Sample Category Title

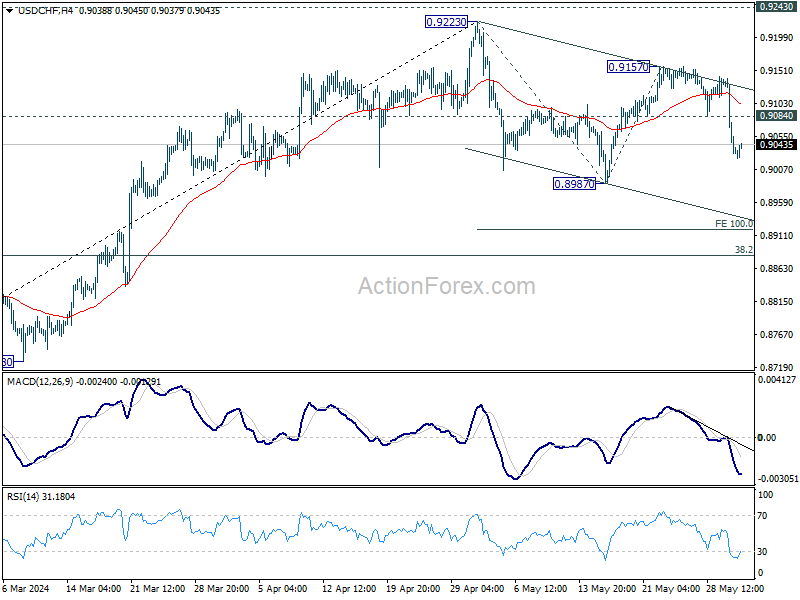

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8995; (P) 0.9070; (R1) 0.9110; More....

Intraday bias in USD/CHF remains on the downside at this point. Fall from 0.9157 is seen as the third leg of the pattern from 0.9223. Deeper fall would be seen to 0.8987 support. Break will target 100% projection of 0.9223 to 0.8987 from 0.9157 at 0.8921. On the upside, above 0.8904 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

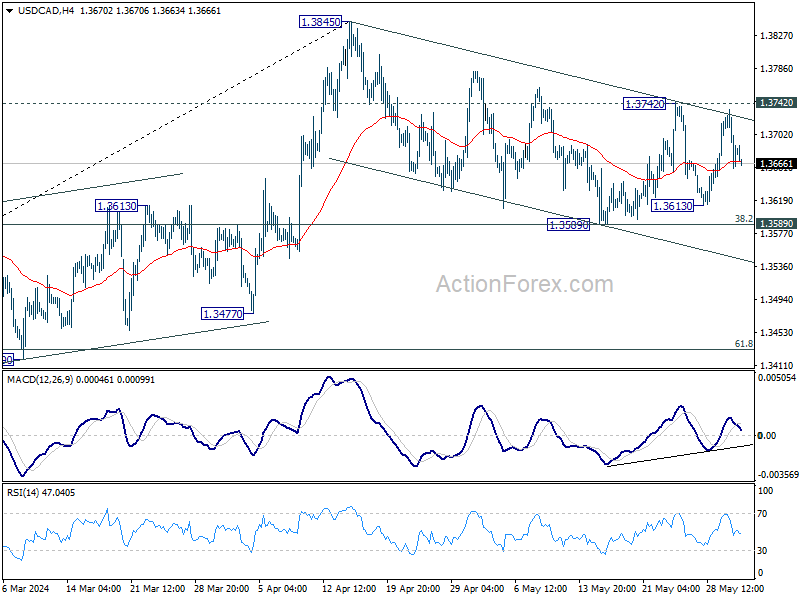

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3650; (P) 1.3692; (R1) 1.3725; More...

Range trading continues in USD/CAD and intraday bias stays neutral at this point. On the upside, break of 1.3742 resistance will revive the case that correction from 1.3845 has completed at 1.3589. Intraday bias will be back on the upside for retesting 1.3845. On the downside, firm break of 1.3589 support will argue that whole rise from 1.3176 has completed at 1.3845 already. Fall from 1.3845 should then resume to 61.8% retracement of 1.3176 to 1.3845 at 1.3432.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

