Sample Category Title

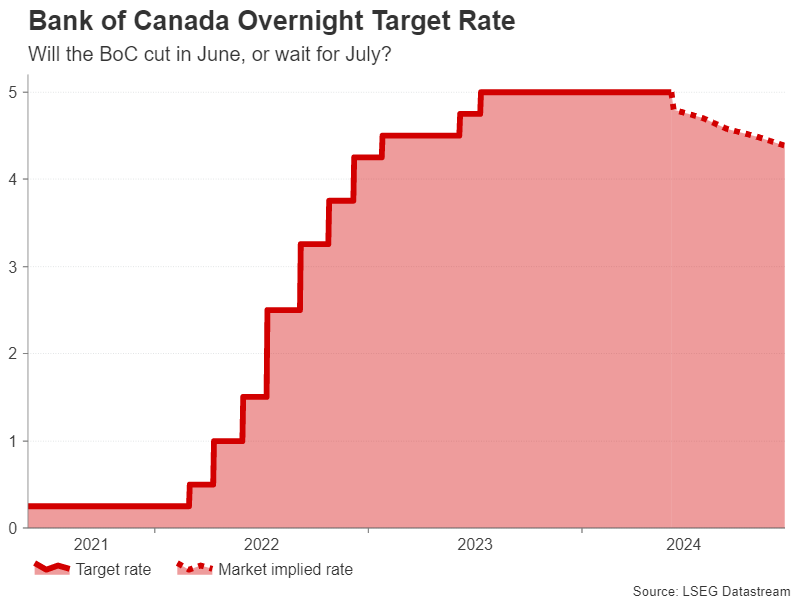

Bank of Canada Edges Closer to Rate Cut But Will it be in June?

- Canadian inflation has been moving in right direction this year

- Investors have assigned a more than 80% probability of a June cut

- But will the BoC move before the Fed; decision is due Wednesday, 13:45 GMT

The race to cut may be reaching the final hurdle

As the race to cut rates reaches fever pitch, much of the attention has been centred on the US Federal Reserve and the European Central Bank. However, the Bank of Canada may well steal the spotlight over the coming week by beating both central banks in cutting first. After finding itself in a similar situation as the Fed in the second half of 2023 when the progress in reducing inflation stalled, the Bank of Canada has had better luck in 2024.

Headline inflation fell to a three-year low of 2.7% in April, while all three underlying measures watched by policymakers also declined to fresh lows, dropping below 3.0%. Wage growth has been somewhat stickier, but seems to be heading downwards, albeit very gradually. Nevertheless, with the unemployment rate creeping upwards over the past year, wage pressures are likely to ease further in the coming months.

More broadly, economic growth has regained some momentum in the last couple of quarters but overall remains tepid amid still subdued consumption, and whilst the housing market seems to be on the mend, it’s unlikely to pose a significant risk to stability.

Will the BoC make the first move?

All this could potentially provide policymakers with the green light they’re looking for to slash rates. In the April policy statement, the Bank had said it will be seeking evidence that the downward momentum in inflation is sustained and that certainly appears to have been the case.

The question for investors is whether or not the progress since the April meeting has been substantial enough for the BoC to start lowering rates as early as June, or will it proceed more carefully and instead flag a cut in July. The odds for easing policy in June rose above 60% following the softer-than-expected April CPI report before reaching 80% after the disappointing Q1 GDP data. A cut in July remains fully priced in.

