Sample Category Title

AUD/USD Analysis: US Dollar Rebounds from Decline

Yesterday, the PMI Manufacturing indices for several countries were published. The news turned out to be disappointing for the US - according to ForexFactory:

→ Final Manufacturing PMI: actual = 51.3; expected = 50.9; previous value = 50.9;

→ ISM Manufacturing PMI: actual = 48.7; expected = 49.8; previous value = 49.2;

This led to a weakening of the US dollar yesterday, as the not-so-strong manufacturing activity data, as reported by Trading Economics, supported arguments in favor of the Federal Reserve lowering interest rates.

As a result, currencies of other countries strengthened against the dollar, notably the AUD/USD exchange rate rose above 0.669 - the highest level in 2 weeks.

However, today the US Dollar is rebounding from yesterday's decline - and this is more clearly visible on the AUD/USD chart, indicating potential internal weakness for the Australian dollar.

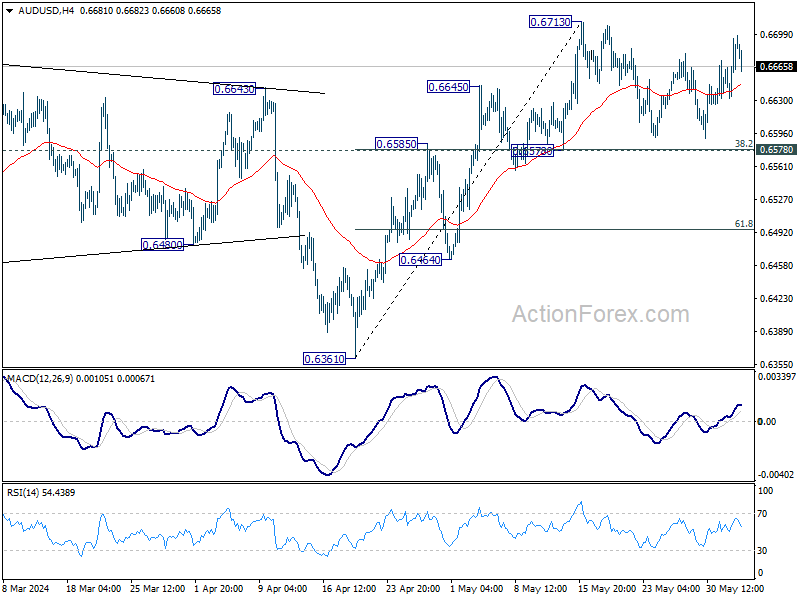

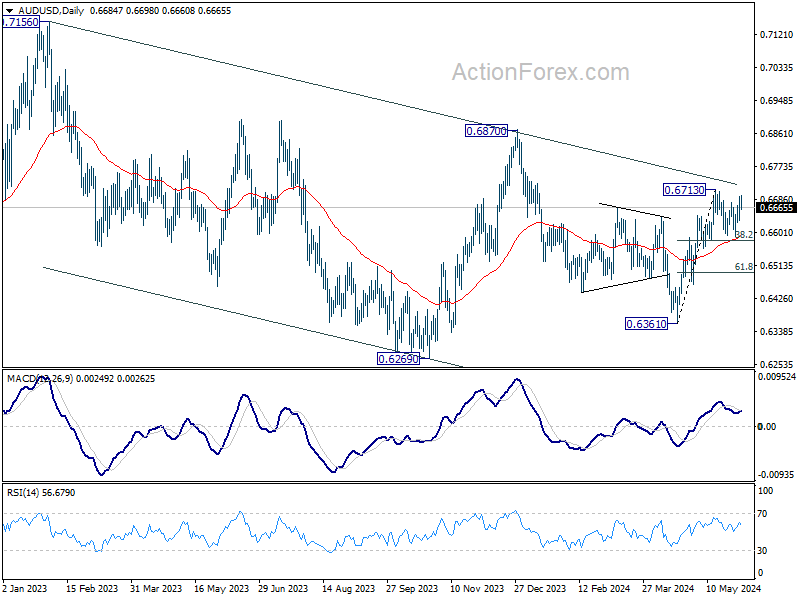

Technical analysis of the daily chart of AUD/USD shows that:

→ since the end of 2023, the market has been in a downtrend (indicated by the red channel);

→ the AUD/USD price is near the upper boundary of this channel;

→ price action is forming a symmetrical triangle pattern (shown by the blue lines), which usually indicates a temporary balance between supply and demand forces. In this case, it could be interpreted as demand exhaustion after a rise of approximately 2.75% in May;

→ the key level of 0.665, which acted as resistance since March, now serves as the central axis of the mentioned triangle;

→ yesterday's and today's (not yet closed) candles may form a bearish engulfing pattern, indicating ongoing selling pressure above the 0.668 level.

