Sample Category Title

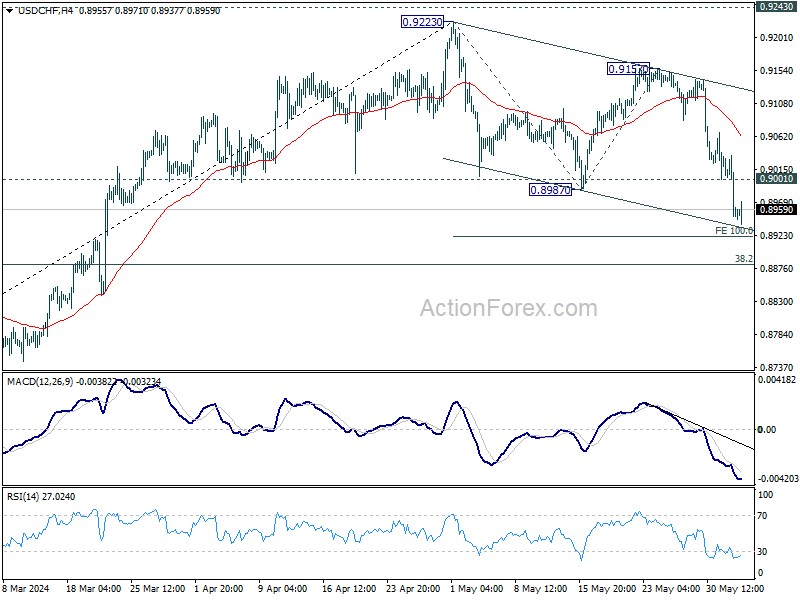

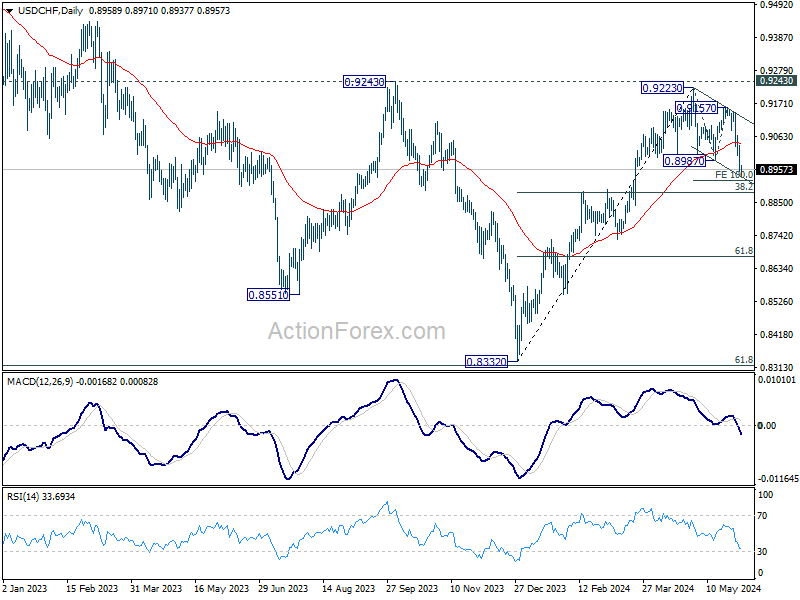

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8926 (P) 0.8983; (R1) 0.9016; More….

USD/CHF's fall from 0.9223 resumed by breaking through 0.8987 support and intraday bias stays on the downside. Next target is 100% projection of 0.9223 to 0.8987 from 0.9157 at 0.8921, and then 0.8883 fibonacci level. On the upside, above 0.9001 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