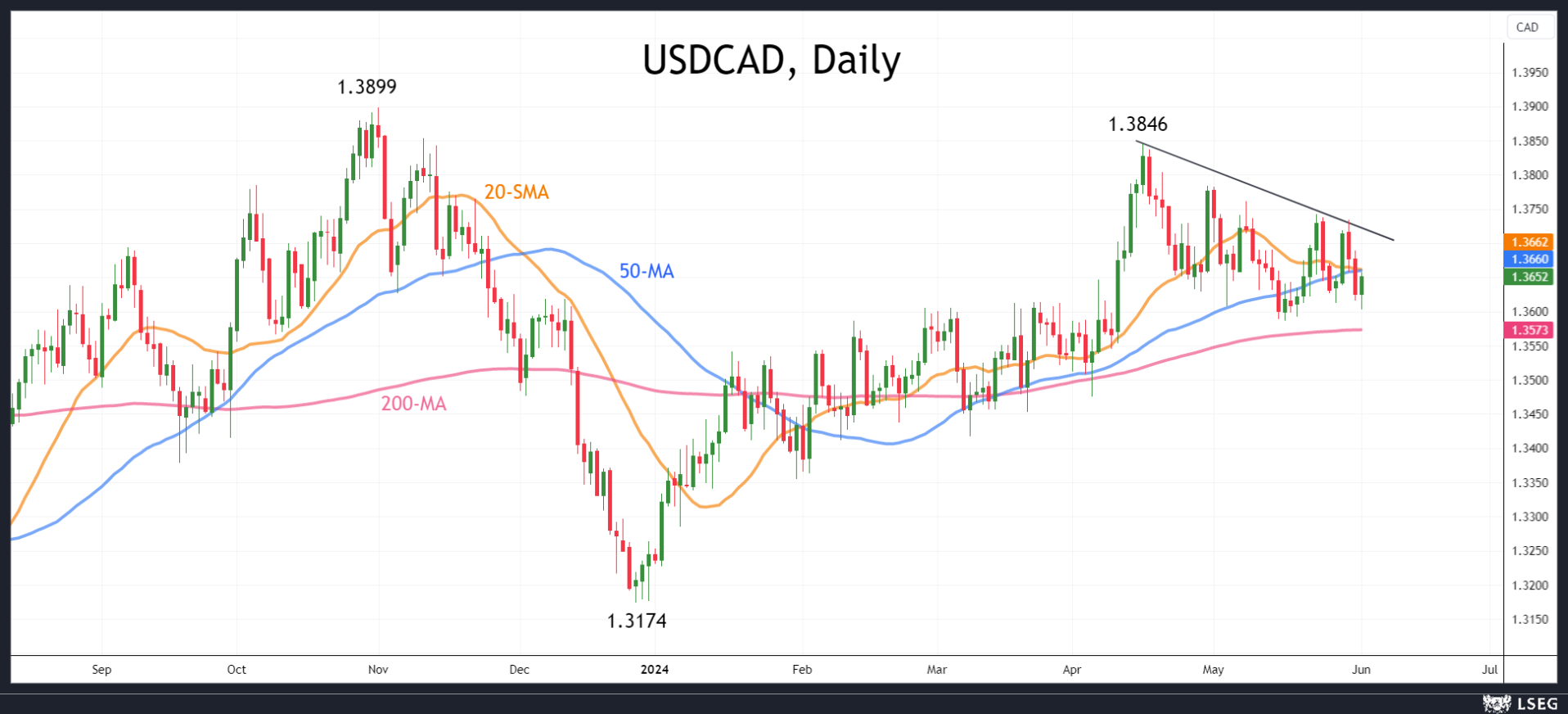

Loonie’s uptrend is on shaky grounds

Should the BoC reduce its overnight rate by 25 basis points on Wednesday, it would likely pressure the Canadian dollar against its US counterpart, endangering the six-week-old uptrend. The loonie could revisit the April low of 1.3846 per US dollar.

However, if the Bank stands pat in June, there could be scope for a rebound towards the 200-day moving average around 1.3570. The risk in this scenario is that should policymakers explicitly signal a cut for the following meeting in July, the loonie is again bound to face selling pressure.

Will the Fed derail a BoC cut

One reason why the BoC might decide to wait until the July meeting or even later is that, apart from wanting to see a further decline in inflation, the Fed is not in a position to do the same. As things currently stand, the US central bank might not start easing before December.

BoC policymakers would probably be wary of moving faster than the Fed and might therefore proceed cautiously as well so as not to hurt the loonie. However, neither would the BoC want to put its easing plans on hold for too long so cutting before the Fed might be inevitable and the most likely outcome is that policymakers will make only modest cuts until the Fed joins the rate-cutting club.

ECB to Make the First Move

- ECB meets on Thursday; a rate cut is expected

- Market will look for hints of back-to-back rate cuts

- A dovish rate cut could match expectations and push euro/dollar lower

- Decision will be announced on Thursday 12:15 GMT, press conference at 12:45 GMT

A 25bps rate cut is expected

On Thursday, the ECB will hold its fourth rate-setting meeting for 2024. The rhetoric from ECB officials since the April 11 gathering leaves little doubt about the outcome. The much-awaited rate decision will be announced at 12:15 GMT by a press statement with the usual press conference following 30 minutes later.

Recent data has not altered ECB’s stance

Since the April ECB meeting, data releases in the euro area have been positive. The recent business surveys and the continued tightness of the labour market portray an economy in recovery. However, keeping rates stable on Thursday following the barrage of dovish commentary could be an enormous hit on ECB’s credibility, which is already in tatters following 2021-2023 inflation jump. Therefore, ECB members are expected to ignore the recent pick-up in inflation and announce the much-awaited rate cut.

ECB to cut rates ahead of the ECB

The market is somewhat worried about the fact that the ECB will make the first move, ahead of the Fed, for the first time in its short history. Up to now, the Fed has always been dictating the start, the end, and the pace of any monetary policy cycle. But with US inflation remaining sticky and the US Presidential elections being only a few months away, Chairman Powell et al have opted to stay on the sidelines.

