Sample Category Title

USDCAD: Influence of Linear Regression Channel and BoC

- Bullish Scenario: Buy above 1.3676 with TP1: 1.3699, TP2: 1.3720, and TP3: 1.3735, with an SL below 1.3665 or at least 1% of account capital. Apply trailing stop.

- Bearish Scenario: Sell below 1.3665 with TP1: 1.3623, with an SL above 1.3686 or at least 1% of account capital.

Fundamental Analysis

The BoC has maintained its official interest rate at 5.0% since July 2023, and markets expect it to cut its overnight rate by 25 basis points (bps) to 4.75% due to signs of cooling inflation in Canada. This decision will highlight the monetary policy divergence between the BoC and the Fed, potentially boosting the USD.

On the US side, recent PCE inflation data, ISM manufacturing PMI, and employment surveys below expectations have increased speculation that the Fed will need to cut rates at least once between September and December to sustain economic growth.

Technical Analysis

USDCAD

- Average Daily Range High (ADR High): 1.3730

- Average Daily Range Low (ADR Low): 1.3619

- Supply Zones (sell): 1.3720 / 1.3735

- Demand Zones (buy): 1.3627

Price consolidation above macro demand zones and in the positive territory of a linear regression channel from April highs suggest a bullish scenario.

Bullish Continuation:

This scenario will be considered with quotes above the daily open and the Asian POC at 1.3676, targeting a break of resistance at 1.3690 towards the supply zone between 1.3720 and 1.3735. This indicates a strengthening of the bulls aiming to renew the uptrend seen in early April.

Bearish Extension:

A pullback below 1.3668 towards the midpoint of the regression channel, coinciding with a volume node from yesterday's ascent around 1.3637, is not ruled out before the BoC rate announcement. The bullish momentum is preserved if quotes do not break the demand zone at the weekly open of 1.3623. If this level is breached, selling could extend towards the next demand zone at 1.3613, potentially challenging the key support at 1.3603.

POC Explained: POC = Point of Control: It is the level or zone where the highest concentration of volume occurred. If there was a previous downward movement from this level, it is considered a sell zone and forms a resistance area. Conversely, if there was a previous upward movement, it is considered a buy zone, usually located at lows, forming support zones.

AUD Shrugs as Australian GDP Misses Estimate

After starting the week with sharp swings, the Australian dollar is showing little movement on Wednesday. AUD/USD is trading at 0.6644 in the European session, down 0.06% on the day.

Australian GDP posts 0.1% growth

Australia’s GDP was a disappointment, with a gain of just 0.1% q/q in the first quarter. This was lower than the revised 0.3% gain in Q4 2023 and below the market estimate of 0.2%. This marked the lowest growth in six quarters due to weak domestic demand and a decline in net trade. Yearly, GDP grew by 1.1% in the first quarter, the weakest level since the fourth quarter of 2020.

How will the Reserve Bank of Australia view the soft GDP release? The RBA is hamstrung between stubbornly high inflation and a weakening economy, as today’s GDP indicated. The RBA has maintained the cash rate at 4.35% since last November and Governor Bullock reiterated on Wednesday that a rate hike is a possibility. Bullock told a Senate committee that if inflation stalled, the RBA “won’t hesitate to move and raise interest rates again”.

The GDP data is unlikely to prod the RBA to cut rates but will dampen expectations of a rate hike. This could mean that the RBA will hold rates into 2025 until policy makers are confident that inflation is firmly under control.

In China, the Caixin Services PMI improved to 54.0 in May, up from 52.5 in April and beating the market estimate of 52.6. This was the fastest pace of expansion in services since July 2023, driven by stronger domestic and external demand. Economic developments in China can have a significant impact on the Australian dollar, as China is Australia’s largest trading partner.