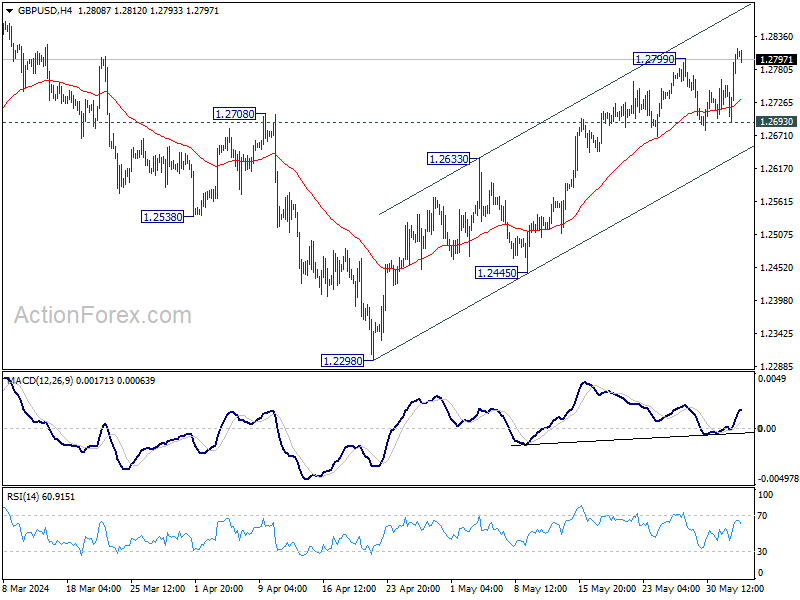

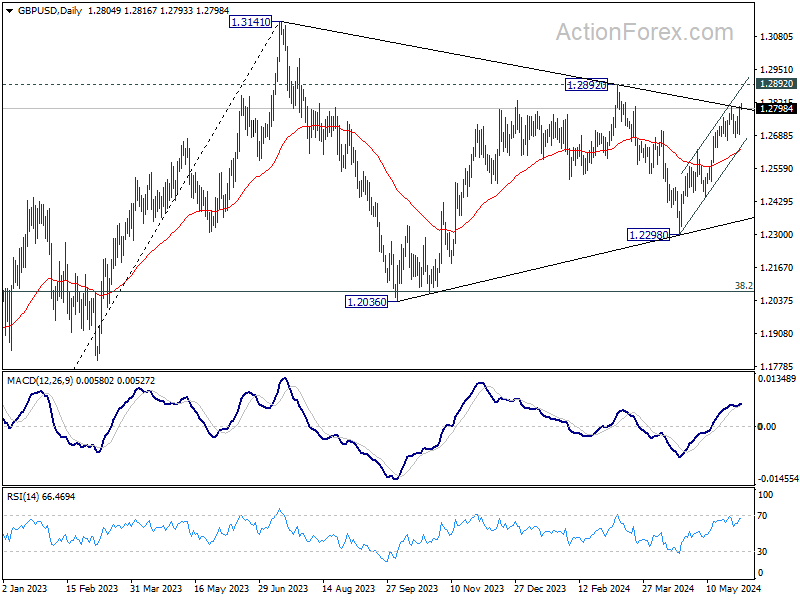

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2732; (P) 1.2770; (R1) 1.2847; More…..

GBP/USD's rally from 1.2298 resumed by breaking through 1.2799 resistance. Intraday bias is back on the upside. Next target is 1.2892 resistance. For now, break of 1.2693 support is needed to indicate short term topping. Otherwise, outlook will stay cautiously bullish in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