Interestingly, the fact that the ECB is making the first move could be interpreted in several ways. One could assume that the Fed is falling behind the curve for the first time in a while, or that the ECB could be making a mistake, like ex-President’s Trichet rate hike move in the summer of 2008, by cutting rates now that the economy is recovering.

Three factors to look for on Thursday

With the rate cut decision being pretty much pre-announced the market’s reaction would depend on three factors:

(a) the size of the rate. Certain ultra-doves tried to pitch the idea for a 50bps rate move. Their aim was to send a very strong message to the market about the ECB’s willingness to ensure inflation does not undershoot. However, this plan has probably been abandoned following Friday’s hotter CPI report.

(b) the new Eurosystem staff projections. In March, the inflation projection for 2026 stood at 1.9%, in line with ECB’s price stability target. A significant revision of this figure could determine ECB’s strategy during 2024.

(c) President Lagarde’s comments about the July meeting. ECB members have been publicly debating about the need for back-to-back rate cuts and hence Lagarde’s comments on this issue could give a strong indication of the behind-the-door discussions.

Likely scenarios for Thursday’s market reaction

The market is currently expecting a 25bps rate cut on Thursday, small revisions of the inflation projections and for President Lagarde to keep the door open to a July move. In this case, the euro/dollar is expected to test the busy 1.0772-1.0806 area.

Should President Lagarde et al decide to cut rates but refrain for commenting on the July meeting’s outcome, giving the impression that there was no widespread support for a similar-sized move in 45 days, the euro could get a boost with the recent high of 1.0894 being the first target.

On the flip side, a 25bps rate cut coupled with brave downward revisions in the inflation projections and Lagarde talking about the need for further action would constitute a dovish cut and thus potentially push euro/dollar towards the 1.0727-1.0735 range.

US: Manufacturing Slips Further into Contraction in May

The ISM Manufacturing Index slipped further into contractionary territory in May, dipping to 48.7 from 49.2 in April, disappointing expectations for a marginal gain. The contraction also became more broad based, with 55% of manufacturing GDP having contracted in May, up from 34% in April.

Demand slowing was reflected by the new orders index dropping deeper into contraction, and additional comments from respondents mentioning "softening". The backlog of orders index also dropped further into contractionary territory.

Output also moderated, and only barely remained in positive territory (50.2). However, employment flipped into expansionary territory in May, rising to 51.1, from 48.6 in April.

One silver lining was that price pressures seem to have eased since April. The prices paid sub-index fell 3.9 percentage points to 57 5.1 pp to 60.9, remaining in "increasing" territory.

Key Implications

The manufacturing sector has remained in contractionary territory for 18 of the last 19 months. The post-pandemic normalization of demand for goods and restrictive monetary policy have both weighed on the sector. The ISM Institute commented that "companies demonstrate an unwillingness to invest due to current monetary policy and other conditions".

May's manufacturing sentiment adds to the growing pile of evidence that high interest rates are acting to slow the economy. Last week's personal income and spending data showed a more cautious consumer to start the second quarter. This slowing should help cool inflationary pressures in the U.S. economy and enable the Fed to take rates lower later this year.

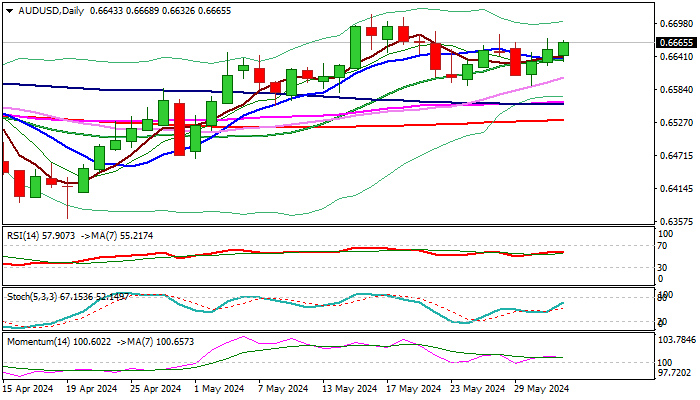

AUD/USD: Bulls Regain Control After a Healthy Correction

AUDUSD stands at the front foot on Monday and extends advance into third straight day, pressuring pivotal barrier at 0.6680 (recent range ceiling).

Fresh strength further improves near term outlook, boosted by positive signal from formation of a higher base at 0.6590 (May 24/30 double-bottom), which signaled a healthy correction from 0.6714 (May 16 top, the highest since mid-Jan).

