Sample Category Title

Focus for Global Trading on EMU and US Inflation Data Series

Markets

The bond market sell-off/curve steepener from earlier this week yesterday ran into resistance. Data were not really high-profile but at least didn’t push a continuation of the ascent in yields. Going into today’s EMU Flash CPI, Spanish May inflation (headline HICP 3.8%, core 3.0%) was close to expectations. US Q1 GDP was slightly downwardly revised, both for the activity components (overall growth 1.3% Q/Qa from 1.6%, consumption 2.0% from 2.5%) and for the price indices (core PCE deflator 3.6% from 3.7%). Admittedly, this is a bit of old news. Nevertheless, after recent upleg in yields it helped to support a correction. US yields eased between 4.8 bps (2-y) and 6.5 bps (5 & 10-y). Bunds still underperformed with yields declining between 2.3 bps (2-y) and 3.8 bps (10-y). Fed Williams as usual kept a balanced assessment. He sees current policy as restrictive enough to continue a gradual disinflation process. Contrary to some other governors he currently sees no compelling evidence of a higher neutral policy rate. Dallas Fed President Lorie Logan has a different bias as she stated that policy might be less restrictive than policymakers anticipated. Lower yields this time only had a mixed impact on equities. The EuroStoxx 50 rebounded modestly (+0.38%), but US indices stayed in red (Nasdaq -1.08%). Still the dollar reversed most of Wednesday’s jump higher. DXY dropped from the 105.15 resistance are to close near 104.72. USD/JPY also eased from the 157+ levels as markets pondered the chances/risks of renewed yen interventions (close 156.82). EUR/USD rose from sub 1.08 levels but gains were modest (close 1.0832).

This morning, risk sentiment on most Asian markets turns positive. US yields are little changed after yesterday’s setback as is the dollar. Later today, the focus for global trading is on the EMU and US inflation data series. EMU headline inflation is expected to slow from 0.6% M/M to 0.2% M/M. However, due to unfavourable base effects, the Y/Y measure likely reaccelerated to 2.5% from 2.4%. Core inflation is expected unchanged at 2.7%. In the US, the report on the April personal income and spending also contains the (core) PCE deflators. The core measure is expected to slow to 0.2% M/M from 0.3% (Y/Y unchanged at 2.8%). Considering yesterday’s price moves, probably an upside surprise is needed for yields to go higher from current levels. The short-term momentum on the dollar turned fairly neutral. Still EUR/USD is captured in a gradual downside pattern. A break below 1.08 could reinforce some further return action lower in the 1.09/1.0724 ST trading range.

News & Views

Inflation in Tokyo accelerated in May with the headline figure picking up from 1.8% to 2.2%. The measure excluding fresh food prices moved higher from 1.6% to 1.9%. Filtering additionally for energy, however, prices rose at a slightly slower pace of 1.7%. This reveals the impact of the government’s renewable energy surcharge introduced this month, jolting electricity prices by 13% y/y. Other government policy is making a proper assessment of actual price pressures even more difficult. It is phasing out previous energy subsidies but has education subsidies in the capital in place. The latter are depressing services inflation to 0.7% y/y, down from 0.8% last month. Other data published this morning showed industrial production unexpectedly declining in April but retail sales jumping 1.2% m/m after a similar sharp contraction the month before. The Japanese yen doesn’t pick a clear direction on the mixed batch of data. USD/JPY retreated yesterday to 156.8 amid global core bond yields easing and is staying there this morning.

Chinese official (government) PMIs slightly missed expectations in May. The composite gauge eased from 51.7 to 51, mainly on an unexpected setback in manufacturing. The sector dropped back in contraction territory (49.5) after two months of minor expansion. Output grew at a slower pace (50.8) but new (export) orders (<50) suggest a more difficult period ahead. Employment continues to struggle. The non-manufacturing gauge held more or less steady at 51.1 but activity also looks vulnerable near-term with new orders still deep in contraction area (46.9). Expectations for the future are less bright than before. Input prices rose to the highest in months in manufacturing (commodities) but eased in services. China’s yuan slid on the release, giving back some of the USD-induced gains yesterday. USD/CNY rises from 7.23 in yesterday’s close to 7.24 currently.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. The 10-y is setting a new YtD top.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell indicated that further tightening was unlikely. Soft US early month data triggering a correction off YTD peak levels. However, the Fed minutes still showed internal debate whether policy is restrictive enough. Sticky inflation suggests any rate cut will be a tough balancing act. The US 10-y yield is rebounding in the 4.30/4.70% trading range.

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view but slower than expected April disinflation and a surprise general election on July 4 complicated matters. A June cut in line with the ECB looks improbable. Sterling extends a recent bull rally. A test of EUR/GBP’s 2024 YtD low (0.8489) is possible. We expect this important support level to hold.