It is possible that during June, bears will attempt to break downwards from the consolidation triangle and resume the prevailing downtrend in the AUD/USD market. A key driver for this scenario to unfold will be the FOMC meeting scheduled for June 12th.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

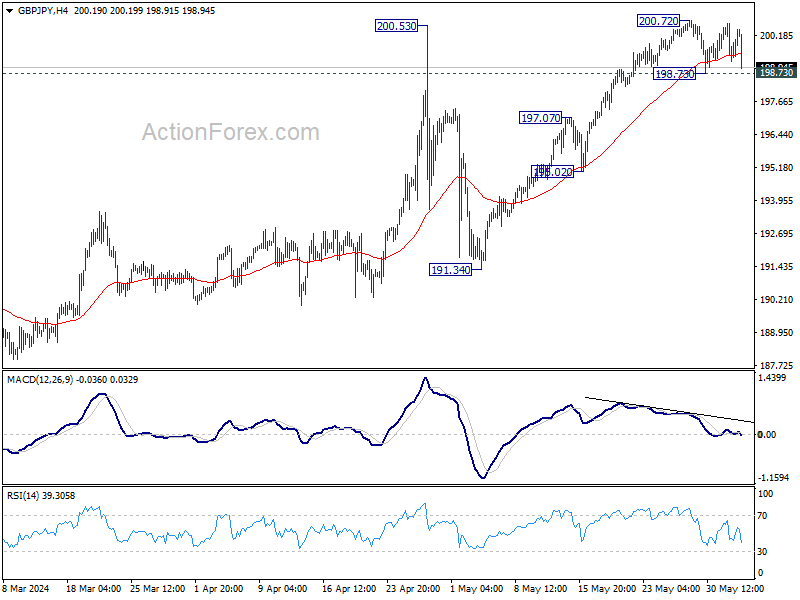

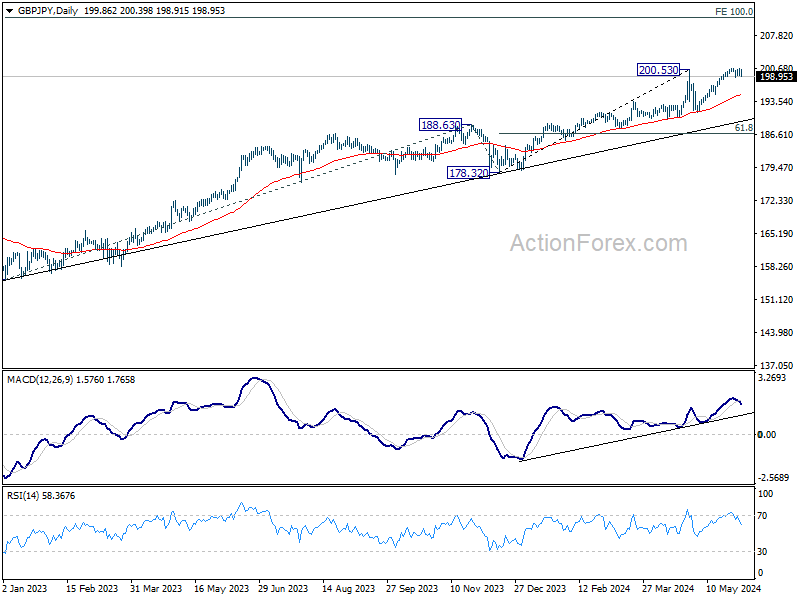

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.19; (P) 199.92; (R1) 200.62; More….

