Sample Category Title

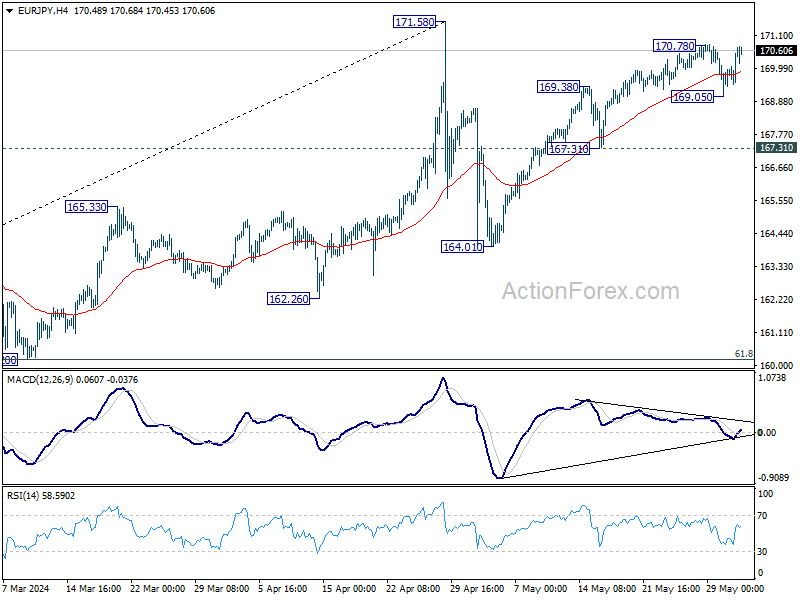

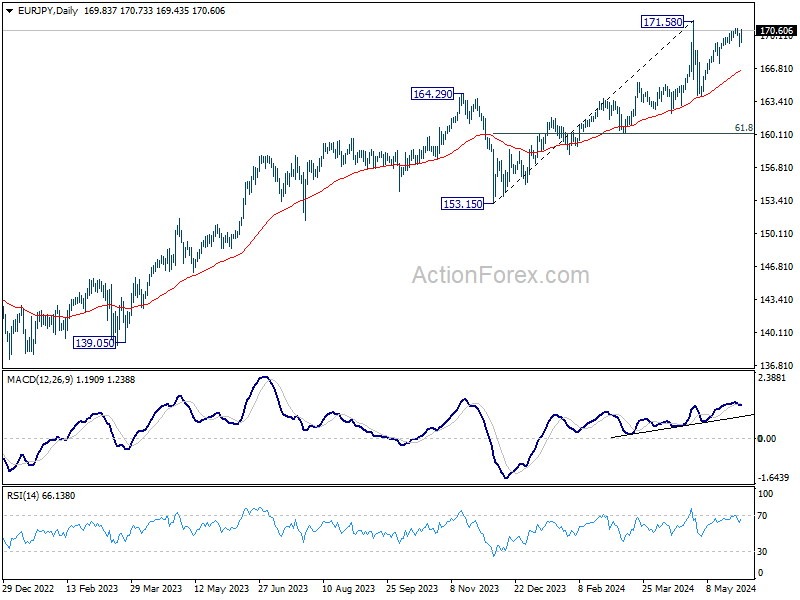

EUR/JPY Weekly Outlook

Despite dipping to 169.05 last week, EUR/JPY quickly recovered. Initial bias is neutral this week first. Break of 170.78 will resume the rally from 164.01 to retest 171.58 high. On the downside, however, below 169.05 will bring deeper fall to 167.31 support. Firm break there should confirm that rise from 164.01 has completed.

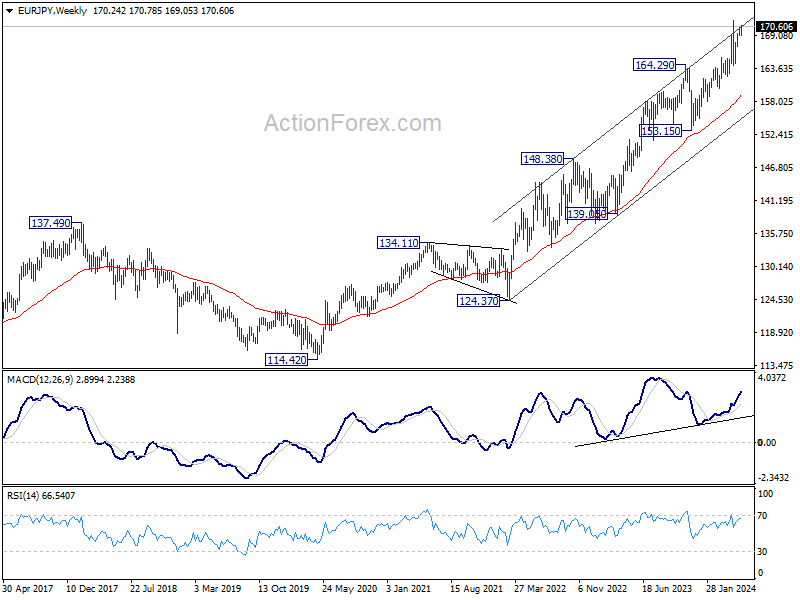

In the bigger picture, a medium top could be formed at 171.58 after brief breach of 169.96 (2008 high). But as long as 55 W EMA (now at 159.15) holds, price actions from there is seen as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

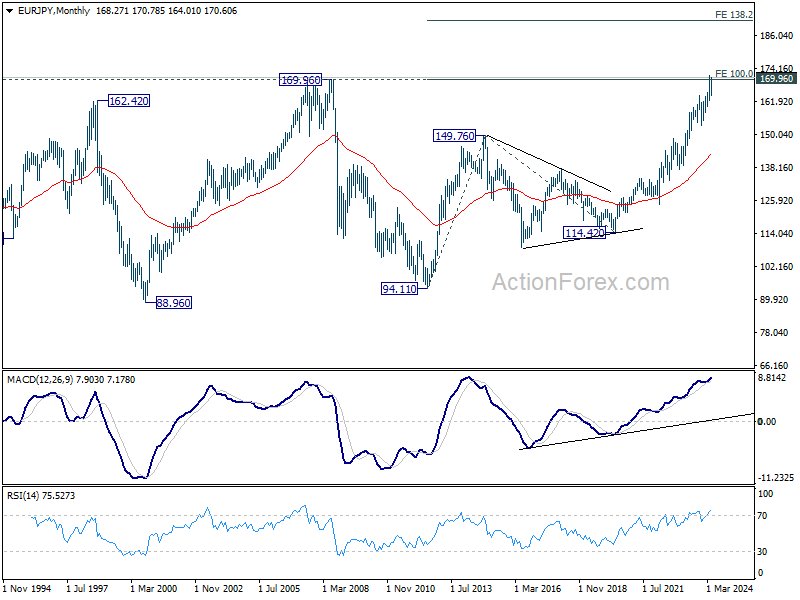

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). 100% projection of 94.11 to 149.76 from 114.42 at 170.07 was already met but there is no signal of reversal yet. Firm break of 170.07 will target 138.2% projection at 191.32. This will remain the favored case as long as 153.15 support holds.