Inflation, Inflation, Inflation

In focus today

Focus today turns to euro area inflation for May which is due 11.00 CET. After German and Spanish headline HICP came in slightly stronger than consensus, we see slight risks of a topside surprise to the euro area headline HICP consensus of 2.5% y/y. We expect headline HICP to print 2.5-2.6% y/y. As for the core HICP we expect this to be unchanged from April at 2.7% y/y, as the recent momentum in services inflation has been too strong, and we expect this to be the case for May too. Ahead of the euro area print, we receive inflation figures from France (08.45 CET), Austria (09.00 CET), Portugal (10.30 CET), and Slovenia (10.30 CET).

In the US we get Fed's favourite price gauge in the form of the PCE print for May at 14.30 CET. Consensus expectations by Reuters have analysts expecting the headline figure at 2.7% y/y, whereas they expect core PCE to print 2.8% y/y, both unchanged from the month prior.

In Norway we get May NAV unemployment figures at 10.00 CET which we expect to stand at 1.9% seasonally adjusted slightly down from April's 2.0% seasonally adjusted.

Economic and market news

What happened overnight

In the US, Donald Trump became the first ever former president to be convicted in a criminal case, as he was found guilty of all 34 charges in the so-called 'hush-money' case. Sentencing is set to take place 11 July. A January poll conducted by Bloomberg and Morning Consult found that 53% of voters in swing states said they would be unlikely to vote for him if convicted of a crime. A more recent poll by the Quinnipiac University conducted in May found 6% of Trump supporters would be less likely to vote for him if convicted of a crime. In a tight race between the former president and the incumbent president Biden, such figures could potentially mean a great deal at the 5 November election.

In China, PMIs for May disappointed to the low side, as the official PMI for the manufacturing sector dropped into retracting territory (below the 50 mark), standing at 49.5. Both March and April had seen expansions to the figure, and economists polled by Reuters had expected an unchanged print from April at 50.4. The non-manufacturing PMI stood at 51.1 (prior 51.2), and composite came in at 51.0 (prior 51.7), hence both remain in expansionary territory despite slight retractions.

In Asia, equity markets are in the green this morning, with Hong Kong in front. US equity futures look set to continue yesterday's session however, as they are in the red this morning, indicating lower prices by opening bell today.

Oil is down around 0.4% this morning with Brent trading around USD 81.6/bbl.

What happened yesterday

In the euro area, the unemployment rate declined to its all-time lowest level in April. The unemployment rate stood at 6.4% in April, with the number of unemployed persons down by 100k, to below 11m for the first time in the euro area's history. Notably, half of this decline came from Italy where the unemployment rate now stands at 6.9%. The biggest economy and country in the euro area, Germany, saw the number of unemployed persons unchanged for the fourth consecutive month.

The strong labour market combined with rising incomes and decent amounts of savings point to an uptick in private consumption this year. However, these factors also put upward pressure on domestic inflation. It is therefore natural, also considering how growth has returned to the euro area economy, that the ECB is in less of a hurry deciding on when to cut interest rates after 6 June, as the ECB has all but promised a cut at this Governing Council meeting.

In the US, growth for Q1 2024 was revised lower to 1.3% q/q (down from 1.6%) in line with market consensus as per Reuters. The downgrade came after recent soft readings in retail sales and equipment spending.

Jobless claims continued edging up in line with market expectations, as initial claims rose to 218k seasonally adjusted whereas 219k had been expected by economists according to Reuters.

In South Africa, the ruling party ANC looks set to come out of the general election as the biggest party once again, however they appear to have also lost their majority which they have held the previous 30 years. As of this morning more than 50% of the votes had been counted, and ANC stood to receive around 42% down from the 57.5% they won in the 2019 election. The new parliament will elect South Africa's next president once it has been formally constituted, and incumbent president, Ramaphosa (ANC leader), is likely to land another term, although the ANC will most likely have to form an alliance with other parties this time around.

