Sample Category Title

Bearish Elliott Wave Sequence in Dollar Index (DXY) Favors Downside

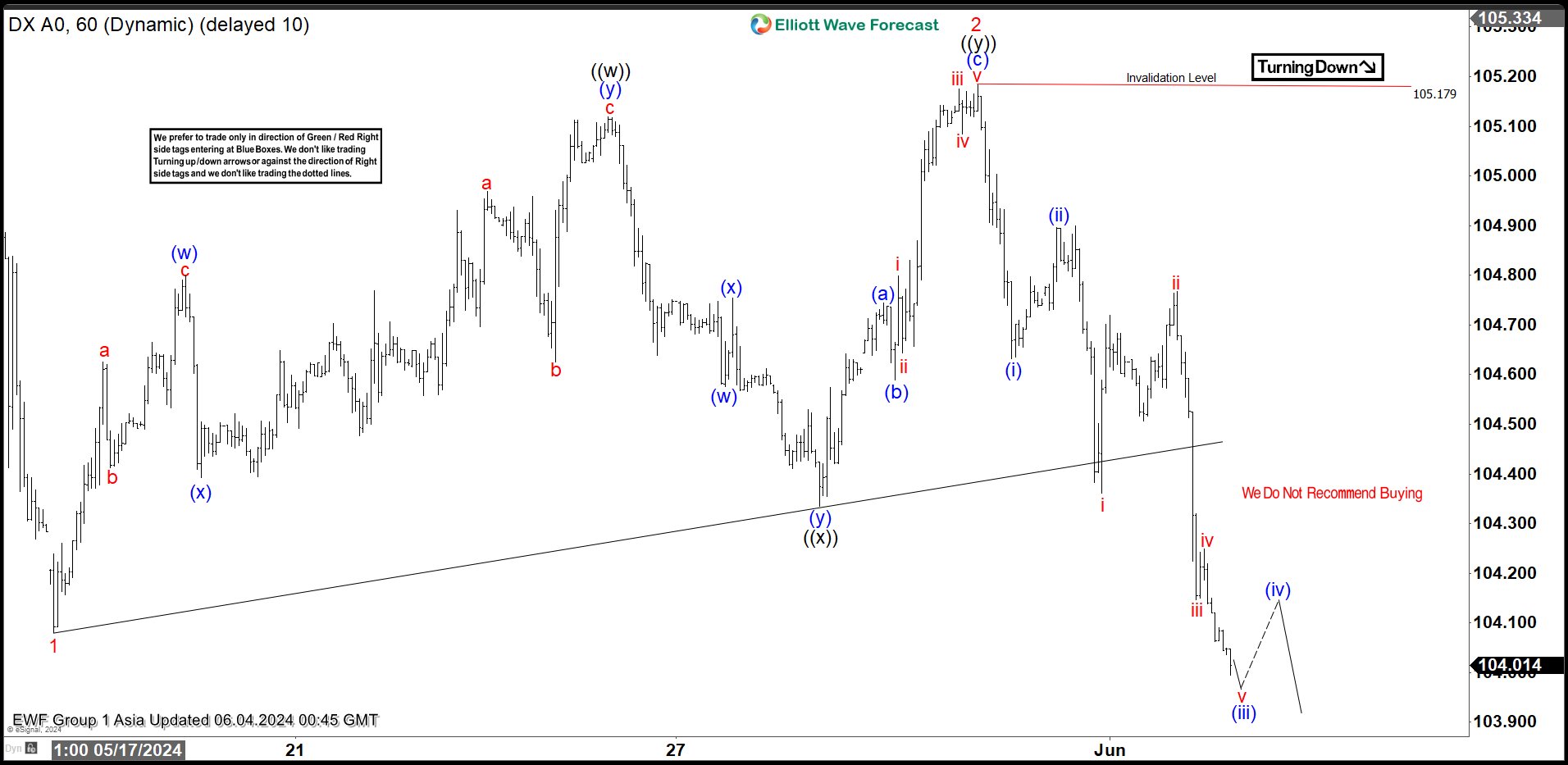

Short Term Elliott Wave in Dollar Index (DXY) shows incomplete bearish sequence from 4.17.2024 high. Down from there, wave 1 ended at 104.08 like the 1 hour chart below shows. Rally in wave 2 unfolded in a double three Elliott Wave structure. Up from wave 1, wave (w) ended at 104.79 and dips in wave (x) ended at 104.39. Wave (y) higher ended at 105.12 which completed wave ((w)) in higher degree. Pullback in wave ((x)) ended at 104.33 and rally in wave ((y)) ended at 105.18 which completed wave 2 in higher degree.