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, break of 198.73 support will indicate rejection by 200.53 high, and short term topping at 200.72. Bias will be back on the downside for 197.07 resistance turned support. On the upside, however, firm break of 200.72 will confirm larger up trend resumption.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Sustained trading above 200.53 will pave the way to 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

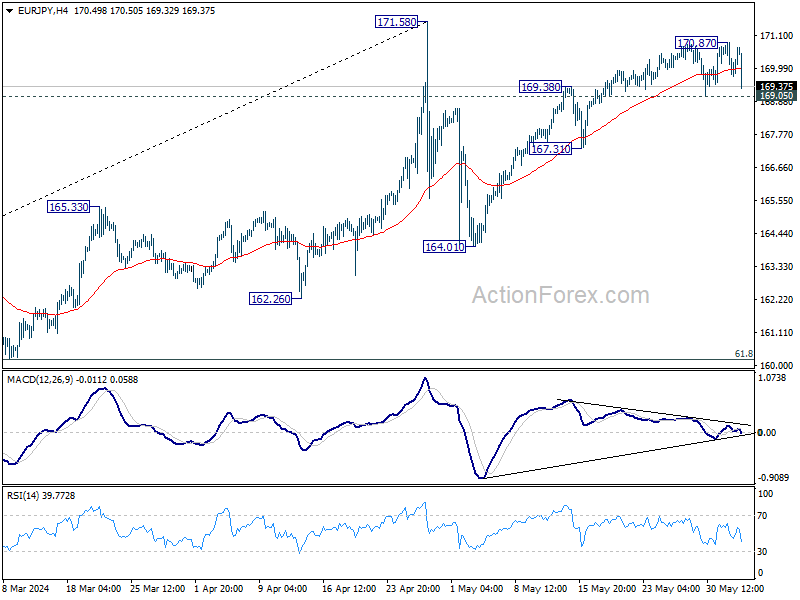

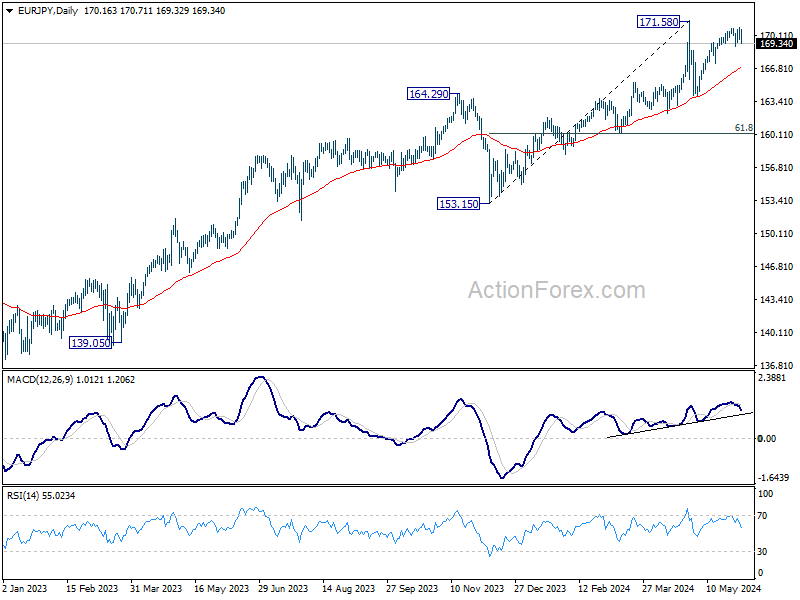

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.66; (P) 170.28; (R1) 170.83; More….

Intraday bias in EUR/JPY is turned neutral again with current retreat. Above 170.87 will resume the rally from 164.01 to retest 171.58 high. ON the downside, break break of 169.05 support should confirm short term topping, and turn bias back to the downside for 167.31 support instead.

In the bigger picture, a medium top was formed at 171.58 after brief breach of 169.96 (2008 high). But as long as 55 W EMA (now at 166.81) holds, price actions from there is seen as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