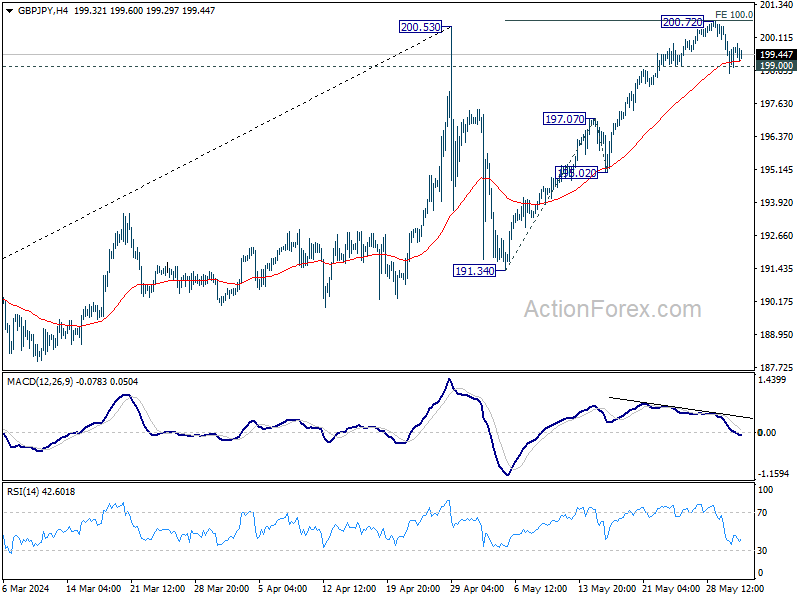

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.80; (P)199.63; (R1) 200.50; More...

Intraday bias in USD/JPY remains neutral at this point. Firm break of 199.00 support will suggest short term topping, on bearish divergence condition in 4H MACD. Rise from 191.34, as the second leg of the corrective pattern from 200.53, might have completed too. Deeper fall should then be seen to 197.07 resistance turned support next.

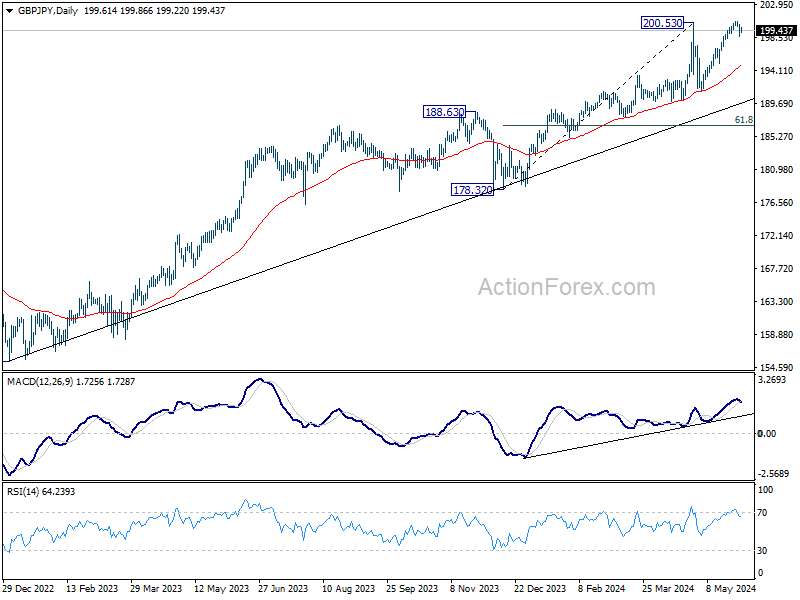

In the bigger picture, a medium term top could be in place at 200.53 after breaching 199.80 long term fibonacci level. As long as 55 W EMA (now at 185.01) holds, price actions from there is seen as correcting the rise from 178.32 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 178.32 support.