Technical picture is positive on daily chart (strong bullish momentum / MA’s in bullish configuration and created multiple bull-crosses), with close above (0.6642 (converged 10/20DMA’s) seen as minimum requirement to keep fresh bulls in play, while sustained break of 0.6670/80 zone (Fibo 61.8% of 0.6714/0.6590 / tops of May 31/28) to confirm reversal and open way for full retracement of 0.6714/0.6590 corrective leg.

Res: 0.6680; 0.6714; 0.6743; 0.6761.

Sup: 0.6642; 0.6626; 0.6590 0; 6558.

Sunset Market Commentary

Markets

On Friday a divergent narrative of in line, rather soft US price deflators and higher than expected EMU May CPI inflation caused US and EMU interest rate markets to part ways, with US yields declining and EMU interest rates still gaining a few bps. Today US and European bonds again moved in the same direction. US yields extend last week’s correction south declining between 1 bps (2-y) and 4.5 bps (30-y). This week’s US eco data starting with the manufacturing ISM later today, will guide market momentum short-term. A new set of not-too-hot activity data might cause markets to again raise the odds of two Fed rate cuts this year rather than only one at the end of the year. A similar reasoning can be developed for positioning on European interest rate markets. Despite last week’s higher than expected EMU inflation investors apparently conclude that enough ECB caution is discounted for now. Money markets, after this week’s 25 bps cut, see one additional step of the ECB in H2, but less than 50% chance of a third one before the end of the year. The ECB on Thursday is unlikely to give a detailed path on its future intentions. Even so, making the step of an inaugural rate cut also includes the message that inflation has cooled enough to reduce policy restriction from here. It makes little sense to do so when you don’t see a decent chance for follow-action in a not that distant future. New ECB staff forecasts in this respect probably will confirm a scenario of EMU inflation returning close to 2.0% next year and in 2026. German yields are ceding between 4.5 bps (2-& 30-y) and 6 bps (5-y). After a positive start in Asia this morning, bond markets gains also support a bid for global equity markets. The Eurostoxx 50 gains 0.9%. The S&P 500 after a solid performance on Friday opens with a decent gain ( 0.4%). Oil (Brent $80.8 p/b) still struggles to avoid further losses after the OPEC+ decision this weekend. The cartel decided to maintain most production cuts in place till end next year, but to potentially scale back 2.2 mln bpd of some voluntary reductions post September 2024. Markets apparently are not convinced that demand will be strong enough to pick up additional supply.

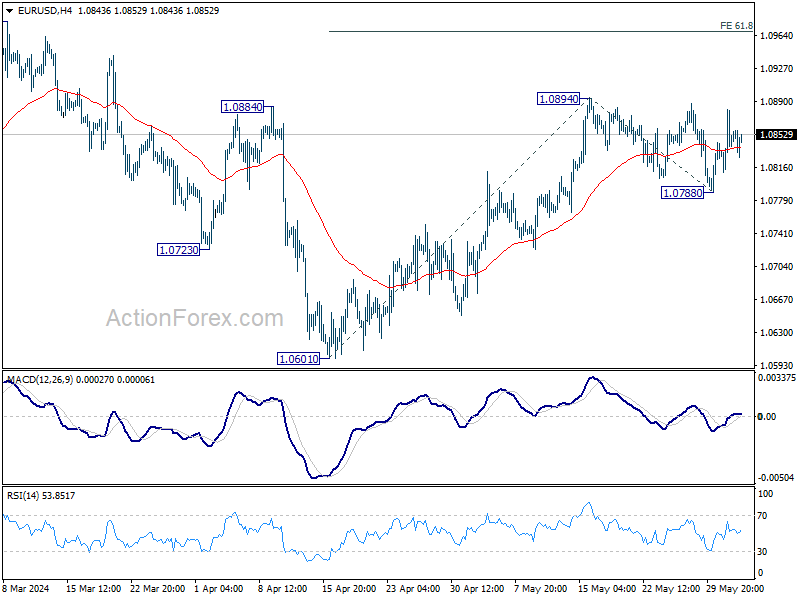

On FX markets the dollar is trading mixed, within established short-term ranges. DXY trades marginally lower at 104.57. Lower yields in core markets (US, EMU, UK) is giving the yen some breathing space (USD/JPY 156.85; EUR/JPY 170.1). EUR/USD trades little changed near 1.085, holding the narrow short-term band between 1.0788 and 1.0895. EUR/GBP this morning tried to resume Friday’s euro-driven rebound. However, divergence between the start of the ECB rate cut cycle and the BoE being forced to stay on hold due to stickier than expected inflation for now prevents further sterling losses (EUR/GBP 0.852).