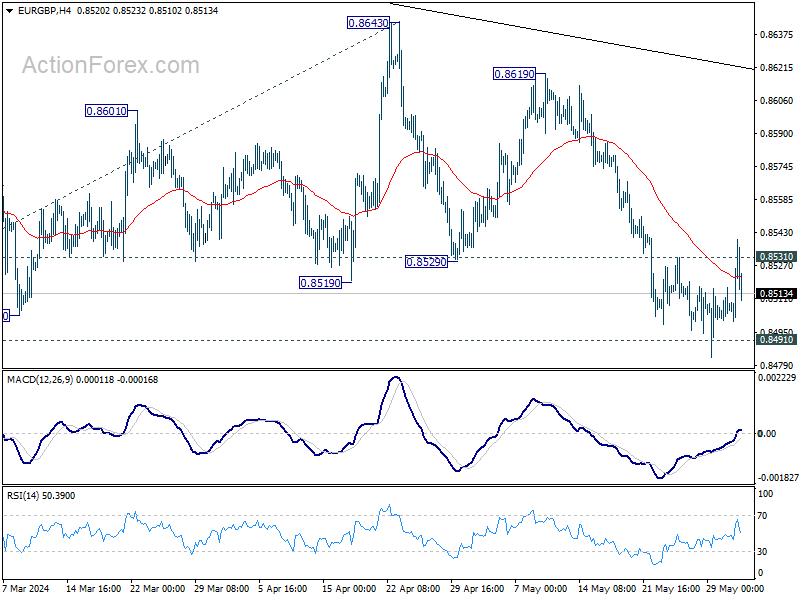

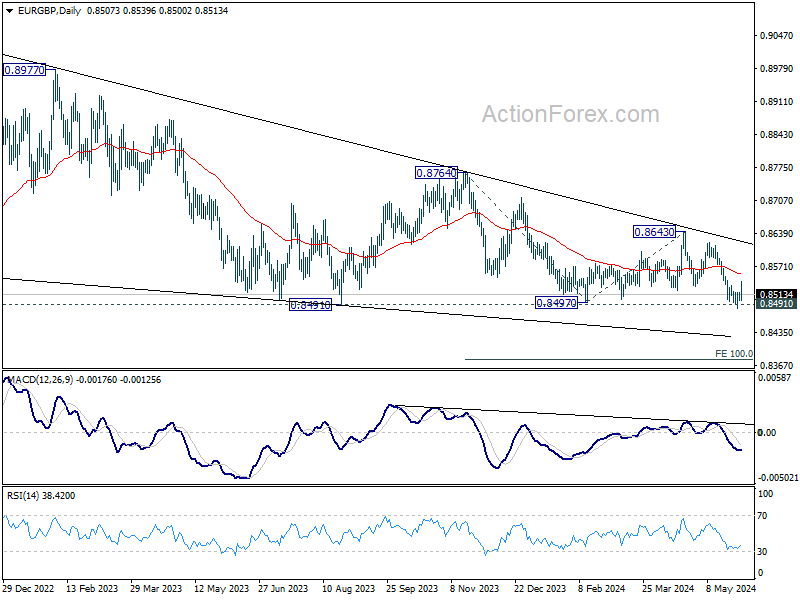

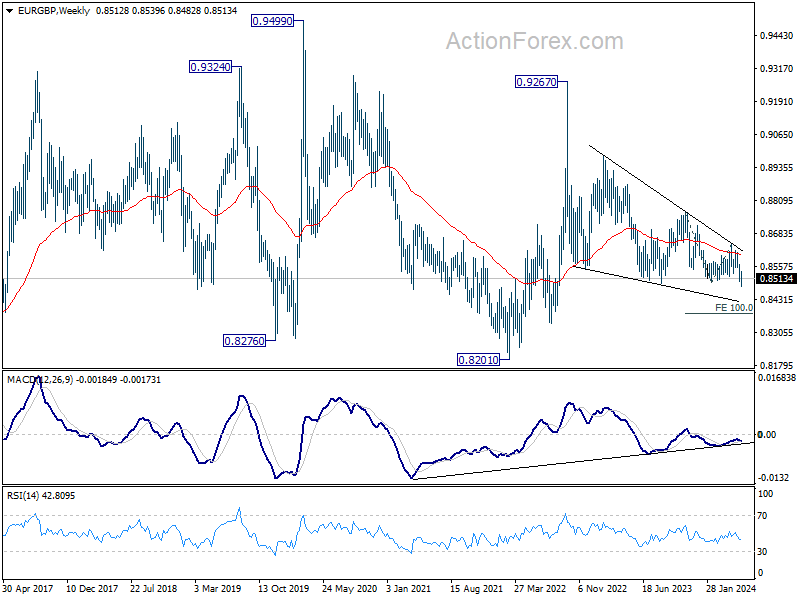

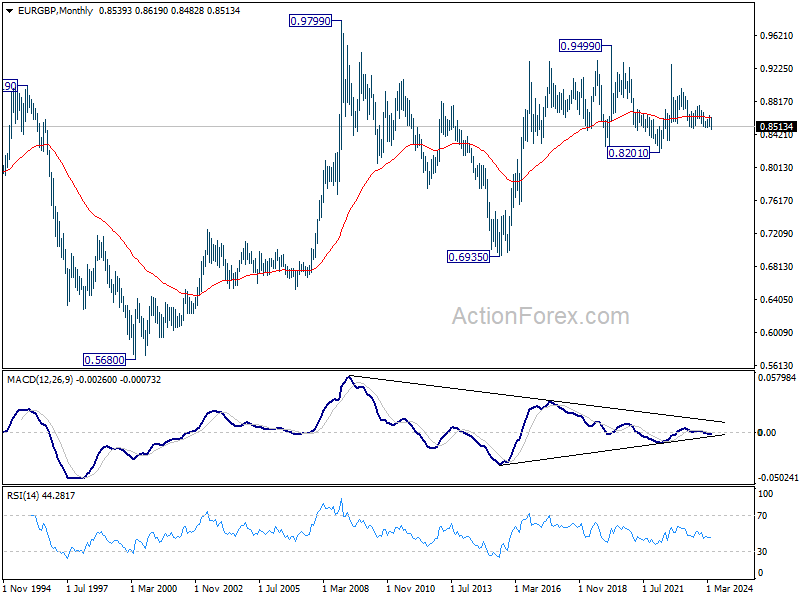

EUR/GBP Weekly Outlook

EUR/GBP breached 0.8491 key support last week but quickly recovered. Initial bias stays neutral this week first. Further decline is expected as long as 55 D EMA (now at 0.8553) holds. Decisive break of 0.8491/7 will resume larger down trend to 0.8376 projection level next. However, sustained break of 55 D EMA will turn bias back to the upside for 0.9643 resistance instead.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