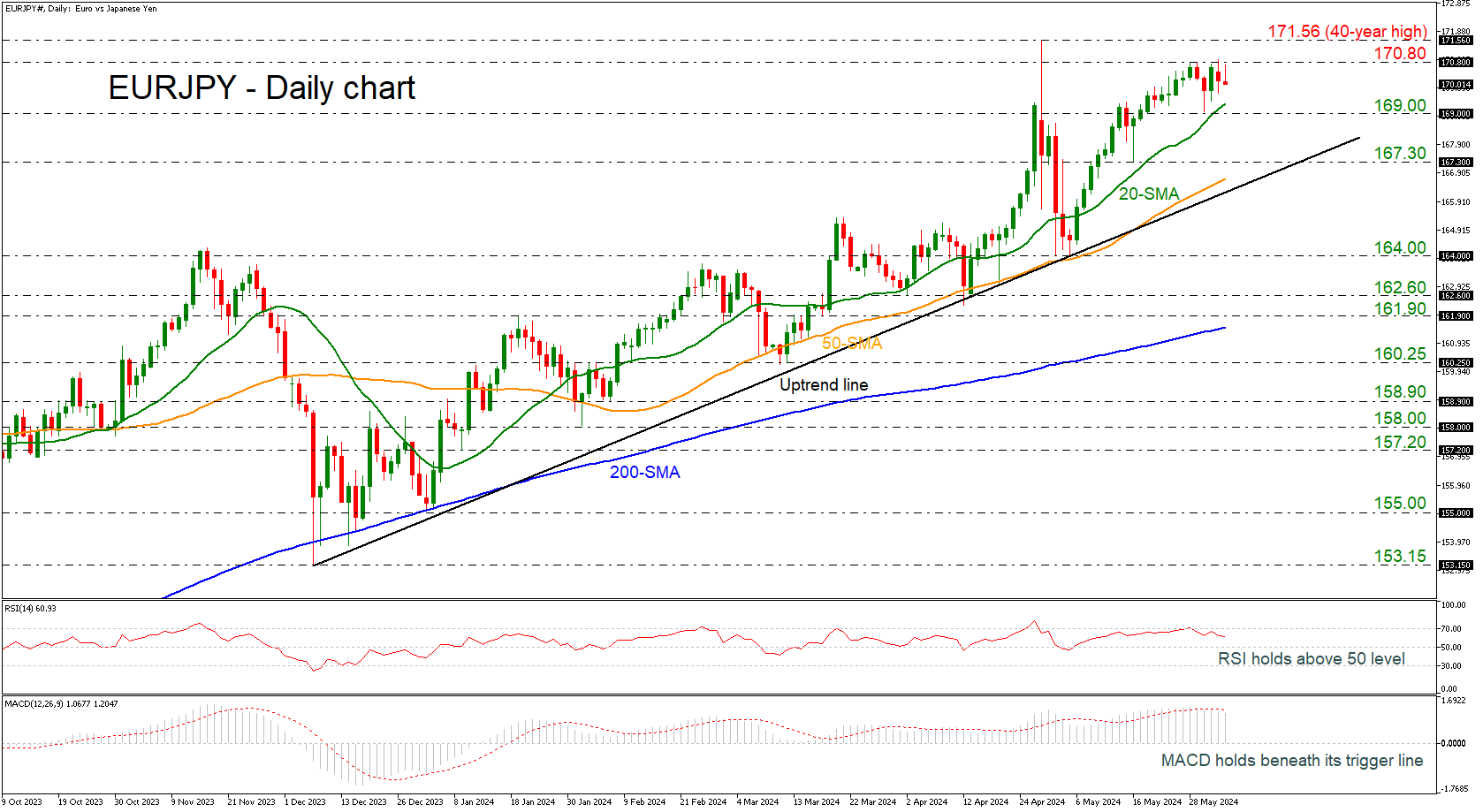

EURJPY Pulls Back from 170.80

- EURJPY seems neutral in very short-term

- RSI and MACD indicate bearish correction

EURJPY could not find enough buyers to expand its bullish move above the 170.80 immediate resistance but it has still been developing well above the long-term rising trend line, which has been drawn since December 12.

The question now is whether the pair will stay resilient above the 169.00 key region. A clear step below it and beneath the 20-day simple moving average (SMA) would press the price back to the 167.30 barrier. Slightly lower, the tentative ascending line around the 50-day SMA at 166.70 could prevent a drop towards 164.00 if it is breached.

Technically, the short-term risk is leaning to the downside. The RSI indicator is moving lower above the neutral threshold of 50, while the MACD is losing some steam beneath its trigger line in the positive territory.

The bulls still have the power to stage a rebound and surpass the 170.80 resistance level. In this case, traders will wait for a close above the 40-year high of 171.56 to confirm the long-term bullish outlook, meeting the 172.00 round number.

To sum up, EURJPY is looking neutral in the very short term and any advances above 170.80 could endorse the broader positive picture.

Swiss CPI unchanged at 1.4% yoy in May, core CPI at 1.2% yoy

Swiss CPI was steady at 1.4% yoy in May. Core CPI was also unchanged at 1.2% yoy. Domestic product inflation was unchanged at 2.0% yoy. Imported products inflation fell from -0.4% yoy to -0.6% yoy.

Comparing with the prior month, CPI rose 0.3% mom in. Core CPI rose 0.2% mom. Domestic product rose 0.5% mom while imported products rises was flat for the month.

Groundhog Day on US Interest Rate Markets

Markets

Groundhog day on US interest rate markets. At the end of April, US money markets were positioned for a first Fed rate cut at the December. It made them vulnerable to soft patches in eco figures. By mid-May, the pendulum swung to a first rate cut in September with follow-up action in December. At this stage, investors picked-up the more hawkish/inflationary details again. At the end of May, they arrived back where they started a month earlier: discounting only one 25 bps rate cut by December. Which made them vulnerable to… soft patches in eco figures. Yesterday’s May US manufacturing ISM immediately pulled the right/wrong strings. The headline figure showed a modest setback, from 49.2 to 48.7 instead of the longed-for modest improvement to 49.5. Apart from March 2024 (50.3), the manufacturing sector has been shrinking since November 2022. Details showed a very small rise in production levels (50.2). New (domestic) orders fell at a significantly faster pace (45.4 from 49.1) but got some buffer by rising export orders (50.6 from 48.7). Manufacturers continue to work through inventory backlogs. The prices paid index decelerated from 60.9 in April to 57 which nevertheless remains the second fastest price growth since August 2022. The report ended on a bright note with the employment subindex growing for the first time since September (51.1 from 48.6). Markets solely focused on weakening demand in the ISM, triggering a rally in US Treasuries. US yields lost 6.5 bps to 11.1 bps (30-yr). The curve move already suggests that something else was at play as well. Oil prices are the culprit. Brent crude started slipping around the start of the US session and the move continued after the ISM. The move is partly supply-inspired (following this weekend’s OPEC+ meeting including scaling back some production cuts from September), partly because of technical reasons (acceleration after losing YTD bottoms around $80.5/b) and partly demand-driven (ISM details). In the end, Brent crude lost almost $3/b, taking the weekly loss to $7/b (currently $77.5/b) and directly impacting long term rates via inflation expectations. German Bunds followed US T’s higher with the belly of the curve outperforming the wings. German yields lost 6.8 bps (2-yr) to 8.8 bps (30-yr). The dollar suffered from both the ISM and lower oil prices (positive correlation since US turned net exporter). EUR/USD closed above the 1.0884/95 resistance area (1.0904). If confirmed, this suggests room to head towards 1.10. The combination of ECB meeting and other key US eco data later this week (services ISM, ADP, payrolls) makes it too soon to call this resistance already definitely broken.