The Index has turned lower in wave 3. Down from wave 2, wave (i) ended at 104.63 and wave (ii) rally ended at 104.89. The Index then nested lower with wave i of (iii) ended at 104.36. Wave ii of (iii) ended at 104.76. The Index extended lower in wave iii towards 104.14 and wave iv ended at 104.25. Wave v lower ended at 103.99 which completed wave (iii). Near term, as far as pivot at 105.18 high stays intact, expect short term rally to fail in 3, 7, or 11 swing for further downside.

Dollar Index (DXY) 60 Minutes Elliott Wave Chart

DXY Elliott Wave Video

https://www.youtube.com/watch?v=mj6ZGzX4NyU

Oil Prices Dive: Is a Rebound on the Horizon?

Key Highlights

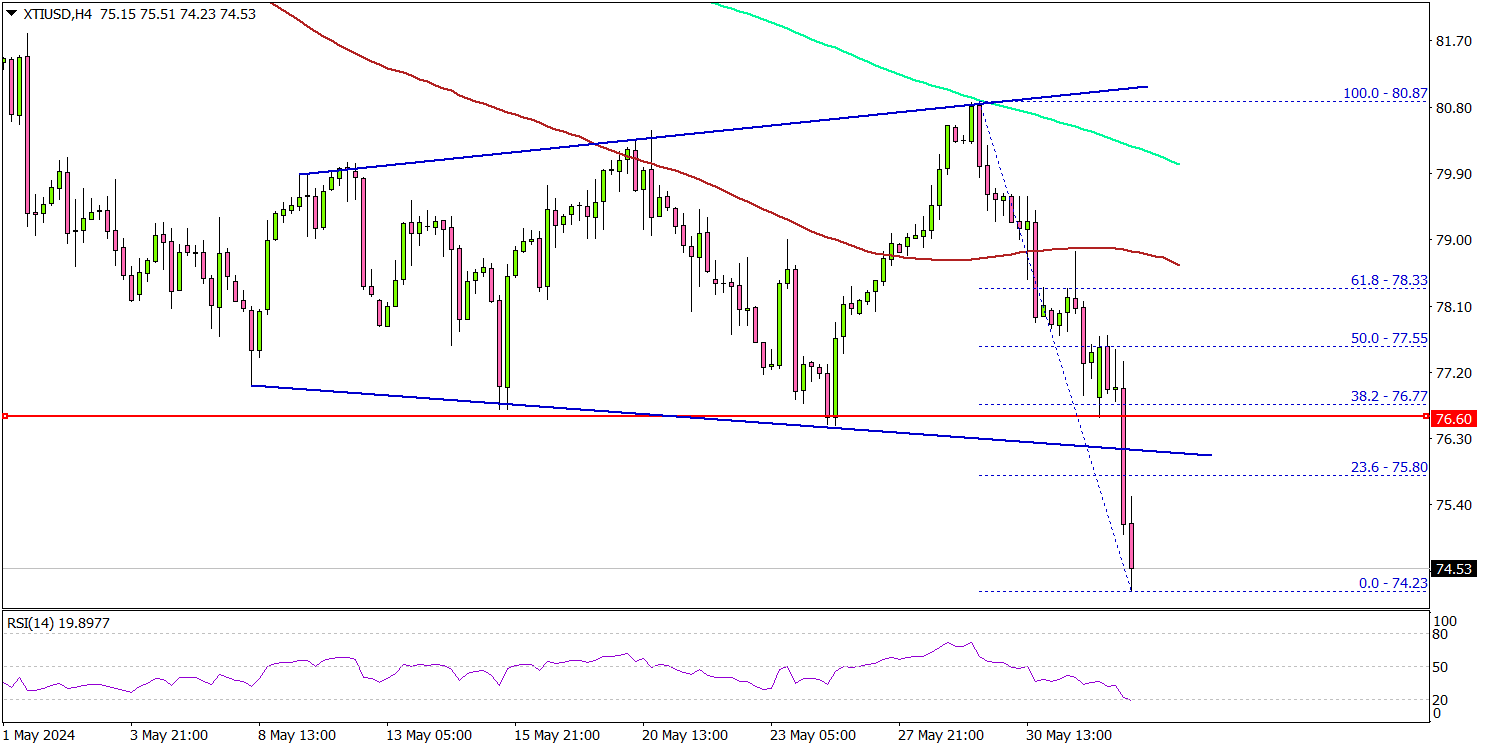

- Crude oil prices extended losses below the $76.80 support.