AUD/USD Technical

- AUD/USD continues to test support at 0.6641. Below, there is support at 0.6603

- 0.6692 and 0.6730 are the next resistance lines

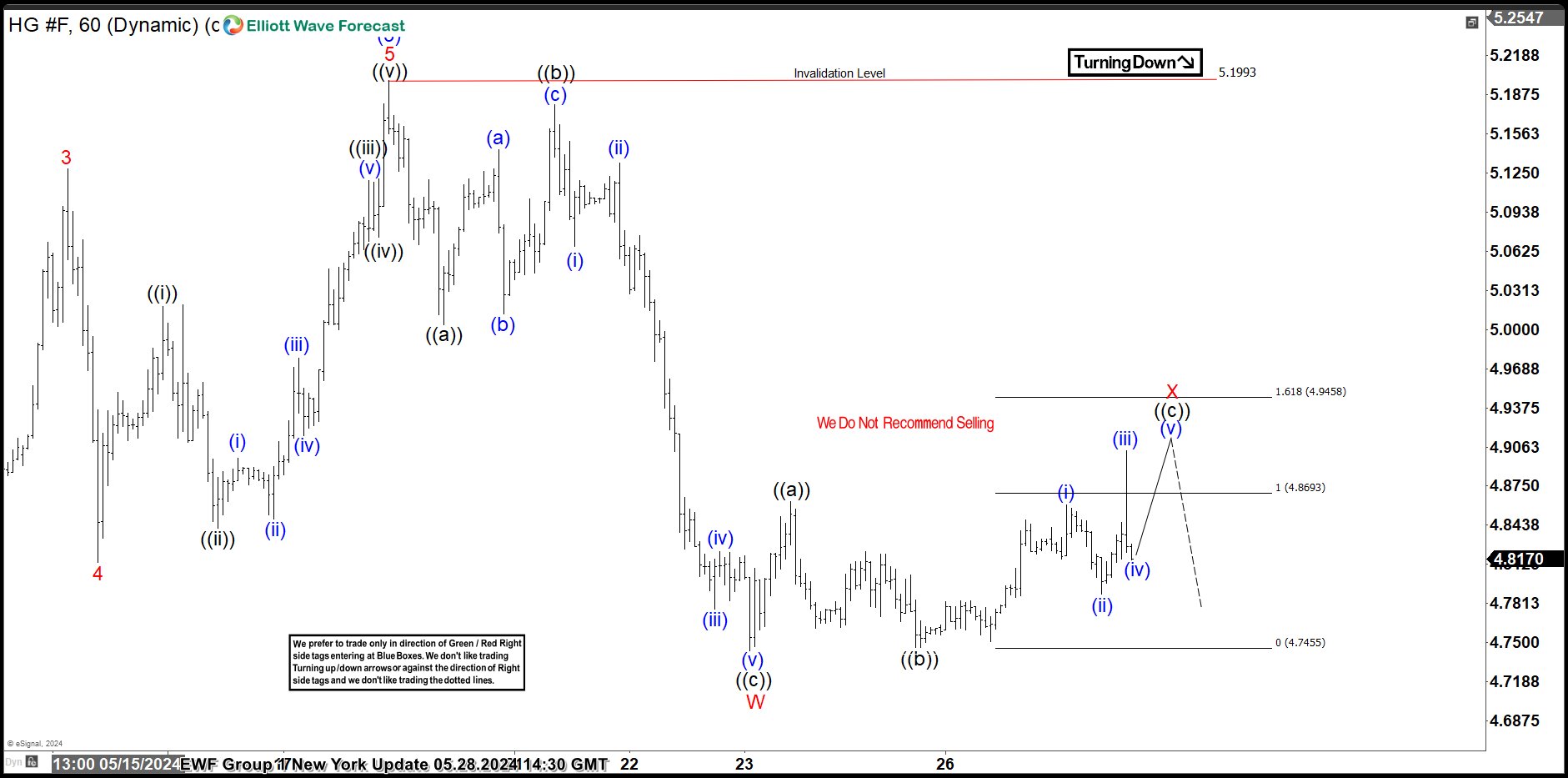

Copper Elliott Wave Analysis: Shorter Cycles Expect Further Decline

Hello traders. Welcome to a new commodity blog post. In this one, we will look at the Copper Elliott wave analysis from our team of analysts. We will especially look at an Elliottwave path discussed in of one of our updates shared with members of ElliottWave-Forecast in May 2024. In conclusion, we will discuss how we will look for the next trade setup on this commodity. Aside from Copper, members get regular Elliott wave updates – five times a day, on 77 other instruments.

In the long term, Copper shows an impulse wave bullish sequence. The intermediate degree impulse wave structure, i.e., (1)-(2)-(3)-(4)-(5), started in October 2023. The price advanced from 3.518 in October 2023 to 5.199 in May 2024. At that high, we recognized that wave (3) of the impulse had been completed. We started analyzing the price action that followed. Our focus was more on the shorter cycles on the H1 and 30-minute charts as we could identify a bearish path in the direction of wave (4) pullback on the higher time frame. On May 23, at 4.7435, we identified wave W of (4). Over a month later, wave X was evolving into a zigzag structure, and we shared the chart below.