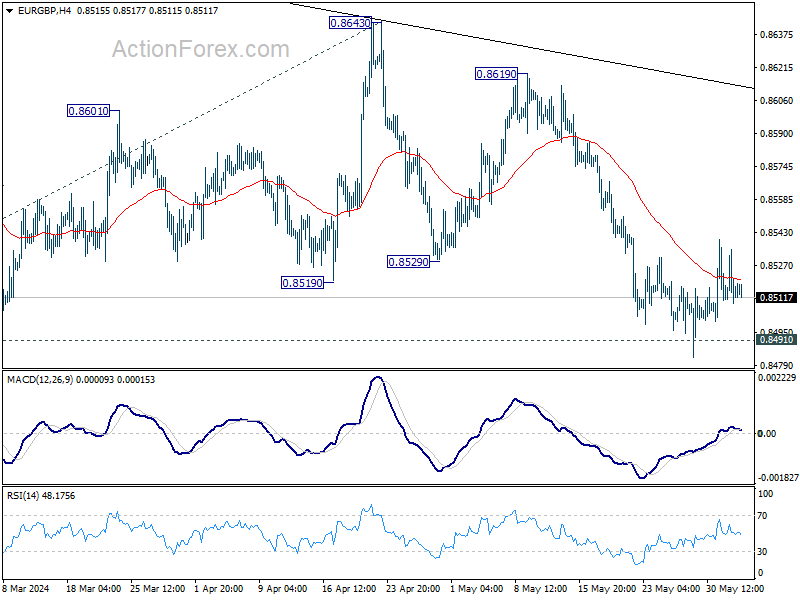

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8504; (P) 0.8520; (R1) 0.8530; More….

Intraday bias in EUR/GBP stays neutral and outlook is unchanged. Further decline is expected as long as 55 D EMA (now at 0.8550) holds. Decisive break of 0.8491/7 will resume larger down trend to 0.8376 projection level next. However, sustained break of 55 D EMA will turn bias back to the upside for 0.9643 resistance instead.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

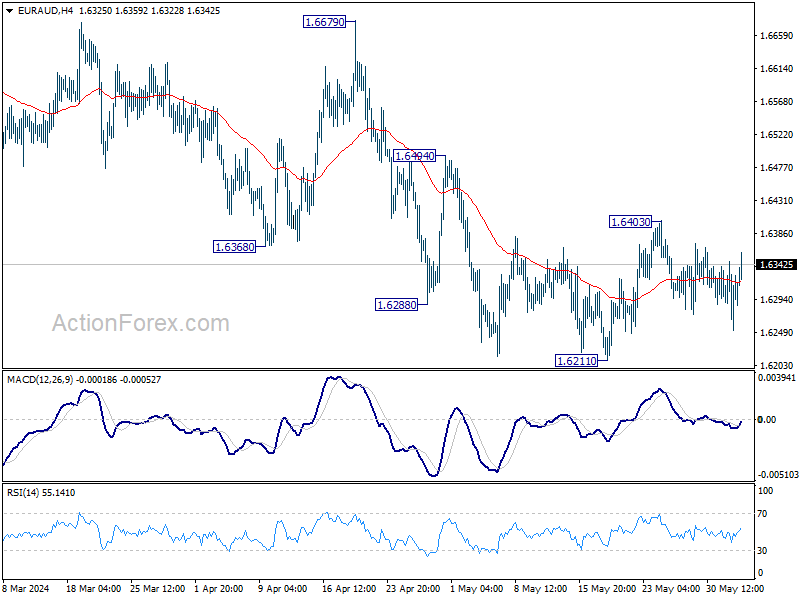

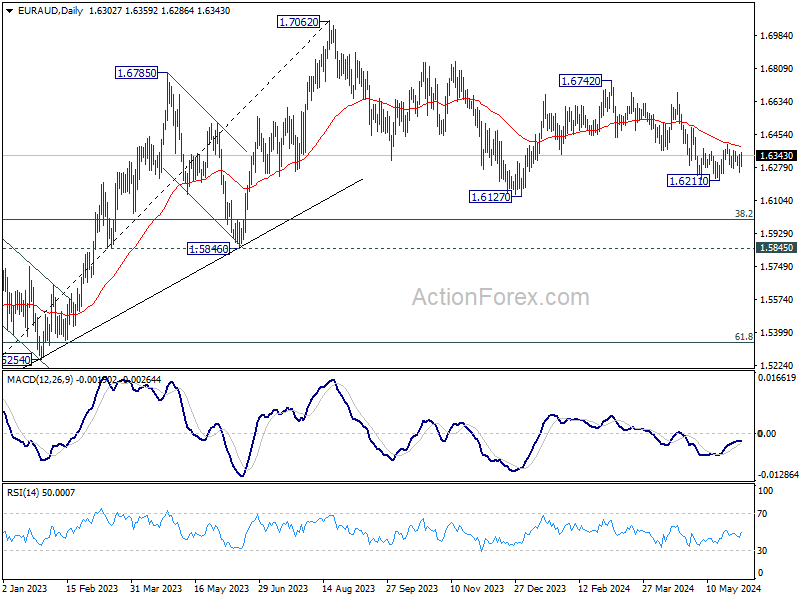

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6252; (P) 1.6301; (R1) 1.6347; More….