- There was a break below a key expanding triangle with support at $76.20 on the 4-hour chart.

- GBP/USD gained pace for a move above the 1.2750 resistance.

- EUR/USD shows positive signs for a move toward the 1.0950 resistance.

Crude Oil Price Technical Analysis

In the past few days, Crude oil prices saw a major decline below the $78.00 zone. The price dipped below the $76.80 and $76.20 support levels.

Looking at the 4-hour chart of XTI/USD, the price even settled below the 200 simple moving average (green, 4-hour) and the 100 simple moving average (red, 4-hour). Finally, the price dipped below the $75.00 level.

A low was formed at $74.20 and the price is now attempting a recovery wave. On the upside, the price is facing hurdles near the $75.80 level.

The next major resistance is near the $76.50 zone, above which the price may perhaps accelerate higher. In the stated case, it could even visit the $78.00 resistance.

If not, the price might dip further and test the $73.50 support. The first major support on the downside is near the $72.40 level. The next major support is at $71.50 or, below which the price might test $70.40. Any more losses might send oil prices toward $70.00.

Looking at EUR/USD, the pair remained supported and it seems like the bulls are aiming for a move toward the 1.0950 resistance.

Economic Releases to Watch Today

- US Factory Orders for April 2024 (MoM) - Forecast +0.6%, versus +1.6% previous.

US 10-year yield plunges as Fed cut expectations heighten slightly

US 10-year Treasury yield dropped significantly overnight, marking its most substantial one-day decline since last December. This sharp fall was triggered by disappointing economic data, revealing contraction in manufacturing activity for the second consecutive month. This indication of a cooling economy lifted optimism among investors slightly, as Fed would still be on track for monetary policy easing this year.

Currently, the probability of an initial rate cut in September has climbed to nearly 60%, according to Fed fund futures. Furthermore, expectations for a total of two rate cuts by year-end have also increased, now standing at 52.8%. However, these speculations could see dramatic shifts depending on the outcomes of upcoming economic reports, including ISM services data and non-farm payroll figures later this week.

Technically, as long as 4.318 support holds, 10-year yield's rebound from 3.780 is still in favor to extend through 4.730 at a later stage. However, as this rise is seen as the second leg of the corrective pattern from 4.997, strong resistance should be seen below there to limit upside. Sustained break of 4.318 will indicate near term reversal, and turn outlook bearish.

Japan’s Suzuki confirms impact of market intervention to support yen

Japan's Finance Minister Shunichi Suzuki confirmed today that recent interventions in the currency market had a notable impact on stabilizing Yen. During a press conference following a regular cabinet meeting, Suzuki explained that the interventions at the end of April and early May were specifically targeted to counteract excessive currency market movements.

According to data released by the Ministry of Finance last Friday, Japan spent JPY 9.79T over the past month to bolster Yen. This data confirmed traders' and analysts' suspicions that Tokyo conducted significant dollar-selling interventions.

These interventions occurred shortly after Yen plummeted to a 34-year low of 160.245 per dollar on April 29 and again in the early hours of May 2 in Tokyo.

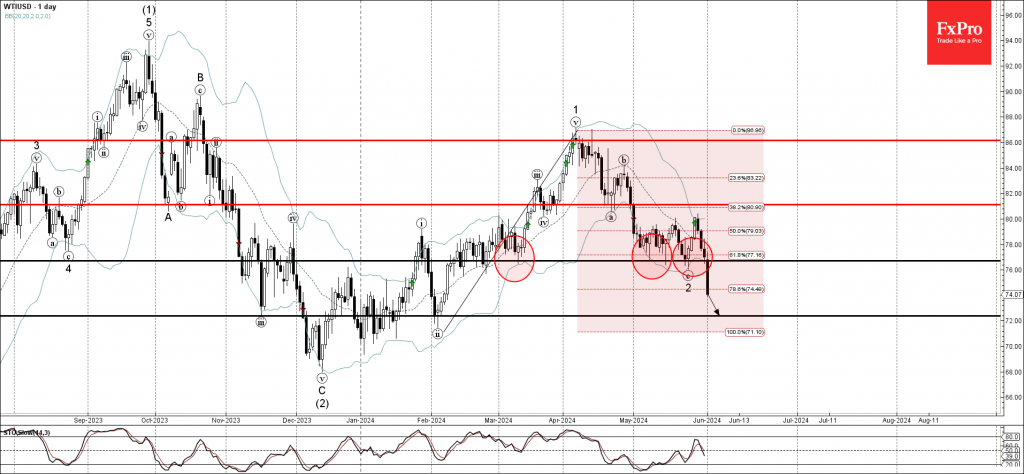

WTI Wave Analysis

- WTI broke key support level 76.70

- Likely to fall to support level 72.00

WTI crude oil recently broke the key support level 76.70 (which has been steadily reversing the price from the middle of February).