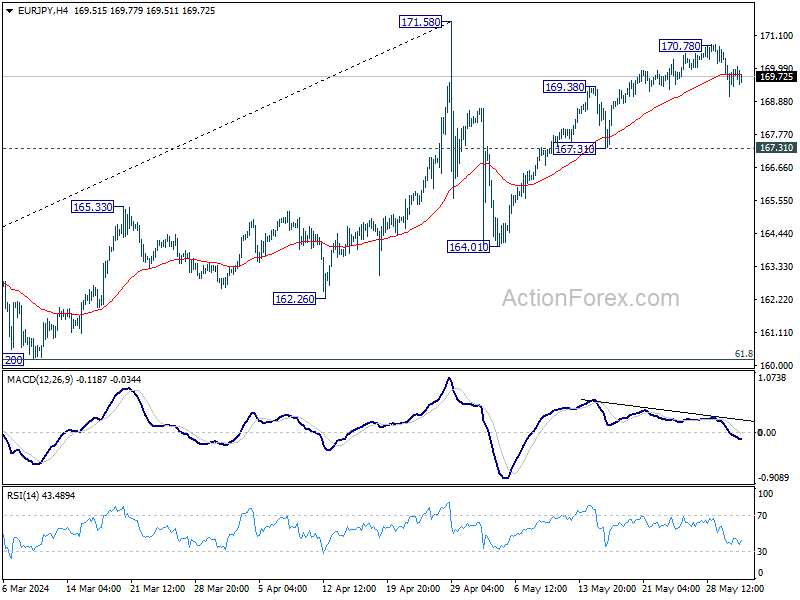

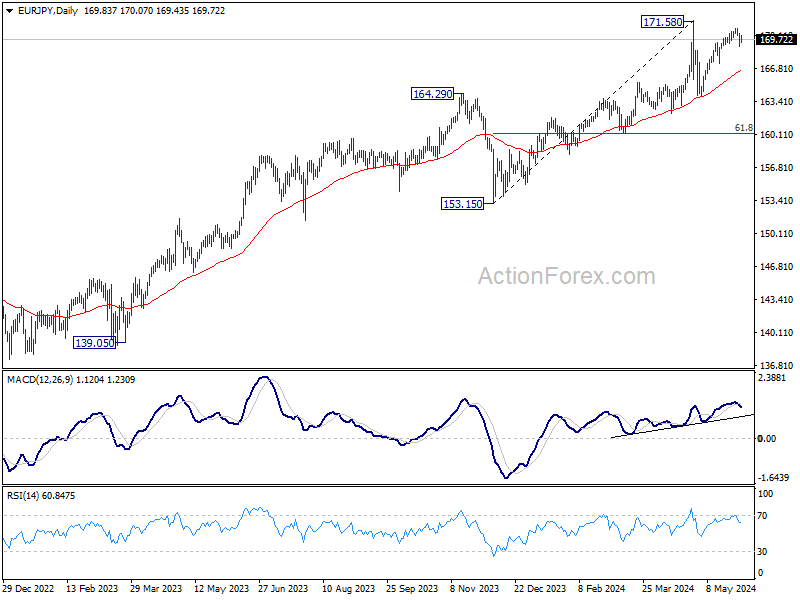

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.14; (P) 169.79; (R1) 170.52; More...

Intraday bias in EUR/JPY remains on the downside at this point. Fall from 170.78 will target 167.31 support first. Firm break there will confirm that corrective pattern from 171.58 has started the third leg, and target 164.01 support next. For now, risk will stay on the downside as long as 170.78 resistance holds, in case of recovery.

In the bigger picture, a medium top could be formed at 171.58 after brief breach of 169.96 (2008 high). As long as 55 W EMA (now at 159.10) holds, price actions from there is seen as correcting the rise from 153.15 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

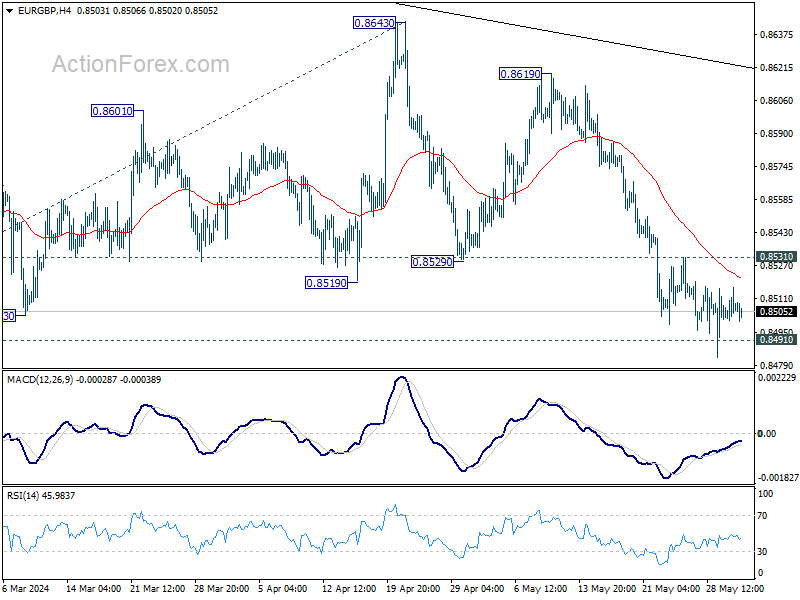

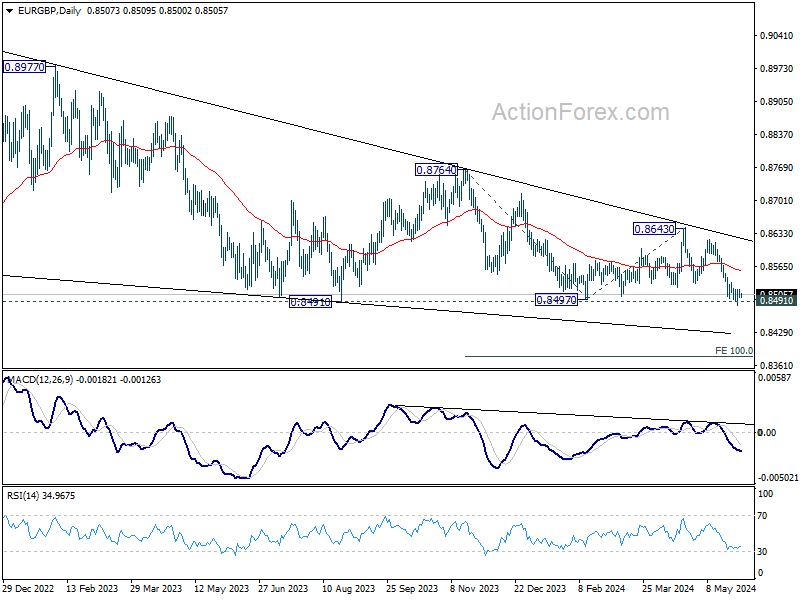

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8500; (P) 0.8509; (R1) 0.8516; More...