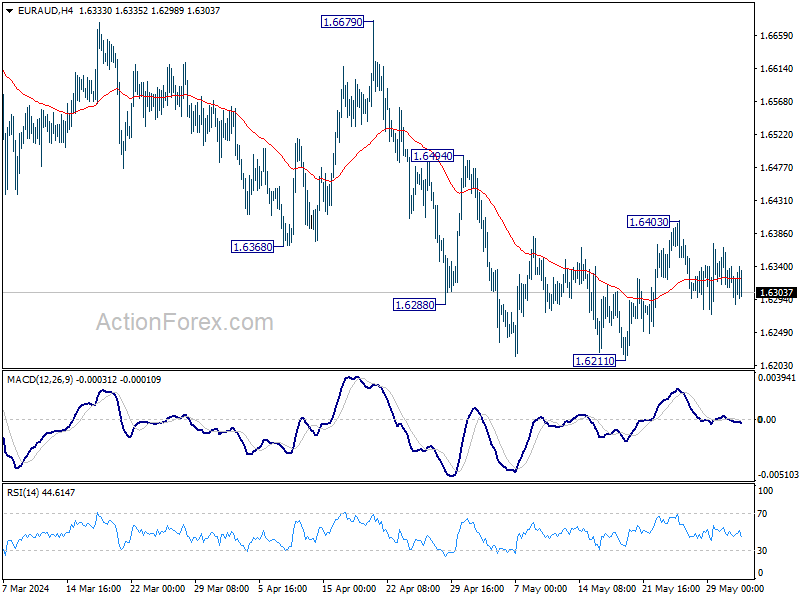

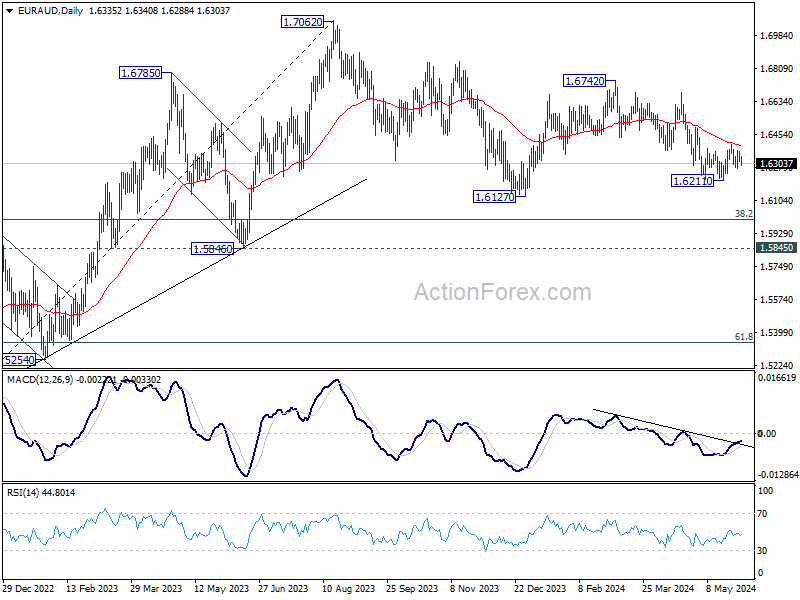

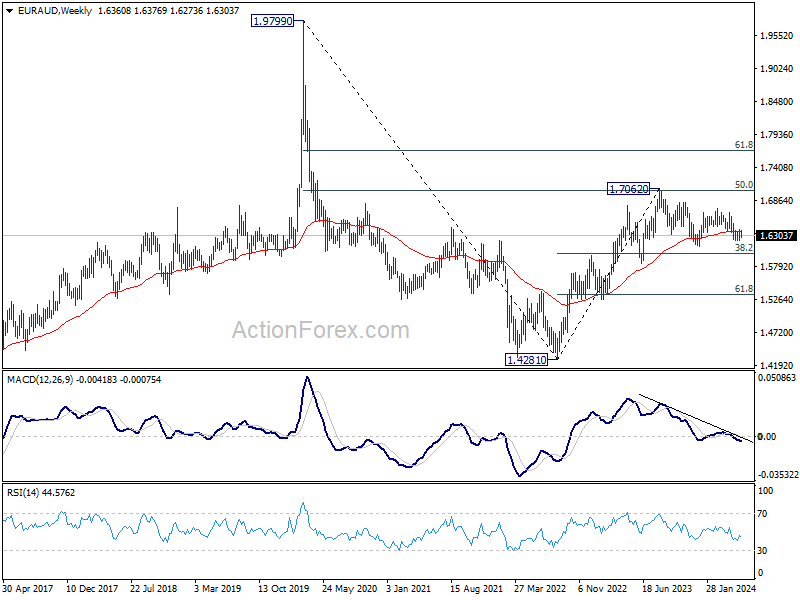

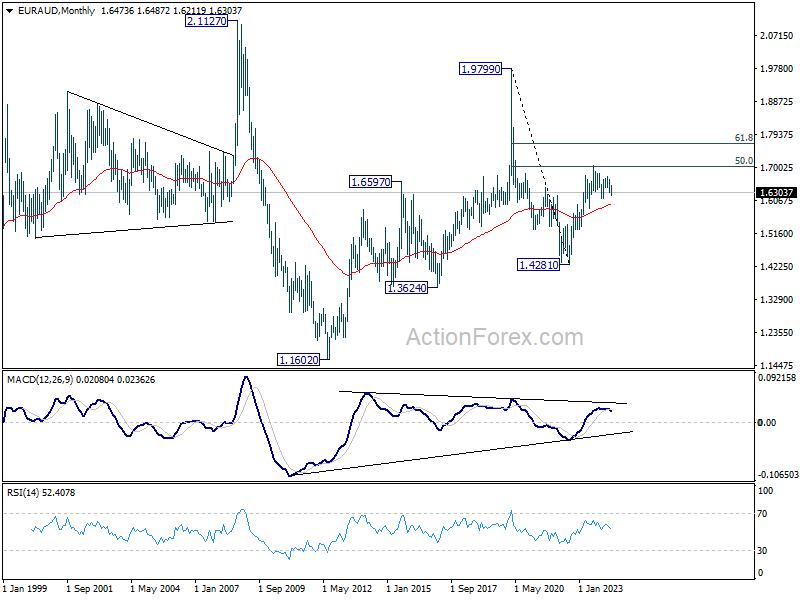

EUR/AUD Weekly Outlook

EUR/AUD stayed in consolidation above 1.6211 short term bottom last week. Initial bias stays neutral this week and more sideway trading could be seen. On the downside, firm break of 1.6211 support will resume the whole decline from 1.6742, as the third leg of the correction from 1.7062. On the upside, above 1.6403 will resume the rebound from 1.6211 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5962) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

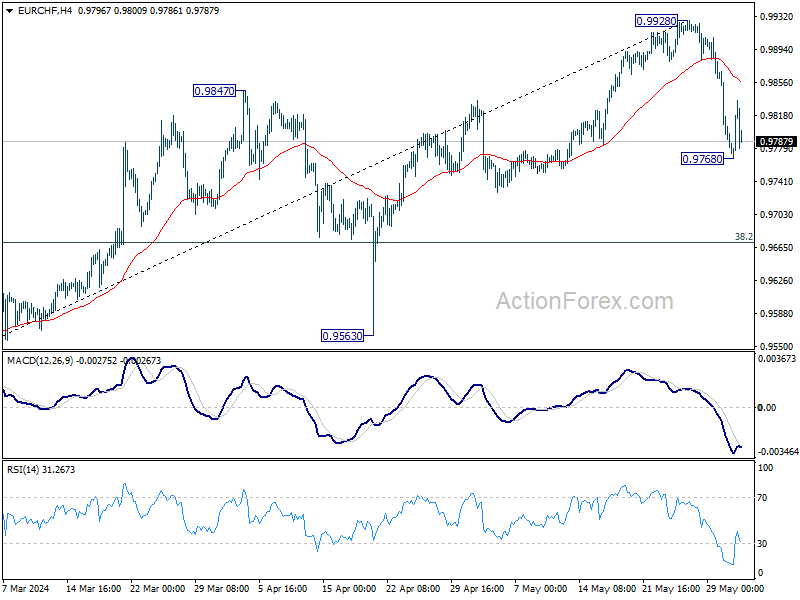

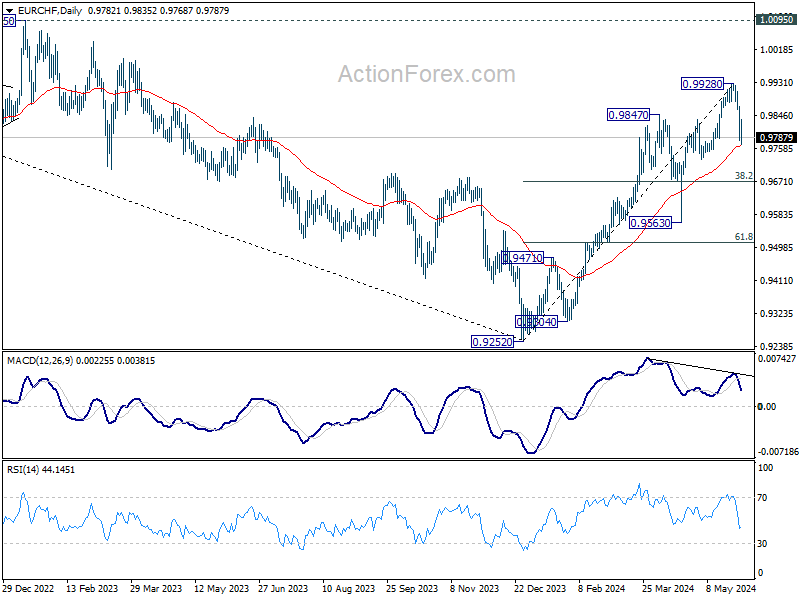

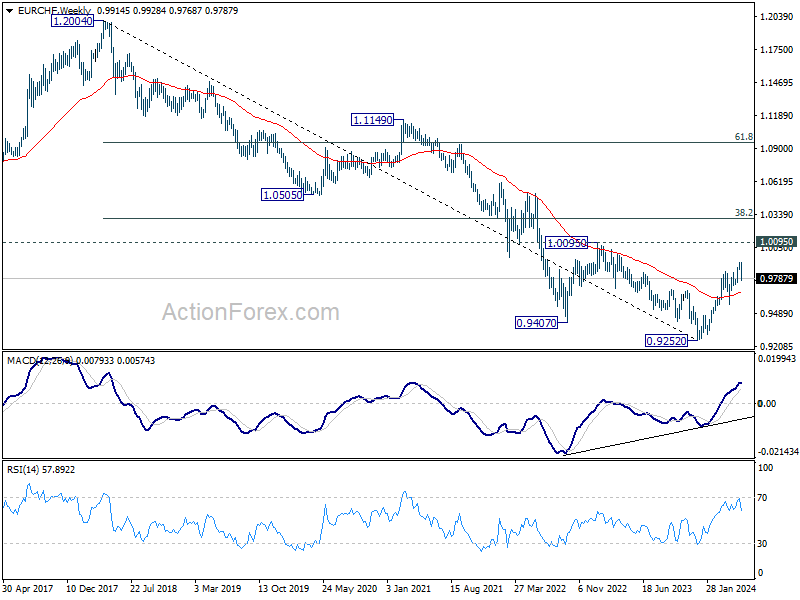

EUR/CHF Weekly Outlook

Considering bearish divergence condition in D MACD, EUR/CHF might have formed a medium term at 0.9928 with last week's steep decline. Risk will now stay mildly on the downside as long as 0.9928 resistance holds, in case of recovery. Break of 0.9768 and sustained trading below 55 D EMA (now at 0.9765), will bring deeper fall to 38.2% retracement of 0.9252 to 0.9928 at 0.9670. Strong support is expected there to complete the pull back and bring rebound.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004.

