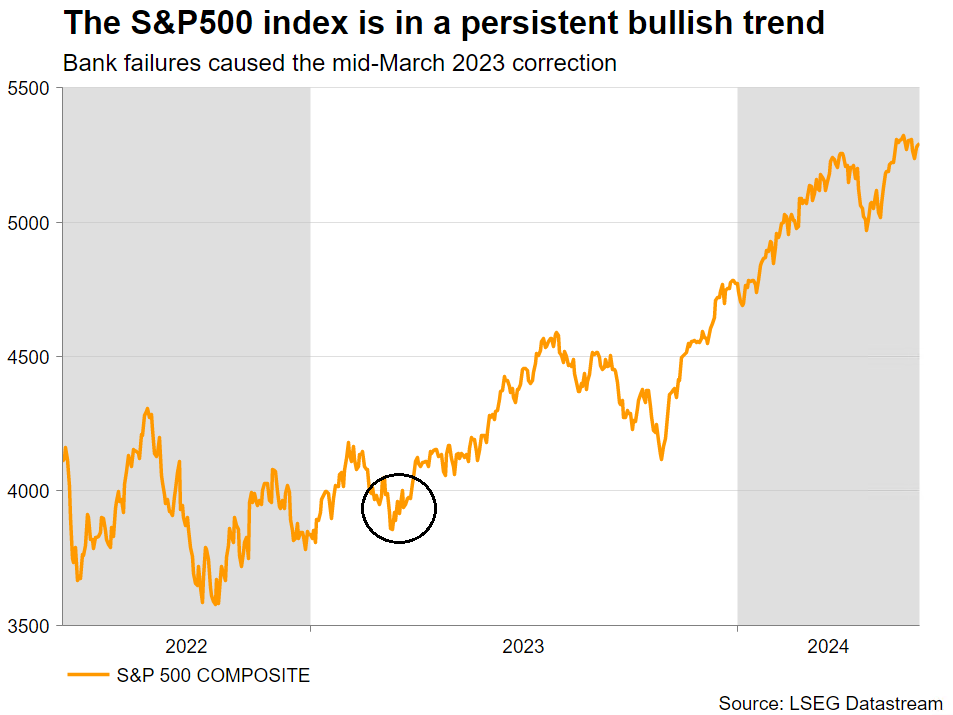

Financial stability is taken very seriously by the Fed, especially following the March 2023 events with the failure of three mid-sized banks. Therefore, another unexpected surge in US yields, on the back of stronger US data, is bound to increase the Fed members’ concerns about similar bank failures.

Similarly, the Fed does not enjoy massive risk-off episodes that cause acute stock market moves. Seasoned market participants are aware of the famous “Fed put” - the belief that the Fed would step in and act appropriately to limit the stock market's decline.

Data this week has significant market-moving potential. A strong set of prints on Friday, for example a sizeable upside surprise in the non-farm payroll figures and a jump in average earnings, could trigger a stock market correction, which could gradually evolve into a crash as market participants realize that the chances of a rate cut before December are extremely low.

In this case, Fed officials might be forced to react by delivering the much-awaited rate cut much faster than currently foreseen, and despite the recent economic data not fully justifying such a move.

Therefore, while intuitively a weaker set of data this week opens the door to a dovish tilt at the June meeting, a very strong set of data prints could push US treasury yields much higher and gradually result in a severe stock market correction. Maybe the threat of financial instability could be the catalyst that the Fed doves have been waiting for.