News & Views

South Korean inflation slowed further in May to 2.7% Y/Y from 2.9% (vs 2.8% consensus), touching the lowest level since July last year. The monthly pace of price growth remains low at 0.1% M/M after an unchanged reading in April. Core inflation excluding food and energy also eased from 2.3% Y/Y to 2.2%, the slowest pace since December 2021. Food prices declined by 0.7%, slowing the Y/Y-measure to 5.1% from 5.9%. Transport related costs were source of upward price pressure, adding 0.6% M/M and 3.8% Y/Y. After the publication, the Bank of Korea acknowledged the progress in inflation, but it is still looking for further evidence that inflation is converging towards its 2% inflation target. The BoK last month kept its policy rate unchanged at 3.5%. However, its assessment at that time was seen as tilting to the softer side, despite an upward revision to the growth outlook. The won is still trading at historically weak levels and might be a reason to stay cautious on starting a protracted rate cut cycle.

Data from the British Retail Consortium showed that total UK retail sales increased 0.7% Y/Y in May. This was above the 3-month moving average of 0.3%, but below the 10 month average growth of 2.0%. BRC assess the May sales development as “a mild recovery”. Food sales increased 3.6% Y/Y in the three months to May. However, non-foods sales decreased 2.4% 3M Y/Y, which is a steeper decline than the 12 month average of -1.7%. Non-food sales also were lower compared the same month last year. BRC said that “despite a strong bank holiday weekend for retailers, minimal improvement to weather across most of May meant only a modest rebound in retail sales last month”. Looking froward, “retailers remain optimistic that major events such as the Euros and the Olympics will bolster consumer confidence this summer”.

Meme Stocks Rally, Oil Tanks

GameStop rallied nearly 90% after Keith Gill, aka Roaring Kitty on Twitter, posted a screenshot on Reddit showing a big stake in option positions (about 120’000 call options that would give him the right to buy 12 mio GameStop shares for $20 each before June 21st). The holdings are unverified and no one knows if Roaring Kitty has any of these positions in hand, but it doesn’t really matter; the only thought that this could be true sent GameStop 90% higher before closing the session 21% up yesterday. Other meme stocks that have their names tied to GameStop-led meme craze like AMC, Beyond Meat, Blackberry and Reddit also benefited from the positive vibes yesterday. E*Trade said they would ban Keith Gill from their platform and the SEC explores possible market manipulation.

Fundamentally, a common denominator between the meme stocks is that they are not profitable companies, therefore the stock rallies don’t have a solid funding. If history is any indication, this wave will also quickly fade. When GameStop will reveal its Q1 earnings later this month, there is a chance that we have a confirmation that the rally is based on nothing beyond an impressive talent to move crowds into a trade.

On a side note, we originally had thought that the meme craze was fueled by a combination of low pandemic rates, piling up savings and bored traders (who were stuck home due to pandemic restrictions). But it turns out that all these factors are no longer valid. What’s also interesting is, thirst for dangerous trades is also visible in a relatively high interest for penny stocks. Finimize reports that 7 out of 10 most traded stocks in the US last month were worth less than $1 a share. So that means, to me, that there is still too much liquidity in the system. And there probably is. The Fed’s balance sheet for example is worth more than $7 trillion today, whereas it was worth around $4 trillion before the pandemic and less than a trillion before the subprime crisis. Bad news is, the Fed is unwinding its balance sheet as a part of its policy tightening policy. Good news is, the Fed said it will start slowing the pace of the balance sheet unwind – for I don’t know why, because that means that the balance sheet will never ever normalize. But the result is that, the financial markets do benefit from the still-ample liquidity despite the relatively high interest rates.

Beyond meme stocks

US yields fell on Monday after the latest ISM manufacturing data showed an unexpected acceleration in contraction in May as prices eased. The combination of faster-than-expected contraction and slower-than-expected price pressures fueled the expectations that the Federal Reserve (Fed) could – eventually – cut rates by the end of the year. The US 2-year yield fell to 4.80%, down from 5% tested at the end of last month, the 10-year tipped a toe below the 4.40% and the US dollar index sank below its 100 and 200-DMA. The softer dollar sent the EURUSD above the 1.09 resistance, Cable rallied past the 1.28 as the USDJPY eased.

All eyes are on US jobs data this week. Soft data should further fuel the dovish Fed expectations.

Lower yields didn’t necessarily translate into gains for the major US indices. The S&P500 remained under pressure before paring gains into the close and eked out a small 0.11% gain only. The tech-heavy Nasdaq gained 0.35%. Nvidia led gains. The stock rallied almost 5% yesterday as its CEO showcased new generations of AI chips at an event in Taipei. Note that Nvidia also announced last week that it would be upgrading its AI accelerators every year instead of every two years, and its new Rubin chip comes just three months after the Blackwell chip, revealed in March. The risinf speed of development is a robust sign that demand for AI is not slowing and the company is doing its best to stay on top of its game. Interestingly, at the same event, AMD also revealed its new chips – less than 2 months after the company’s last announcement. Alas, AMD dropped 2% on the news.