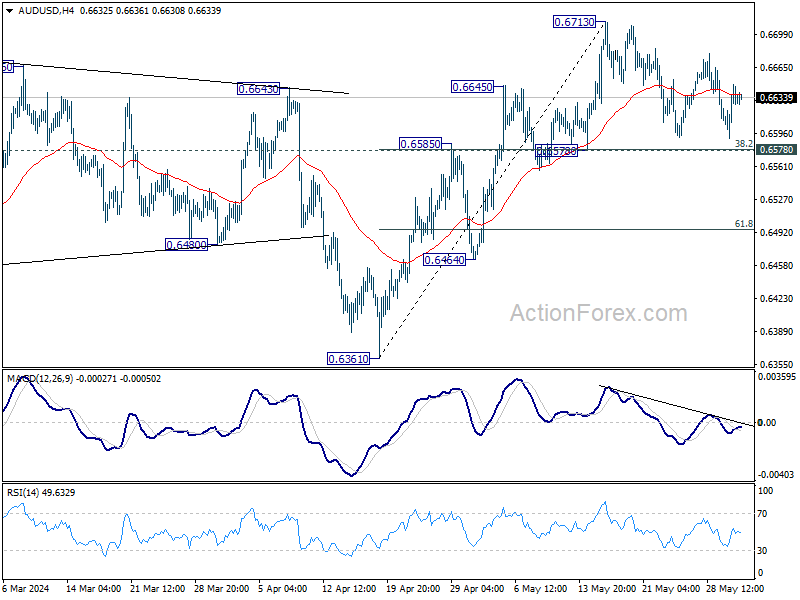

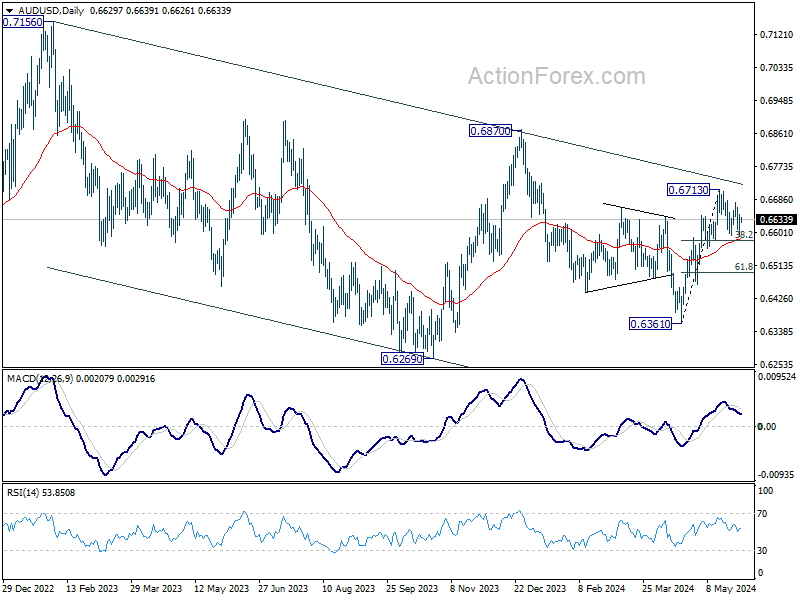

AUD/USD Daily Report

Daily Pivots: (S1) 0.6599; (P) 0.6624; (R1) 0.6656; More...

AUD/USD is staying in consolidation from 0.6714 and intraday bias remains neutral. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Inflation Data from Eurozone and US Takes Center Stage

Dollar continues its struggle to find direction, and stay in familiar range against most major currencies except against Swiss Franc. Markets shift their focus to the upcoming release of April US PCE data for guidance. Currently Fed fund futures are indicating a 50/50 chance of a rate cut by September. Recent comments from Fed officials hinted at the unlikelihood of further rate hikes. However, Fed's outlook and market sentiment could shift dramatically if today's data suggests re-acceleration of inflation. But absent significant surprises, attention is likely to turn to next week's employment figures.

Euro is currently trading as as this week's weakest performer amidst anticipations for Eurozone CPI flash report. Forecasts suggest slight increase in headline CPI to 2.5% a steady core CPI at 2.7%. With ECB nearly set to introduce the first rate cut of this cycle next week, a subsequent rate cut in July seems improbable, as the central bank aims to manage market expectations carefully. Traders are poised to look beyond today's figures, focusing on next week's rate decision and forthcoming economic projections.

Overall in the markets, Swiss Franc is maintaining its position as the strongest for the week, followed by Yen and Australian Dollar. Euro ranks as the weakest, trailed by British Pound and Canadian Dollar, with Dollar and New Zealand Dollar mixed in the middle.