Intraday bias in EUR/GBP remains neutral at this point. Further decline is expected as long as 0.8531 minor resistance holds. Decisive break of 0.8491/7 will resume larger down trend to 0.8376 projection level next. On the upside, break of 0.8531 will turn bias back to the upside for stronger rebound.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

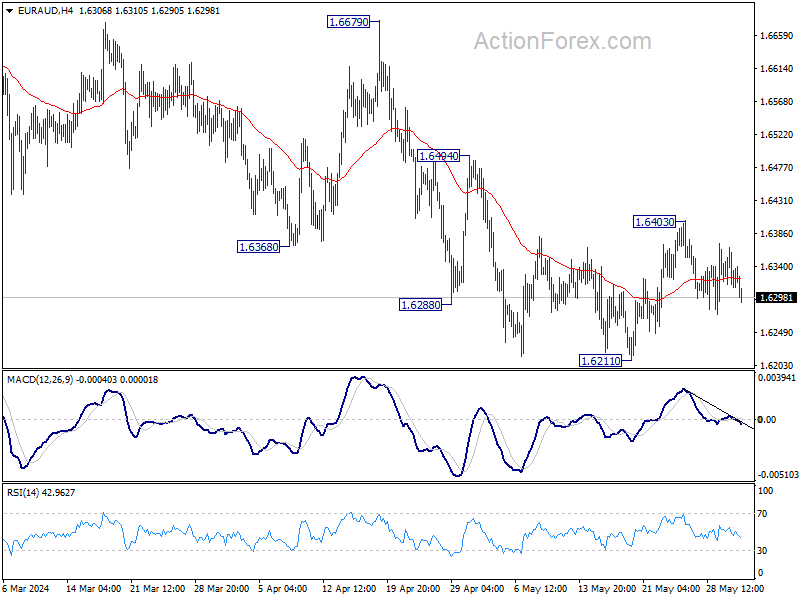

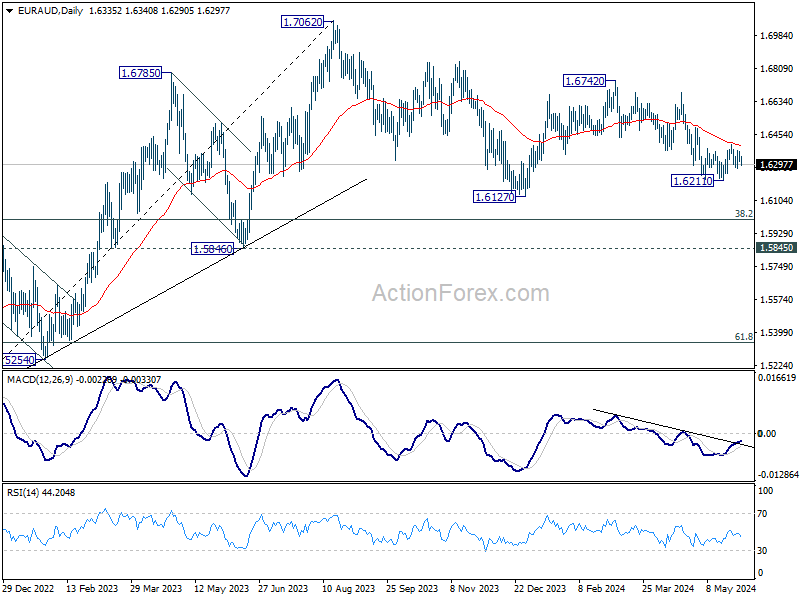

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6307; (P) 1.6338; (R1) 1.6363; More...