No change in EUR/AUD's outlook as sideway trading continues in range of 1.6211/6403. On the downside, firm break of 1.6211 support will resume the whole decline from 1.6742, as the third leg of the correction from 1.7062. On the upside, above 1.6403 will resume the rebound from 1.6211 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

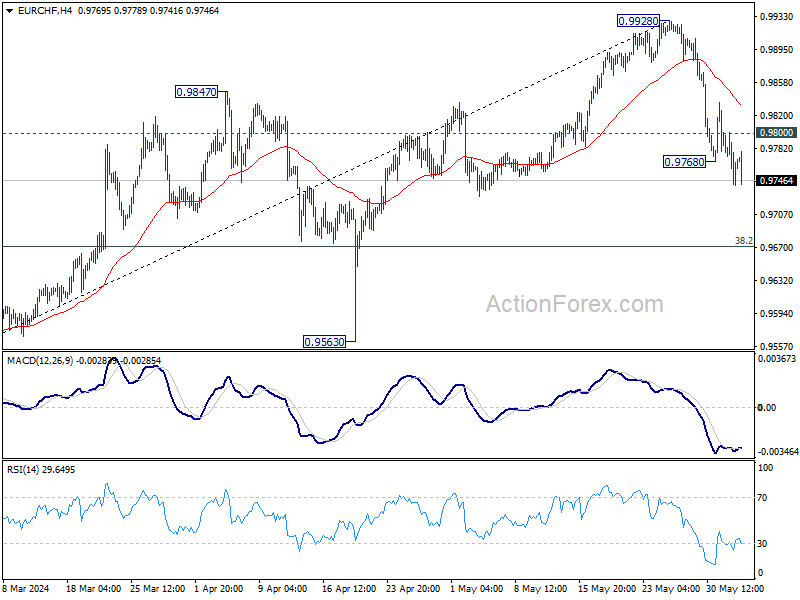

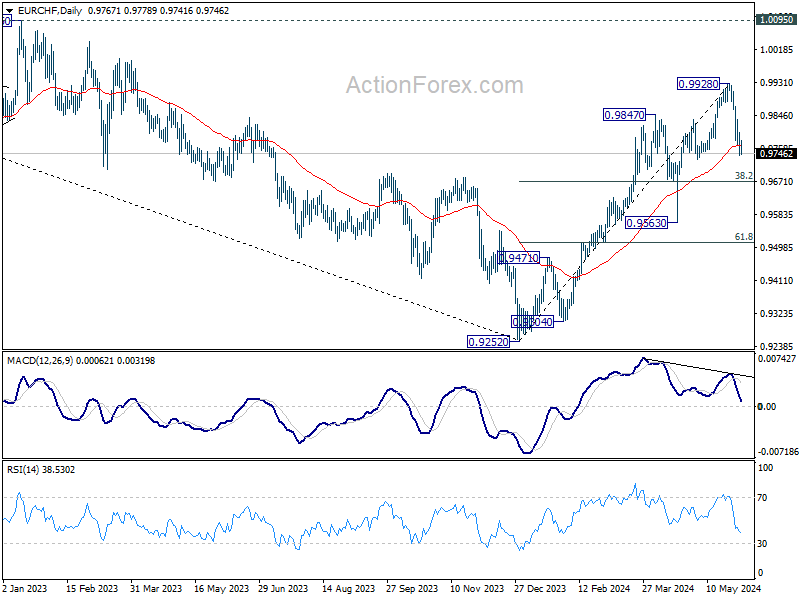

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9739; (P) 0.9772; (R1) 0.9802; More….

EUR/CHF's fall from 0.9928 resumed after brief recovery and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 0.9765) will pave the way to 38.2% retracement of 0.9252 to 0.9928 at 0.9670. Strong support is expected there to complete the pull back and bring rebound. On the upside, above 0.9800 minor resistance will turn intraday bias neutral again first.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004.