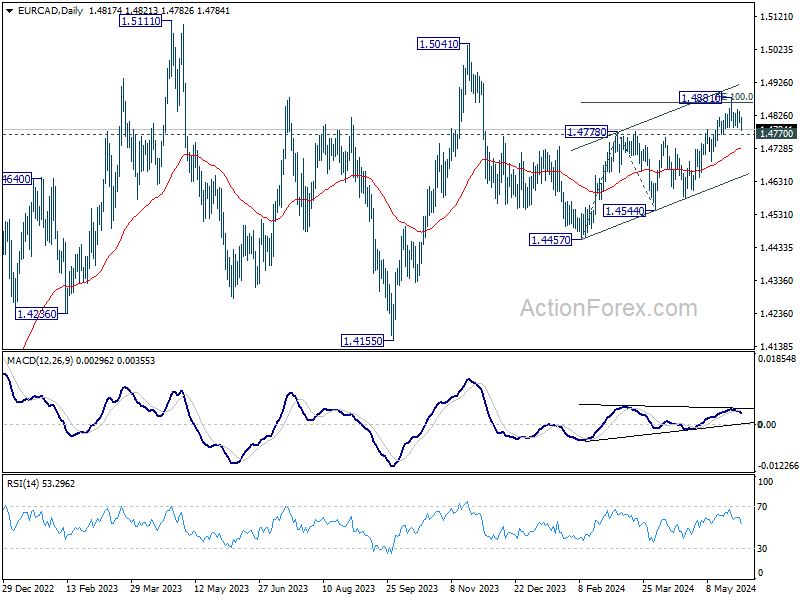

Given that Canada will release GDP data, EUR/CAD would be an interesting one to watch today. Break of 1.4770 support would confirm short term topping at 1.4881. More importantly, in this case, corrective rebound from 1.4457 could have completed too after hitting 100% projection of 1.4457 to 1.4478 from 1.4544. Deeper fall would be seen to 55 D EMA (now at 1.4729). Sustained break there will raise the chance that fall from 1.5041 is ready to resume through 1.4457.

In Asia, at the time of writing, Nikkei is up 1.11%. Hong Kong HSI is up 1.06%. China Shanghai SSE is up 0.04%. Singapore Strait Times is up 0.27%. Japan 10-year JGB yield is up 0.0115 is up 1.071. Overnight, DOW fell -0.86%. S&P 500 fell -0.60%. NASDAQ fell -1.08%. 10-year yield fell -0.070 to 4.554.

Fed's Williams: Policy well-positioned, unlikely to see further rate hikes

New York Fed President John Williams told CNBC overnight that current monetary policy is "well-positioned" and "restrictive" enough to help bring inflation down to target levels. He added that further rate hikes are unlikely, stating, "I don't see that as the likely case."

Williams highlighted that interest rates in the US will "eventually need to come down" based on data analysis, but the timing will depend on how effectively the Fed achieves its goals. He expects inflation to moderate in the second half of this year as the economy finds better balance and global inflationary pressures ease.

However, Williams emphasized, "Inflation is still above our 2% longer-run target, and I am very focused on ensuring we achieve both of our dual mandate goals."

Fed's Bostic: No rate hikes expected, but inflation risks remain

Atlanta Fed President Raphael Bostic told Fox Business overnight that he does not expect further rate hikes to be necessary to bring inflation down to the target. However, he cautioned that if inflation were to reaccelerate, "I'd have to take on board the likelihood that a rate increase is appropriate."

Bostic emphasized the need for economic data to show the economy is "sufficiently strong" and that inflation is moving closer to Fed's 2% target before supporting any rate cuts, but he clarified, "That's not my outlook today." He anticipates that inflation will decrease "very slowly" over the year, reaching 2% target by 2025 or later.

Fed's Logan: Interest rates may be less restrictive than anticipated

Dallas Fed President Lorie Logan suggested at an event overnight that interest rates might not be "as restrictive as" policymakers had anticipated.

Emphasizing the need for flexibility, she added, "It's really important to keep all options on the table and that we continue to be flexible."

Nevertheless, Logan also noted there are "good reasons" to believe that inflation is heading back to 2%, " perhaps a bit slower and a little bit clunkier maybe than we thought at the beginning of the year."