Copper Elliott Wave Analysis – $HG_F, 05.28.2024Copper Elliott Wave Analysis

On May 28, 2024, we shared the chart above with members identifying the extreme zone where wave X should be resisted. The short-term sellers are expected to gain control and drive prices lower for wave Y of (4). From the next day, wave X found resistance as we expected, and the sell-off resumed.

Copper Elliott Wave Analysis – $HG_F, 05.30.2024

We shared the chart above with members two days later. The essence was to emphasize that wave (4) has not yet concluded for buyers to re-enter. We reckoned that the wave ((a)) of Y of (4) could be around the completion stage, paving the way for another bounce for ((b)). In that case, shorter cycles support further decline until wave Y of (4) has concluded. We already have an extreme zone in sight where we expect wave (4) to complete and attract buyers for wave (5). When wave (5) begins, shorter cycles will support buying the pullbacks in 3, 7, or 11 swings.

Crypto Goes Up After a Rest

Market picture

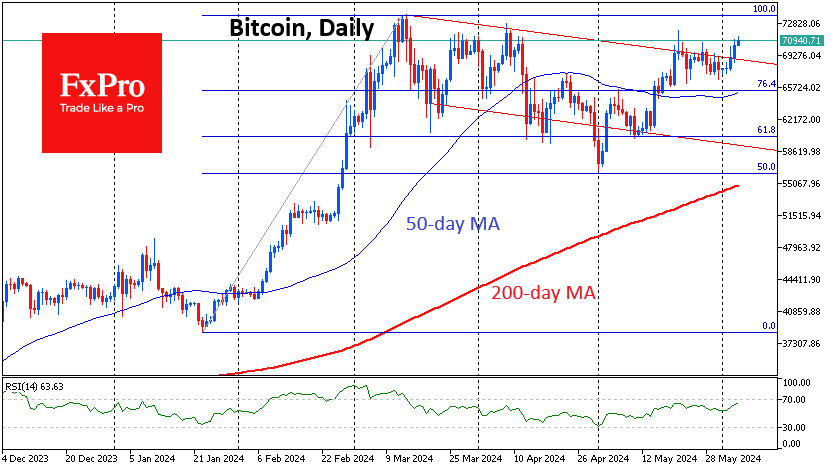

Crypto market capitalisation rose by 2.9% in 24 hours to $2.63 trillion. Among the top coins, BNB is up an impressive 11%, and Solana is up 5%. Altcoins have steadily been gaining strength over the last few days of downtime.

Active buyers came to Bitcoin, raising the price by 4.4%. The price of the first cryptocurrency again exceeded $71K, returning to the area of last month’s highs and the pivotal area of the last three months. Technically, Bitcoin has already broken the resistance of the descending channel and is testing horizontal resistance. The ability to go above $71K opens the way for a renewal of historical highs, which could happen very quickly.

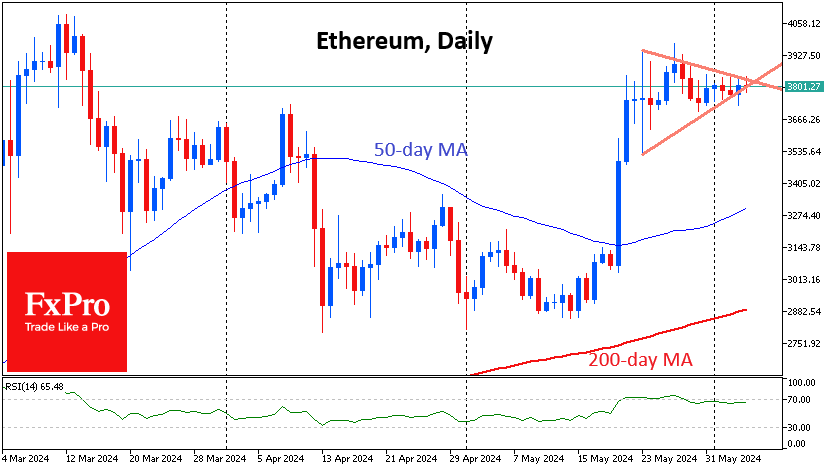

Interestingly, Bitcoin’s positive dynamics did not help Ethereum to get out of its triangle. The price has already reached its top at $3800, which promises an imminent burst of volatility but does not give a direct indication of the direction.