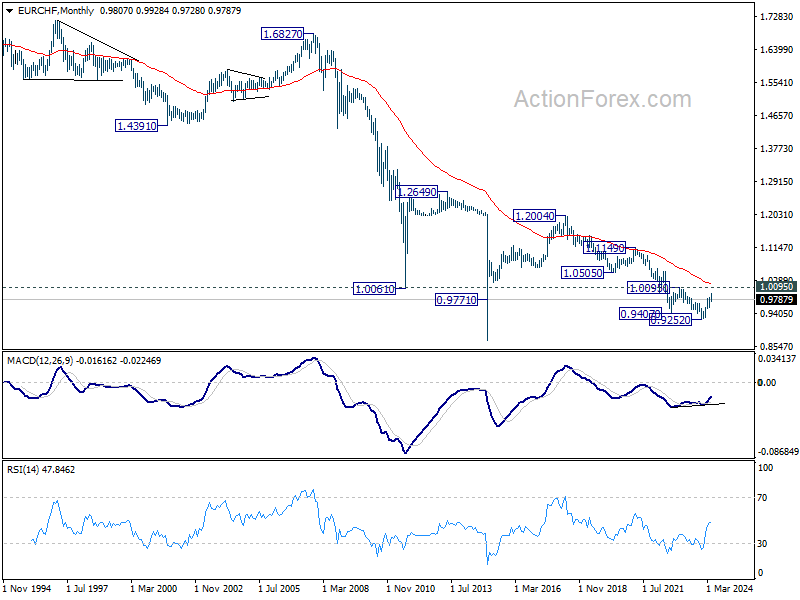

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

The Weekly Bottom Line: Bank of Canada in Focus

U.S. Highlights

- Revisions to economic growth in the first quarter featured a mark down to consumer spending.

- That theme continued in April, where a contraction in real personal consumption expenditures came as a confirmation that restrictive rates are working.

- Inflation also took another step in the right direction. But sticky services inflation still has room to fall before the Fed can feel confident that inflation has been tamed.

Canadian Highlights

- Canadian economic growth missed to the downside in the first quarter. A strong increase in domestic demand was offset by inventory drawdowns.

- As the dust settles, markets have increased their bets for a June rate cut to their highest level since the last monetary policy meeting.

- We acknowledge the risks around a cut next week, but ultimately believe the Bank of Canada will wait until July to pull the trigger.

U.S. – A Slight Downshift

Bond yields are climbing down from this week’s highs as a pair of high-profile data releases suggest the some of the steam is being let out of the U.S. economy. While there isn’t anything released this week that is going to meaningfully move the needle on the timing of the Fed’s decision, it was encouraging to see that the current restrictive policy stance is cooling the economy. That said, there is still enough strength underlying the economy to keep the Fed’s policy rate right where it is until later this year.

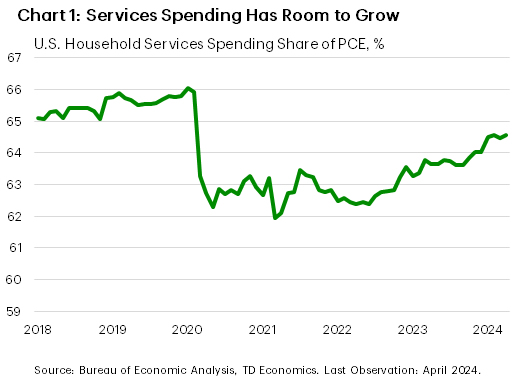

First up was the refresh of the first quarter’s GDP data. Top-line economic growth was shaved down a smidge, to a below trend 1.3% quarter-on-quarter (q/q, annualized) change. Consumer spending too was marked down, from 2.5% to a more trend-like 2.0%. That said, faced with persistently strong price growth and high interest rates, the ability of households to keep buying stuff and spending money on experiences has defied expectations. Specifically, the shift back to services spending has kept demand up on the primarily domestic portion of the economy facing a tight labor market. Moreover, there is room for this trend to run if households continue to adjust their expenditures back towards a pre-pandemic mix, where household services consumption accounted for just shy of 66% of personal consumer expenditures (compared to 64.6% as of April, Chart 1).

So, it came as a welcome surprise that April’s Personal Consumption and Expenditures (PCE) survey showed real PCE pull back 0.1% month-on-month (m/m). More good news came as the core PCE deflator edged down to 0.2% m/m, leaving the annual pace of price growth to 2.8%. That said, the three- and six-month core PCE inflation rates are still 3.5% and 3.2% (annualized), respectively, as the past few months of strong price growth continue to be felt.

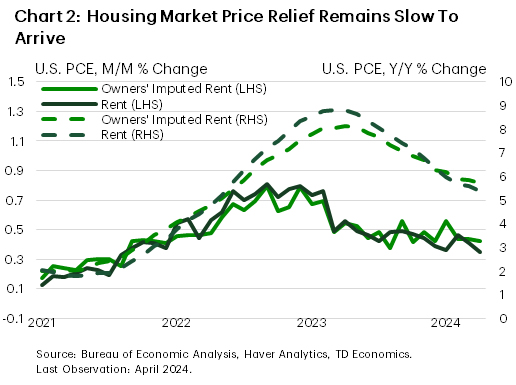

Importantly, while the deceleration in core price growth was welcome, special attention has to be paid to rents and housing costs that have been propping up core price growth. Together the two categories make up roughly 15% of PCE and will be critical to taming inflation. On this front, there was only marginal relief in April. Rent inflation came in at a “soft” 0.4% m/m (the print was 0.35% m/m unrounded). This is in line with the average reading from the prior five months (Chart 2). On the homeownership side too, implied rents came in at the same 0.4% m/m, roughly unchanged from the last few months. Sustained over a year, the 0.4% monthly pace would translate to 4.9% annual growth. The annual rates on the two shelter components are now cruising along at 5.7% and 5.4% for the imputed and actual rent measures, respectively.

For the Fed, April’s data were a step in the right direction, but there is still more work to be done before rate cuts become imminent. So now, all eyes are focused on data coming next week, and specifically the May payrolls report. After April’s real spending and payrolls data surprised to the downside, the focus will be for any signs that the month was not a one-off and weaker momentum continued into May.

Canada – Bank of Canada in Focus

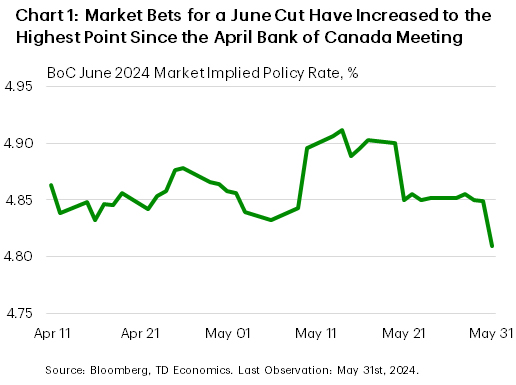

Anticipation is high for the Bank of Canada’s (BoC) interest rate decision next week. Interest rate relief is on the horizon, but the pressing question remains whether the BoC will cut in June or July. For the past several weeks bets were skewed towards June. With first quarter GDP growth missing to the downside compared to consensus and the BoC’s estimates, the scales tipped further in June’s direction, with markets pricing in nearly an 80% chance of a move. This is the most conviction markets have had since the BoC’s April 10th meeting (Chart 1), but we’d argue that an interest rate reduction next week is not a slam dunk.

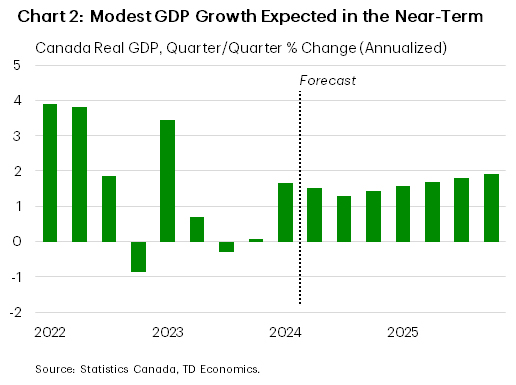

High interest rates are doing their part to cool economic activity, evidenced by the fact that economic expansion effectively flatlined for most of 2023. The Q1 GDP miss also comes on top of a downward revision to the fourth quarter, which now shows no growth. However, the details under the hood were more constructive of decent, albeit temporary, economic strength. For one, final domestic demand, a good barometer for internal economic health, grew at the fastest pace in eight quarters. Business investment and government spending contributions were also encouraging. This quarter, like many in the past two years, was heavily swayed by inventory drawdowns, which subtracted nearly 1.5 percentage points (ppts) from Canada’s GDP in Q1. We expect growth will hum along at a below-trend pace for the next several quarters (Chart 1) as the economy continues to grapple with higher interest rates.

The Bank of Canada should continue to focus their policy decisions on meeting their inflation mandate. In this sense, rate cuts have been justified for some time, especially as headline inflation has printed under 3.0% for four consecutive readings. Further, the average three month annualized change in the BoC’s preferred core measures have been sub-2% for the last two months.