Elsewhere, crude oil had a rough session. The barrel of crude went on a free fall, cleared the a critical support at $75pb level and is trading near the $73.50pb this morning. OPEC’s plans to wind down supply cuts after the Q3, combined with a soft US data weighed heavier than the rising Fed cut bets. From a technical perspective, US crude is now at the limit of oversold market conditions and a positive correction is healthy at the current levels. Next support is seen at $72pb (a minor Fibonacci level) and the key resistance stands at $75pb.

Nordic Outlook: Inflation Have Been Stronger Than Expected

In focus today

This morning, we published our latest edition of Nordic Outlook in which we take a closer look at the major economies. We see that growth and inflation have been stronger than expected, pointing to fewer interest rates cuts delivered at a slower pace. In the Nordic countries the picture is more mixed, however the overall outlook remains for both higher growth and lower interest rates. Read more in Nordic Outlook - Warmer than expected, 4 June.

In Switzerland, May inflation is released at 08:30 CEST. Inflation is set to remain within the SNB's 0-2% target range with headline expected to pick up to 1.5% given the full impact from higher rents still set to feed through. The print today is the final one before the SNB meeting on 20 June, and with a recent topside surprise in inflation in April, stronger than expected growth, a weaker CHF and recent comments from SNB President Jorden, a cut at the June meeting no longer remains a done deal.

In the US, we get the Job Openings and Labor Turnover survey (JOLTs) for April this afternoon (16.00 CET). Job openings and hirings have trended lower lately, signalling cooling demand for workers.

In Japan, we get data for cash earnings in April early Wednesday morning. With the release we begin to look for the pass-through of the solid spring wage hikes, although April is probably a bit early still to see a large effect.

In China, we get the Caixin services PMI for May. Consensus amongst economist expects a very slight uptick to 52.6 from 52.5 in April, which was very close to its long-term average. There is however some downside risk after the official NBS non-manufacturing PMI which showed some softness last Friday.

In Sweden, first Deputy Governor Anna Breman will be discussing the economic situation and current monetary policy. At 08:40 the Minister of Finance holds a press briefing regarding the economic situation together with the Prime Minister.

Danske Morning Mail will be off Wednesday 5 June due to Constitutional Day in Denmark. We look forward to return Thursday 6 June!

Both the Bank of Canada and the central bank of Poland will convene and announce their respective policy rates on Wednesday. We expect them both to maintain their respective current rate levels of 5.00% (BoC) and 5.75% (central bank of Poland).

We will also be getting ISM services out of the US. Earlier, the PMI services index showed a modest rebound in both current and incoming business activity, but still only modest price pressures were seen. We also get the ADP private sector jobs report for May. In April, private sector jobs growth outpaced weaker growth in public employment. Consensus expects ADP to print 175k for May down from April's 192k.

In the euro area we will be looking out for April PPI data on Wednesday.

Economic and market news

What happened overnight

In Japan, Bank of Japan (BoJ) governor Kazuo Ueda told the Japanese parliament it was the policy of the BoJ to let financial markets determine long-term Japanese interest rates. However, he moderated the comment by following up saying, the BoJ may conduct 'nimble' market operations should long-term interest rates spike.

Asian equity markets are mostly in the red this morning apart from Hong Kong.

US equities closed mixed yesterday with the Dow Jones and Russell 2000 down, whereas the S&P500 and Nasdaq gained. Equity futures are flat this morning.

Oil prices took a dive yesterday, as Brent broke below the USD 80-mark, ending at USD78.36/bbl, down around 4%. This morning Brent is lower again trading at around USD77.8/bbl.

What happened yesterday

In the US, the ISM manufacturing for May came in below consensus expectations of 49.6, down from April's 49.2, as the May figure stood at 48.7. US Treasury yields retracted some on the back of the data release, with the 10Y UST shedding around 5bp in the immediate aftermath of the release.

In Sweden, Manufacturing PMI rose to a two-year high of 54.0 and is now close to the index's historical average of 54.3. The biggest contribution came from new orders. The spread between new orders and inventories continues to widen. As it is a leading indicator for the overall PMI figure, the manufacturing industry looks to be on the right track for recovery and the overall figure might very well soon reach 55-60.

In Mexico, the Nobel Prize winning climate scientist Claudia Sheinbaum won a landslide victory becoming the country's first female president. Sheinbaum ran on a platform of expanding the welfare policies, something analysts have pointed to being a tricky task lying ahead of her, given low economic growth and a hefty budget deficit.

The USD increased by around 4% against the Mexican Peso (USDMXN) on the back of the result, and Mexican equity markets ended around 6% lower, as Sheinbaum's green-left party together with two allied parties were nearing the two-third majority it would require changing the constitution - something investors fear would involve a dismantling of independent regulators.