Range trading in EUR/AUD continues and intraday bias stays neutral at this point. On the downside, firm break of 1.6211 support will resume the whole decline from 1.6742, as the third leg of the correction from 1.7062. On the upside, above 1.6403 will resume the rebound from 1.6211 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

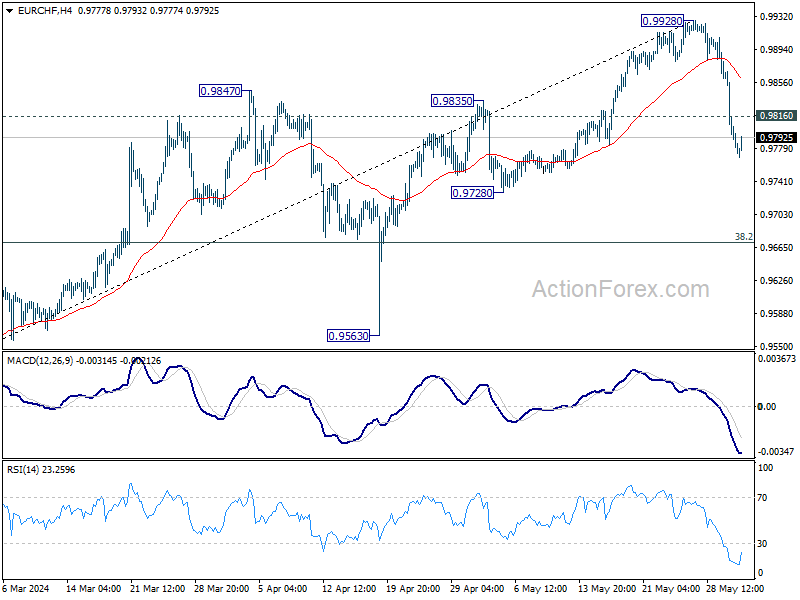

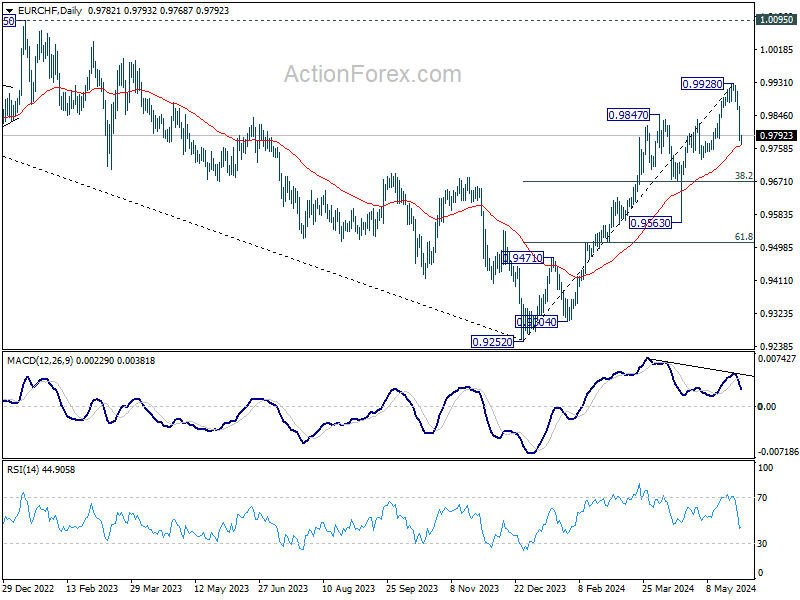

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9750; (P) 0.9817; (R1) 0.9853; More....

Intraday bias in EUR/CHF remains on the downside at this point. Firm break of 0.9728 support will carry larger bearish implications and target 38.2% retracement of 0.9252 to 0.9928 at 0.9670. On the upside, above 0.9816 minor resistance will turn intraday bias neutral first. But risk will stay mildly on the downside as long as 0.9928 resistance holds, in case of recovery.

In the bigger picture, as long as 0.9728 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004. However, firm break of 0.9728 will raise the chance of bearish reversal and turn focus to 0.9563 support for confirmation.