News & Views

The Czech manufacturing downturn softened in May according to S&P Global’s PMI. It increased from 44.7 to 46.1 (vs 45.5 expected). It’s the second to best outcome since August 22 with the PMI already in contraction territory since June 2022. Details showed output, new orders, employment and purchasing activity all continuing their decline but at a slower pace. Panelists continued to highlight subdued domestic and external client demand, especially from key European export markets, including Germany. Hopes of improved customer interest sparked the second-strongest degree of confidence in the year ahead outlook for output in over two years. Input prices increased only marginally, but output charges ticked up at the fastest pace in just over a year, highlighting the inflationary risks challenging the Czech National Bank. EUR/CZK remains stuck near 24.70 where it has been trading since mid-May.

Mexican assets underperform today after Claudia Sheinbaum from the ruling Morena party won a landslide presidential election victory. The leftwing close ally of current president Lopez Obrador won nearly 60% of the votes according to a partial official count. The Morena party and its allies are also expected to win both houses of congress with what will be close to a two-third majority needed to push though constitutional changes. Some fear a weakening of democracy in this scenario given proposals by the previous president like popular elections for supreme court judges and directors of the electoral institute. USD/MXN surges from 17 to 17.50, the weakest MXN-rate YTD. MXN swap rates rise by 10-15 bps across the curve.

Graphs

USD/INR: Indian rupee jumps as first estimates indicate a decisive victory for PM Modi’s ruling party.

Dutch TTF natural gas reference contract extends uptrend to highest level YtD after an unplanned outage in Norwegian production.

USD/MXN: Mexican peso declines as the outcome of presidential and Congress elections is seen raising the risk of market unfriendly policy.

EMU 10-y swap returning lower in the established trading range as markets are preparing for inaugural ECB rate cut.

US ISM manufacturing falls to 48.7, corresponds to 1.7% annualized GDP Growth

US ISM Manufacturing PMI fell from 49.2 to 48.7 in May, below expectation of 49.8. Looking at some details, new orders fell from 49.1 to 45.4. Production fell from 51.3 to 50.2. Employment rose from 48.6 to 51.1. Prices fell from 60.9 to 57.0.

ISM said: “The past relationship between the Manufacturing PMI and the overall economy indicates that the May reading (48.7 percent) corresponds to a change of plus-1.7 percent in real gross domestic product (GDP) on an annualized basis."