Despite inflation dynamics suggesting the economy is ready for a cut, we still believe the BoC will pull the trigger in July. Firstly, Governor Macklem has only acknowledged progress, but hasn’t explicitly signaled any intention to make a move. Further, in the recent summary of deliberations, some council members stressed that the risk was lower that higher rates would slow activity more than necessary. In an effort to increase transparency and forward guidance, the Bank can use next week to tee up a July rate cut, while allowing themselves to see two more inflation prints to confirm that durable 2% price growth is in sight.

We also recently wrote about monetary policy divergence with the Federal Reserve and how much room the BoC can run on their own before risking a destabilization in the Canadian dollar. In short, this won’t be the first time that policy divergence has happened between the two central banks. Meanwhile, Governor Macklem continues to stress that the Bank will act independently. Stay tuned for Bank’s decision next week!

Weekly Economic & Financial Commentary: Amid Higher Yields, Market Inflation Expectations Remain Stable

Summary

United States: May-laise

- Markets digested a light lineup of economic data on the holiday-shortened week. The second look at first quarter GDP revealed an economy increasingly pressured by high interest rates as headline growth was revised lower. To that end, the April Personal Income and Spending report suggested consumers may be taking their foot off the gas as they round into Q2. The latest read on inflation did not show the “meaningful progress” on inflation the Fed is looking for, but it is at least consistent with cooling price growth and leaves the door open for cuts later this year.

- Next week: ISM Manufacturing Index (Mon.), JOLTS (Tue.), Employment (Fri.)

International: South Africa Heading for Coalition Government; China's Economy Remains Under Pressure

- South Africa's incumbent political party is set to lose its legislative majority in National Assembly elections and, in turn, relinquish a piece of policymaking power. But the composition of the legislative coalition will determine the direction of policy as well as the direction of local financial markets. Also, May sentiment data in China were underwhelming, suggesting China's economy is still under pressure.

- Next week: Mexico Presidential Election (Sun.), Bank of Canada (Wed.), European Central Bank (Thu.)

Interest Rate Watch: Amid Higher Yields, Market Inflation Expectations Remain Stable

- Since the start of the year, expectations for a later start to Fed easing in the wake of stubbornly-high inflation have pushed up benchmark Treasury yields. Notable in the advance of nominal yields has been relatively stable inflation expectations among market participants. Fairly steady breakeven rates suggest markets still view the Fed's commitment to 2% inflation as credible.

Topic of the Week: “I Am Not Paying $20 for a Hamburger”

- The latest Beige Book unveiled a growing sense of weariness among business owners amid a pullback in discretionary spending. Outlooks grew “somewhat more pessimistic amid reports of rising uncertainty and greater downside risks.”

Summary 6/3 – 6/7

Monday, Jun 3, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q1 | 12.20% | 16.40% |

| 00:30 | JPY | Manufacturing PMI May F | 50.5 | 50.5 |

| 01:45 | CNY | Caixin Manufacturing PMI May | 51.5 | 51.4 |

| 07:30 | CHF | Manufacturing PMI May | 45.4 | 41.4 |

| 07:45 | EUR | Italy Manufacturing PMI May | 48 | 47.3 |

| 07:50 | EUR | France Manufacturing PMI May F | 46.7 | 46.7 |

| 07:55 | EUR | Germany Manufacturing PMI May F | 45.4 | 45.4 |

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 47.4 | 47.4 |

| 08:30 | GBP | Manufacturing PMI May F | 51.3 | 51.3 |

| 13:30 | CAD | Manufacturing PMI May | 49.4 | |

| 13:45 | USD | Manufacturing PMI May F | 50.9 | 50.9 |

| 14:00 | USD | ISM Manufacturing PMI May | 49.8 | 49.2 |

| 14:00 | USD | ISM Manufacturing Prices Paid May | 60 | 60.9 |

| 14:00 | USD | ISM Manufacturing Employment Index May | 48.6 | |

| 14:00 | USD | Construction Spending M/M Apr | 0.20% | -0.20% |

| 23:50 | JPY | Monetary Base Y/Y May | 2.20% | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Capital Spending Q1 | |

| Forecast: 12.20% | Previous: 16.40% | ||

| 00:30 | JPY | Manufacturing PMI May F | |

| Forecast: 50.5 | Previous: 50.5 | ||

| 01:45 | CNY | Caixin Manufacturing PMI May | |

| Forecast: 51.5 | Previous: 51.4 | ||

| 07:30 | CHF | Manufacturing PMI May | |

| Forecast: 45.4 | Previous: 41.4 | ||

| 07:45 | EUR | Italy Manufacturing PMI May | |

| Forecast: 48 | Previous: 47.3 | ||

| 07:50 | EUR | France Manufacturing PMI May F | |

| Forecast: 46.7 | Previous: 46.7 | ||

| 07:55 | EUR | Germany Manufacturing PMI May F | |

| Forecast: 45.4 | Previous: 45.4 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI May F | |

| Forecast: 47.4 | Previous: 47.4 | ||

| 08:30 | GBP | Manufacturing PMI May F | |

| Forecast: 51.3 | Previous: 51.3 | ||

| 13:30 | CAD | Manufacturing PMI May | |

| Forecast: | Previous: 49.4 | ||

| 13:45 | USD | Manufacturing PMI May F | |

| Forecast: 50.9 | Previous: 50.9 | ||

| 14:00 | USD | ISM Manufacturing PMI May | |

| Forecast: 49.8 | Previous: 49.2 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid May | |

| Forecast: 60 | Previous: 60.9 | ||

| 14:00 | USD | ISM Manufacturing Employment Index May | |

| Forecast: | Previous: 48.6 | ||

| 14:00 | USD | Construction Spending M/M Apr | |

| Forecast: 0.20% | Previous: -0.20% | ||

| 23:50 | JPY | Monetary Base Y/Y May | |

| Forecast: 2.20% | Previous: 2.10% | ||

Tuesday, Jun 4, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Current Account Balance (AUD) Q1 | 5.9B | 11.8B |

| 06:30 | CHF | CPI M/M May | 0.40% | 0.30% |

| 06:30 | CHF | CPI Y/Y May | 1.40% | |

| 07:55 | EUR | Germany Unemployment Change May | 7K | 10K |

| 07:55 | EUR | Germany Unemployment Rate May | 5.90% | 5.90% |

| 14:00 | USD | Factory Orders M/M Apr | 0.70% | 1.60% |

| 22:45 | NZD | Terms of Trade Index Q1 | 2.80% | -7.80% |

| 23:30 | JPY | Labor Cash Earnings Y/Y Apr | 1.70% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Current Account Balance (AUD) Q1 | |

| Forecast: 5.9B | Previous: 11.8B | ||

| 06:30 | CHF | CPI M/M May | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 06:30 | CHF | CPI Y/Y May | |

| Forecast: | Previous: 1.40% | ||

| 07:55 | EUR | Germany Unemployment Change May | |

| Forecast: 7K | Previous: 10K | ||

| 07:55 | EUR | Germany Unemployment Rate May | |

| Forecast: 5.90% | Previous: 5.90% | ||

| 14:00 | USD | Factory Orders M/M Apr | |

| Forecast: 0.70% | Previous: 1.60% | ||

| 22:45 | NZD | Terms of Trade Index Q1 | |

| Forecast: 2.80% | Previous: -7.80% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Apr | |

| Forecast: 1.70% | Previous: 0.60% | ||

Wednesday, Jun 5, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Services PMI May F | 53.6 | 53.6 |

| 01:30 | AUD | GDP Q/Q Q1 | 0.20% | 0.20% |

| 01:45 | CNY | Caixin Services PMI May | 52.6 | 52.5 |

| 06:45 | EUR | France Industrial Output M/M Apr | 0.50% | -0.30% |

| 07:45 | EUR | Italy Services PMI May | 54.5 | 54.3 |

| 07:50 | EUR | France Services PMI May F | 49.4 | 49.4 |

| 07:55 | EUR | Germany Services PMI May F | 53.9 | 53.9 |

| 08:00 | EUR | Eurozone Services PMI May F | 53.3 | 53.3 |

| 08:30 | GBP | Services PMI May F | 52.9 | 52.9 |

| 09:00 | EUR | Eurozone PPI M/M Apr | -0.50% | -0.40% |

| 09:00 | EUR | Eurozone PPI Y/Y Apr | -7.80% | |

| 12:15 | USD | ADP Employment Change May | 175K | 192K |

| 12:30 | CAD | Labor Productivity Q/Q Q1 | 0.40% | 0.40% |

| 13:45 | CAD | BoC Interest Rate Decision | 4.75% | 5.00% |

| 13:45 | USD | Services PMI May F | 54.8 | 54.8 |

| 14:00 | USD | ISM Services PMI May | 51 | 49.4 |

| 14:30 | USD | Crude Oil Inventories | -4.2M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Services PMI May F | |