Japan's Tokyo CPI core rises in May, industrial production weakens in Apr

In May, Japan's Tokyo CPI core (excluding fresh food) increased from 1.6% yoy to 1.9% yoy, matching expectations. This rise was primarily driven by higher electricity costs. However, CPI core-core (excluding food and energy) slowed slightly from 1.8% yoy to 1.7% yoy. Private sector service inflation also decreased from 1.6% yoy to 1.4% yoy. The headline CPI saw an uptick from 1.8% yoy to 2.2% yoy.

April's industrial production declined by -0.1% mom, falling short of the anticipated 1.5% mom rise. The Ministry of Economy, Trade, and Industry maintained its assessment that industrial production "showed weakness while fluctuating indecisively." Among the 15 industrial sectors surveyed, seven reported lower output, while eight saw increases. Manufacturers expect output to rise by 6.9% in May before falling by -5.6% in June.

Additionally, April's retail sales jumped by 2.4% yoy, surpassing the expected 1.9% increase. Unemployment rate remained steady at 2.6%.

China's manufacturing PMI falls back into contraction in May

China's official PMI Manufacturing index fell from 50.4 to 49.5 in May, below the expected 50.5, indicating contraction after two months of expansion. The new manufacturing export order subindex also dropped significantly to 47.2 from 50.6 in April, highlighting weakening external demand.

PMI Non-Manufacturing index ticked down slightly from 51.2 to 51.1, missing the expectation of 51.5. Within this sector, the construction new order subindex decreased to 44.1 from 45.3, and the service sector business activity subindex declined to 47.4 from 50.3, showing reduced activity.

PMI Compositewhich combines manufacturing and non-manufacturing data, fell from 51.7 to 51.0, indicating a slowdown in overall economic activity.

Looking ahead

Eurozone CPI flash is the main focus in EUropean session. Germany import prices and retail sales, Swiss retail sales, France consumer spending, UK mortgage approvals will also be released. Later in the day, Canada will publish GDP. US will release personal income and spending, PCE inflation, and Chicago PMI.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6599; (P) 0.6624; (R1) 0.6656; More...

AUD/USD is staying in consolidation from 0.6714 and intraday bias remains neutral. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y May | 2.20% | 1.80% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y May | 1.90% | 1.90% | 1.60% | |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y May | 1.70% | 1.80% | ||

| 23:30 | JPY | Unemployment Rate Apr | 2.60% | 2.60% | 2.60% | |

| 23:50 | JPY | Industrial Production M/M Apr P | -0.10% | 1.50% | 4.40% | |

| 23:50 | JPY | Retail Trade Y/Y Apr | 2.40% | 1.90% | 1.20% | 1.10% |

| 01:30 | AUD | Private Sector Credit M/M Apr | 0.50% | 0.40% | 0.30% | 0.40% |

| 01:30 | CNY | NBS Manufacturing PMI May | 49.5 | 50.5 | 50.4 | |

| 01:30 | CNY | NBS Non-Manufacturing PMI May | 51.1 | 51.5 | 51.2 | |

| 05:00 | JPY | Housing Starts Y/Y Apr | 13.9% | -0.20% | -12.80% | |

| 06:00 | EUR | Germany Import Price Index M/M Apr | 0.50% | 0.40% | ||

| 06:00 | EUR | Germany Retail Sales M/M Apr | 0.10% | 1.80% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Apr | 0.20% | -0.10% | ||

| 06:45 | EUR | France GDP Q/Q Q1 | 0.20% | 0.20% | ||

| 08:30 | GBP | Mortgage Approvals Apr | 62K | 61K | ||

| 08:30 | GBP | M4 Money Supply M/M Apr | 0.40% | 0.70% | ||

| 09:00 | EUR | Eurozone CPI Y/Y May P | 2.50% | 2.40% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May P | 2.70% | 2.70% | ||

| 12:30 | CAD | GDP M/M Mar | 0.00% | 0.20% | ||

| 12:30 | USD | Personal Income M/M Apr | 0.30% | 0.50% | ||

| 12:30 | USD | Personal Spending Apr | 0.30% | 0.80% | ||

| 12:30 | USD | PCE Price Index M/M Apr | 0.30% | 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y Apr | 2.70% | 2.70% | ||

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.30% | 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 2.80% | 2.80% | ||

| 13:45 | USD | Chicago PMI May | 40 | 37.9 |

Cliff Notes: In Need of Capacity

Key insights from the week that was.