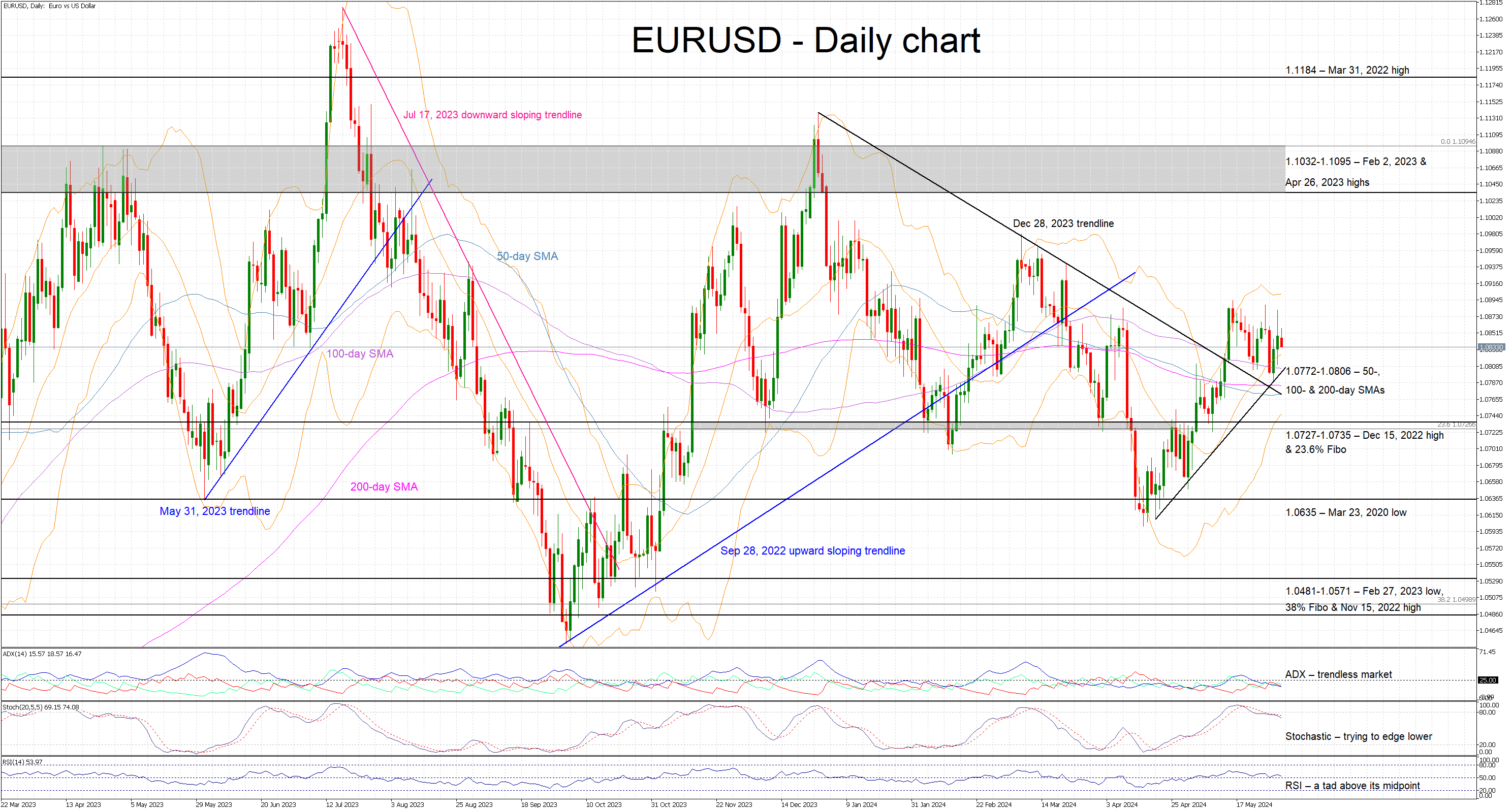

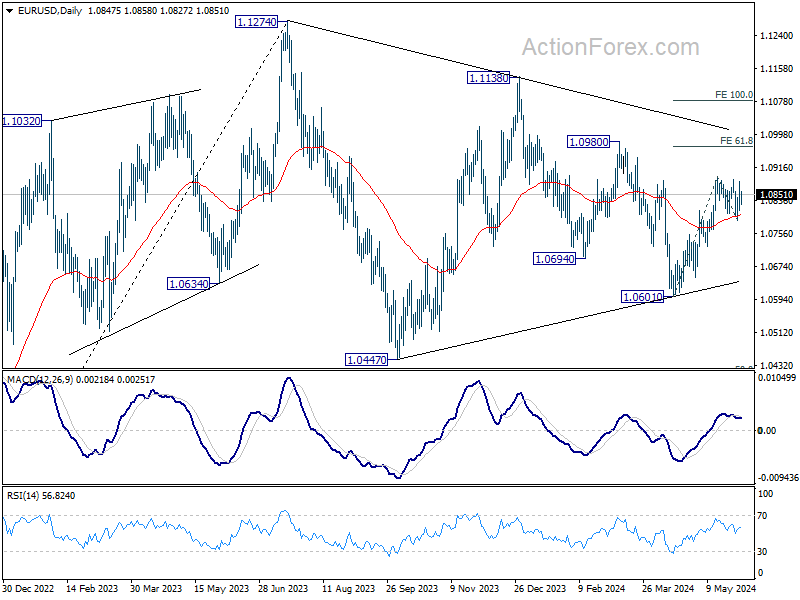

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0812; (P) 1.0847; (R1) 1.0883; More….

No change in EUR/USD's outlook as range trading continues. Intraday bias stays neutral at this point. On the upside, firm break of 1.0894 will resume whole rally from 1.0601, and target 61.8% projection of 1.0601 to 1.0894 from 1.0788 at 1.0969. For now, risk will stay on the upside as long as 1.0788 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