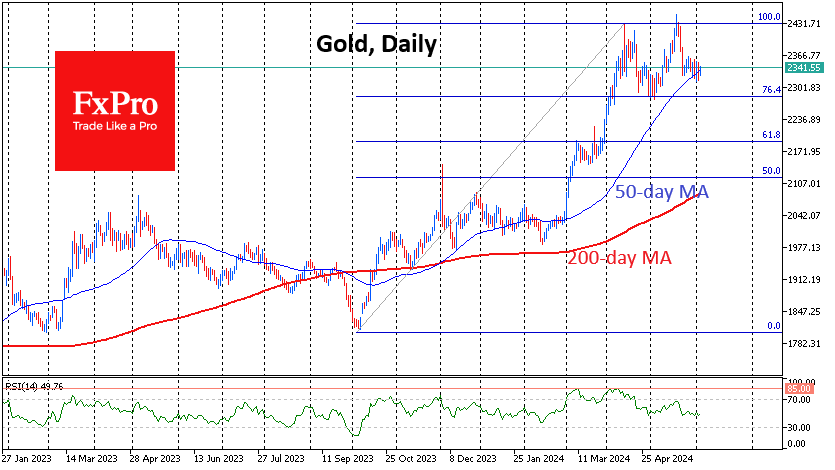

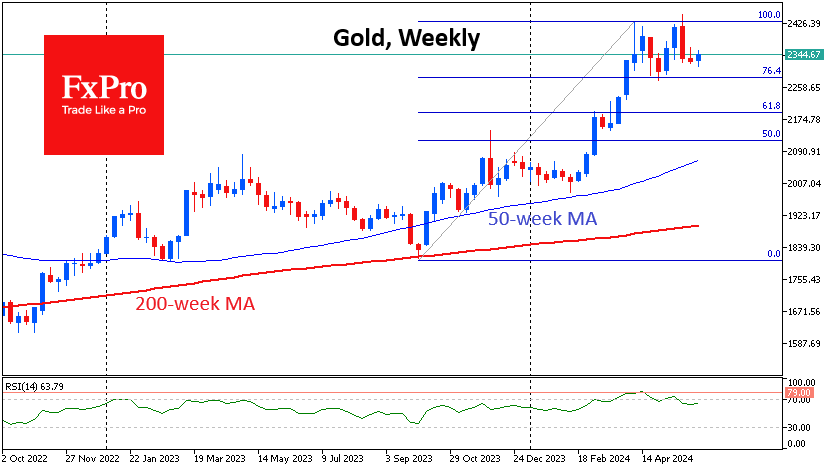

Gold: Moonshot to $2800 or Dive Below $2000?

Gold volatility has fallen markedly in recent days as gold traders consider their next move, while many commodities are in a corrective decline.

In May, the gold price climbed towards $2450, above the peaks of April, but failed to consolidate near all-time highs. During the last two weeks, the price has changed in the range of $2330-2360, with a slight downward trend, which can be seen on the daily candlestick charts.

Right now, Gold has dropped to support in the form of the 50-day moving average, which is enjoying temporary interest from short-term buyers. The 50-day moving average has been effectively acting as uptrend support since last October.

It is easy to see the result of this support as the prices of other actively traded metals (silver, platinum, copper) have been steadily losing ground for the past week. But there is no guarantee that this will continue.

Further declines in prices for raw material assets may cause bulls in Gold to capitulate. This fight for the trend is in full swing.

The first signal that the bullish trend is breaking would be a sustained price drop below $2320. It is also worth closely watching the behaviour of Silver and Platinum. Their further plunge could tip the scales in Gold towards the sellers. A full-fledged correction could bring the gold price back to $2000 or lower before it becomes interesting for long-term buyers again.

However, it cannot be ruled out that Gold will be able to withstand the sell-off in related assets and subsequently pull them back up, as it did in January. Such a turn of events would trigger a scenario of gold growth with the potential to take the price to the area of $2800. And it could be quite an aggressive fast rally rather than a smooth climb.

Sunset Market Commentary

Markets

The US 10-yr yield tested 4.31% support after a small miss in May ADP employment change. The US economy added 152k jobs (vs 175k expected) with April figures marginally downwardly revised to 188k (from 192k). The deviation wasn’t big enough to trigger a strong market reaction both because of the solid nature of the job gain and because of the Treasury rally we’ve already had over the past four trading sessions. The chief economist at ADP nevertheless warned that job gains and pay growth are slowing going into the second half of the year with some pockets of weakness already visible tied both to producers and consumers (eg manufacturing firms cut 20k jobs). Wage growth for workers who changed jobs slowed for the second month (to 7.8% Y/Y) while it stayed at 5% Y/Y for those who remained in their job. EUR/USD easily held below the 1.09 resistance area after the ADP, even as risk sentiment turned outright risk-on as well today. Main European stock markets rise up to 1.8% for the EuroStoxx 50.

The Bank of Canada’s first policy rate cut this cycle (4.75% from 5%) triggered a second test of US support levels. BoC governor Macklem said that it is reasonable to expect further cuts if inflation eases. The BoC is seen as a frontrunner in the monetary policy cycle. The test was blocked by a consensus-beating US services ISM. The ISM rebounded from 49.4 (only second monthly <50 outcome since start of Covid-pandemic) to 53.8 vs a consensus estimate of 51. Details showed a welcome acceleration in new orders (54.1 from 52.2) while price pressures remain elevated (58.2 from 59.2). Jobs were lost, though at a slower pace than in April (47.1 from 45.9). Daily changes across US and German yields curves are currently limited to -1 bp.