News background

According to BitcoinTreasuries, the total volume of bitcoin products held by the ETF reached 1,035,233 BTC ($71.4bn), equivalent to 4.93% of the digital gold issue.

After bitcoin crossed the $70K level, more than half of the coins remained inactive, indicating long-term confidence in the asset, CryptoQuant noted. Long-term holders’ sales have driven Bitcoin’s decline since March. According to Bitfinex’s on-chain analysis, the trend has slowed, with investors shifting to hoarding coins.

Deribit noted that the current values of the implied volatility of Bitcoin and Ethereum options indicate expectations of a calm situation in the cryptocurrency market in the coming weeks.

According to The Block, 455,000 new coins appeared on the Solana blockchain in May. The figure reached a one-month high due to low barriers to entry and hype around meme tokens. According to CoinGecko, the segment has a market capitalisation of $9.4bn, with dogwifhat (WIF) and Bonk (BONK) being the largest assets.

Tether co-founder Brock Pierce is convinced that the Chinese government will lift the 2021 ban on cryptocurrency mining and trading. According to him, it is a matter of when, not if.

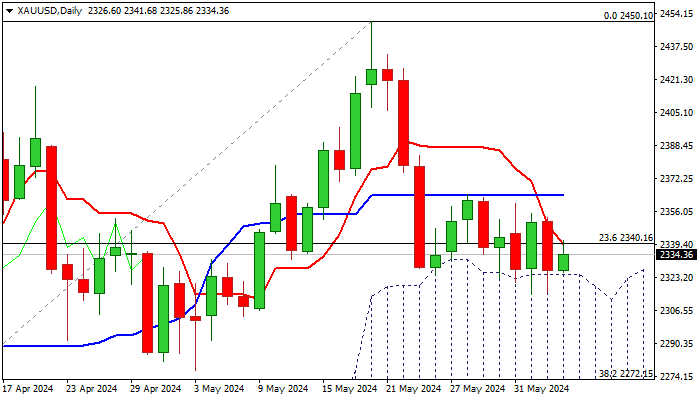

XAU/USD: Key Economic Events This Week Eyed for Fresh Direction Signals

Gold price edges higher early Wednesday, bouncing off the floor of near term range and remaining without clear direction as markets await fresh signals from key economic events this week.

Conflicting technical indicators on daily chart contribute to near term sideways mode, though slight bullish bias to persist as long as the price stays above the top of thick daily Ichimoku cloud ($2324) which contained several attacks in past two weeks, marking significant support.

On the other hand, the price is weighed down by negative 14-d momentum and Tenkan/Kijun-sen bear cross.

US services PMI will be in focus today (f/c 49.4 Apr) and if May figure remains below 50 threshold, it will be positive signal for gold.

A series of reports from the US labor sector commenced with release of JOLTS job openings report on Tuesday (Apr figure dropped well below forecast / previous release and hit the lowest in over two years).

Markets await release of US ADP private sector payroll, due later today (173K f/c vs 192K Apr) and top economic event of the week – US nonfarm payrolls (due on Friday, May 185K f/c vs Apr 175K).

Overall stronger labor data would signal further delay in Fed’s first rate cut (probably to be shifted to November) and generate negative signal for the yellow metal, while signals of weakening US labor sector would add to expectations for the first rate cut in September, which would deflate dollar.

Look for initial direction signals on form break of daily cloud top ($2324 – bearish) od daily Kijun-sen / recent range top ($2363 – bullish).

Res: 2345; 2363; 2382; 2398.

Sup: 2324; 2300; 2272; 2222.

Eurozone PPI down -1.0% mom, -5.7% yoy in Apr

Eurozone PPI fell -1.0% mom in April, below expectation of -0.5% mom. Over the 12-month period, PPI fell -5.7% yoy, below expectation -5.1% yoy. For the month, industrial producer prices increased by 0.3% for intermediate goods, 0.2% for capital goods, 0.2% for durable consumer goods, 0.1% for non-durable consumer goods. PPI decreased by -3.6% for energy.