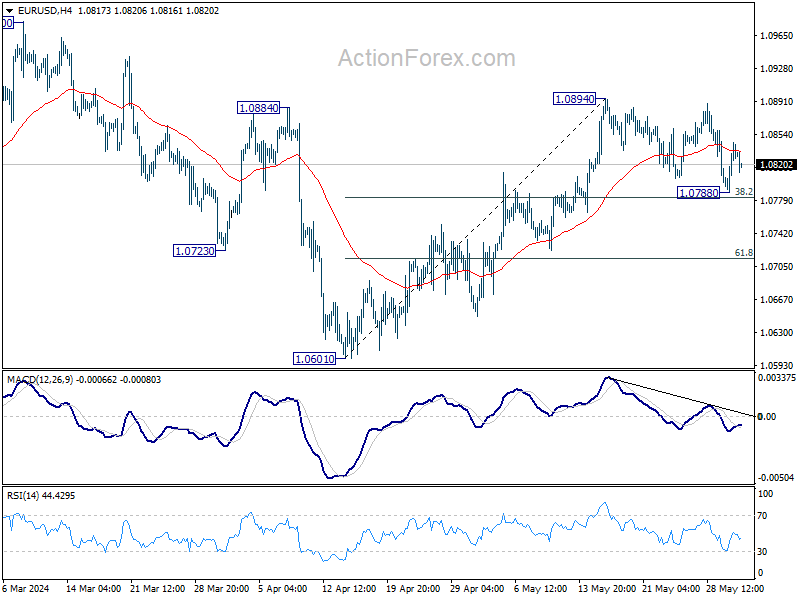

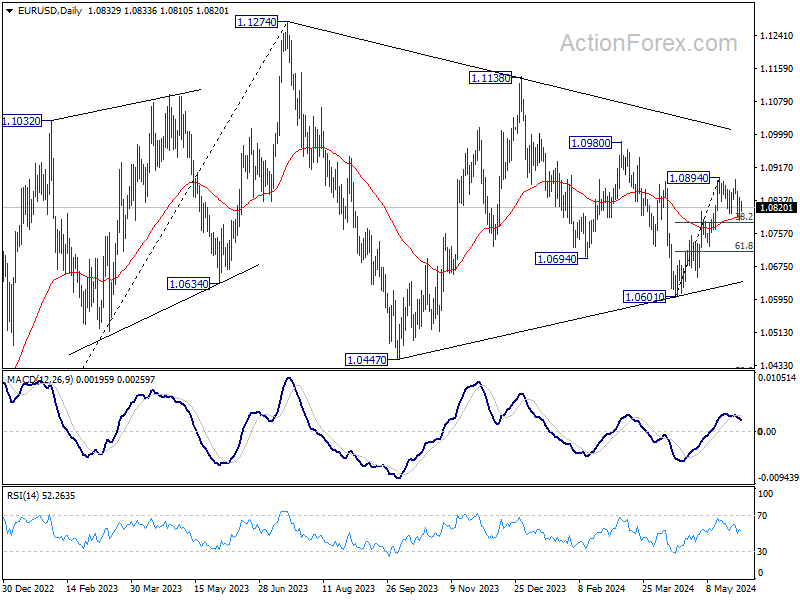

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0798; (P) 1.0822; (R1) 1.0855; More....

Intraday bias in EUR/USD stays neutral as range trading continues. On the upside, firm break of 1.0894 will resume the rise from 1.0601 towards 1.0980 resistance next. However, sustained trading below 38.2% retracement of 1.0601 to 1.0894 at 1.0782 will argue that rebound from 1.0601 has completed. Deeper fall would be seen to 61.8% retracement at 1.0713.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