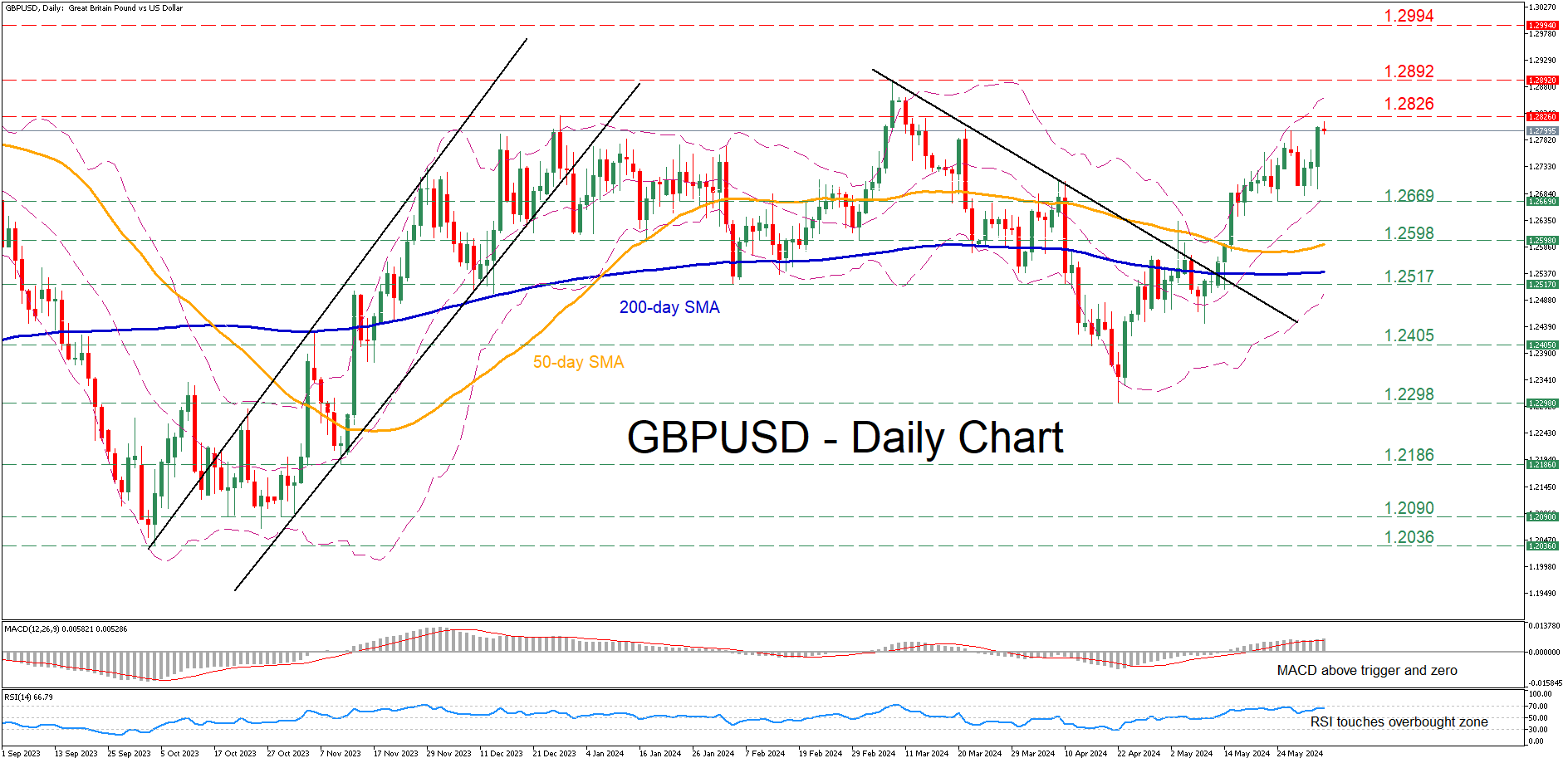

GBPUSD Surges to Fresh 2-Month High

- GBPUSD advances to its highest level since March 13

- But the advance starts to look overstretched

- Momentum indicators approach overbought conditions

GBPUSD has been in a steady recovery following its bounce off the 2024 bottom of 1.2298, with the price violating both the 50- and 200-day simple moving averages (SMAs). On Tuesday, the pair posted a fresh two-month peak, but quickly sustained some losses as the rally is starting to look overdone.