The breakout of the support level 76.70 coincided with the breakout of the 61.8% Fibonacci correction of the previous upward from the start of February.

WTI crude oil can be expected to fall further to the next support level 72.00 (which stopped the previous minor correction ii in February).

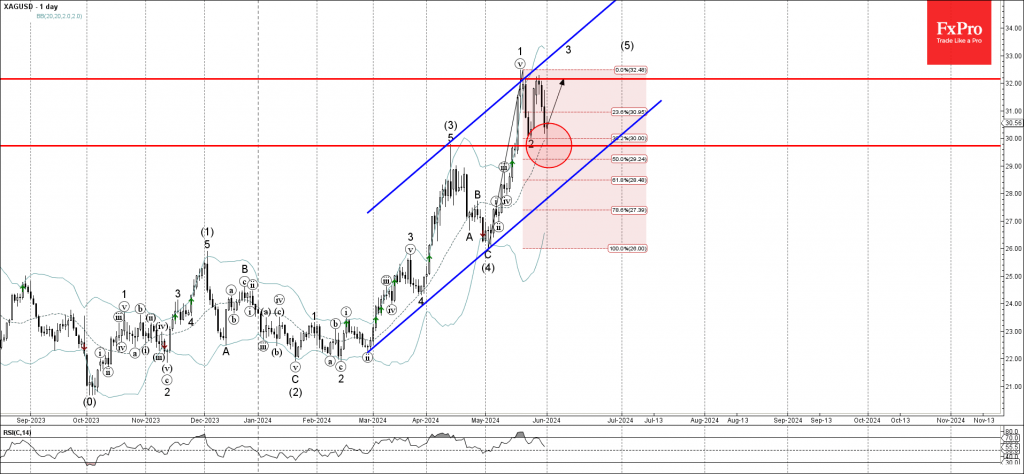

Silver Wave Analysis

- Silver reversed from support level 29.70

- Likely to rise to resistance level 32.00

Silver recently reversed up from the key support level 29.70 (former monthly high from April), which stopped the previous intermediate impulse wave (3).

The support level 29.70 was strengthened by the 20-day moving average and by the 38.2% Fibonacci correction of the previous upward impulse wave 1 from the start of May.

Given the clear daily uptrend, Silver can be expected to rise further to the next resistance level 32.00 (which formed the previous daily Evening Star in May).

Swiss Franc Climbing, Eyes Swiss Inflation

Swiss franc has extended its gains on Monday. USD/CHF is trading at 0.8961 in the North American session, down 0.68%.

Swiss franc rally continues

The Swiss franc posted its strong weekly gain of the year last week, rising 1.35%. The Swissie jumped over 1% on Thursday after Swiss National Bank President Jordan hinted that the central bank could intervene in the currency markets in order to keep a lid on inflation.

Thomas’ comments gave a boost to the Swiss currency, which has sagged in 2024. Even with last week’s strong gains, however, the Swiss franc has plunged 7.1% against the US dollar. The Swiss franc weakened after the Swiss National Bank unexpectedly lowered interest rates in March. A weaker Swiss franc helped make Swiss exports more competitive on world markets, but the currency’s sharp descent may have become too much of a good thing, as it is feeding inflation and raising concerns at the central bank.

The Swiss franc’s downswing has had a strong impact on market expectations for a rate cut at the June 28th meeting. In early May, swap markets priced a 66% probability of a rate cut, which has fallen to around 40%. The SNB isn’t likely to make good on Jordan’s threat to buy Swiss francs unless the currency continues to show a sharp depreciation, but last week’s jump shows how comments from central bankers can cause sharp swings in the currency markets.

Switzerland releases May CPI on Tuesday. This is the final economic release prior to the central bank’s rate meeting and could be a major factor in the SNB’s rate decision. Swiss CPI is expected to tick up to 0.4% m/m in May, compared to 0.3% in April.

USD/CHF Technical

- USD/CHF is testing support 0.8966. Below, there is support at 0.8909

- 0.9061 and 0.9118 are the next resistance lines

Nasdaq 100: Bullish Reversal Remains Intact Supported by Positive Momentum in 10-year T-Note Futures

- Macro factor (10-year US Treasury yield) has likely taken over the driver’s seat in dictating the short to medium-term directional movements of the major US stock indices.