In Australia, the Monthly CPI Indicator rose to 3.6%yr in April, from 3.5%yr in March and 3.4%yr in January and February. By sub-category, there were various differences relative to expectations which offset one another – a notable increase in prices for clothing and footwear (+4.0%mth) and a pull-forward of the health insurance premium increase met by another fall in electricity prices, principally due to another round of energy rebates in Tasmania (–1.9%mth). While the latest figures point to a slight upside surprise for the Q2 CPI, subsequent updates – especially the quarterly services components next month – will be crucial for gauging the balance of risks into mid-year.

This week’s consumer and housing updates came in on the softer side. Growth in nominal retail sales printed a feeble 0.1% (1.3%yr) in April, continuing the past six months’ very subdued trend. Falling retail prices in certain segments may be partially to blame, though underlying volumes clearly remain weak. Meanwhile, the –0.3% decline in dwelling approvals points to a fragile outlook for new dwelling investment, at odds with the needs of a rapidly growing economy.

In the lead-up to next week’s Q1 GDP report, the ABS also released two partial indicators of investment.

Construction activity surprised materially to the downside, contracting –2.9% in Q1. Declines were recorded across both private and public sectors (–2.4% and –4.3%) and were broad-based across segments, with non-residential building works particularly weak (–7.0%). The sharp decline in hours worked in the sector was the likely culprit behind the moderation in activity. That said, there remains a sizeable pipeline of construction projects yet to be completed and, given the extra boost to the pipeline from recent Federal and State Government budgets, construction activity has scope to remain at a high level.

The Q1 CAPEX survey subsequently reported a 1.0% lift in capital expenditure. Spending on machinery and equipment, which feeds into GDP, posted a solid 3.3% lift, while building and structures moderated, –0.9%, the mining sector acting as a drag across both segments. On spending intentions, the second estimate for 2024/25 CAPEX plans remained optimistic, up 13% compared to the second estimate a year ago. In our view, this implies an 8.3% rise in nominal CAPEX spending over the financial year, or roughly 5.25% on an inflation-adjusted basis. Constructive for the medium-term outlook, businesses still see a need to build capacity and alleviate constraints.

Our Q1 GDP preview will be published later today on WestpacIQ. Looking further out, Chief Economist Luci Ellis’ essay this week investigates the key risks Australia and its policymakers face as we seek to return inflation to target and foster a recovery in GDP growth to or above trend.

Following Australia’s Budget a fortnight ago, this week it was New Zealand’s turn. Spending and revenue forecasts have both been lowered, and the return to surplus delayed. For all the detail, see Westpac New Zealand Economics’ Budget report.

In the US this week, the Federal Reserve's May Beige Book pointed to subdued conditions across the economy. 10 of 12 districts reported "slight or modest growth", and the remaining 2 no growth. Retail spending was little changed, with "lower discretionary spending " observed. Growth in housing demand was also modest, population and the labour market were supportive but affordability and borrowing capacity remain significant headwinds.

The Beige Book’s view on labour market momentum remains at odds with nonfarm payrolls but in line with the household survey, eight districts reporting "negligible to modest job gains, and the remaining four Districts reported no changes in employment". Commentary around headcounts suggests a mixed picture. Some districts reported businesses increasing headcounts, while others allowed headcounts to shrink through natural attrition. Businesses are seemingly taking down the ‘need help’ sign as the economy slows.

Helpfully for services inflation, "Several Districts reported that wage growth was at pre-pandemic historical averages or was normalizing toward those rates". Price increases were considered modest, consumers pushing "back against additional price increases ". Evident here is that discounts are becoming necessary to entice consumers to spend.

Looking at the economy as a whole, US Q1 GDP growth was revised marginally lower in the second estimate to 1.3% annualised (prev 1.6%), primarily as a result of softer consumption. After a strong 2023, consumption growth in Q1 is now estimated at a below-trend 2.0% annualised. What's more, April retail sales (released earlier in the month) suggests this moderation in growth continued into Q2. A moderation in growth to, or slightly below trend, will alleviate remaining concerns over inflation and allow the FOMC to ease from late-2024.