If the price extends its upward trajectory, the bulls could initially attack the December 2023 high of 1.2826. A violation of that region could set the stage for the 2024 peak of 1.2892. Failing to halt there, the pair could storm towards the July 2023 resistance of 1.2994.

On the flipside, should the pair reverse lower, the recent support of 1.2669 could act as the first line of defence. Further retreats could cease around 1.2598, a region that held strong both in January and March. Failing to halt there, the price could descend towards the February bottom of 1.2517.

Overall, even though GBPUSD surged to a fresh two-month high on Tuesday, its rally appears to be running out of juice. Nevertheless, a break below the 50-day SMA is needed for the short-term outlook to turn bearish.

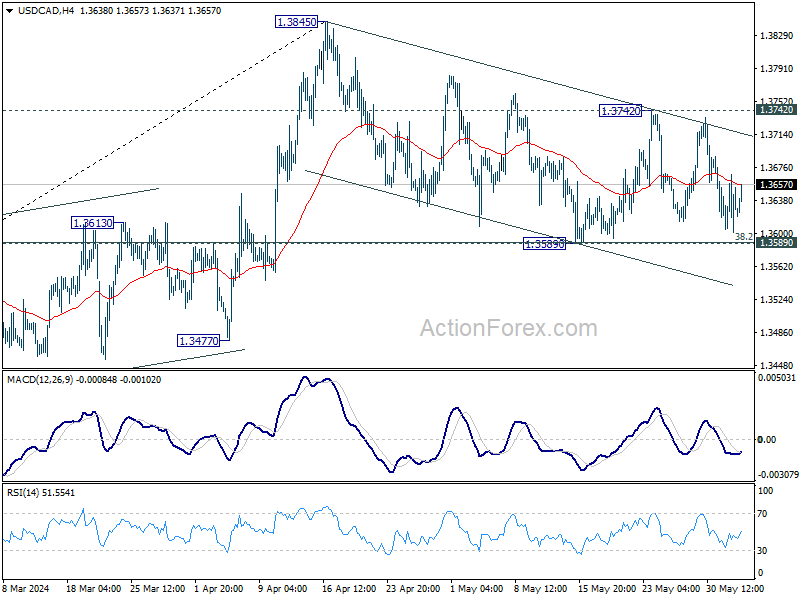

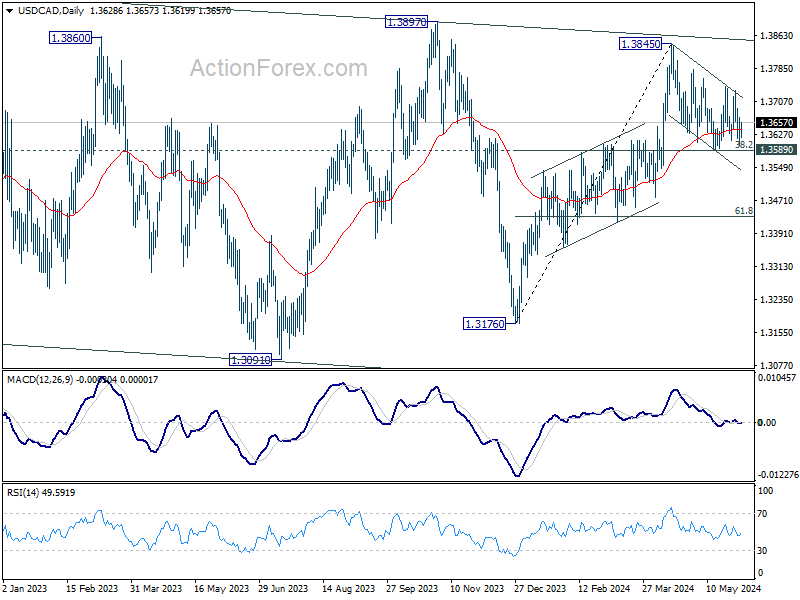

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3597; (P) 1.3633; (R1) 1.3664; More….