EU PPI fell -0.1% mom, -5.5% yoy. The largest monthly decreases in industrial producer prices were recorded in France (-3.6%), Croatia (-1.9%) and Greece (-1.8%). The highest increases were observed in Denmark (+2.8%), Ireland (+0.8%) and Finland (+0.3%).

UK PMI services finalized at 52.9, expansion slows, price pressures ease

The latest PMI data from the UK indicates a deceleration in the service sector for May, with the Services PMI dropping to 52.9 from April's 55.0, marking the slowest growth rate since November. The Composite PMI, which aggregates both services and manufacturing, also experienced a downturn, finishing at 53.0 compared to 54.1 the previous month.

Joe Hayes, Principal Economist at S&P Global Market Intelligence, provided insights into the broader implications of these figures, stating that the PMI survey reflected a "reasonable rate of expansion" in the UK service sector. Coupled with data from the manufacturing sector, the PMIs collectively suggest an approximate GDP growth of around 0.3% for the second quarter.

A significant development from the PMI surveys is the moderation in price increases for UK services, which have risen at the slowest pace in over three years. This marks the third consecutive month of diminishing selling price inflation in the service sector, a trend that will likely be welcomed by BoE. According to Hayes, this trend suggests that "the trajectory of services prices is moving in the right direction," potentially easing concerns about persistent inflationary pressures.

Eurozone PMI composite finalized at 52.2, a 12-month high

Eurozone PMI Services was finalized at 53.2 in May, slightly down from April's 53.3. PMI Composite was finalized at 52.2, up from prior month's 51.7, a 12-month high. Also, business confidence surged to 27-month high. Inflation rates cooled but remained above pre-pandemic averages.

A closer look at individual countries reveals varying levels of economic activity. Spain leads with a robust Composite PMI of 56.6, marking a 14-month high. Germany follows with a Composite PMI of 52.4 and hitting a 12-month peak. Conversely, Italy's PMI dipped to a three-month low of 52.3, and France lagged with a Composite PMI of 48.9 and marking a two-month low.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, commented on the broader implications of these figures: "The spectre of recession is off the table." He highlighted the crucial role of the service sector in driving this positive shift, noting, "In Germany, we can now talk of an upward trend, Italy's business activity remains solid, and Spain has improved from an already strong position." However, he also acknowledged the challenges facing France, which has seen a recent dip in economic performance.

NZDUSD Extends Recovery to Fresh Highs

- NZDUSD posts an almost 3-month high on Tuesday

- But the risk of an impending correction increases

- Oscillators approach overbought conditions

NZDUSD has been in an aggressive uptrend following its 2024 bottom of 0.5851 in mid-April. On Tuesday, the pair stormed to its highest level since March 8 before sustaining minor losses probably due to some profit taking.

Should the bulls attempt to push the price higher, immediate resistance could be found at the February-March double top region of 0.6215. A violation of that zone could pave the way for 0.6257, which is the 78.6% Fibonacci retracement of the 0.6368-0.5851 downleg. Failing to halt there, the pair may challenge the December 2023 high of 0.6368.

On the flipside, if the recovery falters, the 61.8% Fibo of 0.6170 could prevent initial declines. Sliding beneath that floor, the price could descend towards the 50.0% Fibo of 0.6109. Even lower, the 38.2% Fibo of 0.6048 could prove to be the next barricade for the bears to overcome.

Overall, NZDUSD has been in a recovery mode for more than a month now, generating a clear structure of higher highs. However, the risk of a pullback is present considering that the short-term oscillators are approaching overbought levels.