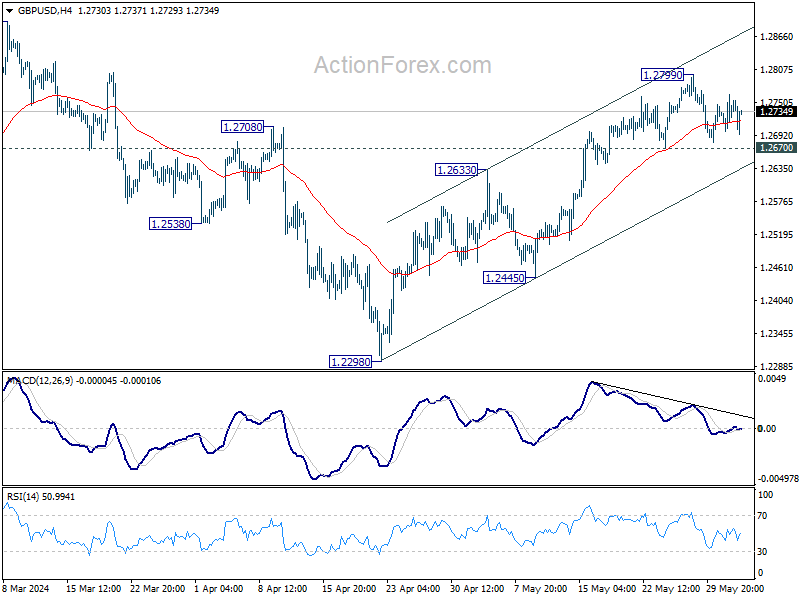

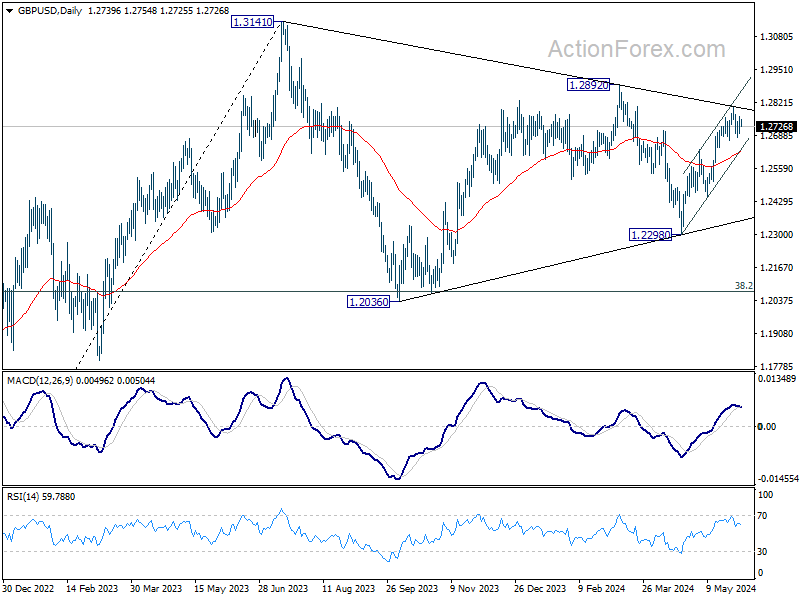

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2706; (P) 1.2736; (R1) 1.2772; More….

GBP/USD is stay in consolidation from 1.2799 and intraday bias remains neutral. Further rise is expected as long as 1.2670 support holds. Above 1.2799 will resume the rally from 1.2298 and target 1.2892 resistance. However, break of 1.2670 will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