Over in Europe, the unemployment rate edged down to 6.4% in April. Continued strength in the labour market data highlights lingering risks for wage growth and services inflation. We expect the ECB to begin their cutting cycle next week at their June meeting, but subsequent easing will be modest in scale and pace, with momentum and risks to be assessed meeting by meeting.

The Grumpy Hawk and Other Scenarios

Current slow growth should start to pick up in the second half of 2024 as the factors weighing on household incomes ease. Scenarios that could send things off track include geopolitics, sticky domestic inflation and ongoing consumer weakness.

Growth in economic activity is expected to be soft in the first half of 2024, driven by weak consumer spending. Beginning in the second half of the year, it will gradually pick up as the factors weighing on household income ease and consumer spending recovers.

Inflation is falling, despite the upside surprise in the March quarter and April month. Monetary policy is restrictive and helping to dampen discretionary spending and so domestic inflation. Wages growth has already peaked; the March quarter result for the Wage Price Index was slightly below our expectations and the detail suggests that this was not simply noise. This implies that domestic labour cost pressures have peaked.

With the RBA in data-dependent mode, surprises in the data flow could change the timing of rate cuts, but not the underlying decision process. The RBA Board recognises that monetary policy is currently contractionary. At some point, it must reduce that restrictive stance and return to something closer to a level it considers to be ‘neutral’. Otherwise, inflation would eventually decline below the target range. Because monetary policy works with a lag, rate cuts need to start before inflation has returned to target.

The question the RBA Board will be asking itself is what it needs to see to be confident that inflation will return to target soon. The likely trajectory of disinflation from here precludes a rate cut much before November. Trimmed mean inflation was still a full percentage point above the top of the target range over the year to the March quarter. Services inflation – a key focus for the RBA Board at present – remains elevated. It will take time for enough evidence to accumulate to convince the Board that the disinflation is on track. But if things turn out as we expect, a forward-looking central bank would want to start reducing the restrictiveness of policy by about November.

What could send things off track from our base case?

As always, there are many shocks that could push outcomes away from our base case. Most of these would be inflationary rather than deflationary. For example, geopolitical tensions could boost energy prices or global goods prices via trade restrictions or a further increase in shipping costs. Domestic supply chain capacity also appears to be still quite constrained relative to peer economies. A few upside and downside scenarios are of particular note.

Upside scenarios

The main thing that would cause the RBA to shift its first rate cut later is inflation remaining sticky above the target range. Recent communication from the Board has focused on services prices, which include non-discretionary services such as rent and insurance where inflation has been very high recently. Inflation in discretionary goods and services is much lower and in many cases is already back in the 2¬–3% target range. It is possible that consumer spending recovers more than expected in response to tax cuts and other fiscal support measures, and so pressure on firms to limit price increases wanes. The spending plans implied by responses in the Westpac–Melbourne Institute Consumer Sentiment survey would suggest that this is a lower probability scenario than previously thought. But after such a long period of cost-of-living pressure, households might instead want to unwind past cutbacks quickly.

Another possible pathway to a later start to the rate-cutting phase would be a stronger outlook for labour costs than expected. This could occur if the Fair Work Commission decision scheduled for Monday awards a larger increase to award and minimum wage rates than we expect, and other bargaining streams follow. Our wages growth forecasts assume an outcome around 4½% but anywhere in the 4–4 ½% range seems reasonable. Another scenario in this vein would be if productivity remains low because of domestic supply constraints, which would also imply that unemployment remains lower than expected. Again, given our analysis pointing to the productivity slump unwinding, this seems unlikely.

A more plausible, and pessimistic, scenario is one where domestic demand and especially consumption remain soft, but supply-driven inflation in key sectors such as housing, insurance, health and especially energy keeps aggregate inflation too high for the RBA Board’s comfort. This ‘grumpy hawk’ scenario would see weak consumer sentiment and a softening labour market collide with difficulties expanding supply in these key sectors.

A particular risk is the domestic energy cost outlook. In Europe, gas prices escalated sharply after Russia’s invasion of Ukraine, but then unwound almost as quickly. By contrast in Australia, the forces pushing up electricity and gas prices are largely home-grown and stickier. Ongoing rebates may manage to ‘tunnel through the mountain’ and meet up with a falling wholesale price on the other side. On current information, though, governments in Australia could end up needing to extend rebates even further to avoid a delayed escalation in household energy bills in a year’s time.