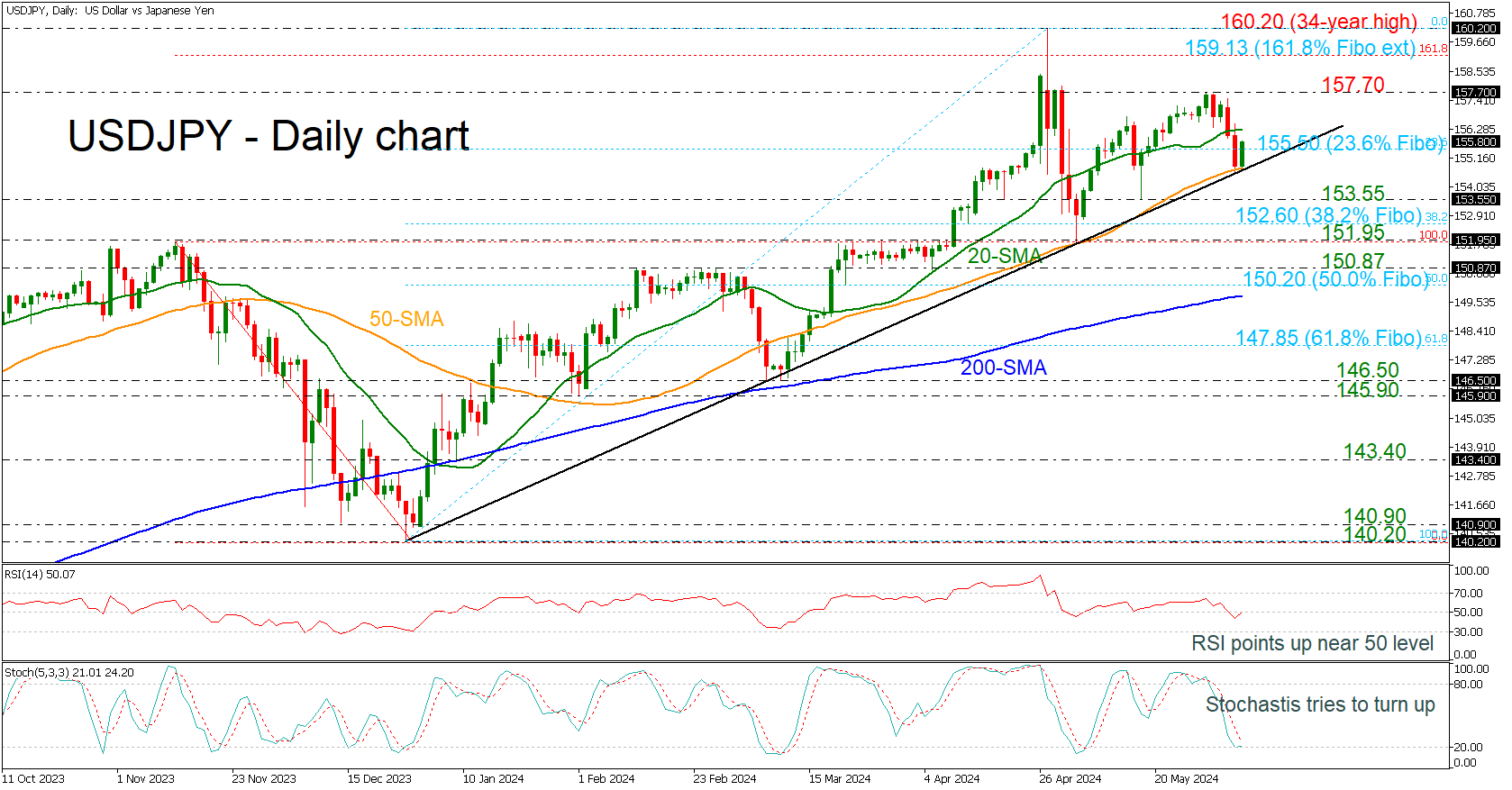

USDJPY Recoups Losses After Bounce Off Rising Line

- USDJPY heads north with first resistance at 20-day SMA

- RSI and Stochastics confirm upside movement

USDJPY has reversed back up again after the strong rebound off the medium-term uptrend line and the 50-day simple moving average (SMA), meeting the 23.6% Fibonacci retracement level of the up leg from 140.20 to 160.20 at 155.50.

Momentum indicators are pointing to a positive bias in the short term with the RSI crossing above the neutral threshold of 50, while the stochastic oscillator is trying to turn higher as it bounced off the oversold region.

In the event of more upside pressure, the 20-day SMA at 156.30 could act as immediate resistance ahead of the previous peak of 157.70. Even higher, the 161.8% Fibonacci extension level of the down leg from 151.95 to 140.20 at 159.13 could be a key level for traders before flirting with the 34-year top of 160.20.

In the negative scenario, a dive beneath the valid ascending trend line could send the pair towards the 153.55 support and the 38.2% Fibonacci of 152.60. A drop lower could erase the latest upward wave, touching the 151.95 and 150.87 levels.

All in all, USDJPY is confirming the upside tendency after the recent upside pullback and only a plunge below the 200-day SMA could switch the outlook to negative.