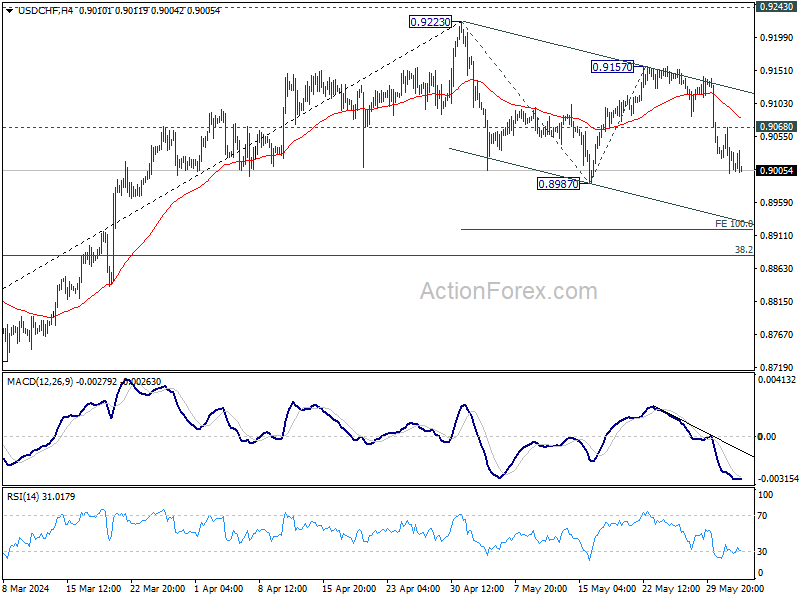

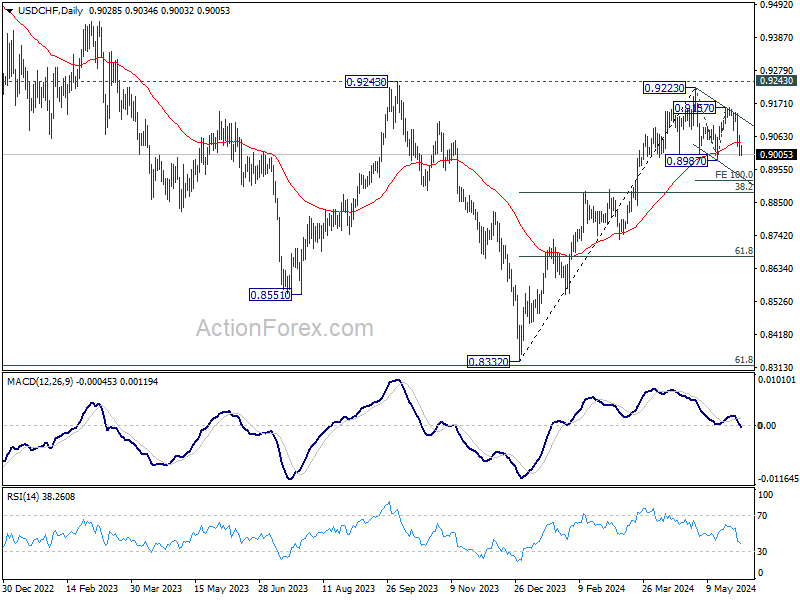

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8995 (P) 0.9032; (R1) 0.9061; More….

No change in USD/CHF's outlook and intraday bias stays on the downside for 0.8987 support. Firm break there will resume whole fall from 0.9223 and target 100% projection of 0.9223 to 0.8987 from 0.9157 at 0.8921. On the upside, above 0.9065 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

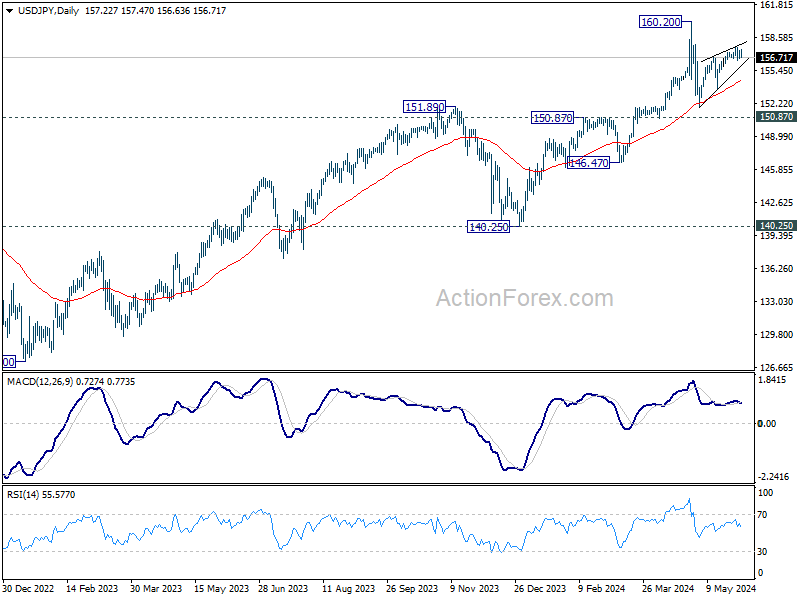

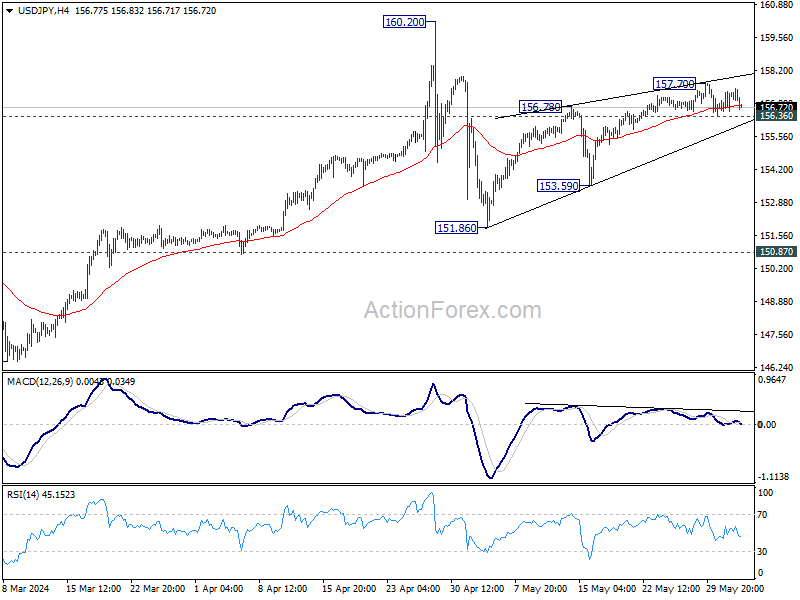

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.77; (P) 157.07; (R1) 157.58; More….

USD/JPY dips mildly today but stays in range of 156.36/157.70. Intraday bias remains neutral for the moment. On the downside, decisive break of 156.36 minor support will confirm short term topping at 157.70, on bearish divergence condition in 4H MACD. Intraday bias will be back on the downside for 153.59 support. Firm break there will target 151.86 and below as the third leg of the corrective pattern from 160.20. However, break of 157.70 will extend the rally from 151.86 towards 160.20.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.