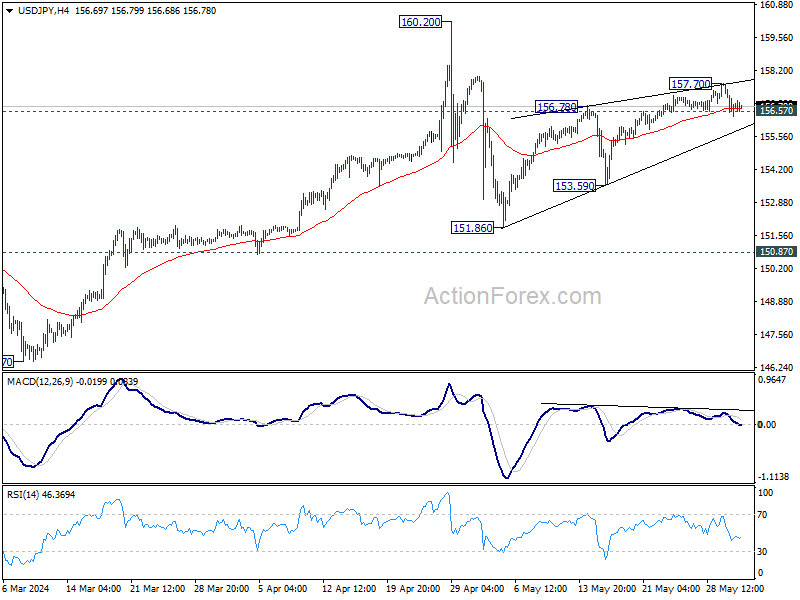

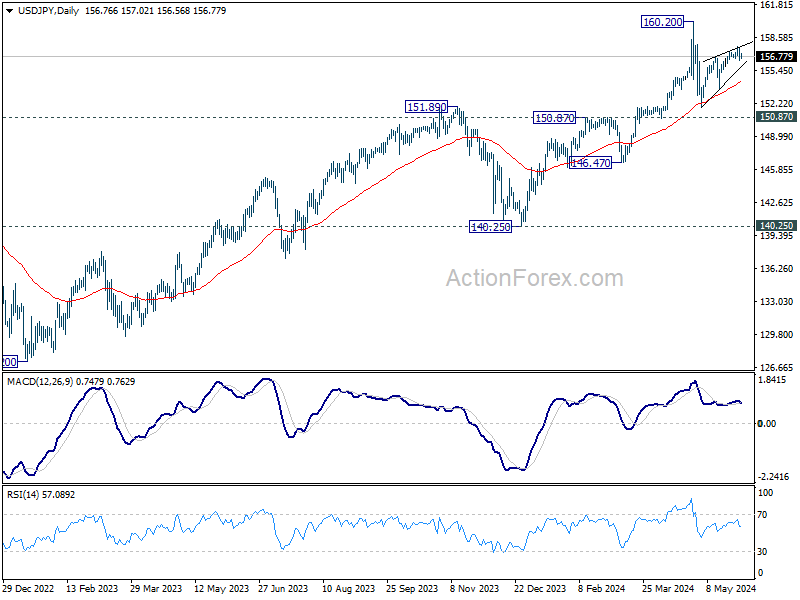

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.23; (P) 156.96; (R1) 157.54; More...

Focus stays on 156.57 minor support in USD/JPY. Decisive break there will confirm short term topping at 157.70, on bearish divergence condition in 4 H MACD. Intraday bias will be back on the downside for 153.59 support. Firm break there will target 151.86 and below as the third leg of the corrective pattern from 160.20.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

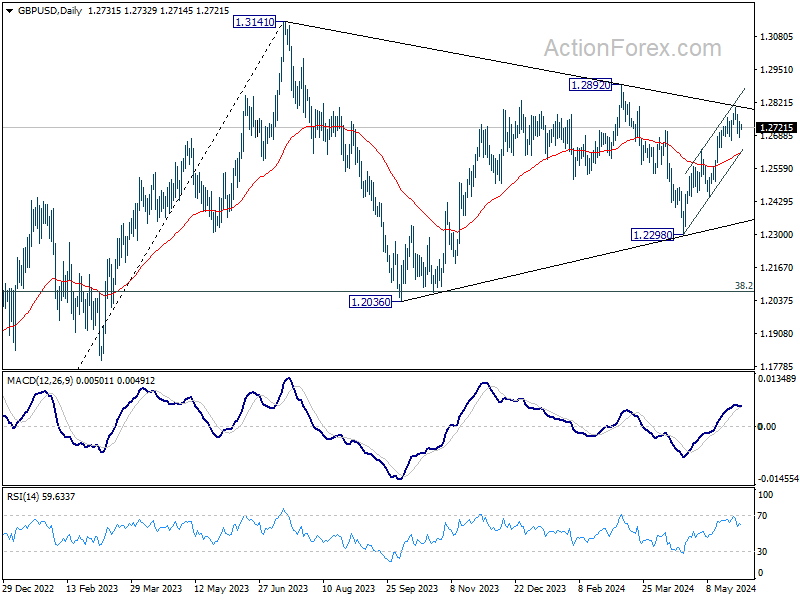

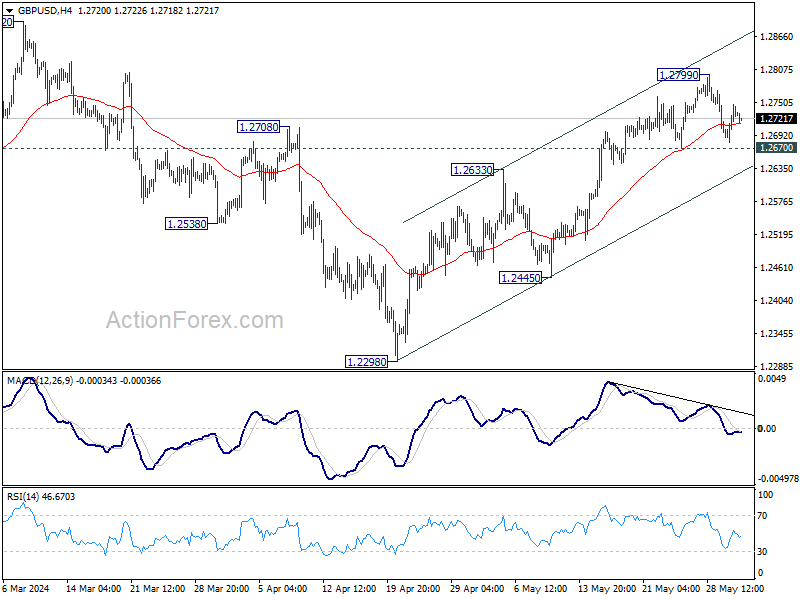

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2693; (P) 1.2721; (R1) 1.2760; More...

Intraday bias in GBP/USD remains neutral at this point and some more consolidations could be seen. Further rise is expected as long as 1.2670 support holds. Above 1.2799 will resume the rally from 1.2298 and target 1.2892 resistance. However, break of 1.2670 will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.