- Last Friday, 31 May key intraday bullish reversals recorded in the S&P 500, Nasdaq 100, and Dow Jones Industrial Average were led by an earlier rally in the 10-year Treasury Note futures that kickstarted in the European session.

- Watch the key short-term support of 18,340 on the Nasdaq 100.

Since our last publication, the Nasdaq 100 has traded higher and printed a fresh intraday all-time high of 18,907 on 23 May reinforced by Nvidia’s rosy Q1 earnings results and upbeat revenue guidance for Q2.

Momentum and micro (firm-based earnings beats or misses) factors matter then. Interestingly, the macro factor has now taken on the driver’s seat since 24 May.

How can we decipher it?

By examining the movement of the 10-year US Treasury yield with the movements of the major US stock indices. From 24 May to 29 May, the US 10-year Treasury yield rallied by 15 basis points (bps) to print a 4-week high of 4.62%, and over the same period, the major US stock indices declined (in reverse tandem) and further extended their losses to last Thursday, 30 May; S&P 500 (-1.31%), Nasdaq 100 (-1.43%), and Dow Jones Industrial Average (-2.45%).

Why did higher US Treasury yields hurt US stock indices?

A further push-up in longer-term US Treasury yields, such as the 10-year yield where the “danger level” is anchored at its major resistance of 5% and clearance above it may unleash a bout of risk-off behaviour among market participants; a negative feedback loop via increasing long-term borrower costs for consumers and corporations which in turn could see a reduction in profit margins of US corporations as well as reduce the quantum of earnings upgrades from sell-side analysts.

Also, the S&P 500 is now trading at a high 12-month forward P/E ratio of 20.3, above its 10-year historical average of 17.8 (according to data from FactSet as of 31 May 2024). This rather lofty valuation number may become harder to sustain if the 10-year US Treasury yield keeps climbing northwards. In addition, the equity risk premium which is measured by the earnings yield of the S&P 500 against the 10-year US Treasury yield may shrink further, making the S&P 500 (US equities) less attractive to US Treasury bonds.