Downside scenarios

There is not enough time for the RBA to see enough evidence of a downside surprise to move much before November. Even if June quarter CPI is much weaker than we expect – a low-probability event – the RBA will want to see more than one quarter of downside before forming a conclusion.

If domestic demand growth slows rather than starting to recover over the course of this year, or the labour market starts to contract, the inflation outlook in 2025 and beyond will be noticeably weaker. If this turns out to be the case, then the RBA will probably seek to unwind the restrictive stance of policy faster than we currently assume. This would imply a faster decline to the low 3s and possibly beyond, rather than an earlier start.

There are a few ways domestic demand could fail to pick up as forecast. In the minutes of the May Board meeting, the RBA indicated that it had been surprised that households had cut back on spending even when their incomes had not fallen. This suggests that consumption has been more interest-sensitive than expected in a high-inflation context. Another possibility – as hinted at by the results of the latest consumer sentiment survey – is that consumers spend less out of the forthcoming tax cuts than they normally would out of extra income.Another way inflation could be lower in the short term is if the unwind in goods inflation turns out to be larger than we or the RBA expect. Currently, the RBA assesses that the disinflation in goods prices is complete. The detail of the April CPI also points to more upside than downside risk in prices of clothing and some other consumer durables. But if demand remains soft, discounting could resume.

Another way inflation could be lower in the short term is if the unwind in goods inflation turns out to be larger than we or the RBA expect. Currently, the RBA assesses that the disinflation in goods prices is complete. The detail of the April CPI also points to more upside than downside risk in prices of clothing and some other consumer durables. But if demand remains soft, discounting could resume.

China’s manufacturing PMI falls back into contraction in May

China's official PMI Manufacturing index fell from 50.4 to 49.5 in May, below the expected 50.5, indicating contraction after two months of expansion. The new manufacturing export order subindex also dropped significantly to 47.2 from 50.6 in April, highlighting weakening external demand.

PMI Non-Manufacturing index ticked down slightly from 51.2 to 51.1, missing the expectation of 51.5. Within this sector, the construction new order subindex decreased to 44.1 from 45.3, and the service sector business activity subindex declined to 47.4 from 50.3, showing reduced activity.

PMI Compositewhich combines manufacturing and non-manufacturing data, fell from 51.7 to 51.0, indicating a slowdown in overall economic activity.

Japan’s Tokyo CPI core rises in May, industrial production weakens in Apr

In May, Japan's Tokyo CPI core (excluding fresh food) increased from 1.6% yoy to 1.9% yoy, matching expectations. This rise was primarily driven by higher electricity costs. However, CPI core-core (excluding food and energy) slowed slightly from 1.8% yoy to 1.7% yoy. Private sector service inflation also decreased from 1.6% yoy to 1.4% yoy. The headline CPI saw an uptick from 1.8% yoy to 2.2% yoy.

April's industrial production declined by -0.1% mom, falling short of the anticipated 1.5% mom rise. The Ministry of Economy, Trade, and Industry maintained its assessment that industrial production "showed weakness while fluctuating indecisively." Among the 15 industrial sectors surveyed, seven reported lower output, while eight saw increases. Manufacturers expect output to rise by 6.9% in May before falling by -5.6% in June.

Additionally, April's retail sales jumped by 2.4% yoy, surpassing the expected 1.9% increase. Unemployment rate remained steady at 2.6%.

Fed’s Logan: Interest rates may be less restrictive than anticipated

Dallas Fed President Lorie Logan suggested at an event overnight that interest rates might not be "as restrictive as" policymakers had anticipated.

Emphasizing the need for flexibility, she added, "It's really important to keep all options on the table and that we continue to be flexible."

Nevertheless, Logan also noted there are "good reasons" to believe that inflation is heading back to 2%, " perhaps a bit slower and a little bit clunkier maybe than we thought at the beginning of the year."

Fed’s Bostic: No rate hikes expected, but inflation risks remain

Atlanta Fed President Raphael Bostic told Fox Business overnight that he does not expect further rate hikes to be necessary to bring inflation down to the target. However, he cautioned that if inflation were to reaccelerate, "I'd have to take on board the likelihood that a rate increase is appropriate."

Bostic emphasized the need for economic data to show the economy is "sufficiently strong" and that inflation is moving closer to Fed's 2% target before supporting any rate cuts, but he clarified, "That's not my outlook today." He anticipates that inflation will decrease "very slowly" over the year, reaching 2% target by 2025 or later.