No change in USD/CAD's outlook as sideway trading continues. Intraday bias stays neutral at this point. On the upside, break of 1.3742 resistance will revive the case that correction from 1.3845 has completed at 1.3589. Intraday bias will be back on the upside for retesting 1.3845. On the downside, firm break of 1.3589 support will argue that whole rise from 1.3176 has completed at 1.3845 already. Fall from 1.3845 should then resume to 61.8% retracement of 1.3176 to 1.3845 at 1.3432.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6650; (P) 0.6672; (R1) 0.6712; More….

Range trading continues in AUD/USD and intraday bias remains neutral for the moment. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

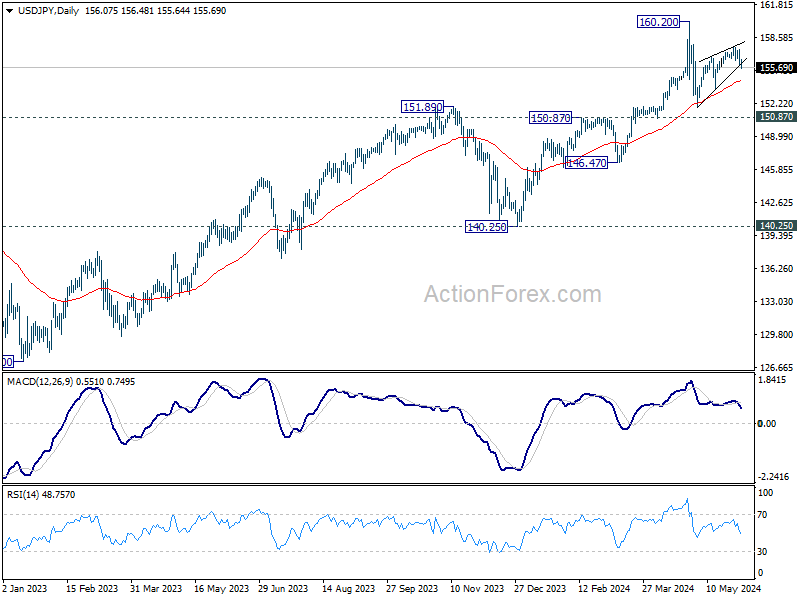

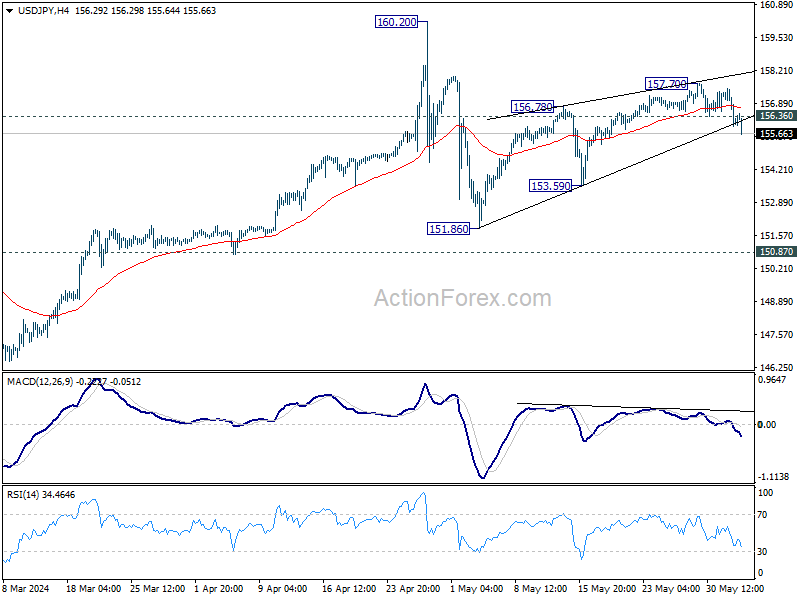

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.53; (P) 156.50; (R1) 157.06; More….

USD/JPY's break of 156.36 minor support argues that rebound from 151.86 has possibly completed with three waves up to 157.70. Corrective pattern from 160.20 might have started the third leg already. Intraday bias is back on the downside for 153.59 support first. Firm break there will solidify this case and target 151.86 support and below. For now, rise will stay on the downside as long as 157.70 resistance holds, in case of recovery.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.