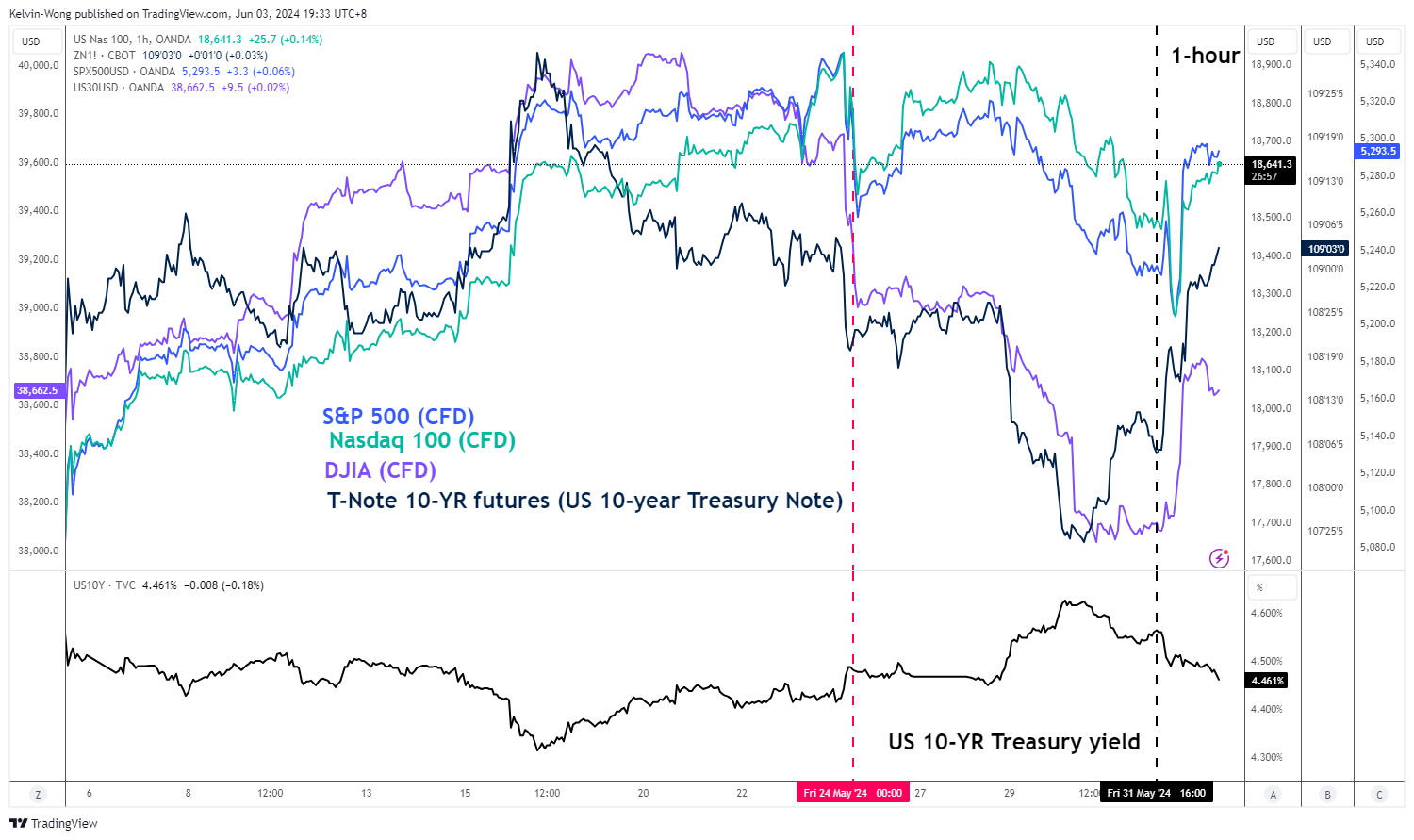

Last Friday’s key bullish reversal in US stock indices was led by 10-year US Treasury Note futures

Fig 1: 10-year US Treasury Note futures direct correlation with S&P 500, Nasdaq 100 & DJIA as of 3 Jun 2024 (Source: Trading View, click to enlarge chart)

All the major US stock indices erased their intraday losses after the second half of last Friday, 31 May US session and rallied strongly into the close with daily gains recorded in the S&P 500 (+0.80%), Dow Jones Industrial Average (+1.51%), and almost unchanged for Nasdaq 100 that reversed up from an earlier intraday loss of -1.9%.

Interestingly, these bullish intraday moves seen in the major US stock indices have been led by a similar bullish reversal seen in the 10-year US Treasury Note futures during last Friday, European session ahead of the start of the US session; bonds pricing 101 where a reduction in the US Treasury yield (in this instance the 10-year) tends to see an increase in the price of the corresponding 10-year US Treasury Note (see Fig 1).

10-year US Treasury Note futures is still exhibiting positive momentum

Fig 2: 10-year US Treasury notes futures (continuous contract) medium-term trends as of 3 Jun 2024 (Source: Trading View, click to enlarge chart)

Since the movement of the 10-year US Treasury Note futures (inverse relationship with US stock indices if one compares them with the 10-year US Treasury yield) has a leading direct correlation with the major US stock indices, it is paramount to analyze the short to medium-term momentum reading of the 10-year US Treasury Note futures since the macro factor is now a significant catalyst in dictating the likely movement of the major US stock indices at least in the short to medium-term.

The daily RSI momentum indicator of 10-year US Treasury Note futures is displaying a series of “high lows” and has not reached its overbought region which suggests a potential incremental bullish momentum reading (see Fig 2).

If the key-medium-term support at 107-23 holds, the 10-year US Treasury Note futures may see the next intermediate resistance coming at 110.12(also the 200-day moving average), and above it exposes the key medium-term resistance at 111-08 (the descending trendline in place since 27 December 2023 swing high.

Nasdaq 100 managed to recapture the 20-day moving average

Fig 3: US Nas 100 major and medium-term trends as of 3 Jun 2024 (Source: Trading View, click to enlarge chart)

Fig 4: US Nas 100 short-term trend as of 3 Jun 2024 (Source: Trading View, click to enlarge chart)

Last Friday, 31 May, the price actions of the US Nas 100 CFD Index (a proxy of the Nasdaq 100 futures) managed to trade back above the 20-day moving average and formed a daily bullish reversal “Dragonfly Doji” candlestick pattern that indicates a potential revival of its bullish impulsive upmove sequence within its medium-term uptrend phase in place since 18 April 2024 (see Fig 3).

Watch the 18,340 short-term pivotal support and a clearance above 18,830 near-term resistance may see the next intermediate resistances coming in at 18,990/19,055 and 19,160/19,180 in the first step (see Fig 4).