| Forecast: 53.6 | Previous: 53.6 | ||

| 01:30 | AUD | GDP Q/Q Q1 | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 01:45 | CNY | Caixin Services PMI May | |

| Forecast: 52.6 | Previous: 52.5 | ||

| 06:45 | EUR | France Industrial Output M/M Apr | |

| Forecast: 0.50% | Previous: -0.30% | ||

| 07:45 | EUR | Italy Services PMI May | |

| Forecast: 54.5 | Previous: 54.3 | ||

| 07:50 | EUR | France Services PMI May F | |

| Forecast: 49.4 | Previous: 49.4 | ||

| 07:55 | EUR | Germany Services PMI May F | |

| Forecast: 53.9 | Previous: 53.9 | ||

| 08:00 | EUR | Eurozone Services PMI May F | |

| Forecast: 53.3 | Previous: 53.3 | ||

| 08:30 | GBP | Services PMI May F | |

| Forecast: 52.9 | Previous: 52.9 | ||

| 09:00 | EUR | Eurozone PPI M/M Apr | |

| Forecast: -0.50% | Previous: -0.40% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Apr | |

| Forecast: | Previous: -7.80% | ||

| 12:15 | USD | ADP Employment Change May | |

| Forecast: 175K | Previous: 192K | ||

| 12:30 | CAD | Labor Productivity Q/Q Q1 | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 13:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 4.75% | Previous: 5.00% | ||

| 13:45 | USD | Services PMI May F | |

| Forecast: 54.8 | Previous: 54.8 | ||

| 14:00 | USD | ISM Services PMI May | |

| Forecast: 51 | Previous: 49.4 | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -4.2M | ||

Thursday, Jun 6, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | 5.50B | 5.02B |

| 05:45 | CHF | Unemployment Rate May | 2.30% | 2.30% |

| 06:00 | EUR | Germany Factory Orders M/M Apr | 0.50% | -0.40% |

| 08:00 | EUR | Italy Retail Sales M/M Apr | 0.30% | 0.00% |

| 08:30 | GBP | Construction PMI May | 52.5 | 53.0 |

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | 0.20% | 0.80% |

| 12:15 | EUR | ECB Rate On Deposit Facility | 3.75% | 4.00% |

| 12:15 | EUR | ECB Main Refinancing Operations Rate | 4.25% | 4.50% |

| 12:30 | USD | Trade Balance (USD) Apr | -69.8B | -69.4B |

| 12:30 | USD | Initial Jobless Claims (May 31) | 215K | 219K |

| 12:30 | USD | Nonfarm Productivity Q1 | 0.30% | 0.30% |

| 12:30 | USD | Unit Labor Costs Q1 | 4.70% | 4.70% |

| 12:30 | CAD | Trade Balance (CAD) Apr | -2.2B | -2.3B |

| 12:45 | EUR | ECB Press Conference | ||

| 14:00 | CAD | Ivey PMI May | 65.2 | 63.0 |

| 14:30 | USD | Natural Gas Storage | 84B | |

| 22:45 | NZD | Manufacturing Sales Q1 | -0.60% | |

| 23:30 | JPY | Household Spending Y/Y Apr | 0.60% | -1.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | |

| Forecast: 5.50B | Previous: 5.02B | ||

| 05:45 | CHF | Unemployment Rate May | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 06:00 | EUR | Germany Factory Orders M/M Apr | |

| Forecast: 0.50% | Previous: -0.40% | ||

| 08:00 | EUR | Italy Retail Sales M/M Apr | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 08:30 | GBP | Construction PMI May | |

| Forecast: 52.5 | Previous: 53.0 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | |

| Forecast: 0.20% | Previous: 0.80% | ||

| 12:15 | EUR | ECB Rate On Deposit Facility | |

| Forecast: 3.75% | Previous: 4.00% | ||

| 12:15 | EUR | ECB Main Refinancing Operations Rate | |

| Forecast: 4.25% | Previous: 4.50% | ||

| 12:30 | USD | Trade Balance (USD) Apr | |

| Forecast: -69.8B | Previous: -69.4B | ||

| 12:30 | USD | Initial Jobless Claims (May 31) | |

| Forecast: 215K | Previous: 219K | ||

| 12:30 | USD | Nonfarm Productivity Q1 | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | Unit Labor Costs Q1 | |

| Forecast: 4.70% | Previous: 4.70% | ||

| 12:30 | CAD | Trade Balance (CAD) Apr | |

| Forecast: -2.2B | Previous: -2.3B | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:00 | CAD | Ivey PMI May | |

| Forecast: 65.2 | Previous: 63.0 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 84B | ||

| 22:45 | NZD | Manufacturing Sales Q1 | |

| Forecast: | Previous: -0.60% | ||

| 23:30 | JPY | Household Spending Y/Y Apr | |

| Forecast: 0.60% | Previous: -1.20% | ||

Friday, Jun 7, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 03:00 | CNY | Trade Balance (USD) May | 71.5B | 72.4B |

| 06:00 | EUR | Germany Industrial Production M/M Apr | 0.20% | -0.40% |

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | 25.5B | 22.3B |

| 06:45 | EUR | France Trade Balance (EUR) Apr | -5.4B | -5.5B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | 720B | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 | 0.30% | 0.30% |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 F | 0.30% | 0.30% |

| 12:30 | USD | Nonfarm Payrolls May | 180K | 175K |

| 12:30 | USD | Unemployment Rate May | 3.90% | 3.90% |

| 12:30 | USD | Average Hourly Earnings M/M May | 0.30% | 0.20% |

| 12:30 | CAD | Net Change in Employment May | 90.4K | |

| 12:30 | CAD | Unemployment Rate May | 6.10% | |

| 14:00 | USD | Wholesale Inventories Apr F | 0.20% | 0.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 03:00 | CNY | Trade Balance (USD) May | |

| Forecast: 71.5B | Previous: 72.4B | ||

| 06:00 | EUR | Germany Industrial Production M/M Apr | |

| Forecast: 0.20% | Previous: -0.40% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | |

| Forecast: 25.5B | Previous: 22.3B | ||

| 06:45 | EUR | France Trade Balance (EUR) Apr | |

| Forecast: -5.4B | Previous: -5.5B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | |

| Forecast: | Previous: 720B | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q1 | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | Nonfarm Payrolls May | |

| Forecast: 180K | Previous: 175K | ||

| 12:30 | USD | Unemployment Rate May | |

| Forecast: 3.90% | Previous: 3.90% | ||

| 12:30 | USD | Average Hourly Earnings M/M May | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 12:30 | CAD | Net Change in Employment May | |

| Forecast: | Previous: 90.4K | ||

| 12:30 | CAD | Unemployment Rate May | |

| Forecast: | Previous: 6.10% | ||

| 14:00 | USD | Wholesale Inventories Apr F | |

| Forecast: 0.20% | Previous: 0.20% | ||

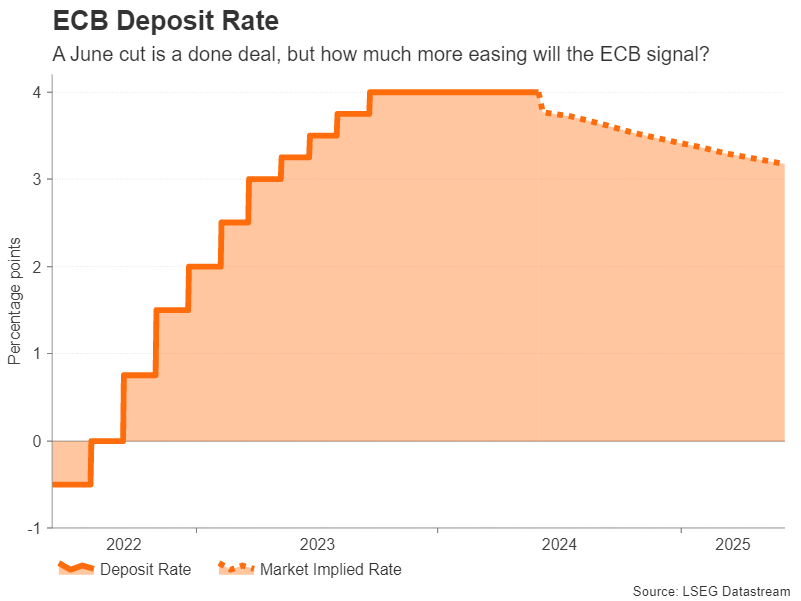

Week Ahead – ECB Rate Cut Might Get Eclipsed by BoC Surprise and NFP Report

- ECB set to slash rates on Thursday, focus on forward guidance

- But will the BoC take the lead when it meets on Wednesday?

- US jobs report eyed on Friday as Fed unyielding on cuts

- OPEC+ might extend some output reductions into 2025

ECB poised to cut rates, but what’s next?