News & Views

Czech April retail sales disappointed. They stagnated (except motor vehicles) compared to March to be up 5.3% Y/Y. Sales of non-food goods rose marginally (0.1% M/M) while sales of food (-0.2%) and automotive fuels (-0.3%) declined in a monthly perspective. Compared to the same month last year, retail trade grew 5.3%, with sales of non-food items 7.1% higher, food sales adding 3.6% and automotive fuels rising 3.9%. Despite a rather slow momentum in retail sales in April, consumer spending is still seen as an important driver for Czech growth further out this year. Solid (real) wage growth data (7% Y/Y nominal, 4.8% Y/Y real) published yesterday in this respect provide hope that the decline in inflation will support Czechs’ real spending capacity. Higher real wage growth and potentially higher domestic spending also support the case for the Czech national bank (CNB) to keep a cautious approach on policy easing. We expect the CNB to slow the pace of rate cuts from this month’s meeting and proceed at this slower pace at the meetings in H2. The risk even is for the CNB to take a pause in its easing cycle toward the end of the year. After rallying from the EUR/CZK 25.40 area to the 24.70 area, the Czech koruna recently settled in a tight sideways range. Still it outperformed regional pears (forint and zloty).

PPI producer prices in EMU in April declined for the sixth consecutive month, easing 1% M/M after a decline of 0.5% in March. Due to less favorable base effects, producer price deflation slowed from -7.6% Y/Y to -5.7%. At first sight this looks still promising for the easing in CPI inflation, too. However, as was the case in many of the previous months, the disinflation process was solely driven by a decline in energy prices (-3.6% M/M from -2.3% M/M in March). PPI ex energy (0.2% M/M) rose for the fourth consecutive month. Prices for intermediate goods (0.3%), capital goods (0.2%), durable consumer goods (0.2%) and non-durable goods (0.1%) all printed in positive territory. In this respect, the PPI data suggest that the deflationary contribution from goods price from last year might be coming to an end.

Graphs

EUR/PLN: zloty awaits tomorrow’s press conference by NBP governor Glapinski after they kept the policy rate unchanged today at 5.75%

EuroStoxx50 rallies back towards cycle high as the impact of growth worries on risk sentiment again proves to be short-lived

USD/CAD: Loonie underperforms after 25 bps rate cut by the BoC with more to come

US 10-yr yield: 4.31% support survives for now, thanks to stronger services ISM

Bank of Canada Cuts Its Policy Rate to 4.75%!

The Bank of Canada cut the overnight rate to 4.75% (from 5.0%), while stating that it will continue with Quantitative Tightening (QT).

The Bank spoke confidently about the economy, stating "economic growth resumed in the first quarter of 2024 after stalling in the second half of last year." It highlighted that "consumption growth was solid at about 3%, and business investment and housing activity also increased. Labour market data show businesses continue to hire, although employment has been growing at a slower pace than the working-age population. Wage pressures remain but look to be moderating gradually. Overall, recent data suggest the economy is still operating in excess supply."

On the inflation outlook, the BoC sounded encouraged, stating "CPI inflation eased further in April, to 2.7%. The Bank’s preferred measures of core inflation also slowed and three-month measures suggest continued downward momentum. Indicators of the breadth of price increases across components of the CPI have moved down further and are near their historical average."

On the future path of policy, the Bank revealed that "with continued evidence that underlying inflation is easing, Governing Council agreed that monetary policy no longer needs to be as restrictive."

Key Implications

Like that one neighbour who has let their yard become overgrown, the BoC has heard the complaints and decided to bring out its policy trimmers to cut rates. Even though the central bank hadn't signaled an intention to cut ahead of today's meeting, the recent softening in inflationary pressures was enough to convince it that now was the time. As our readers know, we have been arguing that the foundation for rate cuts has been in place for all of 2024. And while the BoC has waited longer than we would have hoped, today starts the process of lower interest rates for Canadians going forward.

We believe that the path forward for the BoC is going to be slow. It has acknowledged that the economy doesn't need such high interest rates any longer. At the same time, it will proceed cautiously. It must ensure that inflationary pressures don't rebound like they have in the U.S. in recent months. It also doesn't want to reignite the housing market, where prospective buyers have been waiting for greater interest rate certainty. We expect the BoC is on a cut-pause-cut path, with the next cut likely occurring in September. This outlook will cause the BoC to diverge significantly from the Fed, which is likely to put greater pressure on the loonie over the coming months.