On the flip side, failure to hold at 18,340 sees the risk of the extension of the corrective decline to expose the next intermediate support at 18,100 (also the 50-day moving average), and a break below it sees the 17,810 key medium-term pivotal support.

June Flashlight for the FOMC Blackout Period

Summary

- The FOMC remained on hold for the sixth consecutive policy meeting on May 1 as elevated inflation and strong job growth earlier this year led policymakers to conclude that policy easing at that time would not be appropriate.

- Data released since the last meeting indicate that the threat of price re-acceleration due to strong economic activity has diminished somewhat. However, we share the universal expectation that the FOMC will keep its target range for the federal funds rate unchanged at 5.25%-5.50% at the conclusion of its policy meeting on June 12.

- We expect to see a nod in the post-meeting statement to the recent mix of activity and price data suggesting a lower risk of price re-acceleration, but we think the Committee will continue to characterize inflation as “elevated.”

- The FOMC will publish its quarterly update to the Summary of Economic Projections (SEP). The last dot plot, which was released in March, showed the median Committee member anticipated 75 bps of easing by year-end 2024. We look for the median projection in the updated dot plot to signal 50 bps of easing by the end of the year. However, we would not be surprised if the median dot shifted up to only 25 bps of anticipated rate cuts in 2024. The May employment report to be released on June 7 may be the deciding factor.

- We will also be keeping a close eye on the Committee's "longer-run" fed funds rate projections. The median longer-run dot was essentially unchanged at 2.5% between June 2019 and December 2023. The median ticked up ever so slightly to 2.56% in the March SEP, and our best guess is that the median longer-run dot is headed modestly higher in the June SEP, probably to a value between 2.625% and 2.75%.

- We do not look for any major changes to the macroeconomic forecasts in the SEP. The Committee's projections for real GDP growth do not seem likely to change materially.The median forecast for the unemployment rate at year-end 2024 may increase by a tenth or two, and median projections of PCE and core PCE inflation rates for this year seem likely to increase by about 0.2 ppt each in our view.

Fewer Signs of Prices Re-Accelerating, but Holding Pattern to Remain

“A lack of further progress” on the inflation front since the start of the year led the Federal Open Market Committee to hold the fed funds target range at 5.25%-5.50% for a sixth straight meeting on May 1. Data in the three months proceeding the FOMC's May meeting showed core PCE inflation strengthening to a 4.4% annualized clip, more than double the pace registered in the second half of 2023 that had previously suggested inflation was quickly returning to the Fed's 2% target. Stronger job growth over the same period alongside a solid pace of activity made inflation's early-year pickup even more unsettling, as sturdy demand stoked concerns that disinflation may have ended prematurely and price growth was at risk of picking up again.

Since the Fed's last meeting, however, the threat of prices re-accelerating and economic growth remaining defiant has weakened somewhat. Inflation as measured by the core PCE deflator eased in April, with the three-month annualized rate slowing to 3.5% (Figure 1). At the same time, job market rebalancing looks to have resumed. Payroll growth downshifted to 175K in April from an average monthly increase of 269K in Q1, the unemployment rate has risen to match a two-year high of 3.9%, while job openings/postings show demand for new workers continues to decline (Figure 2). There are fewer signs of current activity shifting into a higher gear as well. Both the ISM manufacturing and ISM services indices registered contractionary readings in April, and real consumer spending edged down over the month.

While more moderate signs of spending and hiring suggest inflation pressures continue to ease, Fed officials have made clear the need to see additional realized progress before reducing the fed funds target range. April's data marked a step in the right direction. However, it still leaves inflation running above target for more than three years and follows a stretch of data that reminded Fed officials of the difficulty in returning inflation to 2% for the long haul. Given this backdrop, we expect the FOMC to leave the fed funds target rate unchanged at the conclusion of its June 11-12 meeting and for the statement to omit any hints of a forthcoming rate cut. Market participants expect a similar outcome, with futures pricing in essentially no chance of a rate change at the June meeting and the next rate move as a cut in Q4.

With the FOMC remaining in a holding pattern, there are likely to be only a few changes to the post-meeting statement. The language around balance sheet run-off will need to be updated to reflect the lower run-off caps for Treasury securities announced at the prior meeting that are now in place. More meaningfully, we expect to see a nod to the recent mix of activity and price data suggesting a lower risk of price re-acceleration ahead. The description of recent economic activity, including hiring, likely will be softened somewhat. The Committee will likely continue to make clear it believes inflation remains too high by continuing to characterize it as “elevated.” However, the statement could acknowledge April's better data by noting that, instead of “a lack of further progress” in recent months, there has been “a lack of consistent progress toward the Committee's 2 percent inflation objective.”