The path by central banks to lower borrowing costs has been far from smooth, but it seems that the European Central Bank will be among the first to reach its desired destination. The ECB meets on Thursday for its June policy decision and is widely expected to cut its three main lending rates by 25 basis points. This would take the deposit rate down to 3.75%, widening the differential with the Fed funds rate, which currently stands at a range of 5.25%-5.50%.

The euro has been surprisingly resilient against all the rate cut speculation, staging a rebound even as a June move became increasingly baked in by the markets. The improving economic picture across the euro area is likely behind the recent bounce. However, stronger growth might make it more difficult for the ECB to cut rates too quickly, especially as inflationary pressures have yet to subside completely.

Hence, the main debate for ECB policymakers at the June meeting will be not so much whether or not to go ahead with the much publicised cut, but by how much and how quickly to ease policy thereafter. Investors think there will be at least one more 25-bps cut after June, but dovish Governing Council members are likely leaning closer to three and maybe even four cuts.

President Lagarde will have a tough balancing act to perform and ultimately, it is the tone of the press conference that markets will react to the most. If Lagarde plays down the prospect of rapid rate reductions, the euro could leap above the $1.09 level.

In other data out of the Eurozone, the final PMI estimates for May will be watched on Wednesday, and German industrial output and trade figures might attract some attention on Friday too.

Will the BoC take the plunge and cut rates?

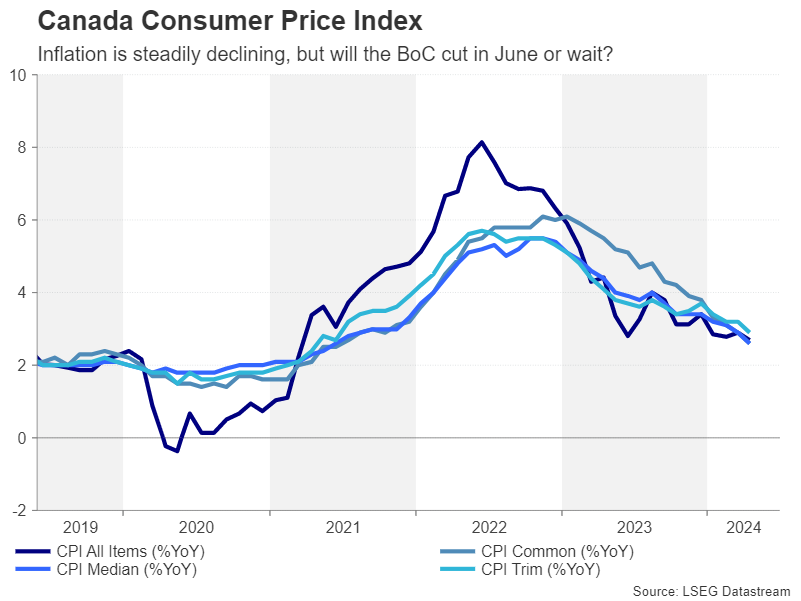

Amid the sticky inflation picture in the US, the ECB is not the only central bank in a much more advantageous position than the Fed. The Bank of Canada has also seen good progress in getting inflation much closer to its target midpoint of 2%. Headline inflation fell to a three-year low of 2.7% in April and all three underlying measures of CPI have been on the decline so far this year, slipping below 3.0%.

With Canada’s labour market cooling slightly over the past year and economic growth being somewhat sluggish, there is a strong case for lowering rates on Wednesday when the Bank meets. However, a 25-bps cut is only 60% priced in by the markets, with a July move seen as much more of a done deal.

The delay to the Fed’s own rate-cutting plans is likely a factor in this as the Bank of Canada will not want to diverge significantly from the Fed out of fear of sparking a sharp slide in the loonie. Nevertheless, the option to cut in June remains firmly on the table and should the BoC deliver such a surprise, policymakers will probably try to signal that this is not the start of an aggressive rate-cutting cycle.

The Canadian dollar is in danger of breaking out of its bullish channel versus the greenback if the BoC cuts rates, while traders will also be keeping an eye on employment numbers for May due on Friday.

NFP and ISM PMIs to shed valuable light

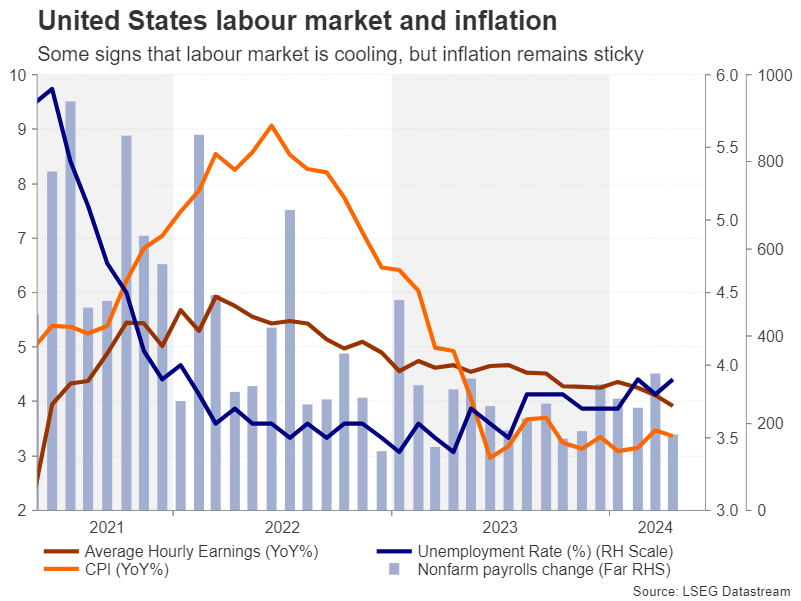

It’s been one setback after another for the Fed this year as inflation has been hovering nearer 3.0% rather than the 2% target, which is looking increasingly elusive. Fed officials remain confident that inflation will eventually resume its downward trajectory, but the tight labour market and robust consumer spending have made the task challenging.

More recently, though, there have been some signs that the jobs market is cooling off and consumers are turning more cautious. Friday’s nonfarm payrolls report will be crucial in setting expectations ahead of the June 12 FOMC meeting.

In April, the US economy added 175k jobs, which was a marked slowdown from the prior month. But what is perhaps a more significant indication that the hiring spree is coming to an end is the fact that the unemployment rate has been slowly inching higher over the past year, reaching 3.9% in April, while wage growth has been moderating too.

If this trend is maintained in the May report, investors are likely to feel more hopeful that the Fed will be able to cut rates by at least once in 2024. One of the headaches for policymakers during this ‘patience’ phase of the policy cycle is that the data has been very mixed and even contradictory.

There’s a risk that the economic releases ahead of the NFP numbers will further confuse markets. They include the ISM manufacturing and services PMIs, due Monday and Wednesday respectively, factory orders and the JOLTS job openings on Tuesday, and the ADP employment report on Wednesday. The ISM PMIs in particular will provide vital updates on business momentum as well as gauging price pressures.

Unless the data clear some of the fog over the Fed policy path, the US dollar will likely continue to trade sideways against a basket of currencies.

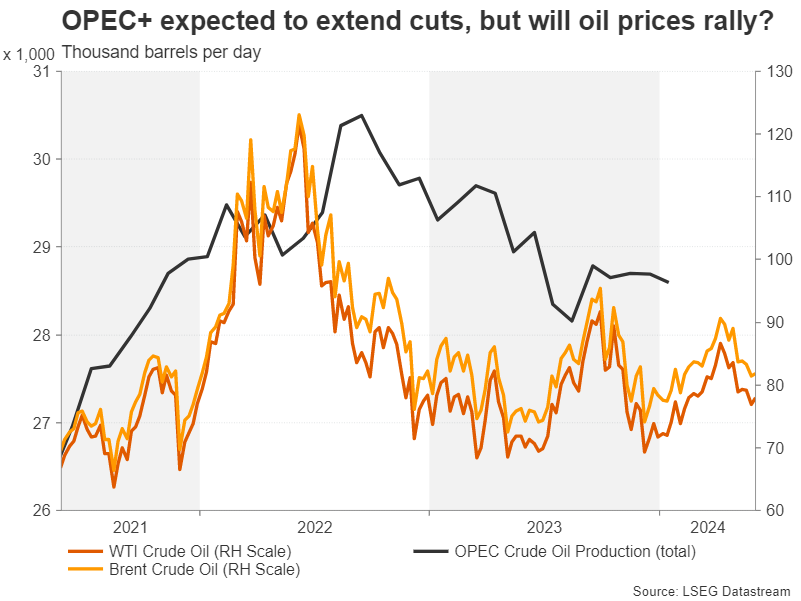

OPEC+ meets, busy week for the aussie

The decision by OPEC and non-OPEC countries on output levels will greet markets on Monday as the cartel is scheduled to hold online meetings on Sunday. Reports suggest that the oil alliance will extend the voluntary cuts of 2.2 million barrels per day into the second half of 2024 while the pledges by all OPEC+ members to restrict output by 3.66 million bpd could be stretched into 2025.