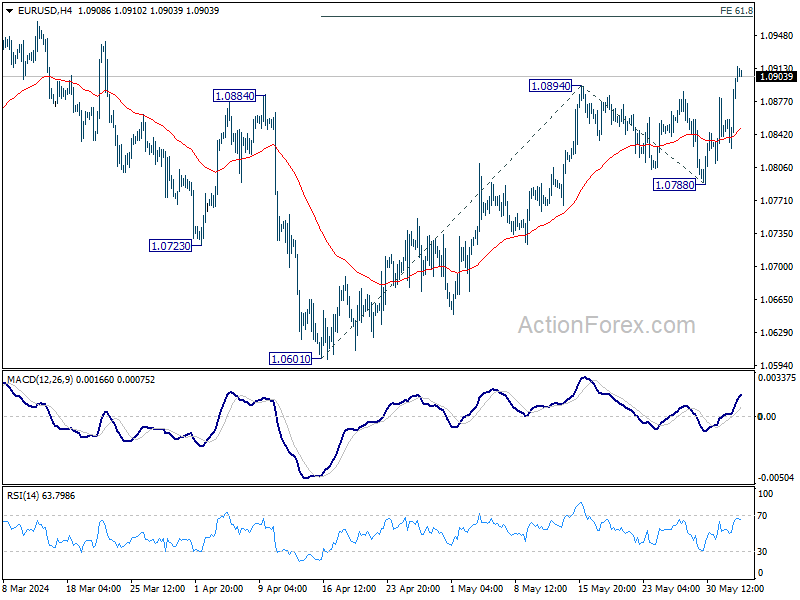

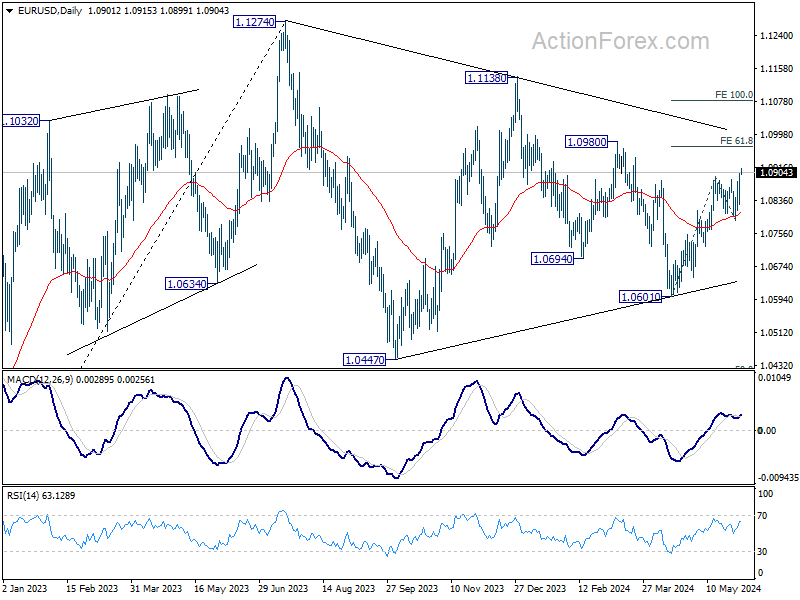

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0854; (P) 1.0879; (R1) 1.0931; More….

EUR/USD's rally from 1.0601 resumed by break through 1.0894 resistance. Intraday bias is back on the upside for t .8% projection of 1.0601 to 1.0894 from 1.0788 at 1.0969. For now, risk will stay on the upside as long as 1.0788 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0788 support will extend the corrective pattern instead.

Dollar’s Decline Sharpens Against European Majors, Yen Sees Rebound

Dollar weakened broadly overnight, particularly against European majors, following disappointing US manufacturing data that also pressured benchmark Treasury yields lower. This data not only pushed benchmark Treasury yields lower but also triggered the greenback's downturn. Despite these movements, the stock markets closed mixed, suggesting that the market reactions were not entirely aligned with the negative data impact. Investors now turn their attention to upcoming economic indicators, such as ISM services data non-farm payroll, hoping these will provide the Dollar with some support.

In the broader currency market, Canadian Dollar is currently the weakest performer for the week at this point, followed by Dollar. Australian Dollar is also underperforming, suggesting that the market mood is not decisively risk-on. Conversely, New Zealand Dollar has been the strongest so far, followed by Swiss Franc and Japanese Yen, with Euro and British Pound holding middle ground.