The statement's guidance around the path of policy likely will remain unchanged. A chorus of Fed speakers in recent weeks have indicated that the need to gain “greater confidence that inflation is moving sustainably toward 2 percent” remains. For clues about the path for the fed funds rate further into this year and 2025, we will look to the update to the Summary of Economic Projections (SEP).

SEP Update: One Cut or Two in 2024?

The SEP, which is released four times per year, was last updated in March. At that time, the median Committee member anticipated 75 bps of easing by year-end (Figure 3). However, the 2024 dots had a decisively upward skew; nine Committee members projected two or fewer rate cuts this year, while just one envisioned more than 75 bps of easing.

Given that inflation has proved a bit stickier than was anticipated in March, it seems like a foregone conclusion that the median 2024 dot is headed higher. The question is, how much higher? We would be very surprised if the median dot moved all the way to 5.375% (i.e. no rate cuts in 2024). A move to 5.125% or 4.875% seems much more likely in our view. As of this writing, we lean slightly toward a median 2024 dot of 4.875%, which would be consistent with two 25 bps rate cuts by year-end. That said, we would not be surprised if the median 2024 projection calls for just one rate cut. We think it will be a close call, with the dovish leaning members still looking for two cuts while the more hawkish leaning members projecting one or zero rate reductions this year. The May employment report to be released on June 7 may be the deciding factor. Financial markets also seem torn between one and two cuts this year, with ~35 bps of easing by year-end priced into fed funds futures (Figure 4). If our base case is realized and the 2024 median dot rises by 25 bps, we would expect the 2025 and 2026 median dots also to rise by 25 bps each, bringing them up to 4.125% and 3.375%, respectively.

We will also be keeping a close eye on the "longer-run" (LR) fed funds rate projections. The longer-run projections represent each participant’s assessment of the fed funds rate that would best satisfy maximum employment and price stability over the longer run. In other words, the LR fed funds rate projections are the participants' views on the neutral policy rate. The median longer-run dot steadily fell for most of the 2010s, eventually settling at 2.5% in 2019. The median LR dot essentially did not move between June 2019 and December 2023. But starting in 2023, the mean LR dot began to climb as a handful of outliers started raising their longer-run projections, and the median ticked ever so slightly higher in the March SEP (Figure 5).

It would not take much for the median LR dot to rise again in the June SEP. Eight participants submitted an LR dot of 2.50% in the March SEP. If just one of those submissions moves up to 2.75%, the median would increase from 2.56% to 2.69%. Two participants flipping from 2.50% to 2.75% would be enough to make the new median 2.75%, all else equal. Furthermore, there seems to be increasing debate about the neutral rate and the degree to which monetary policy is restrictive. The topic came up in the minutes from the May FOMC meeting, and Governor Waller dedicated a recent speech to the topic of r-star. The New York Fed's Survey of Primary Dealers reveals a growing consensus among private sector forecasters that the neutral policy rate has moved higher (Figure 6). Thus, our best guess is that the median LR dot is headed higher in the June SEP to reflect this new reality, probably to a value between 2.625% and 2.75%.

Elsewhere in the SEP, we do not expect any major changes. The Committee's projections for real GDP growth do not seem likely to change much. The median projection in the March SEP for 2024 real GDP growth was 2.1%. Our most recent forecast is not much different and looks for 1.8% real GDP growth in 2024 on a Q4/Q4 basis. We do not see any compelling reason the 2025 and 2026 median growth numbers would move much from their current trend-like 2% projections.

The median projection in the March SEP for the unemployment rate in Q4-2024 was 4.0%, and we think this may rise by 0.1-0.2ppt. The current unemployment rate is 3.9%, although this may change in the May employment report to be released on June 7. We would interpret any small rise in the Committee's median projection for the unemployment rate as a reflection of the gradual uptick in the jobless rate since the end of 2023. We do not expect any changes to the median projections for the unemployment rate in 2025 or 2026.

We expect the median 2024 PCE and core PCE inflation projections to rise by about 0.2 ppt each. In March, the median participant expected headline PCE inflation of 2.4% and core PCE inflation of 2.6% in 2024. Our latest forecast is for 2.6% on headline and 2.8% on core, and we expect the median Committee projection to be close to our most recent forecast. The 2025 and 2026 inflation projections may rise by a tenth to reflect the stickier dynamics seen through the first half of this year, but upward revisions by a larger amount do not seem likely to us.