Oil prices haven’t been impressed by the rumours but an agreement that takes the cuts into next year would be positive for the outlook.

Elsewhere, the Australian dollar will be on standby for the latest domestic GDP readings on Wednesday. Australia’s economy has been steadily losing steam over the past few quarters and it’s expected that GDP growth held at a meagre 0.2% q/q in Q1.

If growth is faster than forecast, this would add to bets that the Reserve Bank of Australia is more likely to hike rates than to cut them in the upcoming months, lifting the aussie.

Chinese data will also be important for the aussie next week. The Caixin manufacturing and services PMIs will be watched on Monday and Wednesday, respectively, while on Friday, investors will be hoping to see stronger exports growth when May trade stats are released.

Finally, Japanese wage figures out on Wednesday might offer the beleaguered yen some support should they show an acceleration in pay growth in April.

Bank of Canada Set to Make the First Interest Rate Cut Next Week

All ducks appear to be in a row for the Bank of Canada to kick-start the policy easing cycle and lower the overnight rate by 25 basis points to 4.75% on Wednesday. The move follows cuts from the Swiss National Bank and the Riksbank (central bank of Sweden) in recent weeks and comes after the overnight rate was held at a restrictive 5% for about a year (the last rate hike was July 2023).

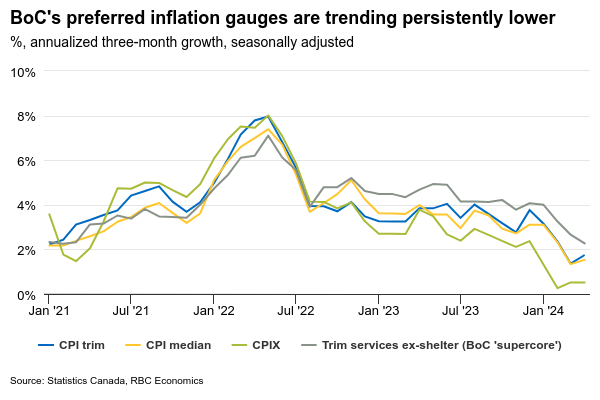

Evidence has continued to build that the current high level of interest rates is no longer needed. The Canadian economy has softened significantly. Gross domestic product per capita posted another decline in Q1 this year. Inflation pressures have also slowed with the closely watched three-month growth rate (annualized) in the BoC’s preferred median and trim core consumer price index measures both running below the 2% inflation target in April. The slowing economic backdrop is raising confidence that lower inflation readings will continue despite signs of a reacceleration in the stronger U.S. economy. At the last interest rate decision, Governor Tiff Macklem said the conditions for lower interest rates appeared to be in place but that the central bank wanted to see more evidence that inflation pressures are trending lower. The two CPI reports since then have both surprised on the downside and should provide the BoC with enough evidence.

Still, while the case for interest rate cuts in Canada is relatively clear—the BoC will likely maintain a cautious tone about the pace of additional cuts after next week. Governor Macklem has mentioned a few areas where price pressures could still resurface. That includes higher energy prices driven by global geopolitical conflicts, and faster increases in wages and/or home prices domestically.

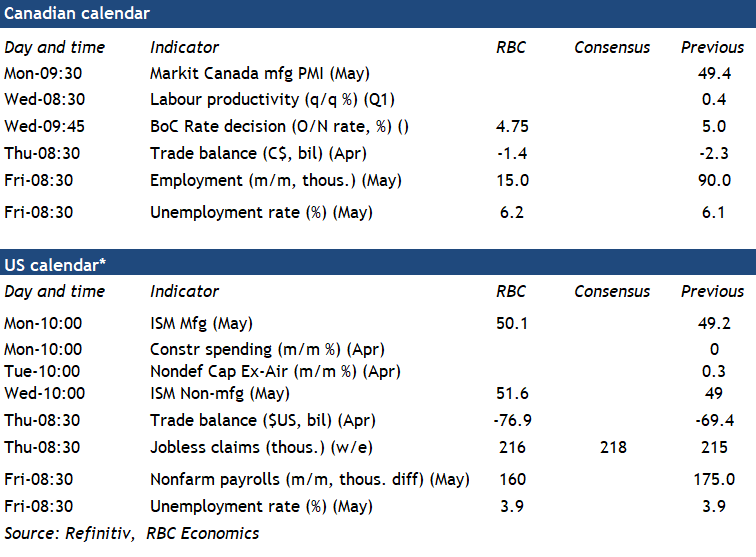

So far, there’s little sign of domestic price pressures reaccelerating. Labour market conditions have continued to cool over the spring as hiring demand slows. We expect next week’s labour market data will show more softening in May with a small 15,000 gain in employment and another tick higher in the unemployment rate to 6.2%. Housing market conditions, in the meantime, have remained weak as buyers continue to be challenged by higher borrowing costs and a lack of affordability. Wary of those risks, the BoC will likely continue to suggest that the pace of additional easing will be slow and gradual. Still, we expect that, ultimately, a softer economy will keep inflation pressures moving lower in Canada. Contingent on that outlook, we look for 100 basis points of interest rate cuts this year that will leave the overnight rate at a still restrictive 4% by the end of 2024.

Week ahead data watch

U.S. employment likely went up by 160,000 in May, slowing from the 175,000 in the prior month. Much of that growth came from health care and social assistance sector, offsetting the weaknesses from manufacturing and information sectors. We expect the unemployment rate to be unchanged from April, at 3.9%.

We look for the April Canadian trade balance to have narrowed to $-1.4B, from the $-2.3B in March. Exports likely increased by 1.4%, with higher oil prices pushed energy trade balance higher. Imports should look little changed from March.

April advance trade report showed goods trade deficits widened by $7.1B in the U.S., with imports (+3.1%) growing at a faster pace than exports (+0.5%) from March. We expect the overall trade deficit to widen as well, from $-69.4B to $-76.9B in April.

Weekly Focus – Strong Euro Area Inflation in May

The main release this week was euro area inflation from May. Inflation rose to 2.6% y/y from 2.4% in April, which was above expectations of 2.5%. The increase in inflation was due to core inflation rising to 2.9% y/y from 2.7% on the back of very strong services inflation. Overall, the inflation in May confirmed the picture we have seen in the past months of a strong underlying pressure on inflation from service prices. This sticky services inflation is a key reason for the ECB to wait for more data before embarking on a series of rate cuts after June as growth has also returned, and the labour market is historically strong.

The historically strong labour market was visible in the euro area unemployment rate, which declined to an all-time low of 6.4% in April. The strong labour market bodes well for an uptick in private consumption this year in combination with rising incomes and decent savings, but it also puts upward pressure on domestic inflation. A recovery may also be in the horizon in Germany where the Ifo index for May showed expectations rising to the highest level since mid-2023. Yet, the assessment of the current business situation declined, so while European growth is undeniably picking up pace, Germany's recovery continues to trail behind.

In the US, consumer confidence for May came in stronger than expected and marked the first time in three months where the confidence indicator rose. Also in the US, Fed's Kashkari said that he did not believe that any FOMC member had ruled out a rate hike.

Out of Asia, we got Chinese PMIs for May from NBS that disappointed to the low side, as the official PMI for the manufacturing sector dropped into retracting territory (below the 50 mark), standing at 49.5. The data highlights the fragility of Chinese growth and the continued need for stimulus, which is also recognized by the government. In Japan, Tokyo inflation (excl. fresh food) increased to 1.9% in May from 1.6%. Core price pressures remain modest though.

Next week focus turns to the ECB and the US jobs market report. The ECB is widely expected to deliver a 25bp rate cut, largely because the governing council members have stated as much. The updated June staff projections are expected to suggest that the prevailing economic and monetary policy narrative stays broadly unchanged, and we expect the rate cut to be formulated as a rollback of the 'insurance hike' from September last year. In the euro area, we also will closely follow the compensation per employee wage data for Q1 that is released with the final national accounts data on Friday.

In the US, the main event next week is the May job market report. We expect nonfarm payrolls to have grown by 190k, a modest uptick from April when weak public sector jobs growth weighed on the headline figure. Average hourly earnings growth likely remained steady at +0.2% m/m. Also in the US, we look out for the ISM data on Monday and Wednesday.

In Asia, we receive wage growth data from Japan and Chinese PMIs. It will be interesting to see if the Caixin PMI can hold up despite the decline in the NBS this week as it has generally been stronger than the NBS PMI. During the week we may get the results of the EU Commission's investigation into Chinese EVs. Finally, we also look out for May inflation in Switzerland which is very important before the June monetary policy meeting.