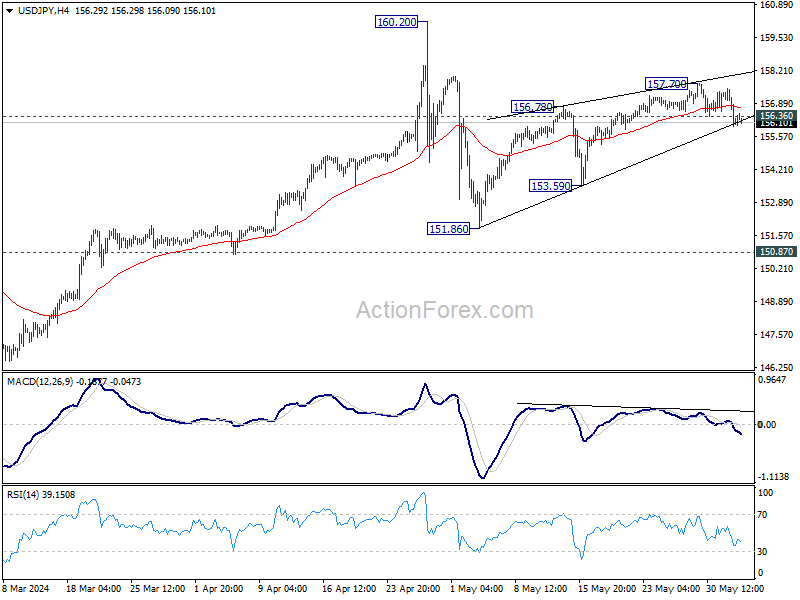

Technically, USD/JPY's break of 156.36 minor support is taken as the first sign that rebound from 151.86 has completed with three waves up to 157.70. Deeper fall will is in favor back to 153.59 support first. Firm break there will likely resume the whole pattern from 160.20 through 151.86 support.

If realized, however, this movement raises a critical question: Will this potential fall in USD/JPY be part of a wider Dollar selloff or could it herald a more extensive rebound in Yen across other currency pairs?

In Asia, at the time of writing, Nikkei is down -0.22%. Hong Kong HSI is up 0.27%. China Shanghai SSE is down -0.14%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield is down -0.0196 at 1.049. Overnight, DOW fell -0.30%. S&P 500 rose 0.11%. NASDAQ rose 0.56%. 10-year yield fell -0.112 to 4.402.

BoJ's Ueda: Monetary policy adjustments possible if inflation rises

BoJ Governor Kazuo Ueda addressed the parliament today, indicating that the central bank is prepared to adjust its level of monetary support if underlying inflation accelerates as forecasted. Ueda added, "If our economic and price outlook, or risks, change, that will also be reason to change the level of interest rates."

Discussing long-term interest rates, Ueda mentioned that the central bank's fundamental approach is to allow market forces to determine these rates. However, he also emphasized that BoJ would conduct "nimble" market operations if long-term interest rates were to spike, highlighting the bank's readiness to increase bond buying when necessary.

Japan's Suzuki confirms impact of market intervention to support yen

Japan's Finance Minister Shunichi Suzuki confirmed today that recent interventions in the currency market had a notable impact on stabilizing Yen. During a press conference following a regular cabinet meeting, Suzuki explained that the interventions at the end of April and early May were specifically targeted to counteract excessive currency market movements.

According to data released by the Ministry of Finance last Friday, Japan spent JPY 9.79T over the past month to bolster Yen. This data confirmed traders' and analysts' suspicions that Tokyo conducted significant dollar-selling interventions.

These interventions occurred shortly after Yen plummeted to a 34-year low of 160.245 per dollar on April 29 and again in the early hours of May 2 in Tokyo.

US 10-year yield plunges as Fed cut expectations heighten slightly

US 10-year Treasury yield dropped significantly overnight, marking its most substantial one-day decline since last December. This sharp fall was triggered by disappointing economic data, revealing contraction in manufacturing activity for the second consecutive month. This indication of a cooling economy lifted optimism among investors slightly, as Fed would still be on track for monetary policy easing this year.

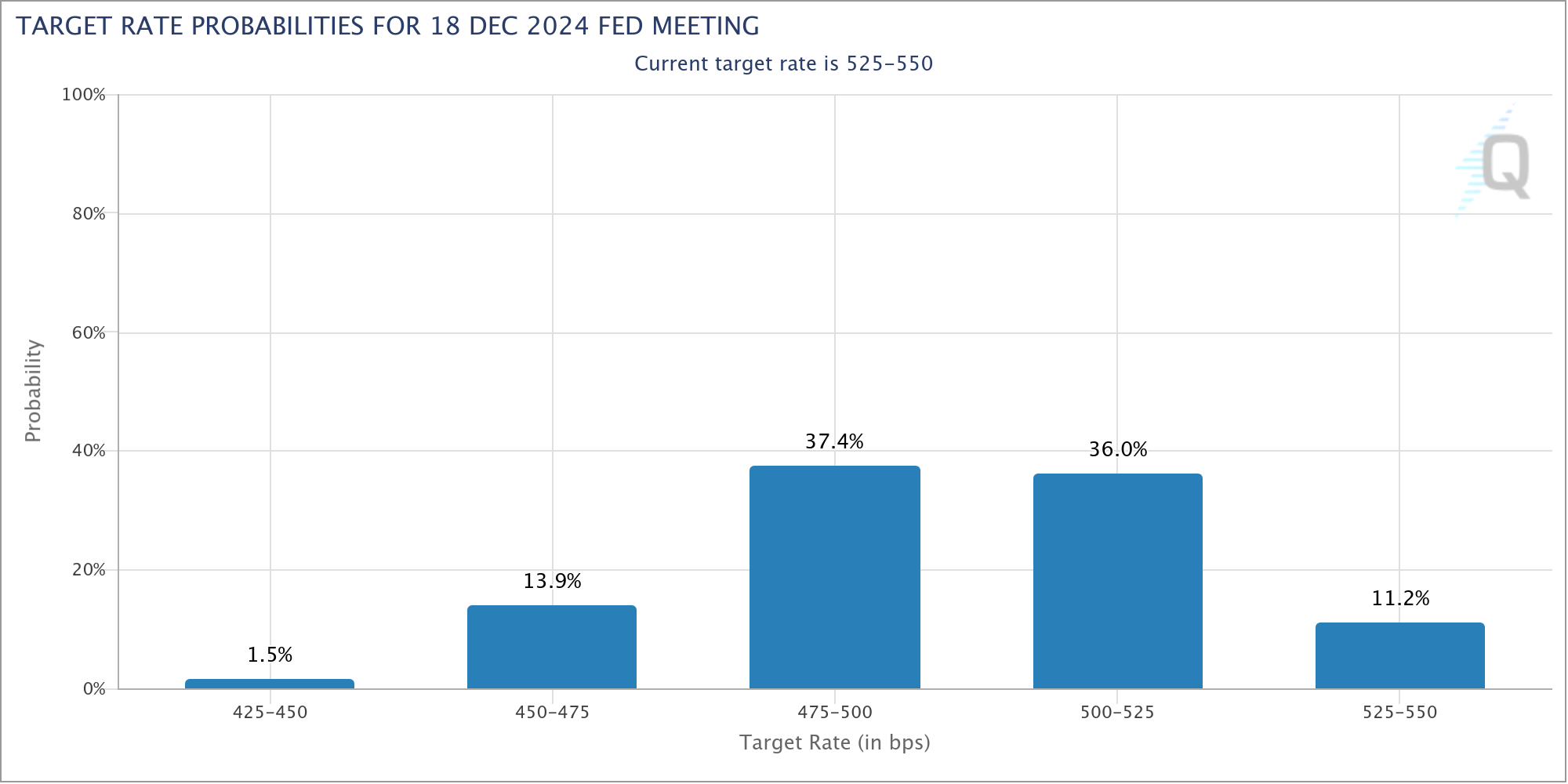

Currently, the probability of an initial rate cut in September has climbed to nearly 60%, according to Fed fund futures. Furthermore, expectations for a total of two rate cuts by year-end have also increased, now standing at 52.8%. However, these speculations could see dramatic shifts depending on the outcomes of upcoming economic reports, including ISM services data and non-farm payroll figures later this week.

Technically, as long as 4.318 support holds, 10-year yield's rebound from 3.780 is still in favor to extend through 4.730 at a later stage. However, as this rise is seen as the second leg of the corrective pattern from 4.997, strong resistance should be seen below there to limit upside. Sustained break of 4.318 will indicate near term reversal, and turn outlook bearish.

Looking ahead

Swiss CPI and Germany unemployment rate featured in European session. Later in the day, US will release factory orders.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0854; (P) 1.0879; (R1) 1.0931; More….

EUR/USD's rally from 1.0601 resumed by break through 1.0894 resistance. Intraday bias is back on the upside for t .8% projection of 1.0601 to 1.0894 from 1.0788 at 1.0969. For now, risk will stay on the upside as long as 1.0788 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0788 support will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y May | 0.90% | 2.20% | 2.10% | |

| 01:30 | AUD | Current Account Balance (AUD) Q1 | -4.9B | 5.9B | 11.8B | 2.7B |

| 06:30 | CHF | CPI M/M May | 0.40% | 0.30% | ||

| 06:30 | CHF | CPI Y/Y May | 1.40% | |||

| 07:55 | EUR | Germany Unemployment Change May | 7K | 10K | ||

| 07:55 | EUR | Germany Unemployment Rate May | 5.90% | 5.90% | ||

| 14:00 | USD | Factory Orders M/M Apr | 0.70% | 1.60% |

BoJ’s Ueda: Monetary policy adjustments possible if inflation rises

BoJ Governor Kazuo Ueda addressed the parliament today, indicating that the central bank is prepared to adjust its level of monetary support if underlying inflation accelerates as forecasted. Ueda added, "If our economic and price outlook, or risks, change, that will also be reason to change the level of interest rates."

Discussing long-term interest rates, Ueda mentioned that the central bank's fundamental approach is to allow market forces to determine these rates. However, he also emphasized that BoJ would conduct "nimble" market operations if long-term interest rates were to spike, highlighting the bank's readiness to increase bond buying when necessary.